Download - GAIL India, 1Q FY 2014

7/27/2019 GAIL India, 1Q FY 2014

http://slidepdf.com/reader/full/gail-india-1q-fy-2014 1/12

Please refer to important disclosures at the end of this report 1

Quarterly highlights (Standalone)Y/E March (` cr) 1QFY2014 1QFY2013 % chg (yoy) 4QFY2013 % chg (qoq)

Net sales 12,856 11,089 15.9 12,409 3.6

EBITDA 1,464 1,899 (22.9) 1,137 28.8

EBITDA margin (%) 11.4 17.1 (574)bp 9.2 223bp

Adj. PAT 808 1,134 (28.7) 618 30.7

Source: Company, Angel Research

For 1QFY2014, GAIL India (GAIL) reported a lower-than-expected profit due to a

higher-than-expected subsidy burden. We maintain our Neutral rating on the

stock.

Top-line grew by 15.9% yoy: The company’s top-line grew by 15.9% yoy to

` 12,856cr (above our estimate of ` 12,296cr), mainly due to increase in net sales

in the Petrochemicals (+92.2% yoy) and Natural Gas trading (+19.7% yoy)

segments. The company’s fuel subsidy burden stood at ` 700cr in 1QFY2014.

EBITDA declined by 22.9% yoy: The Petrochemicals segment’s EBIT grew by

123.8% yoy to ` 438cr. However, Natural Gas trading segment’s EBIT decreased

39.0% to ` 303cr and the LPG segment reported a loss of ` 11cr in 1QFY2014

compared to a profit of ` 437cr in 1QFY2013. GAIL’s EBITDA therefore declined

by 22.9% yoy to ` 1,464cr in 1QFY2014; the EBITDA margin contracted by

574bp yoy to 11.4%.

Higher depreciation and taxes drags PAT: The depreciation expense increased by

29.4% yoy to ` 281cr, whereas the tax rate stood at 34.0% in 1QFY2014

compared to 32.7% in 1QFY2013. Consequently, the net profit declined by

28.7% yoy to ` 808cr, which is below our estimate of ` 918cr.

Outlook and valuation: Over the past one year, gas production from the

KG basin has declined significantly. Further, we do not expect any meaningful

increase in the production at KG D6 over the coming two years. Hence, we expect

utilization levels for GAIL’s pipelines to remain low during FY2014. Moreover, a

cap on the gas marketing margin (which is currently under review by the PNGRB)

would remain an overhang on the stock. Hence, we maintain our Neutral ratingon the stock.

Key financials - Standalone

Y/E March (` cr) FY2012 FY2013E FY2014E FY2015E

Net sales 40,441 47,522 49,700 48,822

% chg 24.6 17.5 4.6 (1.8)

Net profit 3,654 4,021 4,171 4,238

% chg 2.6 10.1 3.7 1.6

OPM (%) 13.8 13.6 16.0 16.6

EPS (`) 28.8 31.7 32.9 33.4

P/E (x) 11.4 10.4 10.0 9.8

P/BV (x) 1.9 1.7 1.5 1.3

RoE (%) 17.9 17.4 15.9 14.4

RoCE (%) 18.5 17.3 16.8 15.3

EV/Sales (x) 1.0 0.8 0.7 0.7

EV/EBITDA (x) 7.5 5.9 4.6 4.2

Source: Company, Angel Research: Note: CMP as of July 25, 2013

NEUTRALCMP ` 329

Target Price -

Investment Period -

Stock Info

Sector

409

Bloomberg Code

Shareholding Pattern (%)

Promoters 57.3

MF / Banks / Indian Fls 15.0

FII / NRIs / OCBs 17.6 Indian Public / Others 10.0

Abs. (%) 3m 1yr 3yr

Sensex 2.1 17.6 9.2

GAIL (4.7) (4.5) (29.2)

10

19,805

5,908

GAIL.BO

GAIL@IN

Beta

Face Value ( ` )

BSE Sensex

Nifty

Reuters Code

41,682

396/276

65,652

0.8

Oil & Gas

Avg. Daily Volume

Market Cap ( ` cr)

52 Week High / Low

Net debt ( ` cr)

Bhavesh Chauhan

Tel: 022 - 3935 7800 Ext: 6821

Vinay Rachh

Tel: 022- 39357600 Ext: 6841

GAIL India

Performance Highlights

1QFY2014 Result Update | Oil & Gas

July 26, 2013

7/27/2019 GAIL India, 1Q FY 2014

http://slidepdf.com/reader/full/gail-india-1q-fy-2014 2/12

GAIL | 1QFY2014 Result Update

July 26, 2013 2

Exhibit 1: 1QFY2014 performance (Standalone)

Y/E March (` cr) 1QFY2014 1QFY2013 % chg (yoy) 4QFY2013 % chg (qoq) FY2013 FY2012 % chg (yoy)

Net sales 12,856 11,089 15.9 12,409 3.6 47,332 40,281 17.5

COGS 10,697 8,085 32.3 9,677 10.5 36,309 30,437 19.3Total operating expenditure 11,391 9,190 24.0 11,272 1.1 41,053 34,842 17.8

EBITDA 1,464 1,899 (22.9) 1,137 28.8 6,469 5,599 15.5

EBITDA margin (%) 11.4 17.1 9.2 13.7 13.9

Other income 58 38 52.6 270 (78.6) 765 648 17.9

Depreciation 281 217 29.4 273 3.0 981 791 24.1

Interest 61 59 4.1 55 11.3 195 116 67.4

PBT 1,224 1,685 (27.3) 1,141 7.3 6,057 5,340 13.4

PBT margin (%) 9.5 15.2 9.2 12.8 13.3

Total tax 416 551 (24.5) 523 (20.4) 2,036 1,686 20.7

% of PBT 34.0 32.7 45.8 33.6 31.6

PAT 808 1,134 (28.7) 618 30.7 4,021 3,654 10.1

Source: Company, Angel Research

7/27/2019 GAIL India, 1Q FY 2014

http://slidepdf.com/reader/full/gail-india-1q-fy-2014 3/12

GAIL | 1QFY2014 Result Update

July 26, 2013 3

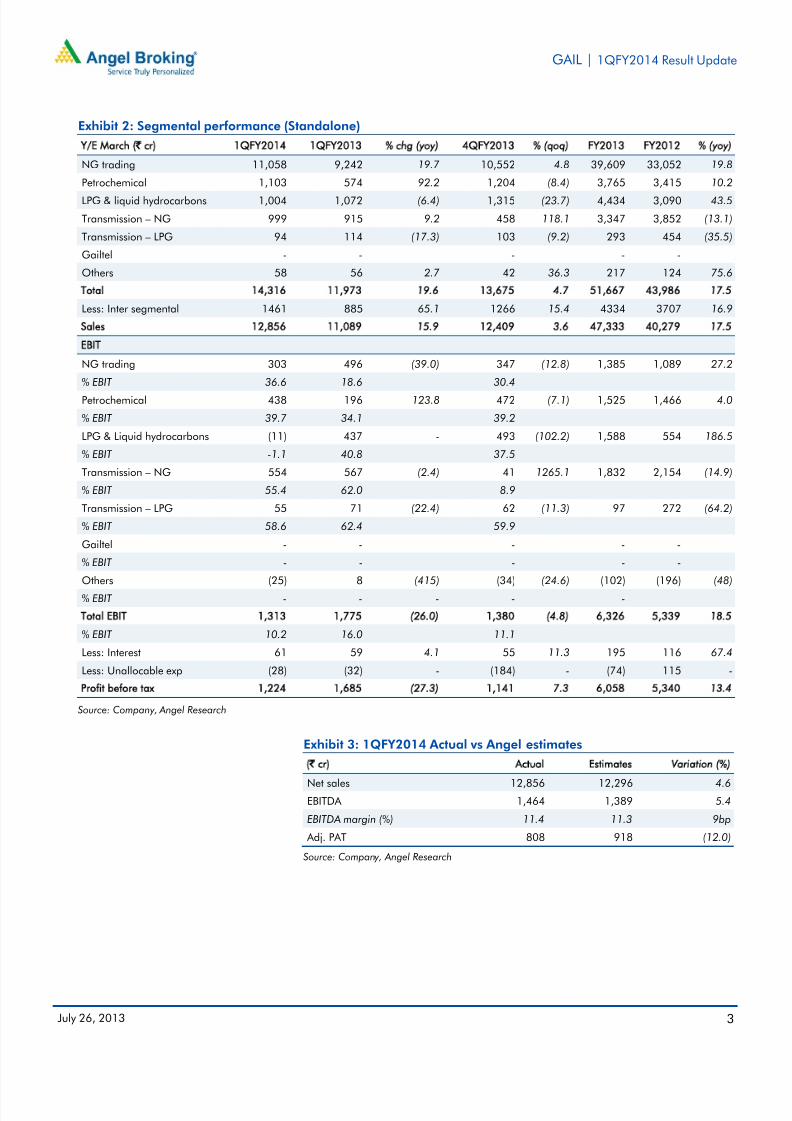

Exhibit 2: Segmental performance (Standalone)

Y/E March (` cr) 1QFY2014 1QFY2013 % chg (yoy) 4QFY2013 % (qoq) FY2013 FY2012 % (yoy)

NG trading 11,058 9,242 19.7 10,552 4.8 39,609 33,052 19.8

Petrochemical 1,103 574 92.2 1,204 (8.4) 3,765 3,415 10.2LPG & liquid hydrocarbons 1,004 1,072 (6.4) 1,315 (23.7) 4,434 3,090 43.5

Transmission – NG 999 915 9.2 458 118.1 3,347 3,852 (13.1)

Transmission – LPG 94 114 (17.3) 103 (9.2) 293 454 (35.5)

Gailtel - - - - -

Others 58 56 2.7 42 36.3 217 124 75.6

Total 14,316 11,973 19.6 13,675 4.7 51,667 43,986 17.5

Less: Inter segmental 1461 885 65.1 1266 15.4 4334 3707 16.9

Sales 12,856 11,089 15.9 12,409 3.6 47,333 40,279 17.5

EBIT

NG trading 303 496 (39.0) 347 (12.8) 1,385 1,089 27.2

% EBIT 36.6 18.6 30.4

Petrochemical 438 196 123.8 472 (7.1) 1,525 1,466 4.0

% EBIT 39.7 34.1 39.2

LPG & Liquid hydrocarbons (11) 437 - 493 (102.2) 1,588 554 186.5

% EBIT -1.1 40.8 37.5

Transmission – NG 554 567 (2.4) 41 1265.1 1,832 2,154 (14.9)

% EBIT 55.4 62.0 8.9

Transmission – LPG 55 71 (22.4) 62 (11.3) 97 272 (64.2)

% EBIT 58.6 62.4 59.9

Gailtel - - - - -

% EBIT - - - - -

Others (25) 8 (415) (34) (24.6) (102) (196) (48)

% EBIT - - - - -

Total EBIT 1,313 1,775 (26.0) 1,380 (4.8) 6,326 5,339 18.5

% EBIT 10.2 16.0 11.1

Less: Interest 61 59 4.1 55 11.3 195 116 67.4

Less: Unallocable exp (28) (32) - (184) - (74) 115 -

Profit before tax 1,224 1,685 (27.3) 1,141 7.3 6,058 5,340 13.4

Source: Company, Angel Research

Exhibit 3: 1QFY2014 Actual vs Angel estimates(` cr) Actual Estimates Variation (%)

Net sales 12,856 12,296 4.6

EBITDA 1,464 1,389 5.4

EBITDA margin (%) 11.4 11.3 9bp

Adj. PAT 808 918 (12.0)

Source: Company, Angel Research

7/27/2019 GAIL India, 1Q FY 2014

http://slidepdf.com/reader/full/gail-india-1q-fy-2014 4/12

GAIL | 1QFY2014 Result Update

July 26, 2013 4

Top-line grew by 15.9% yoy: The company’s top-line grew by 15.9% yoy to

` 12,856cr (above our estimate of ` 12,296cr) due to increase in revenues from the

Petrochemicals and Natural Gas trading segments which grew by 92.2% and

19.7% yoy to `

1,103cr and `

11,058cr, respectively. The company’s fuel subsidy burden stood at ` 700cr in 1QFY2014 ( ` 700cr in 1QFY2013 and ` 587cr in

4QFY2013).

Exhibit 4: Net sales grew by 15.9% yoy

11,260 10,45511,089

11,361

12,474 12,40912,856

3 4

. 6

1 7 . 6

2 5 .

0

1 7 . 1

1 0 . 8

1 8 . 7

1 5 . 9

-

5.0

10.015.0

20.0

25.0

30.0

35.0

40.0

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

3QFY12 4QFY12 1QFY13 2QFY13 3QFY13 4QFY13 1QFY14

( % )

( `

c r )

Net Sales Net Sales growth (RHS)

Source: Company, Angel Research

Exhibit 5: GAIL’s subsidy share stood at `700cr

536

1,397

700786

700587

700

0

200

400

600

800

1,000

1,200

1,400

1,600

3QFY12 4QFY12 1QFY13 2QFY13 3QFY13 4QFY13 1QFY14

( `

c r )

Source: Company, Angel Research

Exhibit 6: Transmission volumes remained flat qoq

119 116110 106 105

99 99

-

20

40

60

80

100

120

140

3QF Y12 4QFY12 1QFY13 2QFY13 3QFY13 4QF Y13 1QFY14

( m m s c m d )

Source: Company, Angel Research

EBITDA declines by 22.9% yoy: The Petrochemicals segment’s EBIT grew by

123.8% yoy to ` 438cr. However, Natural Gas trading segment’s EBIT decreased

39.0% to ` 303cr and the LPG segment reported a loss of ` 11cr in 1QFY2014

compared to a profit of ` 437cr in 1QFY2013. The loss in LPG segment was due to

lower LPG prices in the quarter coupled with lack of supply of cheaper gas from

KG-D6. GAIL’s EBITDA therefore declined by 22.9% yoy to ` 1,464cr in

1QFY2014; the EBITDA margin contracted by 574bp yoy to 11.4%.

7/27/2019 GAIL India, 1Q FY 2014

http://slidepdf.com/reader/full/gail-india-1q-fy-2014 5/12

GAIL | 1QFY2014 Result Update

July 26, 2013 5

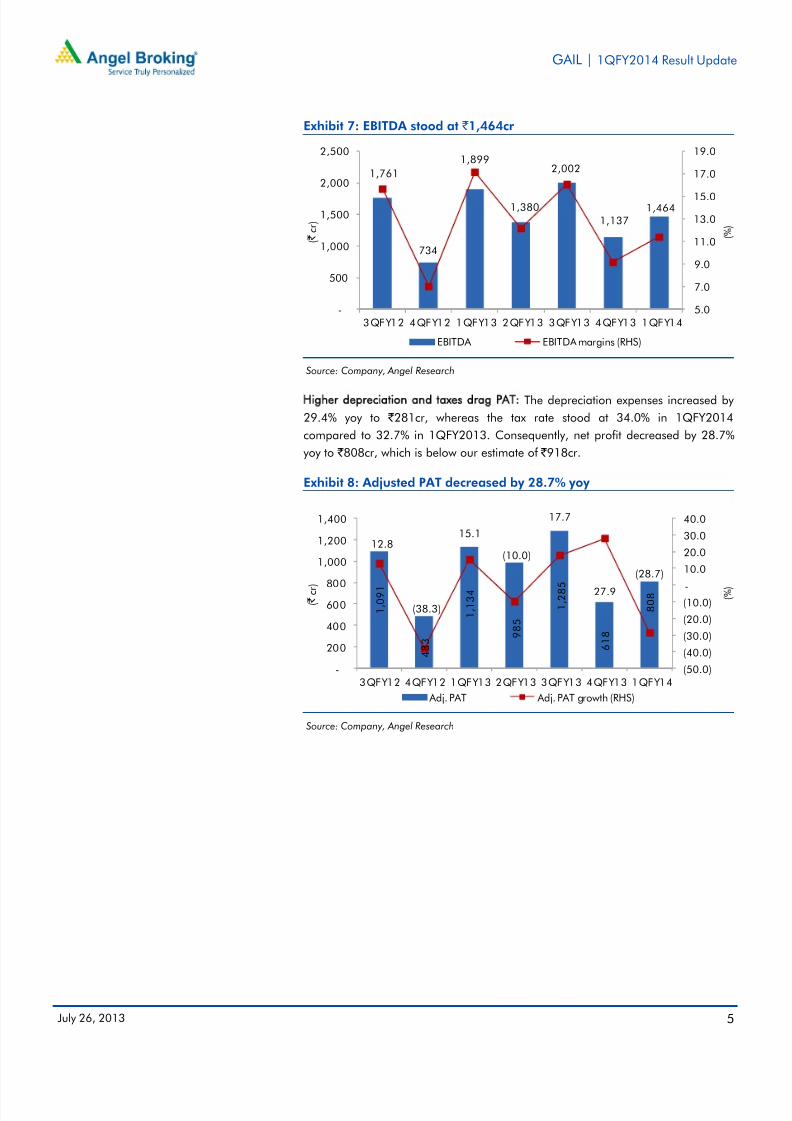

Exhibit 7: EBITDA stood at ` 1,464cr

1,761

734

1,899

1,380

2,002

1,1371,464

5.0

7.0

9.0

11.0

13.0

15.0

17.0

19.0

-

500

1,000

1,500

2,000

2,500

3QFY12 4QFY12 1QFY13 2QFY13 3QFY13 4QFY13 1QFY14

( % )

( `

c r )

EBITDA EBITDA margins (RHS)

Source: Company, Angel Research

Higher depreciation and taxes drag PAT: The depreciation expenses increased by

29.4% yoy to ` 281cr, whereas the tax rate stood at 34.0% in 1QFY2014

compared to 32.7% in 1QFY2013. Consequently, net profit decreased by 28.7%

yoy to ` 808cr, which is below our estimate of ` 918cr.

Exhibit 8: Adjusted PAT decreased by 28.7% yoy

1 , 0

9 1

4 8 3

1 , 1

3 4

9 8 5

1 , 2

8 5

6 1 8

8 0 8

12.8

(38.3)

15.1

(10.0)

17.7

27.9

(28.7)

(50.0)

(40.0)

(30.0)

(20.0)

(10.0)

-

10.020.0

30.0

40.0

-

200

400

600

800

1,000

1,200

1,400

3QFY12 4QFY12 1QFY13 2QFY13 3QFY13 4QFY13 1QFY14

( % )

( `

c r )

Adj. PAT Adj. PAT growth (RHS)

Source: Company, Angel Research

7/27/2019 GAIL India, 1Q FY 2014

http://slidepdf.com/reader/full/gail-india-1q-fy-2014 6/12

GAIL | 1QFY2014 Result Update

July 26, 2013 6

Investment arguments

Upstream segment could see triggers: GAIL’s asset portfolio includes prospective

basins such as Myanmar fields and CBM blocks. We view these blocks as a

potential upside for the stock. Of the 27 exploratory blocks owned by GAIL, nine

blocks have potential hydrocarbon discoveries. Any material success in the form of

a major discovery could be a key catalyst for the stock.

Falling domestic gas production remains a concern: GAIL is expanding its

transmission capacity from 170mmscmd currently to 300mmscnd in the next two

years. However, gas production from the KG basin has declined significantly over

the past one year. Looking ahead, we do not expect any meaningful increase in

production at KG D6 in the coming year. Hence, we expect utilization levels for

GAIL’s pipelines to remain low during FY2014-15.

Outlook and valuation

Over the past one year, gas production from the KG basin has declined

significantly. Further, we do not expect any meaningful increase in the production

at KG D6 over the coming two years. Hence, we expect utilization levels for GAIL’s

pipelines to remain low during FY2014. Moreover, a cap on the gas marketing

margin (which is currently under review by PNGRB) would remain an overhang on

the stock. Hence, we maintain our Neutral rating on the stock.

Exhibit 9: SOTP valuation (FY2015E)

Business segment (` cr) EV `/share

NG transmission (EV/EBITDA 5.0x) 19,222 152

LPG transmission (EV/EBITDA 4.0x) 1,350 11

NG trading (EV/EBITDA 4.0x) 2,743 22

Petrochemicals (EV/EBITDA 4.0x) 7,481 59

LPG and liquid hydrocarbons (EV/EBITDA 4.0x) 4,627 36

E&P upsides (EV/boe 4.0x) 1,601 13

Investments (Book/Market Value X 80%) 2,868 23

Total EV 39,891 315

Net debt (1,582) (12)

Equity value (`) 41,473 327

Source: Company, Angel Research

7/27/2019 GAIL India, 1Q FY 2014

http://slidepdf.com/reader/full/gail-india-1q-fy-2014 7/12

GAIL | 1QFY2014 Result Update

July 26, 2013 7

Exhibit 10: Key assumptions

Particulars FY2014E FY2015E

Gas transmission volumes (mmscmd) 108 115

Gas trading volumes (mmscmd) 79 84 Source: Company, Angel Research

Exhibit 11: Angel EPS forecast vs consensus

(`) Angel forecast Bloomberg consensus Variation (%)

FY2014E 32.9 35.6 (7.6)

FY2015E 33.4 37.6 (11.1)

Source: Company, Angel Research

Exhibit 12: One-year forward P/E

0

100

200

300

400

500

600

700

800

A u g - 0

7

J a

n - 0

8

J u

n - 0

8

N o v - 0

8

A p r - 0 9

S e

p - 0

9

F e

b - 1

0

J

u l - 1 0

D e c - 1

0

M a y - 1

1

O

c t - 1 1

M a r - 1 2

A u g - 1

2

J a

n - 1

3

J u

n - 1

3

S h a r e p r i c e ( ` )

7x 10x 13x 16x 19x

Source: Company, Angel Research

Exhibit 13: Recommendation summary

Company CMP TP Reco. Mcap Upside P/E (x) P/BV (x) EV/EBITDA (x) RoE (%) RoCE (%)

(`) (`) (` cr) (%) FY14E FY15E FY14E FY15E FY14E FY15E FY14E FY15E FY14E FY15E

RIL 891 - Neutral 291,041 - 12.3 11.6 1.3 1.2 7.3 6.9 12.3 11.8 8.7 8.5

ONGC 305 387 Buy 262,268 27 8.8 7.3 1.5 1.3 3.8 2.8 18.3 19.4 19.0 21.1

Cairn India 305 364 Buy 58,208 19 4.9 5.3 1.0 0.9 2.6 2.4 22.6 17.8 21.8 17.4

GAIL 329 - Neutral 41,682 - 10.0 9.8 1.5 1.3 4.6 4.2 15.9 14.4 16.8 15.3

Source: Angel Research

Company background

Incorporated in August 1984, GAIL is India's flagship transmission and distribution

natural gas company engaged in the businesses of natural gas, LPG, liquid

hydrocarbons and petrochemicals. The company’s segments include Natural Gas

Marketing, Natural Gas Transmission, Liquefied Petroleum Gas (LPG)

Transmission Projects and other Hydrocarbon Production. Currently, GAIL operates

a natural gas transmission network of ~8,000km, with a capacity of 170mmscmd.

The company also has 27 oil and gas exploration blocks and three coal bed

methane blocks. The company has also diversified into exploration and production

and city gas distribution (CGD).

7/27/2019 GAIL India, 1Q FY 2014

http://slidepdf.com/reader/full/gail-india-1q-fy-2014 8/12

GAIL | 1QFY2014 Result Update

July 26, 2013 8

Profit and Loss Statement (Standalone)

Y/E March (` cr) FY2010 FY2011 FY2012 FY2013 FY2014E FY2015E

Net Sales 24,996 32,459 40,281 47,332 49,700 48,822

Other operating income - - 160 190Total operating income 24,996 32,459 40,441 47,522 49,700 48,822

% chg 5.1 29.9 24.6 17.5 4.6 (1.8)

Total Expenditure 20,327 27,004 34,842 41,053 41,730 40,741

Net Raw Materials 17,609 22,006 30,437 36,309 38,487 39,257

Other Mfg costs 950 2,046 3,755 3,959 2,395 613

Personnel 621 753 650 785 848 871

Other 1,147 2,199 - - - -

EBITDA 4,669 5,455 5,599 6,469 7,969 8,081

% chg 14.9 16.8 2.6 15.5 23.2 1.4

(% of Net Sales) 18.7 16.8 13.8 13.6 16.0 16.6

Depreciation & Amortization 562 650 791 981 1,840 1,852

EBIT 4,107 4,804 4,808 5,488 6,130 6,228

% chg 17.2 17.0 0.1 14.1 11.7 1.6

(% of Net Sales) 16.4 14.8 11.9 11.5 12.3 12.8

Interest & other Charges 70 83 116 195 220 253

Other Income 541 519 648 765 215 248

(% of PBT) 11.8 9.9 12.1 12.6 3.5 4.0

Share in profit of Associates - - - - - -

Recurring PBT 4,578 5,240 5,340 6,057 6,125 6,223

% chg 8.6 14.4 1.9 13.4 1.1 1.6

Extraordinary Expense/(Inc.) - - - - - -

PBT (reported) 4,578 5,240 5,340 6,057 6,125 6,223

Tax 1,439 1,679 1,686 2,036 1,954 1,985

(% of PBT) 31.4 32.0 31.6 33.6 31.9 31.9

PAT (reported) 3,140 3,561 3,654 4,021 4,171 4,238

Add: Share of earnings of asso. - - - - - -

Less: Minority interest (MI) - - - - - -

Prior period items - - - - - -

PAT after MI (reported) 3,140 3,561 3,654 4,021 4,171 4,238

ADJ. PAT 3,140 3,561 3,654 4,021 4,171 4,238

% chg 12.0 13.4 2.6 10.1 3.7 1.6(% of Net Sales) 12.6 11.0 9.0 8.5 8.4 8.7

Basic EPS (`) 24.8 28.1 28.8 31.7 32.9 33.4

Fully Diluted EPS (̀ ) 24.8 28.1 28.8 31.7 32.9 33.4

% chg 12.0 13.4 2.6 10.1 3.7 1.6

7/27/2019 GAIL India, 1Q FY 2014

http://slidepdf.com/reader/full/gail-india-1q-fy-2014 9/12

GAIL | 1QFY2014 Result Update

July 26, 2013 9

Balance Sheet (Standalone)

Y/E March (` cr) FY2010 FY2011 FY2012 FY2013E FY2014E FY2015E

SOURCES OF FUNDS

Equity Share Capital 1,268 1,268 1,268 1,268 1,268 1,268Reserves& Surplus 15,655 17,985 20,356 23,363 26,519 29,742

Shareholders’ Funds 16,924 19,253 21,624 24,631 27,788 31,011

Minority Interest - - - - - -

Total Loans 1,480 1,973 4,889 7,389 8,389 9,389

Deferred Tax Liability 1,390 1,633 1,769 1,769 1,769 1,769

Other Long Term Liabilities - 15 278 278 278 278

Long Term Provisions - 289 338 338 338 338

Total Liabilities 19,794 23,164 28,898 34,405 38,561 42,784

APPLICATION OF FUNDS

Gross Block 17,904 22,144 26,307 28,807 33,307 37,607

Less: Acc. Depreciation 9,115 9,741 10,449 11,430 13,269 15,122

Net Block 8,789 12,404 15,858 17,377 20,037 22,485

Capital Work-in-Progress 5,426 5,846 7,942 8,530 7,330 5,330

Goodwill - - - - - -

Investments 2,073 2,583 3,549 3,549 3,549 3,549

Long Term Loans and advances - 1,687 1,996 1,996 1,996 1,996

Other non-current assets - 73 272 272 272 272

Current Assets 13,884 9,420 9,468 16,077 18,927 22,477

Cash 4,343 2,131 931 7,285 9,971 13,588

Loans & Advances 7,606 4,596 5,211 5,211 5,211 5,211

Other 1,935 2,692 3,325 3,580 3,745 3,678

Current liabilities 10,378 8,848 10,186 13,396 13,550 13,325

Net Current Assets 3,506 572 (719) 2,681 5,377 9,152

Mis. Exp. not written off - - - - - -

Total Assets 19,794 23,164 28,898 34,405 38,561 42,784

7/27/2019 GAIL India, 1Q FY 2014

http://slidepdf.com/reader/full/gail-india-1q-fy-2014 10/12

GAIL | 1QFY2014 Result Update

July 26, 2013 10

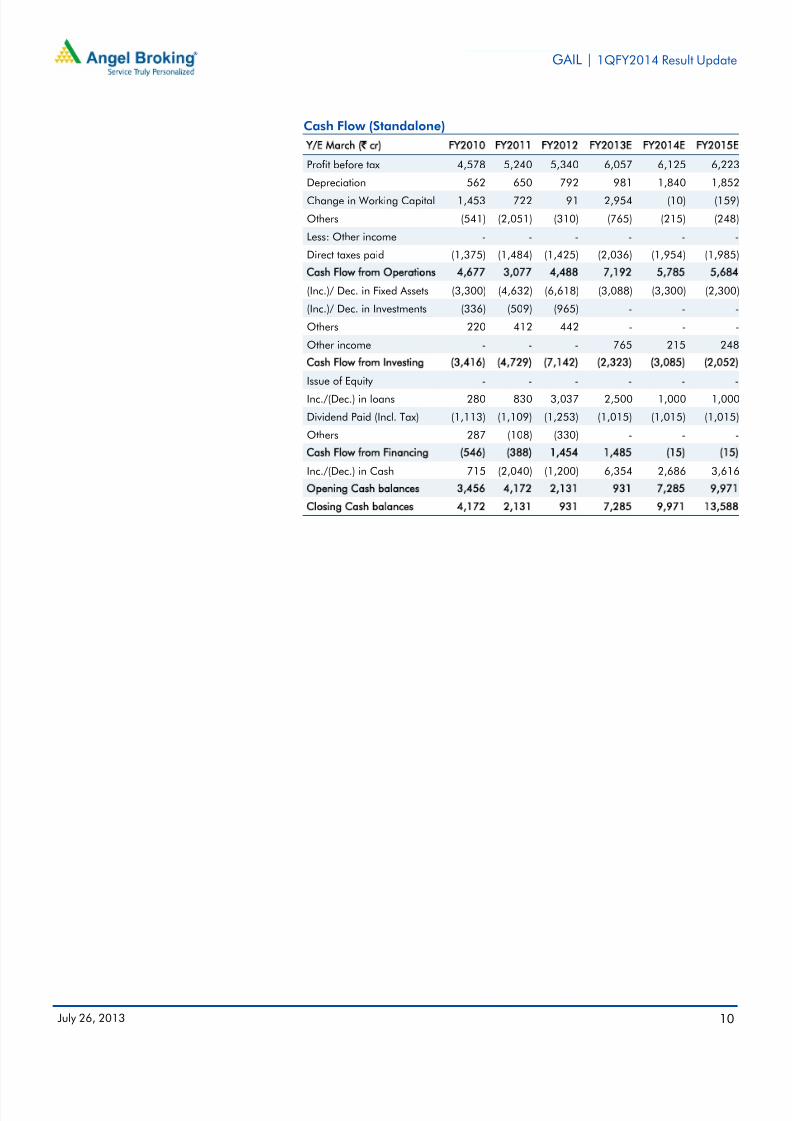

Cash Flow (Standalone)

Y/E March (` cr) FY2010 FY2011 FY2012 FY2013E FY2014E FY2015E

Profit before tax 4,578 5,240 5,340 6,057 6,125 6,223

Depreciation 562 650 792 981 1,840 1,852Change in Working Capital 1,453 722 91 2,954 (10) (159)

Others (541) (2,051) (310) (765) (215) (248)

Less: Other income - - - - - -

Direct taxes paid (1,375) (1,484) (1,425) (2,036) (1,954) (1,985)

Cash Flow from Operations 4,677 3,077 4,488 7,192 5,785 5,684

(Inc.)/ Dec. in Fixed Assets (3,300) (4,632) (6,618) (3,088) (3,300) (2,300)

(Inc.)/ Dec. in Investments (336) (509) (965) - - -

Others 220 412 442 - - -

Other income - - - 765 215 248

Cash Flow from Investing (3,416) (4,729) (7,142) (2,323) (3,085) (2,052)

Issue of Equity - - - - - -

Inc./(Dec.) in loans 280 830 3,037 2,500 1,000 1,000

Dividend Paid (Incl. Tax) (1,113) (1,109) (1,253) (1,015) (1,015) (1,015)

Others 287 (108) (330) - - -

Cash Flow from Financing (546) (388) 1,454 1,485 (15) (15)

Inc./(Dec.) in Cash 715 (2,040) (1,200) 6,354 2,686 3,616

Opening Cash balances 3,456 4,172 2,131 931 7,285 9,971

Closing Cash balances 4,172 2,131 931 7,285 9,971 13,588

7/27/2019 GAIL India, 1Q FY 2014

http://slidepdf.com/reader/full/gail-india-1q-fy-2014 11/12

GAIL | 1QFY2014 Result Update

July 26, 2013 11

Key Ratios

Y/E March FY2010 FY2011 FY2012 FY2013E FY2014E FY2015E

Valuation Ratio (x)

P/E (on FDEPS) 13.3 11.7 11.4 10.4 10.0 9.8P/CEPS 11.3 9.9 9.4 8.3 6.9 6.9

P/BV 2.5 2.2 1.9 1.7 1.5 1.3

Dividend yield (%) 2.3 2.3 3.0 2.4 2.4 2.4

EV/Sales 1.5 1.2 1.0 0.8 0.7 0.7

EV/EBITDA 7.9 7.1 7.5 5.9 4.6 4.2

EV/Total Assets 1.9 1.7 1.5 1.1 0.9 0.8

Per Share Data (`)

EPS (Basic) 24.8 28.1 28.8 31.7 32.9 33.4

EPS (fully diluted) 24.8 28.1 28.8 31.7 32.9 33.4

Cash EPS 29.2 33.2 35.0 39.4 47.4 48.0

DPS 7.5 7.5 9.9 8.0 8.0 8.0

Book Value 133.4 151.8 170.5 194.2 219.1 244.5

DuPont Analysis (%)

EBIT margin 16.4 14.8 11.9 11.5 12.3 12.8

Tax retention ratio 68.6 68.0 68.4 66.4 68.1 68.1

Asset turnover (x) 1.7 1.8 1.7 1.7 1.8 1.7

ROIC (Post-tax) 19.2 17.9 13.4 13.2 15.0 14.7

Cost of Debt (Post Tax) - - - - - -

Leverage (x) - - - - - -

Operating ROE 19.2 17.9 13.4 13.2 15.0 14.7

Returns (%)

ROCE (Pre-tax) 22.1 22.4 18.5 17.3 16.8 15.3

Angel ROIC (Pre-tax) 38.3 38.1 27.3 28.4 30.8 27.6

ROE 19.8 19.7 17.9 17.4 15.9 14.4

Turnover ratios (x)

Asset Turnover (Gross Block) 1.4 1.6 1.7 1.7 1.6 1.4

Inventory / Sales (days) 9.0 8.4 8.3 8.2 8.7 9.0

Receivables (days) 20 18 18 17 18 19

Payables (days) 86 69 66 77 82 84

WC cycle (ex-cash) (days) (2) (13) (14) (24) (34) (34)

Solvency ratios (x)Net debt to equity (0.3) (0.1) 0.0 (0.1) (0.2) (0.2)

Net debt to EBITDA (1.1) (0.5) 0.1 (0.5) (0.6) (1.0)

Interest Coverage (EBIT/Int.) 58.7 58.0 41.3 28.1 27.9 24.6

7/27/2019 GAIL India, 1Q FY 2014

http://slidepdf.com/reader/full/gail-india-1q-fy-2014 12/12

GAIL | 1QFY2014 Result Update

July 26 2013 12

Research Team Tel: 022 – 3935 7800 E-mail: [email protected] Website: www.angelbroking.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Pvt. Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliablesources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as thisdocument is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report .

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannottestify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel Broking Pvt. Limited endeavours to update on a reasonable basis the information discussed in this material, there may beregulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Pvt. Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment bankingor other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or

in the past.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to thelatest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates mayhave investment positions in the stocks recommended in this report.

Disclosure of Interest Statement GAIL

1. Analyst ownership of the stock No

2. Angel and its Group companies ownership of the stock No

3. Angel and its Group companies' Directors ownership of the stock No

4. Broking relationship with company covered No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors.

Ratings (Returns) : Buy (> 15%) Accumulate (5% to 15%) Neutral (-5 to 5%)Reduce (-5% to -15%) Sell (< -15%)