Download - GARP DUBAI CHAPTER

GARP DUBAI CHAPTER

Chapter Meeting

A Practical Approach to Internal Capital Adequacy Assessment Process (ICAAP)

Lola AhmedHead of Risk Management

Invest Bank, UAE

13th June 2012

ABOUT THE SPEAKER

� Lola Ahmed is an accomplished and enterprising banking professional with solid 37 years of experience and a strategist with charismatic trinity of leadership, management & team development, and administrative skills, backed by extensive experience who currently is head the Risk Management at Invest Bank in Sharjah.

� A visionary with proven expertise in all areas of Banking with proficiency in implementation of Risk Management Frameworks, Internal Capital Adequacy & Assessment Process (ICAAP) Basel II Frameworks, Basel III approaches, Project Finance, Corporate Commercial Banking, Contractor Finance . She is well versed with all Credit and Operational Risk Frameworks from both Basel II and Basel III perspectives with deep knowledge and domain expertise in developing Rating Models, all Credit Risk Management Frameworks for Standardized, Foundation and Advanced Measurement Approaches, Validations of all frameworks, Internal Capital Adequacy Assessment Process (ICAAP), RAROC and Operational Risk Frameworks (BIA to AMA Approaches).

ABOUT THE SPEAKER

� Lola’s Other Areas of Expertise include Change & Transitional Management ; System Development, Integration and Implementation ; Strategic Planning ; Translation of Business Strategy to Action Plans ; Credit Risk & Relationship Management ; Remedial and Recovery – Rescheduling / Restructuring ; Credit Control and Administration ; Extensive Financial & Analytical Skills ; Development of Marketing Strategies ; Writing Policies & guiding for procedural frameworks.

� She has conducted various workshops and has also represented the Bank on various seminars and conferences, risk Management Committees, active contributor to working groups of the UAE Central Bank.

� Prior to joining Invest bank she was a Corporate Manager with Barclays Bank, having had extensive experience for 21 years and two years with HSBC. She has an MBA in Finance from TIU, Missouri, USA and a CRA in addition to many certifications.

Lola Ahmed Lola Ahmed Lola Ahmed Lola Ahmed Head of Risk ManagementHead of Risk ManagementHead of Risk ManagementHead of Risk Management

Invest BankInvest BankInvest BankInvest Bank, Sharjah, UAE, Sharjah, UAE, Sharjah, UAE, Sharjah, UAE

GARPGARPGARPGARP

GLOBAL ASSOCIATION OF RISK PROFESSIONALS GLOBAL ASSOCIATION OF RISK PROFESSIONALS GLOBAL ASSOCIATION OF RISK PROFESSIONALS GLOBAL ASSOCIATION OF RISK PROFESSIONALS

DUBAI DUBAI DUBAI DUBAI –––– CHAPTER MEETINGCHAPTER MEETINGCHAPTER MEETINGCHAPTER MEETING

13th June 201213th June 201213th June 201213th June 2012

The views presented herein are of the presenter and not the Bank.

WORKSHOP STRUCTURE WORKSHOP STRUCTURE WORKSHOP STRUCTURE WORKSHOP STRUCTURE

AGENDAAGENDAAGENDAAGENDA

A very brief recap and overview of Basel II accord A very brief recap and overview of Basel II accord A very brief recap and overview of Basel II accord A very brief recap and overview of Basel II accord ---- followed by :followed by :followed by :followed by :

•What is ICAAP, What is ICAAP, What is ICAAP, What is ICAAP,

•The Definition andThe Definition andThe Definition andThe Definition and

•Objectives of ICAAP,Objectives of ICAAP,Objectives of ICAAP,Objectives of ICAAP,

•The difference between Regulatory and Economic Capital.The difference between Regulatory and Economic Capital.The difference between Regulatory and Economic Capital.The difference between Regulatory and Economic Capital.

•Guiding Principles of ICAAP,Guiding Principles of ICAAP,Guiding Principles of ICAAP,Guiding Principles of ICAAP,

•Key Features of ICAAP Key Features of ICAAP Key Features of ICAAP Key Features of ICAAP ----

A step by step Approach & methodology to preparing an ICAAPA step by step Approach & methodology to preparing an ICAAPA step by step Approach & methodology to preparing an ICAAPA step by step Approach & methodology to preparing an ICAAP

A few worksheets and policy guidelines will also be shown to A few worksheets and policy guidelines will also be shown to A few worksheets and policy guidelines will also be shown to A few worksheets and policy guidelines will also be shown to understand the calculation and process.understand the calculation and process.understand the calculation and process.understand the calculation and process.

A QUICK RECAP &A QUICK RECAP &A QUICK RECAP &A QUICK RECAP &

AN OVERVIEW OF BASEL II ACCORD AN OVERVIEW OF BASEL II ACCORD AN OVERVIEW OF BASEL II ACCORD AN OVERVIEW OF BASEL II ACCORD

Basel II Accord issued by Basel Committee of Banking Basel II Accord issued by Basel Committee of Banking Basel II Accord issued by Basel Committee of Banking Basel II Accord issued by Basel Committee of Banking Supervision (BCBS) in June 2004, provided additional Supervision (BCBS) in June 2004, provided additional Supervision (BCBS) in June 2004, provided additional Supervision (BCBS) in June 2004, provided additional guidelinesguidelinesguidelinesguidelines––––

With emphasis on risk management processes for calculation of minimum capital requirements i.e. risk sensitive capital requirements

And established market disclosure requirements

A QUICK RECAP &A QUICK RECAP &A QUICK RECAP &A QUICK RECAP &

AN OVERVIEW OF BASEL II ACCORD AN OVERVIEW OF BASEL II ACCORD AN OVERVIEW OF BASEL II ACCORD AN OVERVIEW OF BASEL II ACCORD

With a prime objective to improve risk management

In short Basel I was Top Down – very broad based, simple, regulatory with common norms.

Basel II is Bottom Up, more internal and choice driven, segment based, with specific norms.

AsAsAsAs aaaa consequenceconsequenceconsequenceconsequence ofofofof BaselBaselBaselBasel II,II,II,II, BanksBanksBanksBanks andandandand FinancialFinancialFinancialFinancialInstitutionsInstitutionsInstitutionsInstitutions areareareare compelledcompelledcompelledcompelled totototo developdevelopdevelopdevelop internalinternalinternalinternalpolicies,policies,policies,policies, approaches,approaches,approaches,approaches, proceduresproceduresproceduresprocedures andandandand aaaa structurestructurestructurestructuretotototo ensureensureensureensure theytheytheythey possesspossesspossesspossess adequateadequateadequateadequate capitalcapitalcapitalcapital inininin thethethethelonglonglonglong termtermtermterm bybybyby factoringfactoringfactoringfactoring inininin allallallall materialmaterialmaterialmaterial risksrisksrisksrisks –––– ThisThisThisThisentireentireentireentire processprocessprocessprocess collectivelycollectivelycollectivelycollectively isisisis calledcalledcalledcalled anananan “ICAAP”“ICAAP”“ICAAP”“ICAAP”....

AnAnAnAn ICAAPICAAPICAAPICAAP processprocessprocessprocess isisisis aaaa tooltooltooltool forforforfor betterbetterbetterbetter riskriskriskriskmanagementmanagementmanagementmanagement andandandand isisisis applicableapplicableapplicableapplicable totototo allallallall Banks,Banks,Banks,Banks,financialfinancialfinancialfinancial organizations,organizations,organizations,organizations, insuranceinsuranceinsuranceinsurance companiescompaniescompaniescompanies....

BASEL II ACCORDBASEL II ACCORDBASEL II ACCORDBASEL II ACCORD

Basel II Basel II Basel II Basel II Accord has Accord has Accord has Accord has

three three three three mutually mutually mutually mutually

reinforcing reinforcing reinforcing reinforcing pillars i.e.pillars i.e.pillars i.e.pillars i.e.

Pillar 1 Pillar 1 Pillar 1 Pillar 1 Minimal Minimal Minimal Minimal Capital Capital Capital Capital RequiremenRequiremenRequiremenRequirements (for CR, ts (for CR, ts (for CR, ts (for CR, MR and OR)MR and OR)MR and OR)MR and OR)

Pillar 2 Pillar 2 Pillar 2 Pillar 2

Supervisory Supervisory Supervisory Supervisory Review Review Review Review

Pillar 3 Pillar 3 Pillar 3 Pillar 3 Market Market Market Market

DisciplineDisciplineDisciplineDiscipline

ICAAP is ICAAP is ICAAP is ICAAP is part of part of part of part of

Pillar 2 Pillar 2 Pillar 2 Pillar 2 and is followed

by supervisory supervisory supervisory supervisory Review (by Review (by Review (by Review (by

the the the the Regulator) Regulator) Regulator) Regulator) .

A SNAP SHOT

10

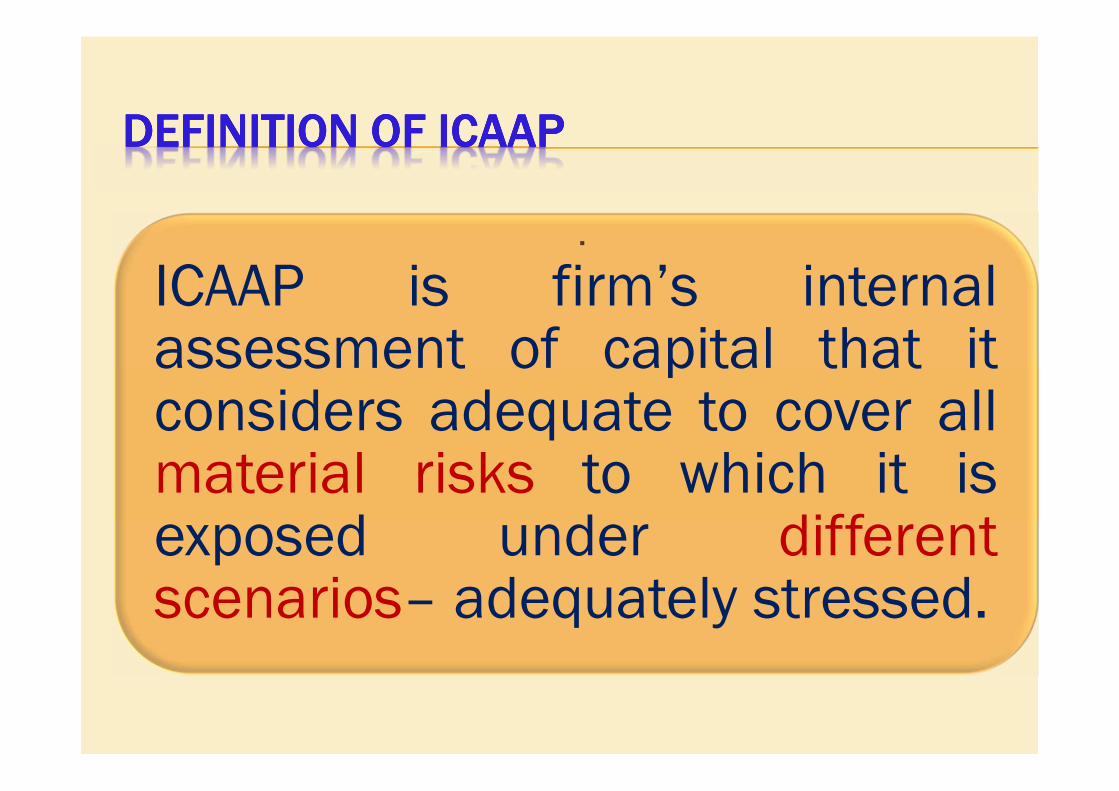

DEFINITION OF ICAAPDEFINITION OF ICAAPDEFINITION OF ICAAPDEFINITION OF ICAAP

ICAAP is firm’s internalassessment of capital that itconsiders adequate to cover allmaterial risks to which it isexposed under differentscenarios– adequately stressed.

.

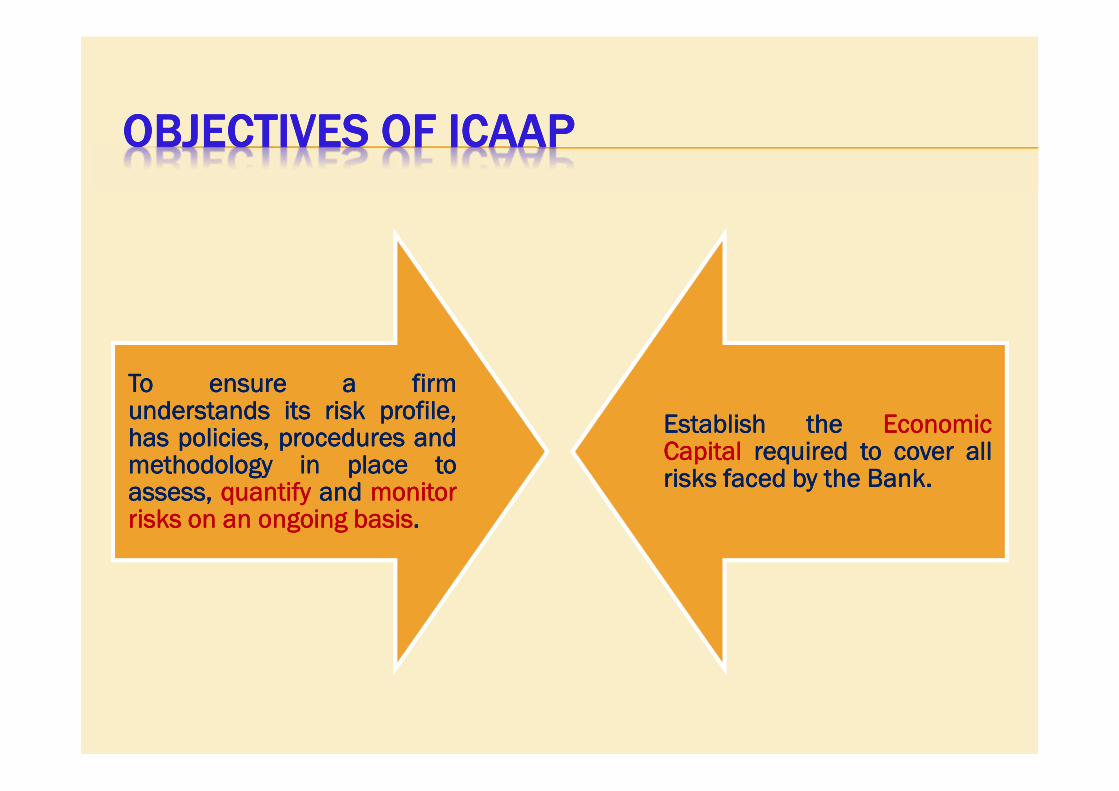

OBJECTIVES OF ICAAPOBJECTIVES OF ICAAPOBJECTIVES OF ICAAPOBJECTIVES OF ICAAP

ToToToTo ensureensureensureensure aaaa firmfirmfirmfirmunderstandsunderstandsunderstandsunderstands itsitsitsits riskriskriskrisk profile,profile,profile,profile,hashashashas policies,policies,policies,policies, proceduresproceduresproceduresprocedures andandandandmethodologymethodologymethodologymethodology inininin placeplaceplaceplace totototoassess,assess,assess,assess, quantifyquantifyquantifyquantify andandandand monitormonitormonitormonitorrisksrisksrisksrisks onononon anananan ongoingongoingongoingongoing basisbasisbasisbasis....

EstablishEstablishEstablishEstablish thethethethe EconomicEconomicEconomicEconomicCapitalCapitalCapitalCapital requiredrequiredrequiredrequired totototo covercovercovercover allallallallrisksrisksrisksrisks facedfacedfacedfaced bybybyby thethethethe BankBankBankBank....

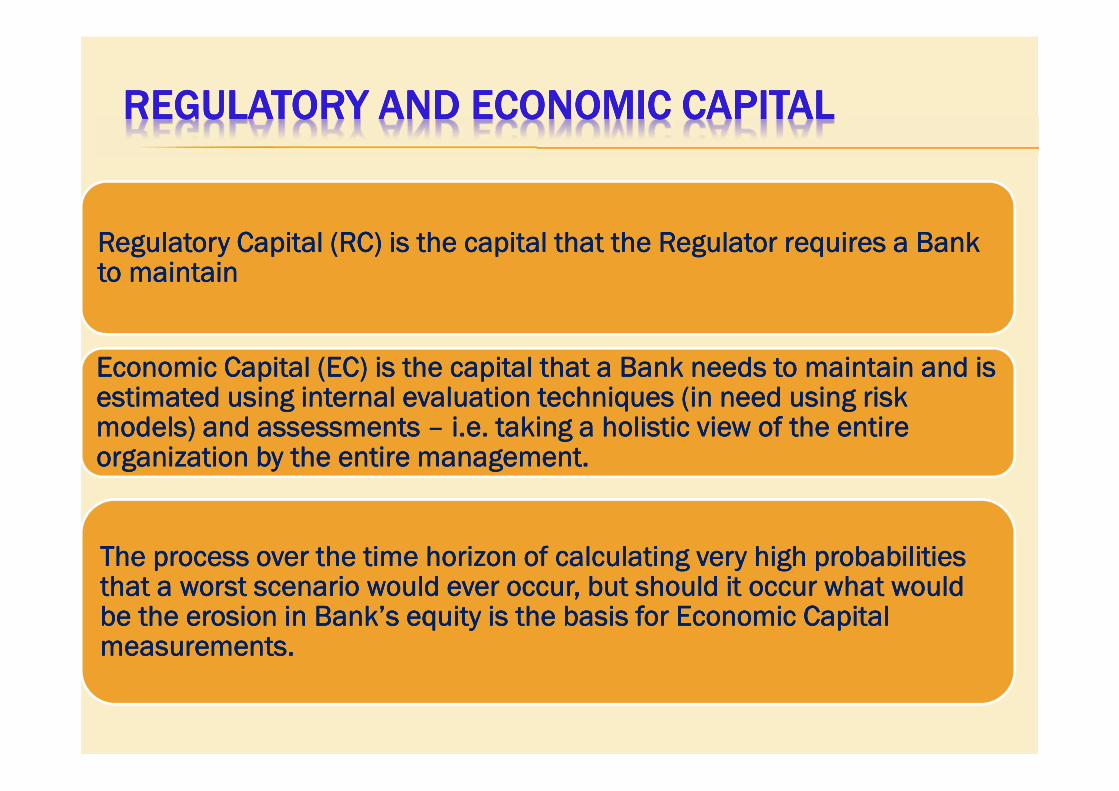

REGULATORY AND ECONOMIC CAPITALREGULATORY AND ECONOMIC CAPITALREGULATORY AND ECONOMIC CAPITALREGULATORY AND ECONOMIC CAPITAL

Regulatory Capital (RC) is the capital that the Regulator requires a Bank Regulatory Capital (RC) is the capital that the Regulator requires a Bank Regulatory Capital (RC) is the capital that the Regulator requires a Bank Regulatory Capital (RC) is the capital that the Regulator requires a Bank to maintain to maintain to maintain to maintain

Economic Capital (EC) is the capital that a Bank needs to maintain and is Economic Capital (EC) is the capital that a Bank needs to maintain and is Economic Capital (EC) is the capital that a Bank needs to maintain and is Economic Capital (EC) is the capital that a Bank needs to maintain and is estimated using internal evaluation techniques (in need using risk estimated using internal evaluation techniques (in need using risk estimated using internal evaluation techniques (in need using risk estimated using internal evaluation techniques (in need using risk models) and assessments models) and assessments models) and assessments models) and assessments –––– i.e. taking a holistic view of the entire i.e. taking a holistic view of the entire i.e. taking a holistic view of the entire i.e. taking a holistic view of the entire organization by the entire management.organization by the entire management.organization by the entire management.organization by the entire management.

The process over the time horizon of calculating very high probabilities The process over the time horizon of calculating very high probabilities The process over the time horizon of calculating very high probabilities The process over the time horizon of calculating very high probabilities that a worst scenario would ever occur, but should it occur what would that a worst scenario would ever occur, but should it occur what would that a worst scenario would ever occur, but should it occur what would that a worst scenario would ever occur, but should it occur what would be the erosion in Bank’s equity is the basis for Economic Capital be the erosion in Bank’s equity is the basis for Economic Capital be the erosion in Bank’s equity is the basis for Economic Capital be the erosion in Bank’s equity is the basis for Economic Capital measurements. measurements. measurements. measurements.

REGULATORY AND ECONOMIC CAPITALREGULATORY AND ECONOMIC CAPITALREGULATORY AND ECONOMIC CAPITALREGULATORY AND ECONOMIC CAPITAL

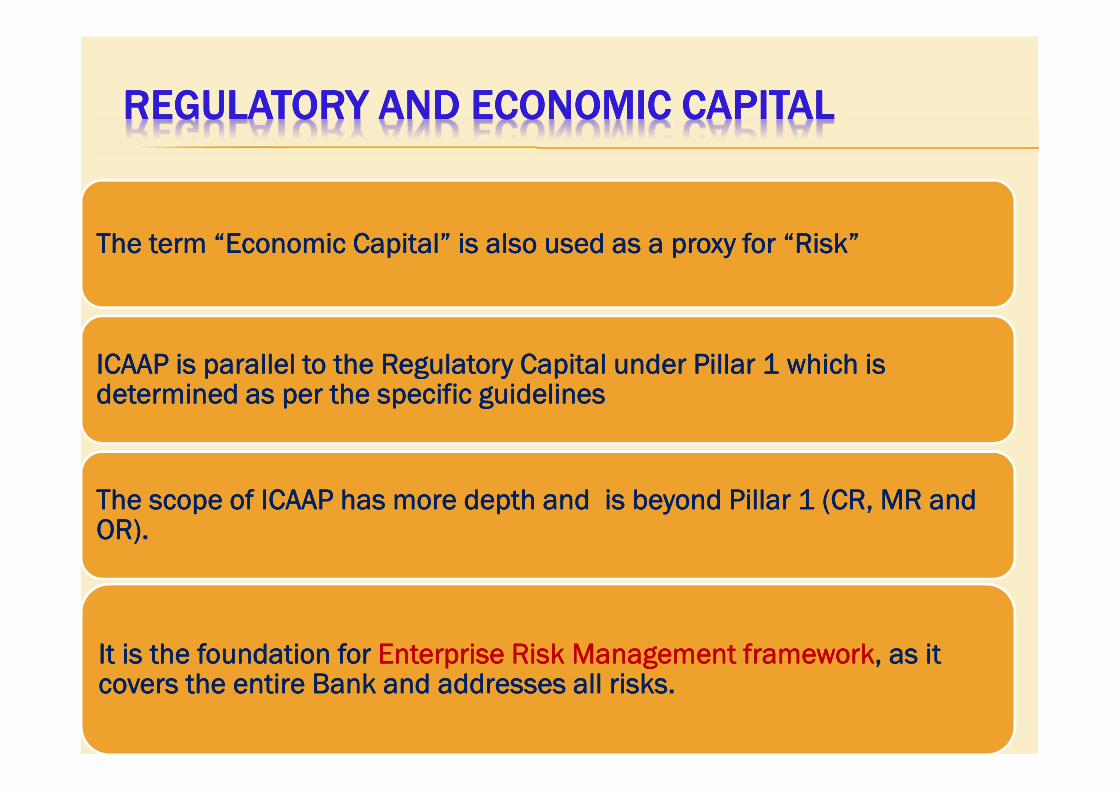

The term “Economic Capital” is also used as a proxy for “Risk”The term “Economic Capital” is also used as a proxy for “Risk”The term “Economic Capital” is also used as a proxy for “Risk”The term “Economic Capital” is also used as a proxy for “Risk”

ICAAP is parallel to the Regulatory Capital under Pillar 1 which is ICAAP is parallel to the Regulatory Capital under Pillar 1 which is ICAAP is parallel to the Regulatory Capital under Pillar 1 which is ICAAP is parallel to the Regulatory Capital under Pillar 1 which is determined as per the specific guidelinesdetermined as per the specific guidelinesdetermined as per the specific guidelinesdetermined as per the specific guidelines

The scope of ICAAP has more depth and is beyond Pillar 1 (CR, MR and The scope of ICAAP has more depth and is beyond Pillar 1 (CR, MR and The scope of ICAAP has more depth and is beyond Pillar 1 (CR, MR and The scope of ICAAP has more depth and is beyond Pillar 1 (CR, MR and OR).OR).OR).OR).

It is the foundation for It is the foundation for It is the foundation for It is the foundation for Enterprise Risk Management frameworkEnterprise Risk Management frameworkEnterprise Risk Management frameworkEnterprise Risk Management framework, as it , as it , as it , as it covers the entire Bank and addresses all risks.covers the entire Bank and addresses all risks.covers the entire Bank and addresses all risks.covers the entire Bank and addresses all risks.

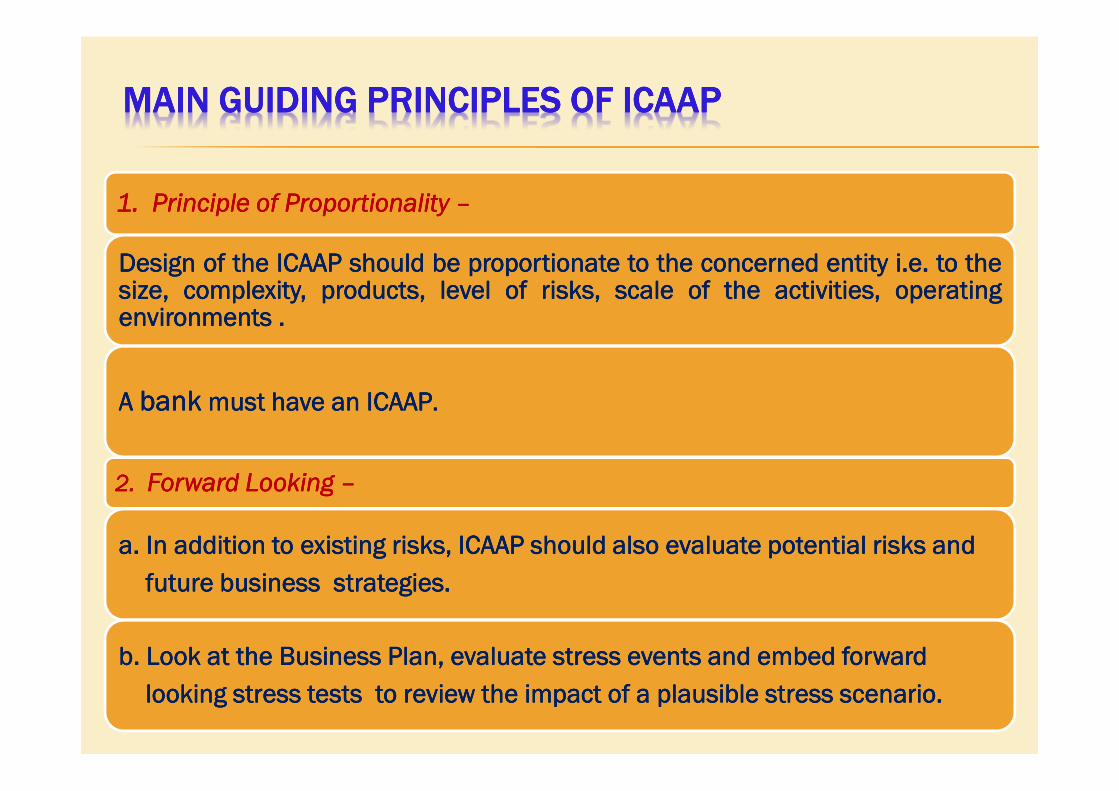

MAIN GUIDING PRINCIPLES OF ICAAPMAIN GUIDING PRINCIPLES OF ICAAPMAIN GUIDING PRINCIPLES OF ICAAPMAIN GUIDING PRINCIPLES OF ICAAP

1. 1. 1. 1. Principle Principle Principle Principle

of of of of ProporProporProporPropor----tionalitytionalitytionalitytionality

2. Forward 2. Forward 2. Forward 2. Forward Looking Looking Looking Looking

3. 3. 3. 3. Ongoing Ongoing Ongoing Ongoing Exercise Exercise Exercise Exercise

4. Evolving 4. Evolving 4. Evolving 4. Evolving NatureNatureNatureNature

Principles Principles Principles Principles

of of of of

ICAAPICAAPICAAPICAAP

MAIN GUIDING PRINCIPLES OF ICAAPMAIN GUIDING PRINCIPLES OF ICAAPMAIN GUIDING PRINCIPLES OF ICAAPMAIN GUIDING PRINCIPLES OF ICAAP

1111.... PrinciplePrinciplePrinciplePrinciple ofofofof ProportionalityProportionalityProportionalityProportionality ––––

DesignDesignDesignDesign ofofofof thethethethe ICAAPICAAPICAAPICAAP shouldshouldshouldshould bebebebe proportionateproportionateproportionateproportionate totototo thethethethe concernedconcernedconcernedconcerned entityentityentityentity iiii....eeee.... totototo thethethethesize,size,size,size, complexity,complexity,complexity,complexity, products,products,products,products, levellevellevellevel ofofofof risks,risks,risks,risks, scalescalescalescale ofofofof thethethethe activities,activities,activities,activities, operatingoperatingoperatingoperatingenvironmentsenvironmentsenvironmentsenvironments ....

AAAA bankbankbankbank mustmustmustmust havehavehavehave anananan ICAAPICAAPICAAPICAAP....

2222.... ForwardForwardForwardForward LookingLookingLookingLooking ––––

aaaa.... InInInIn additionadditionadditionaddition totototo existingexistingexistingexisting risks,risks,risks,risks, ICAAPICAAPICAAPICAAP shouldshouldshouldshould alsoalsoalsoalso evaluateevaluateevaluateevaluate potentialpotentialpotentialpotential risksrisksrisksrisks andandandand

futurefuturefuturefuture businessbusinessbusinessbusiness strategiesstrategiesstrategiesstrategies....

bbbb.... LookLookLookLook atatatat thethethethe BusinessBusinessBusinessBusiness Plan,Plan,Plan,Plan, evaluateevaluateevaluateevaluate stressstressstressstress eventseventseventsevents andandandand embedembedembedembed forwardforwardforwardforward

lookinglookinglookinglooking stressstressstressstress teststeststeststests totototo reviewreviewreviewreview thethethethe impactimpactimpactimpact ofofofof aaaa plausibleplausibleplausibleplausible stressstressstressstress scenarioscenarioscenarioscenario....

MAIN GUIDING PRINCIPLES OF ICAAPMAIN GUIDING PRINCIPLES OF ICAAPMAIN GUIDING PRINCIPLES OF ICAAPMAIN GUIDING PRINCIPLES OF ICAAP

3. Ongoing Exercise 3. Ongoing Exercise 3. Ongoing Exercise 3. Ongoing Exercise ––––

ICAAP is a dynamic, continuous process and not a one time static process to ensure entity has sufficient capital at all times for all risks.

Subject to regular review

4. Evolving Nature 4. Evolving Nature 4. Evolving Nature 4. Evolving Nature ––––

Need to monitor the ICAAP for its efficacy so that it can be improved based on changes in Business Plan and the risk profile / risk appetite.

Use simpler methods for some risks but plan to switch to advanced techniques as you progress and if changes in risk levels warrants.

KEY FEATURES OF ICAAPKEY FEATURES OF ICAAPKEY FEATURES OF ICAAPKEY FEATURES OF ICAAP

Basel II has outlined five main features of ICAAP as follows :Basel II has outlined five main features of ICAAP as follows :Basel II has outlined five main features of ICAAP as follows :Basel II has outlined five main features of ICAAP as follows :

1. Senior Management Oversight 1. Senior Management Oversight 1. Senior Management Oversight 1. Senior Management Oversight –––– including Board of Directors including Board of Directors including Board of Directors including Board of Directors

• Responsibility is entrusted to the BOD and senior management proportionate to the Business Plan, Strategy, Risk Profile, risk appetite, current and future capital needs.

2. ICAAP’s relevance to all material risks 2. ICAAP’s relevance to all material risks 2. ICAAP’s relevance to all material risks 2. ICAAP’s relevance to all material risks ––––

• Have comprehensive and complete framework for identification, quantification, aggregation and reporting. Establish internal capital adequacy goals and have an internal process for control, review and audits.

• Basel II has not given has not given has not given has not given a comprehensive list of all risks - It is the Bank’s responsibility to identify all the material risks.

• In addition to CR, MR and OR, review and assess all material risks all material risks all material risks all material risks viz:

• Concentration Risks (in assets, geographic, activity, products etc)

• IRRIBB – Interest Rate Risk in the Banking Book -

• Liquidity Risk and Other RisksOther RisksOther RisksOther Risks such as :•Strategic Risk, Business Risk, Reputation Risk, Legal Risk, Model Risk property

risks etc

KEY FEATURES OF ICAAP (CONTD…)KEY FEATURES OF ICAAP (CONTD…)KEY FEATURES OF ICAAP (CONTD…)KEY FEATURES OF ICAAP (CONTD…)

3333....ComprehensiveComprehensiveComprehensiveComprehensive CapitalCapitalCapitalCapital Assessment,Assessment,Assessment,Assessment, aggregationaggregationaggregationaggregation &&&& StressStressStressStress TestingTestingTestingTesting ––––

• Calculate capital charge for each of the risks on a granular level.

• Should form an integral part of the risk management and decision making culture i.e. actively used by the Bank.

• Hence a thorough analysis of Bank’s activities, its business units, its products, operating, regulatory and market environments, historical scenarios etc is required.

• Aggregation can be based on simple aggregation or by taking diversification effects if applicable.

KEY FEATURES OF ICAAP (CONTD…)KEY FEATURES OF ICAAP (CONTD…)KEY FEATURES OF ICAAP (CONTD…)KEY FEATURES OF ICAAP (CONTD…)

4. Level of Disclosure to the Regulator4. Level of Disclosure to the Regulator4. Level of Disclosure to the Regulator4. Level of Disclosure to the Regulator

• Reporting and Monitoring - Have appropriate framework with necessary information on the risk profile, trends, and capital requirements, accuracy of data accuracy of data accuracy of data accuracy of data and the stress scenarios.

• Have clear policies defining all risks and describing the clear policies defining all risks and describing the clear policies defining all risks and describing the clear policies defining all risks and describing the methodology methodology methodology methodology used for calculations

KEY FEATURES OF ICAAP (CONTD…)KEY FEATURES OF ICAAP (CONTD…)KEY FEATURES OF ICAAP (CONTD…)KEY FEATURES OF ICAAP (CONTD…)

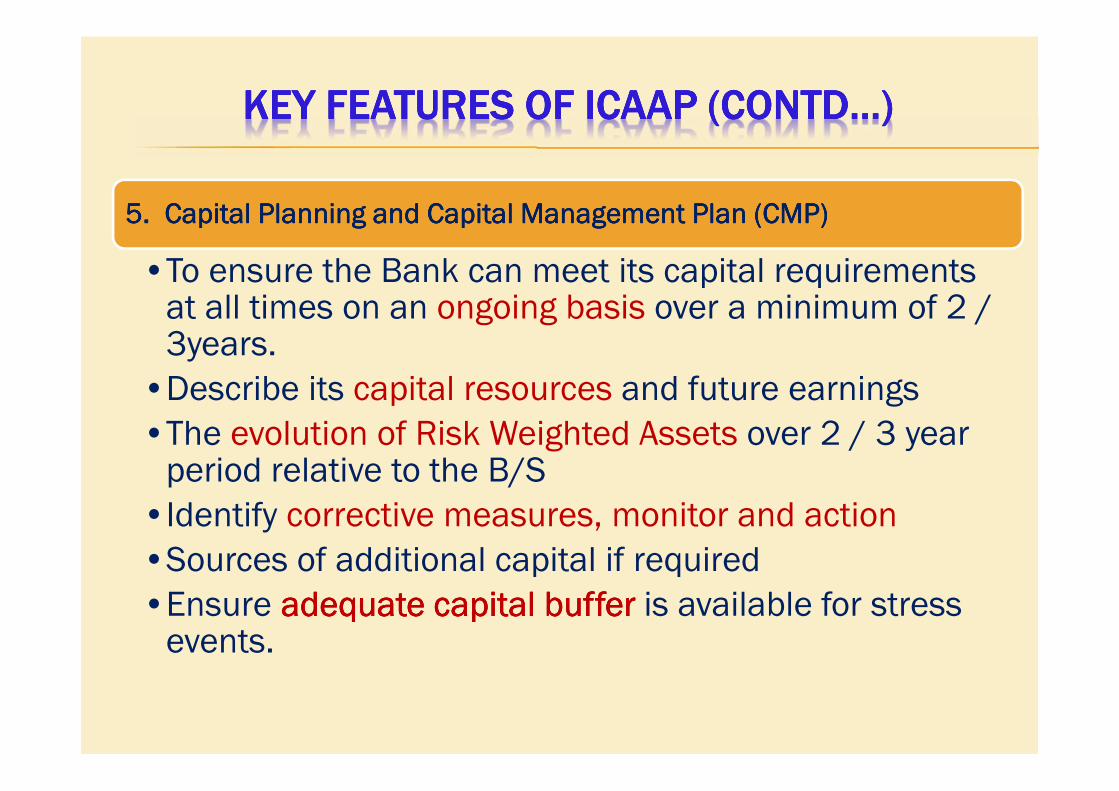

5. Capital Planning and Capital Management Plan (CMP)5. Capital Planning and Capital Management Plan (CMP)5. Capital Planning and Capital Management Plan (CMP)5. Capital Planning and Capital Management Plan (CMP)

•To ensure the Bank can meet its capital requirements at all times on an ongoing basis over a minimum of 2 / 3years.

•Describe its capital resources and future earnings

•The evolution of Risk Weighted Assets over 2 / 3 year period relative to the B/S

•Identify corrective measures, monitor and action

•Sources of additional capital if required

•Ensure adequate capital buffer adequate capital buffer adequate capital buffer adequate capital buffer is available for stress events.

EMBEDDING OBJECTIVES, PRINCIPLES AND FEATURES

INTO ICAAP

OVERVIEW OF APPROACH FOR

IDENTIFICATION, MATERIALITY AND METHODS

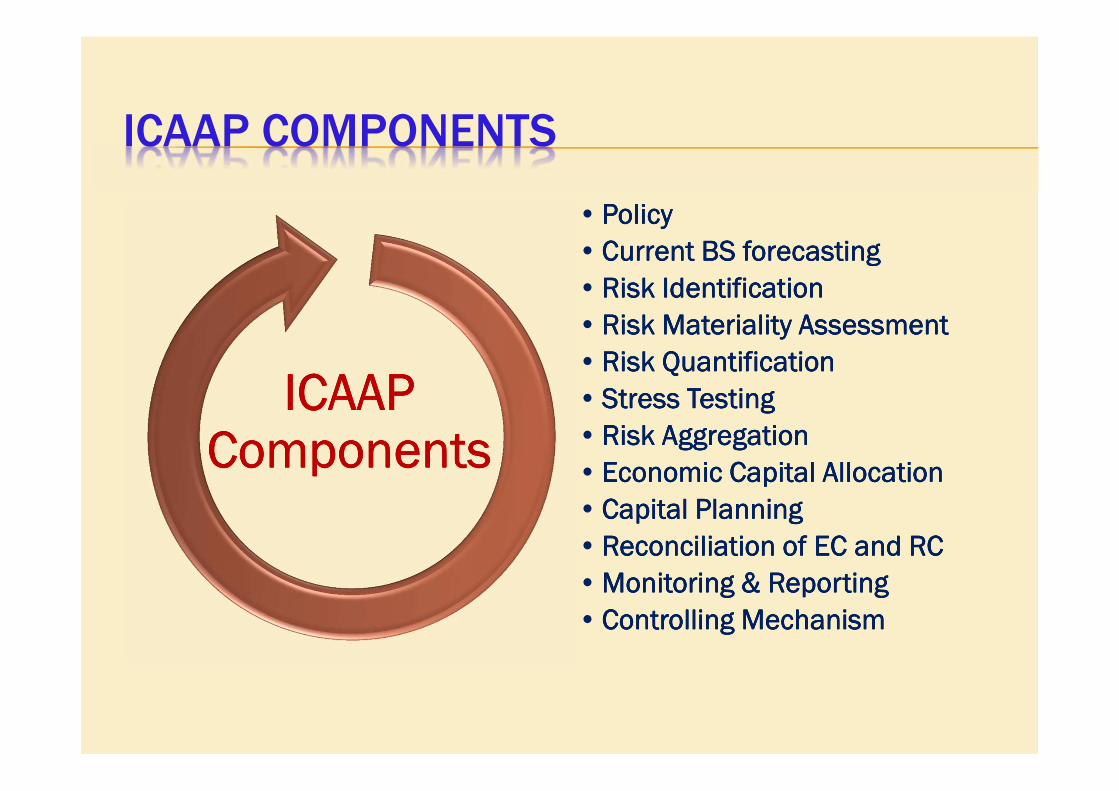

ICAAP COMPONENTS

• PolicyPolicyPolicyPolicy

• Current BS forecastingCurrent BS forecastingCurrent BS forecastingCurrent BS forecasting

• Risk IdentificationRisk IdentificationRisk IdentificationRisk Identification

• Risk Materiality AssessmentRisk Materiality AssessmentRisk Materiality AssessmentRisk Materiality Assessment

• Risk QuantificationRisk QuantificationRisk QuantificationRisk Quantification

• Stress TestingStress TestingStress TestingStress Testing

• Risk AggregationRisk AggregationRisk AggregationRisk Aggregation

• Economic Capital AllocationEconomic Capital AllocationEconomic Capital AllocationEconomic Capital Allocation

• Capital PlanningCapital PlanningCapital PlanningCapital Planning

• Reconciliation of EC and RCReconciliation of EC and RCReconciliation of EC and RCReconciliation of EC and RC

• Monitoring & ReportingMonitoring & ReportingMonitoring & ReportingMonitoring & Reporting

• Controlling MechanismControlling MechanismControlling MechanismControlling Mechanism

ICAAP ICAAP ICAAP ICAAP ComponentsComponentsComponentsComponents

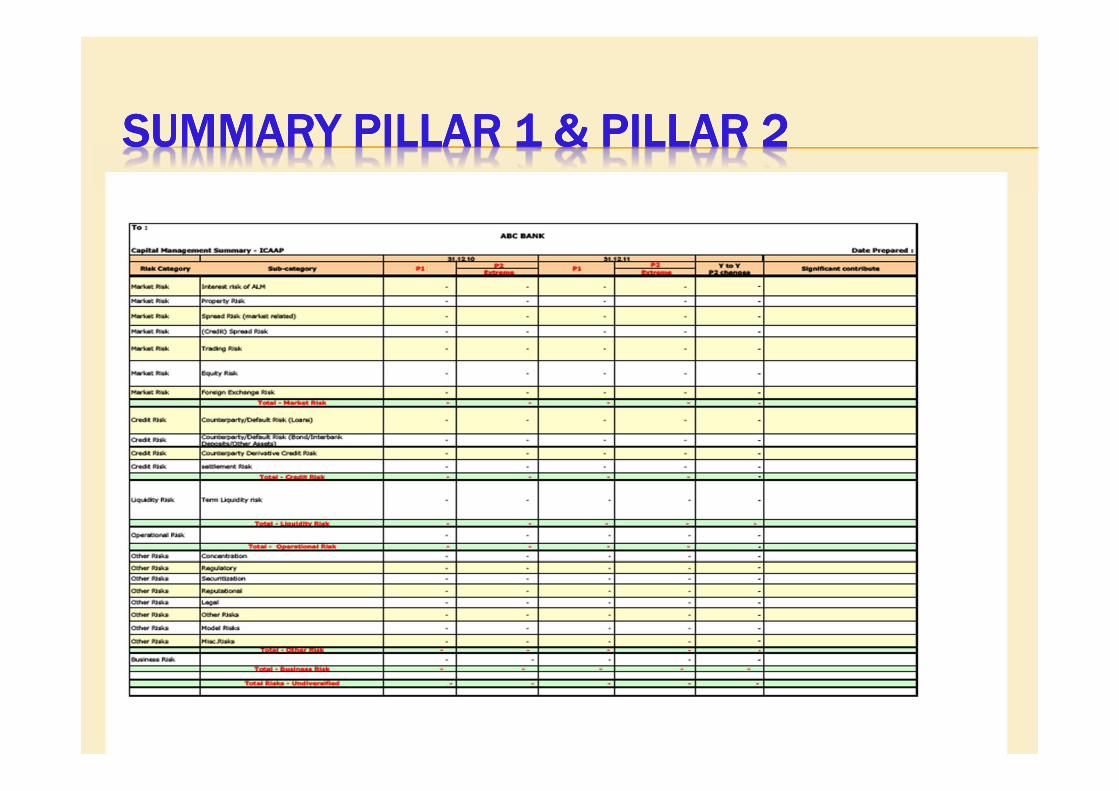

SUMMARY PILLAR 1 & PILLAR 2SUMMARY PILLAR 1 & PILLAR 2SUMMARY PILLAR 1 & PILLAR 2SUMMARY PILLAR 1 & PILLAR 2

ICAAP POLICIESICAAP POLICIESICAAP POLICIESICAAP POLICIES

Develop and establish detailed policies (ideally two separate ideally two separate ideally two separate ideally two separate policiespoliciespoliciespolicies) :

One to outline the Bank’s Integrated Policy for ICAAP One to outline the Bank’s Integrated Policy for ICAAP One to outline the Bank’s Integrated Policy for ICAAP One to outline the Bank’s Integrated Policy for ICAAP which should encompass Identification, Assessment of material risks, define Risk Appetite, Risk Management Framework, together with the approach taken to manage all risks :

Direction for Policy writing is provided by way of basic contents –

ICAAP POLICIESICAAP POLICIESICAAP POLICIESICAAP POLICIES

Second Policy should outline Measurement, Aggregation and Second Policy should outline Measurement, Aggregation and Second Policy should outline Measurement, Aggregation and Second Policy should outline Measurement, Aggregation and

utilization of Bank’s capital for all the risks, ICAAP Approach, utilization of Bank’s capital for all the risks, ICAAP Approach, utilization of Bank’s capital for all the risks, ICAAP Approach, utilization of Bank’s capital for all the risks, ICAAP Approach,

Processes, Definitions, Hedging Objectives etc.Processes, Definitions, Hedging Objectives etc.Processes, Definitions, Hedging Objectives etc.Processes, Definitions, Hedging Objectives etc.

Some guidelines Some guidelines Some guidelines Some guidelines ::::

� IntroductionIntroductionIntroductionIntroduction

� Approaches (define the approach being used and why)

� ICAAP process (Risk Assessment, Total Required Risk Capital,

Risk Bearing Capacity (available vs required), Monitoring and

Mitigants)

� Hedging objectives

ICAAP POLICIESICAAP POLICIESICAAP POLICIESICAAP POLICIES

� BOTTOM UP APPROACHBOTTOM UP APPROACHBOTTOM UP APPROACHBOTTOM UP APPROACH

� Introduction,

� Risk Assessment (definition, chosen measurement method substantiating the choice, internal / external models),

� scenario analysis / stress testing, techniques used to validate the chosen methods and results.

� Comparison of results between ICAAP and Pillar 1 where relevant supported by source documents.

� Allocation and calculation.

ICAAP POLICIESICAAP POLICIESICAAP POLICIESICAAP POLICIES

Suggested format –

Please list the Risk type and have the following standard headings

under each :

� Definition

� Chosen ICAAP measurement method and why

� Detailed description of method

� Results – as at 31-12-11 - ??

� List Mitigants or instant Management actions (e.g. movement in

interest rates)

� Stress Testing

� Comparison with Pillar 1

Where necessary elaborate or expand ….

APPROACHES

3 Approaches for assessing and calculating EC3 Approaches for assessing and calculating EC3 Approaches for assessing and calculating EC3 Approaches for assessing and calculating EC3 Approaches for assessing and calculating EC3 Approaches for assessing and calculating EC3 Approaches for assessing and calculating EC3 Approaches for assessing and calculating EC

Top Down Approach (TDA) Top Down Approach (TDA) Top Down Approach (TDA) Top Down Approach (TDA) or Earnings Approach or Earnings Approach or Earnings Approach or Earnings Approach

Also known as Library Approach.

Here the volatility of the P & L and its impact is

analyzed

A (global) Stress Scenario A (global) Stress Scenario A (global) Stress Scenario A (global) Stress Scenario Approach Approach Approach Approach –

Extraordinary events are assessed and taken into account that can have

considerable impact on the Bank that may need protection. These events are individually compared with the available capital. No probability is attached

only impact is measured or estimated and compared to the available capital.

Bottom Up Approach (BUA) Bottom Up Approach (BUA) Bottom Up Approach (BUA) Bottom Up Approach (BUA) or A Value Approachor A Value Approachor A Value Approachor A Value Approach

Also known as Questionnaire Approach.

All risks are assessed and modeled individually, summed taking into

account the diversification effects.

Of the three, for this Of the three, for this Of the three, for this Of the three, for this regionregionregionregion, the BUA is more practical to adopt and offers more realistic , the BUA is more practical to adopt and offers more realistic , the BUA is more practical to adopt and offers more realistic , the BUA is more practical to adopt and offers more realistic

calculationscalculationscalculationscalculations

ALLOCATION AND CALCULATION

Steps :Steps :Steps :Steps :

A. Risk Identification and Assessment

B. Calculate Total Required Risk Capital and determine Risk Coverage

Capital – RCC

C. Compare the available with the Required Risk Capital called the called the called the called the

Risk Bearing CapacityRisk Bearing CapacityRisk Bearing CapacityRisk Bearing Capacity

ALLOCATION AND CALCULATION

How –

Use the following three Hedging Objectives (Extreme, severe, moderate) – i.e.

using of scenarios at different confidence levels

1.1.1.1. Extreme / survival scenarioExtreme / survival scenarioExtreme / survival scenarioExtreme / survival scenario – also known as Worst Case ScenarioWorst Case ScenarioWorst Case ScenarioWorst Case Scenario – at at at at

99.9%99.9%99.9%99.9% confidence level.confidence level.confidence level.confidence level.

Means the Economic Risk is unlikely to exceed (99.9% probability) when

compared to the sustainable Economic Risk Coverage Capital.

2.2.2.2. Going Concern or the Early Warning LevelGoing Concern or the Early Warning LevelGoing Concern or the Early Warning LevelGoing Concern or the Early Warning Level – at :

o 95% confidence (severe)95% confidence (severe)95% confidence (severe)95% confidence (severe) i.e. 5% probability of happening each year

and estimation of risks happening once in 20 years.

3.3.3.3. Going Concern or the Early Warning LevelGoing Concern or the Early Warning LevelGoing Concern or the Early Warning LevelGoing Concern or the Early Warning Level – at :

o 80% confidence (moderate)80% confidence (moderate)80% confidence (moderate)80% confidence (moderate) i.e 20% probability of happening each year

and estimation of risks happening once in every 5 years.

AGGREGATION OF RISK TYPES

Table 1 Aggregation of risk types

Bottom-Up Market Credit Operational Business Others Not If Applicable

Diversified Diversified

Risk drivers

X1 X2 X3 X4 X5 => X1+X2+X3 +X4+X5

F(X1,X2,X3,X4,X5)

Stress Y1 Y2 Y3 Y4 Y5 => Y1+Y2+Y3

+Y4+Y5 F(Y1,Y2,Y3,Y4,Y5)

Total Z1 Z2 Z3 Z4 Z5 => Z1+Z2+Z3

+Z4+Z5 B1 = F(Z1,Z2,Z3,Z4,Z5) ↓

METHODOLOGY

ICAAP AND WAY FORWARD

ICAAP presents opportunity to define a way forward strategy by introducing changes to the definition of risk appetite, risk tolerance and make Capital as an integral part of business Capital as an integral part of business Capital as an integral part of business Capital as an integral part of business planning.planning.planning.planning.

ICAAP allows for sound identification and quantification of all material risks and determine Economic Capital consistent with the institutions risk profile thus protecting institutions own funds in turn fostering financial stability.

ICAAP AND WAY FORWARD

Initially ICAAP was perceived to be mere regulatory compliance exercise – institutions now appreciate that they can leverage on Pillar 2 to strengthen and promote complete integration of risks, liquidity and capital management within business and strategic planning, with meaningful scenarios testing for capital budgeting.

Attribution of roles and responsibilities to different process owners / business units, fosters realization that the ICAAP process involves the whole structure of the organization and promotes co-operation and stimulates intelligent business but risk aware decisions.

SUMMARY SUMMARY SUMMARY SUMMARY

The transformation and evolution has aimed at recognizing :The transformation and evolution has aimed at recognizing :The transformation and evolution has aimed at recognizing :The transformation and evolution has aimed at recognizing :

Other risks Other risks Other risks Other risks that that that that

contribute contribute contribute contribute to capital to capital to capital to capital erosion,erosion,erosion,erosion,

The The The The distortions distortions distortions distortions in material in material in material in material risks that risks that risks that risks that

contributed contributed contributed contributed in banking in banking in banking in banking by financial by financial by financial by financial innovations, innovations, innovations, innovations,

Need to Need to Need to Need to enhance enhance enhance enhance

risk risk risk risk sensitivitysensitivitysensitivitysensitivity

Limited Limited Limited Limited attention attention attention attention given to given to given to given to

risk risk risk risk mitigation mitigation mitigation mitigation (hedging (hedging (hedging (hedging

etc)etc)etc)etc)

Need to give Need to give Need to give Need to give emphasis to emphasis to emphasis to emphasis to

risk risk risk risk management management management management

processes processes processes processes within bankswithin bankswithin bankswithin banks

Need to Need to Need to Need to establish establish establish establish

strong strong strong strong control and control and control and control and

risk risk risk risk management management management management

culture culture culture culture amongst the amongst the amongst the amongst the

Board of Board of Board of Board of Directors and Directors and Directors and Directors and

senior senior senior senior managementmanagementmanagementmanagement

Capture all Capture all Capture all Capture all new new new new

financial financial financial financial instrumentsinstrumentsinstrumentsinstruments

TANGIBLE BENEFITSTANGIBLE BENEFITSTANGIBLE BENEFITSTANGIBLE BENEFITS

If B II is implemented correctly and intelligently it will :If B II is implemented correctly and intelligently it will :If B II is implemented correctly and intelligently it will :If B II is implemented correctly and intelligently it will :

Reduce capital Requirements

Increase investment capital

Increase revenue

Cut down costs

Increase credit ratings

Improvements in risk measurements, controls and performance

Increase shareholder value

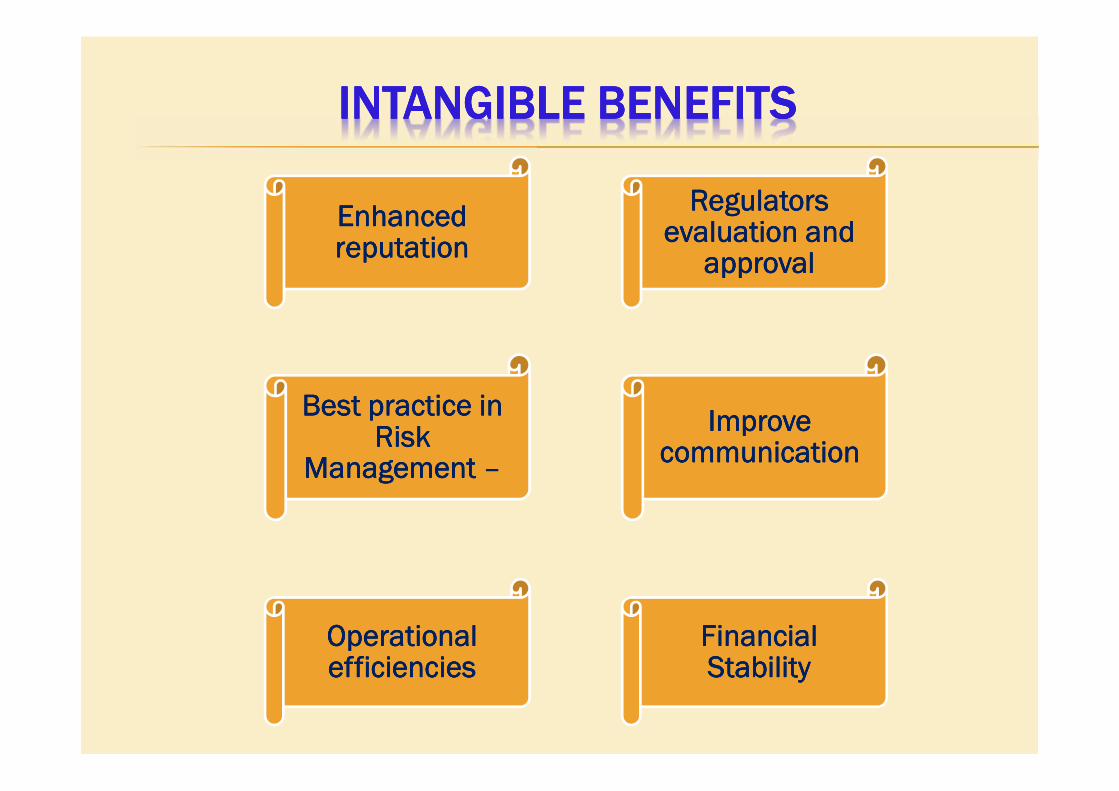

INTANGIBLEINTANGIBLEINTANGIBLEINTANGIBLE BENEFITSBENEFITSBENEFITSBENEFITS

Enhanced Enhanced Enhanced Enhanced reputationreputationreputationreputation

Regulators Regulators Regulators Regulators evaluation and evaluation and evaluation and evaluation and

approvalapprovalapprovalapproval

Best practice in Best practice in Best practice in Best practice in Risk Risk Risk Risk

Management Management Management Management ––––

Improve Improve Improve Improve communicationcommunicationcommunicationcommunication

Operational Operational Operational Operational efficienciesefficienciesefficienciesefficiencies

Financial Financial Financial Financial StabilityStabilityStabilityStability

CHALLENGESCHALLENGESCHALLENGESCHALLENGES

Lack of IT systems & Lack of IT systems & Lack of IT systems & Lack of IT systems & data collection data collection data collection data collection ––––

Process for data Process for data Process for data Process for data collection, collection, collection, collection,

determining the determining the determining the determining the quality of the data, quality of the data, quality of the data, quality of the data, storage storage storage storage –––– archiving archiving archiving archiving

etc.etc.etc.etc.

Uncertainties from Uncertainties from Uncertainties from Uncertainties from the Regulators with the Regulators with the Regulators with the Regulators with regard to guidelines.regard to guidelines.regard to guidelines.regard to guidelines.

Shortage of Basel Shortage of Basel Shortage of Basel Shortage of Basel and Risk and Risk and Risk and Risk

Management Management Management Management ExpertiseExpertiseExpertiseExpertise

Costs of Costs of Costs of Costs of implementationimplementationimplementationimplementation

Effective use of Risk Effective use of Risk Effective use of Risk Effective use of Risk reporting systems reporting systems reporting systems reporting systems

Active involvement of Active involvement of Active involvement of Active involvement of the BODthe BODthe BODthe BOD

Appropriate Appropriate Appropriate Appropriate documentation / documentation / documentation / documentation / policies and risk policies and risk policies and risk policies and risk

management management management management systems vissystems vissystems vissystems vis----àààà----vis vis vis vis one’s own Bank.one’s own Bank.one’s own Bank.one’s own Bank.

Lack of knowledge Lack of knowledge Lack of knowledge Lack of knowledge and expertise within and expertise within and expertise within and expertise within the entire industry.the entire industry.the entire industry.the entire industry.

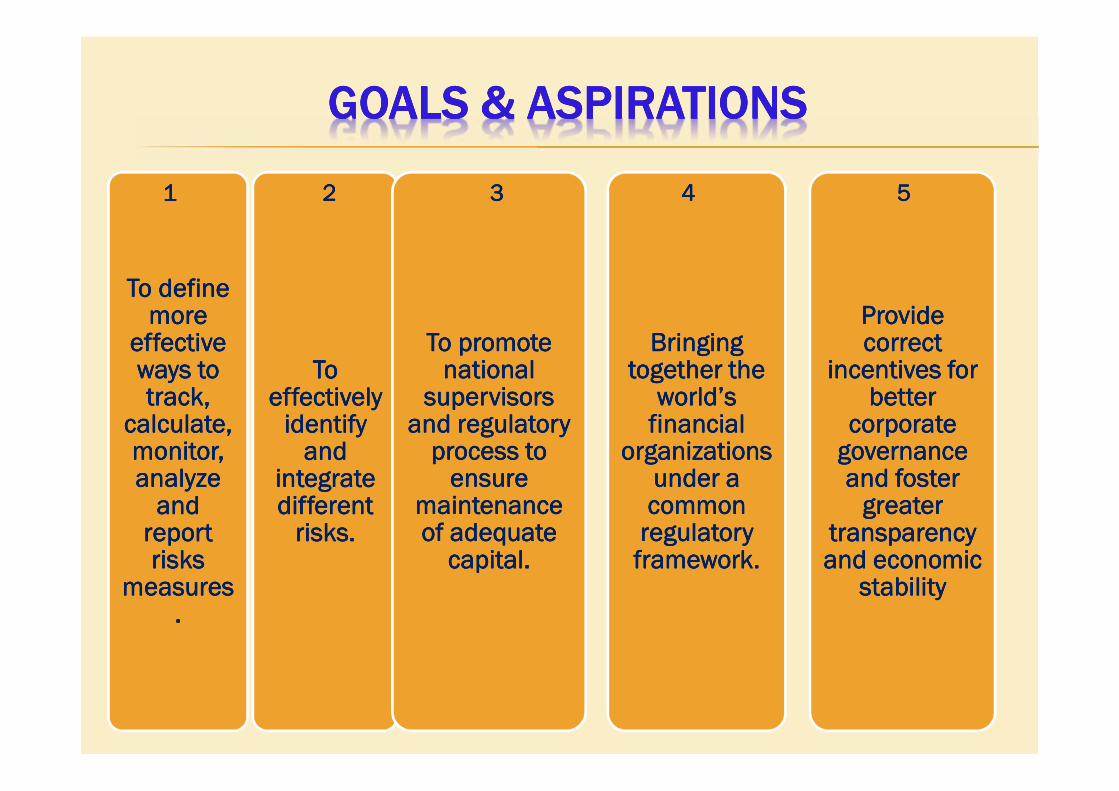

GOALS & ASPIRATIONSGOALS & ASPIRATIONSGOALS & ASPIRATIONSGOALS & ASPIRATIONS

To define To define To define To define more more more more

effective effective effective effective ways to ways to ways to ways to track, track, track, track,

calculate, calculate, calculate, calculate, monitor, monitor, monitor, monitor, analyze analyze analyze analyze

and and and and report report report report risks risks risks risks

measuresmeasuresmeasuresmeasures....

To To To To effectively effectively effectively effectively

identify identify identify identify and and and and

integrate integrate integrate integrate different different different different

risks.risks.risks.risks.

To promote To promote To promote To promote national national national national

supervisors supervisors supervisors supervisors and regulatory and regulatory and regulatory and regulatory

process to process to process to process to ensure ensure ensure ensure

maintenance maintenance maintenance maintenance of adequate of adequate of adequate of adequate

capital.capital.capital.capital.

Bringing Bringing Bringing Bringing together the together the together the together the

world’s world’s world’s world’s financial financial financial financial

organizations organizations organizations organizations under a under a under a under a common common common common

regulatory regulatory regulatory regulatory framework.framework.framework.framework.

Provide Provide Provide Provide correct correct correct correct

incentives for incentives for incentives for incentives for better better better better

corporate corporate corporate corporate governance governance governance governance and foster and foster and foster and foster

greater greater greater greater transparency transparency transparency transparency and economic and economic and economic and economic

stabilitystabilitystabilitystability

1111 3333 4444 55552222

GOALS & ASPIRATIONSGOALS & ASPIRATIONSGOALS & ASPIRATIONSGOALS & ASPIRATIONS

Improve trust Improve trust Improve trust Improve trust in the financial in the financial in the financial in the financial organizations organizations organizations organizations

by aligning by aligning by aligning by aligning capital capital capital capital

adequacy and adequacy and adequacy and adequacy and liquidity liquidity liquidity liquidity

assessment assessment assessment assessment more closely more closely more closely more closely

with the with the with the with the fundamental fundamental fundamental fundamental

risks.risks.risks.risks.

Bring in each Bring in each Bring in each Bring in each banks banks banks banks

experience and experience and experience and experience and instill best instill best instill best instill best

practice, with practice, with practice, with practice, with sophisticated sophisticated sophisticated sophisticated

and analytically and analytically and analytically and analytically driven risk driven risk driven risk driven risk

management management management management tools.tools.tools.tools.

Create Create Create Create awareness of awareness of awareness of awareness of

risk sensitivity, risk sensitivity, risk sensitivity, risk sensitivity, in different in different in different in different

jurisdictions, jurisdictions, jurisdictions, jurisdictions, different sizes different sizes different sizes different sizes

of Banks.of Banks.of Banks.of Banks.

Finally bring in Finally bring in Finally bring in Finally bring in financial financial financial financial

stability and stability and stability and stability and economically economically economically economically

safe and viable safe and viable safe and viable safe and viable environment.environment.environment.environment.

6666 8888 99997777

BASEL III - M E REGION OUTLOOK

Banking in this region is evolving and is advancing towards maturity. Regulatory change is constant and we are in the most progressive, nascent era.

In this phase, understanding and awareness is building that capital and liquidity are keys to any financial institution for its sustenance.

The Banking sector’s indicators shows the system is currentystable, is well capitalized with good asset quality and a relatively strong liquidity base to provide financing and spur economic activities.

BASEL III - M E REGION OUTLOOK

While the risk of financial contagion from Euro debt crisis is a key concern, the UAE Banking sector, although may have limited exposure to the troubled countries, maintains adequate buffers to absorb losses.

Banks are standing on solid financial ground and are not concerned of meeting new requirements under Basel III, with the regulator encouraging own stress tests to ensure industry remains resilient.

Having said that, this is an emerging economy and the outlook is uneven as the external environment continues to be threatened by the Eurozone sovereign debt crisis and a fragile US recovery.

QUESTIONS?QUESTIONS?QUESTIONS?QUESTIONS?

THANKTHANKTHANKTHANK YOU!YOU!YOU!YOU!