Global Boxboard Market ReviewSailing in a World of Volatility and Uncertainty

Alejandro MataSenior Economist, European Forest Products

RISI Asian Conference

May 2018

© Copyright 2018 RISI, Inc. | Proprietary Information

2

• Bachelor’s degree in Engineering, MBA degree earned in 2007

• Worked in business and market intelligence functions for one of Europe’s leading paper producers

• Has been analyzing and forecasting the industry since 2009

• Author of the Paper Trader Europe, Paper Packaging Monitor Europe, the European Graphic 5-Year and 15-Year Forecasts and the European Paper Packaging 5-Year and 15-Year Forecasts

Senior Economist, European Forest Products

Alejandro Mata

© Copyright 2018 RISI, Inc. | Proprietary Information

3© Copyright 2018 RISI, Inc. | Proprietary Information

Economic Tailwind Boosting Demand

4

…But What If the Wind Changes?© Copyright 2018 RISI, Inc. | Proprietary Information

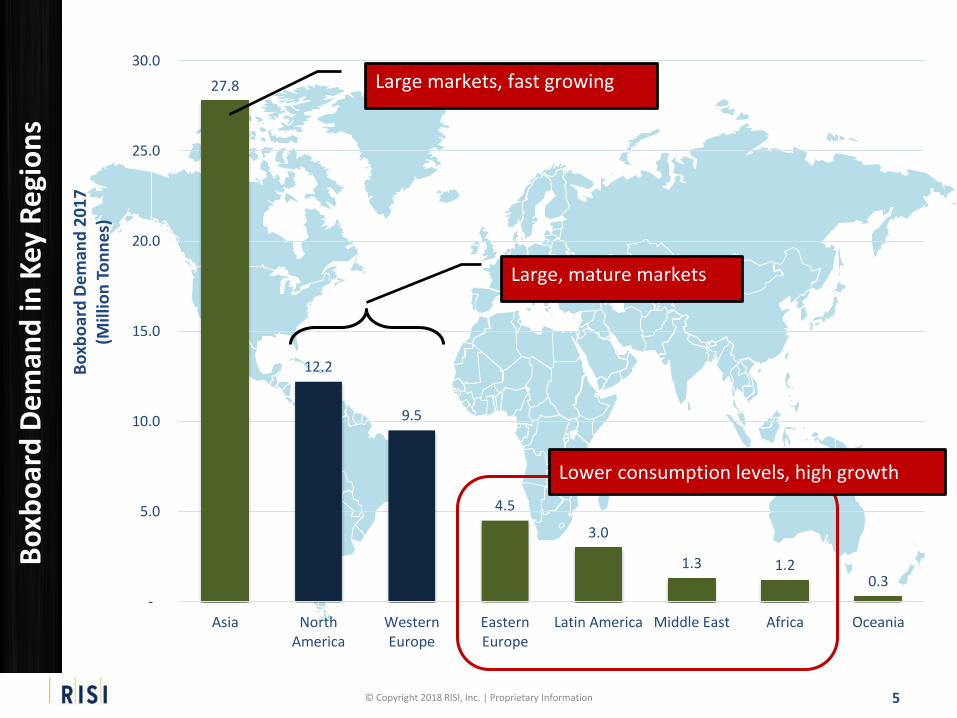

27.8

12.2

9.5

4.5

3.0

1.3 1.20.3

-

5.0

10.0

15.0

20.0

25.0

30.0

Asia NorthAmerica

WesternEurope

EasternEurope

Latin America Middle East Africa Oceania

Bo

xbo

ard

De

man

d 2

01

7(M

illio

n T

on

ne

s)Large markets, fast growing

Large, mature markets

Lower consumption levels, high growth

Bo

xbo

ard

De

man

d in

Key

Re

gio

ns

5© Copyright 2018 RISI, Inc. | Proprietary Information

6© Copyright 2018 RISI, Inc. | Proprietary Information

-4%

-2%

0%

2%

4%

6%

8%

10%

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

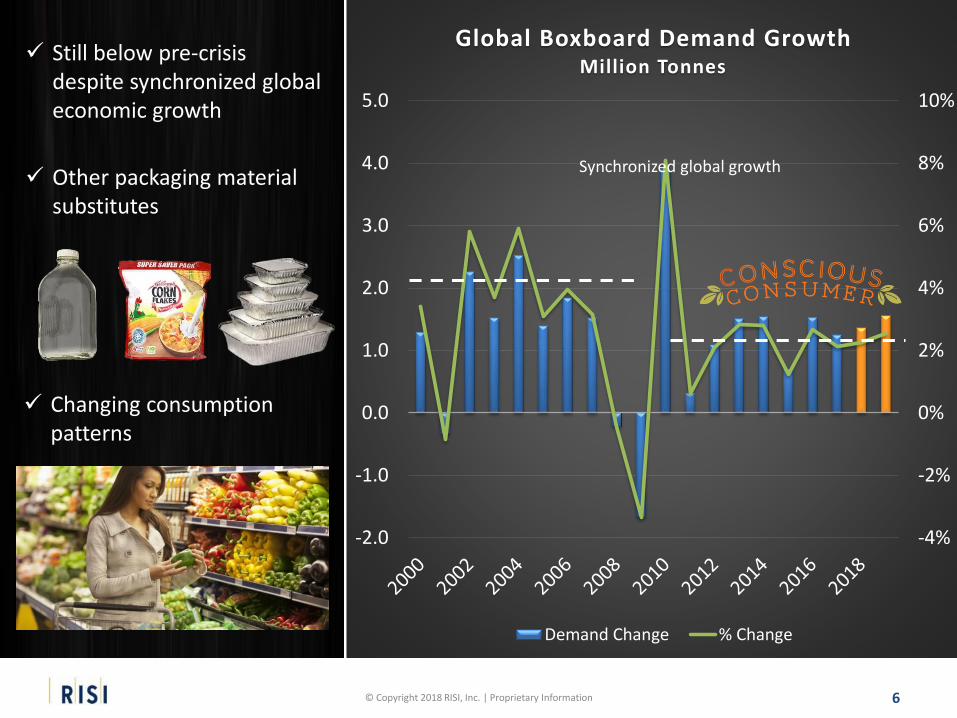

Global Boxboard Demand GrowthMillion Tonnes

Demand Change % Change

Synchronized global growth

Still below pre-crisis despite synchronized global economic growth

Other packaging material substitutes

Changing consumption patterns

7© Copyright 2018 RISI, Inc. | Proprietary Information

8© Copyright 2018 RISI, Inc. | Proprietary Information

9© Copyright 2018 RISI, Inc. | Proprietary Information

Plastics Substitution

10© Copyright 2018 RISI, Inc. | Proprietary Information

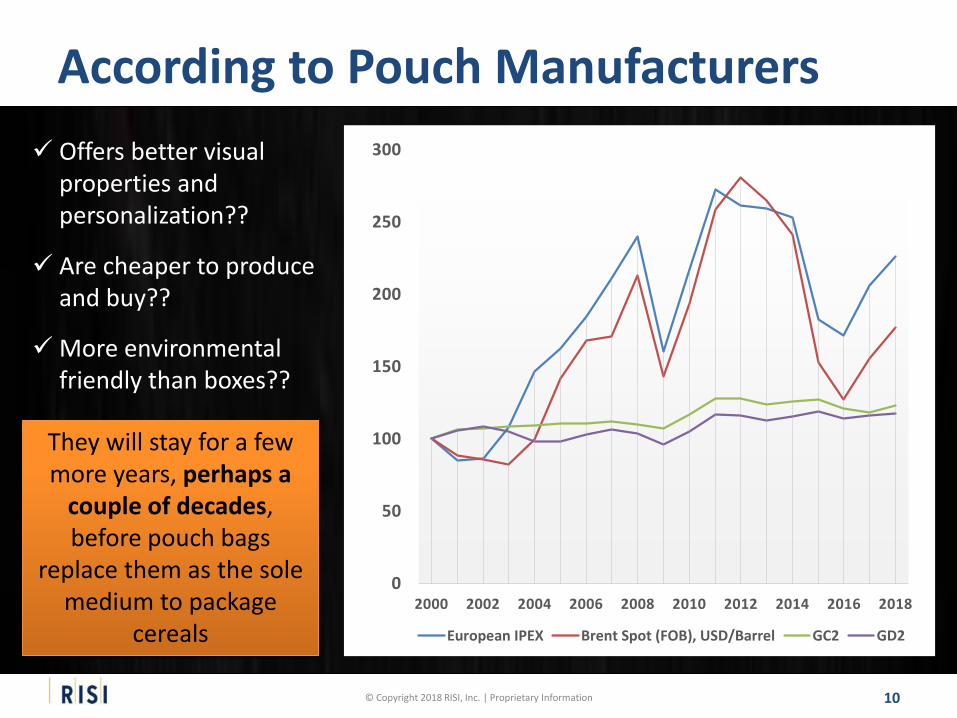

Offers better visual properties and personalization??

Are cheaper to produce and buy??

More environmental friendly than boxes??

They will stay for a few more years, perhaps a

couple of decades, before pouch bags

replace them as the sole medium to package

cereals

According to Pouch Manufacturers

0

50

100

150

200

250

300

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

European IPEX Brent Spot (FOB), USD/Barrel GC2 GD2

11© Copyright 2018 RISI, Inc. | Proprietary Information

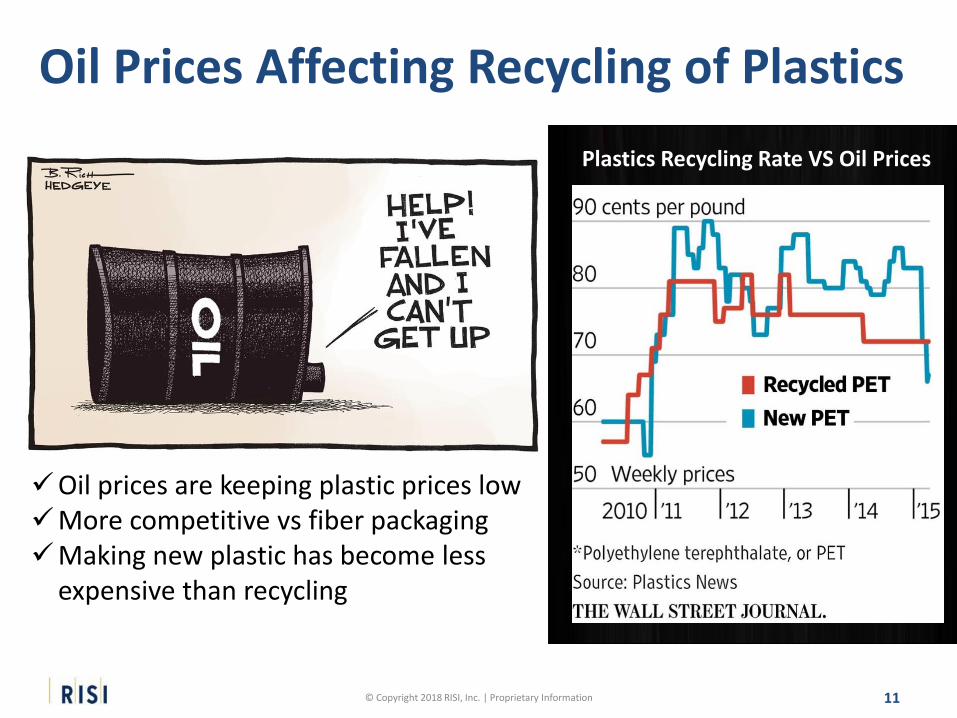

Oil prices are keeping plastic prices lowMore competitive vs fiber packagingMaking new plastic has become less

expensive than recycling

Oil Prices Affecting Recycling of Plastics

Plastics Recycling Rate VS Oil Prices

12© Copyright 2018 RISI, Inc. | Proprietary Information

Map of countries banning plastics

Plastic Bag Ban

BannedUsage FeeBan Failed

13© Copyright 2018 RISI, Inc. | Proprietary Information

14© Copyright 2018 RISI, Inc. | Proprietary Information

78%

80%

82%

84%

86%

88%

90%

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

Op

era

tin

g R

ate

Gro

wth

in

Mil

lio

n T

on

ne

s

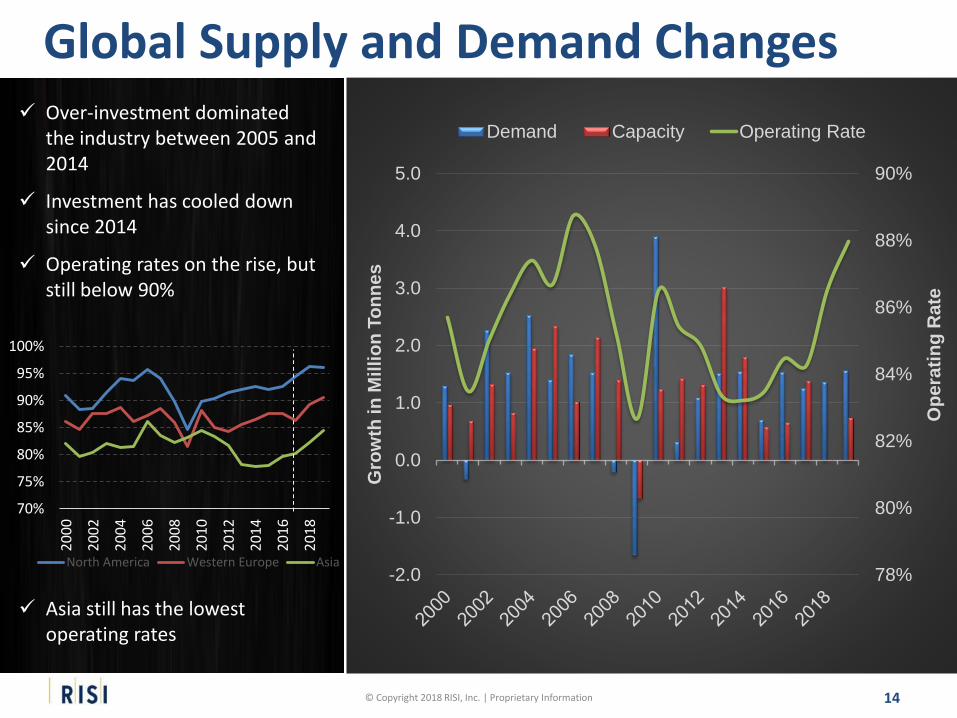

Demand Capacity Operating Rate Over-investment dominated

the industry between 2005 and 2014

Investment has cooled down since 2014

Operating rates on the rise, but still below 90%

70%

75%

80%

85%

90%

95%

100%

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

20

16

20

18

North America Western Europe Asia

Asia still has the lowest operating rates

Global Supply and Demand Changes

15© Copyright 2018 RISI, Inc. | Proprietary Information

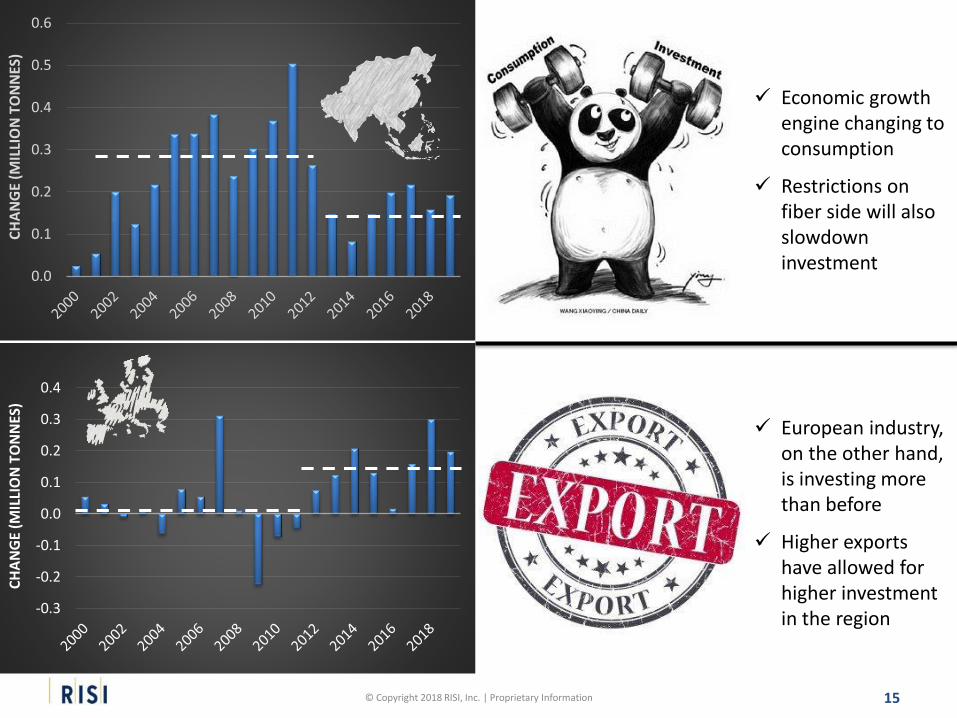

0.0

0.1

0.2

0.3

0.4

0.5

0.6C

HA

NG

E (M

ILLI

ON

TO

NN

ES)

-0.3

-0.2

-0.1

0.0

0.1

0.2

0.3

0.4

CH

AN

GE

(MIL

LIO

N T

ON

NES

)

Economic growth engine changing to consumption

Restrictions on fiber side will also slowdown investment

European industry, on the other hand, is investing more than before

Higher exports have allowed for higher investment in the region

16© Copyright 2018 RISI, Inc. | Proprietary Information

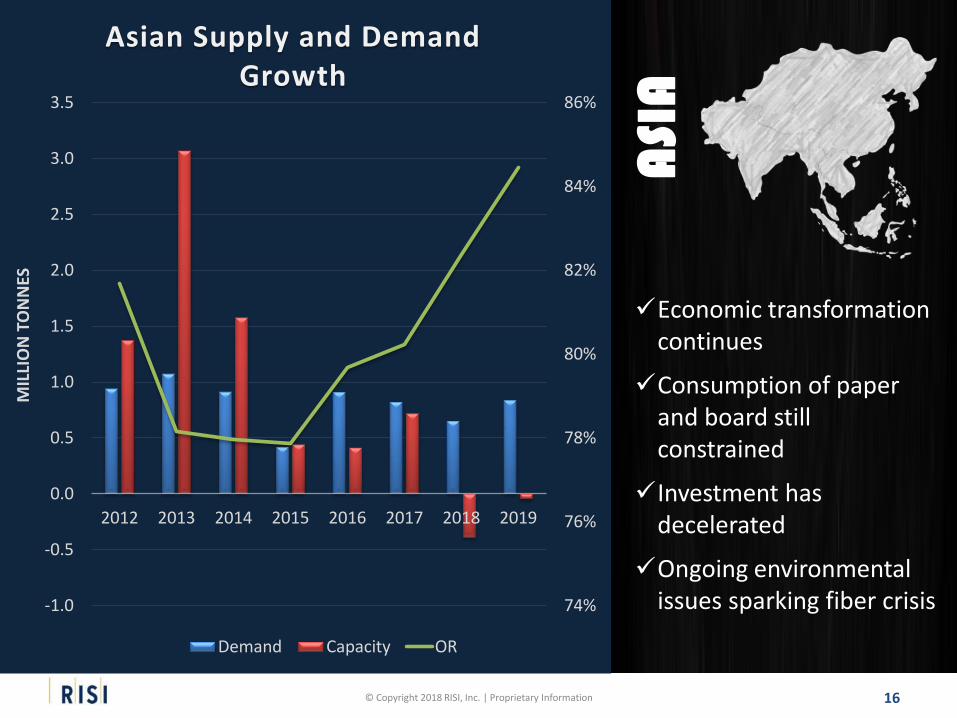

74%

76%

78%

80%

82%

84%

86%

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2012 2013 2014 2015 2016 2017 2018 2019

MIL

LIO

N T

ON

NES

Asian Supply and Demand Growth

Demand Capacity OR

Economic transformation continues

Consumption of paper and board still constrained

Investment has decelerated

Ongoing environmental issues sparking fiber crisis

ASI

A

17© Copyright 2018 RISI, Inc. | Proprietary Information

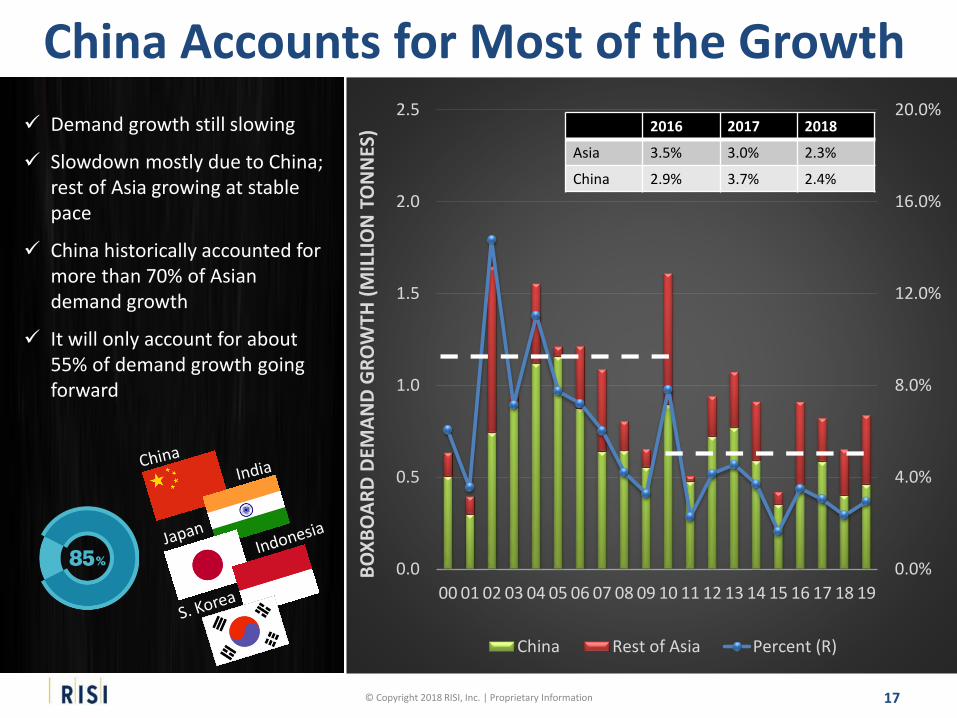

0.0%

4.0%

8.0%

12.0%

16.0%

20.0%

0.0

0.5

1.0

1.5

2.0

2.5

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19

BO

XB

OA

RD

DEM

AN

D G

RO

WTH

(M

ILLI

ON

TO

NN

ES)

China Rest of Asia Percent (R)

Demand growth still slowing

Slowdown mostly due to China; rest of Asia growing at stable pace

China historically accounted for more than 70% of Asian demand growth

It will only account for about 55% of demand growth going forward

2016 2017 2018

Asia 3.5% 3.0% 2.3%

China 2.9% 3.7% 2.4%

China Accounts for Most of the Growth

18© Copyright 2018 RISI, Inc. | Proprietary Information

Remember This?

China is the largest buyer of PfR in the World

19© Copyright 2018 RISI, Inc. | Proprietary Information

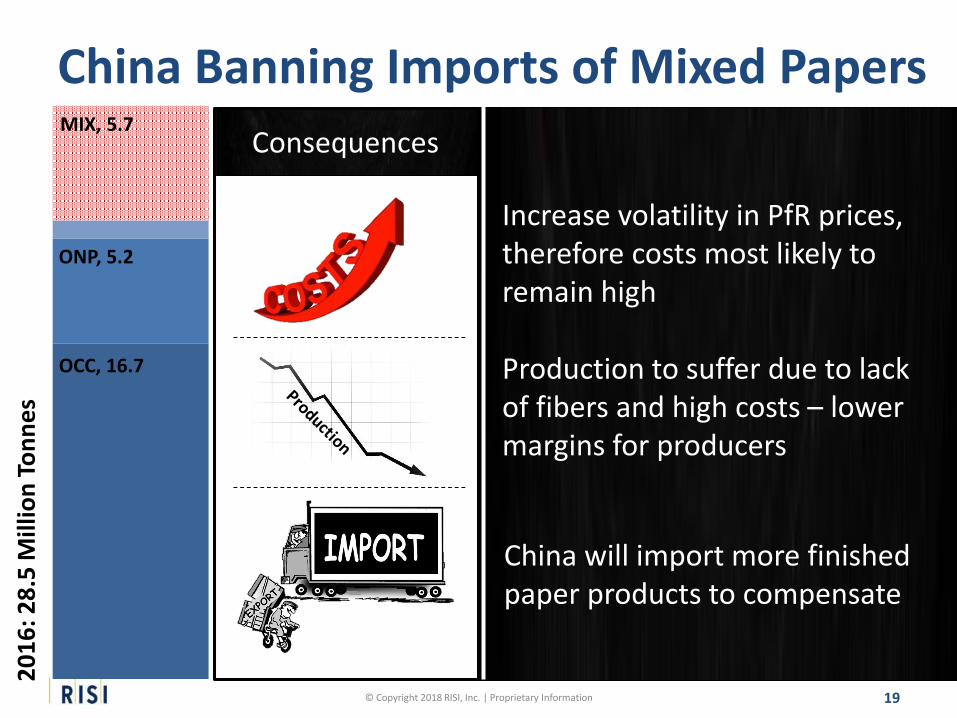

China Banning Imports of Mixed Papers2

01

6: 2

8.5

Mill

ion

To

nn

es

MIX, 5.7

ONP, 5.2

OCC, 16.7

Increase volatility in PfR prices, therefore costs most likely to remain high

Consequences

Production to suffer due to lack of fibers and high costs – lower margins for producers

China will import more finished paper products to compensate

20© Copyright 2018 RISI, Inc. | Proprietary Information

China Banning Imports of Mixed Papers

How to compensate for the missing fiber?

Increase domestic collection?

More market pulp?

Imports of finished paper products?

Diverting fiber away from low margin paper & board grades (graphics) ?

21© Copyright 2018 RISI, Inc. | Proprietary Information

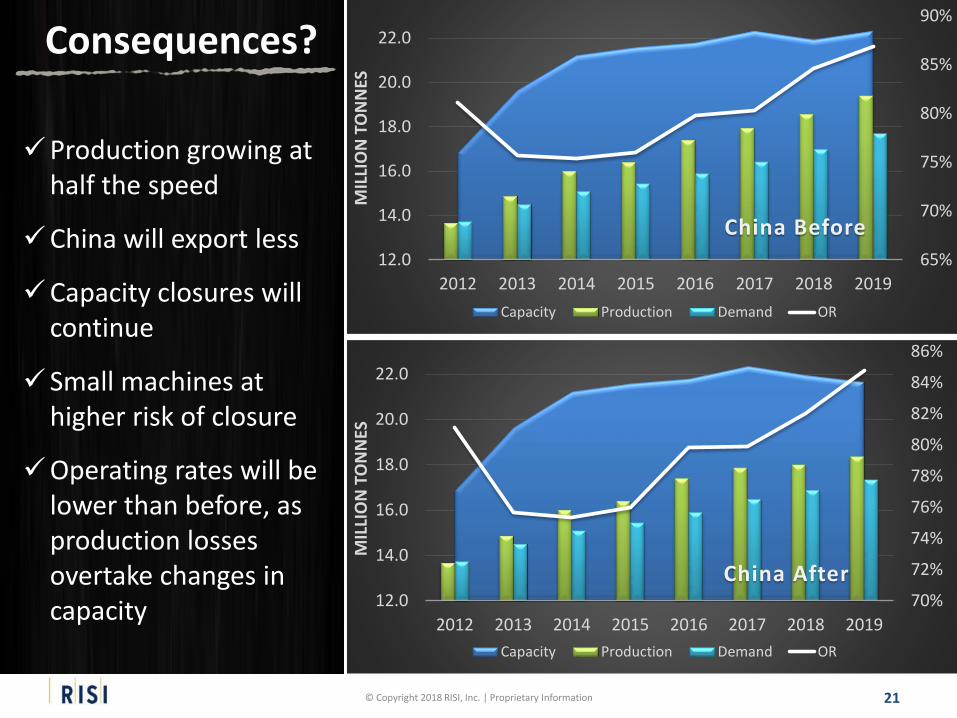

Consequences?

65%

70%

75%

80%

85%

90%

12.0

14.0

16.0

18.0

20.0

22.0

2012 2013 2014 2015 2016 2017 2018 2019

MIL

LIO

N T

ON

NES

China Before

Capacity Production Demand OR

70%

72%

74%

76%

78%

80%

82%

84%

86%

12.0

14.0

16.0

18.0

20.0

22.0

2012 2013 2014 2015 2016 2017 2018 2019

MIL

LIO

N T

ON

NES

China After

Capacity Production Demand OR

Production growing at half the speed

China will export less

Capacity closures will continue

Small machines at higher risk of closure

Operating rates will be lower than before, as production losses overtake changes in capacity

22© Copyright 2018 RISI, Inc. | Proprietary Information

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

00 02 04 06 08 10 12 14 16 18

BO

XB

OA

RD

NET

IMP

OR

TS (

MIL

LIO

N T

ON

NES

)

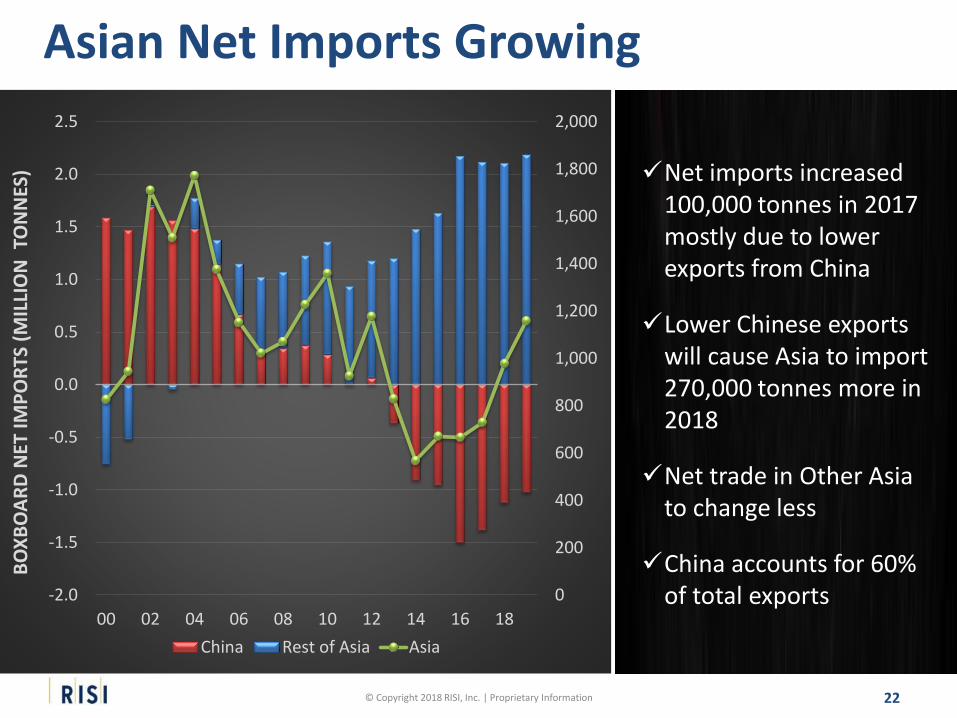

China Rest of Asia Asia

Net imports increased 100,000 tonnes in 2017 mostly due to lower exports from China

Lower Chinese exports will cause Asia to import 270,000 tonnes more in 2018

Net trade in Other Asia to change less

China accounts for 60% of total exports

Asian Net Imports Growing

23© Copyright 2018 RISI, Inc. | Proprietary Information

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

0.0

2.0

4.0

6.0

8.0

10.0

12.0

2012 2013 2014 2015 2016 2017 2018 2019

Chinese Boxboard Demand Million Tonnes

Virgin Recycled % Virgin % Recycled

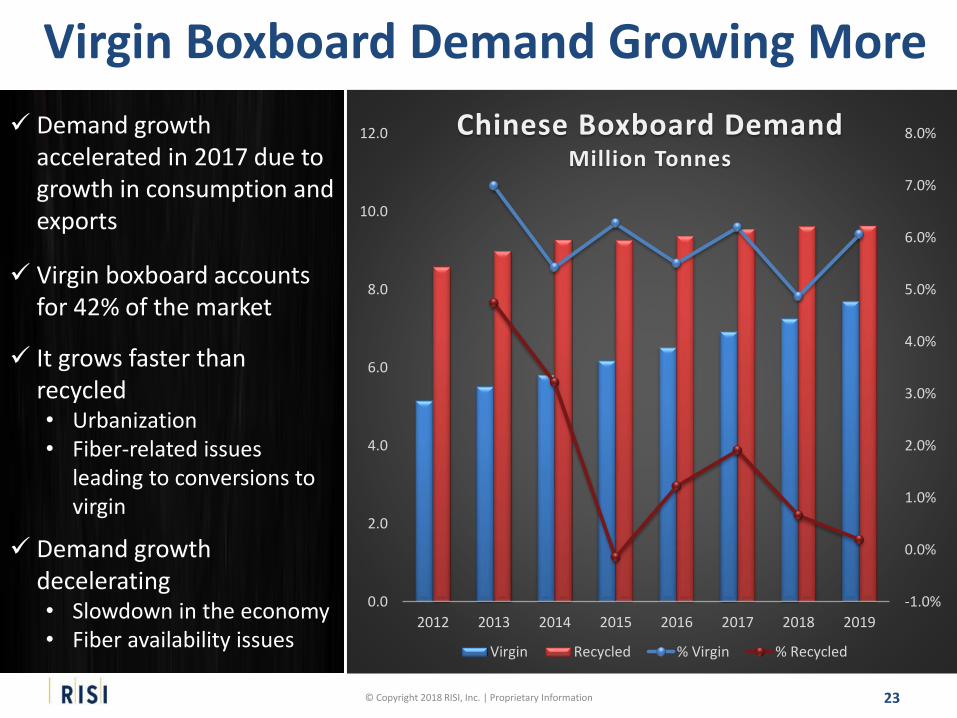

Demand growth accelerated in 2017 due to growth in consumption and exports

Virgin boxboard accounts for 42% of the market

It grows faster than recycled • Urbanization • Fiber-related issues

leading to conversions to virgin

Demand growth decelerating• Slowdown in the economy• Fiber availability issues

Virgin Boxboard Demand Growing More

24© Copyright 2018 RISI, Inc. | Proprietary Information

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

2012 2013 2014 2015 2016 2017 2018 2019

Chinese Boxboard CapacityMillion Tonnes

Virgin Recycled

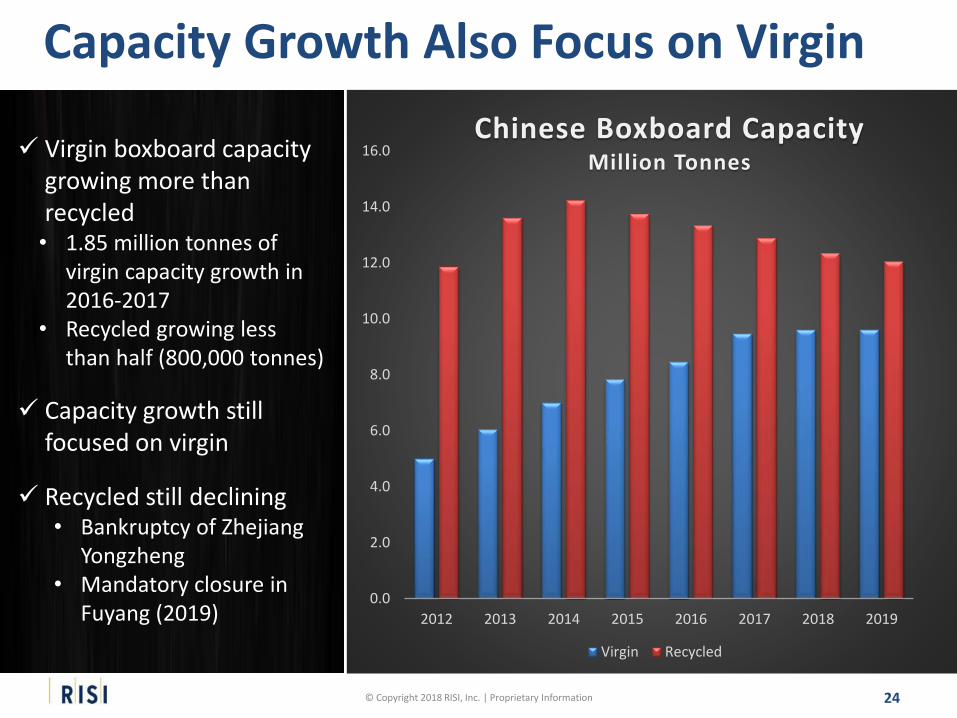

Virgin boxboard capacity growing more than recycled• 1.85 million tonnes of

virgin capacity growth in 2016-2017

• Recycled growing less than half (800,000 tonnes)

Capacity growth still focused on virgin

Recycled still declining• Bankruptcy of Zhejiang

Yongzheng• Mandatory closure in

Fuyang (2019)

Capacity Growth Also Focus on Virgin

25© Copyright 2018 RISI, Inc. | Proprietary Information

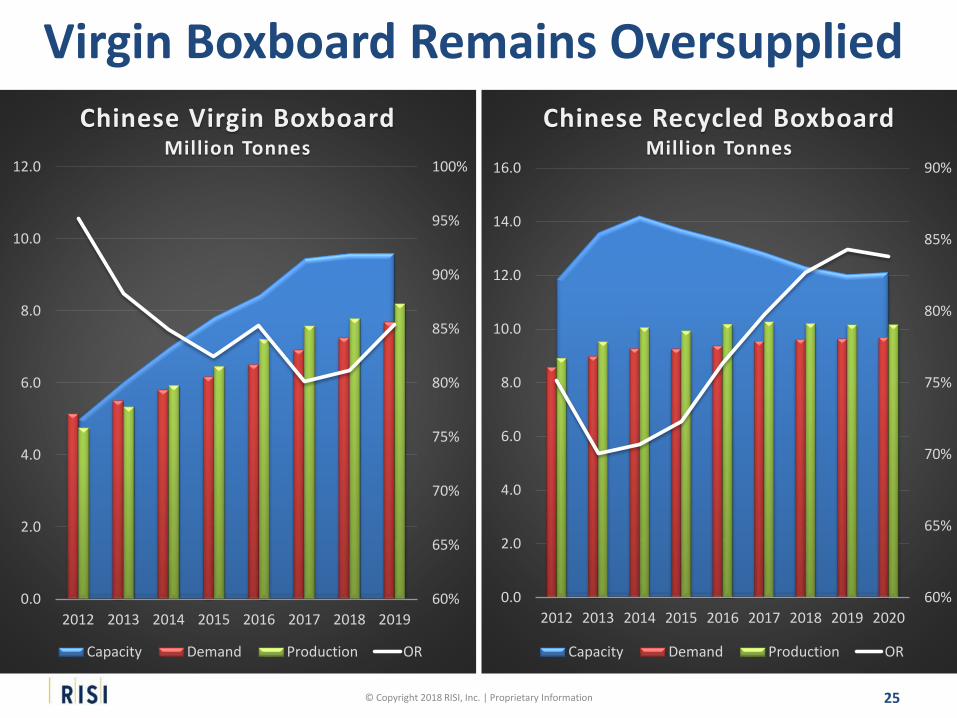

60%

65%

70%

75%

80%

85%

90%

95%

100%

0.0

2.0

4.0

6.0

8.0

10.0

12.0

2012 2013 2014 2015 2016 2017 2018 2019

Chinese Virgin BoxboardMillion Tonnes

Capacity Demand Production OR

60%

65%

70%

75%

80%

85%

90%

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

2012 2013 2014 2015 2016 2017 2018 2019 2020

Chinese Recycled BoxboardMillion Tonnes

Capacity Demand Production OR

Virgin Boxboard Remains Oversupplied

26© Copyright 2018 RISI, Inc. | Proprietary Information

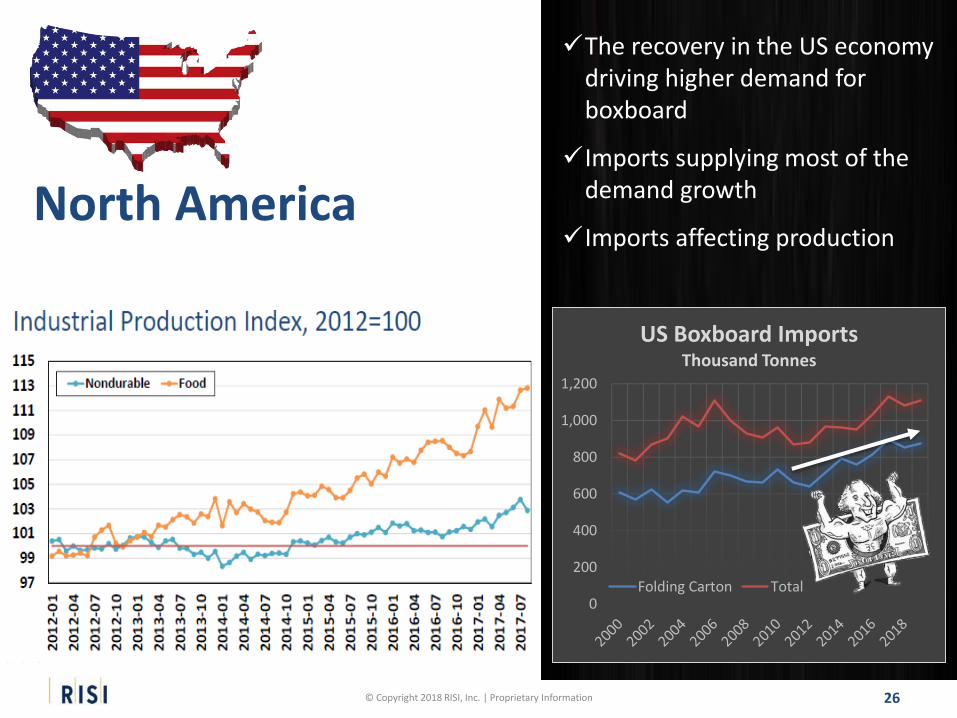

North America

The recovery in the US economy driving higher demand for boxboard

Imports supplying most of the demand growth

Imports affecting production

0

200

400

600

800

1,000

1,200

US Boxboard Imports Thousand Tonnes

Folding Carton Total

27© Copyright 2018 RISI, Inc. | Proprietary Information

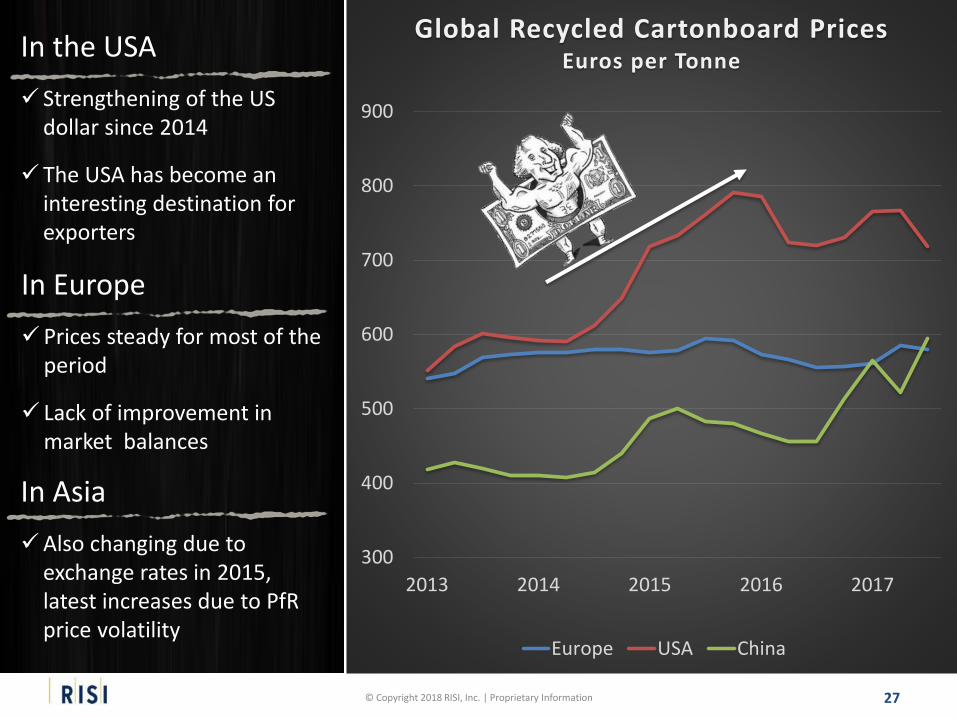

300

400

500

600

700

800

900

2013 2014 2015 2016 2017

Global Recycled Cartonboard PricesEuros per Tonne

Europe USA China

In the USA

Strengthening of the US dollar since 2014

The USA has become an interesting destination for exporters

In Europe

Prices steady for most of the period

Lack of improvement in market balances

In Asia

Also changing due to exchange rates in 2015, latest increases due to PfRprice volatility

28© Copyright 2018 RISI, Inc. | Proprietary Information

Vir

gin

Mar

kets

Do

ing

Bet

ter

Ch

alle

ngi

ng

Co

nd

itio

ns

in t

he

CR

B M

arke

t Demand not strong enough due to Change in people’s buying behavior

(fewer purchases of processed food) Fiercer threat from plastics

Imports rising rapidly Most of the imports from Europe

and Asia fall within recycled cartonboard in the USA

Capacity fell nearly 11% in 2017

Demand doing better (growth in liquid packaging board, cupstock)

Producers benefiting from food service market (cups, takeout containers)

Imports not impacting virgin boxboard markets much

Capacity rising slowly

Virgin Market Is Doing Better

29© Copyright 2018 RISI, Inc. | Proprietary Information

86.0%

87.0%

88.0%

89.0%

90.0%

91.0%

92.0%

93.0%

-300

-200

-100

0

100

200

300

400

500

600

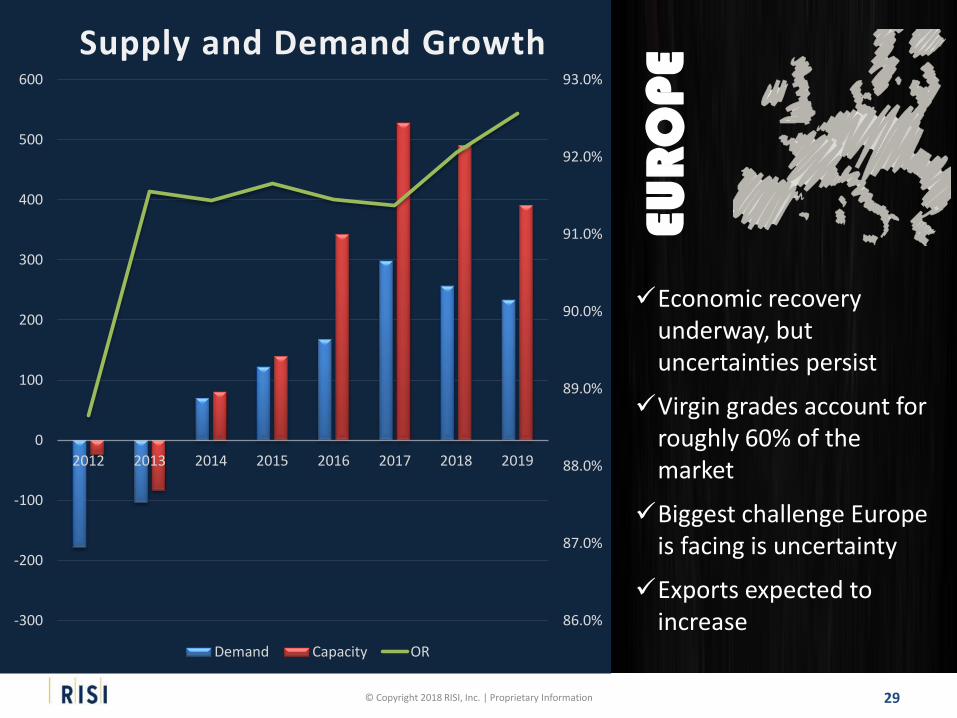

2012 2013 2014 2015 2016 2017 2018 2019

Supply and Demand Growth

Demand Capacity OR

Economic recovery underway, but uncertainties persist

Virgin grades account for roughly 60% of the market

Biggest challenge Europe is facing is uncertainty

Exports expected to increase

EUR

OPE

30© Copyright 2018 RISI, Inc. | Proprietary Information

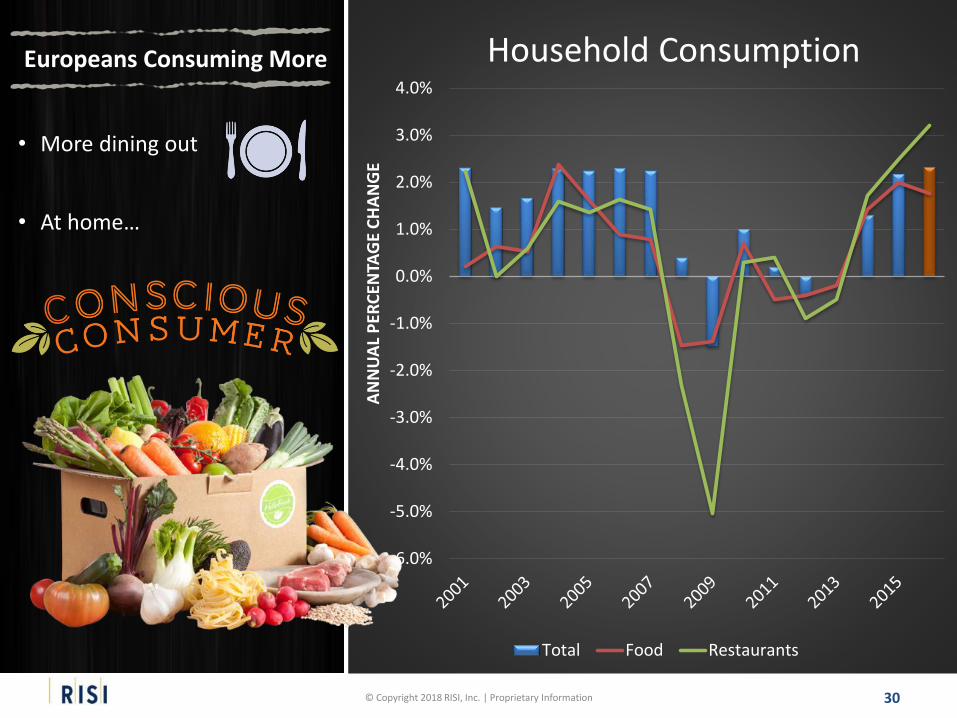

• More dining out

Europeans Consuming More

• At home…

-6.0%

-5.0%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

AN

NU

AL

PER

CEN

TAG

E C

HA

NG

E

Total Food Restaurants

Household Consumption

31© Copyright 2018 RISI, Inc. | Proprietary Information

-50

-40

-30

-20

-10

0

10

20

30

40

50

Mar

-08

No

v-0

8

Jul-

09

Mar

-10

No

v-1

0

Jul-

11

Mar

-12

No

v-1

2

Jul-

13

Mar

-14

No

v-1

4

Jul-

15

Mar

-16

No

v-1

6

Jul-

17

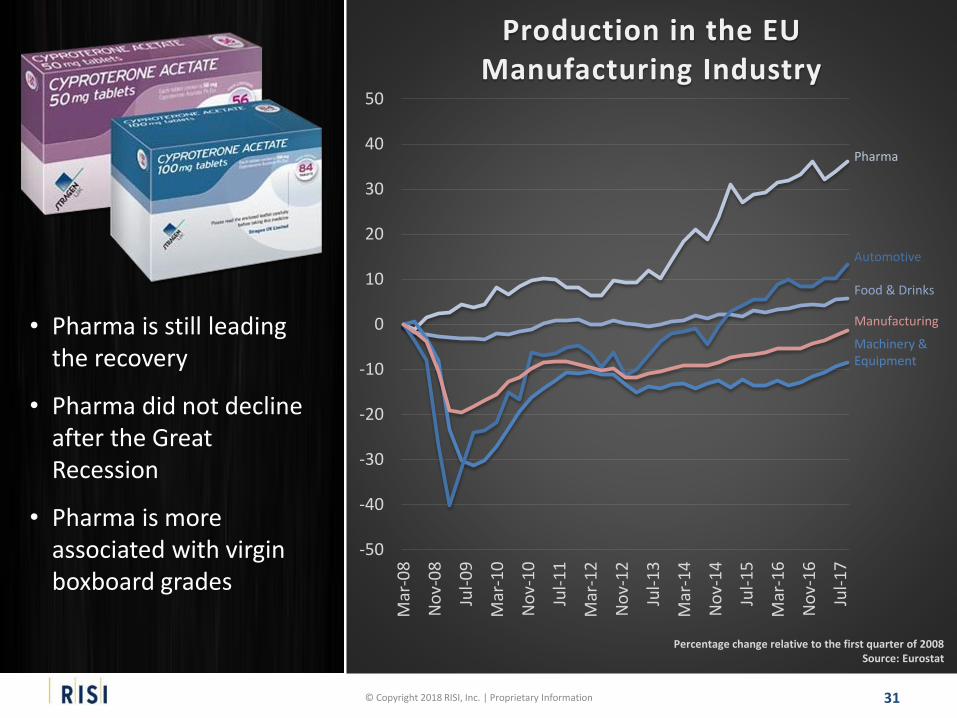

Production in the EU Manufacturing Industry

• Pharma is still leading the recovery

• Pharma did not decline after the Great Recession

• Pharma is more associated with virgin boxboard grades

Pharma

Automotive

Food & Drinks

Manufacturing

Machinery & Equipment

Percentage change relative to the first quarter of 2008Source: Eurostat

32© Copyright 2018 RISI, Inc. | Proprietary Information

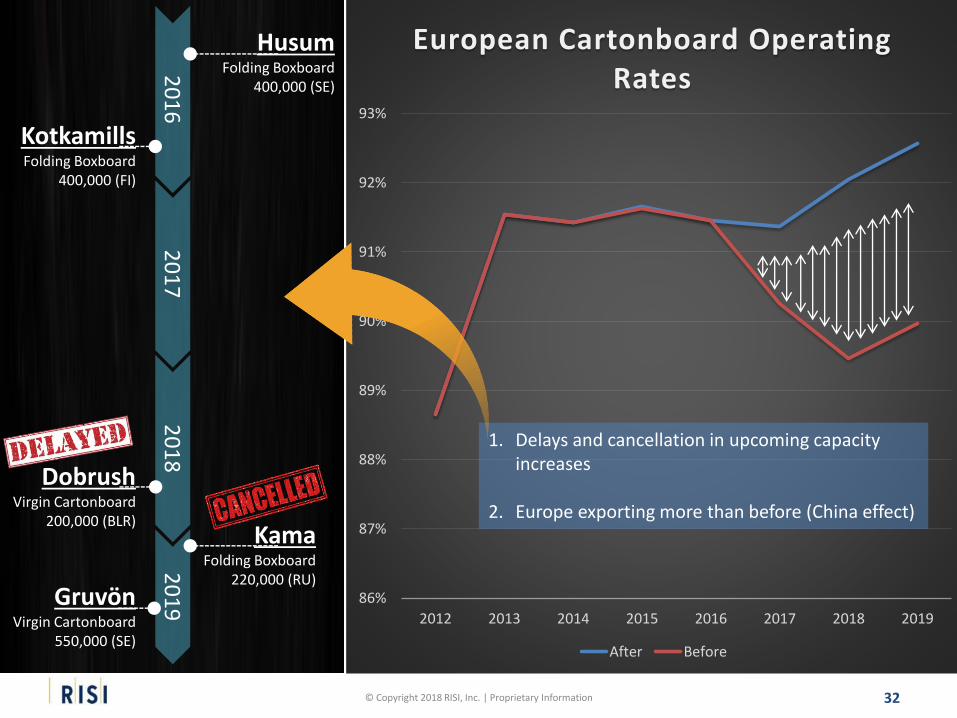

86%

87%

88%

89%

90%

91%

92%

93%

2012 2013 2014 2015 2016 2017 2018 2019

European Cartonboard Operating Rates

After Before

1. Delays and cancellation in upcoming capacity increases

2. Europe exporting more than before (China effect)

20

16

20

17

20

18

20

19

KotkamillsFolding Boxboard

400,000 (FI)

HusumFolding Boxboard

400,000 (SE)

DobrushVirgin Cartonboard

200,000 (BLR)Kama

Folding Boxboard220,000 (RU)

GruvönVirgin Cartonboard

550,000 (SE)

33© Copyright 2018 RISI, Inc. | Proprietary Information

600

650

700

750

800

850

900

950

1,000

1,050

1,100

2013 2014 2015 2016 2017

Virgin CartonboardEuros per Tonne

Europe USA China

Strengthening of the USD

Higher market pulp prices

350

400

450

500

550

-

2

4

6

8

10

12

14

16

Latin America N. America Europe Asia

Mill

ion

To

nn

es

Europe exporting more to the United States

Exporting to Asia has become more interesting due to the increase in Asian prices in 2017

Europe remains one of the lowest-cost regions producing virgin boxboard

Asian Prices Rose the Most in 2017

34© Copyright 2018 RISI, Inc. | Proprietary Information

Questions?

35

European Paper Packaging 5-Year and 15-Year Forecasts

www.risi.com/forecasts

Paper Packaging Monitor Europe

www.risi.com/ppme

Thank you!For more information:

© Copyright 2018 RISI, Inc. | Proprietary Information