© 2015 IHS. ALL RIGHTS RESERVED.

GLOBAL CHEMICAL

INDUSTRY UPDATE

Chris Wheeler, Principal Analyst- Olefins

IHS Chemical

Presented at the Houston Business Roundtable

January 20, 2016

© 2015 IHS. ALL RIGHTS RESERVED.

IHS – Who we are and what we do

2

Agriculture

Electronics &

Telecom

Government

Metals &

Mining Healthcare

Financial

Military &

Security

Chemicals

Automotive

Energy

Coal

Transportation

Shipping

Aerospace &

Defense

Construction

Power &

Utilities

Energy

Oil & Gas

Consumer

& Retail

© 2015 IHS. ALL RIGHTS RESERVED.

IHS Chemical – Our portfolio

3

Chemical Insights

Aromatics & Fibers

Olefins & Derivatives

Chlor-Alkali & Vinyls

Plastics & Polymers

Syngas Chemicals

Specialty Chemicals

Special Studies

Technology & Analytics

Process Economics

Cost Curve Analytics

Capital Cost Services

Scenarios

Special Studies

Business Information &

Same-Day Analysis

Chemical Week

Chemical Company Analysis

Regional or Country Analysis

Directory of Chemicals Producers

Member Events

Consulting & Advisory Services

Strategy

Commercial Analysis

Transaction

Legal Services

Technology

Renewables

Specialties

Training

© 2015 IHS. ALL RIGHTS RESERVED.

The petrochemical value chain is extensive

4

Presentation Name / Month 2015

Oil, Gas

Production

Hydrocarbon

Feed

Monomer/Base

Chemicals

Resins Derivatives &

Intermediates

Converters: Pellets to bags,

film, bottles or fiber Manufactured

Goods

Retail Consumers

© 2015 IHS. ALL RIGHTS RESERVED.

Key Issues Being

Discussed in the

Global Chemical

Industry

Crude Oil Price Outlook

• V-shape / U-shape / L-shape recovery

Demand Growth & The Economy

• Low Crude as a demand stimulus

US NGL Supply

• Ethane & Propane availability

Need for infrastructure investment

to support expanding regional trade

5

CEO Roundtable Discussions at

AFPM, APIC, CPCIC, EPCA

© 2015 IHS. ALL RIGHTS RESERVED.

Key Issues Being

Discussed in the

Global Chemical

Industry

Non-conventional & On-Purpose

Production Technologies

China, China, China

• Shifting demand growth / slowing

economy / currency / stock market

• Coal-to-Chems / On-purpose / and

Conventional Investments

• Private Company Market Share

• Adoption of Responsible Care Charter

Lifting of Iran Sanctions Impact

“Sustainability”, GHG Emissions,

Carbon Tax, Bio-Based Chemicals

6

CEO Roundtable Discussions at

AFPM, APIC, CPCIC, EPCA

© 2015 IHS. ALL RIGHTS RESERVED.

When Energy Markets Move Chemical

Markets Respond • Rapid decline in crude oil pricing

causes supply-chains to “pause” as

buyers anticipate lower prices.

• Lower production costs combined with

a pause in demand, can result in

sudden price declines, which can

serve to stimulate demand:

Higher GDP growth; lower use of

recycle plastics; stimulate

substitution

• Falling prices / lower margins force re-

assessment of capital spending

projects slowing additions creating

a pause/reversal of CAPEX inflation.

• Combination of these impacts can

create tight markets in the future

© 2015 IHS, Inc. No portion of this presentation may be reproduced, reused, or

otherwise distributed in any form without prior written consent.

© 2015 IHS. ALL RIGHTS RESERVED.

After Falling From the Cliff, Crude Prices Continue

Search of Bottom

Crude Oil Price Outlook to 2017

0

20

40

60

80

100

120

140

Brent - WTI

Brent FOB

Dubai FOB

WTI Cushing

Assumptions

Weak pricing will continue given

little decrease in US and OPEC

production levels

Demand growth is not sufficient

to absorb crude supply on offer

before 2H 2016

Strong US crude and product

inventories, lift of export ban

exacerbate downward pressure

Price forecast risks

Downside: Strong US production

continues amid prospects of price war

with return of Iranian production to

unsanctioned trading.

Upside: Complicated geopolitical

situation initiates price rally.

Unexpected increase in demand.

January 2016

© 2015 IHS. ALL RIGHTS RESERVED.

Global Crude Oil Inventories Are High,

and Are Creeping Higher

January 2016

Crude Oil Inventory

250

300

350

400

450

500

550

Jan Apr Jul Oct Jan Apr Jul Oct Jan

Mil

lio

n B

arr

els

Five-Year Range Five-Year Average Last 2 Years

Recent US Gasoline and Diesel stocks

are Close to 5 year High Levels

2014 2015

Seasonal drop

in US refinery

operating rates

Global crude inventory exceeded 60 days

of global supply (>5500 Million Barrels)

Source: Energy Information Administration (EIA)

China has been adding storage capacity

and increasing stored crude volume

© 2015 IHS. ALL RIGHTS RESERVED.

Demand Can Be Stimulated By Macro-economic

And Substitution Effects • Basic chemicals and

derivatives are the

fundamental building blocks

for many durable and non-

durable consumer goods.

• Global economic growth

drives the demand growth for

basic chemicals

• Low energy prices stimulate

economic growth; this will

translate into accelerated

growth for basic chemicals

• Lower relative prices spur

growth where chemicals can

substitute against other

materials

© 2015 IHS. ALL RIGHTS RESERVED.

Accelerated Demand Growth Can Drive Global

Utilization Rates Higher For Most Segments

0

2

4

6

8

10

12

0

2

4

6

8

10

12

Olefins Aromatics ECU Methanol Plastics BaseChemicals &

Plastics

Capacity IHS Base

Low Elasticity, Low GDP

High Elasticity, High GDP

Demand or Capacity Growth, %

• With the exception of methanol,

expected improvement in global

GDP drives demand growth

higher than forecast capacity

expansions

• IHS base forecast for most

segments sit at or below

historical average; plastics is

higher driven by substitution

assumptions

• Downside case would be

problematic for all value chains

except chlor-alkali (vinyls)

• Assuming GDP strengthens,

implication is that for most value

chains utilization rates will be

rising

Demand Growth Range vs. Capacity: 2016-2020

© 2015 IHS. ALL RIGHTS RESERVED.

0

50

100

150

200

250

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Ethylene Methanol Propylene Chlorine Paraxylene Benzene

Million Metric Tons

Global Base Chemicals Cumulative Demand Growth 2010 - 2020 = 224 Million Metric Tons

© 2015 IHS, Inc. No portion of this presentation may be reproduced, reused, or

otherwise distributed in any form without prior written consent.

Total

Growth

MM Tons

AAGR:

2010/20 MM

Tons/Yr

AAGR:

2010/20, %

Ethylene 61.6 5.6 3.5

Methanol 52.4 4.8 6.9

Propylene 47.8 4.3 4.2

Chlorine 28.1 2.6 3.6

Paraxylene 19.4 1.8 4.5

Benzene 14.7 1.3 2.3

© 2015 IHS. ALL RIGHTS RESERVED.

Capital Investment Peaks 2013-2015; Asia Slows

Dramatically, N. America Accelerates, Middle

East Is Steady

0

25

50

75

100

125

150

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

ROW Europe S. America N. America Asia Pacific Middle East

Global Chemical CAPEX, 2014 US $ Billions

© 2015 IHS. ALL RIGHTS RESERVED.

• Lower crude price in the US

depress gas-based margins in

the near-term, but recovery

improves with energy and tighter

markets; ethane price rise

threatens ethylene/PE margins

• An assumption to a return of

normal operations and pressure

from trade, eases Europe off of

current supply-constrained highs

• Asia shows improvement going

forward as improving profits in

methanol and C/A margins offset

weakness in propylene

14

0

50

100

150

200

250

300

350

400

450

00 02 04 06 08 10 12 14 16 18 20

Global N. America W. Europe Asia

Global: Basic Chemicals & Plastics EBIT Comparison*

Source: IHS © 2015 IHS

Do

lla

rs P

er

Me

tric

To

ns

*Weighted Average Earnings Before Interest & Taxes

Global EBIT Will Pull Back Slightly In The Near-term

Before Accelerating As Demand Growth Exceeds Supply

© 2015 IHS. ALL RIGHTS RESERVED.

• North America (USA)

Leverage low cost natural gas based

chemicals into investments in ethylene,

propylene and methanol based derivatives.

Invest to establish export channels to

market that exceed historical norms

• Middle East (Saudi Arabia)

Moderated investment pace, diversified

feedslate to support downstream market

development and continued industrial

expansion well beyond ethylene chemistry

• North East Asia (China)

Strong domestic investment focused on

reducing import dependencies.

Leverage coal to chemicals technology

near term © 2015 IHS, Inc. No portion of this presentation may be reproduced, reused, or

otherwise distributed in any form without prior written consent.

Raw Material & Energy Costs

Demand Growth & Access to Markets

Technology &

Economies of Scale

Chemical Industry

Investments Seek A

Sustainable Advantage

Key Drivers For Investments In New Capacity

Will Vary By Region

© 2015 IHS. ALL RIGHTS RESERVED.

Top 5 Countries Adding Base Chemical Capacity 231 Million Tons from 2010 to 2020

0

20

40

60

80

100

120

China UnitedStates

SaudiArabia

S. Korea India

Chlorine Paraxylene Benzene

Methanol Propylene Ethylene

Million Metric Tons

Top five will add nearly 75%

of base chemical capacity.

China will dominate new

capacity, adding 45% of total

Investment capital has shifted to

North America, however, the vast

majority of new investment continues

to accelerate in Asia/Pacific,

dominated by China

© 2015 IHS. ALL RIGHTS RESERVED.

CHINA CHEMICAL

INDUSTRY

• Become “global leader”, beyond size, have core

proprietary technologies, competitive advantage,

global brand, international scope & breadth

• Global leadership role responding to energy

changes, changes in regional markets (Japan &

Korea), cutting edge of innovative solutions

• Understand chemical value-chain, from well-head to

consumers; understand China’s position at each

stage of the value-chain and developments needed

to be a leader

• Address over-capacity issues

• Shut down inefficient capacity with significant

environmental impact

• Restructure portfolio to replace imports related to

domestic product quality and performance

• Focus on supply-chain optimization

• Focus on strategic emerging industries – build

integrated clusters of innovative leading technology

chemicals; including specialty chemical clusters.

© 2015 IHS. ALL RIGHTS RESERVED.

Regional Trade Is Critical To Success In

The Global Chemical Industry

• Trade is an essential element of basic

chemical supply chains

• Low cost regions such as North

America and the Middle East will

export increasing volumes

• On-purpose technology will change

propylene trade patterns

• Significant investment in ships, ports,

and infrastructure is needed to

support increasing trade volumes

© 2015 IHS, Inc. No portion of this presentation may be reproduced, reused, or

otherwise distributed in any form without prior written consent.

5 Countries Adding 75% of Base Chemical

Capacity: 2010 to 2020 (231 MM Metric Tons)

© 2015 IHS. ALL RIGHTS RESERVED.

But Chemical Trade Continues To Globalize, Connecting

Advantaged Feeds With Markets, Labor And Capital

• Trade will continue to grow,

connecting resource-rich

geographies with high growth

markets.

• By 2020 global trade will have

more than doubled from 2000

levels, representing about 50%

of global production.

• Pressure on high-cost

producers servicing markets

targeted by advantaged

capacity will intensify.

• Global supply-chain expertise

and well crafted go-to-market

strategies increase in

importance.

19

0

100

200

300

400

500

0%

10%

20%

30%

40%

50%

Global: Total Trade & 2020 Exports, Base Chemicals & Plastics

Source: IHS © 2015 IHS

% o

f 2

02

0 P

rod

uc

tio

n E

xp

ort

ed

To

tal E

xp

ort

s, M

illio

n M

etr

ic T

on

s

© 2015 IHS. ALL RIGHTS RESERVED.

China Remains Central To Basic Chemical Trade

© 2015 IHS, Inc. No portion of this presentation may be reproduced, reused, or

otherwise distributed in any form without prior written consent.

0%

25%

50%

75%

0

20

40

60

05 10 15 20

Net Equi. Imports Domestic Demand

Self-Sufficiency

MM Metric Tons %, Self-Sufficiency

0%

25%

50%

75%

0

20

40

60

05 10 15 20

Net Equiv Exports Domestic Demand

Net Exports, % of Cap.

MM Metric Tons % of Capacity

US Ethylene Demand & Equivalent Trade China Ethylene Demand & Equivalent Trade

© 2015 IHS. ALL RIGHTS RESERVED.

The Impact of Energy

At The Extremes…

Summary of key

trends

• Basic chemicals and derivatives markets

adjust to “new energy” dynamics

• …lower energy and lower prices for

plastics can represent a demand stimulus

• Pause in capital project approval

combined with stronger demand growth

can result in tight markets for certain

value chains; higher margins

• Emerging changes in China market will

continue to have a global impact in most

value chains

• Lifting of sanctions on Iran likely to

impact PE and methanol near term

• Expanding (or contracting) regional trade

requires detailed understanding of

logistics developments and solid go-to-

market strategies

© 2015 IHS. ALL RIGHTS RESERVED.

The Impact of Energy

At The Extremes…

Beyond 2020…

• Crude oil price trend in relation to

NAM natural gas and China coal:

impact on rate of demand growth and

investment location decisions

• Availability of low-cost ethane and

propane in North America to support

continued investments; both domestic

and international

• Developments in on-purpose

technology for olefins versus

traditional routes, including the use of

methanol as a route to olefins.

• Impact of coal-to-chemicals and on-

purpose propylene in China:

private/provincial investment versus

state-owned; self-sufficiency and surplus

capacity impacting trade with China.

© 2015 IHS. ALL RIGHTS RESERVED.

The ethylene value chain

23

Presentation Name / Month 2015

Polyethylene

(LDPE, HDPE,

LLDPE)

Monoethylene

Glycol (MEG) Ethylene Oxide

Ethylene

Ethylbenzene/

Styrene

Others

Ethylene

Dichloride

(EDC)

Vinyl Chloride

Monomer (VCM) Pipes & Fittings, Profiles &

Tubes, Films & Sheets, Wires &

Cables, Bottles

Appliance and Electrical/Electronics, Food Packaging/Food, Service

Ware, Medical Products, Furniture Components, Foam Board and

Sheathing, Building Insulation, Rigid Packaging, Automotive

Components, Refrigerator Components, Electrical Components,

Electronics/Electrical Appliances, Paper Coating, Nonwoven Binders

LLDPE

LDPE

HDPE

Film – garbage bags, food packaging

Injection Molding – housewares, lids, caps

Sheet – geo membranes

Blow Molding – bottles, containers for household chemicals,

antifreeze, Injection Molding – smaller containers for

pharmaceuticals, shampoo, cosmetics , Film and Sheet –

packaging, liners ,Pipe and Tubing

Film and Sheet – packaging (high clarity film markets), films

Extrusion Coating – coating paper, paperboard for packaging

Injection Molding – housewares, toys, molded furniture

Antifreeze, Polyester (fiber and PET),

Household cleaning, Paint &

coatings, Industrial &Institutional

Cleaning, Personal Care, Lubricants,

Construction, Cosmetics, Paper,

Automotive, Consumer Electronics,

Textiles

© 2015 IHS. ALL RIGHTS RESERVED.

The propylene value chain

24

Presentation Name / Month 2015

Propylene Oxide

Acrylonitrile

Acrylic Acid

Propylene

Cumene

Polypropylene Random Copolymer

Oxo Chemicals

Isopropyl Alcohol

Ethylene/Propylen

e Elastomers

Homopolymer

Hereophasic (impact)

Copolymer

flexible & rigid packaging, fibers, film, large

molded parts, thermoformed containers

Cast film, thermoforming, blow molding,

sheet extrusion, blown film

Corrugated pipe, thin wall injection molding,

bumpers, blow molding bottle

Phenol Phenolics, epoxys, polycarbonate

ABS Resins, SAN Resins, Acrylic

Fiber, Nitrile Rubber, Acrylamide

Propylene Glycol, Glycol

Ethers, Isopropanol Amines

Solvents

Butanol, 2-

Ethylhexanol

EPDM/EPM

Others Polygas Chemicals, Nonene,

Dodecene, Heptene

Urethane flexible foams, flexible foams

Construction, foods, drugs, cosmetics,

environmentally friendly antifreeze

Commodity acrylate esters, superabsorbent polymers,

surface coatings, water treatment/petroleum

Automotive, houseware, pipe,

conduit and fittings, packaging,

apparel

Surface coatings, plasticizers,

Automotive, construction/roofing, polymer

modification, oil and cable insulation, oil

additives, appliance parts, hoses

Propane/

Butane/

Gas Oil/

Naphtha

Methanol

Allyl chloride/

Epichlorohydrin Epoxy resins, synthetic glycerin, ECH elastomers, specialty water treatment

chemicals, wet-strength resins for paper production and surfactants

FCCU

Off-

Gas

from

Refin

eries

Refinery

Alkylat-

ion

Units

© 2015 IHS. ALL RIGHTS RESERVED.

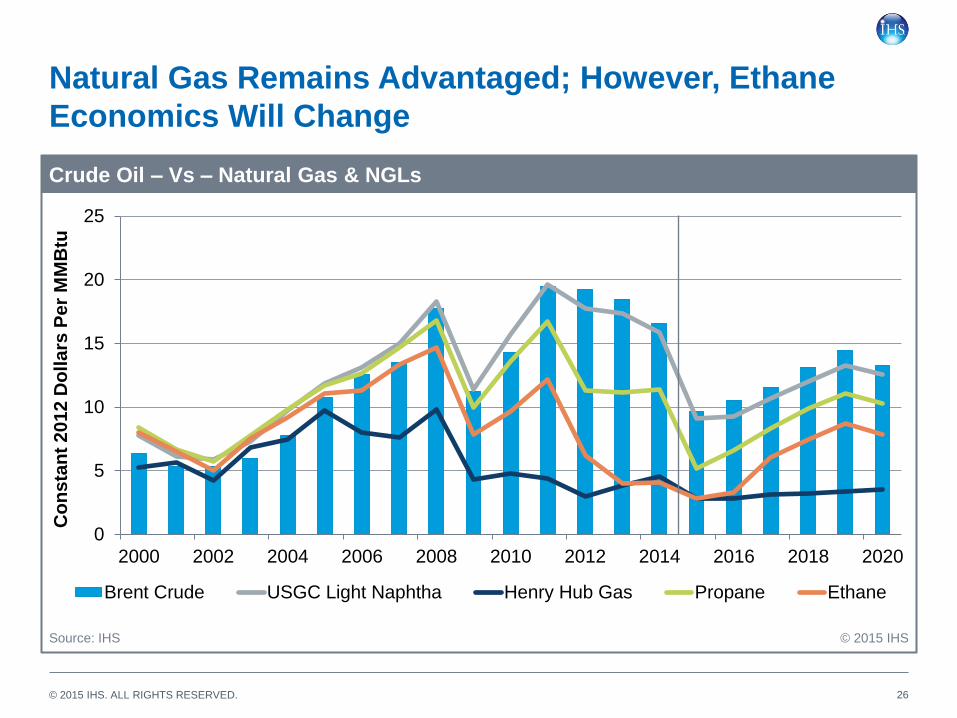

North America

NGL Feedstock

25

• North America natural gas remains well

supplied but “methane demand constrained”

including LNG exports in the forecast.

• North America NGL balance shows there is

sufficient ethane supply to handle current

wave of new US ethylene crackers (10 million

metric tons).

• Ethane supply for an additional 15 million

metric tons of ethylene beyond 2020 is

available at the “right price”.

• Propane supply will be long in the near

term, making propane the likely competitive

feedstock compared to ethane.

• Ethane prices will rise to reflect higher

demand and support extraction of higher cost

supply; propane parity / competitive ethylene

derivative exports, provide a price ceiling.

© 2015 IHS. ALL RIGHTS RESERVED.

Natural Gas Remains Advantaged; However, Ethane

Economics Will Change

0

5

10

15

20

25

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Brent Crude USGC Light Naphtha Henry Hub Gas Propane Ethane

Crude Oil – Vs – Natural Gas & NGLs

© 2015 IHS

Co

ns

tan

t 2

01

2 D

oll

ars

Pe

r M

MB

tu

Source: IHS

26

© 2015 IHS. ALL RIGHTS RESERVED.

US Ethane Demand To Increase faster than Supply Exports (waterborne and pipe) and capacity additions (creep and greenfield)

27

50

60

70

80

90

100

0

500

1000

1500

2000

2500

3000

3500

2005 2010 2015 2020 2025 2030 2035

Total Ethane, bpd US ethane recoved, bpd US ethane recovery, %

Th

ou

sa

nd

Ba

rre

ls P

er

Da

y,

Eth

an

e

Pe

rce

nt

Eth

an

e R

ec

ove

ry

US Supply

© 2015 IHS Source: IHS

© 2015 IHS. ALL RIGHTS RESERVED.

North America Ethylene Capacity Growth: 2014–2020 Completed or Firm Projects (Thousand Metric Tons)

28

January 2016

Ethylene Capacity Additions Total Additions

Projected North American Ethylene (2014 - 2020) (Thousand Metric Tons per Year) 2014-2021

Company Location

BASF/Total Port Arthur. TX 128

ChevronPhillips Cedar Bayou, TX 1500

Dow Freeport, TX 1500

Dow Plaquemine, LA 250

Eastman Longview, TX 17

Equistar Channelview I, TX 182

Equistar Channelview II, TX 182

Equistar Corpus Christi, TX 363

Equistar La Porte, TX 385

ExxonMobil Baytown, TX 1500

Flint Hills Port Arthur, TX 100

Formosa Point Comfort, TX 1150

Indorama Lake Charles, LA 370

LACC LLC Lake Charles, LA 1000

Oxy/Mexichem Ingleside, TX 550

Shin-Etsu Plaquemine, LA 500

Sasol Lake Charles, LA 1550

Westlake Calvert City, KY 82

Westlake Lake Charles I, LA 110

Westlake Lake Charles II, LA 24

Williams Geismar, LA 258

Braskem Idesa Mexico 1000

Nova Sarnia 168

Firm: 12869

© 2015 IHS. ALL RIGHTS RESERVED.

Propylene Market View North America PDH Propylene Capacity Additions Latest Update

29

Propylene Capacity Additions

Projected North American Propylene (2014 - 2020) (Thousand Metric Tons per Year)

Company Location

Total Additions

2014-2021+ Technology

BASF Freeport, TX 475 MTP

Dow Freeport, TX 750 PDH

Enterprise Mont Belvieu, TX 750 PDH

Ascend Alvin, TX 1173 PDH

Formosa Point Comfort, TX 600 PDH

Williams Redwater, Alberta 525 PDH

Firm: 4273

Possible Propylene Capacity Additions

Other Announcements

Company Location

Total Additions

2014-2021+

Flint Hills Resources Houston, TX 750

Williams Western Canada 525

Dow Freeport, TX 750

Sunoco Marcus Hook, PA 600

Announced: 2625

January 2016

© 2015 IHS. ALL RIGHTS RESERVED.

Propylene Supply Diversification From By-Product/Co-Product of Refining/Steam Crackers to On-Purpose

30

0

50

100

150

10 11 12 13 14 15 16 17 18 19 20

Stm. Crackers FCC Splitters Dehydro

Metathesis Methanol to Olefins Coal to Olefins

Coal to Propylene HS FCC Others On-Purpose

Total Capacity

World: PG/CG Propylene Prod. by Feedstock

Source: IHS © 2015 IHS

Millio

n M

etr

ic T

on

s

© 2015 IHS. ALL RIGHTS RESERVED.

Propylene Capacity Additions Overwhelm Demand Growth

Five years of excess capacity through end 2019

31

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

10 11 12 13 14 15 16 17 18 19 20

Mil

lio

n M

etr

ic T

on

s

North America Middle East China

West Europe Others Annual Demand Increase

Global Propylene Capacity Additions vs. Demand Growth

Source: IHS © 2015 IHS

© 2015 IHS. ALL RIGHTS RESERVED.

Polyethylene

Key Issues

32

• Global demand growth healthy:

~1.3xGDP (2015-2020)

• Excess capacity growth concentrated

in low cost / high demand regions of

North America, Middles East, and

China

• Low crude brings improved margins

for naphtha-based producers; WEP

capacity closures postponed; Asia

capacity runs at higher rates

• South America projects postponed

until conditions improve.

• North Americas joins Middle East as

major global exporter: look for

increasing competitive environment

for domestic market

© 2015 IHS. ALL RIGHTS RESERVED.

• North America experiencing

unprecedented margin acceleration

due to tight supply/demand.

• Imports of resins and finished goods

expected to continue to increase into

North America with no new capacity

on the horizon until 2019

• New capacity in China and Middle

East likely to continue downward

pressure on prices in those regions.

• Chinese self sufficiency likely to

redirect trade flows away from China

and to other regions that are short

resin like the Americas

33

Polypropylene

Key Issues

© 2015 IHS. ALL RIGHTS RESERVED.

Questions?

34