Please refer to page 26 for important disclosures and analyst certification, or on our website

www.macquarie.com/research/disclosures.

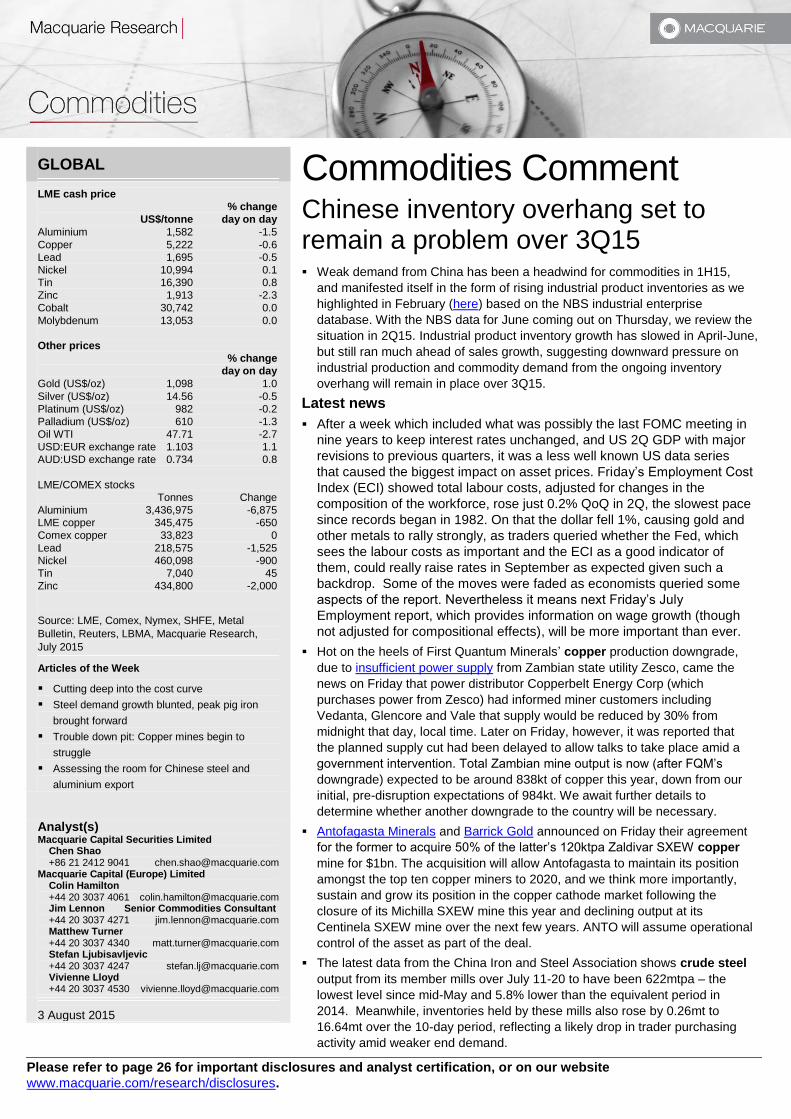

GLOBAL

LME cash price

% change

US$/tonne day on day

Aluminium 1,582 -1.5

Copper 5,222 -0.6

Lead 1,695 -0.5

Nickel 10,994 0.1

Tin 16,390 0.8

Zinc 1,913 -2.3

Cobalt 30,742 0.0

Molybdenum 13,053 0.0

Other prices

% change

day on day

Gold (US$/oz) 1,098 1.0

Silver (US$/oz) 14.56 -0.5

Platinum (US$/oz) 982 -0.2

Palladium (US$/oz) 610 -1.3

Oil WTI 47.71 -2.7

USD:EUR exchange rate 1.103 1.1

AUD:USD exchange rate 0.734 0.8

LME/COMEX stocks

Tonnes Change

Aluminium 3,436,975 -6,875

LME copper 345,475 -650

Comex copper 33,823 0

Lead 218,575 -1,525

Nickel 460,098 -900

Tin 7,040 45

Zinc 434,800 -2,000

Source: LME, Comex, Nymex, SHFE, Metal

Bulletin, Reuters, LBMA, Macquarie Research,

July 2015

Articles of the Week

Cutting deep into the cost curve

Steel demand growth blunted, peak pig iron

brought forward

Trouble down pit: Copper mines begin to

struggle

Assessing the room for Chinese steel and

aluminium export

Analyst(s) Macquarie Capital Securities Limited Chen Shao +86 21 2412 9041 [email protected] Macquarie Capital (Europe) Limited Colin Hamilton +44 20 3037 4061 [email protected] Jim Lennon Senior Commodities Consultant +44 20 3037 4271 [email protected] Matthew Turner +44 20 3037 4340 [email protected] Stefan Ljubisavljevic +44 20 3037 4247 [email protected] Vivienne Lloyd +44 20 3037 4530 [email protected]

3 August 2015

Commodities Comment Chinese inventory overhang set to remain a problem over 3Q15 Weak demand from China has been a headwind for commodities in 1H15,

and manifested itself in the form of rising industrial product inventories as we

highlighted in February (here) based on the NBS industrial enterprise

database. With the NBS data for June coming out on Thursday, we review the

situation in 2Q15. Industrial product inventory growth has slowed in April-June,

but still ran much ahead of sales growth, suggesting downward pressure on

industrial production and commodity demand from the ongoing inventory

overhang will remain in place over 3Q15.

Latest news

After a week which included what was possibly the last FOMC meeting in

nine years to keep interest rates unchanged, and US 2Q GDP with major

revisions to previous quarters, it was a less well known US data series

that caused the biggest impact on asset prices. Friday’s Employment Cost

Index (ECI) showed total labour costs, adjusted for changes in the

composition of the workforce, rose just 0.2% QoQ in 2Q, the slowest pace

since records began in 1982. On that the dollar fell 1%, causing gold and

other metals to rally strongly, as traders queried whether the Fed, which

sees the labour costs as important and the ECI as a good indicator of

them, could really raise rates in September as expected given such a

backdrop. Some of the moves were faded as economists queried some

aspects of the report. Nevertheless it means next Friday’s July

Employment report, which provides information on wage growth (though

not adjusted for compositional effects), will be more important than ever.

Hot on the heels of First Quantum Minerals’ copper production downgrade,

due to insufficient power supply from Zambian state utility Zesco, came the

news on Friday that power distributor Copperbelt Energy Corp (which

purchases power from Zesco) had informed miner customers including

Vedanta, Glencore and Vale that supply would be reduced by 30% from

midnight that day, local time. Later on Friday, however, it was reported that

the planned supply cut had been delayed to allow talks to take place amid a

government intervention. Total Zambian mine output is now (after FQM’s

downgrade) expected to be around 838kt of copper this year, down from our

initial, pre-disruption expectations of 984kt. We await further details to

determine whether another downgrade to the country will be necessary.

Antofagasta Minerals and Barrick Gold announced on Friday their agreement

for the former to acquire 50% of the latter’s 120ktpa Zaldivar SXEW copper

mine for $1bn. The acquisition will allow Antofagasta to maintain its position

amongst the top ten copper miners to 2020, and we think more importantly,

sustain and grow its position in the copper cathode market following the

closure of its Michilla SXEW mine this year and declining output at its

Centinela SXEW mine over the next few years. ANTO will assume operational

control of the asset as part of the deal.

The latest data from the China Iron and Steel Association shows crude steel

output from its member mills over July 11-20 to have been 622mtpa – the

lowest level since mid-May and 5.8% lower than the equivalent period in

2014. Meanwhile, inventories held by these mills also rose by 0.26mt to

16.64mt over the 10-day period, reflecting a likely drop in trader purchasing

activity amid weaker end demand.

Macquarie Research Commodities Comment

3 August 2015 2

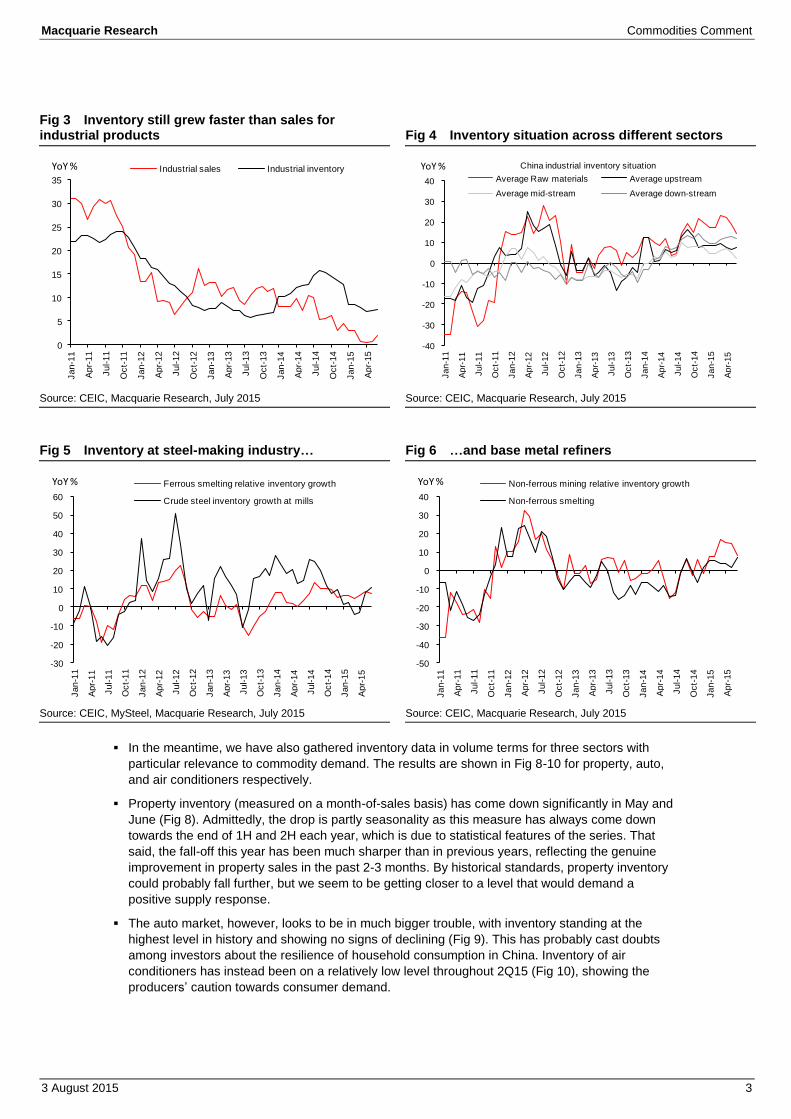

Inventory overhang to remain for China in 3Q15

Weak demand from China has been a headwind for commodities in 1H15, and manifested itself in

the form of rising industrial product inventories as we highlighted in February (here) based on the

NBS industrial enterprise database. With the NBS data for June coming out on Thursday, we

review the situation in 2Q15. Industrial product inventory growth has slowed in April-June, but still

ran much ahead of sales growth, suggesting downward pressure on industrial production and

commodity demand from the ongoing inventory overhang will remain in place over 3Q15.

The lack of reliable and comprehensive inventory data has been a major obstacle to analysts’

attempts to gauge China’s industrial product inventory. We’ve taken an innovative approach by

looking at the difference between inventory growth and sales growth of industrial sectors (referred

to as “relative inventory growth” in this note) with the straightforward theory that higher/lower

growth of inventory than sales conceptually corresponds to restocking/destocking.

The results have been supportive – we do see a strong negative correlation between relative

industrial inventory growth and Industrial Production (IP) growth (Fig 1); on a sectoral level, our

indicator also seems to reflect reality well, e.g. the relative inventory growth for ferrous mining

industry closely tracking a survey result of domestic iron ore mine inventory (Fig 2).

Fig 1 Relative inventory growth correlates well with the overall economy…

Fig 2 …and sectoral inventory indicators

Source: CEIC, Macquarie Research, July 2015 Source: CEIC, MySteel, Macquarie Research, July 2015

So as shown in Fig 1, relative industrial inventory growth remained positive in 2Q15, suggesting

industrial companies were still building up inventory compared with their sales. This is not to say

inventory growth per se was still rising; actually, both inventory and sales growth has been

declining, but the former still grew faster (Fig 3). In other words, real demand for industrial

products has been even weaker than the sluggish IP growth.

While the general trends are largely the same across different industrial sectors for relative

inventory growth, the further towards the upstream of industrial chains, the more volatile relative

inventory growth tends to be. In recent months, we have also seen a sharper drop in our inventory

indicator for raw materials than for other sectors (Fig 4), which is in line with the fact that the raw

material producers have seen larger price drops than other industrial sectors owing to the

whiplash effect from weaker downstream demand (and of course, lower prices).

More specifically, besides the falling relative inventory growth at iron ore mines, relative inventory

at ferrous smelting (which is largely steel-making) has remained low in 2Q15, and that at non-

ferrous smelting (i.e. base metal refining) hit a peak in January-February and slowed down since

then. Coal inventory at miners has largely stopped rising in absolute terms, but given double-digit

negative sales growth, the need for destocking remains (Fig 7). The conditions for a few other

sectors are shown at the end of this note.

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

-15

-10

-5

0

5

10

15

Ja

n-1

1

Apr-

11

Ju

l-11

Oct-

11

Ja

n-1

2

Apr-

12

Ju

l-12

Oct-

12

Ja

n-1

3

Apr-

13

Ju

l-13

Oct-

13

Ja

n-1

4

Apr-

14

Ju

l-14

Oct-

14

Ja

n-1

5

Apr-

15

Industrial inventory relative growth

Nominal IP, MoM - RHS

YoY % %

0

1

2

3

4

5

6

7

8

-20

-10

0

10

20

30

40

Ju

l-1

2

Sep

-12

No

v-1

2

Ja

n-1

3

Ma

r-13

Ma

y-1

3

Ju

l-1

3

Sep

-13

No

v-1

3

Ja

n-1

4

Ma

r-14

Ma

y-1

4

Ju

l-1

4

Sep

-14

Nov

-14

Ja

n-1

5

Ma

r-15

Ma

y-1

5

Ferrous mining relative inventory growth - LHS

Domestic iron mine inventory - days of consumption by domestic mills

YoY % Days

Macquarie Research Commodities Comment

3 August 2015 3

Fig 3 Inventory still grew faster than sales for industrial products

Fig 4 Inventory situation across different sectors

Source: CEIC, Macquarie Research, July 2015 Source: CEIC, Macquarie Research, July 2015

Fig 5 Inventory at steel-making industry… Fig 6 …and base metal refiners

Source: CEIC, MySteel, Macquarie Research, July 2015 Source: CEIC, Macquarie Research, July 2015

In the meantime, we have also gathered inventory data in volume terms for three sectors with

particular relevance to commodity demand. The results are shown in Fig 8-10 for property, auto,

and air conditioners respectively.

Property inventory (measured on a month-of-sales basis) has come down significantly in May and

June (Fig 8). Admittedly, the drop is partly seasonality as this measure has always come down

towards the end of 1H and 2H each year, which is due to statistical features of the series. That

said, the fall-off this year has been much sharper than in previous years, reflecting the genuine

improvement in property sales in the past 2-3 months. By historical standards, property inventory

could probably fall further, but we seem to be getting closer to a level that would demand a

positive supply response.

The auto market, however, looks to be in much bigger trouble, with inventory standing at the

highest level in history and showing no signs of declining (Fig 9). This has probably cast doubts

among investors about the resilience of household consumption in China. Inventory of air

conditioners has instead been on a relatively low level throughout 2Q15 (Fig 10), showing the

producers’ caution towards consumer demand.

0

5

10

15

20

25

30

35

Ja

n-1

1

Ap

r-11

Ju

l-11

Oct-

11

Jan

-12

Apr-

12

Jul-

12

Oct-

12

Ja

n-1

3

Ap

r-13

Ju

l-13

Oct-

13

Ja

n-1

4

Ap

r-14

Ju

l-14

Oct-

14

Jan

-15

Apr-

15

Industrial sales Industrial inventoryYoY %

-40

-30

-20

-10

0

10

20

30

40

Jan-1

1

Ap

r-1

1

Jul-1

1

Oc

t-1

1

Jan-1

2

Ap

r-1

2

Jul-1

2

Oc

t-1

2

Jan-1

3

Ap

r-1

3

Ju

l-1

3

Oc

t-1

3

Jan-1

4

Ap

r-1

4

Jul-1

4

Oc

t-1

4

Ja

n-1

5

Ap

r-1

5

Average Raw materials Average upstream

Average mid-stream Average down-stream

YoY % China industrial inventory situation

-30

-20

-10

0

10

20

30

40

50

60

Ja

n-1

1

Ap

r-1

1

Ju

l-1

1

Oc

t-1

1

Ja

n-1

2

Ap

r-1

2

Ju

l-1

2

Oc

t-1

2

Ja

n-1

3

Ap

r-1

3

Ju

l-1

3

Oc

t-1

3

Ja

n-1

4

Ap

r-1

4

Ju

l-1

4

Oc

t-1

4

Ja

n-1

5

Ap

r-1

5

Ferrous smelting relative inventory growth

Crude steel inventory growth at mills

YoY %

-50

-40

-30

-20

-10

0

10

20

30

40

Ja

n-1

1

Apr-

11

Ju

l-11

Oct-

11

Ja

n-1

2

Apr-

12

Ju

l-12

Oct-

12

Ja

n-1

3

Apr-

13

Ju

l-13

Oct-

13

Ja

n-1

4

Apr-

14

Ju

l-14

Oct-

14

Ja

n-1

5

Apr-

15

Non-ferrous mining relative inventory growth

Non-ferrous smelting

YoY %

Macquarie Research Commodities Comment

3 August 2015 4

Fig 7 Coal inventory still too high on a relative basis

Fig 8 Property inventory dropped significantly on stronger sales

Source: CEIC, Sxcoal, Macquarie Research, July 2015 Source: CEIC, Macquarie Research, July 2015

Fig 9 Auto makers have too much inventory… Fig 10 …while A/C makers are much more cautious

Source: Wind, Macquarie Research, July 2015 Source: Wind, Macquarie Research, July 2015

Coming back to a more general perspective, inventory levels tend to be pro-cyclical – weak/strong

end-user demand doesn’t only directly reduce/increase the need for finished product inventory as

a buffer for fluctuations of sales, but also suppresses/boosts prices and the market value of

inventory, which pushes companies to further lower/raise inventory levels.

The implication is that major inventory cycles tend to coincide with general economic cycles and

exacerbate the latter. In China’s current case, industrial companies are facing the double whammy

of weak demand and relatively high inventory, and such vicious cycles are usually not easy to

break.

Another implication is that inventory cycles could be indicative of the overall economic trends.

From this angle, Fig 1 suggests the current level of relative inventory growth is still too high to be a

positive factor for economic growth and commodity demand. As it takes time for relative inventory

growth to be dragged towards/below zero, it seems likely that the inventory overhang will remain a

negative factor for commodities’ outlook in 3Q15.

-60

-40

-20

0

20

40

60

80

100

120

-40

-30

-20

-10

0

10

20

30

40

50

Ja

n-1

1

Apr-

11

Ju

l-11

Oct-

11

Ja

n-1

2

Apr-

12

Ju

l-12

Oct-

12

Ja

n-1

3

Apr-

13

Ju

l-13

Oct-

13

Ja

n-1

4

Apr-

14

Ju

l-14

Oct-

14

Ja

n-1

5

Apr-

15

Coal ming relative inventory growth

Coal stock at key state-owned mines - RHS

YoY % YoY %

0

1

2

3

4

5

6

7

8

9

Jan

Fe

b

Mar

Ap

r

May

Jun

Ju

l

Aug

Sep

Oc

t

Nov

Dec

2012 2013 2014 2015

Ratio between property inventory and monthly sales

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

Ja

n

Fe

b

Ma

r

Apr

May

Jun

Jul

Au

g

Se

p

Oct

Nov

Dec

2012 2013 2014 2015

Ratio between auto inventory and monthly sales

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

Ja

n

Fe

b

Ma

r

Apr

May

Jun

Jul

Au

g

Se

p

Oct

Nov

Dec

2012 2013 2014 2015

Ratio between A/C inventory and monthly sales

Macquarie Research Commodities Comment

3 August 2015 5

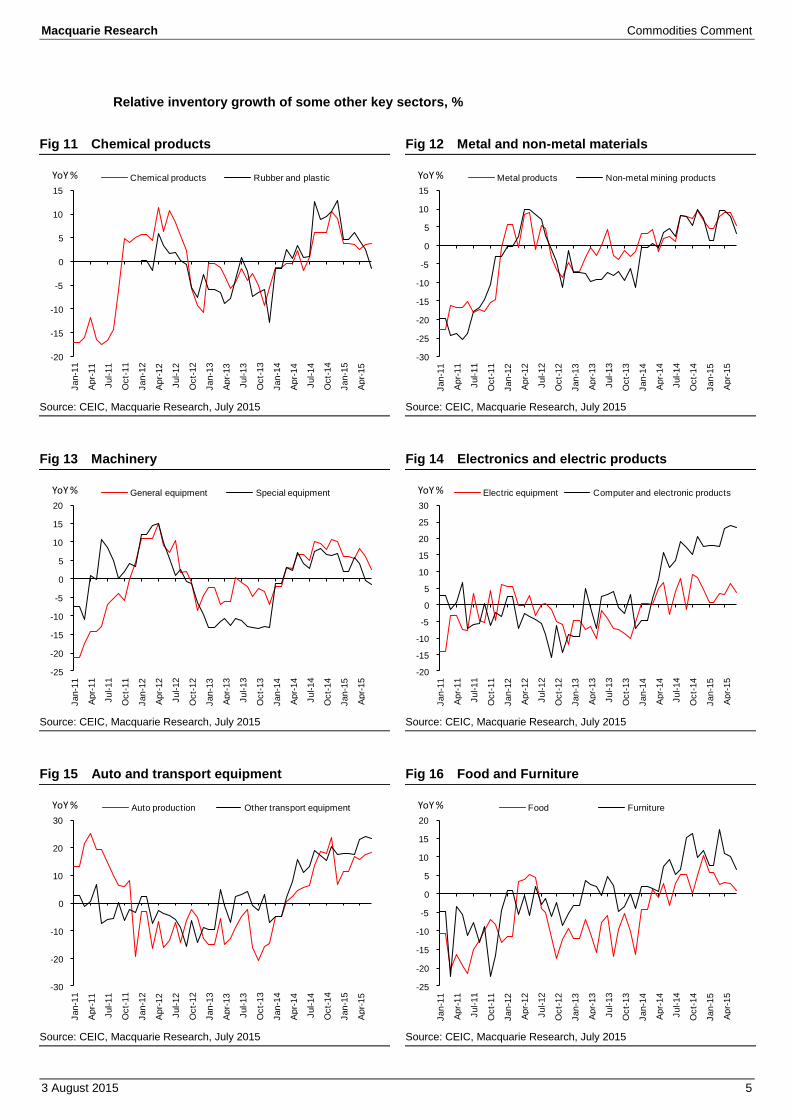

Relative inventory growth of some other key sectors, %

Fig 11 Chemical products Fig 12 Metal and non-metal materials

Source: CEIC, Macquarie Research, July 2015 Source: CEIC, Macquarie Research, July 2015

Fig 13 Machinery Fig 14 Electronics and electric products

Source: CEIC, Macquarie Research, July 2015 Source: CEIC, Macquarie Research, July 2015

Fig 15 Auto and transport equipment Fig 16 Food and Furniture

Source: CEIC, Macquarie Research, July 2015 Source: CEIC, Macquarie Research, July 2015

-20

-15

-10

-5

0

5

10

15

Ja

n-1

1

Apr-

11

Ju

l-1

1

Oct-

11

Ja

n-1

2

Apr-

12

Ju

l-1

2

Oct-

12

Ja

n-1

3

Apr-

13

Ju

l-1

3

Oct-

13

Ja

n-1

4

Apr-

14

Ju

l-1

4

Oct-

14

Ja

n-1

5

Apr-

15

Chemical products Rubber and plasticYoY %

-30

-25

-20

-15

-10

-5

0

5

10

15

Ja

n-1

1

Apr-

11

Ju

l-1

1

Oct-

11

Ja

n-1

2

Apr-

12

Ju

l-1

2

Oct-

12

Ja

n-1

3

Apr-

13

Ju

l-1

3

Oct-

13

Ja

n-1

4

Apr-

14

Ju

l-1

4

Oct-

14

Ja

n-1

5

Apr-

15

Metal products Non-metal mining productsYoY %

-25

-20

-15

-10

-5

0

5

10

15

20

Ja

n-1

1

Apr-

11

Ju

l-11

Oct-

11

Ja

n-1

2

Apr-

12

Ju

l-12

Oct-

12

Ja

n-1

3

Apr-

13

Ju

l-13

Oct-

13

Ja

n-1

4

Apr-

14

Ju

l-14

Oct-

14

Ja

n-1

5

Apr-

15

General equipment Special equipmentYoY %

-20

-15

-10

-5

0

5

10

15

20

25

30

Ja

n-1

1

Ap

r-1

1

Ju

l-1

1

Oc

t-1

1

Ja

n-1

2

Ap

r-1

2

Ju

l-1

2

Oc

t-1

2

Ja

n-1

3

Ap

r-1

3

Ju

l-1

3

Oc

t-1

3

Ja

n-1

4

Ap

r-1

4

Ju

l-1

4

Oc

t-1

4

Ja

n-1

5

Ap

r-1

5

Electric equipment Computer and electronic productsYoY %

-30

-20

-10

0

10

20

30

Ja

n-1

1

Ap

r-1

1

Ju

l-1

1

Oc

t-1

1

Ja

n-1

2

Ap

r-1

2

Ju

l-1

2

Oc

t-1

2

Ja

n-1

3

Ap

r-1

3

Ju

l-1

3

Oc

t-1

3

Ja

n-1

4

Ap

r-1

4

Ju

l-1

4

Oc

t-1

4

Ja

n-1

5

Ap

r-1

5

Auto production Other transport equipmentYoY %

-25

-20

-15

-10

-5

0

5

10

15

20

Ja

n-1

1

Apr-

11

Ju

l-11

Oct-

11

Ja

n-1

2

Apr-

12

Ju

l-12

Oct-

12

Ja

n-1

3

Apr-

13

Ju

l-13

Oct-

13

Ja

n-1

4

Apr-

14

Ju

l-14

Oct-

14

Ja

n-1

5

Apr-

15

Food FurnitureYoY %

Macquarie Research Commodities Comment

3 August 2015 6

Closing price * Closing price *

31-Jul-15 31-Jul-15 30-Jul-15 30-Jul-15 % ch. day 2015 YTD Ave 2014

US$/tonne US¢/lb US$/tonne US¢/lb on day US$/tonne US$/tonne

LME Cash

Aluminium 1,582 72 1,607 73 -1.5 1,761 1,867

Aluminium Alloy 1,696 77 1,696 77 0.0 1,781 1,951

NAASAC 1,685 76 1,694 77 -0.6 1,829 2,086

Copper 5,222 237 5,253 238 -0.6 5,859 6,862

Lead 1,695 77 1,703 77 -0.5 1,857 2,096

Nickel 10,994 499 10,978 498 0.1 13,341 16,867

Tin 16,390 743 16,265 738 0.8 16,693 21,893

Zinc 1,913 87 1,957 89 -2.3 2,115 2,164

Cobalt 30,742 1,394 30,746 1,395 0.0 29,894 31,251

Molybdenum 13,053 592 13,050 592 0.0 16,998 25,548

LME 3 Month

Aluminium 1,618 73 1,643 75 -1.5 1,782 1,894

Aluminium Alloy 1,700 77 1,700 77 0.0 1,794 1,974

NAASAC 1,710 78 1,720 78 -0.6 1,855 2,117

Copper 5,230 237 5,260 239 -0.6 5,851 6,828

Lead 1,702 77 1,713 78 -0.6 1,867 2,113

Nickel 11,040 501 11,025 500 0.1 13,395 16,935

Tin 16,300 739 16,175 734 0.8 16,712 21,887

Zinc 1,916 87 1,951 88 -1.8 2,122 2,167

Cobalt 30,500 1,383 30,500 1,383 0.0 30,017 31,287

Molybdenum 13,250 601 13,250 601 0.0 17,059 25,548

* LME 2nd ring price - 1300 hrs London time. Year-to-date averages calculated from official fixes.

1,098 1,088 1.0 1,194 1,266

14.56 14.64 -0.5 16.32 19.07

982 984 -0.2 1,137 1,384

610 618 -1.3 753 803

47.71 49.05 -2.7 52.89 93.36

1.103 1.091 1.1 1.114 1.329

0.734 0.728 0.8 0.776 0.903

Change since last report Cancelled End-14 Ch. since

(tonnes) 31-Jul-15 30-Jul-15 Volume Percent warrants stocks end-14

LME Aluminium 3,436,975 3,443,850 -6,875 -0.2% 1,431,450 4,205,225 -768,250

Shanghai Aluminium 318,564 318,911 -347 -0.1% - 207,428 111,136

Total Aluminium 3,755,539 3,762,761 -7,222 -0.2% - 4,412,653 -657,114

LME Copper 345,475 346,125 -650 -0.2% 26,850 177,025 168,450

Comex Copper 33,823 33,823 0 0.0% - 24,150 9,673

Shanghai Copper 103,117 101,251 1,866 1.8% - 111,915 -8,798

Total Copper 482,415 481,199 1,216 0.3% - 313,090 169,325

LME Zinc 434,800 436,800 -2,000 -0.5% 55,000 690,825 -256,025

Shanghai Zinc 177,214 176,763 451 0.3% - 83,471 93,743

Total Zinc 612,014 613,563 -1,549 -0.3% - 774,296 -162,282

LME Lead 218,575 220,100 -1,525 -0.7% 57,050 221,975 -3,400

Shanghai Lead 14,500 15,968 -1,468 -9.2% - 63,604 -49,104

Total Lead 233,075 236,068 -2,993 -1.3% - 285,579 -52,504

Aluminium Alloy 13,040 13,040 0 0.0% 140 26,520 -13,480

NASAAC 50,840 51,500 -660 -1.3% 3,380 80,700 -29,860

Nickel 460,098 460,998 -900 -0.2% 152,874 414,900 45,198

Tin 7,040 6,995 45 0.6% 1,580 12,135 -5,095

Source: CME, LBMA, LME, Reuters, SHFE, Macquarie Research

Exchange Stocks

Prices

Gold - London PM Fix (US$/oz)

Silver - LBMA Silver Price (US$/oz)

Platinum - London 3pm price (US$/oz)

Palladium - London 3pm price (US$/oz)

Oil WTI - NYMEX latest (US$/bbl)

EUR : USD exchange rate - latest

AUD : USD exchange rate - latest

Friday 31 July 2015

Macquarie Research Commodities Comment

3 August 2015 7

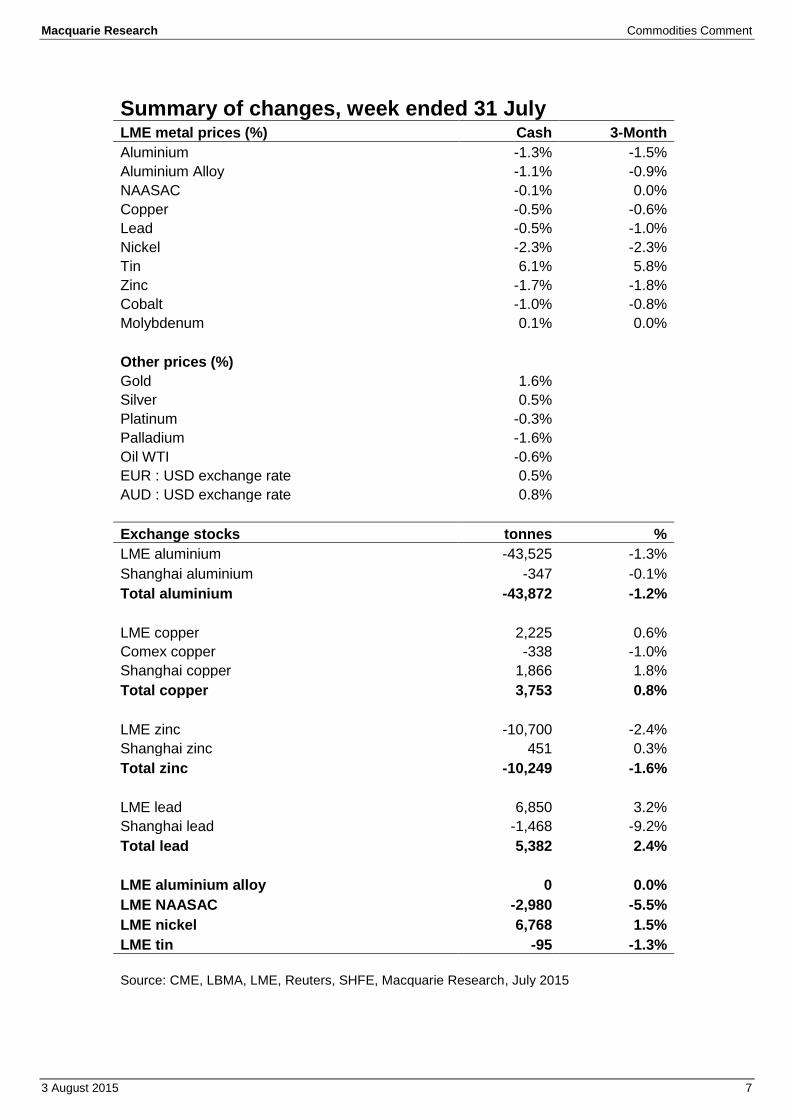

Summary of changes, week ended 31 July LME metal prices (%) Cash 3-Month

Aluminium -1.3% -1.5%

Aluminium Alloy -1.1% -0.9%

NAASAC -0.1% 0.0%

Copper -0.5% -0.6%

Lead -0.5% -1.0%

Nickel -2.3% -2.3%

Tin 6.1% 5.8%

Zinc -1.7% -1.8%

Cobalt -1.0% -0.8%

Molybdenum 0.1% 0.0%

Other prices (%) Gold 1.6%

Silver 0.5% Platinum -0.3% Palladium -1.6% Oil WTI -0.6% EUR : USD exchange rate 0.5% AUD : USD exchange rate 0.8%

Exchange stocks tonnes %

LME aluminium -43,525 -1.3%

Shanghai aluminium -347 -0.1%

Total aluminium -43,872 -1.2%

LME copper 2,225 0.6%

Comex copper -338 -1.0%

Shanghai copper 1,866 1.8%

Total copper 3,753 0.8%

LME zinc -10,700 -2.4%

Shanghai zinc 451 0.3%

Total zinc -10,249 -1.6%

LME lead 6,850 3.2%

Shanghai lead -1,468 -9.2%

Total lead 5,382 2.4%

LME aluminium alloy 0 0.0%

LME NAASAC -2,980 -5.5%

LME nickel 6,768 1.5%

LME tin -95 -1.3%

Source: CME, LBMA, LME, Reuters, SHFE, Macquarie Research, July 2015

Macquarie Research Commodities Comment

3 August 2015 8

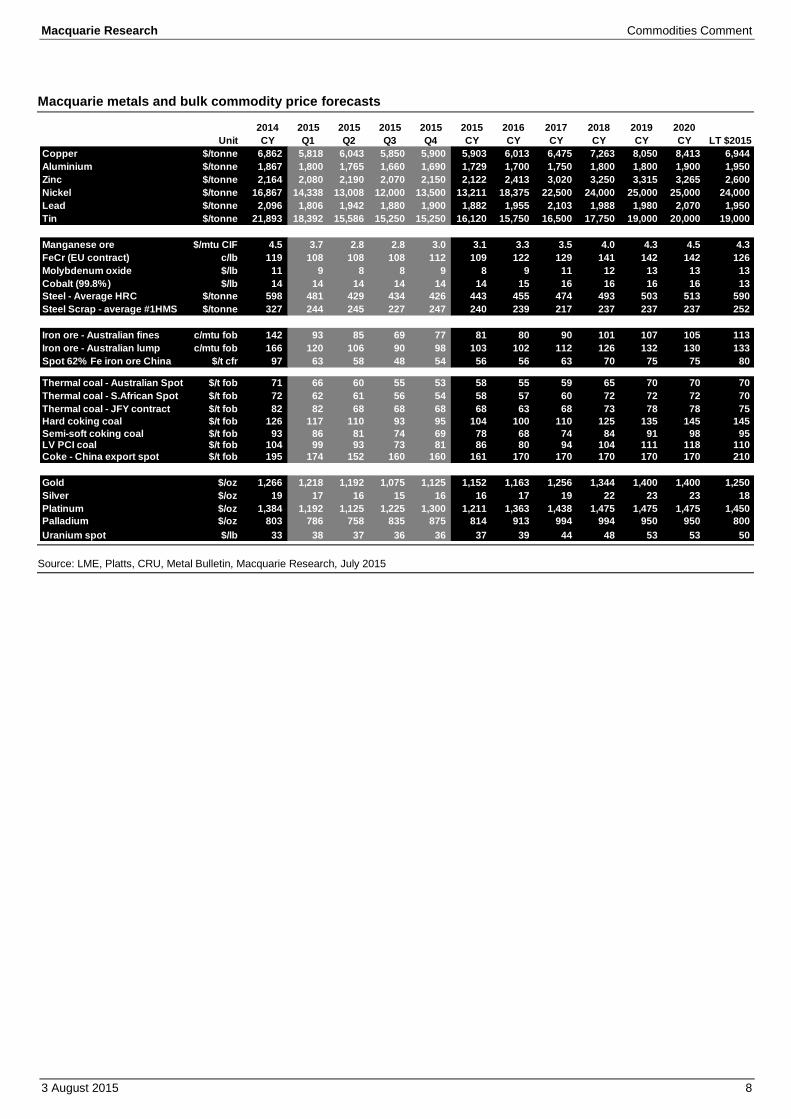

Macquarie metals and bulk commodity price forecasts

Source: LME, Platts, CRU, Metal Bulletin, Macquarie Research, July 2015

2014 2015 2015 2015 2015 2015 2016 2017 2018 2019 2020

Unit CY Q1 Q2 Q3 Q4 CY CY CY CY CY CY LT $2015

Copper $/tonne 6,862 5,818 6,043 5,850 5,900 5,903 6,013 6,475 7,263 8,050 8,413 6,944

Aluminium $/tonne 1,867 1,800 1,765 1,660 1,690 1,729 1,700 1,750 1,800 1,800 1,900 1,950

Zinc $/tonne 2,164 2,080 2,190 2,070 2,150 2,122 2,413 3,020 3,250 3,315 3,265 2,600

Nickel $/tonne 16,867 14,338 13,008 12,000 13,500 13,211 18,375 22,500 24,000 25,000 25,000 24,000

Lead $/tonne 2,096 1,806 1,942 1,880 1,900 1,882 1,955 2,103 1,988 1,980 2,070 1,950

Tin $/tonne 21,893 18,392 15,586 15,250 15,250 16,120 15,750 16,500 17,750 19,000 20,000 19,000

Manganese ore $/mtu CIF 4.5 3.7 2.8 2.8 3.0 3.1 3.3 3.5 4.0 4.3 4.5 4.3

FeCr (EU contract) c/lb 119 108 108 108 112 109 122 129 141 142 142 126

Molybdenum oxide $/lb 11 9 8 8 9 8 9 11 12 13 13 13

Cobalt (99.8%) $/lb 14 14 14 14 14 14 15 16 16 16 16 13

Steel - Average HRC $/tonne 598 481 429 434 426 443 455 474 493 503 513 590

Steel Scrap - average #1HMS $/tonne 327 244 245 227 247 240 239 217 237 237 237 252

Iron ore - Australian fines c/mtu fob 142 93 85 69 77 81 80 90 101 107 105 113

Iron ore - Australian lump c/mtu fob 166 120 106 90 98 103 102 112 126 132 130 133

Spot 62% Fe iron ore China $/t cfr 97 63 58 48 54 56 56 63 70 75 75 80

Thermal coal - Australian Spot $/t fob 71 66 60 55 53 58 55 59 65 70 70 70

Thermal coal - S.African Spot $/t fob 72 62 61 56 54 58 57 60 72 72 72 70

Thermal coal - JFY contract $/t fob 82 82 68 68 68 68 63 68 73 78 78 75

Hard coking coal $/t fob 126 117 110 93 95 104 100 110 125 135 145 145

Semi-soft coking coal $/t fob 93 86 81 74 69 78 68 74 84 91 98 95 LV PCI coal $/t fob 104 99 93 73 81 86 80 94 104 111 118 110

Coke - China export spot $/t fob 195 174 152 160 160 161 170 170 170 170 170 210

Gold $/oz 1,266 1,218 1,192 1,075 1,125 1,152 1,163 1,256 1,344 1,400 1,400 1,250

Silver $/oz 19 17 16 15 16 16 17 19 22 23 23 18

Platinum $/oz 1,384 1,192 1,125 1,225 1,300 1,211 1,363 1,438 1,475 1,475 1,475 1,450

Palladium $/oz 803 786 758 835 875 814 913 994 994 950 950 800

Uranium spot $/lb 33 38 37 36 36 37 39 44 48 53 53 50

Macquarie Research Commodities Comment

3 August 2015 9

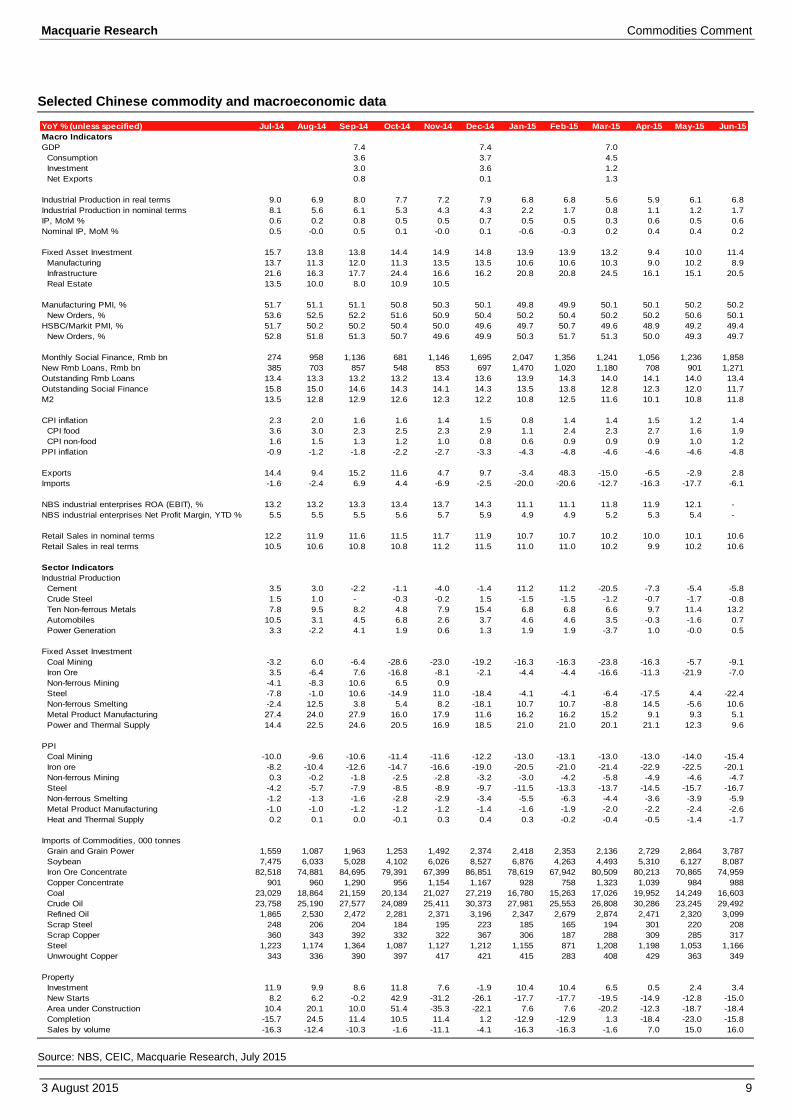

Selected Chinese commodity and macroeconomic data

Source: NBS, CEIC, Macquarie Research, July 2015

YoY % (unless specified) Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 Dec-14 Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15

Macro Indicators

GDP 7.4 7.4 7.0

Consumption 3.6 3.7 4.5

Investment 3.0 3.6 1.2

Net Exports 0.8 0.1 1.3

Industrial Production in real terms 9.0 6.9 8.0 7.7 7.2 7.9 6.8 6.8 5.6 5.9 6.1 6.8

Industrial Production in nominal terms 8.1 5.6 6.1 5.3 4.3 4.3 2.2 1.7 0.8 1.1 1.2 1.7

IP, MoM % 0.6 0.2 0.8 0.5 0.5 0.7 0.5 0.5 0.3 0.6 0.5 0.6

Nominal IP, MoM % 0.5 -0.0 0.5 0.1 -0.0 0.1 -0.6 -0.3 0.2 0.4 0.4 0.2

Fixed Asset Investment 15.7 13.8 13.8 14.4 14.9 14.8 13.9 13.9 13.2 9.4 10.0 11.4

Manufacturing 13.7 11.3 12.0 11.3 13.5 13.5 10.6 10.6 10.3 9.0 10.2 8.9

Infrastructure 21.6 16.3 17.7 24.4 16.6 16.2 20.8 20.8 24.5 16.1 15.1 20.5

Real Estate 13.5 10.0 8.0 10.9 10.5

Manufacturing PMI, % 51.7 51.1 51.1 50.8 50.3 50.1 49.8 49.9 50.1 50.1 50.2 50.2

New Orders, % 53.6 52.5 52.2 51.6 50.9 50.4 50.2 50.4 50.2 50.2 50.6 50.1

HSBC/Markit PMI, % 51.7 50.2 50.2 50.4 50.0 49.6 49.7 50.7 49.6 48.9 49.2 49.4

New Orders, % 52.8 51.8 51.3 50.7 49.6 49.9 50.3 51.7 51.3 50.0 49.3 49.7

Monthly Social Finance, Rmb bn 274 958 1,136 681 1,146 1,695 2,047 1,356 1,241 1,056 1,236 1,858

New Rmb Loans, Rmb bn 385 703 857 548 853 697 1,470 1,020 1,180 708 901 1,271

Outstanding Rmb Loans 13.4 13.3 13.2 13.2 13.4 13.6 13.9 14.3 14.0 14.1 14.0 13.4

Outstanding Social Finance 15.8 15.0 14.6 14.3 14.1 14.3 13.5 13.8 12.8 12.3 12.0 11.7

M2 13.5 12.8 12.9 12.6 12.3 12.2 10.8 12.5 11.6 10.1 10.8 11.8

CPI inflation 2.3 2.0 1.6 1.6 1.4 1.5 0.8 1.4 1.4 1.5 1.2 1.4

CPI food 3.6 3.0 2.3 2.5 2.3 2.9 1.1 2.4 2.3 2.7 1.6 1.9

CPI non-food 1.6 1.5 1.3 1.2 1.0 0.8 0.6 0.9 0.9 0.9 1.0 1.2

PPI inflation -0.9 -1.2 -1.8 -2.2 -2.7 -3.3 -4.3 -4.8 -4.6 -4.6 -4.6 -4.8

Exports 14.4 9.4 15.2 11.6 4.7 9.7 -3.4 48.3 -15.0 -6.5 -2.9 2.8

Imports -1.6 -2.4 6.9 4.4 -6.9 -2.5 -20.0 -20.6 -12.7 -16.3 -17.7 -6.1

NBS industrial enterprises ROA (EBIT), % 13.2 13.2 13.3 13.4 13.7 14.3 11.1 11.1 11.8 11.9 12.1 -

NBS industrial enterprises Net Profit Margin, YTD % 5.5 5.5 5.5 5.6 5.7 5.9 4.9 4.9 5.2 5.3 5.4 -

Retail Sales in nominal terms 12.2 11.9 11.6 11.5 11.7 11.9 10.7 10.7 10.2 10.0 10.1 10.6

Retail Sales in real terms 10.5 10.6 10.8 10.8 11.2 11.5 11.0 11.0 10.2 9.9 10.2 10.6

Sector Indicators

Industrial Production

Cement 3.5 3.0 -2.2 -1.1 -4.0 -1.4 11.2 11.2 -20.5 -7.3 -5.4 -5.8

Crude Steel 1.5 1.0 - -0.3 -0.2 1.5 -1.5 -1.5 -1.2 -0.7 -1.7 -0.8

Ten Non-ferrous Metals 7.8 9.5 8.2 4.8 7.9 15.4 6.8 6.8 6.6 9.7 11.4 13.2

Automobiles 10.5 3.1 4.5 6.8 2.6 3.7 4.6 4.6 3.5 -0.3 -1.6 0.7

Power Generation 3.3 -2.2 4.1 1.9 0.6 1.3 1.9 1.9 -3.7 1.0 -0.0 0.5

Fixed Asset Investment

Coal Mining -3.2 6.0 -6.4 -28.6 -23.0 -19.2 -16.3 -16.3 -23.8 -16.3 -5.7 -9.1

Iron Ore 3.5 -6.4 7.6 -16.8 -8.1 -2.1 -4.4 -4.4 -16.6 -11.3 -21.9 -7.0

Non-ferrous Mining -4.1 -8.3 10.6 6.5 0.9

Steel -7.8 -1.0 10.6 -14.9 11.0 -18.4 -4.1 -4.1 -6.4 -17.5 4.4 -22.4

Non-ferrous Smelting -2.4 12.5 3.8 5.4 8.2 -18.1 10.7 10.7 -8.8 14.5 -5.6 10.6

Metal Product Manufacturing 27.4 24.0 27.9 16.0 17.9 11.6 16.2 16.2 15.2 9.1 9.3 5.1

Power and Thermal Supply 14.4 22.5 24.6 20.5 16.9 18.5 21.0 21.0 20.1 21.1 12.3 9.6

PPI

Coal Mining -10.0 -9.6 -10.6 -11.4 -11.6 -12.2 -13.0 -13.1 -13.0 -13.0 -14.0 -15.4

Iron ore -8.2 -10.4 -12.6 -14.7 -16.6 -19.0 -20.5 -21.0 -21.4 -22.9 -22.5 -20.1

Non-ferrous Mining 0.3 -0.2 -1.8 -2.5 -2.8 -3.2 -3.0 -4.2 -5.8 -4.9 -4.6 -4.7

Steel -4.2 -5.7 -7.9 -8.5 -8.9 -9.7 -11.5 -13.3 -13.7 -14.5 -15.7 -16.7

Non-ferrous Smelting -1.2 -1.3 -1.6 -2.8 -2.9 -3.4 -5.5 -6.3 -4.4 -3.6 -3.9 -5.9

Metal Product Manufacturing -1.0 -1.0 -1.2 -1.2 -1.2 -1.4 -1.6 -1.9 -2.0 -2.2 -2.4 -2.6

Heat and Thermal Supply 0.2 0.1 0.0 -0.1 0.3 0.4 0.3 -0.2 -0.4 -0.5 -1.4 -1.7

Imports of Commodities, 000 tonnes

Grain and Grain Power 1,559 1,087 1,963 1,253 1,492 2,374 2,418 2,353 2,136 2,729 2,864 3,787

Soybean 7,475 6,033 5,028 4,102 6,026 8,527 6,876 4,263 4,493 5,310 6,127 8,087

Iron Ore Concentrate 82,518 74,881 84,695 79,391 67,399 86,851 78,619 67,942 80,509 80,213 70,865 74,959

Copper Concentrate 901 960 1,290 956 1,154 1,167 928 758 1,323 1,039 984 988

Coal 23,029 18,864 21,159 20,134 21,027 27,219 16,780 15,263 17,026 19,952 14,249 16,603

Crude Oil 23,758 25,190 27,577 24,089 25,411 30,373 27,981 25,553 26,808 30,286 23,245 29,492

Refined Oil 1,865 2,530 2,472 2,281 2,371 3,196 2,347 2,679 2,874 2,471 2,320 3,099

Scrap Steel 248 206 204 184 195 223 185 165 194 301 220 208

Scrap Copper 360 343 392 332 322 367 306 187 288 309 285 317

Steel 1,223 1,174 1,364 1,087 1,127 1,212 1,155 871 1,208 1,198 1,053 1,166

Unwrought Copper 343 336 390 397 417 421 415 283 408 429 363 349

Property

Investment 11.9 9.9 8.6 11.8 7.6 -1.9 10.4 10.4 6.5 0.5 2.4 3.4

New Starts 8.2 6.2 -0.2 42.9 -31.2 -26.1 -17.7 -17.7 -19.5 -14.9 -12.8 -15.0

Area under Construction 10.4 20.1 10.0 51.4 -35.3 -22.1 7.6 7.6 -20.2 -12.3 -18.7 -18.4

Completion -15.7 24.5 11.4 10.5 11.4 1.2 -12.9 -12.9 1.3 -18.4 -23.0 -15.8

Sales by volume -16.3 -12.4 -10.3 -1.6 -11.1 -4.1 -16.3 -16.3 -1.6 7.0 15.0 16.0

Macquarie Research Commodities Comment

3 August 2015 10

Articles of the Week

Cutting deep into the cost curve

Like a hot knife through butter, most commodity prices are now slicing with relative ease into

industry cost curves. Given that for many metals and bulks there is an imminent need to take

capacity offline amid clear oversupply, this is natural at the current point in the cycle. Concepts of

cost support are thus less relevant in the short term where it is all about inflicting enough pain to

force hard decisions on capacity. However, cost structures still matter for through the cycle

equilibrium. Meanwhile, this reporting season has a common theme – further cost outs at metals

and mining companies. We review movements in cost curves and the factors driving the cost

reductions – many of which are unlikely to reverse anytime soon.

Figure 1 below shows the extent of the challenge for metals and mining. Versus the 90th

percentile (a measure we still consider flawed for modern markets – further details here) the vast

majority have lower current spot prices – significantly lower in certain cases. Or, looking at it

another way in figure 2, decent proportions of global supply across metals and bulks are currently

losing money on a cash plus sustaining capital basis - over a third in areas like met coal, nickel

and aluminium. The only mined market where everyone remains cash positive is potash, and

given the inherent overcapacity the spirit of producer discipline will be further tested in this market

over the coming year – we would expect a push into the cost curve sooner rather than later.

Fig 1 The vast majority of mined commodities are now trading well into the cost curve…

Fig 2 …with over a third of supply currently loss-making in met coal, nickel and aluminium

Source: LME, Platts, Wood Mackenzie, Macquarie Research, July 2015 Source: Platts, Wood Mackenzie, Macquarie Research, July 2015

That a significant proportion of supply is under pressure should not be a surprise, given prices are

at multi-year lows. Indeed, it could be said the surprise is that more isn’t lossmaking, or that we

haven’t seen more aggressive supply responses. The main reason for this is that cost structures

themselves are falling rapidly, and where potential for further cost gains can be shown, producers

will continue to keep capacity in the market and try and improve their own competitive position.

Unfortunately, when everyone is doing the same things, the fundamental imbalance is not solved.

The current reporting season is showing further evidence of aggressive cost outs at mining

companies, with Vale’s $15.8/t FOB for iron ore reported on Thursday just the latest in a series of

positive surprises. There are three core reasons why costs have been coming down:

Currency: All currencies have been depreciating against the US dollar, but commodity currencies

more than most (as would be expected given falling commodity prices). With decent parts of

mining cost structures denominated in local currencies, the equivalent USD cost has of course

fallen. Figure 3 shows YTD performance of 6 key producer currencies – while the RUB may only

be down 3% this year, on a 12-month view it has almost halved, while the BRL has certainly

helped Vale’s cost structure. It should be noted that, with many curves having Chinese or US

producers at the top end, wider currency depreciation against the USD tends to steepen cost

curves.

-40%

-30%

-20%

-10%

0%

10%

20%

Po

tash

Go

ld

Zin

c

Co

pp

er

Th

erm

al C

oa

l

Ura

niu

m

PG

M b

aske

t

Iro

n O

re

Alu

min

ium

Ma

ng

an

ese

ore

Me

t Co

al

Nic

ke

l

Current spot price premium over 90th percentile

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

Po

tash

Go

ld

Zin

c

Co

pp

er

Th

erm

al C

oa

l

Ura

niu

m

Iro

n O

re

PG

M b

aske

t

Ma

ng

an

ese

ore

Me

t Co

al

Nic

ke

l

Alu

min

ium

Proportion of supply curve underwater

Macquarie Research Commodities Comment

3 August 2015 11

Fig 3 Commodity currency depreciation has been a key theme for 2015…

Fig 4 …with currency alone moving industry average costs down by ~20% in some cases from 2013 levels

Source: Bloomberg, Macquarie Research, July 2015 Source: Wood Mackenzie, Macrobond, Macquarie Research, July 2015

Energy: While the first oil price drop was almost a year ago now, these things take a while to

feed into mining cost structures. But now the effects are being seen, and in many cases they are

significant, particularly for those where diesel-heavy mining processes or freight rates as a

significant part of the cost structure. The only miners not to have felt this benefit are those who

previously has a subsidised rate, where the government has now reduced the subsidy – for

example smaller Indonesian thermal coal producers who were buying subsidised diesel illegally.

While depreciating FX steepens cost curves, falling energy prices tend to make them shallower as

inefficient producers gain most benefit.

Producer self-help: This is not an area to be underestimated – whether debottlenecking existing

operations or stripping down contractor costs miners in the main have done much of what they

can to help protect against further margin erosion. Moreover, many of these cuts are sustainable

should discipline be maintained. The challenge now will be to eke out further gains given the easy

hits have already been exhausted, particularly as sustaining capital may have to resume an

upward trend.

It is definitely fair to say the shift in Chinese cost structures was one of the key areas analysts

(ourselves included) got wrong over recent years. While China was growing rapidly, core inflation

was ~4% and mining cost inflation running at over 10% per annum on a like for like basis. Making

assumptions that USD mining inflation would continue to rise at 5% per annum seemed fair,

particularly as the RMB was still appreciating.

Fig 5 Lower energy costs are only now starting to push through into cost structures

Fig 6 We have seen heavy disinflationary pressures running through Chinese domestic mining

Source: Reuters, Macquarie Research, July 2015 Source: NBS, Macquarie Research, July 2015

-3%

-8%-10%

-11% -12%

-26%-30%

-25%

-20%

-15%

-10%

-5%

0%

RUB ZAR CLP CAD AUD BRL

YTD commodity currency depreciation versus USD

75

80

85

90

95

100

105

110

2010 2011 2012 2013 2014 2015

Production weighted USD index

Gold Copper

DXY

0

20

40

60

80

100

120

140

160

2007 2009 2011 2013 2015

Brent crude, US$/bbl

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

Co

al

Ste

el

Iro

n o

re m

inin

g

Base m

eta

ls

Petr

ole

um

& N

atu

ral G

as

Ch

em

ical P

roducts

Ele

ctr

onic

com

ponents

Fabri

cate

d M

eta

l P

roduct

Pla

stic P

roducts

Ag

s +

Fo

od

Pap

er M

an

ufa

ctu

ring

Textile

Gen

era

l E

quip

ment

Auto

mo

bile

Tra

nsport

Eq

uip

ment

Co

nsum

er G

ood

Pri

nting &

Reco

rdin

g

Fo

od

Ele

ctr

icity P

roduction

To

bacco

Bevera

ges

Clo

thin

g

Ph

arm

aceutical

Fo

od

Serv

ices

Wate

r S

up

ply

PP

I b

y s

ecto

r, 2

01

4

Upstream

Downstream

Midstream

Macquarie Research Commodities Comment

3 August 2015 12

Instead, as China slowed, inflation bottlenecks gave way to overcapacity in all areas with

disinflationary pressures running through the whole economy. As shown in figure 6, upstream

sectors have indeed been worst hit with producer price inflation in 2014 ranging from -4% for base

metals to -11% for coal. As a result, Chinese cost structures have gone down, not up, adding

further downward pressure to the sharp end of global cost curves.

Of course, the nature of cost structures is very different across individual commodities. The drop

in energy prices has had a notable effect on iron ore, given ~30% of costs are more or less oil-

linked. The same is true for thermal coal, where the effect has also seen a reasonable flattening

of the curve, meaning everyone is feeling a bit of pain, but not really enough to invoke widespread

cuts. While the higher premium certainly helped in 2014, on a LME cash basis much of the curve

has been losing money for a considerable period of time, just not enough. For copper, aside from

a short period in 2009 prices have consistently traded at the top end or even out of the cost curve,

but not anymore – we feel a decent proportion of copper mine output is struggling at these price

levels. Unlike others however, we don’t think there needs to be significant copper supply cuts.

Fig 7 The move lower in the contestable iron ore cost curve has been dramatic…

Fig 8 …while for thermal coal, the cost curve has also flattened considerably

Source: SMM, Company Reports, Macquarie Research, July 2015 Source: Wood Mackenzie, Macquarie Research, July 2015

Fig 9 On a LME cash basis, aluminium has traded into the cost curve for a while…

Fig 10 …whereas copper has spent much of the past decade out the curve, but pressure has returned

Source: Wood Mackenzie, Macquarie Research, July 2015 Source: Wood Mackenzie, Macquarie Research, July 2015

In the very short term, cost curves are not important for setting the price in many markets. Rather,

they are important for determining how much balance sheet pain marginal producers can take

before liquidity is drained and hard decisions on capacity cuts have to be made. The more cost

structures fall, the more prices have to fall to force this point – figure 11 looks at the drop in

marginal costs across commodities over the past 2 years.

0

20

40

60

80

100

120

140

160

180

0 250 500 750 1000 1250 1500 1750 2000

$/t C

FR

Ch

ina, 6

2%

basis

million tonnes

Evolution of iron ore cost curve

2013

2014

2015

40

50

60

70

80

90

100

110

120

0 200 400 600 800 1000

60

00

kca

l NA

R C

FR

Ch

ina

($

/t)

Cumulative Volume (mt)

Seaborne thermal coal supply curve - CFR South China

2012 costs 2014 costs 2015 costs

400

800

1200

1600

2000

2400

2800

3200

3600

1984 1988 1992 1996 2000 2004 2008 2012

$/tAluminium costs and prices

Price Ninth Decile

Upper Quartile Median

Lower Quartile

0

40

80

120

160

200

240

280

320

360

400

440

1980 1984 1988 1992 1996 2000 2004 2008 2012

$/lb

Price Ninth Decile

Copper costs and pricesCopper costs and prices

YTD 2015price

Macquarie Research Commodities Comment

3 August 2015 13

However, assuming suitable cuts are made, cost structures will again be important for through the

cycle prices, particularly given general expectations of ongoing overcapacity. This may allow for

some price recovery in selected commodities, but in a low inflation world this is barely anything to

get excited about. Rather, raw material constraints (nickel, and eventually zinc and copper) still

offer the better hope of price upside in the coming years.

Fig 11 Marginal costs have fallen across all commodities over the past 24 months, but much more sharply for bulks

Source: LME, Platts, Wood Mackenzie, Macquarie Research, July 2015

-2%-7% -8%

-12%-15%

-22%

-32% -33% -33%

-52%-60%

-50%

-40%

-30%

-20%

-10%

0%

Zin

c

Co

pp

er

Go

ld

Nic

ke

l

Alu

min

ium

Ura

niu

m

Ma

ng

an

ese

ore

Me

t Co

al

Th

erm

al C

oa

l

Iro

n O

re

Change in marginal cost level over the past 24 months

Macquarie Research Commodities Comment

3 August 2015 14

Steel demand growth blunted, peak pig iron brought forward

If the Chinese economic slowdown has surprised in its severity, then the slowdown in steel

consumption has been even more acute. And when you are talking about an economy which

represents 50% of worldwide production and 45% of consumption then this becomes a global

problem. With China now poised to be a much larger net exporter of steel than we had previously

expected, we have taken the opportunity to update our global balance. The result is just 0.7%

CAGR in global steel demand through the end of the decade, and China losing its position as the

key consumption growth driver to India and other emerging Asian economies.

With a relatively negligible growth rate in steel production, and the available scrap pool continuing

to grow, 2014’s global pig iron production now looks to have marked the peak for the foreseeable

future. This has obvious implications for the raw materials, with required iron ore displacement

now larger and more pressure on marginal met coal supply to exit permanently.

China’s construction sector has been important to the growth in global steel, and last year

consumed over 300mt – more than total consumption across the US and Western Europe

combined. Its decline this year has been equally important in pulling global steel down in 2015.

The downturn in China’s property sector has been well documented, and while property sales are

now recovering strongly, early indicators for steel consumption remain weak – developers seem

content to run down inventory rather than advance new projects. YoY growth in property

investment is now running at lower levels than in Q1 2009, while prestressed concrete piles – the

first thing driven into the ground in medium-large building projects – are seeing output down 10%

YoY in 2015 to date. We view this as a more tangible indicator than unaudited numbers such as

new starts.

That is not to say things won’t improve into the second half after what has been an incredibly weak

period – indeed, we think they will as asset allocation towards property recovers. However, any

aggressive uplift (such as that seen in H2 2013) would have to be government directed, which

currently looks unlikely, given they seem satisfied with the way the property market has trended in

recent times. Given this, we see total construction demand for steel falling 6% this year to 286mt

(crude steel equivalent), with the residential contribution down 10% YoY. Moreover, given that the

‘base’ build for China is more like 10m residential units per annum than the ~12m units seen in

recent years, we expect the general trend to be lower in the coming years. We may not yet have

hit peak Chinese steel, but we likely have seen peak consumption in the construction sector.

Fig 1 China’s tangible construction market indicators continue to exhibit weakness...

Fig 2 …with peak steel in construction now past, and entering a period of steady decline

Source: NBS, Macquarie Research, July 2015 Source: CISA, NBS, Macquarie Research, July 2015

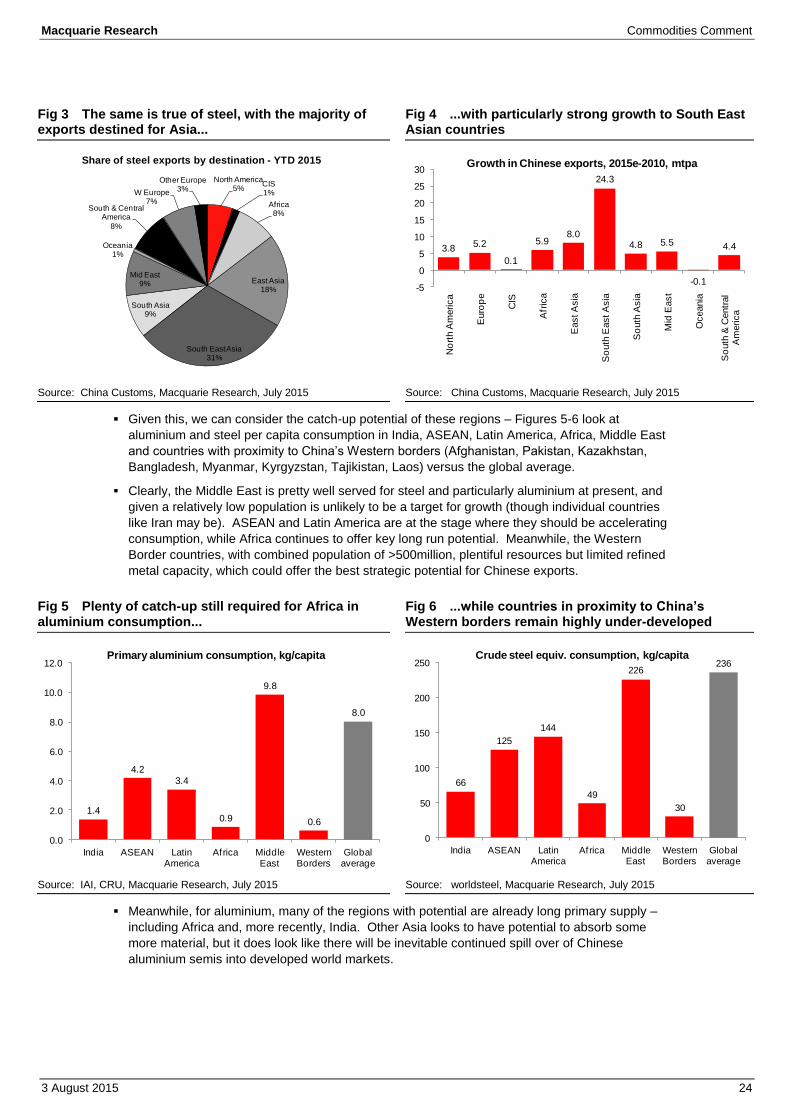

One area where we have changed our view is steel export volumes from China. While the

overcapacity in the domestic steel industry has been apparent for the past couple of years, we

thought a combination of rising demand and improving corporate behaviour (including capacity

rationalisation and consolidation) would see export volumes drop over time towards ~30mtpa

crude steel equivalent. Neither of those factors now look to be in place, with demand struggling

and China’s MIIT now encouraging exports as a solution to overcapacity, certainly delaying the

hard decisions on capacity at least. As a result, we now model over 100mt of net exports on a

crude steel equivalent basis – for more details on where these will be targeted please refer to this

recent report.

-40

-30

-20

-10

0

10

20

30

40

50

60

0

5

10

15

20

25

30

35

40

45

50

Jan

-08

Jun

-08

No

v-0

8

Apr-

09

Se

p-0

9

Feb-1

0

Jul-10

Dec-1

0

May

-11

Oct-

11

Mar-

12

Au

g-1

2

Jan

-13

Jun

-13

Nov-1

3

Apr-

14

Se

p-1

4

Feb-1

5

Property investment (3mma)Pre-stressed Concrete - RHSYoY

%

0

50

100

150

200

250

300

350

2000

2002

2004

2006

2008

2010

2012

2014

2016F

2018F

2020F

mil

lio

n to

nn

es

Steel demand in Chinese construction

Industrial

Commercial

Residential

Macquarie Research Commodities Comment

3 August 2015 15

Increasing China’s production clearly has an impact on the global steel market – essentially

production expectations elsewhere have to drop, all other things being equal. Given the sustained

period of low steel industry margins expected over the coming years, we have essentially removed

any growth plans from the model from everywhere except India (where we have pared back

production growth slightly), and moderated capacity creep expectations. Areas like Japan and the

US will also have also seen production held at or below 2015 levels – the former due to China’s

impact on its key export markets and the latter due to a general lack of domestic industry

competitiveness amid dollar strength.

Fig 3 The growing gap between Chinese steel production and consumption...

Fig 4 …has led to net exports over 100mtpa on a crude steel basis, a level we now consider sustainable

Source: NBS, Mysteel, CISA, Macquarie Research, July 2015 Source: China Customs, Macquarie Research, July 2015

While China is set to remain over 50% of global production, on our new modelling it never reaches

50% of steel consumption. Indeed, India and other Asian countries are set to become the new

growth engines for the global steel economy. For 2014-2020, we now expect a global demand

CAGR of 0.7%, but following the 2.3% drop in the current year, this means a 1.3% CAGR from this

point forward. In terms of China, the equivalent 2014-2020 CAGR is zero, but post the 3.7% fall this

year the CAGR is 0.7%, with autos and machinery gains offsetting construction losses. Meanwhile,

we have India growing at a 7.5% CAGR – far and away the best among major economies.

Developed world consumption is essentially flat – there is some upside risk here should we see a

construction and infrastructure rebound, but given the fiscal pressures on many economies, these

would likely have to be private sector-led rather than getting government kickers.

Fig 5 China’s steel consumption is in the ‘peaking out’ phase...

Fig 6 …with India and other Asian countries now set to be the larger growth driver

Source: worldsteel, NBS, Macquarie Research, July 2015 Source: worldsteel, NBS, Macquarie Research, July 2015

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

Jan-13 Jan-14 Jan-15

YoY change in Chinese steel production and consumption

Real Demand Steel production-40

-20

0

20

40

60

80

100

120

140

160

Ja

n-0

6

Ma

y-0

6

Se

p-0

6

Ja

n-0

7

Ma

y-0

7

Se

p-0

7

Ja

n-0

8

Ma

y-0

8

Se

p-0

8

Ja

n-0

9

Ma

y-0

9

Se

p-0

9

Ja

n-1

0

Ma

y-1

0

Se

p-1

0

Ja

n-1

1

Ma

y-1

1

Se

p-1

1

Ja

n-1

2

Ma

y-1

2

Se

p-1

2

Ja

n-1

3

Ma

y-1

3

Se

p-1

3

Ja

n-1

4

Ma

y-1

4

Se

p-1

4

Ja

n-1

5

Ma

y-1

5

Ch

ine

se s

teel t

rad

e, c

rud

e b

asis

, an

nu

alis

ed, m

t

Chinese steel exports

Imports Exports Net Exports

414 273 344 366 360 360 381 377 381 381 378 374 370

473

529

607 655 675 729 756 728 735 739 747 752 755

450

386

451 483 494

496 503 497 514 531 548 565 583

-

100

200

300

400

500

600

700

800

900

1,000

1,100

1,200

1,300

1,400

1,500

1,600

1,700

1,800

1,900

2008

2009

2010

2011

2012

2013

2014e

2015f

2016f

2017f

2018f

2019f

2020f

mil

lio

n to

nn

es

Crude steel consumption

Developed China Emerging Markets

(10)

(5)

-

5

10

15

20

25

30

35

40

Ch

ina

Jap

an

Ind

ia

Oth

er A

sia

US

A

Latin

Am

eri

ca

Weste

rn E

uro

pe

CIS

Oth

er

million to

nnes

Change in steel consumption, 2020 vs. 2015

Macquarie Research Commodities Comment

3 August 2015 16

With a relatively negligible growth rate now projected for steel production, and the available scrap

pool continuing to grow, global blast furnace iron output is in an even more challenging situation

than steel. The leverage to China has been a benefit (and may well be again next year), but we

are now looking at global production of 1,220mt in 2014 marking the peak for the foreseeable

future, and have global pig iron production 40mt lower than this by the end of the decade.

Certainly, the scrap element does give some uncertainty to these forecasts, given that basic

oxygen furnace steel mills have a certain degree of flexibility to substitute between produced pig

iron and purchased scrap. The fixed asset element of the blast furnace and associated facilities

(sinter plant, coke ovens) also add a layer of complexity.

Presently, the equation is very much in favour of making pig iron using purchased raw materials to

the greatest extent possible. This has the potential to delay the scrap cycle; however, we do tend

to consider scrap inelastic in the long run such that any reprieve for pig iron output is likely to be a

temporary one.

Fig 7 Macquarie global steel production and consumption

Source: worldsteel, NBS, Macquarie Research, July 2015

Peak pig iron output naturally means increased challenges for raw materials. Not least, the

contestable iron ore market has hit saturation point, and is now in the ‘peaking out’ phase which

had previously been projected for nearer the end of the decade.

With Chinese domestic iron ore, having already lost ~100mtpa over the past two years, now

reaching the minimum expected volume, falling blast furnace output now means falling imports.

This will be gradual rather than a collapse, but after over 20 years of consecutive growth –

including 2008 and 2009 – is in itself a significant market event.

Steel Consumption - Crude Steel Basis (million tonnes) CAGR

2013 2014 2015f 2016f 2017f 2018f 2019f 2020f 2014-2020

China 729 756 728 735 739 747 752 755 0.7%

Japan 69 72 69 70 70 70 70 70 -0.5%

India 78 80 86 93 100 107 115 124 7.5%

Other Asia 152 158 155 161 166 169 173 176 1.8%

USA 105 117 114 114 114 112 110 108 -1.3%

Latin America 81 86 82 84 86 88 90 91 1.0%

Western Europe 169 173 177 178 178 177 175 173 0.0%

CIS 78 70 66 68 69 70 72 73 0.8%

Other 125 128 127 127 129 132 135 138 1.2%

Total World 1585 1640 1602 1630 1652 1672 1692 1708 1.3%

World, Ex-China 857 884 874 895 912 926 939 953 1.3%

Crude Steel Production (m tonnes) CAGR

2013 2014 2015f 2016f 2017f 2018f 2019f 2020f 2014-2020

Japan 111 111 105 104 104 104 100 100 -1.7%

China 789 839 841 849 842 849 855 858 0.4%

India 81 87 92 97 102 107 112 117 5.1%

Other Asia 102 109 106 106 110 113 113 113 0.5%

North America 119 121 111 113 113 112 112 111 -1.4%

Western Europe 179 180 177 179 180 180 181 181 0.1%

Brazil 34 34 34 35 35 35 35 36 0.8%

South/Central America 12 11 10 10 10 11 11 11 -0.8%

CIS 108 106 101 103 103 104 104 105 -0.2%

Other 81 83 84 84 84 85 85 86 0.5%

Total World 1617 1681 1661 1679 1683 1700 1708 1716 0.3%

World Ex-China 827 842 820 830 841 850 852 859 0.3%

China share 48.8% 49.9% 50.6% 50.5% 50.0% 50.0% 50.1% 50.0%

Macquarie Research Commodities Comment

3 August 2015 17

Fig 8 Peak pig iron is set to mean falling Chinese imports...

Fig 9 …and with the majors still ramping, continued displacement of marginal capacity

Source: Customs Statistics, NBS, Macquarie Research, July 2015 Source: Customs Statistics, NBS, Macquarie Research, July 2015

With the majors (BHP, Rio, Vale, FMG, Anglo and Roy Hill) continuing to grow output, the

pressure will continue to bear on marginal players to make way. Under our previous forecasts,

limited displacement was required from 2017 onwards, with growth from the majors matching

overall demand growth. With blast furnace output in a downtrend, even without growth from the

majors we will need displacement, and with the growth between 60-80mt will be required each

year through 2019 – not a pleasant environment for any iron ore producer.

Fig 10 Macquarie iron ore balance – more displacement to come

Source: worldsteel, Customs Statistics, Macquarie Research, July 2015

0

200

400

600

800

1000

1200

1400

1600

1800

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015f

2016f

2017f

2018f

2019f

Destination of contestable iron ore supply

China imports

China domestic

Ex-China imports

0

100

200

300

400

500

600

700

800

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15F

4Q

15F

1Q

16F

2Q

16F

3Q

16F

4Q

16F

1Q

17F

2Q

17F

3Q

17F

4Q

17F

1Q

18F

2Q

18F

3Q

18F

4Q

18F

Supply required ex-majors, mtpa

million tonnes

Pig iron + DRI production 2013 2014 2015F 2016F 2017F 2018F 2019F

China 716 749 737 743 725 717 707

Ex-China 464 471 466 469 475 480 480

Total 1180 1220 1202 1213 1200 1198 1187

Total ex-China seaborne iron ore demand 2013 2014 2015F 2016F 2017F 2018F 2019F

Europe 119 118 119 121 120 120 120

Japan 134 133 122 122 122 122 117

Korea 66 78 74 74 77 80 80

Other 69 103 114 106 105 106 106

Total 388 432 430 422 425 428 423

Total China iron ore demand 2013 2014 2015F 2016F 2017F 2018F 2019F

China demand 1144 1208 1169 1192 1162 1150 1133

Total iron ore demand (China + ex-China) 1531 1640 1599 1613 1587 1578 1556

Seaborne iron ore supply 2013 2014 2015F 2016F 2017F 2018F 2019F

Total majors 867 1011 1106 1194 1245 1296 1336

YoY 144 95 88 50 51 40

Total variable supply annualised (after disruption) 665 629 492 419 342 282 220

YoY delta (displacement) 71 (36) (137) (73) (77) (60) (62)

Macquarie Research Commodities Comment

3 August 2015 18

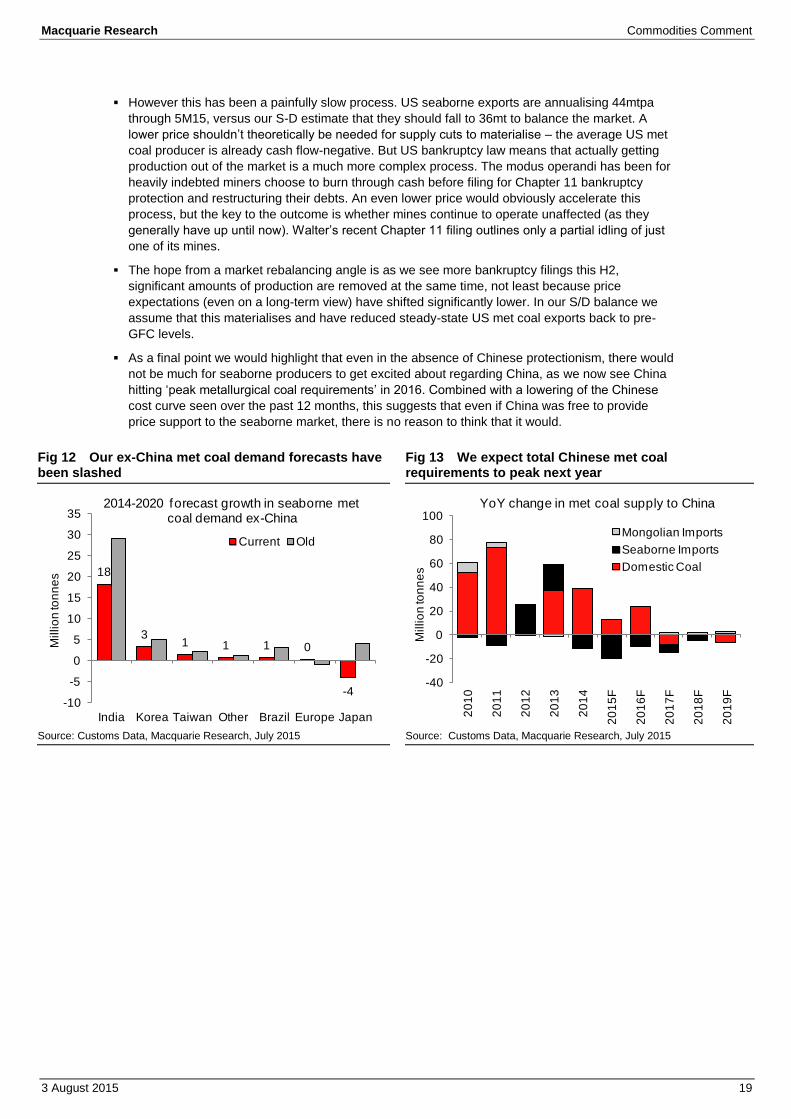

Our pig iron production downgrades also have bearish implications for our seaborne met coal

supply-demand balance, which we have updated below. The key points are as follows:

Ex-China met coal demand growth has been significantly reduced, from +43mt 2014-2020 to

just +20mt 2014-2020. Europe aside, import projections for all major seaborne importers have

been cut. India remains the only source of significant demand growth going forward.

Chinese imports, now a function of protectionist trade policy, have been reduced by 15-20%

from 2015 to 2018. This to reflect current import run-rates, which are below our previous

expectations. In addition, we see China hitting peak ‘metallurgical coal requirements’ in 2016.

The result of the former two points is that US export projections have been slashed. We now

see steady state exports as being under 30mt, versus ~40mt previously.

Fig 11 Metallurgical coal seaborne supply and demand

Source: Customs Data, Macquarie Research, July 2015

Our ex-China demand revisions put into focus just how reliant the seaborne met coal market is

going to be on Indian demand going forward. Unlike thermal coal, where concerns are building

that domestic production could sort itself out to the detriment of imports, Indian domestic met coal

qualities are poor and yields are low. India remains the market’s structural demand growth driver,

albeit our projections are more conservative than before. Meanwhile demand growth from all other

importers is, on our forecasts, going to be more-or-less flat over the next five years.

In previous years, this ‘displaced’ volume may have been able to find a home in China, by ‘pricing

in’. That is no longer possible with Chinese imports now effectively determined by protectionist

policy rather than supply-push, which was the main driver in previous years. New coal quality

standards introduced at the start of this year – trace element inspections in particular – have

helped keep seaborne coal out and the risk is that this protectionism increases further.

The implication is that we will need to see much larger supply cuts than we were previously

assuming, almost all of which we have attributed to the US. There is no disputing that US met coal

producers account for the marginal tonnes in the market and that if economics were to play out

freely, these would be the cuts addressing market oversupply.

Growth

Met coal demand (mt) 2012 2013 2014 2015F 2016F 2017F 2018F 2019F 2020F 2014-2020

Europe 54 53 56 55 56 57 57 57 57 0

Japan 57 57 55 53 53 53 53 51 51 -4

Korea 28 31 33 33 33 35 36 36 36 3

Taiw an 9 10 11 12 12 12 12 12 12 1

China 52 73 62 42 32 25 21 22 21 -41

India 38 40 47 52 54 57 60 62 65 18

Brazil 15 15 19 20 20 20 20 20 20 1

Other 5 9 11 11 11 11 11 11 11 1

Total Demand 258 289 294 277 271 269 269 271 273 -20

% change YoY 7.5% 12.0% 1.7% -5.5% -2.2% -0.7% - 0.6% 0.9%

Growth

Met coal supply (mt) 2012 2013 2014 2015F 2016F 2017F 2018F 2019F 2020F 2014-2020

Australia 145 170 186 188 187 185 183 183 183 -4

Canada 30 34 30 27 27 27 27 27 28 -3

USA 59 57 51 36 30 28 28 28 28 -23

China 1 1 1 1 1 1 1 1 1 -

Russia 10 14 13 13 13 13 13 13 14 1

Other 13 13 13 13 14 16 18 19 20 8-

Total Supply 258 289 294 277 271 269 269 271 273 -20

% change YoY 7.0% 12.0% 1.7% -5.5% -2.2% -0.7% - 0.6% 0.9%

Macquarie Research Commodities Comment

3 August 2015 19

However this has been a painfully slow process. US seaborne exports are annualising 44mtpa

through 5M15, versus our S-D estimate that they should fall to 36mt to balance the market. A

lower price shouldn’t theoretically be needed for supply cuts to materialise – the average US met

coal producer is already cash flow-negative. But US bankruptcy law means that actually getting

production out of the market is a much more complex process. The modus operandi has been for

heavily indebted miners choose to burn through cash before filing for Chapter 11 bankruptcy

protection and restructuring their debts. An even lower price would obviously accelerate this

process, but the key to the outcome is whether mines continue to operate unaffected (as they

generally have up until now). Walter’s recent Chapter 11 filing outlines only a partial idling of just

one of its mines.

The hope from a market rebalancing angle is as we see more bankruptcy filings this H2,

significant amounts of production are removed at the same time, not least because price

expectations (even on a long-term view) have shifted significantly lower. In our S/D balance we

assume that this materialises and have reduced steady-state US met coal exports back to pre-

GFC levels.

As a final point we would highlight that even in the absence of Chinese protectionism, there would

not be much for seaborne producers to get excited about regarding China, as we now see China

hitting ‘peak metallurgical coal requirements’ in 2016. Combined with a lowering of the Chinese

cost curve seen over the past 12 months, this suggests that even if China was free to provide

price support to the seaborne market, there is no reason to think that it would.

Fig 12 Our ex-China met coal demand forecasts have been slashed

Fig 13 We expect total Chinese met coal requirements to peak next year

Source: Customs Data, Macquarie Research, July 2015 Source: Customs Data, Macquarie Research, July 2015

18

31 1 1 0

-4-10

-5

0

5

10

15

20

25

30

35

India Korea Taiwan Other Brazil Europe Japan

Millio

n to

nn

es

2014-2020 forecast growth in seaborne met coal demand ex-China

Current Old

-40

-20

0

20

40

60

80

100

20

10

20

11

20

12

20

13

20

14

20

15

F

20

16

F

20

17

F

20

18

F

20

19

F

Millio

n to

nn

es

YoY change in met coal supply to China

Mongolian Imports

Seaborne Imports

Domestic Coal

Macquarie Research Commodities Comment

3 August 2015 20

Trouble down pit: Copper mines begin to struggle

Amid the swirl of recent price shocks, which have taken copper to six-year lows of below $5,200/t,

the focus has chiefly (and not inappropriately) been on demand and the conditions of the Chinese

economy. However, China’s equity market convulsions aside, news on the fundamentals side for

copper has been mostly more supportive. While last week’s July China flash PMI reading was

weak, June trade data showed imports of concentrate posted another strong uptick, maintaining

an 11% YTD growth figure, while cathodes were relatively flat YoY. Meanwhile, as 2Q production

reports begin to come in revealing a few downgrades and as a raft of disruption stories from Chile,

China, Zambia and PNG begin to filter through, the mining side of the equation has begun to look

shakier. We reiterate our view that a significant proportion of copper mine output is struggling at

these price levels. We set out in the table below the main copper mine disruption news items that

have recently been circulating, with details of any production cuts made as a result.

Fig 1 Latest actual, estimated and potential disruption to copper mine output

Incident Mine/company/

country capacity

Disruption (kt Cu)

Zambia power rationing on low water levels ~0.9Mtpa 25 China mine closures on prices 1.6Mtpa 20 Ok Tedi temporary suspension on lack of rain, prices 100ktpa 10 Codelco contractor strike 2Mtpa 5 Los Bronces/Collahuasi drought and technical problems 0.85Mtpa ? FCX "potential adjustments to mine plans and future copper and molybdenum production volumes to reduce costs"

1.55Mtpa ?

Source: Company reports, media sources, Macquarie Research, July 2015

#8 copper miner (by equity stake) First Quantum Minerals announced the receipt of force

majeure from Zambia’s Zesco power utility on Monday due to low rainfall hampering hydropower

performance, and warned that its Sentinel and Kansanshi mines “are currently operating at

reduced capacities”. Ahead of further clarity in their 2Q15 quarterly production report, due on

Wednesday, we estimate around 10kt loss from Sentinel and 15kt from Kansanshi, to add to our

20kt existing disruption assumption for other Zambian mines due to the power issues.

A trickier estimate concerns China mine output closures. Official sources state that domestic

copper-in-concentrate production is down by 10.1% YTD at 846kt. However, it is our

understanding that on occasion copper-in-concentrate has been confused with copper concentrate

by some reportees, and so treat this data with caution. Our best estimate using other sources

including BGRIMM gives ~1.59Mt total 2014 mined copper output. With concentrates imports of

+11% YTD, only partially accounted for by smelter capacity expansions, we cautiously amend

2015 output from 1.2% growth to flat, removing a further 20kt directly due to price action.

Fig 2 Official sources indicate steep mine cutbacks in China – we estimate, at best, flat mine output

Fig 3 In other countries, early reporting gives weak mine output growth projection of 1.5%

Source: China Customs, NBS, CEIC, Macquarie Research, July 2015 Source: Cochilco, company reports, Macquarie Research, July 2015

0

200

400

600

800

1000

1200

1400

0

50

100

150

200

250China copper-in-concentrate output (kt) vs

concentrate imports (kdmt, RHS)

0

1000

2000

3000

4000

5000

6000

Reported 2014 copper mine output vs 2015 projection from early reports, top 10 countries ex-

China

2014 2015E

-1%

+3%

-5% +7% -8% -11% +7% +37% +2% +19%

Total reports tracked2014: 10.97Mt (57% of total mined Cu)

2015E: 11.13Mt (56% of est. total)+1.5% YoY growth implied

Macquarie Research Commodities Comment

3 August 2015 21

On Tuesday, Ok Tedi Mining Ltd announced a temporary shutdown mainly related to low rainfall,

which has put a stop to concentrate barge shipments down the Fly river to its seaport facilities.

The state-owned PNG miner noted however that it would at this time of production stoppage lay

off 30% of its expatriate workforce and 15% of its nationals, calling the redundancies “essential to

help position OTML to better cope with a low commodity price environment”. We expect the

stoppage to last a few weeks, and have shaved 10kt of production to allow 88kt Cu for 2015. No

further amendments have been made, but we expect this event to add further pressure to the

concentrates market and spot TCRCs, as this mine is a key custom supplier to the Asian smelters.

Noisier but at this stage less impactful for supply have been events at #1 miner Codelco, where a

contractor strike escalated into violent protests, the occupation of the 60ktpa El Salvador mine and

the police shooting of a worker last Friday. Later on Tuesday we learnt that strike action had

spread to the much larger 400ktpa Chuquicamata mine, with the CEO confirming work had

stopped in a statement. As this stage it is difficult to say how impactful these disturbances may be,

and have thus limited disruption estimate to 5kt until we see how the situation develops.

Elsewhere, while we lack the detail to make disruption amendments as yet, we note the warnings

on potential outages from #2 miner Freeport McMoran and #9 miner Anglo American. The

former announced on Tuesday a “comprehensive review of operating plans” which will

“incorporate potential adjustments to mine plans and future copper and molybdenum production

volumes to reduce costs and preserve valuable resources for anticipated improved market

conditions in the future”. Details of the review are expected this quarter, and may entail shutdowns

and/or curtailments, with the smaller Arizona mines most likely to be at risk given their size versus

the rest of the portfolio, lack of currency advantage (being based in the US) and FCX’s past

behaviours at these operations during times of low prices. For Anglo, the main problem is water

and the lack thereof. Drought conditions have begun to hamper output at Los Bronces, though the

company had made allowances for this in 2015 guidance and so no unexpected disruptions have

resulted. We identify this as a key risk going forward, however, with the company stating that “full

year production remains partially dependent on weather conditions in the second half”.

Meanwhile, some interest has been stirred up by #4 miner BHP Billiton’s announcement that

group copper output will fall to 1.5Mt in the financial year to June 2016, from 1.7Mt in Financial

Year 2015, but we point out that the company warned of significant grade declines at Escondida at

the end of 2015, thus we have not made a fresh downward revision due to their recent guidance.