© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

Global Propylene Market

Motivated to Change

Chuck Carr, IHS Senior Director - Propylene

September, 2014

IHS Asia Chemical Conference

Singapore

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

Global Propylene Market

• The “Big Picture” and what is motivating the

changes

• China continues to strive towards self

sufficiency

• North America NGL’s impact supply

• Overbuild on the horizon…..prices forecast to

weaken

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

Global Propylene Market

• The “Big Picture” and what is motivating the

changes

• China continues to strive towards self

sufficiency

• North America NGL’s impact supply

• Overbuild on the horizon…..prices forecast to

weaken

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

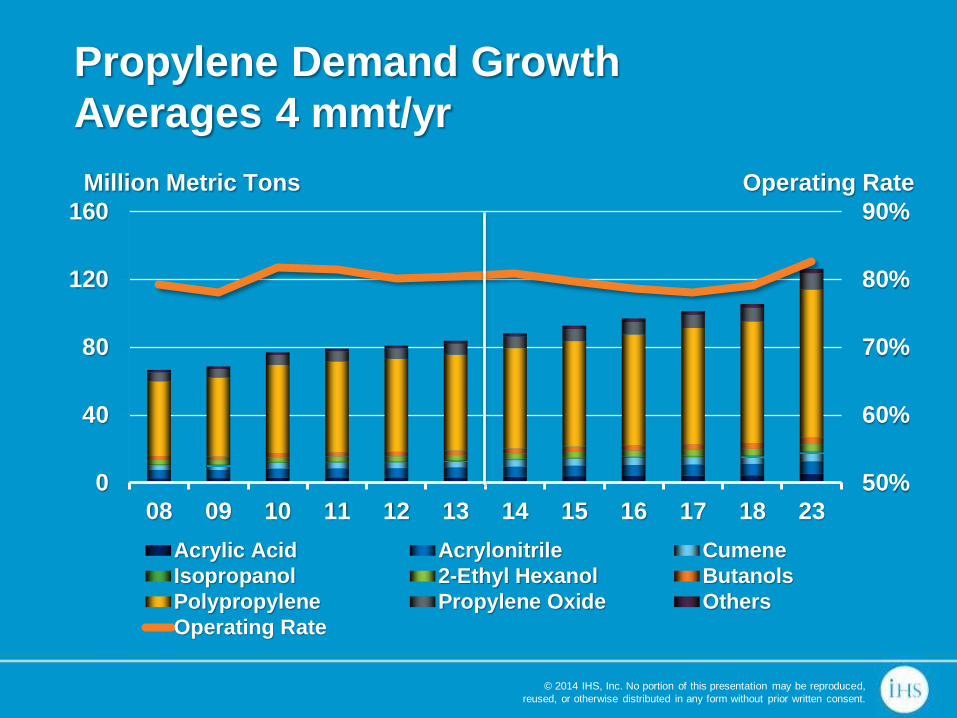

Propylene Demand Growth

Averages 4 mmt/yr

50%

60%

70%

80%

90%

0

40

80

120

160

08 09 10 11 12 13 14 15 16 17 18 23

Acrylic Acid Acrylonitrile Cumene

Isopropanol 2-Ethyl Hexanol Butanols

Polypropylene Propylene Oxide Others

Operating Rate

Operating Rate Million Metric Tons

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

Stm. Crackers

55%

FCC Splitters

31%

Dehydro 5%

Metathesis 4%

HS FCC 3%

Others On-Purpose

1%

Coal /Methanol

To Olefins 1%

Stm. Crackers

46%

FCC Splitters

25%

Dehydro 13%

Metathesis 4%

Methanol to Olefins

2%

Coal to Olefins

5% Coal to

Propylene 1%

HS FCC 3%

Others On-Purpose

1%

Capacity Additions….PDH and CTO

Lead the On-Purpose Wave

2013 2018

Doubling On-Purpose Capacity

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

50

60

70

80

90

0

10

20

30

40

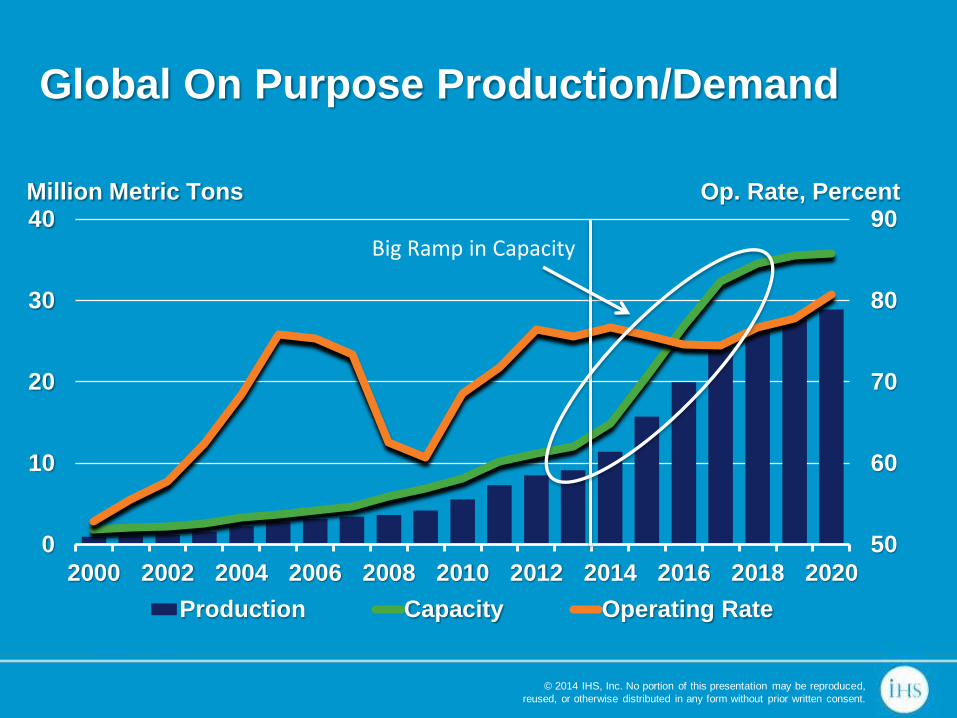

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Production Capacity Operating Rate

Million Metric Tons Op. Rate, Percent

Global On Purpose Production/Demand

Big Ramp in Capacity

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

Cumene 40%

Oligomers 40%

IPA 20% Total World Propylene 2020+

Refinery

FCC/Coker

Steam

Crackers

On-Purpose

30% – 35%

40% - 45%

25% - 30%

LPG/Fuel 35%

Polygas/ Dimersol

15%

Alkylation 50%

Metathesis 11%

PDH 43% Olefin

Cracking 1%

Via Methanol

30%

HS FCC 14%

Others On-Purpose

1%

Fuels 24% Direct

8%

Splitters 68%

Acrylic

Acid 4%

Acrylonitrile 6% Cumene

4%

Isopropanol

1%

2-Ethyl

Hexanol 3%

Butanols

3%

Propylene

Oxide 8%

Others

2%

Polypropylene

69%

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

Global Propylene Market

• The “Big Picture” and what is motivating the

changes

• China continues to strive towards self

sufficiency

• North America NGL’s impact supply

• Overbuild on the horizon…..prices forecast to

weaken

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

0

25

50

75

100

125

150

08 09 10 11 12 13 14 15 16 17 18 23

N. America S. America W. Europe C. Europe CIS & Baltics

Africa Middle East Indian Subc. NE Asia SE Asia

Million Metric Tons

Asia Leads Demand Growth…..

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

China’s Propylene Self-Sufficiency is

Rapidly Improving

0

10

20

30

40

50

60

70

80

90

100

0

10

20

30

40

50

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Production Net Equivalent Import (Export) Self-sufficiency

Million Metric Tons Percent, %

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

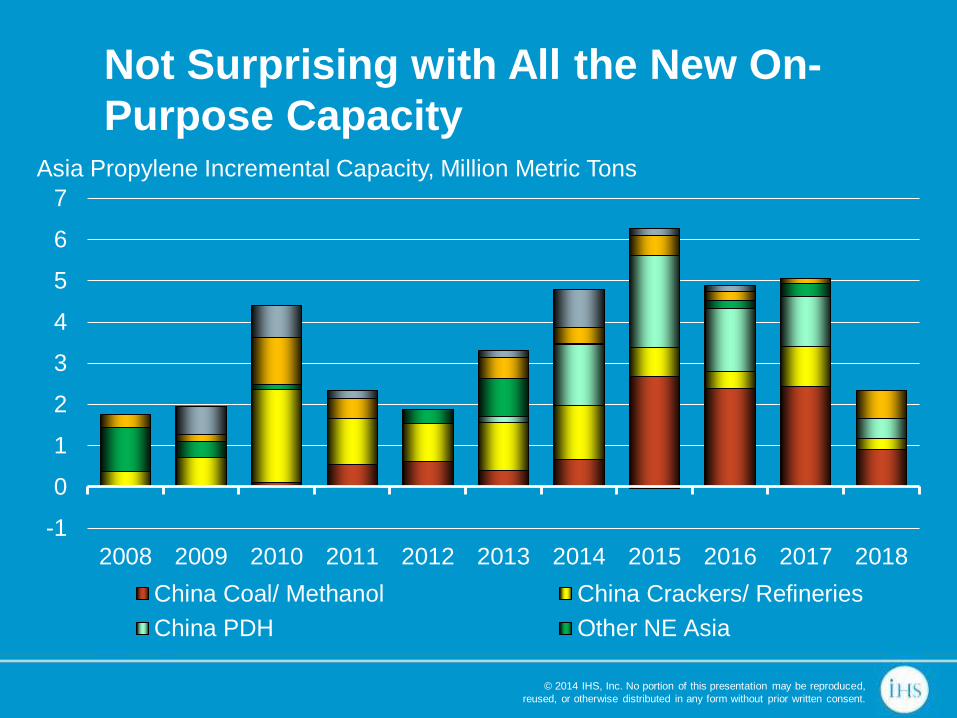

Not Surprising with All the New On-

Purpose Capacity

-1

0

1

2

3

4

5

6

7

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

China Coal/ Methanol China Crackers/ Refineries

China PDH Other NE Asia

Asia Propylene Incremental Capacity, Million Metric Tons

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

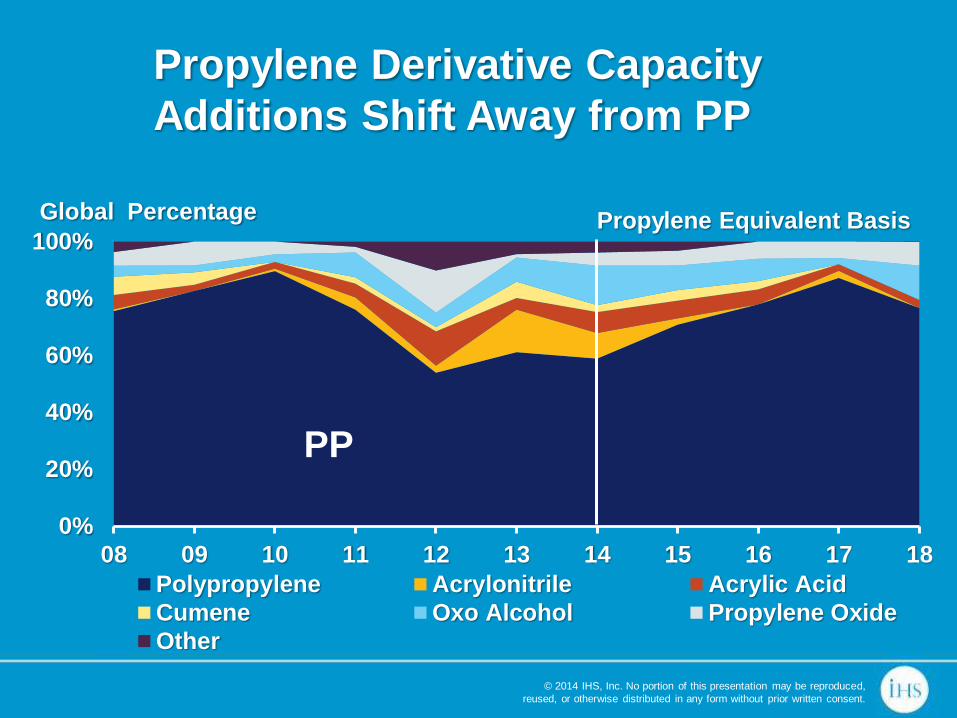

Propylene Equivalent Basis

Propylene Derivative Capacity

Additions Shift Away from PP

0%

20%

40%

60%

80%

100%

08 09 10 11 12 13 14 15 16 17 18

Polypropylene Acrylonitrile Acrylic Acid

Cumene Oxo Alcohol Propylene Oxide

Other

PP

Global Percentage

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

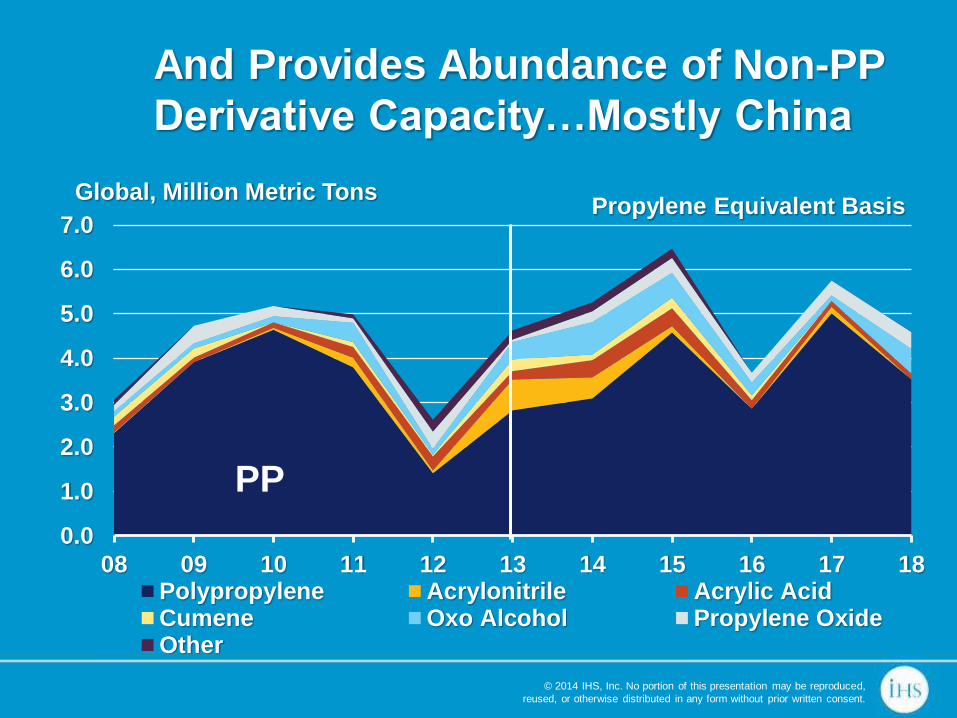

08 09 10 11 12 13 14 15 16 17 18Polypropylene Acrylonitrile Acrylic AcidCumene Oxo Alcohol Propylene OxideOther

PP

Propylene Equivalent Basis

And Provides Abundance of Non-PP

Derivative Capacity…Mostly China

Global, Million Metric Tons

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

Global Propylene Market

• The “Big Picture” and what is motivating the

changes

• China continues to strive towards self

sufficiency

• North America NGL’s impact supply

• Overbuild on the horizon…..prices forecast to

weaken

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

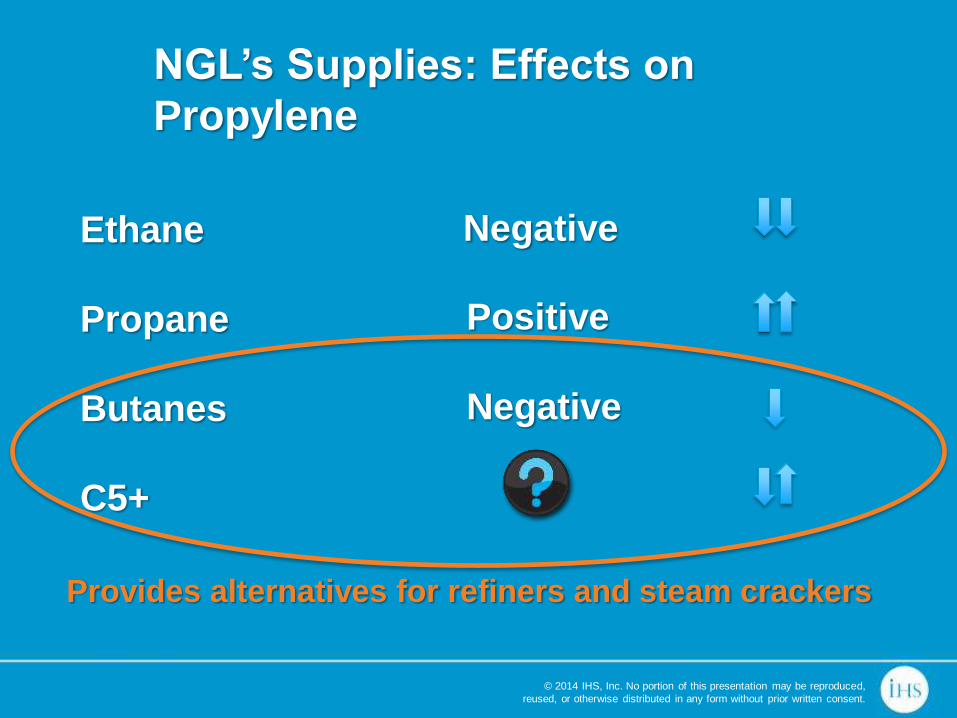

Ethane

Propane

Butanes

C5+

Provides alternatives for refiners and steam crackers

NGL’s Supplies: Effects on

Propylene

Negative

Positive

Negative

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

North America Propane Abundance

Supports Global PDH Additions

0

500

1,000

1,500

2,000

2,500

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

MBPD

Domestic Exports

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

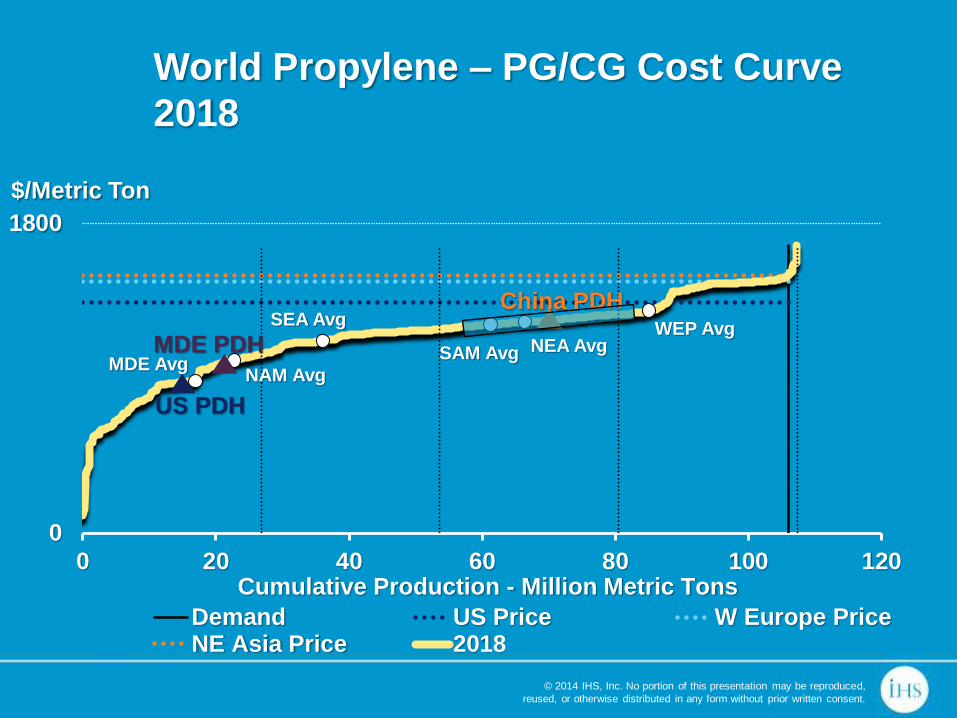

MDE Avg NAM Avg

NEA Avg SAM Avg

SEA Avg WEP Avg

0

1800

0 20 40 60 80 100 120

$/Metric Ton

Demand US Price W Europe PriceNE Asia Price 2018

Cumulative Production - Million Metric Tons

US PDH

MDE PDH

China PDH

World Propylene – PG/CG Cost Curve

2018

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

0

2205

0

100

95 98 01 04 07 10 13 16 19 22

Alky Alternative Value Spot Refinery Grade

Contract Polymer Grade

Dollars Per Metric Ton Cents Per Pound

US Propylene Prices Stay

Discounted Versus Alky Alternatives

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

0

5

10

15

20

25

0

20

40

60

80

100

02 J 03 J 04 J 05 J 06 J 07 J 08 J 09 J 10 J 11 J 12 J 13 J 14 J 15 J

Margin RG Wtd Avg Acq (Estimated)

PG Benchmark Contract

Price, Cents Per Pound Margin

Margin Gain by Splitters

Propylene Splitter Margin – More

Motivation for Refiners

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Return on Investment for an Alky Unit in US

ROI @ $75 Million ROI @ $150 Million ROI @ $225 Million

Propylene Alkylation Economics

Revived – Will Refiners Invest?

0%

+

_

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

Global Propylene Market

• The “Big Picture” and what is motivating the

changes

• China continues to strive towards self

sufficiency

• North America NGL’s revive supply

• Overbuild on the horizon…..price forecast

weakens

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

-8.0

-4.0

0.0

4.0

8.0

12.0

90 92 94 96 98 00 02 04 06 08 10 12 14 16 18

Million Metric Tons

North America Middle EastChina West EuropeOthers Other AsiaAnnual Demand Increase

Capacity Overwhelms

Anticipated Demand Growth

Global Propylene Capacity Additions

Versus Demand Growth

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

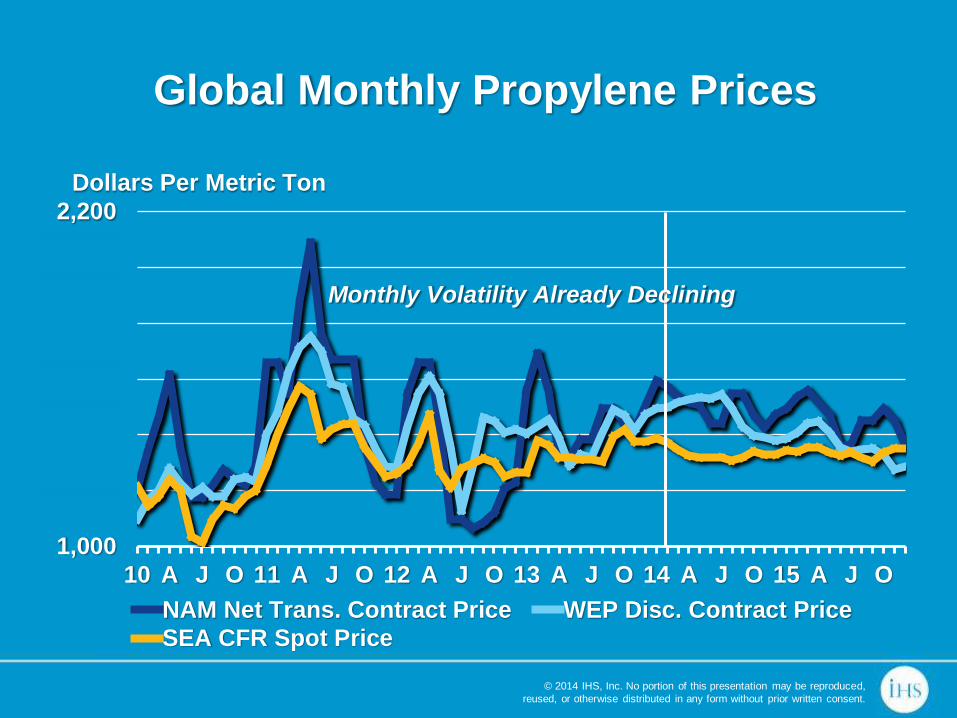

1,000

1,200

1,400

1,600

1,800

2,000

2,200

10 A J O 11 A J O 12 A J O 13 A J O 14 A J O 15 A J O

NAM Net Trans. Contract Price WEP Disc. Contract Price

SEA CFR Spot Price

Dollars Per Metric Ton

Monthly Volatility Already Declining

Global Monthly Propylene Prices

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

Global Propylene Net Equivalent

Trade Contracts With the Overbuild

-15.0

-12.0

-9.0

-6.0

-3.0

0.0

3.0

6.0

9.0

12.0

15.0

08 09 10 11 12 13 14 15 16 17 18 23

North America West Europe Middle East Asia (Ex China) China

Net Imports

Net Exports

Million Metric Tons

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

0.5

0.7

0.9

1.1

1.3

1.5

0.5

0.7

0.9

1.1

1.3

1.5

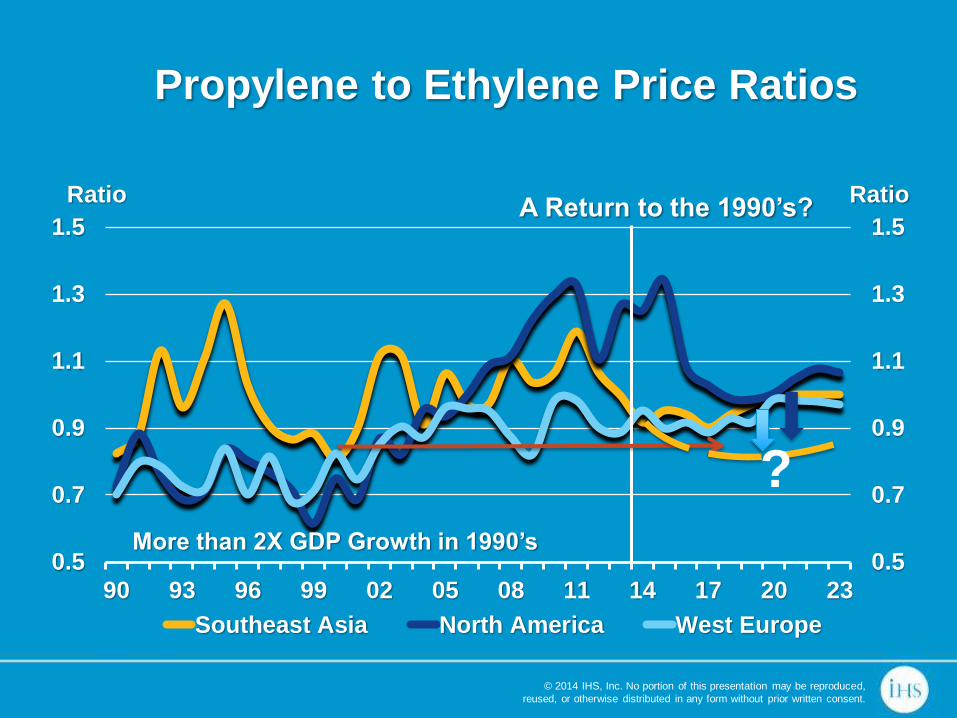

90 93 96 99 02 05 08 11 14 17 20 23

Ratio Ratio

Southeast Asia North America West Europe

?

Propylene to Ethylene Price Ratios

More than 2X GDP Growth in 1990’s

A Return to the 1990’s?

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

-5.0

-3.0

-1.0

1.0

3.0

5.0

7.0

90 92 94 96 98 00 02 04 06 08 10 12 14 16 18 20 22

Average GDP

Elasticity from 1990-

99'= 2.14

Average GDP

Elasticity from

2000-07 = 1.58

Forecast GDP

Elasticity from

2010-17 = 1.55

Forecast

GDP

Elasticity

from

2018-23=1.15

World PG/CG Propylene GDP

Elasticity

Could Get a Boost from Weaker Prices

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

0

1,800

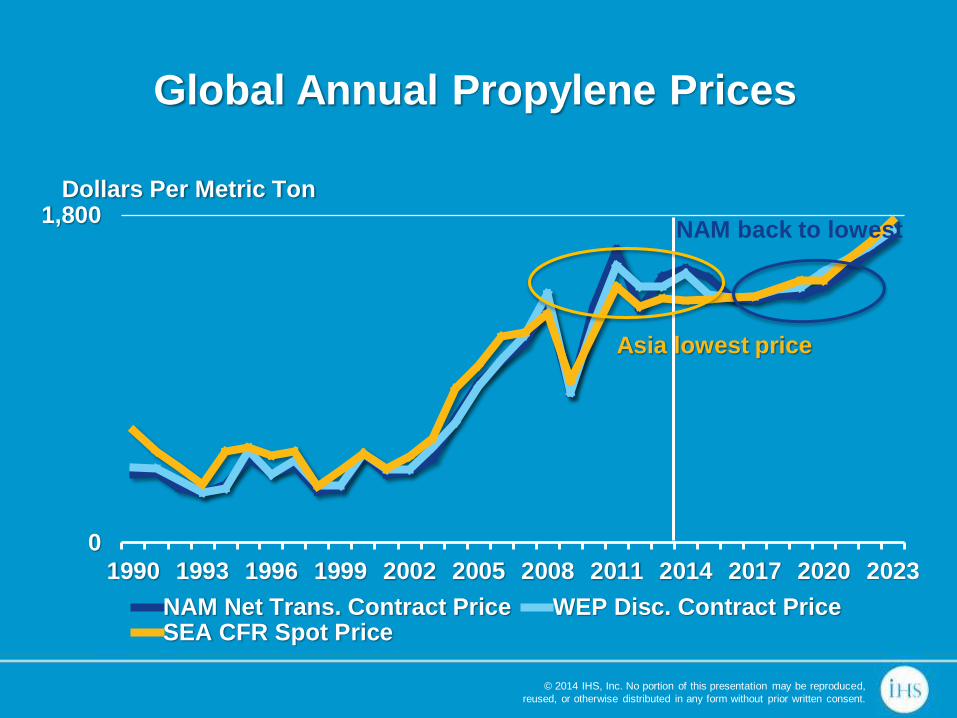

1990 1993 1996 1999 2002 2005 2008 2011 2014 2017 2020 2023

NAM Net Trans. Contract Price WEP Disc. Contract PriceSEA CFR Spot Price

Dollars Per Metric Ton

NAM back to lowest

Asia lowest price

Global Annual Propylene Prices

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

Conclusions

• Propylene demand growth could get a boost if

oversupply of propylene and propylene

derivatives significantly weakens prices

• Abundance of North America NGL’s will provide

a mixed impact on propylene supply

• On-purpose will continue to be the growth

engine for propylene supply. Could methane

based propylene via methanol could be the next

wave

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

Thank You