Saudi Aramco: Company General Use

Global Techno-Economic Trends for Solar PV and Relevance for MENA 22 January 2016: American University of Beirut

Peter Durante: Division Head – New & Emerging Technology + Market Intelligence Team Saudi Aramco’s Power Systems Renewables Department

2

Saudi Aramco: Company General Use

Photovoltaics (PV): Scalability and versatility From the smallest to largest plants, and to every corner of the world & beyond

3

Saudi Aramco: Company General Use

Global Installation Trends – GWp Net Additions by Tech

-50,000.00

0.00

50,000.00

100,000.00

150,000.00

200,000.00

250,000.00

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Marine

Geothermal

Biomass & Waste

Solar

Wind

Hydro

Gas

Coal

Oil

Nuclear

Data source: BNEF 2015, subscriber database

4

Saudi Aramco: Company General Use

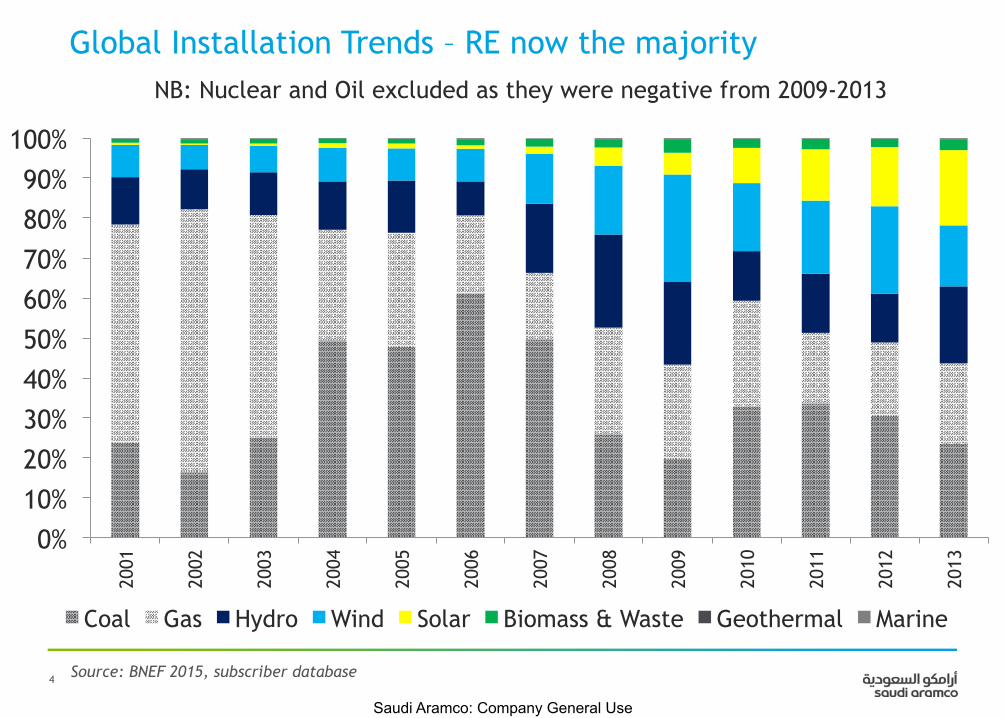

Global Installation Trends – RE now the majority

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

100% 20

01

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

NB: Nuclear and Oil excluded as they were negative from 2009-2013

Coal Gas Hydro Wind Solar Biomass & Waste Geothermal Marine

Source: BNEF 2015, subscriber database

5

Saudi Aramco: Company General Use

Global Installation Trends – Solar’s share growing

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

% of Total Renewable Energy Capacity Additions by Technology Data Source: BNEF 2015

Marine

Geothermal

Biomass & Waste

Solar

Wind

Hydro

Data source: BNEF 2015, subscriber database

6

Saudi Aramco: Company General Use

Solar Cell Price Decline in Perspective

• Importance of up to date market intelligence.

99% Cost reduction since 1976

-85% since 2008

7

Saudi Aramco: Company General Use

Evolution of Wind and PV LCOE

8

Saudi Aramco: Company General Use

LCOE (Levelized Cost of Energy) Comparison Unsubsidized cost of energy comparison ($/MWh)

Source : Lazard's Levelized Cost of Energy Analysis—Version 9.0 (2015)

DEWA PV PPA = $0.0584/kWh Jordan PV PPAs = $0.061-0.077/kWh

Egyptian Wind PPA ~ $0.04/kWh – 2015 Moroccan Wind PPA ~$0.031/kWh - 2016

9

Saudi Aramco: Company General Use

Costs (and capacity) – What was previously seen as overly optimistic now seems prescient or even conservative

2009

Installed capacity at end-2014 = +180GW

Utility PV cost:

PPA awarded for $0.0584/kWh by DEWA in early 2015

for 2016/7 first power

Other utility PPAs from $0.061-0.085 globally

10

Saudi Aramco: Company General Use

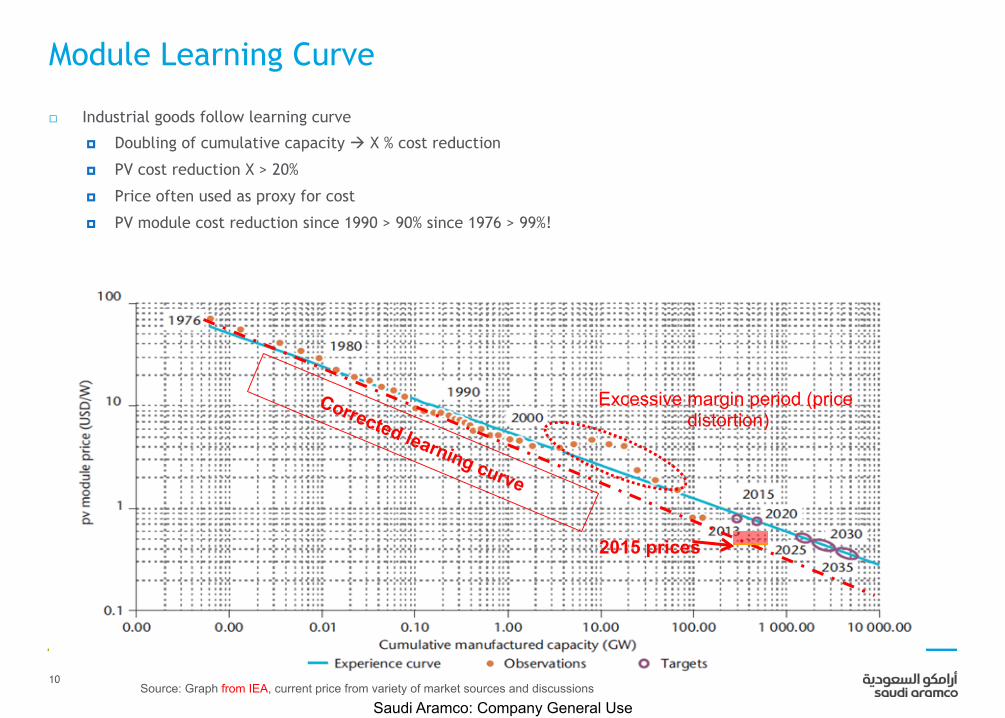

! Industrial goods follow learning curve

! Doubling of cumulative capacity " X % cost reduction

! PV cost reduction X > 20%

! Price often used as proxy for cost

! PV module cost reduction since 1990 > 90% since 1976 > 99%!

Module Learning Curve

Excessive margin period (price distortion)

Source: Graph from IEA, current price from variety of market sources and discussions

2015 prices

11

Saudi Aramco: Company General Use

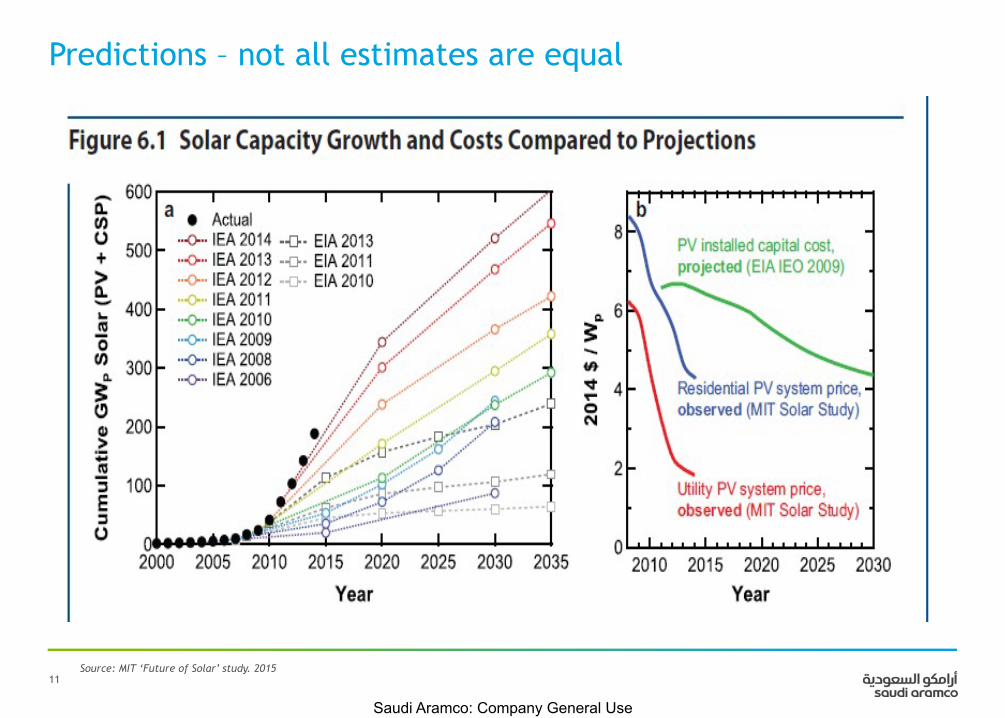

Predictions – not all estimates are equal

Source: MIT ‘Future of Solar’ study. 2015

12

Saudi Aramco: Company General Use

PV & Wind – leading growth in the energy sector

Source: New energy outlook 2015, Bloomberg New Energy Finance Note: ‘Other Renewables’ = hydro, geothermal, biomass, solar thermal, marine and ‘flexible capacity’ (storage, demand response, etc.) Note: Solar Thermal (CSP) remains less than 1% of installed capacity by 2040 Note: Energy from solar + wind in this forecast = 30% of global total

2012 Fossil Fuel

Nuclear

Other Renewables

Wind

Solar PV

2040

Technology 2012 GW 2040 GW Growth Solar PV 101 3,687 36.5 X

Wind 282 2,033 7.2 X

Other Renewables 1,235 2,572 2.1 X

Coal 1,800 2,310 1.3 X

Nat Gas 1,472 2,448 1.7 X

Oil 359 320 0.9 X

Nuclear 336 533 1.6 X

13

Saudi Aramco: Company General Use

Predictions within top clean-tech analysts also vary (2020 annual installs – 135GW or 80GW?)

Data source: BNEF 2015 New Energy Outlook Data source: GTM 2020 Outlook

14

Saudi Aramco: Company General Use

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2010 2015 2020 2025 2030 2035 2040 2045 2050

GW

cum

mul

ativ

e in

stal

lati

on

Year

BNEF

Agora low

Agora high

IEA (hi-Ren Scenario)

UBSe

Forecasts of Global Installed PV Capacity

15

Saudi Aramco: Company General Use

Cost Reduction Drivers

• Modules

- Efficiency

- Cheaper material

- Less material

- Optimized production

- (Disruptive technology)

• Inverter

- Power Electronics

- Mass production

- Dematerialization

• BOS

- Standardization

- Optimization

- Functional integration

• Installation

- Automation

- Pre-assembly

- Optimization

• Energy

- Higher specific yield

• Financing

- Bankability

- Relative WACC

• O&M

- Automation

- Remote sensing

16

Saudi Aramco: Company General Use

Efficiency is on the Rise - Examples

• Top 10 manufacturer.

• Multi-crystalline Silicon

! Top thin film manufacturer.

! CdTe

11.6%

2011

15.6%**

2015

15.9%*

2011

19.1%*

2015

* Best module, ** best production line (average Q1 2015 at 14.6%)

17

Saudi Aramco: Company General Use

Efficiency Drives Cost Down Beyond Module

• Increased module efficiency :

" Less Material (to build module)

" Less land

" Less civil works

" Less racking

" Shorter cabling

" Less work

Source data: ITRPV and BNEF

18% 15%

8% 10%

32% 26%

12%

12%

8%

7%

16%

13%

7%

6%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

current (15%) next (18%)

Effect of cell efficiency increase

Ground

Mounting

Wiring

Inverter

Module assembly

Cell conversion

Wafer

-11%

Efficiency increase largely justifies a higher cell cost. Example: Cell cost +25% à System cost -11%

18

Saudi Aramco: Company General Use

Efficiency is on the Rise: Expansions have higher efficiency 2011 market ≈30GW * 50% " 15 GW

2015 market ≈50GW * 30% " 15 GW

# (Entire) 20GW growth from advanced concepts!

Source: GTM Research

19

Saudi Aramco: Company General Use

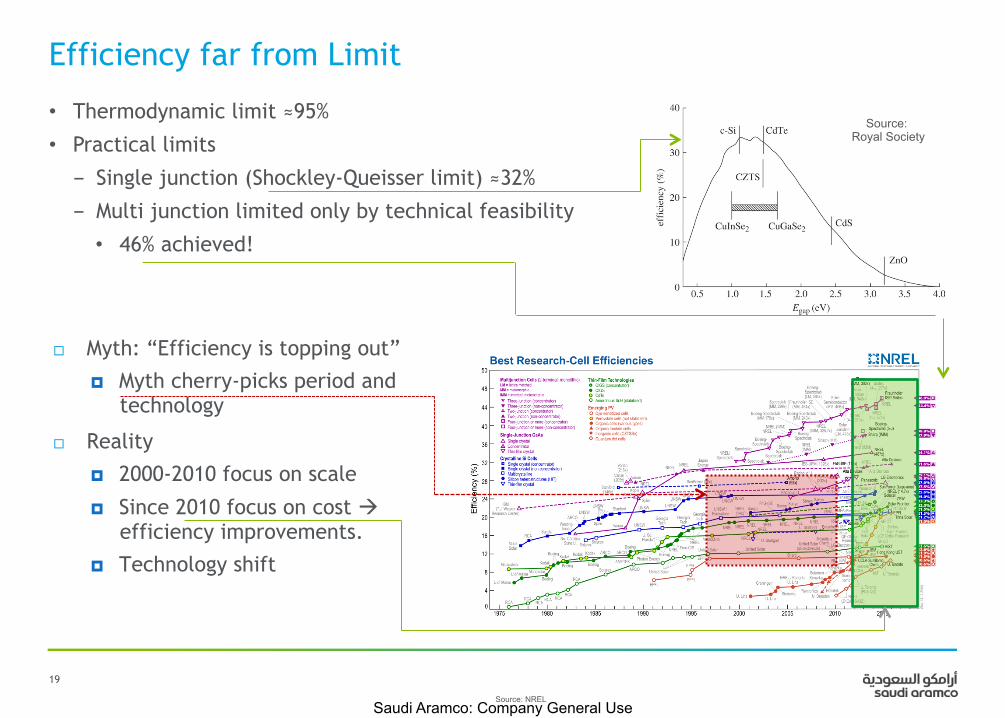

Efficiency far from Limit

• Thermodynamic limit ≈95%

• Practical limits

- Single junction (Shockley-Queisser limit) ≈32%

- Multi junction limited only by technical feasibility

• 46% achieved!

Source: NREL

Source: Royal Society

! Myth: “Efficiency is topping out”

! Myth cherry-picks period and technology

! Reality

! 2000-2010 focus on scale

! Since 2010 focus on cost " efficiency improvements.

! Technology shift

20

Saudi Aramco: Company General Use

8%

12%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

current (15%) 2050 (30%)

Ground

Mounting

Wiring

Inverter

Module assembly

Cell conversion

Wafer

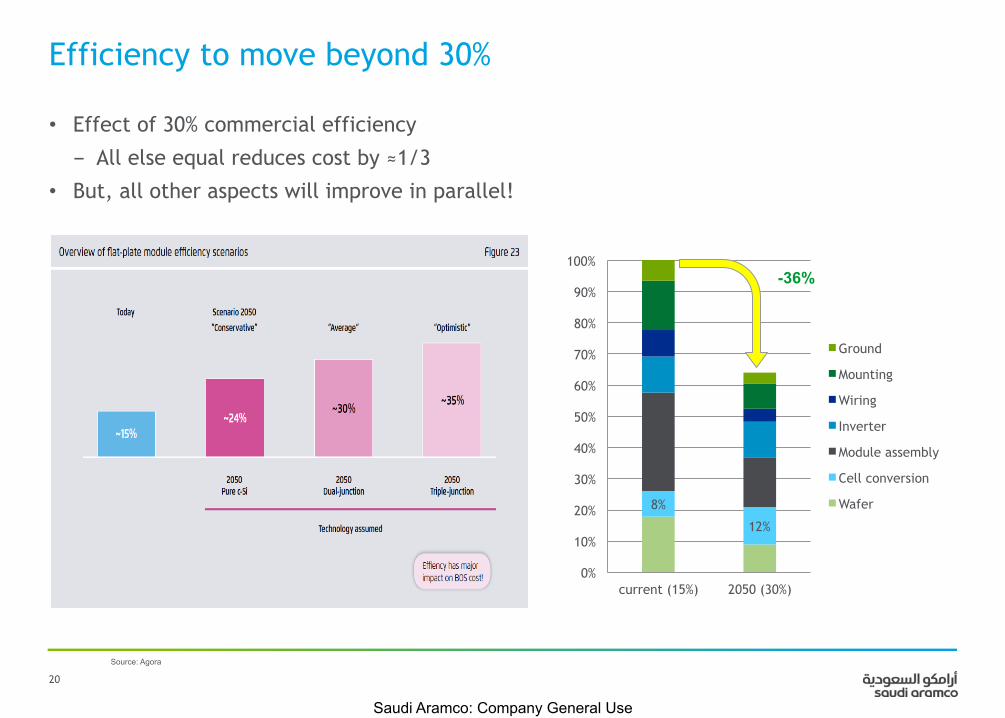

Efficiency to move beyond 30%

• Effect of 30% commercial efficiency

- All else equal reduces cost by ≈1/3

• But, all other aspects will improve in parallel!

Source: Agora

-36%

21

Saudi Aramco: Company General Use

Inverter Learning Curve

• Similar price decline as for PV modules

• Increased power density (dematerialization)

• Road free to further >2/3 cost reduction

Source: Agora

1995 2005 2014

25kg/kW 10.5kg/kW 2.4kg/kW

22

Saudi Aramco: Company General Use

Balance of System Cost is Declining

• BOS cost can be improved considerably.

- Rail-less, automation, functional integration, pre-assembly, standardization, etc.

Source: Agora

23

Saudi Aramco: Company General Use

Expect disruption

• Forecasts assume:

- No technology breakthrough

- Incremental improvements only

• “Disruptive” events likely in next 35 years

- 3RD Generation PV (i.e. Perovskites)

- Roll-to-roll coating

- Default building material (no more racking cost)

- Cheap storage " >4 time larger PV market potential (learning curve " ≈1/3 cost reduction)

- Fully automated installation

- Fully automated cleaning

- Commercial efficiencies beyond 30%

- …

24

Saudi Aramco: Company General Use

Thank you…

25

Saudi Aramco: Company General Use

• Bloomberg New Energy Finance:

- New Energy Outlook 2015

• Agora Energiewende ‘Current and Future Cost of Solar Photovoltaics’ (2015)

• Lazard’s Levelized Cost of Energy 9.0 (2015)

• MIT Energy Institute: Future of Solar Energy (2015)

• GTM Research Global PV Demand Outlook 2015-2020 (2015)

• US National Renewable Energy Lab – National Center for Photovoltaics

• IHS

• UBS Research

Key Sources: