Download - Home Buyers Guide Standard Bank

Home loans

Home owner’s manual

3

Index

Chapter 1 – Introduction 5

Chapter 2 – Housing finance 5

• Keystepstobuyingahome 5

• Roleplayersinthehomebuyingprocess 8

• Whereareyouintheprocess? 9

Chapter 3 – Affordability and budgeting 10

• Affordabilityisveryimportant 10

• Yourbudget 10

• Incomeandexpenditureguide 10

• Howtoimproveyouraffordability 11

Chapter 4 – Costs and expenses 12

• Thecostswhenyoutakeahomeloanfromus 12

• Theexpensesyouwillhaveasahomeowner 13

Chapter 5 – Things to know about a home loan 15

• General 15

• Rightsandobligations 17

• 10questionstoaskyourattorney 18

Chapter 6 – Contracts 20

• Whatisacontract? 20

• Differentcontractsinthehome-buyingprocess 20

• Breachofcontract 20

Chapter 7 – Wills 21

• Makingawill 21

Chapter 8 – Building a house 23

Chapter 9 – Sectional title 24

• Wealsogranthomeloansforsectionaltitledevelopments 24

Chapter 10 – The National Credit Act (NCA) 26

• WhatistheNCA? 26

• FactsabouttheNCA 26

Chapter 11 – Useful contact numbers 28

Chapter 12 – Income and expenditure guide 28

4

Chapter 1 – IntroductionWelcometotheworldofhomeownership!

Thankyoufortrustingustobeyourpartnerinthe

bigdecisionofbecomingahomeowner.Thereare

manythingstoconsiderandthismanualwillguide

youthroughthem.Ahomeisprobablyoneofthe

mostexpensivethingsthatyouwilleverbuyand

youneedtounderstandwhatthismeansforyou.

Owningpropertymeansyouhaveanassetyouwant

togrowinvalue.Itistherefore,essentialtolook

afteryourpropertytokeepyourinvestmentsafe.

Yourproperty(theasset)canalsohelpyoutomake

money:

• Propertyvaluesgenerallygrowovertime,which

meansyoumaysellyourpropertyformorethan

youpaidforitandusethisprofittobuyanother

one.Butthat’snotall…

• Youcanaddroomsormakeimprovementsto

yourhomewhichwillnotonlymakeitmore

comfortableforyouandyourfamilybutwillalso

addtoitsvalue.Youneedtomakesurethatthe

renovationsareprofessionallydoneortheycould

haveanegativeeffectonthevalueofyour

property.

• Youcanaddroomsthatyoucanrentouttomake

someextramoney.

• Youcanaddorconvertroomstorunyour

businessfromhome.

Owningahomemeansthatyouwillbetakingon

newfinancialresponsibilities.Ahousecanrangein

pricefromafewhundredthousandtomillionsof

rands.Mostpeopledonothaveenoughcashtopay

forthehousetheywanttobuyandhavetoborrow

themoney.

Housingfinancemakesitpossibleforyoutobuy

ahouse.Ifyoubuyahouseandusefinance,you

havetheresponsibilityofrepayingalargedebt

whichmaybeoveralongperiod.

Therearealsootherfinancialresponsibilitiesthat

comewithhomeownership:

• Youwillhavetopayforservicessuchaslights

andwater.

• Youwillhavemaintenanceexpensestokeepthe

houseingoodcondition,forexample,painting.

• Youwillhavetopayinsurancetocoveryour

houseagainstfireorotherdamage.

• Youwillhavetopayratesandtaxes.

• Inthecaseofsectionaltitle,youwillhavetopay

levies.

Thishandbookgivesyousomebasicinformation

abouthomeownershipandhomeloanstohelpyou

tounderstandthembetter.

Pleasedonothesitatetocontactyournearest

branchorourcustomercontactcentreon

0860123001formoreinformation.

Enjoyyourhome.

Chapter 2 – Housing finance

Thefollowingstepsinthehome-buyingprocessare

importanttonote.Asyouhaveanexistinghome

loanaccountwithus,youwouldhavebeenthrough

thefirstfewstepsmentionedbelow.Evenso,you

cansharethisinformationwithfriendsandfamily

whoareconsideringbuyingahomeandyoucan

usethesamestepswhenyouwanttobuyanew

home.

Taketimetoreadthroughallthesecarefullysothat

youarepreparedeverystepoftheway.

Key steps to buying a home

Step 1: Budgeting and affordability

Thefirststepistoworkouthowmuchyoucan

affordtopayeverymonth.Thisisnotonlyonyour

monthlyhomeloaninstalment,butalsoincludes

insurance(bothforthebuildingandthecontents

ofyourhome),assurance(alifepolicytocover

theloanshouldanythinghappentoyou),rates

andtaxes,levies,waterandlightsaswellasyour

livingexpenses.Youshouldtakeallyourdebt

commitmentsintoaccounttoensurethatyoudo

notspendmorethanyoucanafford.

Generally,spendingabout30%ofyourincomeona

homeloanrepaymentisreasonablyaffordable.Itis

alsoagoodideatoapproachusforapledgebefore

yougohousehunting.Thatwayyouknowthe

homeloanamountyouqualifyfor.SeeChapter3–

Affordabilityandbudgetingformoreinformation.

5

Step 2: House hunting

Onceyouknowhowmuchyoucanafford,you

needtodecidewhatkindofhousesuitsyourneeds

andyourpocket.Youcanbuildorbuyafreehold

property(ahouseonasinglestand),acluster

homeoryoucanbuyasectionaltitleunitina

complex.SeeChapter9formoreinformationabout

sectionaltitleandChapter8forinformationabout

buildingahome.

Step 3: Make an Offer to Purchase

Ifyouhavedecidedonthepropertyyouwouldlike

tobuy,youwillneedtofillinanOffertoPurchase.

Thisdocumentissometimesalsoknownasan

AgreementofSaleorDeedofSale.Basically,itis

awrittenagreementstatingthatyouwanttobuy

thepropertyandthetermsandconditionsunder

whichyouagreetobuyit.Ifthebuyingpriceofthe

propertyisbelowR250000,afive-daycoolingoff

periodapplies.Thismeansthatyouhavefivedays

aftersigningtheOffertoPurchasetowithdraw

youroffer.Afterthefivedays,youwillbelegally

boundtotheagreementandyoumayfindyourself

introubleifyouthenwanttocancelthedeal.

FormoreinformationaboutanOffertoPurchase

refertoChapter6–ContractsandChapter5–

Thingstoknowabouthomeloansunderrightsand

obligations.

Step 4: Seller accepts your offer

TheOffertoPurchasehastobenegotiated.

Youshouldnotewhichfixturesandfittingsformpart

ofthesale.Allthepermanentfixturesandfittings

suchaslightfittings,carpets,tiles,curtainrailsand

pelmets,andbuilt-incupboardsareincludedin

thesaleunlessyouandtheselleragreeotherwise.

Anymovableitemsincludedinthesalemustbe

negotiatedbetweenyouandtheseller.Itisalso

importanttounderstandtheconditionsunderwhich

youwilloccupytheproperty.Inparticular,makesure

thattheoccupantofthepropertyiswillingtoleave

thepremisesonthedateagreedtointheOfferto

Purchase.Onceyouhavenegotiatedtheoffer,the

sellerwillaccepttheOffertoPurchaseandyouareon

yourwaytobecomingahomeowner.SeeChapters5

and6formoreinformation.

Step 5: Apply for a home loan

Younowneedtofillinahomeloanapplicationform

andgiveusallyourpersonalinformationandthe

requiredsupportingdocuments.

Thedocumentsweneedare:

• Proofofincome

• CertifiedcopyofSouthAfricanidentity

documentorpassport

• Yourspouseorpartner’sidentityorpassport

number,ifyouaremarriedincommunityof

propertyorifyouaredoingajointapplication

• Proofofyourcurrentstreetaddress(municipalor

Telkomaccount,orvalidTVlicence)

• Yourincometaxreferencenumber(ifapplicable).

Step 6: Requirements will be confirmed

Wecanstartprocessingyourhomeloanapplication

assoonaswehaveyourhomeloanapplication,

thesignedOffertoPurchaseandothersupporting

documents.Thisincludesmakingsurethatyoucan

affordtheloanamountyouareapplyingforand

creditcheckstoseehowyouhavebeenconducting

yourotheraccounts.

Step 7: A property valuation is done

Thepropertyisthesecurityforyourloan.Thismeans

thatwehavetherighttosellyourhometorecover

theoutstandingamountsowingtousifyoudo

notpayyourinstalmentseverymonth.Wedoa

propertyvaluationtocheckwhetherthepresent

marketvalueofthepropertycoverstheamount

thatyouwanttoborrow.

Step 8: A decision is made

Afterconsideringyourincome,affordability,credit

standingandpropertyassessment,wewillmakea

finaldecisiononyourloanapplication.

Step 9: Quotation letter

Ifyourhomeloanapplicationisapproved,wewill

sendyouaquotationletter.Theletterwillinclude

importantinformationaboutthehomeloanaswell

asanyspecialconditionsthatwillapplytotheloan.

6

Step 10: Registration attorney

instructed to register the bond

Wewillappointaregistrationattorneytoattend

totheregistrationofyourbond.Thisattorneywill

makesurethatthepropertyistransferredintoyour

nameandthatthemortgagebondisregistered.

Step 11: You sign the necessary documents at

the attorneys’ offices and pay the relevant costs

Youwillberequestedtosignallthenecessary

documentsattheregisteringandtransferring

attorneys’offices.Thetransferandbondregistration

feesmustbepaidinfullatthedifferentattorneys

beforethebondcanberegisteredinyourname

attheDeedsOffice.SeeChapter4–Costsand

expensesforthefeesthatwillapply.

Note:thetransferringattorneyistheseller’s

attorneyandtheymustmakesurethatthe

propertyistransferredoutoftheseller’sname.

AlsoseeChapter5–Thingstoknowaboutahome,

10thingstoaskyourattorney.

Step 12: Documents sent to Deeds Office for

registration in your name

Oncealldocumentsareinorderandallfeeshave

beenpaidinfull,theattorneyswillsubmitthe

documentstotheDeedsOffice.Thisprocessis

referredtoas“lodgement”.

7

Step 13: Home loan registered in your name at

Deeds Office by registering attorney

WhentheDeedsOfficehascheckedallthe

documents,thetransactionwillberegistered.

Thisnormallytakesabout10workingdaysfrom

whenthedocumentswerelodgedwiththe

DeedsOffice.

Theprocessondateofregistrationisasfollows:

• Propertyistransferredfromthesellertoyou

(thebuyer).

• Yourmortgagebondisregistered.

• Seller’sbondiscancelled.

• Fundsarepaidtorelevantparties.

• Youareadvisedthatthebondhasbeen

registered.

• Theamountyouowewillbeshownonyour

homeloanaccount.

Note:Becauseoftheinvolvementofotherparties

andtransactions,itcouldtakeuptothreemonths

afteryourloanisapprovedforyourbondto

beregistered.

Step 14: Confirmation of your instalments

Wewillsendyoualettertoconfirmyourbondhas

beenregisteredandwhatyourinstalmentswill

be.Wewillsendyouahomeloanstatementtwice

ayearshowingtheoutstandingbalanceonyour

homeloanaccount.Ifyoudonotgetastatement

itdoesnotmeanthatyouraccountisfullypaidup.

Itremainsyourresponsibilitytomakesurethatyou

arealwaysinformedofthestatusofyouraccount.

It is also your responsibility to make sure that

we have up-to-date contact details (telephone

numbers and postal address) to be able to

communicate with you. If your details change

at any time, it is very important that you give us

your new details.

Step 15: Your first monthly instalment

Yourfirstpaymentisdue30daysaftertheproperty

isregisteredinyourname.Itiscompulsorytoset

upadebitorderorsalarydeductiontomakesure

yourhomeloaninstalmentispaidinfullandon

timeeverymonth.

Forbuildingloans:yourfirstinstalmentisdue

within30daysafter90%oftheloanhasbeenpaid

oronoccupation.

Step 16: Attorney sends title deed and mortgage

bond documents to us for safekeeping

Ifyouhaveanyquestions,pleasevisityournearest

branchorcallourcustomercontactcentreon

0860123001.

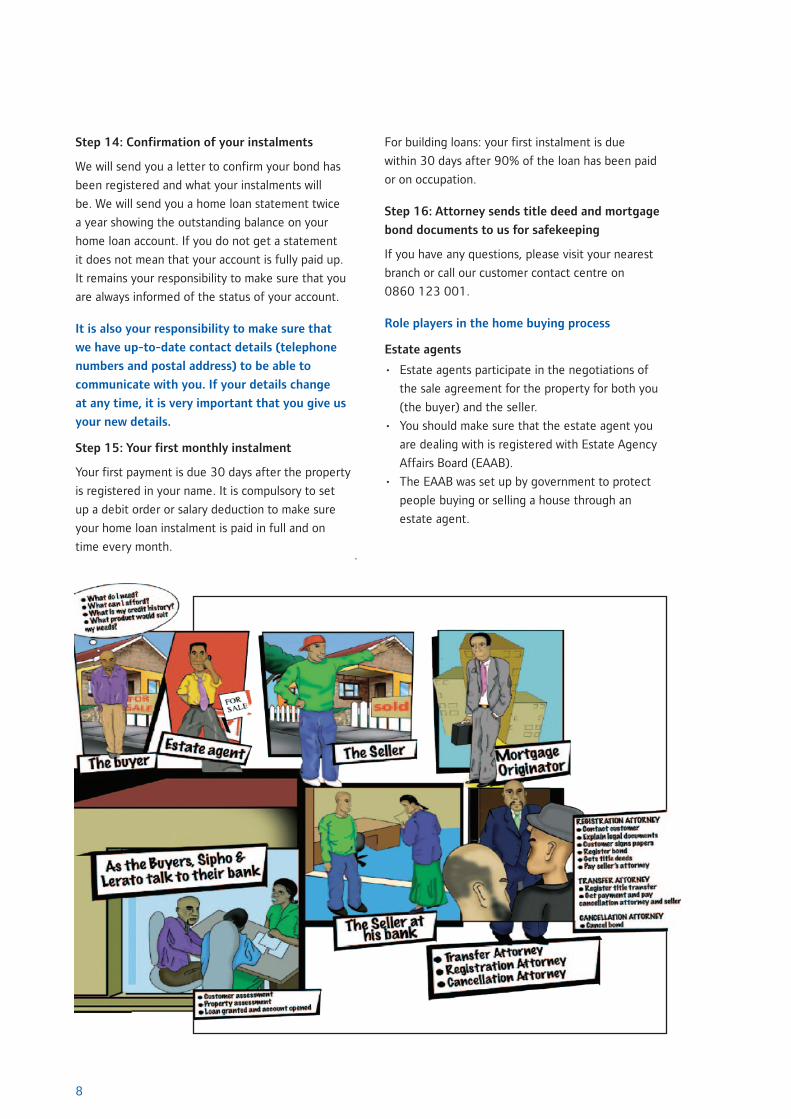

Role players in the home buying process

Estate agents

• Estateagentsparticipateinthenegotiationsof

thesaleagreementforthepropertyforbothyou

(thebuyer)andtheseller.

• Youshouldmakesurethattheestateagentyou

aredealingwithisregisteredwithEstateAgency

AffairsBoard(EAAB).

• TheEAABwassetupbygovernmenttoprotect

peoplebuyingorsellingahousethroughan

estateagent.

8

Developers

• Developerscanbeanindividualorcompany

thatbuysapieceoflandanddevelopsitintoa

housingcomplex.

• Thehousingcomplexcaneitherbefreestanding

orsectionaltitle.

The seller

• Isthepersonorentitythatisthelegalregistered

ownerofthepropertyandwantstosellit.

The buyer

• Isthepersonwhoisbuyingtheproperty.

The occupant

• Isthepersonlivingontheproperty.Thisisnot

necessarilytheselleroftheproperty.

Your bank

• Weassistyouwiththeloanapplicationprocess

andthenlendmoneytoyoutopaytheseller.

• Youcanapplyforahomeloanthrougha

mortgageoriginatorwhoisapersonwhocan

alsoassistyouwithgettinghomeloanfinance.

The seller’s bank

• Theseller’sbankensuresthatanyloantheseller

mighthaveonthepropertyispaidinfullbefore

itistransferredintoyourname.

Where are you in the process?

Youcanusethediagrambelowtohelpyoutotrack

whereyouareintheprocess.

Shouldyouhaveanyquestionsatanystageduring

theprocess,youcancallourCustomerContact

Centreon0860123001.

9

Occupation date

(…../…../…../)

Application

(…../…../…../)

Property assessment

(…../…../…../)

Bond grant

(…../…../…../)

Pay fees at attorneys

and sign documents

Bond registration

(…../…../…../)

Loan payout

(…../…../…../)

Commence instalments

(…../…../…../)

Chapter 3 – Affordability and budgeting

Affordability is very important

Withhomeownershipcomemanyresponsibilities.

Oneoftheseiskeepingtoyourfinancial

commitments.Ifyoutakeoutanyloans,youmust

besurethatyouwillbeabletopaythemback.

Ask yourself these questions:

HowmuchsparemoneydoIhaveattheendof

everymonth?

HaveIsavedmoneyforunexpectedexpenses?

AmIspendingmoremoneythanIearn?

AmIlivingoncredit?

DoIhaveanyaccountsthatareoverdue?

Itisveryseriousifyoudonotpayyourhomeloan

instalments.Youcanloseyourhome,yourdeposit

andallthatyouhavepaidonyourloan.Youmust

thinkcarefullyaboutyourfinancesbeforeandafter

youhavetakenoutahomeloan.

• Beforeyoudecidetotakeoutahomeloanyou

mustworkoutyourincomeandexpenditure.

Youmustknowwhatitwillcostyoueachmonth

toliveinyourhome.Theseexpenseswill

includeyourhomeloanrepayments,repairsand

maintenancetotheproperty,municipalservices

suchaswaterandelectricity,levies,andrates

andtaxesonyourproperty.

Theseexpensesareinadditiontoyournormal

livingexpenses.SeeChapter4–Costsand

expensesfordetailsofthedifferentcostsand

expensesrelatedtohomeownership.

• Onceyouhaveyourhomeloanyouwillneedto

consideryourfinancialpositionbeforeyoutake

onanyadditionalexpenses.Again,youshould

bearinmindthatyourhomeloaninstalment

couldincreaseatanytimedependingon

changesintheinterestrate.

Your budget

Itisalwaysagoodideatodrawupabudgetto

helpyoutomanageyourfinances.Abudgetwill

helpyoutounderstandhowmuchmoneyyou

haveavailablebycomparingyourincomewith

yourexpenses.

Income and expenditure guide

Theincomeandexpenditureguidehelpsyouto

understandyourmonthlyincomeandexpenditure

andhowitcontributestoyourapplication.

Tofillinyourincomeandexpenditurestatement

youneedindividualgrossincomeandexpenses.

Ifyourexpensesareshared(forexample,youare

married)thenonlyonepartnerneedstorecord

theirexpenses.Makesurethatyouarerealisticand

honestwithyourselfwhenyoufillinyourincome

andexpenditurestatement.Bearinmindincreases

intheinterestrateandcostofliving.

Please see the back of this handbook for an

income and expenditure guide that you can use

for ongoing budgeting.

10

11

How to improve your affordability

Whenapplyingforahomeloan,thereareanumber

ofwaysinwhichyoucanimproveyouraffordability.

1. Your employer may have a housing assistance

scheme

Manyemployersassisttheirstaffwithbuyinga

home.Thisisusuallyamonthlyhousingsubsidy

orallowance.Thissubsidyorallowancehelpsyou

toaffordyourhomeloaninstalments.Checkwith

youremployerifthereisanassistanceschemein

place.Mostbankswillonlyallowyoutousepartof

youremployerhousingsubsidywhenworkingout

youraffordability.Thisisagoodthing,becauseif

youloseorchangeyourjob,youwillstillbeableto

affordyourinstalments.

2. Use your savings

Useyoursavingstoputdownasbigadepositas

possible.Thiswayyouwillneedtoborrowless

moneywhichmeansyoupaylessinterestandyour

monthlyinstalmentwillbemoreaffordable.

3. Government subsidy

Ifyouqualify,thegovernmentmaygrantyoua

housingsubsidy.Thissubsidyisaonce-offlump

sumpaymenttowardsthecostofyourhouse.You

donothavetorepaythemoney,butitmustbe

usedforhousingandyoumaynotsellthehouse

withinaspecifiedperiodwithoutpermissionfrom

theProvincialHousingDepartment.Thesubsidywill

bepaiddirectlytousandcanreducetheamount

youneedtoborrow.

Youmayqualifyforagovernmentsubsidyif:

• YouareaSouthAfricancitizenorapermanent

resident.

• Youareafirst-timehomebuyer.

• Youareatleast21yearsold.

• Youaremarried(civilandcustomary)orliving

withalong-termpartner.

• Yourjointgrossmonthlyincomeisnotmorethan

R7000amonth.

• Youaresinglewithfinancialdependants.

• Youmusthaveacashdeposit.

Ifyouqualifyforagovernmentsubsidy,depending

onthetypeofsubsidyyouget,wemaybeableto

applyforitonyourbehalf.Thesubsidywillnotbe

approvedifwedeclineyourhomeloanapplication

orthehomeisnotregisteredinyourname.

Speaktoyourhomeloanconsultantformore

informationonsubsidies.

4. Settling outstanding debts

SincetheNationalCreditAct(NCA)wasintroduced

inJune2007,youhavetodisclose(mention)all

yourdebttouswhenyouapplyforanytypeof

loan.Ifyoupayoutstandingdebtsbeforeyouapply

foryourhomeloanyourchancesofqualifyingfor

theloanamountyouwantwillimprove.

12

Chapter 4 – Costs and expenses

The costs when you take a home loan from us

1. The deposit

Wehavetherighttoaskyoutopayadeposit.

Thebiggerthedeposityoucanputdown,the

smallerthehomeloanyouwillhavetotakeand

thelessinterestyouwillhavetopay.

2. Initiation fee

Thisisthechargetopreparethedocuments

andprocessyourloanapplication.Wenotethe

initiationfeeinyourquotationletterandalso

discussitwithyouafteryourhomeloanhas

beenapproved.

3. Service fee

Wechargeamonthlyservicefeeonyourhome

loan.Wenotetheservicefeeinyourquotation

letterandalsobediscussitwithyouafteryour

homeloanhasbeenapproved.

4. Transfer fees

Alawyerpreparesthedocumenttotransferthe

titledeedforthepropertyfromtheseller’sname

toyourname.Asthebuyeroftheproperty,you

paythetransferfeesupfront.Thesearecalculated

onthebuyingprice.Notransferdutyispayable

forloansuptoR500000butthetransferring

attorney’sfeewillstillapply.Thetransferring

attorneywilladviseyouoftheamountthatyou

willneedtopay.Thesefeesmustbepaidbefore

registrationormaybeincludedinthehomeloan

amount.Yourquotationletterwillshowwhether

thefeeswillbeincludedinyourloanamount.

• Youdonotneedtopaytransferfeesifyou

arebuyingapropertyinanewdevelopment

(off-plan)orifyouareapplyingforaloanto

buildanewhouse.

5. Bond registration fees

Ourlawyer,calledaconveyancer,willalsoprepare

thebondregistrationdocumentssothatthebond

isregisteredinyourname.Theywillsendthese

documentstotheDeedsOfficewhereownership

detailsofeverysinglepropertyinthatareaisfiled.

Thechargeforthiscalledabondregistrationfee.

You(thebuyer)areresponsibleforbond

registrationfeesbeforeregistrationorthey

maybeincludedinthehomeloanamount.Your

quotationletterwillshowwhetherthefeeswill

beincludedintheloanamount.

6. Home-owner’s insurance

Home-owner’sinsurancecoversdamagetothe

structureofyourhouse.Theinsuranceprotects

youandusagainstanylossesifyourhouse

isdamagedordestroyedanditistherefore

compulsory.Forexample,ifyourhousecatches

fireorisdamagedbyfloods,thisinsurancehelps

topayfortherepairs.Itdoesnotcoverdamage

tothehousecausedbylackofmaintenanceor

thefurnitureinsidethehouse.

Youcanusetheinsurancecoveravailablefrom

usoryoucangotoaninsurancecompanyofyour

choice.Thisappliestofree-standingproperties.

Ifyouarebuyingasectionaltitleproperty,the

bodycorporatewillarrangethiscoverthrough

aninsurancecompanyofitschoice.

Pleaserefertoyourpolicytounderstandwhat

iscovered.Ifyoutakeapolicyfromus,the

monthlypremiumwillbeincludedinyourmonthly

debitorder.

13

7. Life assurance

Youneedtoconsiderwhatwillhappentoyour

familyifyoudieorbecomedisabled.

Itisimportanttohaveadequatelifecovertosettle

yourhomeloanifsomethingunexpectedhappens.

AlsoseeChapter7–Makingawill.Rememberto

alwayscheckyourpolicydocumentscarefullytosee

whatyouarecoveredfor.

Thepolicycancoverthefollowing:

• Death.

• Disability.

• Retrenchment.

Ifyoutakeapolicyfromus,weincludethe

premiuminyourmonthlydebitorder.

The expenses you will have as a home owner

1. Monthly instalments

Assoonasthepropertyandhomeloanis

registeredinyourname,youmuststartmaking

repayments,evenifyouhavenotmovedinto

yourhouse.Afterthat,youmustpayyourloan

instalmenteverymonthforthedurationofthe

agreedloanperiod.

Yourmonthlyinstalmentincludesaportionto

repaytheamountthatyouhaveborrowedanda

portiontopaytheinterestontheloanamount.

Werecommendthatyoupayyourhomeloan

instalmentbydebitordereverymonth.

Ifyouhavearrangedtomoveintoyourhouse

beforethebondisregisteredinyourname,you

willhavetopayoccupationalrenttotheowner

ofthehouse.

Itisimportanttoknowthatyourmonthly

instalmentwillincreaseanddecreasedepending

ontheprimeinterestrate.Pleasereferto

Chapter5formoreinformationonthis.

2. Electricity

Youwillhavetopayadeposittohaveelectricity

connectedtoyourhome.Thenyouwillhave

topayfortheelectricityyouuseeverymonth.

Dependingonthesysteminthearea,youcan

useaprepaidcardsystemoryoucanbebilled

monthlyfortheamountofelectricityyouuse.

Thecostforelectricitycandifferfrommonth

tomonth.Youmustpaytheserviceprovider

directlyfortheelectricityyouuse.

3. Water

Youwillneedtopayadeposittohavewater

connectedtoyourhome.Dependingonthe

systeminthearea,youcanalsouseaprepaid

systemoryoucanbebilledmonthlyforthe

amountofwateryouuse.Yourlocalmunicipality

orotherserviceproviderwillsendyouamonthly

accountforthewateryouusedduringtheprevious

month.Youmustpaytheserviceproviderdirectly

forthewateryouuse.

14

4. Municipal rates and taxes

Yourlocalmunicipalitywillsendyouanaccount

forratesandtaxesandyoumustpaythem

directly.Thisamountusuallystaysthesamefor

ayear.Thelocalmunicipalityusesthemoney

itreceivesfromratesandtaxestoprovide

seweragefacilities,repairandbuildroads,put

upstreetlightsandcollectrefuse.Notethatthe

localauthoritymayattachyourpropertyandsell

itifyoudonotpayyourrates

andtaxes.

5. Maintenance and repairs

Asahomeowner,youareresponsibleforthe

maintenanceofyourproperty.Itisbestto

attendtosmallrepairsandmaintenancework

onaregularbasis,andnotleavethemuntil

theybecomebigandexpensivejobs.Thisway

youkeepyourhouseingoodconditionandits

valueismaintained.Makesureyouincludesome

moneyinyourbudgetforthis.

6. Home improvements

Youcanincreasethevalueofyourpropertyif

youbuildanextensiontoyourhouseoradd

anotherroom.Ifyoumakeotherimprovements,

forexample,layfloortiles,thiscanincreasethe

valueofyourproperty.Theseextensionsand

improvementsmustmeetstandardrequirements.

Poorworkmanshipandpoorqualityofmaterials

usedwillnotincreasethevalueofyourproperty–

theycanevenreduceitsvalue.

7. Levies

Ifyouhaveboughtasectionaltitlepropertylike

aflatortownhouse,therearecostsforrunning

thecomplex,whichyouwillhavetocontributeto

everymonth.Thesecostsinclude:

• Rates

• Taxes

• Insurancepremiums

• Repairsandmaintenanceofthecommon

property,suchasthegardenandthebuildings

• Wagesandsalariesofcleanersandotherstaff

• Waterandelectricityusedonthecommon

property.

Chapter 5 – Things to know about a home loan

General

What is a home loan?

Whenyoubuyahouse,youpayapurchaseprice.

Thisisthepriceyouandtheselleragreeto.Ifyou

donothavethecashtopaythefullpurchaseprice,

youcanapplytoustoborrowmoney.Themoney

youborrowtobuyahouseiscalledahomeloanor

amortgagebond.

Ifyouqualify,wewillgiveyouahomeloan.

Youmayneedtopayadeposit.Wewillthenlend

youtheremainderofthepurchasepriceofthe

houseyouwanttobuy.Thisamountiscalledthe

capitalorloanamount.

Whenyoubuyaproperty,theTitleDeedisthe

legaldocumentthatstatesthatyouownthe

property.Assecurityforthehomeloanwegrant

you,amortgagebondisregistered.Amortgage

bondisthelegaldocumentregisteredwiththe

DeedsOfficeagainsttheTitleDeed,toindicate

thatyouhavealoancommitmenttous.

Themortgagebondwillberegisteredagainstthe

TitleDeeduntilyourhomeloanispaidoffinfull.

Althoughthereisamortgagebondregisteredin

ourfavourtheTitleDeedisinyourname.

Youthereforeownthepropertyandhaveownership

responsibilitiessuchasmaintainingtheproperty,

payingratesandtaxesandrepayingyourhome

loan.Ifyoudonotwantthepropertyitisyour

responsibilitytosellit.Wedonotownyourproperty;

wemerelyhavearighttoitifyoudonotrepayyour

homeloan.

How long do I have to pay off my loan?

Yourhomeloanmustberepaidtouswithina

certainperiod.Thisiscalledtherepaymentperiod

orloanterm.Whatyoucanaffordtorepayevery

monthwilldeterminetherepaymentperiodofyour

loan.Youragewillalsobetakenintoconsideration.

Therepaymentperiodisusually20years,butitcan

gouptoamaximumof30yearsincertaincases.

15

Can I pay my loan off in a shorter time?

Yes,ifyoucanpayyourloaninashortertime,

youwillsavealotofmoney.

The savings are great

Itisalsoagoodideatomakeextralumpsumor

severalextramonthlypayments.Becauseinterest

ischargedonthedailybalanceanyamountyou

depositintoyouraccountwillreducetheamount

ofinterestyoupayontheoutstandingbalance

eachmonth.

Remember:Nomatterhowmuchmoreyoupay

eachmonthorhowoftenyoumakeadeposit,

youmustpaytheminimuminstalmentbythedue

dateasshowninyourloanagreement.

How do I pay my monthly home loan instalment?

Theloanispaidoffinmonthlypaymentscalled

instalments.Thesemustbepaidonorbeforethe

duedateeverymonth.

Youcanpayyourmonthlyhomeloaninstalmentin

oneofthefollowingways:

• Debitorder–thisgivesuspermissionto

withdrawyourmonthlyhomeloaninstalment

fromyoursavingsorcurrentaccount.

• Salarydeduction–youcanaskyouremployer

todeductyourhomeloaninstalmentfromyour

salaryeachmonth.Youremployerthensends

ustheinstalmentamountandyourhomeloan

accountiscredited.Thisisalsocalledapayroll

deduction.Itisyourresponsibilitytoletyour

employerknowifyourinstalmentchangesso

thatyourhomeloandoesnotgointoarrearsdue

toincorrectpaymentsbeingmadetous.

Tomakepayingyourinstalmentseasier,ontime

andforthecorrectamounteverymonth,itis

compulsorythatyousignadebitorderorsalary

deduction.Alwaysmakesurethatthereisenough

moneyinyourtransactionaccountsothatthedebit

orderisnotreturnedbecausetherearenotenough

fundsintheaccount.Askustoarrangethatyour

debitorderorsalarydeductionisprocessedon

thedaythatyougetpaid.Thatwayyouwillnotbe

“tempted”tospendsomeofthemoneythatyou

needforyourhomeloaninstalment.

16

Whereyouhavetakeninsurancepolicieswhich

applytoyourhomeloan,themonthlypremiumswill

beincludedinyourmonthlydebitorder.

Note:Ifyouarerentingouttheproperty,andthe

amountofrentyougetislessthantheinstalment,

youwillhaveto“makeup”thedifference.Youare

responsibleformakingsurethatyoupaythefull

instalmentduebytheduedateotherwiseyour

homeloanaccountwillbeinarrears.

Will my instalment change when the interest

rate increases or decreases?

Yourhomeloaninstalmentwillchangeasthe

interestratechanges.Whentheinterestrategoes

up,yourmonthlyinstalmentwillgoup.Whenthe

interestrategoesdown,yourmonthlyinstalment

willgodown.Interestratechangesareannounced

inthemediaandthenewinstalmentswillbecome

payablethenexttimeapaymentisdue.

Wewillsendyoualetterwhentheinterest

ratechangesandletyouknowwhatyournew

instalmentwillbe.Ifyoupayyourhomeloanby

debitorder,thecorrectinstalmentwillautomatically

bedeductedthenexttimeapaymentisdue.

Does the capital amount get less over the

loan period?

Whenyoupayyourmonthlyhomeloaninstalment,

yourpaymentfirstlypaystheinterestforthat

month.Secondly,itpaysyourinsurancepremiums

andservicefee.Andlastly,itpaysthecapital(loan)

amount.Thecapitalamountthenbecomesalittle

less.Thenextmonth’sinterestisnowcalculatedon

thelesseramount.Overtime,youwillpaymoreoff

yourcapitalamounteachmonth.

How are my payments recorded?

Wewillopenahomeloanaccountinyourname.

Yourmonthlyinstalmentswillbepaidintothis

account.Wewillsendyouastatementofthis

accounttwiceayear,showingthedateonwhich

paymentsweremade,theamountspaid,the

interestchargedandthebalanceowingon

theaccount.

Ifyoupayyourinstalmentusingasalarydeduction

ordebitorder,you’llalsoseethesepaymentson

thestatementofthesavingsorcurrentaccount

fromwhichthemoneyisdrawn.

Can I pay more than my instalment each month?

Yes,ifyoucanaffordit,youshould.Itiscalled

acceleratedpayments.Ifyoupayalittlemoreon

yourinstalmenteachmonth,youwillreduce

therepaymentperiodofyourbondandsave

alotofmoney.

What happens if I pay my home loan instalment

after the due date or I cannot afford to pay

my loan?

Non-paymentonyourhomeloanmayaffectyour

abilitytogetcreditinthefuture.Itisimportantto

makepaymentseverymonthontheduedateto

avoidyouraccountgoingintoarrears.

Itisalsoimportanttomakesurethatyouearn

enoughmoneytorepayyourloanandstickto

yourbudget.Payyourhomeloaninstalmentsfirst

anddonotoverspendonotherthings.Budgeting

ishowyoukeeparecordofyourmonthlyincome

andexpenses.

Thereareseriouseventsthatwouldaffectyour

abilitytomakeyourmonthlyinstalmentssuchas

retrenchment,lossofemploymentorpartner’s

income,shortpayandillhealth.Youshould

approachusifyourunintoproblemsandgetadvice

immediatelyifyouarenotabletomakeyour

monthlyrepayments.

Ifyoudonotmakeapaymentatall,wecanevict

youandrepossessyourhomeasitisthesecurity

foryourloan.

17

You can contact our Customer Debt Management

(CDM) department on 0860 102 270 if you are

having financial difficulty and want to discuss

your options with us.

How can I use my home loan to make alterations

and improvements, and what are the options to

refinance my loan?

Renovatingahomeispartofmaintenance.For

example,ifyourepaintthehouseandreplace

gutters.Theseexpensesusuallypreventyour

propertyfromdeterioratingbutwillnotcontribute

toitsvalue.Youmayincreaseitsvalueifyou

upgradethepropertybyreplacingcarpetswith

tiles,retilingthebathroomoraddanotherroom.

Theseitemsareconsideredascosmeticandany

increaseinthevalueofthepropertyisminimal

comparedtotheirretailcost.

• Furtheradvances–ifyourpropertyincreasesin

valueyoucanregisterasecondbondtoaccess

additionalfunds.

• AccessBond–youcanwithdrawavailablefunds

fromyourAccessBond.

• Re-advance–ifyoudonothaveanAccessBond

youmayapplyforare-advancetoaccesssome

oftheamountyouhavealreadypaid.

When can I sell my house?

Youcansellyourhousebeforeyourloantermisup.

Youwill,however,havetogiveus90days’written

noticeofyourintentiontosettleyourhomeloan

otherwisewewillchargenoticeinterest.Youshould

contactusassoonasyoudecidetosellyourhome.

Remember:Ifyouhavelookedafteryourproperty

andpaidyourmonthlyinstalmentsontime,you

mayhavesomeequity(value)inyourproperty.

Oncethebalanceowingonyourhomeloanispaid

andtheothercostsinvolvedinsellingtheproperty

aresettled,theamountleftoverisforyou.Youcan

usethismoneyasadepositonanotherproperty.

Rights and obligations

Whatareyourrightsandobligationsasahome

buyerandhomeloancustomer?

Amortgageloanmaybeyourmostimportantfinancial

commitment.Itisimportantforyoutounderstand

thewiderresponsibilitiesandrightsthatyouhave

asahomebuyerandhomeowner.Pleasealsorefer

toChapter10–NCA.Thefollowingaresomeofthe

importantthingstokeepinmind:

• AftersigningtheOffertoPurchaseyouhavea

cooling–offperiodoffive(5)dayswhereyoucan

withdraworcanceltheOffertoPurchase.Thisonly

appliestopropertieswithabuyingpriceofless

thanR250000.

• Oncethefive-dayperiodhaslapsed,theOfferto

Purchaseisalegallybindingcontractandifyou

terminateittherecouldbelegalimplications.

• Makesurethatyouhaveviewedyourpropertyand

thatitmeetsyourrequirements.Makesureyou

arehappywithanyclausesregarding,forexample,

occupationdateandoccupationalrent.

• Youshouldbesatisfiedthattheselleroroccupant

willleavethepropertywillinglywhenrequired.

• Youmayaskfortransferofthepropertytobe

delayeduntiltheselleroroccupanthasleftthe

property.

• Ifamonthlyhousingsubsidyfromyouremployer

applies,itisyourresponsibilitytoarrangethe

paperworkwiththemtoputthesubsidyinplace.

• Ifyouremployerdeductstheinstalmentfromyour

salaryandthenpaysus,itisyourresponsibilityto

letyouremployerknowiftherepaymentamount

changes.

• Issuesofhomequalityaretheresponsibilityofthe

seller,builderordeveloper,andyouasthebuyer.

Homesthatarelessthanfiveyearsoldmustalso

haveaNationalHomeBuildersRegistrationCouncil

LimitedWarranty.

• Rememberthatyourhomeloanrepaymentdoes

notcoverwater,electricity,andratesandtaxes.You

mustpaythemunicipalityorserviceproviderdirectly.

• Itisimportantthatyoumaketherepaymentson

yourhomeloantom,akesureyoukeepahealthy

creditrecord.

• Ifyoufinditdifficulttomakerepaymentson

yourhomeloan,contactusassoonaspossible.

Wewillhelpwherepossibletorearrangeyour

repaymentsormakeanalternativeplanwithyou.

• Youhavetherighttoapproachadebtcounsellor.

Ifyouenterintodebtreviewwithadebtcounsellor,

youwillnothaveaccesstoanyfurthercreditor

loansfromallcreditproviders,notonlyus,until

yourfinancialpositionhasimproved.

• Ifyoudonotmaketherequiredrepaymentson

time,wemayendyouragreementandtakelegal

actionagainstyou.

Ifwehavetoendyouragreementearlydueto

non-payment:

• Wewillletyouknowinwritingandchargeyou

forthecostsofservingthatnotice.

• Youwillstillbeliableforthebalanceoutstanding

onyourloan.

• Ifyoudefaultontheloanatanytime,wehave

therighttorecoverdefaultadministrationand

collectioncostsinlinewiththelaw.

Therearesuspensiveandspecialconditionsthat

youmustkeeptobeforeyoucanbeusetheloan.

Theattorneywillpointtheseouttoyouinthe

creditagreementthatyousignattheiroffice.

• Whenyouhavepaidupyourmortgagebond

wewillletyouknowhowtodealwithannual

insurancepremiums,otherchargesand

administrativematters.

• Whensigningattheattorney’soffice,makesure

thatyoureadyourentirecreditagreementand

understandit.

Ifyoudonotunderstandanyclausesinthecredit

agreement,youarehavetherighttoasktheattorney

questionsortocontactustoexplainthemtoyou.

10 questions to ask your attorney

1. Who do I pay the deposit to?

Thiswilldependonwhatyourcontractsays.You

canpayyourdepositeithertotheestateagent

ortheconveyancersappointedtohandlethe

transfer.Theybothhavetrustaccountswhere

yourmoneyisprotected.Makesureyouget

theappropriatereceiptsandthatyoupaythe

depositintothecompany’saccount–notthe

individual’sortheseller’saccount.

2. Who gets the interest on the deposit?

Unlessotherwiseagreed,theinterestispaid

toyouafterregistrationoftransfer.Onyour

writtenauthority,bothyourestateagentand

conveyancercanarrangeforittobeinvestedin

aninterest-bearingaccount,andwillactinyour

interestsbyplacingitinthebestshort-term

investmentaccountavailable.

3. Who do I pay the occupational rent to?

Youroccupationalrentgoestotheestateagent

ortheconveyancer.Theywillusuallypayit

intotheseller’sbondaccountordirectlytothe

seller,iftheyhavepaidoffenoughoftheirbond

account.Youcouldpayitdirectlyintotheseller’s

bondaccountifagreed,butyoumayberequired

toprovideproofofpaymenteachmonth.

4. When will I have to sign transfer documents?

Thismayonlybeafewweeksafterthesale

agreementissigned.Usuallyyourconveyancer

willwaituntilthebondisgrantedandtheyhave

receivedthecancellationfiguresfortheseller’s

existingbond.Onlythencantheguarantee

authorityformsbefilledinandandsigned.

Youcanphonetheconveyancerforanupdate

atanytime.

18

5. How long will the transfer take to register?

Thisdependsonthecircumstancesanddue

datesforthebondgrant,andontheguarantees

stipulatedintheDeedofSale.Theaverageis

aboutthreemonthsfromthedateofsale.

Whentherearenocomplications,registration

canbecompletedwithintwomonths.Where

therearecomplications,registrationcanbe

delayed.Insuchcases,youwillneedtostayin

touchwithyourconveyancer.

6. What will my transfer and bond costs be?

Yourestateagentandattorneyshouldbeable

toanswerthisquestionbasedonascheduleof

transferandbondcosts.Theactualtransferfees

dependonthebuyingpriceoftheproperty.

Bondcostsdependonthetotalloanamount

registeredandwhetheryouarebuyinginyour

ownnameorinatrust,closecorporationor

company.Yourattorneywillgiveyouyour

exactcosts.

7. When must I pay my transfer costs?

Thisusuallyhappensafewweeksafterthesale,

whenyousignyourdocuments.Yourconveyancer

(Whohastopaythetransferduty)willneed

paymentinadvance.Thetransfercostsarethe

majorchargeonmosttransfers–aswellastherates

orleviesduetogetaclearancecertificate.Donot

delaymakingapayment–itwilldelaythetransfer.

8. Who will register the mortgage bond?

Wehaveapanelofconveyancers,andoneof

thesewillbeinstructedtoregisteryourbond.

Ifthetransferconveyancerisoneofthose

onthepanel,theywillprobablydothebond

registrationaswell.Thebondcostswillbethe

same,thoughyourtransfermaygothrough

fasterifthesameconveyancerdoesboth.

9. Who will contact me

on registration?

Yourconveyancershouldcontact

youondateofregistration.Youwillalso

begivenafinalstatementoftheaccount.Your

estateagentmayalsophoneyoutoconfirm

registration.Wewillsendyoualettertoletyou

knowoftheregistrationofyourbondandthe

dateyourfirstinstalmentisdue.

10. Where will I get the keys to the property?

Itisbesttomakeanarrangementwithyour

estateagenttopickupthekeysfromthemon

theagreeddayofoccupation.

19

Chapter 6 – Contracts

What is a contract?

Acontractisawrittenagreementbetweentwoor

morepeople.

Inacontract,thesepeoplearecalledtheparties.

Acontractliststhethingsthepartiesagreeto.

Thesearecalledthetermsandconditions.

Thepartiessignthecontractonlywhentheyclearly

understandandagreetothetermsandconditions.

Assoonasthecontractissigned,thelawsaysit

islegallybinding.Eachpartymustkeeptoitsside

ofthedealandneitherpartycanpulloutofthe

agreement.

Different contracts in the home-buying process

Inapropertytransactionlikebuyingahome,there

areanumberofcontractsthatyouenterinto.

Theyare:

1. An Offer to Purchase

AnOffertoPurchasemusthavethefollowing

information:

• Adescriptionoftheproperty,includingstand

number

• Addressandsize

• Thebuyingprice

• Thedateofoccupation

• Theamountofoccupationalrent

• Whatfixturesandfittingsaresoldwiththehouse

• Thetimeyouhavetoarrangefinance.

Thefollowingareimportantthingstoknowabout

anOffertoPurchase:

• AfteryouhavesignedtheOffertoPurchase

youhaveacooling–offperiodoffive(5)days

inwhichyoucanwithdraworcancelit.Thisonly

appliestopropertieswithabuyingpriceless

thanR250000.

• Oncethefivedayshaveexpired,anOfferto

Purchaseisalegallybindingcontract.Ifyouend

thecontracttherecouldbelegalimplications.

• Makesurethatyouhaveviewedtheproperty

anditmeetsyourneeds,andthatyouarehappy

withanyclausesabout,forexample,occupation

dateandoccupationalrent.

• Youshouldbesatisfiedthattheselleroroccupant

willleavethepropertywillinglywhenneeded.

• Youmayaskforthetransferofthepropertyto

bedelayeduntiltheselleroroccupanthasleft

theproperty.

2. Home loan agreement

Whenyouapplyforahomeloanfromus,yousign

acontractcalledaloanagreement.Signingthe

agreementmeansyouagreetoallthetermsand

conditionsoftheagreement.Youmustreadallof

thetermsandconditionsverycarefullybeforeyou

signtheagreement.Ifyouhaveanyquestions,

pleaseaskoneofourrepresentativesoralawyerto

explainthemtoyou.

3. Building contract

Thisisacontractyousignwithabuildingcontractor

tohaveyourhousebuilt.SeeChapter8–Building

loans–formoreinformationaboutbuildingcontracts.

Breach of contract

Ifyoubreakanyofthetermsandconditionsof

theagreement,youwillbeinbreachofcontract.

Forexample,ifyoudonotpayyourfullinstalment

amountbytheduedate.

Whathappensifyouareinbreachofyourhome

loanagreement?

20

Ifyoudonotpayaninstlament,thefollowingcan

happen:

• Wewillletyouknowinwritingthatyouhavenot

paidtheinstalmentduetous.

• Youwillbeaskedtocontactustomake

arrangementstorectifythesituation.

• Ifyoudonotcontactus,andyouraccount

remainsinarrears,wewillhandyouraccount

overtoourlawyers.Yourhousecouldbetaken

fromyouandsoldtosomeoneelse.

• Themoneywegetfromthesaleofyourhome

willbeusedtopayofforreducetheoutstanding

loanamount.

• Youwillstillberesponsibleforanymoneyowing

tousafteryourhousehasbeensold.

• Yourcreditrecordwillshowthis,whichwillmake

itdifficultforyoutogetcreditinthefuture.

You can contact our Customer Debt Management

(CDM) department on 0860 102 270 if you are

having financial difficulty and want to discuss

your options with us.

Chapter 7 – Wills

Making a will

Duringyourlifetimeyoucollectpossessionscalled

yourassets.Theycouldbe:

• Acar

• Money

• Abusiness

• Ahouse

Duringyourlifetimeyoucanalsoincurliabilities.

Youhaveanobligationtopaytheseaccountsand

debts.Theycouldbe:

• Debts,likehirepurchase

• Loanagreements

• Storeaccounts

• Schoolfees.

Yourestateismadeupofassetsandliabilities.When

youdieyourassetsandliabilitiescontinuetoexist.

Yourestateisnowcalledadeceasedestate.Your

relativeswillneedtoknowwhattodowithyour

estate.Youareresponsiblefordecidingwhatisdone

withyourestateandyouwillneedtodrawupawill.

Awillisadocumentthathasinformationabout

yourestateandsayswhatmusthappentoitwhen

youdie.Awillletsyoumakethedecisionastowho

shouldinherityourhouse.Asahomeowner,it’s

importanttohaveawill.

Inyourwill,younamethepeoplewhomyouwant

toinherityourestate.Thesepeoplearecalledyour

beneficiaries.Theycanbeyourspouseorpartner,

yourchildrenorrelatives.

Ifyoudieandthereismoneyoutstandingonyour

homeloan,itwillhavetobepaidbeforeyour

beneficiarieswillbeabletoinherittheproperty.

Forthisreason,werecommendedthatyouhave

lifecovertopayoffyourhomeloansothatthe

propertycanbetransferredtoyourbeneficiaries.

Speaktoafinancialconsultantatyournearest

branchtohelpyoudrawupawill.

21

22

Chapter 8 – Building a house

Ifyouhavechosentobuildahouseinsteadof

buyinganexistingproperty,thereisinformation

youshouldknow.

Chooseabuilderordeveloperwhoisregistered

withtheNationalHomeBuildersRegistration

Council(NHBRC)

The National Home Builders Registration

Council (NHBRC)

TheNHBRCisabodythatprotectshomebuyersby

settingandmaintainingstandardsinthehome-

buildingindustry.

Check list

• Checkthereputationofthehomebuilder.

• Asktoseethehomebuilder’scurrentNHBRC

registrationcertificate.

• PhonetheNHBRCtoconfirmthebuilderisstill

registered.

• Taketimetoinspectsomeofthehousesthe

builderhasbuiltandcompleted.

• Makesurethatthebuildergivesyouacontract

forthebuildingofyournewhome.

Beforebuildingstarts,youwillneedtosigna

buildingcontractwhichmustinclude:

• Thestandnumberonwhichthehouseisbeingbuilt.

• Thesizeandpriceofthelandyouarebuying.

• Alistofallinternalandexternalfixturestobe

fittedbythebuilder,forexample,lightfittings,

plugs,ceilingsandroofcovering.

• Buildingexpenses.

• Thecostofdrawinguptheplansandlodging

themwiththelocalauthority.

• Thetimeitwilltaketobuildthehouse.

• Aguaranteefromthebuilderthatanymajor

problemswiththehousewillbefixed,freeof

charge,withinthefirstthreemonthsafteryou

movein.

• Theagreementmuststatethatifwedonot

grantyouabond,theagreementfallsaway.

Youcanapplyforaloanoncethebuilderhas

givenyouaquotationandyouhavesigned

theagreement.

Assoonasyourhomeloanisregisteredandthe

contractsigned,buildingcanbegin.

Wewillpaythebuilderordeveloperatcertain

stagesinthebuildingprocess.Forexample,

thebuilderwillgettheirfirstpaymentoncethe

foundationshavebeenlaid.

Letter of satisfaction or ‘happy letter’

Whenthehouseiscompleted,thebuilderwilllet

youknowwhenyoucanmoveintoyournewhome.

Thebuilderwillgiveyoualettertosign.Thisletter

iscalledadeliverynote,letterofsatisfactionora

happyletter.

Youmustbesatisfiedwiththebuilder’s

workmanshipbeforeyousignthehappyletter.

Donotsignitifyouarenotsatisfiedwiththehouse

orthebuilding.Donotmoveintothehouseuntil

thebuilderhasfixedeverythingyouwantfixed.

Prepareasnaglistwithallthethingsthatyouare

notsatisfiedwithandgiveittothebuilder.

Oncethesehavebeenrectifiedandyouare

satisfiedyoucansignthehappyletter.

Wewillpaythebuildertheirfinalpaymentonly

afteryouhavesignedthehappyletter.

Pleaseaskyourhomeloanconsultantforour

BuildingLoanbrochurewhichcontainsmore

informationaboutbuildingahome.

23

Chapter 9 – Sectional title

We also grant home loans for sectional title

developments

What do you buy?

Whenyoubuyintoasectionaltitlecomplexyou

buyasectionorsectionsofthecommonproperty.

Thesearecollectivelyknownasaunit.

In a sectional title development you own a unit

Thiscanbeaunitinacomplexorafree-standing

house.Theunitmayalsohaveanexclusiveuse

area,suchasagardenorparkingbay.Althoughby

lawitbelongstothesectionaltitledevelopment,

onlytheunitownerhastherighttousethisarea.

Youwillalsoshareownershipofthecommonareas,

likethedriveways,grassedareasandlifts.

Everyownerhastherighttousetheseareas.

What part of the property do you own if you buy

into sectional title?

Youwillbuyasectionplusanundividedshareof

thecommonproperty.Takentogether,thisproperty

iscalledyourunit.

What part of the building makes up a section?

Asectionextendstothemid-pointofouteror

dividingwalls,thelowerpartoftheceilingandthe

upperpartofthefloor.

What is common property?

Thecommonpropertyisthatpartofadevelopment

thatdoesnotformpartofanysection.Structures

andareasinthiscategoryinclude:

• Driveway

• Garden

• Swimmingpool

• Corridors

• Lift

• Entrancefoyer

• Parkingbay

• Outerwalls

• Foundations

• Roof.

Who controls the common property?

Commonpropertyisalwayscontrolledbythe

bodycorporate.Itsdecisionsarelegalandbinding.

Whatthismeansisthateventhoughpartsofthe

commonpropertyaredesignatedasexclusive

useareas,theyareunderthecontrolofthebody

corporateandaresubjecttotherulesofthescheme.

What is an exclusive use area?

Itisanaspectofthepropertythatyoudonotown,

butoverwhichyoualonehaveuse.Thiscouldbe

anyofthefollowing:

• Parkingbay

• Garden

• Patio

• Garage

• Storeroom.

Readthroughyourcontractcarefullytofindout

whichareasformpartofthepropertyyouwant

tobuy.Theareasshouldbemarkedclearlyonthe

propertyplanandthecontractorshouldexplainthis

toyouindetail.Askyourestateagentorlawyerfor

advicebeforeyoucommityourself.

The body corporate

Thebodycorporateismadeupofallthepeople

whohaveboughtaunitinasectionaltitle

development.Eachownerhasanequalvoteonhow

tomanagethedevelopment.Tomakemanaging

thedevelopmenteasier,thebodycorporate

electsasmallgroupoftrusteesfromamongthe

residentstomakedecisionsonitsbehalf.Usually,

thetrusteeshavetheskillstomanageasectional

titledevelopmentproperly.Thetrusteesdrawupan

annualbudget,decideonhouserulesandmanage

therunningofthedevelopment.Sometimesthe

trusteeswillusetheservicesofamanagingagent

tohelpwithtasks,forexample,calculatingand

collectingmonthlyleviesfromeachowner.

24

What does the body corporate do?

Itcontrolsandrunsthescheme.Trusteesare

appointedbythebodycorporatetoadministerthe

complexonadailybasis.Thetrusteesalsomake

majordecisionsaboutthecomplex.

Who are the trustees?

Thetrusteesareusuallyownersofunitswho

havebeenentrustedwiththetaskofdaily

administrationofthedevelopment.Theyare

appointedbythebodycorporateatanannual

generalmeeting(AGM).

Financial statements

Itisimportantthatyoucheckthefinancial

statementsofthecomplexandmakesurethatthe

trusteesarenotincurringanydebtsonyour

behalfsincethiscouldputyourpropertyatrisk

fromcreditors.

Who may not be a trustee?

• Themanagingagent;

• membersoftheirstaff;and

• anemployeeofthebodycorporate.

Levies

Apartfromtheusualmonthlyexpenses,suchas

homeloaninstalmentsandwaterandelectricity

bills,ownersofsectionaltitleunitsalsopaya

monthlylevytotheirbodycorporate.Thislevy

goestowardsthecostsofrunningthe

developmentsuchas:

• Maintenanceandrepairstotheoutsideoftheunits

• Maintenanceofthecommonareas

• Homeowner’sinsurance

• Municipalratesandtaxesforthelandonwhich

thedevelopmentisbuilt

• Waterandelectricityforthecommonareas.

Allthechargesareputtogetherandthetotalcost

issharedbetweentheowners.Thebiggeryour

sectionis,thebiggeryourshareofthetotalcosts

willbe.Ifasectionaltitledevelopmentseems

expensive,remember,astheownerofafree-

standinghouse,youwouldberesponsibleforthese

costsbyyourself.

Itisimportanttopayyourmonthlyleviesasnon-

paymentcouldresultinyourpropertybeingsoldby

thebodycorporatetorecovertheunpaidlevies.

Pleaseaskyourhomeloanconsultantformore

informationaboutsectionaltitles.

25

Chapter 10 – The National Credit Act

What is the National Credit Act?

TheNationalCreditAct(NCA)cameintoeffect

on1June2007.TheaimoftheNCAistoprotect

youfromundueriskandtocreateafairandnon-

discriminatorymarketplaceforlending.

Anumberofpracticessuchasrecklesslending,

lackoftransparency,discriminationandexploitation

ofconsumerswereidentifiedintheconsumer

creditmarket.Itwasrecommendedthatthesebe

correctedthroughtheintroductionoftheNCA.

Facts about the NCA

• Improveddisclosure

TheNCArequiresacreditprovidertogiveyoua

quotationandpre-agreementstatementbefore

youenterintoacreditagreement.Thequotation

isvalidforaminimumoffivebusinessdaysand

mustgivethefullcostofthecredit.Youwillalso

getacopyofthedocumentthatrecordsthe

agreement,whichmustbeinplainlanguage,

clearandtothepoint.

• Impactoncreditbureauxinformation

TheNCAplacesobligationsoncreditbureaux

abouttheaccuracyandretentionperiodsof

creditinformation.Theseinclude:

a)Thebureauxmustmakesurethatinformation

heldaboutyouisaccurate,uptodateand

confidential.

b)Theykeepsubjectiveadversedata–these

changefromthreeyearstooneyear.

c) Whenyoulodgeadisputeorquerywitha

registeredcreditbureauabouttotheinformation

onitsrecords,itwillneedtoinvestigatethe

disputewithin20daystofindoutitsvalidity.

Acreditprovidercannotdeclineyourapplication

ifyouhaveenteredadisputeorhavelodgeda

querywithacreditbureau.

• Unsolicited(unwelcome)selling

TheNCAspecificallybanscreditprovidersfrom

harassingyoutoapplyforcreditortoenterinto

acreditagreement.Therearealsolimitations

regardingyourenteringintoacreditagreementin

aprivatedwellingoryourplaceofemployment.

• Marketingpractices

TheNCAsetsoutrequirementsfor

advertisements–theymaynotusemisleading,

fraudulentordeceptiveinformation.Itrequires

thatifanadvertisementreferstothecostof

credit,itmustgivetheinstalmentamount,the

numberofinstalments,theinterestratethat

isapplicable,andtheresidualorfinalamount

payable,whereapplicable.

• Recklesscredit

TheNCAhaswaystodealwithdebtandto

createalternativesifyouhavetoomuchdebt.

Recklesscreditgrantingisnotallowedunder

theNCA.

Recklesscreditisdefinedasthefollowing:

a)Givingyoucreditwithoutfirstcheckingyour

abilitytotakeonfurthercredit.

b)Youbecomeoverindebtedaftertakingon

newcredit.

c) Yousignedthecreditagreementbutdid

notgenerallyunderstanditscosts,risksor

obligations.

• Thecontract

TheNCAtriestoeducateyouaboutyourrights.

TheActprotectsyoufromunfairdiscrimination

onthebasisofrace,genderorothergroundsset

outintheConstitution.

26

• Interestrates

TheNCAstatesthatacreditprovidermaycharge

aninterestratethatvariesduringthetermof

theagreement,butonlyifthevariationislinked

toareferencerate.TheNCAalsocapscharges

andinterestowedunderthecreditagreement

whenyoufallintoarrearsonyourloanorcredit

agreements.Furthermore,youwillbenotified,

inwriting,ofanychangestointerestorcredit

feesorcharges.TheNCAalsolaysdownmaximum

serviceandinitiationfees,andinterestrates

dependingonthetypeofcreditagreement.

• Costofinsurance

TheNCAstatesthatacreditprovidermayneed

youtotakeoutcreditinsurancefornolonger

thanthedurationofthecreditagreement.

i) Inthecaseoflifeinsurance,theamountof

insurancemaynotbemorethanthetotal

outstandingobligationtothecreditprovider

undertheagreement.

ii) Inthecaseofinsuranceoveranimmovable

asset,theamountmaynotbemorethanthefull

assetvalueofthatproperty.

Inaddition,youmustbetoldaboutyourrightto

waiveaproposedpolicyfromthecreditprovider

andtakeoutapolicyofyourchoice.

Wherethecreditproviderarrangesinsurancefor

you,itmaynotchargeanyadditionalamountover

andabovetheactualcostoftheinsurance.

• Disputeresolution

TheNationalCreditRegulator(NCR)actsas

aninformalcourttosortoutanyproblemsthat

youexperiencewithcredittransactions,credit

bureauxandcreditproviders.

27

Chapter 11 – Useful contact numbers

Type of enquiry Contact number

General enquiries 0860 123 001

Application forms (new and further loans) 0860 123 001

Property information service 0860 123 001

Short-term insurance

- Sales and quotations

- Service

0860 123 474

0860 123 741

Home Loan Protection Plan 0860 123 911

Home owner’s insurance

- Service

- Claims

0860 121 141

0860 123 444

Customer debt management (if you are having financial difficulty and want to discuss options with us)

0860 102 270

Properties in possession – marketing 0860 103 869

28

Chapter 12 – Income and expenditure guide

Youcancopythistohelpyouwithyourmonthlybudgeting

Net monthly income

Net monthly income Explanation Amount

Monthly salary (principal applicant)

This is the gross salary reflected on your payslip or the amount deposited in a bank account on a regular basis if you are self-employed.

R

Monthly salary (other applicants)

This is the gross salary reflected on your payslip or the amount deposited in a bank account on a regular basis if you are self-employed.

R

Allowances in cash Any cash allowance (provided it can be proven as sustainable over a period of time).

R

Commissions Any commission earned averaged over 12 months with the first and last month excluded.

R

Investments Any investment income, for example, dividends or interest averaged over the year.

R

Maintenance Any cash you get in the form of maintenance. R

Grant subsidies Any subsidises you get on a monthly basis, such as a housing subsidy from your employer.

R

Rental Rental income you get (this is the rental estimate that you give us). R

Pension Any pension amounts you receive. R

Other Any other income that may be acceptable to us. R

Total net monthly income

Total of all income R

29

Monthly expenditure

Salary deductions Explanation Amount

Tax – PAYE/SITE The amount of PAYE/SITE shown on your payslip. If you are a provisional tax payer then annual statements can be used or it can be estimated for each month.

R

Pension The amount of money deducted each month for pension or provident fund contributions as shown on your payslip.

R

UIF The amount of UIF shown on your monthly payslip. R

Medical aid The amount deducted for medical aid contributions as shown on your monthly payslip.

R

Monthly living expenses

Explanation.

Insurance premiums Any insurance premiums: • Household contents/vehicle • Home owner’s comprehensive insurance (an estimated value,

if applying for a new loan)• Cellphone • Funeral • Medical.

R

Life assurance premiums

Any life assurance premiums, including death, disability and retrenchment cover.

R

Electricity and water Average of 12 months’ electricity and water bills for all other homes as well as for the home for which you are applying for a loan. You must assume this and estimate it for the home loan you have applied for.

R

Rates, taxes, and levies

Any rates and taxes or levies applicable to other homes as well as for the home for which you are applying for a loan. You must assume this and estimate it for the home loan you have applied for.

R

Accommodation rental

Any accommodation rental. If you are currently renting but the home loan will replace your place of residence, then this can be left blank.

R

Leases Any lease agreements, including rental and vehicle leases. R

Hire purchase agreements

Any Credit agreements. R

Telephone and cellphone, including line rental

Average of 12 months’ telephone and cellphone bills. R

Alimony or maintenance

Any amounts you need to pay every month in terms of alimony or maintenance.

R

Planned savings Any amount that you have planned to save on a monthly basis. R

Donations and pocket money

If any funds you pay for pocket money or donations to charity on a monthly basis.

R

Education – fees, books and accommodation

Any education fees that you need to be pay on a monthly basis. Average of 12 months.

R

Clothing Any clothing expenses, excluding clothing accounts paid on a monthly basis.

R

30

Groceries The amount you pay for groceries on a monthly basis averaged over 12 months.

R

Medical bills Any medical bills averaged on a monthly basis, excluding medical aid.

R

Domestic and garden help

Monthly salaries of domestic and/or garden employees. R

Security Monthly premiums for security. You need to be assume and estimate this for the home for which you are applying for a loan.

R

Transport Any petrol, bus fare or parking fees averaged for 12 months, excluding any car repayment. If you have a tracker facility, you need to add this.

R

Entertainment Any entertainment expenses averaged over 12 months. R

TV rental, M-Net and DSTV subscription

Monthly subscriptions for TV rentals, M-Net and DSTV. R

Subscriptions Any other monthly subscriptions, for example, Internet service provider.

R

Suretyship payments The monthly surety payments need to be taken into account only if you have been called on to honour the surety agreement.

R

Retirement annuity contributions

Any monthly retirement annuity contributions. R

Funeral plans Any monthly funeral plan payments other than those specified under insurance premiums.

R

Retail store accounts Any monthly payments made on retail store accounts, for example, Edgars.

R

Other financial agreements

The monthly instalment or payment you make on credit cards and other loans, like vehicle and asset finance or student loans, including other home loans still in existence.

R

Other (specify) Any other living expenses not specified above. R

Total monthly expenses

Total of all expenses R

Total monthly income R

Minus total monthly expenses R

= Surplus R

Thesurplus(theamountleftoverafterexpenses)mustatleastcoverthetotalinstalmentofyournew

homeloan.

29

Authorised financial services and registered credit provider (NCRCP15)The Standard Bank of South Africa Limited (Reg. No. 1962/000738/06). SBSA 62106 08/10