WHOLESALE BANKING & MARKETS

Johann Kruger CA (SA), CFA and Gerry Daly IFRS and Financial Risk Management Consultants

IMPACT OF IFRS

IFRS accounting for financial instruments:

Loan

FX forward

Interest rate swap

Cash

Liquid resources: investment in bonds

AGENDA

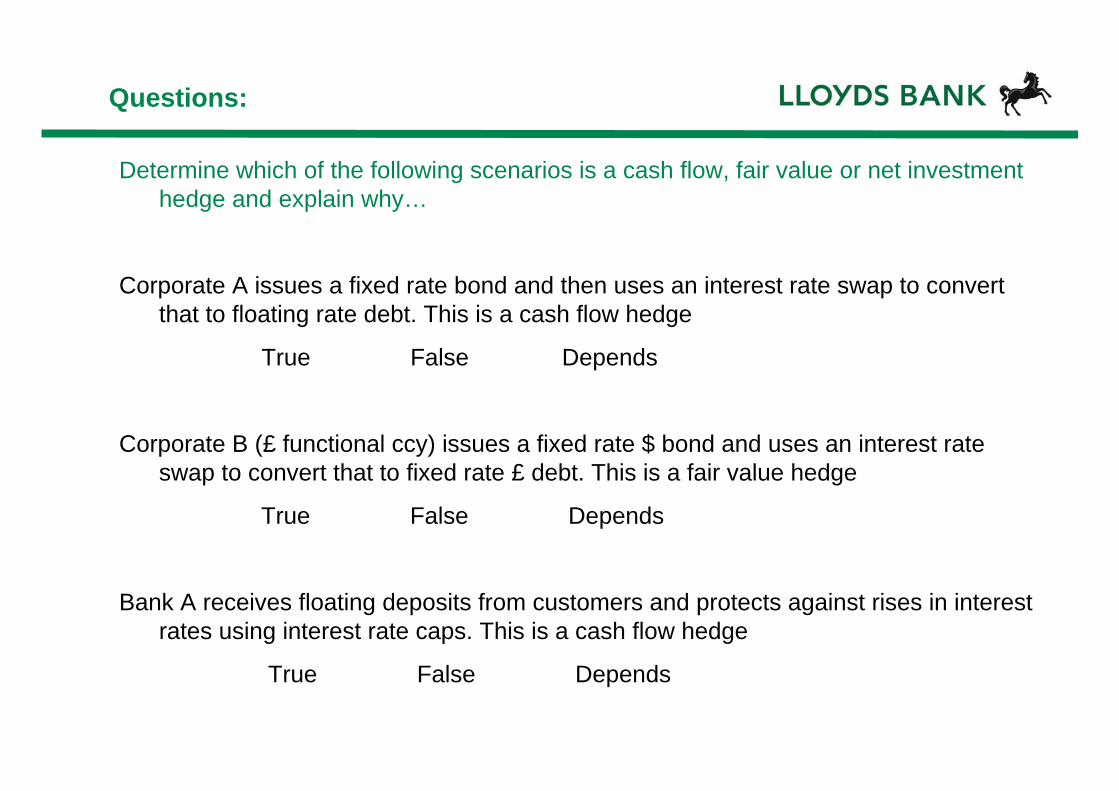

Determine which of the following scenarios is a cash flow, fair value or net investment hedge and explain why…

Corporate A issues a fixed rate bond and then uses an interest rate swap to convert that to floating rate debt. This is a cash flow hedge

True False Depends

Corporate B (£ functional ccy) issues a fixed rate $ bond and uses an interest rate swap to convert that to fixed rate £ debt. This is a fair value hedge

True False Depends

Bank A receives floating deposits from customers and protects against rises in interest rates using interest rate caps. This is a cash flow hedge

True False Depends

Questions:

Determine which of the following scenarios is a cash flow, fair value or net investment hedge and explain why…

Corporate C hedges its floating rate facility by using interest rate swaps to convert floating rate debt to fixed rate debt. This is a cash flow hedge

True False Depends

Corporate D sells an interest rate Floor to generate income. It has floating rate debt which it wishes to hedge. This is a cash flow hedge

True False Depends

Corporate E issues inflation linked debt and uses an interest rate swap to convert to fixed rate debt. This is a cash flow hedge

True False Depends

Questions:

CASE STUDY: MEET ENGINE LTD

Winning commercial contracts and managing financial risks

High value-add UK engineering company

Engine Ltd

UK held company

Pays dividends in £

£ and US$ denominated costs

£, US$ and EUR denominated sales

30% gross margin

15% net profit margin

Holds only minimally necessary cash

6

Engine wins a large contract

In May 2011 Engine ltd signed a contract for sale of engine components to big UK name (a defense contractor)

Contract involves sourcing a significant amount of high-tech components from the US

Competitors are in US, Brazil and Singapore

Where should Engine Ltd base the production for the contract?

Hedge FX on USD purchases?

How should Engine Ltd fund the project?

FUNDING THE PROJECT, INTEREST RATE RISK

Borrowings, cash, short term investments and hedging the interest rates

Funding the project

Engine arranges a bank borrowing of £10m, with a bullet repayment in 4 years Expects interest rates to rise soon – enters into an interest rate swap (‘IRS’) Draws on the loan but does not need the cash for 6 months – invests in high

quality corporate bonds Later sells the bonds and spends cash on incremental CAPEX for the project

Financial Instruments Measurement Categories –IAS 39

Fair value through PL

Available for sale

Loans and receivables

Held to maturity

FINA

NC

IAL A

SSETS

Fair value through PL

Other liabilities

FINA

NC

IAL LIA

BILITIES

PL

Not revalued

Not revalued

Equity

Fair value revaluation:

-How would the borrowing be classified?

-And the cash?

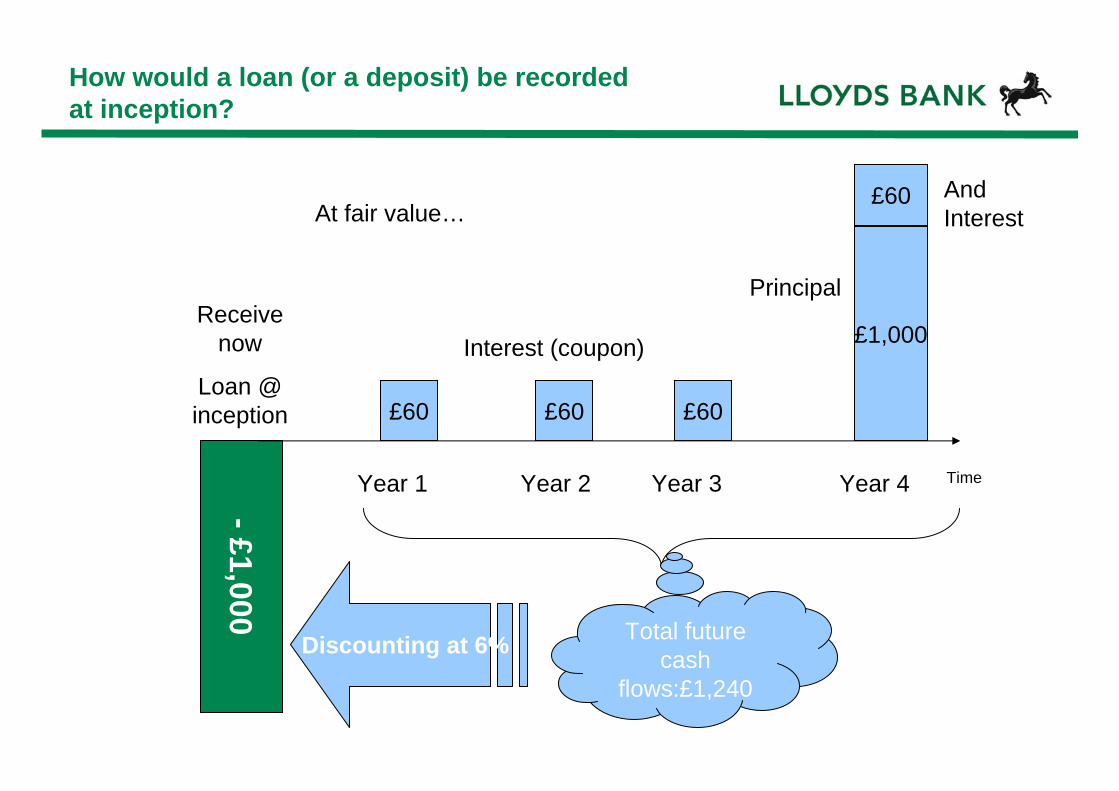

How would a loan (or a deposit) be recorded at inception?

£1,000

Year 4

£60 And Interest

Interest (coupon)

£60 £60 £60

-£1,000

Year 1 Year 2 Year 3

Receive now

Loan @ inception

Discounting at 6% Total future cash

flows:£1,240

Time

Principal

At fair value…

How would the investment in bonds be classified?

Fair value through PL

Available for sale

Loans and receivables

Held to maturity

FINA

NC

IAL A

SSETS

Fair value through PL

Other liabilities

FINA

NC

IAL LIA

BILITIES

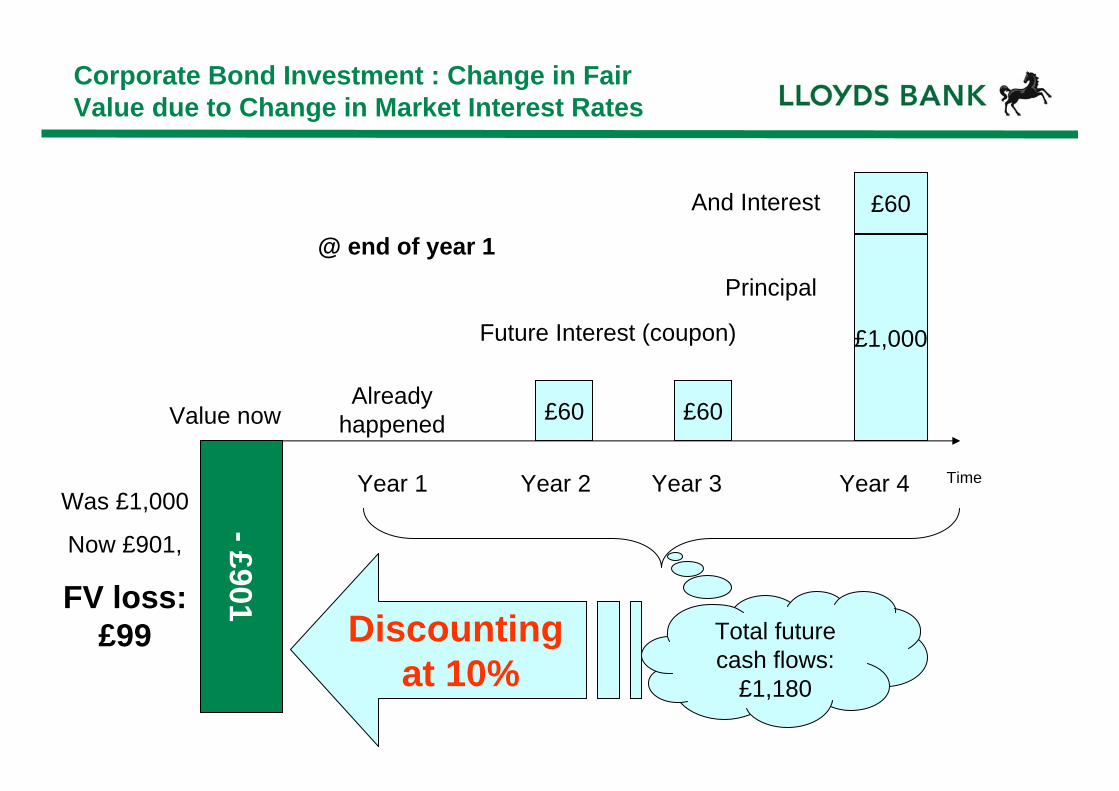

Corporate Bond Investment : Change in Fair Value due to Change in Market Interest Rates

Principal

Future Interest (coupon)

£60 £60

£1,000

-£901

Year 1 Year 2 Year 3 Year 4

£60

Total future cash flows:

£1,180

Value now

Time

Already happened

@ end of year 1

Was £1,000

Now £901,

FV loss: £99 Discounting

at 10%

And Interest

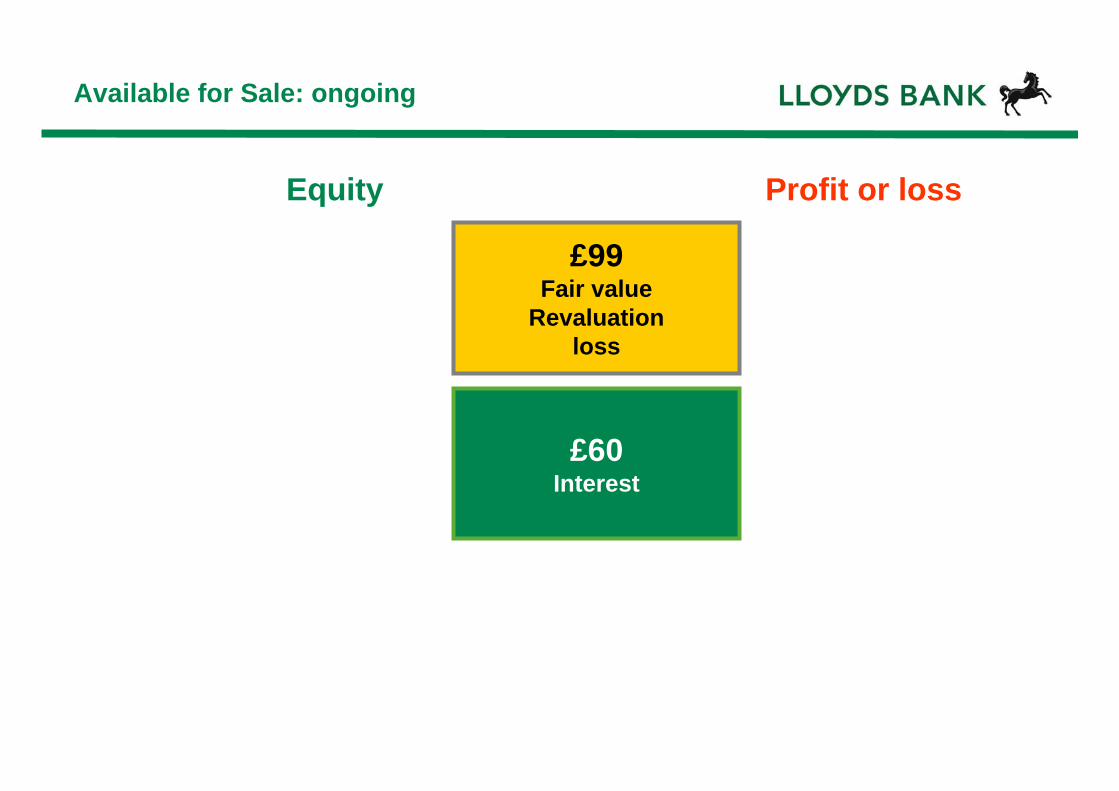

Available for Sale: ongoing

£99Fair value

Revaluationloss

£60Interest

Profit or lossEquity

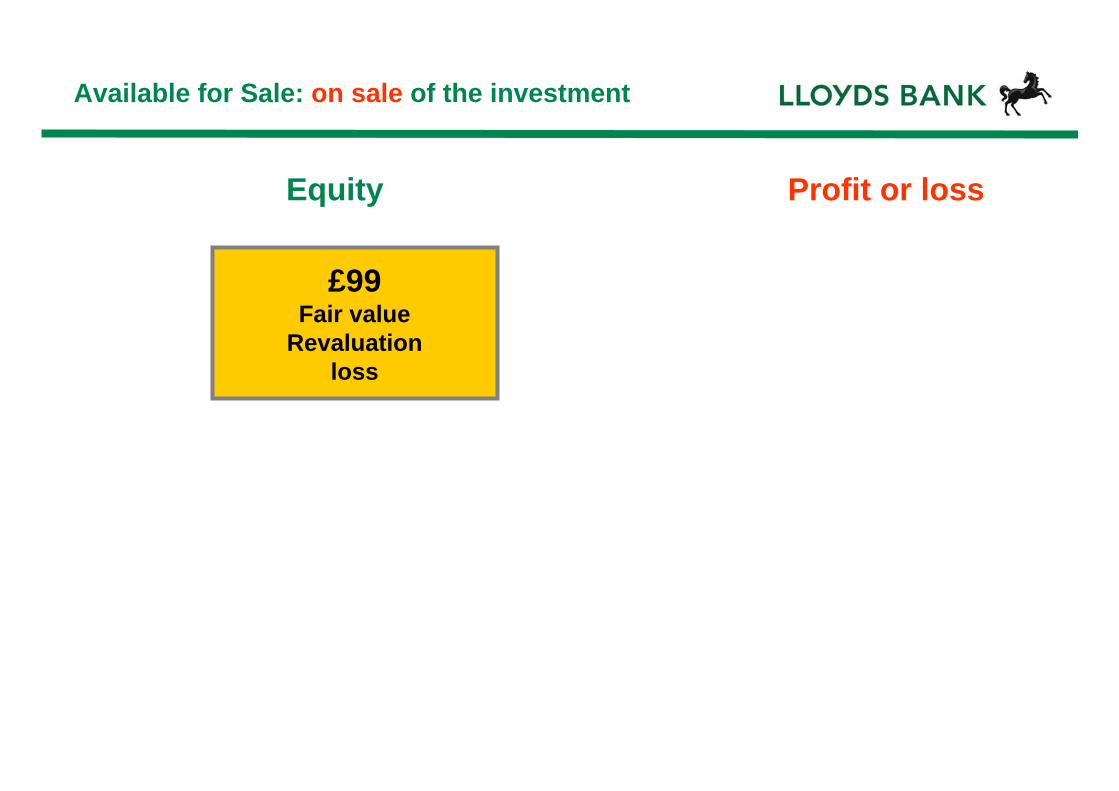

Available for Sale: on sale of the investment

£99Fair value

Revaluationloss

Profit or lossEquity

Funding the project – interest rate risk

Borrowed £10m, bullet 4 years Expects interest rates to rise– enters into an interest rate swap

Revenue uncorrelated to interest vs. floating interest on debt

Interest rate exposure

Balance sheet

Profit & Loss account

- 10mFloating rate debt

+ Fixed revenue (uncorrelated with i%)

+ £10m Operating assets

- Floating interest

Cash Flow & Accounting

Volatility

Interest rate hedge – before IFRS (UK GAAP)

Balance sheet

Profit & Loss account

-£10mFloating debt

- Fixed i% (swap)+ Fixed revenue (uncorrelated with i%)

+ £10m Operating assets

- Fixed i%+ floating i% SWAP

(FV)

+ floating interest (swap)- floating interest (debt)

= Smoother cash flows

and accounting

profits

UK GAAP: swap is off BS, coupon accruals in P&L acct

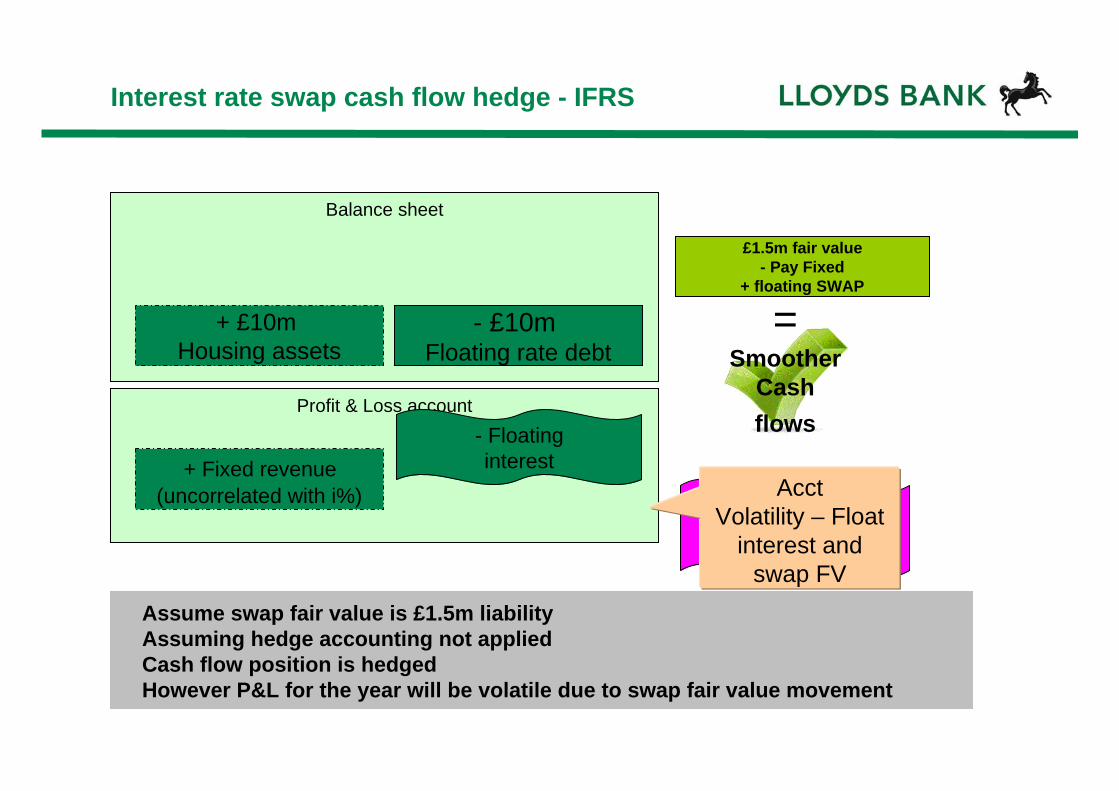

Assume swap fair value is £1.5m liabilityAssuming hedge accounting not appliedCash flow position is hedged However P&L for the year will be volatile due to swap fair value movement

Interest rate swap cash flow hedge - IFRS

Balance sheet

Profit & Loss account

- £10m Floating rate debt

+ Fixed revenue (uncorrelated with i%)

+ £10m Housing assets

£1.5m fair value- Pay Fixed

+ floating SWAP

Dr £1.5m change in FV- Pay Fixed

+ floating SWAP

= Smoother

Cash flows- Floating

interestAcct

Volatility – Float interest and

swap FV

CFH accounting allows to “park” fair value of the swap in equityAnd then release a portion to P&L to reflect the hedged rate

Cash flow hedge accounting

Profit & Loss account

Balance sheet

- £10m Floating rate debt

+ Fixed revenue (uncorrelated with i%)

+ £10m Operating assets

£1.5m fair value- Pay Fixed

+ floating SWAP

- Fixedinterest

Dr £1.5m change in FV- Pay Fixed

+ floating SWAP

Assets Liabilities

Equity

Release to P&

L- Floating interest

- Fixed interest Charge (per the swap)

Hedge effectiveness test for IRS – an example

Key Phases Of A Swap Underwrite And Syndication

Transparent: “Market Hedge”& relationship banks for syndication agreed

Confidential: Market hedge transacted based on agreed margin

Relationship: Banks supply credit / intermediation level

Competitive: Smart Hedge reviews pricing levels & selects counterparties

Counterparties informed and intermediation effected

AT EXECUTION SYNDICATION PHASEPRE EXECUTION

1 2 3 4 5

1. Defining the hedge structure

2. Testing it against IAS 39 criteria

3. Exploring the impact of not applying hedge accounting

4. Design desired solution

5. Producing hedge documentation

6. Prospective hedge effectiveness testing

7. Retrospective hedge effectiveness testing

8. Accounting journal entries

The hedging/hedge accounting process

FORMAL DESIGNATION

Reliable measurement

of effectiveness

The hedge is expected to be and is highly

effective

formal hedge documentation + risk management

policy

Requires hedge effectiveness between 80‐125%:

125%

100%

80%

No hedge accounting (P&L)

Ineffectiveness to P&L

CF: No Ineffectiveness FV: Ineffectiveness to P&L

No hedge accounting (P&L)

HedgeEffectiveness

IAS 39.96 Cash flow hedge lesser of the cumulative change

IAS 39 requires hedge effectiveness between 80-125%:

Regression parameters

R-squared >.8

Slope 0.8 to 1.25

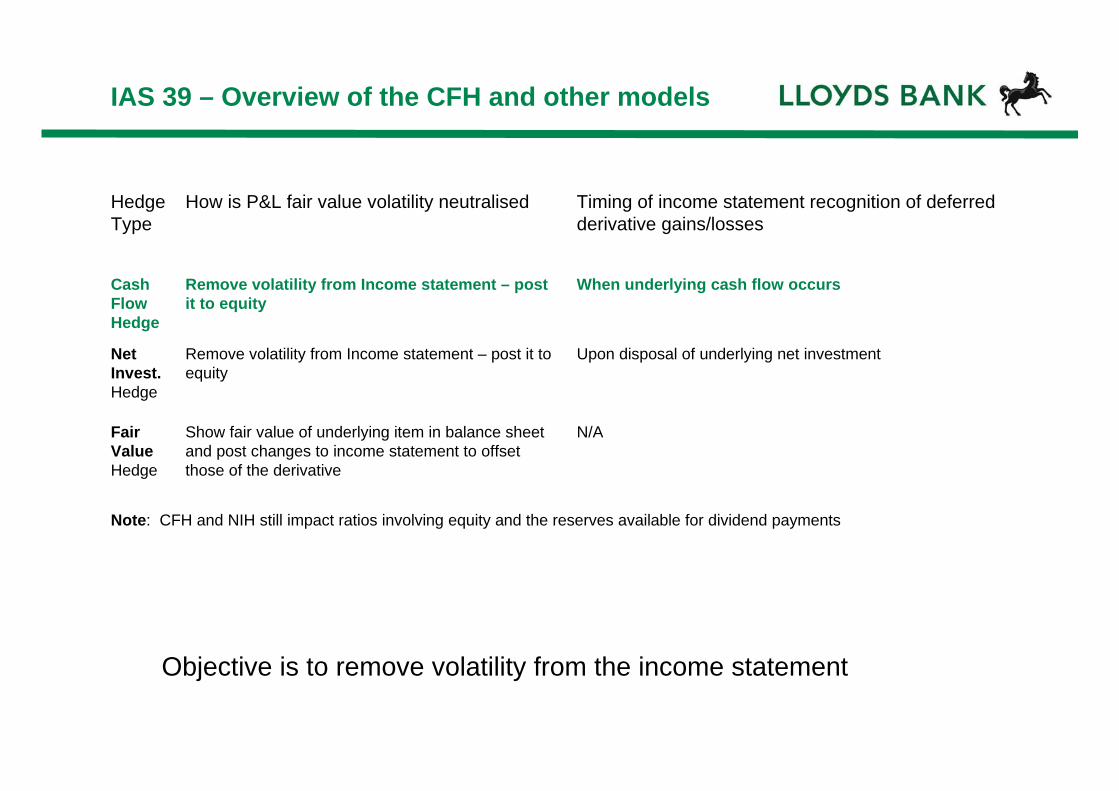

Hedge Type

How is P&L fair value volatility neutralised Timing of income statement recognition of deferred derivative gains/losses

Cash Flow Hedge

Remove volatility from Income statement – post it to equity

When underlying cash flow occurs

Net Invest.Hedge

Remove volatility from Income statement – post it to equity

Upon disposal of underlying net investment

Fair Value Hedge

Show fair value of underlying item in balance sheet and post changes to income statement to offset those of the derivative

N/A

Note: CFH and NIH still impact ratios involving equity and the reserves available for dividend payments

Objective is to remove volatility from the income statement

IAS 39 – Overview of the CFH and other models

HEDGING THE FX RISKS OF THE PROJECT

Protecting the downside FX value of future cash flows

Hedging FX

Engine decides to use FX options to hedge FX risk of USD purchases Matching maturity and amount and currency

Designated as cash flow hedges

Intrinsic value basis

Delivery of components to Energy Ltd is delayed, the USD cash flows occur 2 months late

Energy would need to amend the hypothtical derivatives, keep hedge relationship, little impact on effectiveness

Options rolled into forwards Forwards settled net

Hedge designation: FX options

Future US$ cash flow

-10 US$

Option to buy +10 US$ buy £

Time Value

Intrinsic Value

May 2011

May 2011 Jan 2012

Jan 2012

Hedge Effectiveness Report for an FX Option

FX Option – Hedge Accounting Journals

Conclusion

So what have we covered today?

Accounting for financial instruments:

Loans / borrowings Cash Investments in a corporate bonds FX options Interest rate swaps

Main hedge accounting models IFRS hedge documentation Hedge effectiveness examples

Questions?