Download - Indonesia advertising dead or alive june2013

Indonesia’s Advertising –

Dead or AliveHarris Thajeb

June 2013

Indonesia’s Advertising

Expenditure

Adex Forecast 2012 vs. 2013

0

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

2007 2008 2009 2010 2011 2012* 2012** 2013***

43,494,27550,167,960

58,316,95469,717,542

87,231,612

107,355,03999,444,038

124,531,845Rp 000,000

+19.5%

+16.2%

+15.3%

+14%

*) Actual Adex 2012**) 2012 projection based on Zenith Report***) 2013 projection based on www.emarketer.com

+25.1%

Adex Growth projection 2011 to 2012 = +14% - while the actual Adex increased

23.1% (8% higher than projection)

Adex Growth projection 2012 to 2013 = +16%

Actual Adex Source: Nielsen Media Index (only covered TV, Newspaper, Magazine & Radio), 2007-2012

+16%

+23.1%

2007 2008 2009 2010 2011 2012

RADIO 132,176 159,566 119,593 131,023 102,239 75,201

MAGAZINE 1,462,933 1,786,623 1,935,982 2,132,816 2,348,637 2,508,427

NEWSPAPER 11,225,138 14,563,473 17,921,640 21,452,387 26,126,469 30,040,592

TV 30,674,028 33,658,298 38,339,739 46,001,316 58,654,267 74,730,820

0

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

Rp 000,000

(67.2%)

(30.0%)

( 2.69%)( 0.12%)

(66.0%)

(30.8%)

( 3.1%)( 0.2%)

Adex Trend by Media 2007 - 2012

(69.6%)

(28.0%)

( 2.3%)( 0.07%)

Gross Adex 2012 by Media Type

http://metrotvnews.com/read/news/2012/01/06/77669/Televisi-Serap-60-Persen-Belanja-Iklan

Magazine

s /

Tabloid

2.7%

Newspap

er

30.0%

TV

60.0%

Radio

0.2%

Digital, Ci

nema &

Outdoor

7.1%

Combining data for mass

media &

digital/cinema/outdoor

media:

• TV was still account for the

largest share by

60%, followed by

newspaper at 30%

• Radio 0.2%

• Magazine & tabloid 2.7%

• The rest 7.1% went to digital

(mobile/internet), cinema,

and outdoor media

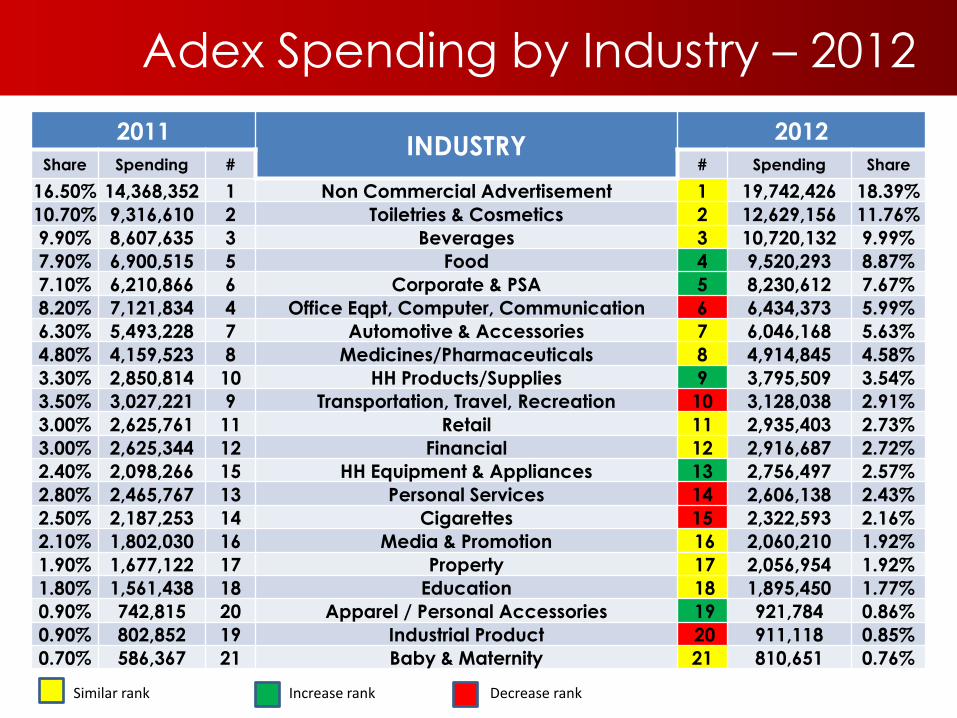

Adex Spending by Industry – 2012

2011INDUSTRY

2012

Share Spending # # Spending Share

16.50% 14,368,352 1 Non Commercial Advertisement 1 19,742,426 18.39%

10.70% 9,316,610 2 Toiletries & Cosmetics 2 12,629,156 11.76%

9.90% 8,607,635 3 Beverages 3 10,720,132 9.99%

7.90% 6,900,515 5 Food 4 9,520,293 8.87%

7.10% 6,210,866 6 Corporate & PSA 5 8,230,612 7.67%

8.20% 7,121,834 4 Office Eqpt, Computer, Communication 6 6,434,373 5.99%

6.30% 5,493,228 7 Automotive & Accessories 7 6,046,168 5.63%

4.80% 4,159,523 8 Medicines/Pharmaceuticals 8 4,914,845 4.58%

3.30% 2,850,814 10 HH Products/Supplies 9 3,795,509 3.54%

3.50% 3,027,221 9 Transportation, Travel, Recreation 10 3,128,038 2.91%

3.00% 2,625,761 11 Retail 11 2,935,403 2.73%

3.00% 2,625,344 12 Financial 12 2,916,687 2.72%

2.40% 2,098,266 15 HH Equipment & Appliances 13 2,756,497 2.57%

2.80% 2,465,767 13 Personal Services 14 2,606,138 2.43%

2.50% 2,187,253 14 Cigarettes 15 2,322,593 2.16%

2.10% 1,802,030 16 Media & Promotion 16 2,060,210 1.92%

1.90% 1,677,122 17 Property 17 2,056,954 1.92%

1.80% 1,561,438 18 Education 18 1,895,450 1.77%

0.90% 742,815 20 Apparel / Personal Accessories 19 921,784 0.86%

0.90% 802,852 19 Industrial Product 20 911,118 0.85%

0.70% 586,367 21 Baby & Maternity 21 810,651 0.76%

Similar rank Increase rank Decrease rank

The Rising Middle Class in Indonesia

World Bank reported in 2011 that 56 % of Indonesia’s 237 million population is middle class – which is around 134 millions of people

This number increased by 45 million people compared to year 2003

Source: Kompas, 19 Dec 2011, based on data from Euromonitor, World Bank

Spectacular Growth of Indonesia Middle Class

(based on daily spending per capita)

0.3 1.31.3

5.03.9

11.7

32.1

38.5

2003 2010(% of population) (% of population)

10-20 US$

6-10 US$

4-6 US$

2-4 US$

World Bank classified middle class by “daily spending ofUS$ 2 – US$ 20 ”

SES Class in INDONESIA (2012)Total population: 240,695,000

Source: Single Source, PT. Roy Morgan Indonesia, 2006 - 2012

3.8% 4.8% 5.7% 7.3% 11.5%6.0% 5.8% 7.8%12.1%

15.0%13.0% 14.7%17.9%

20.3%

23.8%28.8%34.8%

30.3%26.6%

25.8%23.5%

22.6% 19.7%18.8%

14.3%24.9%

17.3% 18.6% 14.8% 9.7%

0%

20%

40%

60%

80%

100%

2008 2009 2010 2011 2012

E

D

C2

C1

B

A

Classification based on Monthly HH Routine Expenditure

There were 49.5% of C class in Indonesia in 2012, growing significantly from 41.7% in 2008

According to BPS, Indonesia economic structure showed that consumption gives high contribution to National GDP, 1.e. around 70%

Source: www.bps.go.id

Consumption Contribution to national GDP

69%

71%

69%

68%

2000 2005 2008 2010

This middle class has their own style on spending. World Bank recorded that in 2010, this middle class spent Rp 113.4 trillion on fashion

Middle Class Spending Type

83

,73

4,3

26

13

6,8

91

,98

5

44

,82

4,2

67

18

1,8

04

,85

9

11

3,4

54

,24

5

19

4,4

93

,63

9

59

,27

8,0

32

23

8,6

65

,90

1 2007 2010

Fashion Goods & service

Shopping abroad

Transportation

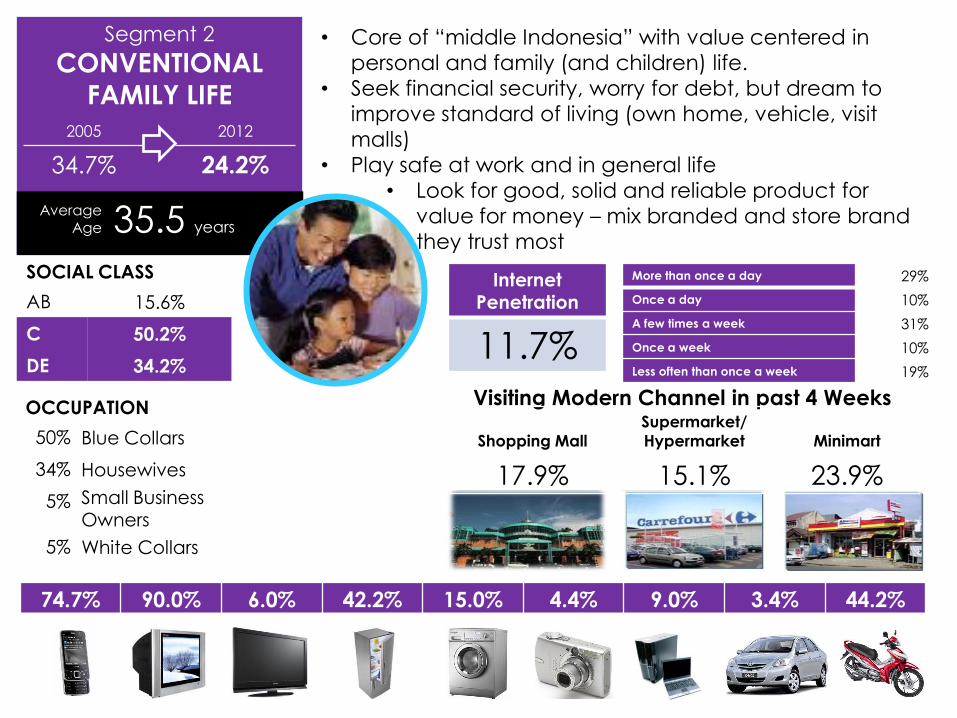

Indonesia Segmentation

2012

Segment 2

CONVENTIONAL

FAMILY LIFE

2005 2012

34.7% 24.2%

Average Age 35.5 years

AB 15.6%

C 50.2%

DE 34.2%

SOCIAL CLASS

50% Blue Collars

34% Housewives

5% Small Business

Owners

5% White Collars

OCCUPATION

74.7% 90.0% 6.0% 42.2% 15.0% 4.4% 9.0% 3.4% 44.2%

Visiting Modern Channel in past 4 Weeks

Shopping Mall

Supermarket/

Hypermarket Minimart

17.9% 15.1% 23.9%

• Core of “middle Indonesia” with value centered in

personal and family (and children) life.

• Seek financial security, worry for debt, but dream to

improve standard of living (own home, vehicle, visit

malls)

• Play safe at work and in general life

• Look for good, solid and reliable product for

value for money – mix branded and store brand

they trust most

Internet Penetration

11.7%

More than once a day 29%

Once a day 10%

A few times a week 31%

Once a week 10%

Less often than once a week 19%

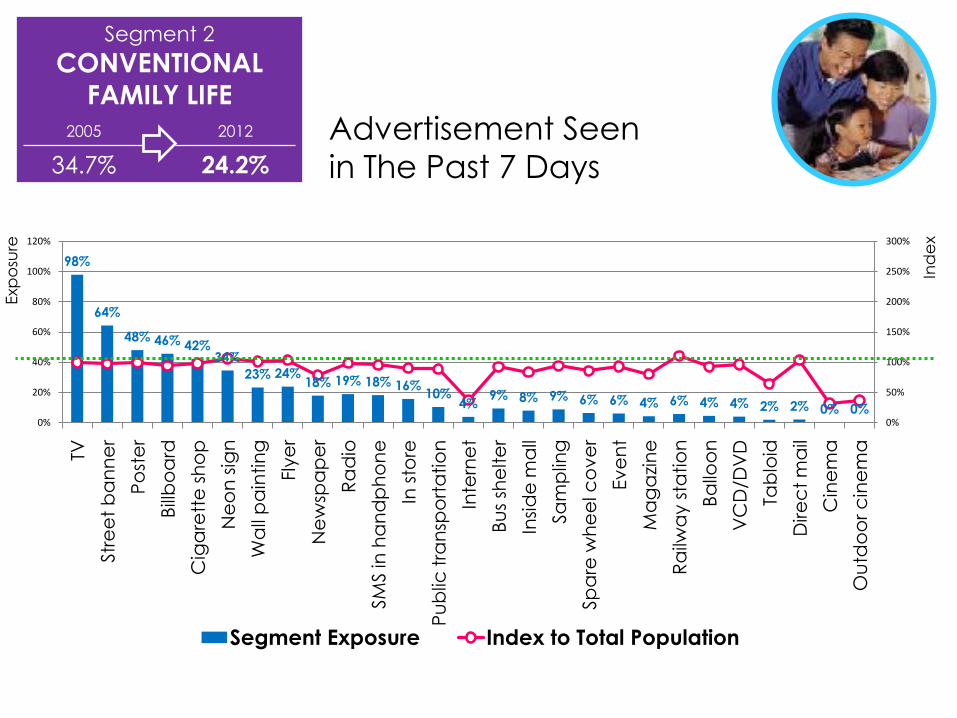

Segment 2

CONVENTIONAL

FAMILY LIFE

2005 2012

34.7% 24.2%

98%

64%

48% 46% 42%34%

23% 24%18% 19% 18% 16%

10%4%

9% 8% 9% 6% 6% 4% 6% 4% 4% 2% 2% 0% 0%0%

50%

100%

150%

200%

250%

300%

0%

20%

40%

60%

80%

100%

120%

TV

Str

ee

t b

an

ne

r

Po

ste

r

Bill

bo

ard

Cig

are

tte

sh

op

Ne

on

sig

n

Wa

ll p

ain

tin

g

Fly

er

Ne

wsp

ap

er

Ra

dio

SM

S in

ha

nd

ph

on

e

In s

tore

Pu

blic

tra

nsp

ort

atio

n

Inte

rne

t

Bu

s sh

elte

r

Insi

de

ma

ll

Sa

mp

ling

Sp

are

wh

ee

l co

ve

r

Ev

en

t

Ma

ga

zin

e

Ra

ilwa

y s

tatio

n

Ba

lloo

n

VC

D/D

VD

Tab

loid

Dire

ct

ma

il

Cin

em

a

Ou

tdo

or

cin

em

a

Segment Exposure Index to Total Population

Advertisement Seen

in The Past 7 Days

Exp

osu

re

Ind

ex

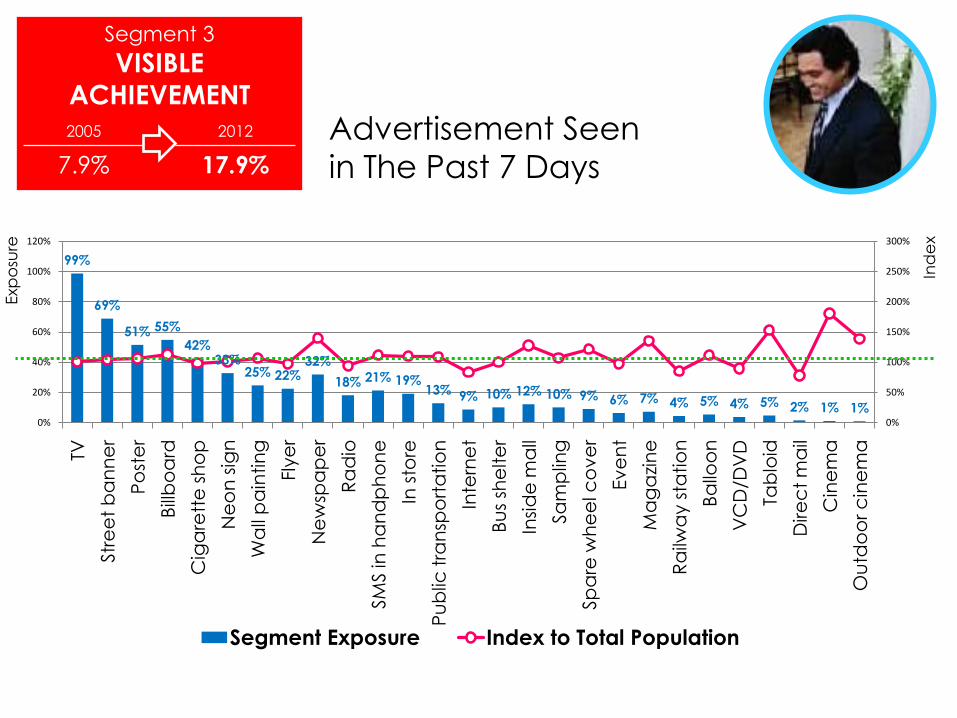

Segment 3

VISIBLE

ACHIEVEMENT

2005 2012

7.9% 17.9%

Average Age 37.2 years

AB 44.6%

C 48.2%

DE 7.2%

SOCIAL CLASS

28% Housewives

27% Blue Collars

18% White Collars

15% Small Business Owners

OCCUPATION

90.9% 90.8% 11.6% 75.6% 37.1% 14.4% 28.7% 7.1% 52.8%

Visiting Modern Channel in past 4 Weeks

Shopping Mall

Supermarket/

Hypermarket Minimart

29.8% 32.8% 37.2%

• Success and confident in their own abilities & position

• Retain traditional values about home, work and

society – work hard to provide family with high quality

environment

• Practical, realistic, and individualistic, do not need to

impress anyone

• Look for quality and value for money, not necessarily

something that is expensive

Internet Penetration

24.4%

More than once a day 27%

Once a day 16%

A few times a week 36%

Once a week 7%

Less often than once a week 14%

Segment 3

VISIBLE

ACHIEVEMENT

2005 2012

7.9% 17.9%

99%

69%

51% 55%

42%33%

25% 22%32%

18% 21% 19%13% 9% 10% 12% 10% 9% 6% 7% 4% 5% 4% 5% 2% 1% 1%

0%

50%

100%

150%

200%

250%

300%

0%

20%

40%

60%

80%

100%

120%

TV

Str

ee

t b

an

ne

r

Po

ste

r

Bill

bo

ard

Cig

are

tte

sh

op

Ne

on

sig

n

Wa

ll p

ain

tin

g

Fly

er

Ne

wsp

ap

er

Ra

dio

SM

S in

ha

nd

ph

on

e

In s

tore

Pu

blic

tra

nsp

ort

atio

n

Inte

rne

t

Bu

s sh

elte

r

Insi

de

ma

ll

Sa

mp

ling

Sp

are

wh

ee

l co

ve

r

Ev

en

t

Ma

ga

zin

e

Ra

ilwa

y s

tatio

n

Ba

lloo

n

VC

D/D

VD

Tab

loid

Dire

ct

ma

il

Cin

em

a

Ou

tdo

or

cin

em

a

Segment Exposure Index to Total Population

Advertisement Seen

in The Past 7 Days

Exp

osu

re

Ind

ex

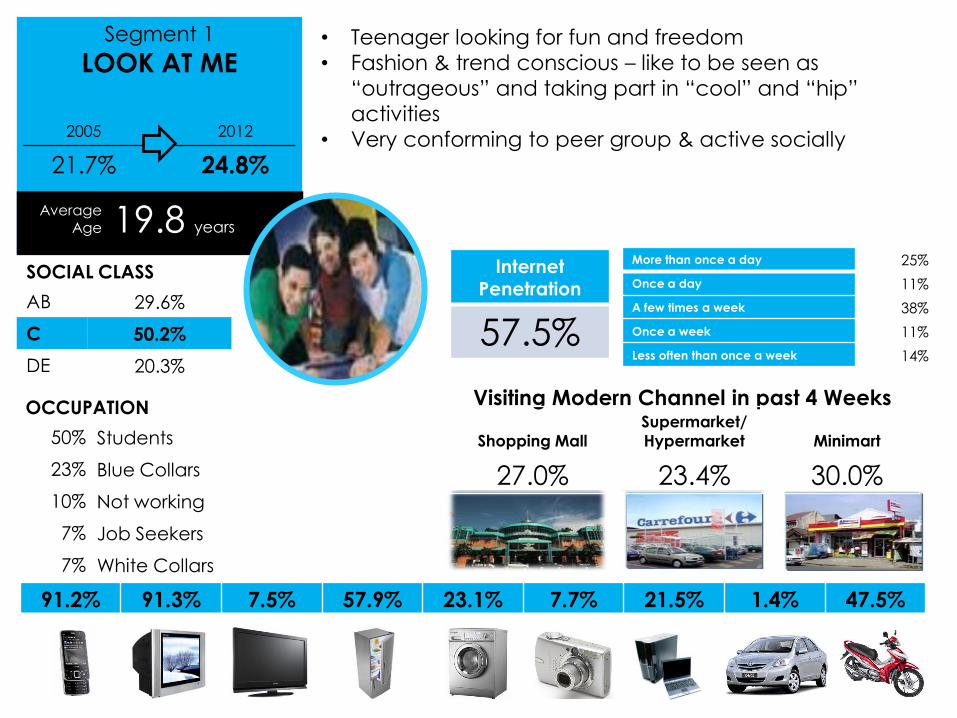

Segment 1

LOOK AT ME

2005 2012

21.7% 24.8%

Average Age 19.8 years

AB 29.6%

C 50.2%

DE 20.3%

SOCIAL CLASS

50% Students

23% Blue Collars

10% Not working

7% Job Seekers

7% White Collars

OCCUPATION

91.2% 91.3% 7.5% 57.9% 23.1% 7.7% 21.5% 1.4% 47.5%

Visiting Modern Channel in past 4 Weeks

Shopping Mall

Supermarket/

Hypermarket Minimart

27.0% 23.4% 30.0%

• Teenager looking for fun and freedom

• Fashion & trend conscious – like to be seen as

“outrageous” and taking part in “cool” and “hip”

activities

• Very conforming to peer group & active socially

Internet Penetration

57.5%

More than once a day 25%

Once a day 11%

A few times a week 38%

Once a week 11%

Less often than once a week 14%

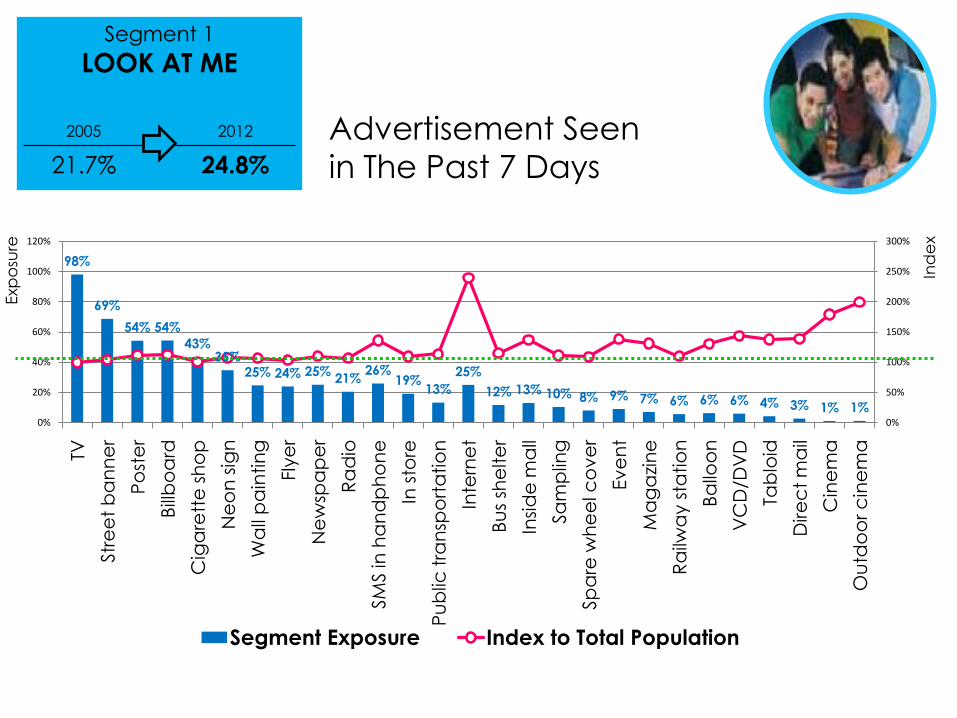

Segment 1

LOOK AT ME

2005 2012

21.7% 24.8%

98%

69%

54% 54%

43%35%

25% 24% 25%21%

26%19%

13%

25%

12% 13% 10% 8% 9% 7% 6% 6% 6% 4% 3% 1% 1%0%

50%

100%

150%

200%

250%

300%

0%

20%

40%

60%

80%

100%

120%

TV

Str

ee

t b

an

ne

r

Po

ste

r

Bill

bo

ard

Cig

are

tte

sh

op

Ne

on

sig

n

Wa

ll p

ain

tin

g

Fly

er

Ne

wsp

ap

er

Ra

dio

SM

S in

ha

nd

ph

on

e

In s

tore

Pu

blic

tra

nsp

ort

atio

n

Inte

rne

t

Bu

s sh

elte

r

Insi

de

ma

ll

Sa

mp

ling

Sp

are

wh

ee

l co

ve

r

Ev

en

t

Ma

ga

zin

e

Ra

ilwa

y s

tatio

n

Ba

lloo

n

VC

D/D

VD

Tab

loid

Dire

ct

ma

il

Cin

em

a

Ou

tdo

or

cin

em

a

Segment Exposure Index to Total Population

Advertisement Seen

in The Past 7 Days

Exp

osu

re

Ind

ex

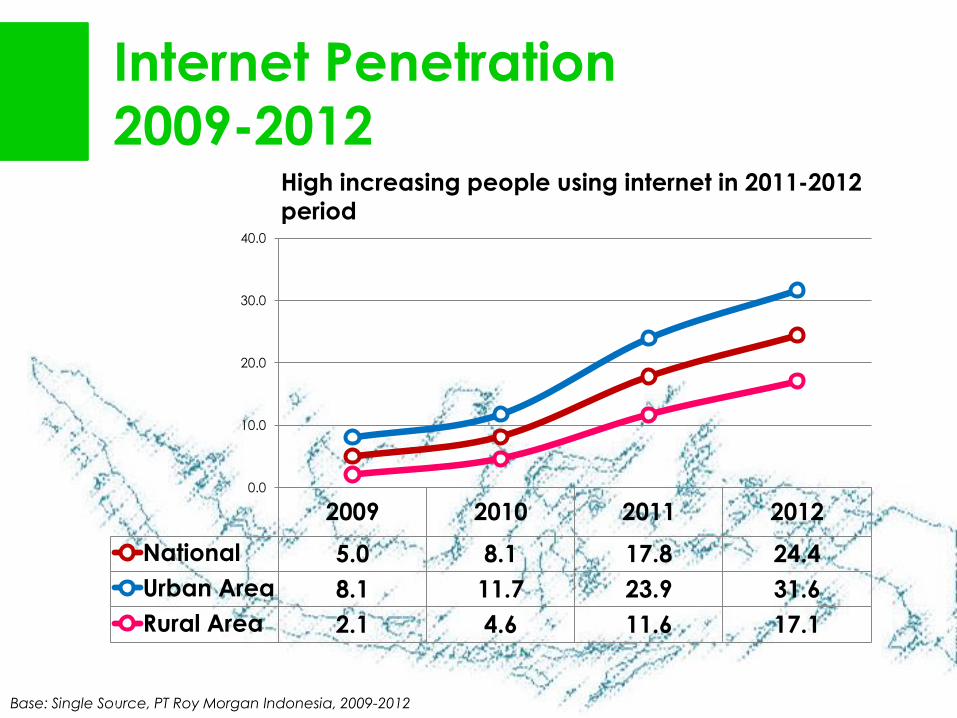

Indonesia Digital

Landscape

ASIA has the BIGGEST number of internet users in the world.

WORLD STATISTICS OF INTERNET USERS

Internet Penetration

2009-2012

Base: Single Source, PT Roy Morgan Indonesia, 2009-2012

2009 2010 2011 2012

National 5.0 8.1 17.8 24.4

Urban Area 8.1 11.7 23.9 31.6

Rural Area 2.1 4.6 11.6 17.1

0.0

10.0

20.0

30.0

40.0

High increasing people using internet in 2011-2012

period

Internet Penetration

By SES Class & Age

Base: Single Source, PT Roy Morgan Indonesia, 2009-2012

2009 2010 2011 2012

A 18.9 24.3 43.2 45.5

B 12.7 20.1 29.4 32.9

C 5.8 8.5 19.3 21.7

D 2.6 3.4 11.2 16.3

E 0.9 3.1 4.2 13.9

0.0

20.0

40.0

60.0

Fast growing internet users among

younger age group in 2011-2012

2009 2010 2011 2012

14-17 12.5 20.0 47.8 57.7

18-24 10.2 16.3 33.6 44.0

25-34 5.0 7.2 15.2 23.2

35-49 1.5 3.0 6.8 11.0

50++ 0.4 1.1 2.3 4.6

0.0

20.0

40.0

60.0

Fast growing internet users among

AB class in 2011-2012

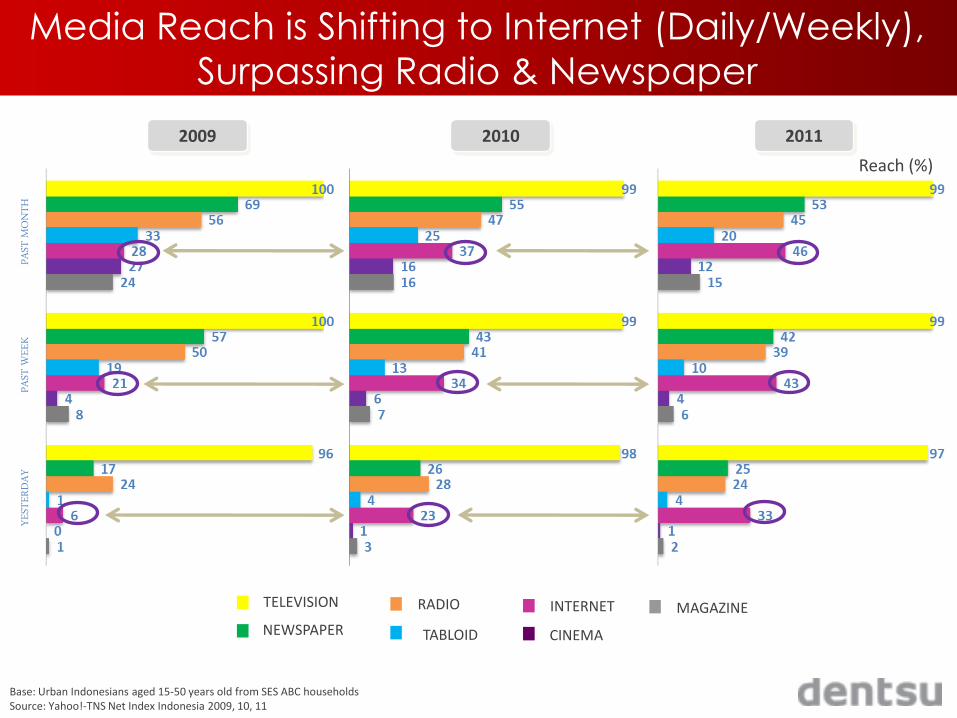

Media Reach is Shifting to Internet (Daily/Weekly),

Surpassing Radio & Newspaper

Base: Urban Indonesians aged 15-50 years old from SES ABC households Source: Yahoo!-TNS Net Index Indonesia 2009, 10, 11

2009 2010

TELEVISION

NEWSPAPER

RADIO

TABLOID

INTERNET

CINEMA

MAGAZINE

Reach (%)

2011

PAST

MON

THPA

ST W

EEK

YEST

ERDA

Y

TOTAL Base: Urban Indonesians aged 15-50 years old from SES ABC households Source: Yahoo!-TNS Net Index Indonesia 2009, 10, 11

Time & Place to Access Internet by Media

0.0

5.0

10.0

15.0

20.0

25.0

1-5 hours

6-10 hours

11-15 hours

16-20 hours

21-25 hours

26-30 hours

> 30 hours

Weekly Time Spent at Home

Laptop/Notebook

Desktop PC

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

1-5 hours

6-10 hours

11-15 hours

16-20 hours

21-25 hours

26-30 hours

> 30 hours

Weekly Time Spent at School

Laptop/Notebook

Desktop PC

0.0

2.0

4.0

6.0

8.0

10.0

12.0

1-5 hours

6-10 hours

11-15 hours

16-20 hours

21-25 hours

26-30 hours

> 30 hours

Weekly Time Spent at Work

Laptop/Notebook

Desktop PC

0.0

2.0

4.0

6.0

8.0

10.0

12.0

1-5 hours

6-10 hours

11-15 hours

16-20 hours

21-25 hours

26-30 hours

> 30 hours

Weekly Time Spent at Wifi/Hotspot Zone

Laptop/Notebook

Desktop PC

Internet Time Spent By Weeks

Internet Activities

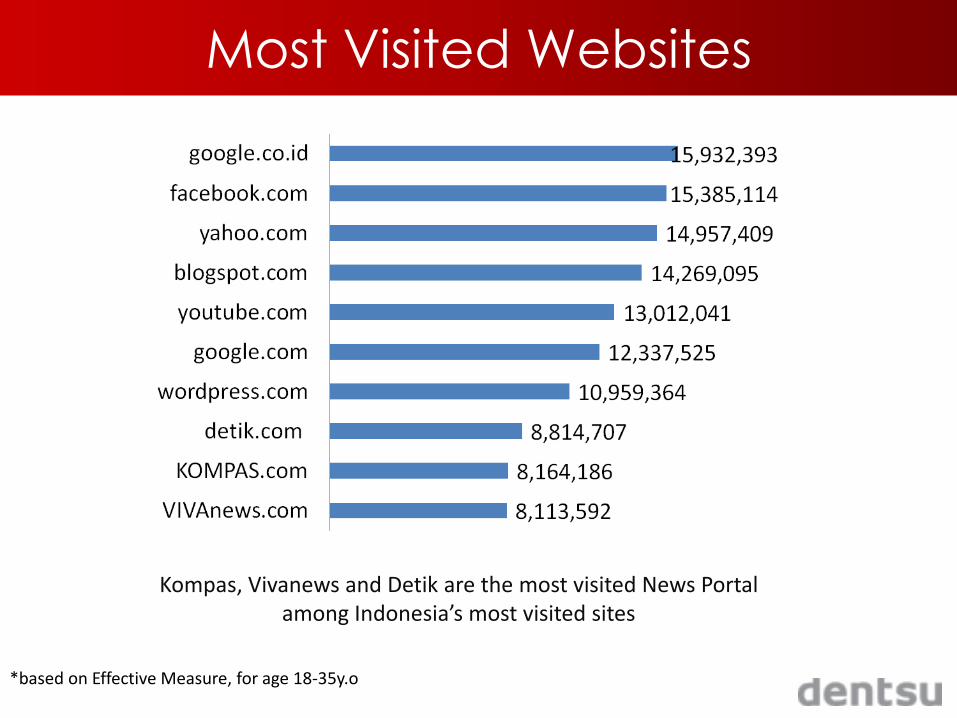

Most Visited Websites

Kompas, Vivanews and Detik are the most visited News Portal among Indonesia’s most visited sites

*based on Effective Measure, for age 18-35y.o

Total Unique

Visitors

(000)

% Reach

GOOGLE.CO.ID 6,058 86.1

FACEBOOK.COM 5,735 81.5

BLOGGER.COM 4,385 62.3

YAHOO.CO.ID 4,282 60.8

YAHOO.COM 4,153 59.0

GOOGLE.COM 3,823 54.3

YOUTUBE.COM 3,298 46.9

WORDPRESS.COM 3,185 45.3

KASKUS.US 2,185 31.0

4SHARED.COM 2,074 29.5

DETIK.COM 1,637 23.3

WIKIPEDIA.ORG 1,614 22.9

TOKOBAGUS.COM 1,391 19.8

TWITTER.COM 1,381 19.6

KOMPAS.COM 1,152 16.4

VIVANEWS.COM 1,105 15.7

Media

Comscore, MF 25+, March 2012

Top Website in Indonesia

5 best local website:

1. Kaskus.Us

2. Detik.com

3. Tokobagus.com

4. Kompas.com

5. Vivanews.com

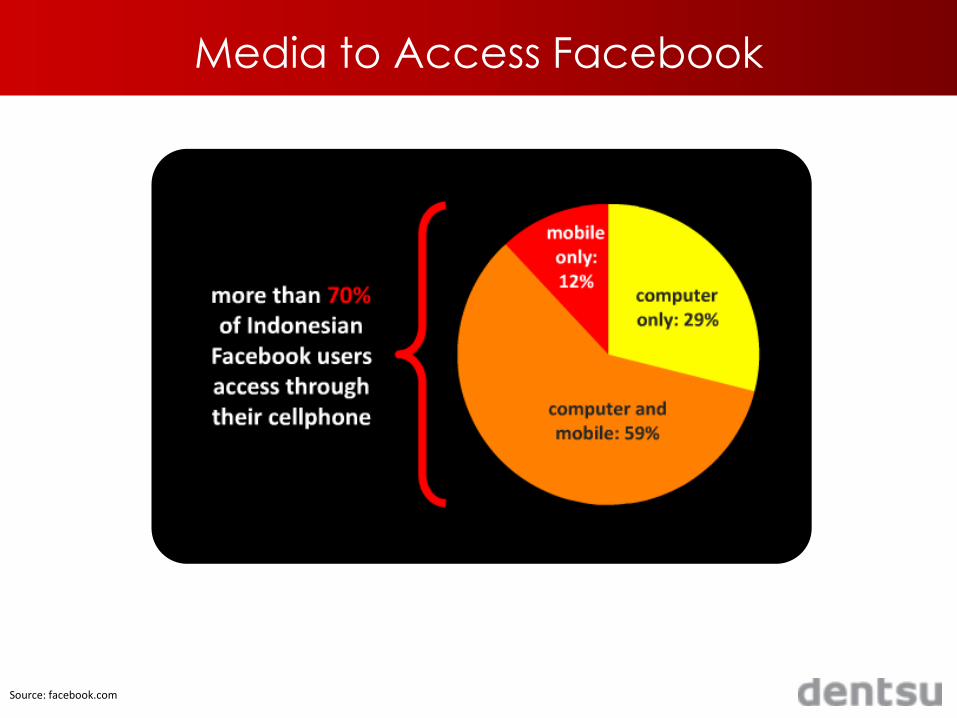

Indonesia Facebook demographics shows that the largest age group is currently 18 - 24 with total of 17.971.071 users, followed by the users in the age of 25 - 34.

Social Networking statistics show that Facebook penetration in

Indonesia is 18.04% compared to the country's population and 146.11% in relation to number of Internet users.

The total number of FB users in Indonesia is reaching 43.831.880 and

grew by more than 2.054.640 in the last 6 months.

Source: SocialBakers.com

Source: facebook.com

Media to Access Facebook

Based on tweet contribution, Indonesia is the number 3 in the history with the most tweets since 1st November 2010.

Source: aworldoftweets.com

Source: SalingSilang Engine, Indonesian Twitter Users

Twitter Access dominated by MOBILE

The Digital Market consist primarily of

young consumers age between 18 to 24 yrs

The characteristics of these young consumers are they tend to switch

and will apt to try something new

The youth dominate social media

attention interest desire memory action

awareness interest search action share

OLD

NEW

Action is now determined more by Sharing

AISAS proves the fact that digital will be a strong medium

(Branding will be strengthen by the quality of search and share)

Buying Process has Changed

sales

The level of trust of Indonesians to use

e -commerce / purchasing online is

increasing. The products mostly

purchased online are 1.Fashion

2.Travel and 3.Books

Purchasing online is increasing

The Prospect of Mobile

Advertising in Indonesia

[1] Mobile Phone Penetration is booming!

• In the past 5 years, mobile

penetration increased from

29.1% 72.3% (2011)….

It covers around 170

millions people

Source: Single Source, PT. Roy Morgan Indonesia, 2007-2011

• The highest contribution

of mobile users comes

from younger age

29.136.0

45.2

59.8

72.3

2007 2008 2009 2010 201184.9 87.9 82.2

67.4

43.0

14-17 18-24 25-34 35-49 50++

Annual Mobile

Penetration

2011 Mobile Penetration

by Age Group

Note: % of penetration by Roy Morgan calculated by excluding multiple usage of handset

Mobile Phone Penetration

2009-2012

Base: Single Source, PT Roy Morgan Indonesia, 2009-2012

2009 2010 2011 2012

National 44.2 50.7 67.8 76.4

Urban Area 54.5 59.7 75.7 83.0

Rural Area 34.3 41.9 59.8 69.6

0.0

20.0

40.0

60.0

80.0

100.0

76.% of people are now using HP, and the growth

both coming from urban & rural areas

Mobile Phone Penetration

By SES Class & Age

Base: Single Source, PT Roy Morgan Indonesia, 2009-2012

2009 2010 2011 2012

A 82.5 79.3 88.9 91.0

B 66.7 76.1 83.8 85.5

C 55.4 55.1 70.5 76.9

D 31.9 39.1 61.4 67.8

E 19.4 34.2 49.3 58.7

0.0

20.0

40.0

60.0

80.0

100.0

The younger age group are the

most using mobile phone

2009 2010 2011 2012

14-17 56.1 59.9 81.2 84.5

18-24 68.3 68.4 82.5 91.4

25-34 51.7 60.1 76.5 86.8

35-49 35.4 43.9 63.5 72.1

50++ 15.9 24.8 39.8 49.0

0.0

20.0

40.0

60.0

80.0

100.0

Fast growing usage of HP among

lower social class in 2011-2012

High mobile penetration puts Indonesia

among the largest market for Mob-Ads in the world

Source: www.buzzcity.com

Annual Mobile

Penetration

2011 Mobile

Penetration by Age

• Buzz City, global mob-ads

network, puts Indonesia as #2

market

• In Feb, BuzzCity served 1.9

billions ads to reach around

27.28 million unique audience

Audience of mob-ads is spreading

nationwide, more male than female, 56% below 30 years

Source: www.buzzcity.com

Annual Mobile

Penetration

2011 Mobile

Penetration by Age

Male76%

Female24%

Gender

• Mob-Ads users profile in Indonesia according to

< 204%

20 - 2427%

25 - 2925%

30 - 3428%

>= 3516%

Age

12.11%

6.98%

3.34%

8.43%

5.83%

13.86%

3.70%

6.12%

12.89%

26.73%

Others

Kalimantan

Sulawesi

Sumatra - Other

Sumatra - Medan

Java - Other

Java - Semarang

Java - Surabaya

Java - Bandung

Java - Jakarta

Location

Excelcom & Telkomsel are among the highest carrier for Mob-Ads

Source: www.buzzcity.com

Annual Mobile

Penetration

2011 Mobile

Penetration by Age

• Carrier for Mob-Ads in Indonesia according to

0.00%

0.24%

1.03%

8.81%

10.24%

11.17%

17.69%

18.21%

32.62%

Fren (Mobile 8)

Esia

Telkom Flexi

Indosat

Axis

Hutchison - 3

Telkomsel

Telkomsel Internet

Excelcom

Carrier

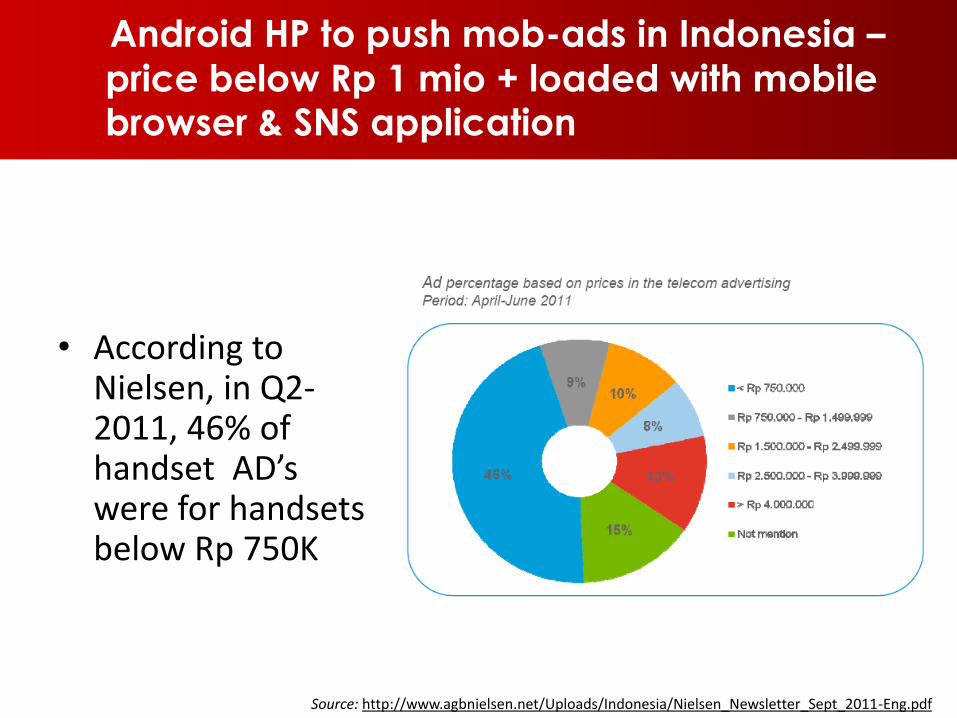

Android HP to push mob-ads in Indonesia –

price below Rp 1 mio + loaded with mobile browser & SNS application

Source: http://www.agbnielsen.net/Uploads/Indonesia/Nielsen_Newsletter_Sept_2011-Eng.pdf

Annual Mobile

Penetration

2011 Mobile

Penetration by Age

• According to Nielsen, in Q2-2011, 46% of handset AD’s were for handsets below Rp 750K

Key Success Factors

Key Success Factors

1 Clear & sharp

understanding of target

market• Not only defining target market by

demographic characteristics.

• More understanding about:

• Consumption behavior

• Shopping behavior

• General “day in a life” of target

market

• etc

Key Success Factors

2 Understanding role of

contact points in the

category• Media clutter and the fast growth of

digital/mobile media makes TV not

enough to reach the target market.

• The importance of each media is

different by category.

• Each media has different role to deliver

different messages

Key Success Factors

3 Digital Advertising (internet

& mobile) is becoming

more and more importantUtilizing digital advertising is becoming

future key success factor to reach target

market – especially youth.

• Advertiser must continuously observe the

fast growth, changes and trends in digital

world - INTERACTIVE and ENGAGING

Thank YouHarris Thajeb

June 2013