1 © GfK July 12, 2016 | Innovation, Fintech and the Future of Banking

Innovation, Fintech and the

Future of Banking

Simon Ware @siware

2 © GfK July 12, 2016 | Innovation, Fintech and the Future of Banking

Technology adoption continues to get faster and faster

3 © GfK July 12, 2016 | Innovation, Fintech and the Future of Banking

Barriers to entry are getting increasingly lower

Content courtesy of

4 © GfK July 12, 2016 | Innovation, Fintech and the Future of Banking

Key themes:

• Deal volumes continue to grow

• Deal size increasing

• Unicorns

• Growth in Asia

• Successful IPO’s

• PayPal

• Square

• WorldPay

• First Data

• Notable failure: Powa

Global investment in financial technology ventures stands at $22.6bn. It grew by $20.8bn between 2010 & 2015

Fintech investment continues to grow

5 © GfK July 12, 2016 | Innovation, Fintech and the Future of Banking

6 © GfK July 12, 2016 | Innovation, Fintech and the Future of Banking

Vertical business models will disaggregate into a new financial platform ecosystem,

enabled by regulation (e.g. PSD2) and open API initiatives

$ $ $ $ $

$

Infrastructure and

Utility Platforms

Consumer Service

Providers

$ $ $ $ $

$

Financial Product

Platforms

$ $ $ $ $

$

AISP - ACCOUNT INFORMATION SERVICE PROVIDER

PISP - PAYMENT INITIATION SERVICE PROVIDER

Including:

AS PSP – ACCOUNTING SERVICE

PAYMENT SERVICE PROVIDER

The new financial services ecosystem

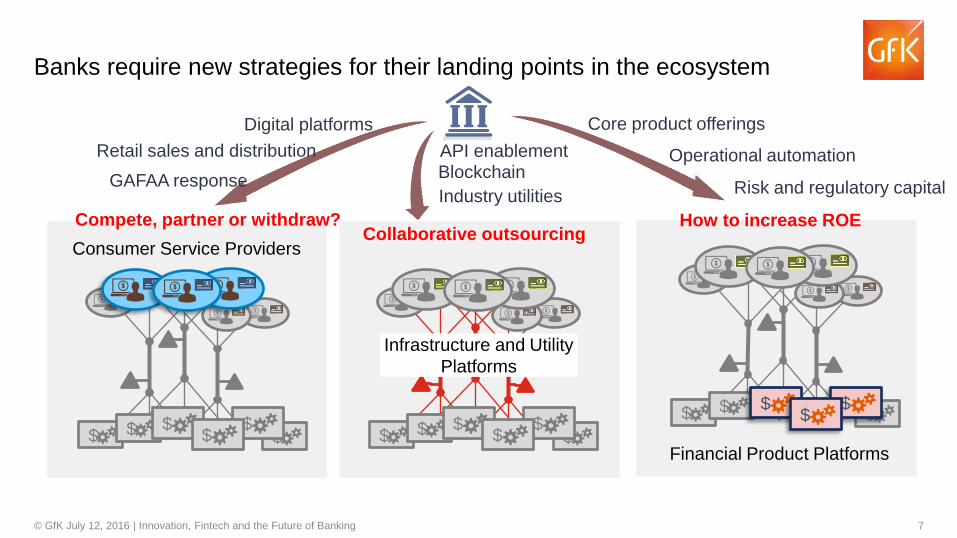

7 © GfK July 12, 2016 | Innovation, Fintech and the Future of Banking

$ $ $ $ $

$

Infrastructure and Utility

Platforms

Consumer Service Providers

$ $ $ $ $

$ Financial Product Platforms

$ $ $ $ $

$

Core product offerings

Operational automation

Industry utilities

Blockchain API enablement

Digital platforms

GAFAA response

Compete, partner or withdraw?

Retail sales and distribution

Collaborative outsourcing How to increase ROE

Risk and regulatory capital

Banks require new strategies for their landing points in the ecosystem

8 © GfK July 12, 2016 | Innovation, Fintech and the Future of Banking

Source: Accenture Research, ‘Data Sharing and Open Data for Banks’ report for HM Treasury

A number of banks in Europe are collaborating with third-party

developers and startups in pursuit of a platform model

8

4

Examples of Banks Investing in a Platform Approach

BBVA,

Spain

• Built a strong developer community using Innovation Challenges based around reuse of aggregated (not personal) data

• The bank is now in the process of building and rolling out an Application Program Interface (API) across different aspects

of its business

Banco

Sabbadell, Spain

• Launched an ‘Open Apps’ innovation program that provides limited access to some APIs for trusted developers

• Perhaps curiously, one of the first integrations the bank sponsored was with Google Glass, enabling users to see their

account balance or receive directions to an ATM.

Crédit Agricole,

France

• Credit Agricole was one of the first banks to launch [in 2012] an open API initiative, which is now the Credit Agricole app

store.

• Applications allow customers to budget their finances and manage their credit card accounts. The API also uses its own

Geolocation service for enhanced customer data on how the apps are being used.

Citi,

Global

• Partnering with startups, platform companies like Uber, and other banks. E.g. Hapoalim, the largest Israeli bank is offering

their APIs to developers to use them along with Citi APIs

• Is attracting developers from over 100 countries with programs like Citi Mobile Challenge

Fidor Bank,

Germany

• Currently developing its API platform for developers. It is engaging independent developers throughout the process.

• It has a roadmap that will open a very wide range of functionality to third parties starting with transfers, payments and

account views before moving on to more complex transactions like KYC verification and new account creation.

Garanti,

Turkey

• Turkey’s second largest bank, Garanti, opens up its APIs to partners who want to integrate with them.

• Has a large range of applications for customers, which mixes those built in-‐house with others designed by third parties

8

9 © GfK July 12, 2016 | Innovation, Fintech and the Future of Banking

Riding the forces of creative destruction

To prosper and survive incumbents need to…

Create Destroy

A digital operating

model

An enduring role in the

emerging ecosystem

Agility and innovation

An attractive culture

Unprofitable

product lines

Inefficient

operations

Legacy technology

Complacency

Fintech collaboration provides banks with a way of directing these forces

and protecting their futures

10 © GfK July 12, 2016 | Innovation, Fintech and the Future of Banking

Why are the banks collaborating?

• Access to consumers

• Access to cutting edge technology

• Poor results from in-house transformation

Both creation and destruction…

• Unsustainable cost:income ratios

• Hunger for talent and cultural challenge

Why are the fintechs collaborating?

• Access to core banking products

• Access to corporate and institutional

markets

• Access to market infrastructure

• Regulatory barriers

• High bank technology spending

The shift to Fintech collaboration

11 © GfK July 12, 2016 | Innovation, Fintech and the Future of Banking

Source: Adapted by Accenture Research from: OCTO Technology, FinTech is cannibalizing banks! (Access English version);

Data supplemented From: UK Government Chief Scientific Adviser “FinTech Futures”

By empowering new business models, Fintech are doing a

noble piece of banks’ work

P2P Payment

E-wallet Real-life txn

data

E-payment Crowdlending Crowdlending Online

advisory

Aggregated

a/c Card-linked

marketing

Invoice

trading

Bitcoin

Wallet

Digital

bank Emerging

Model

Card-linked

marketing

Current

Model Bank Credit Consultants Separate A/cs Coupon Debit Card Credit Score Credit Card Bank Credit Invoice Factoring Bank Transfer Traditional Bank

Role of Fintechs

Front Office

Customer focused

High Margin

Merchant Payment

Credit SME

Personal Loan

Project Lending

Private Banking

Bank Portal

e-Payment

Couponing Factoring fee

Bank Total Market Reach

Role of Banks

Back Office

Essential & Regulated

Low Margin

Core Banking Product

Platforms

2

12 © GfK July 12, 2016 | Innovation, Fintech and the Future of Banking

$ $ $ $ $

$

Infrastructure and

Utility Platforms

Consumer Service

Providers

$ $ $ $ $

$

Financial Product

Platforms

$ $ $ $ $

$

Examples from the Accenture Fintech Innovation Lab

13 © GfK July 12, 2016 | Innovation, Fintech and the Future of Banking

14 © GfK July 12, 2016 | Innovation, Fintech and the Future of Banking

Source: Accenture Research, Celent, Banknxt

How banks are engaging with Fintech and Innovation

• Easiest and richest way of engaging startups

• Joint research and product development, partnering on

open platform or ecosystem innovation, connecting via

incubators

Examples

• Setting up a venture capital arm to invest in startups

• Good way to get deep into emerging disruptors but

requires deep pockets, feasible by cash-rich banks

• Acquire FinTech startups outright, integrating them or

running them as standalone entities

• Risk of parent bank’s legacy processes and culture

bleeding into acquired entity

• Build new innovations in-house to create products that

rival the best of FinTech

• Likely slower speed-to-market

• Santander UK agreement with Funding Circle to drive

referrals

• Fidor Bank Germany has architected its own open

platform for third-party developers

• Santander InnoVentures invested $4 million in Ripple

Labs

• Banks’ total investment in FinTech startups is estimated

at $5bn (2015), predominantly by the US banks

• Notable acquisition of Simple by BBVA Compass

• Citi’s internal innovation team has built its own

cryptocurrency similar to Bitcoin and aimed at cross-

border transactions, branding it “Citicoin”

Collaborate

1

Invest

2

Acquire

3

Build

4