Download - INVESTING FOR A BETTER LIFE - Nielsen

1INVESTING FOR A BETTER LIFE Copyright © 2013 The Nielsen Company

F E AT U R E D I N S I G H T S

I N V E S T I N G F O R A B E T T E R L I F EA LIFE INSURANCE L ANDSCAPE STUDY IN INDIA

BY: SUBHASH CHANDRA, EXECUTIVE DIRECTOR, NIELSEN

• INTENTION TO INVEST IN LIFE INSURANCE DROPS BY THREE PERCENTAGE POINTS FROM 20% TO 17%

• LIFE INSURANCE PENETRATION IN INDIA UP BY 3% COMPARED TO 2010

• INSTANCES OF WOMEN INVESTING IN LIFE INSURANCE UP BY 6% IN 2013

For a sector that majority of Indians entrust their savings with, life

insurance is easily an important indicator of India’s financial health. And

true to this, the prevailing weak economic landscape has had an impact

on the life insurance industry in India with overall intention to purchase

polices taking a hit. But despite the weak rupee, inflation and general

concern over key financial indicators, Nielsen’s findings showed that life

insurance penetration in India is up by three percent in 2013 to touch 66

percent.

DELIVERING CONSUMER CLARITY

2 INVESTING FOR A BETTER LIFE

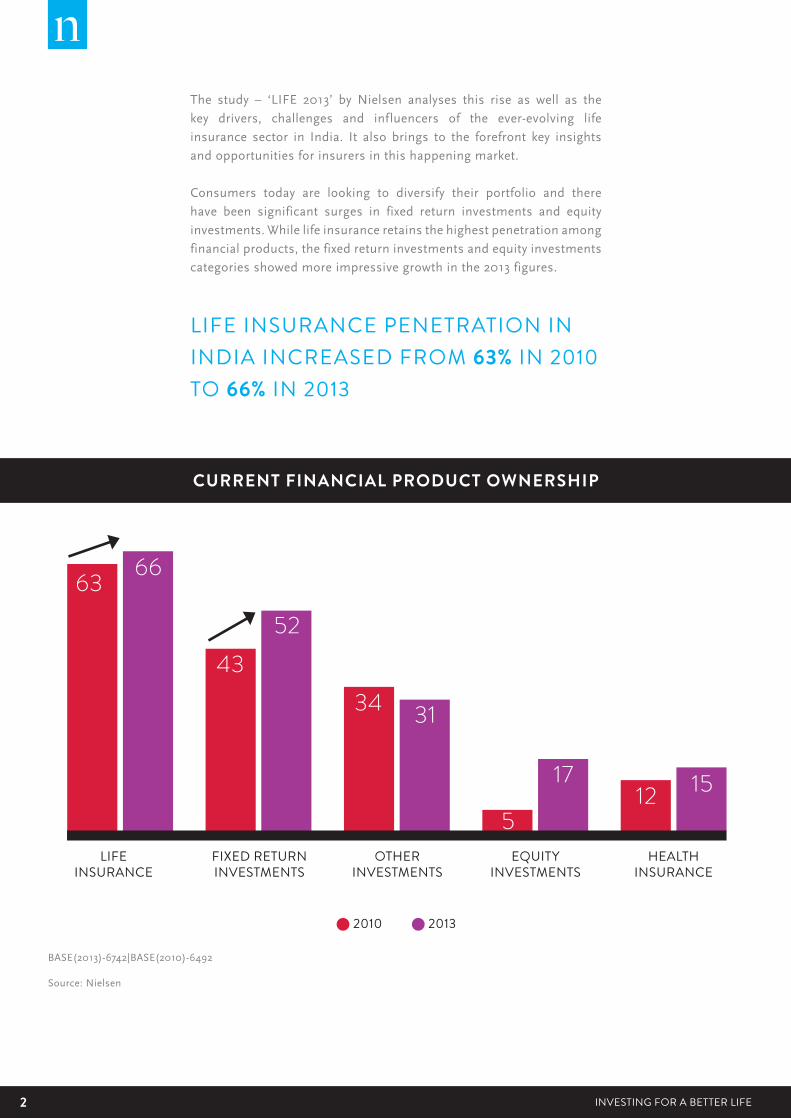

The study – ‘LIFE 2013’ by Nielsen analyses this rise as well as the

key drivers, challenges and influencers of the ever-evolving life

insurance sector in India. It also brings to the forefront key insights

and opportunities for insurers in this happening market.

Consumers today are looking to diversify their portfolio and there

have been significant surges in fixed return investments and equity

investments. While life insurance retains the highest penetration among

financial products, the fixed return investments and equity investments

categories showed more impressive growth in the 2013 figures.

2010

LIFEINSURANCE

FIXED RETURNINVESTMENTS

OTHERINVESTMENTS

EQUITYINVESTMENTS

HEALTHINSURANCE

2013

CURRENT FINANCIAL PRODUCT OWNERSHIP

BASE(2013)-6742|BASE(2010)-6492 Source: Nielsen

LIFE INSURANCE PENETRATION IN INDIA INCREASED FROM 63% IN 2010 TO 66% IN 2013

63

4352

34 31

5

1712 15

66

3INVESTING FOR A BETTER LIFE Copyright © 2013 The Nielsen Company

A smaller ticket size and single premium options for insurance covers

can prove to be useful instruments for tapping the young Indian market.

This generation of prospective buyers is likely to appreciate policies

that are flexible in terms of withdrawal and allow them to fulfill their

short-term goals.

INTENTION TO INVEST IN LIFE INSURANCE

The average Indian consumer is getting younger by the day and his

wallet’s getting fatter. More disposable income in the hands of the

youth has directly impacted their policy purchase decisions. The age

group of 22 to 30 showed a higher intent for purchase of life insurance

products (18%) than the 31 to 40 age group (16%). However, barriers

for this category included the long term nature of the investment,

followed by the low rate of returns and the challenge of getting money

back on maturity.

2010

22-30 YEARS 31-40 YEARS 41-50 YEARS

2013

INTENTION TO INVEST IN LIFE INSURANCE

Source: Nielsen

HIGHER INTENTION TO INVEST IN LI AMONG YOUNGER AGE GROUP

2119

16 17 1618

4 INVESTING FOR A BETTER LIFE

PREMIUMS UP, LIFE COVER DOWN

The average SEC B and C Indian prioritizes security, is conservative

and yearns for a better lifestyle. While life insurance covers the first two

aspects, it also promises the third in the long run. Growing awareness

and increasing salaries have resulted in a significant 1.8 times rise

in the average annual premiums paid in 2013 as compared to 2010.

However, the proportion of life cover in comparison to annual income

has come down.

BRIDGING THE GAP

While people are paying more premiums than ever before, the right way

to tap the SEC B and C market for insurers could be a more lucrative

life cover. The Nielsen survey found that the low cover was a very

important gap with half the respondents feeling that their life cover was

not adequate. Going forward, this is likely to emerge as a great window

for the emerging players.

WOMEN AND INSURANCE

There is a far higher awareness of financial products amongst women

today, whether for investment purposes, or for securing their or their

children’s future – and this leads to an active role in the financial

decision-making process within the family. The incidence of women

investing in insurance surged by six percent to touch 59 percent in 2013.

Nearly half (49%) of the female respondents cited their children’s

future as the main reason for investing in life insurance and 44 percent

indicated that life insurance was important in case of untimely death.

This shows how important it is for marketers and advertisers of life

insurance products to actively involve and engage women in their

communication.

WHILE ANNUAL PREMIUM PAID HAS INCREASED, LIFE COVER AS A PROPORTION OF INCOME HAS REDUCED.

1.3

1.07

2010

OVERALL

MEN

WOMEN

2013

LIFE COVER AS A PROPORTION OF ANNUAL INCOME

LIFE INSURANCE PENETRATION - BY GENDER

Source: Nielsen

Source: Nielsen

63

65

53

59

68

66

2010 2013

5INVESTING FOR A BETTER LIFE Copyright © 2013 The Nielsen Company

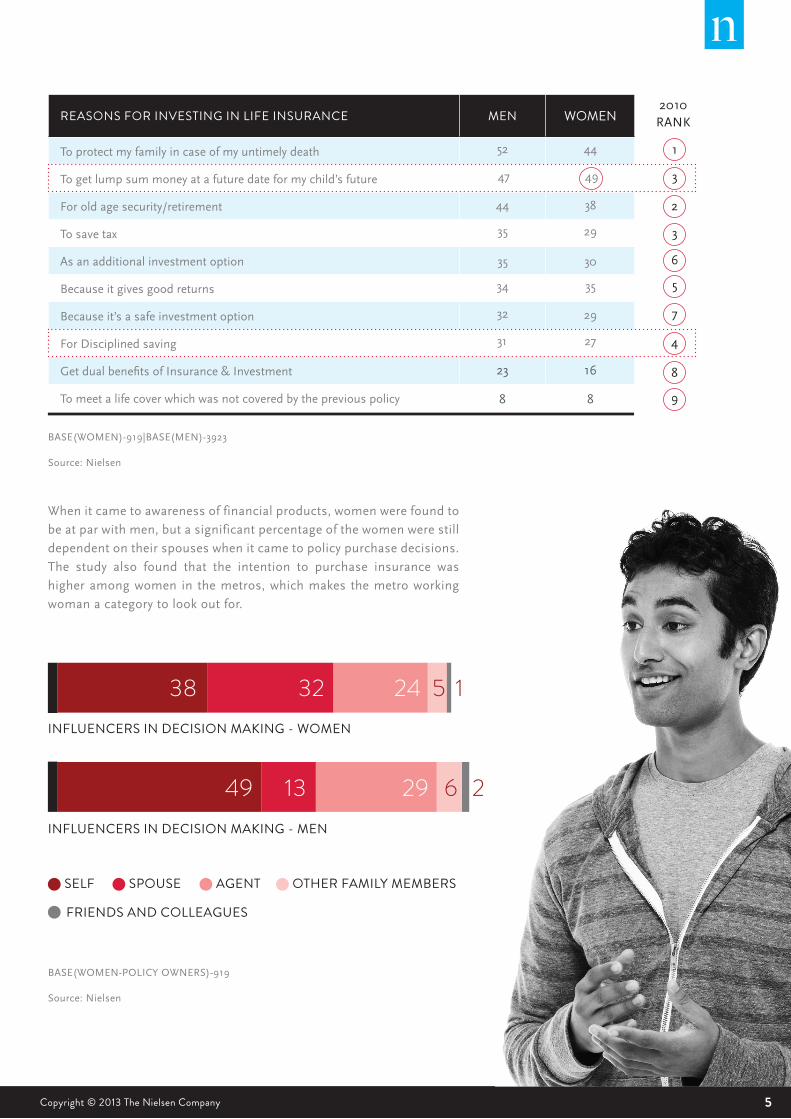

When it came to awareness of financial products, women were found to

be at par with men, but a significant percentage of the women were still

dependent on their spouses when it came to policy purchase decisions.

The study also found that the intention to purchase insurance was

higher among women in the metros, which makes the metro working

woman a category to look out for.

INFLUENCERS IN DECISION MAKING - WOMEN

INFLUENCERS IN DECISION MAKING - MEN

SELF AGENT SPOUSE OTHER FAMILY MEMBERS

FRIENDS AND COLLEAGUES

REASONS FOR INVESTING IN LIFE INSURANCE MEN WOMEN

To protect my family in case of my untimely death 52 44

To get lump sum money at a future date for my child’s future 47 49

For old age security/retirement 44 38

To save tax 35 29

As an additional investment option 35 30

Because it gives good returns 34 35

Because it’s a safe investment option 32 29

For Disciplined saving 31 27

Get dual benefits of Insurance & Investment 23 16

To meet a life cover which was not covered by the previous policy 8 8

2010RANK

1

3

2

3

6

5

7

4

8

9

BASE(WOMEN)-919|BASE(MEN)-3923

Source: Nielsen

BASE(WOMEN-POLICY OWNERS)-919

Source: Nielsen

38

49

32

13

24

29

5 1

6 2

6 INVESTING FOR A BETTER LIFE

LIFE’S GOOD FOR PRIVATE PLAYERS

A major transformation in the life insurance industry in India is the slow

but steady decentralization of dominance. Although the Life Insurance

Corporation of India (LIC) still dominates the life insurance market,

private insurers are also getting a decent share of the pie. Compared

to a paltry six percent in 2010, 16 percent of the respondents in the

Nielsen study purchased their first policy from private insurers in 2013.

The majority of these buyers belong to the SEC A category, whose

monthly earning is more than Rs 50,000, and the 22 to 30 age group,

who are willing and capable of experimenting. For private insurers, this

is an incredible opportunity to educate prospective buyers about their

products. The internet has facilitated this communication with more

people searching for information and researching financial products

online than ever before.

THE WAY FORWARDWith new entrants and private players in the mix, the insurance

landscape in India is expected to become more dynamic. In order to

attract more women and the youth, the offerings by these players as well

as the older ones will become more diversified and flexible. But since

life insurance already has a strong penetration, the trick to stand out

would be to align marketing strategies to involve these high potential

consumer categories and make them feel involved in the insurance

policy decisions of the household.

METROS

OWNERSHIP

INTENTION

NON METROS

56 7119 14

BASE(WOMEN-METRO)-1303|BASE(WOMEN NON METROS)-330

Source: Nielsen

FIRST POLICY PURCHASED FROM 2010 2013

LIC 94 84

PRIVATE 6 16

FIRST POLICY PURCHASED FROM OVERALL NEWENTRANTS

LIC 84 77

PRIVATE 16 23

Age=22-30 years

Belong mainly to SEC A

Average monthly income>50000

Source: Nielsen

7INVESTING FOR A BETTER LIFE Copyright © 2013 The Nielsen Company

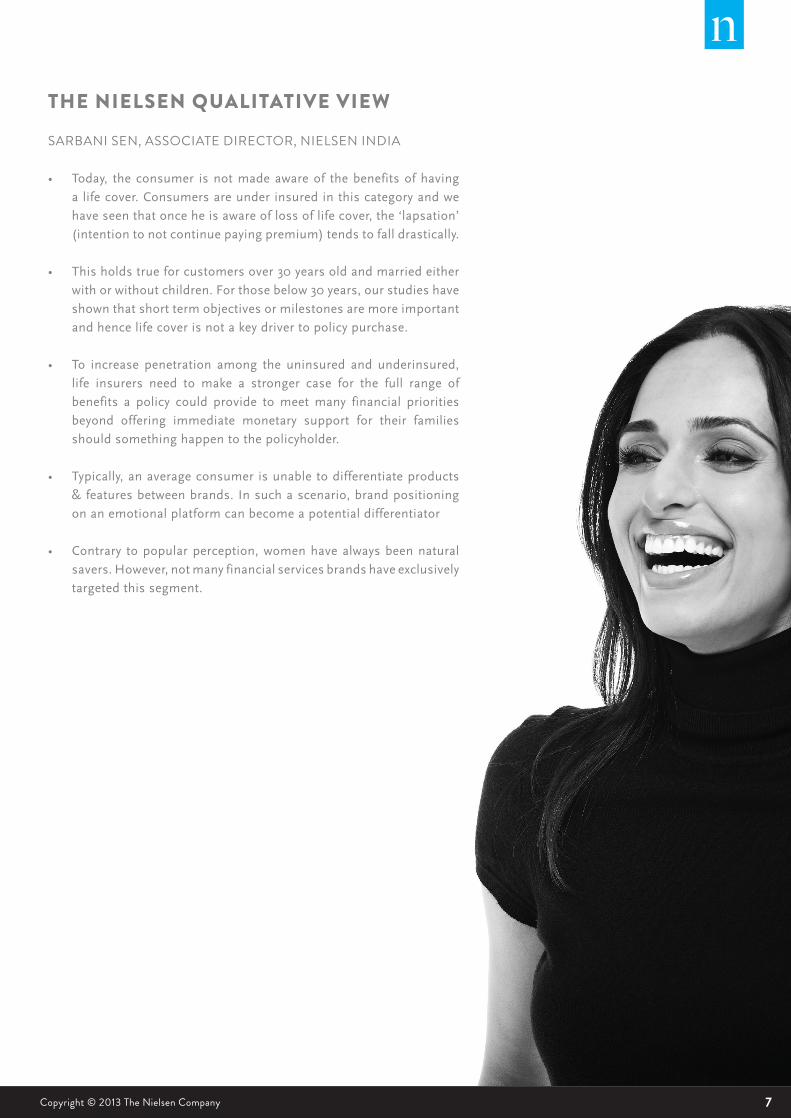

THE NIELSEN QUALITATIVE VIEW

SARBANI SEN, ASSOCIATE DIRECTOR, NIELSEN INDIA

• Today, the consumer is not made aware of the benefits of having

a life cover. Consumers are under insured in this category and we

have seen that once he is aware of loss of life cover, the ‘lapsation’

(intention to not continue paying premium) tends to fall drastically.

• This holds true for customers over 30 years old and married either

with or without children. For those below 30 years, our studies have

shown that short term objectives or milestones are more important

and hence life cover is not a key driver to policy purchase.

• To increase penetration among the uninsured and underinsured,

life insurers need to make a stronger case for the full range of

benefits a policy could provide to meet many financial priorities

beyond offering immediate monetary support for their families

should something happen to the policyholder.

• Typically, an average consumer is unable to differentiate products

& features between brands. In such a scenario, brand positioning

on an emotional platform can become a potential differentiator

• Contrary to popular perception, women have always been natural

savers. However, not many financial services brands have exclusively

targeted this segment.

8 INVESTING FOR A BETTER LIFE

ABOUT NIELSEN Nielsen Holdings N.V. (NYSE: NLSN) is a global information and

measurement company with leading market positions in marketing

and consumer information, television and other media measurement,

online intelligence and mobile measurement. Nielsen has a presence

in approximately 100 countries, with headquarters in New York, USA

and Diemen, the Netherlands.

For more information, visit www.nielsen.com.

Copyright © 2013 The Nielsen Company. All rights reserved. Nielsen

and the Nielsen logo are trademarks or registered trademarks of

CZT/ACN Trademarks, L.L.C. Other product and service names are

trademarks or registered trademarks of their respective companies.

SUBHASH CHANDRA,

EXECUTIVE DIRECTOR,

NIELSEN, INDIA

ABOUT THE AUTHOR

Vikram Budhraja & Poorva Shinde contributed to this issue of Featured

Insights