Download - Investment 101

Basic Investment Knowledge to Get You Started

Your Financial Wellbeing Workshops

Keith Tan

DISCLAIMER

This information contained within this presentation has been obtained from sources that author believes to be reliable and accurate but no representation or warranty, expressed or implied, is made as to the fairness, accuracy, completeness or correctness of the information. Neither the author nor any of his associates, nor any director, officer or employee of his company accepts any liability whatsoever for any loss arising directly or indirectly from any use of this presentation.

The presentation is being made available to you solely for your information only. It does not have regard to your specific objectives, financial situation and particular needs. This presentation is not intended for distribution to any other person. The information in this presentation may not be reproduced in whole or in part without the prior written consent of the author.

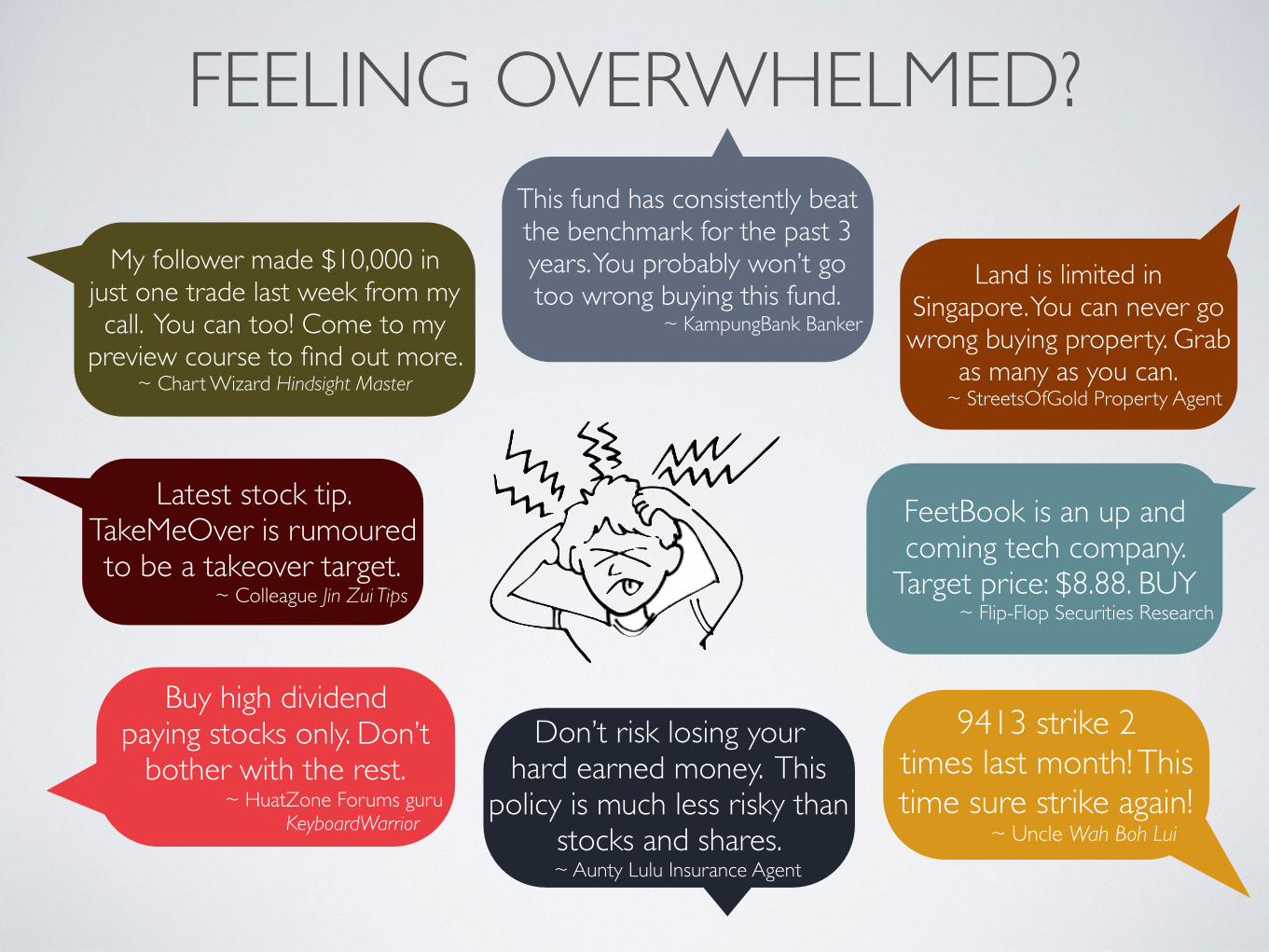

FEELING OVERWHELMED?

Buy high dividend paying stocks only. Don’t

bother with the rest.~ HuatZone Forums guru

KeyboardWarrior

9413 strike 2 times last month! This time sure strike again!

~ Uncle Wah Boh Lui

My follower made $10,000 in just one trade last week from my call. You can too! Come to my

preview course to find out more. ~ Chart Wizard Hindsight Master

This fund has consistently beat the benchmark for the past 3 years. You probably won’t go too wrong buying this fund.

~ KampungBank Banker

FeetBook is an up and coming tech company.

Target price: $8.88. BUY~ Flip-Flop Securities Research

Latest stock tip. TakeMeOver is rumoured to be a takeover target.

~ Colleague Jin Zui Tips

Don’t risk losing your hard earned money. This

policy is much less risky than stocks and shares.~ Aunty Lulu Insurance Agent

Land is limited in Singapore. You can never go wrong buying property. Grab

as many as you can.~ StreetsOfGold Property Agent

DO YOU HAVE A PLAN?

Random?

Opportunistic?

Gamble?

HOW HAVE YOU BEEN INVESTING?

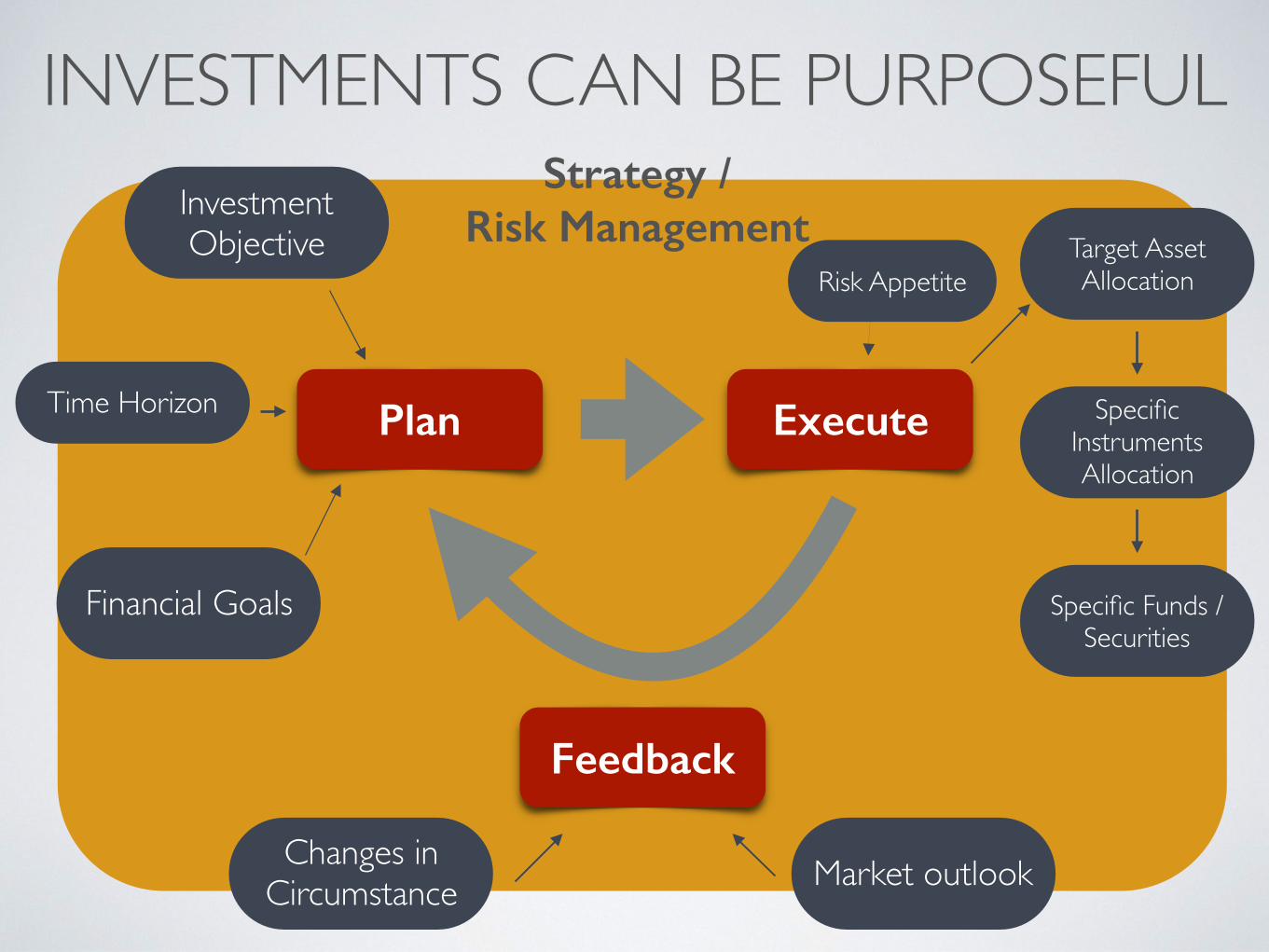

Strategy / Risk Management

INVESTMENTS CAN BE PURPOSEFUL

Plan Execute

Investment Objective

Time Horizon

Financial Goals

Specific Instruments Allocation

Specific Funds / Securities

Target Asset Allocation

Feedback

Changes in Circumstance Market outlook

Risk Appetite

PLAN• What is your investment objective?

• Passive income, retirement fund, children’s education fund, etc.

• What is your time horizon?• Short (3-5 yrs), Medium (5-10 yrs), Long (>10 yrs)

• Determine your financial goal as specific as possible• e.g. to have a retirement fund of $1.5M by the age of 60

• Determine the inputs required to reach that goal• e.g. to set aside $1000 a month, assuming a return of 5% p.a.

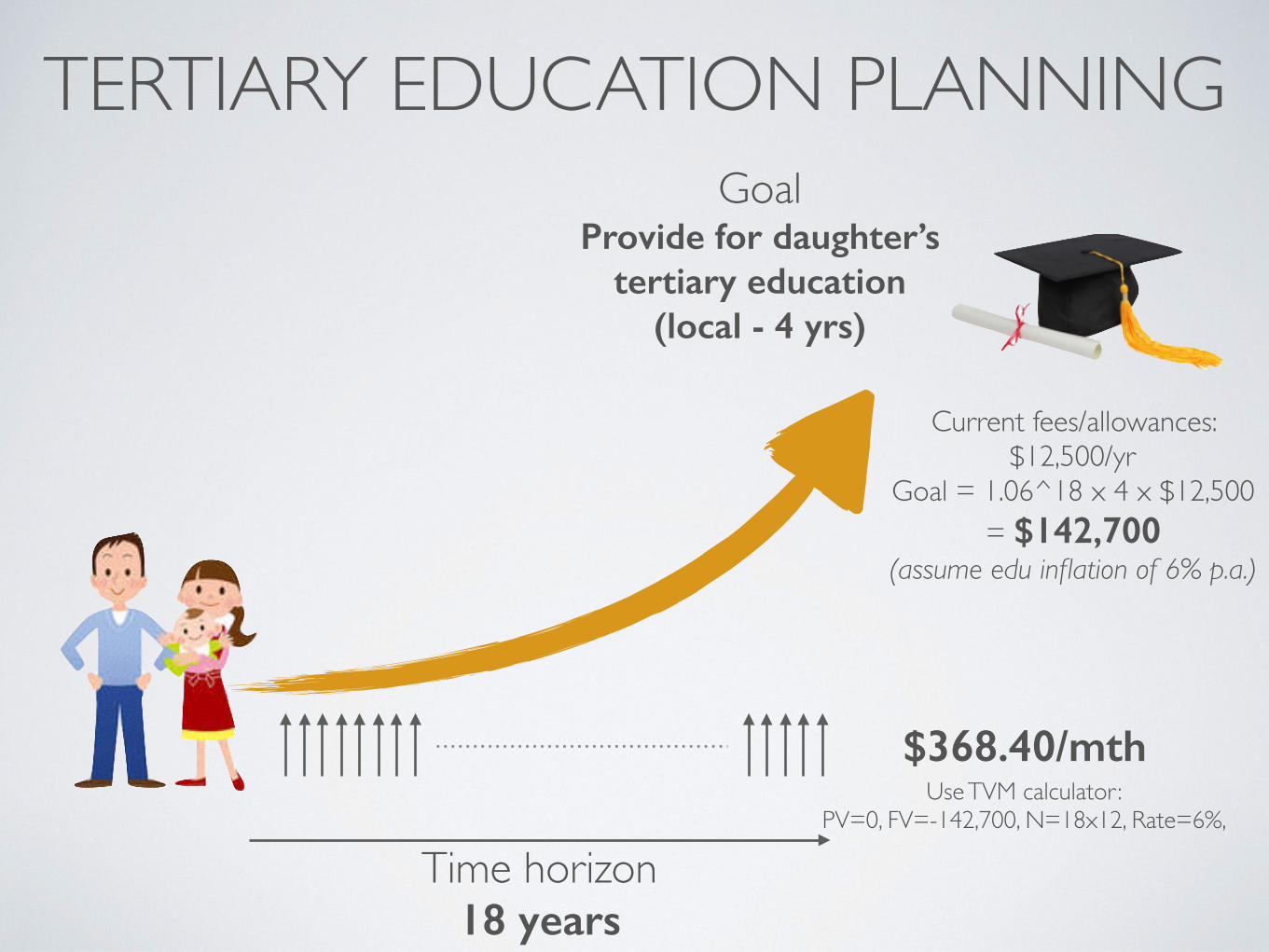

CASE STUDY

TERTIARY EDUCATION PLANNING

Time horizon18 years

GoalProvide for daughter’s

tertiary education (local - 4 yrs)

Current fees/allowances: $12,500/yr

Goal = 1.06^18 x 4 x $12,500 = $142,700

(assume edu inflation of 6% p.a.)

$368.40/mthUse TVM calculator :

PV=0, FV=-142,700, N=18x12, Rate=6%,

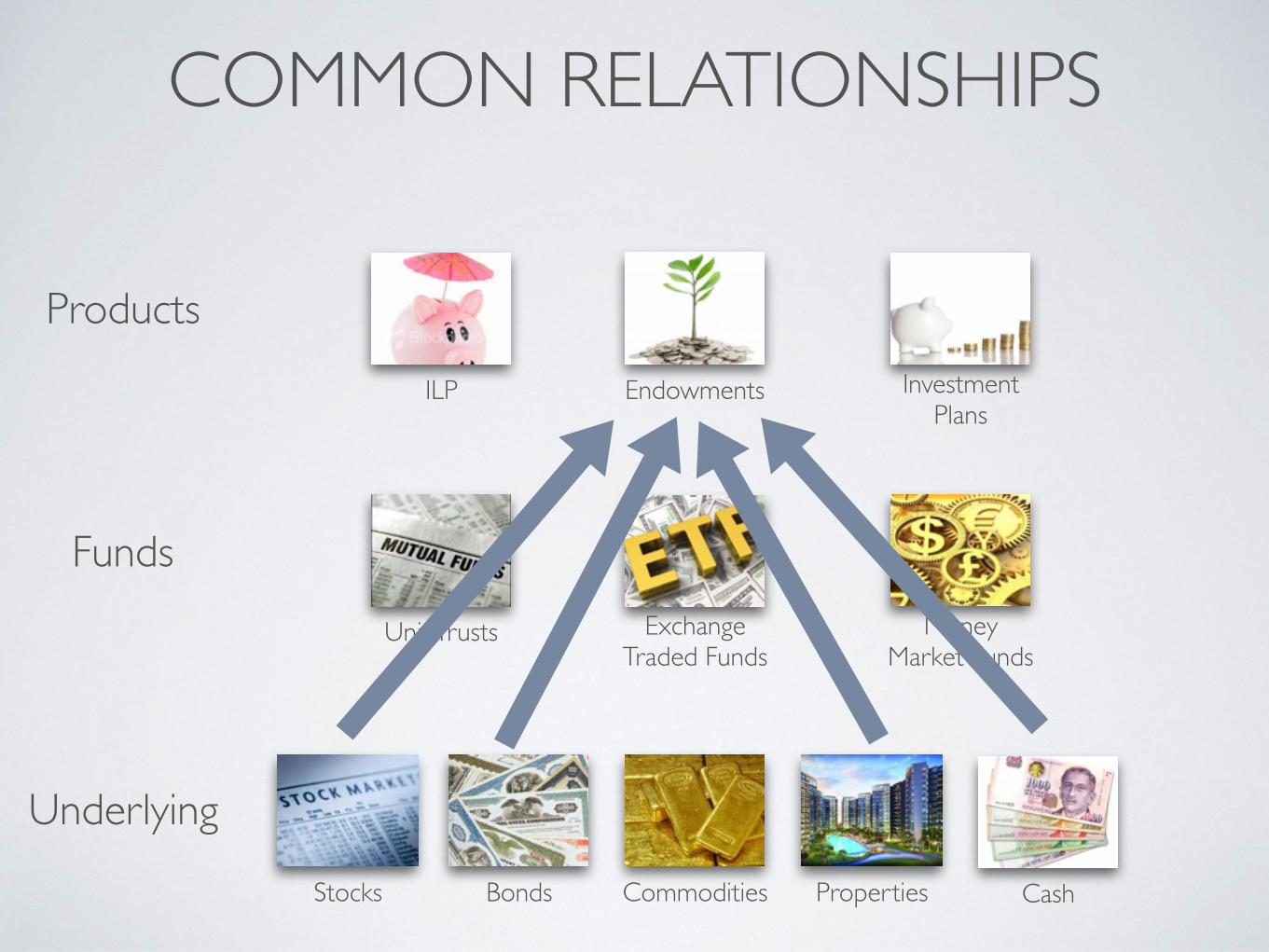

WHAT DO PEOPLE COMMONLY INVEST IN?

Unit Trusts

FundsExchange

Traded FundsMoney

Market Funds

ILP

ProductsEndowments Investment

Plans

Bonds Commodities Properties CashStocks

Underlying

COMMON RELATIONSHIPS

Unit Trusts

FundsExchange

Traded FundsMoney

Market Funds

ILP

ProductsEndowments Investment

Plans

Bonds Commodities Properties CashStocks

Underlying

COMMON RELATIONSHIPS

Unit Trusts

FundsExchange

Traded FundsMoney

Market Funds

ILP

ProductsEndowments Investment

Plans

Bonds Commodities Properties CashStocks

Underlying

COMMON RELATIONSHIPS

Unit Trusts

FundsExchange

Traded FundsMoney

Market Funds

ILP

ProductsEndowments Investment

Plans

Bonds Commodities Properties CashStocks

Underlying

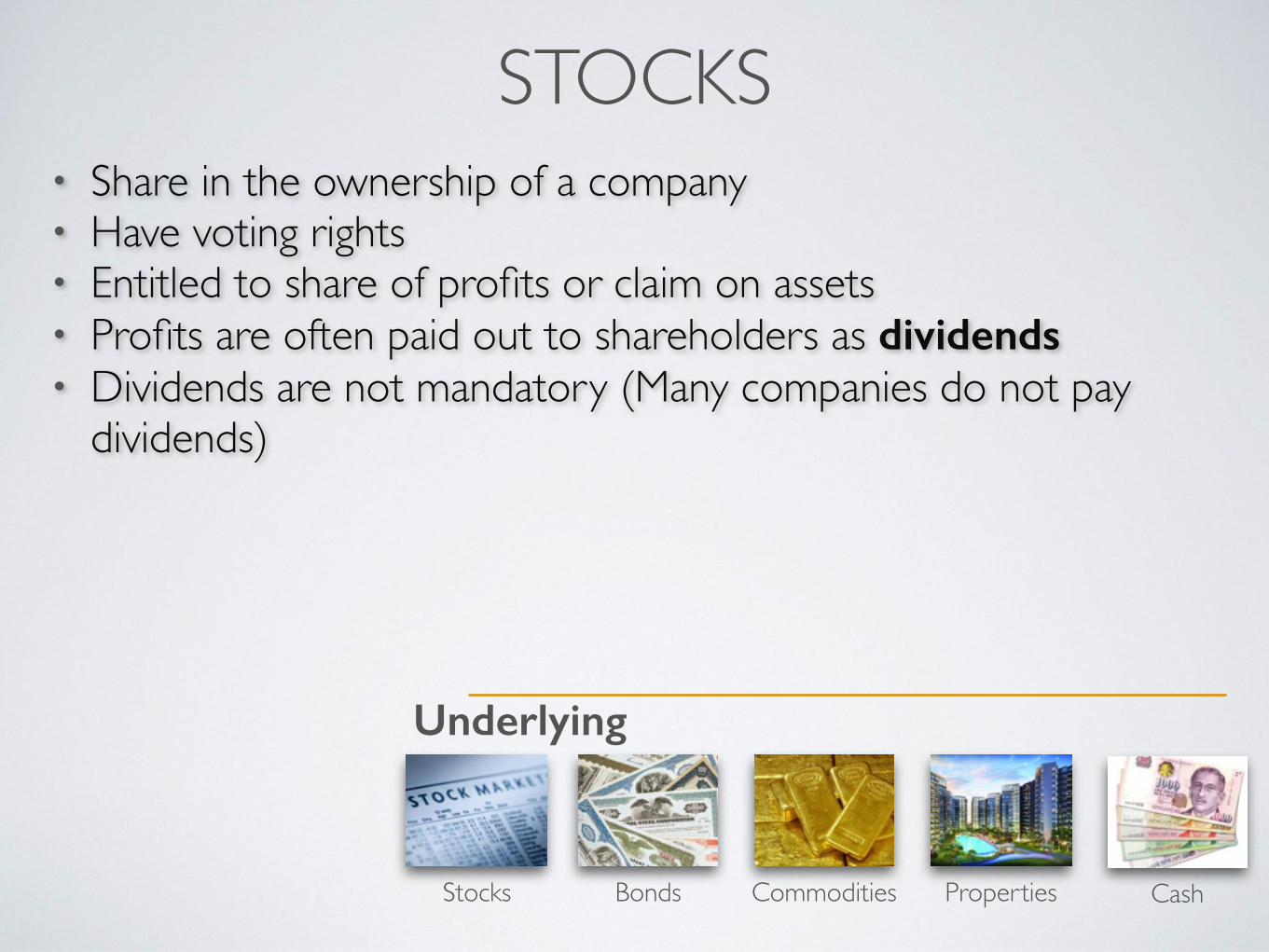

STOCKS

Bonds Commodities Properties CashStocks

Underlying

• Share in the ownership of a company• Have voting rights• Entitled to share of profits or claim on assets• Profits are often paid out to shareholders as dividends • Dividends are not mandatory (Many companies do not pay

dividends)

STOCKS

Bonds Commodities Properties CashStocks

Underlying

• Two sources:• Primary market: IPO• Secondary market: Stock exchange

(e.g. SGX)• To buy and sell in secondary market, go

through brokers

STOCKS

Bonds Commodities Properties CashStocks

Underlying

• Understanding stock prices

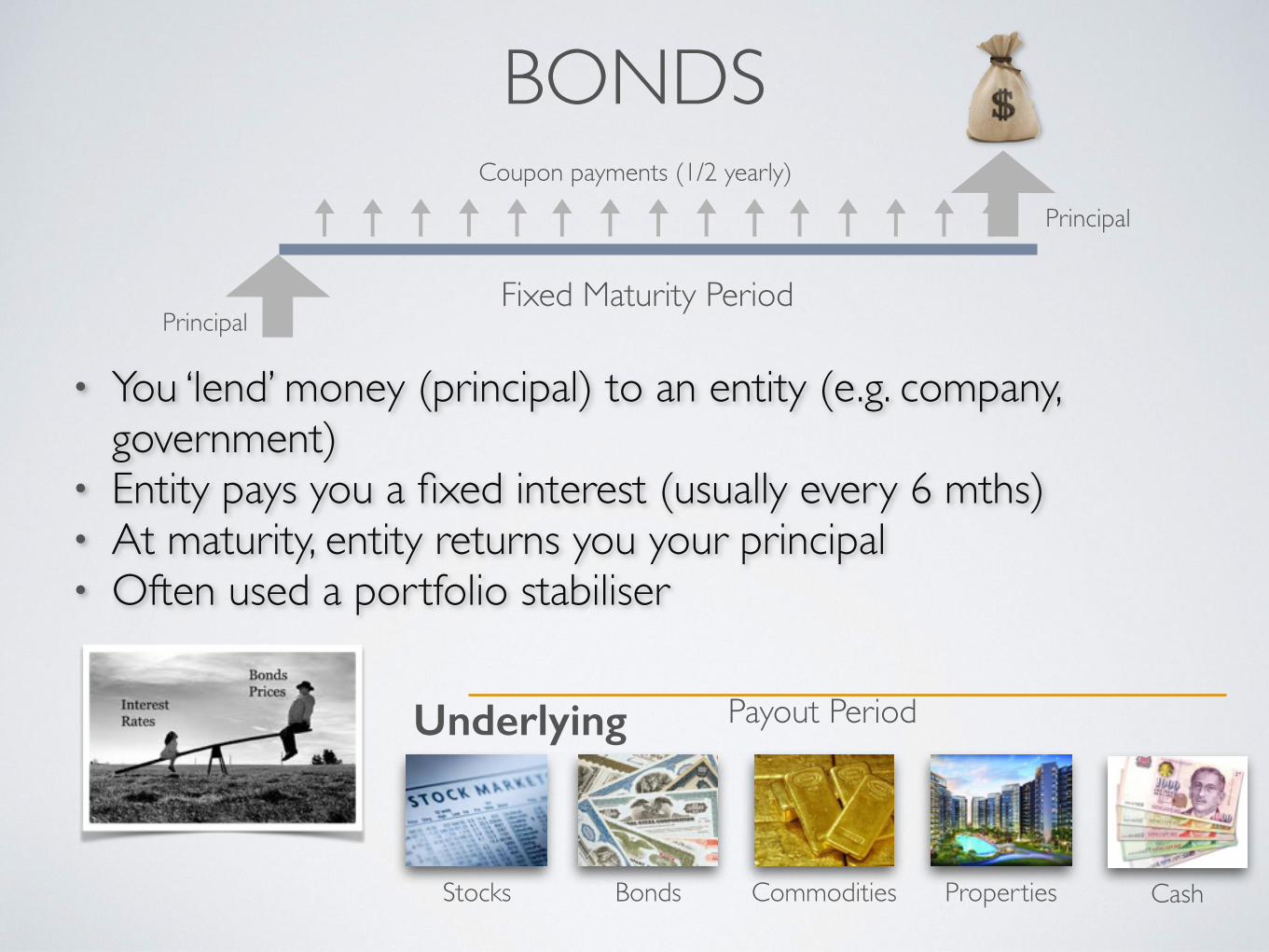

BONDS

Bonds Commodities Properties CashStocks

Underlying

• You ‘lend’ money (principal) to an entity (e.g. company, government)

• Entity pays you a fixed interest (usually every 6 mths)• At maturity, entity returns you your principal• Often used a portfolio stabiliser

Payout Period

Fixed Maturity PeriodPrincipal

Principal

Coupon payments (1/2 yearly)

COMMODITIES

Bonds Commodities Properties CashStocks

Underlying

• Precious metals (e.g. gold, platinum)• Energy (e.g. Crude oil, coal)• Agriculture (e.g. wheat, corn, rice)• Difficult to invest in physical asset (other than gold)• Can invest through proxies*

• Companies that deal with commodities (mining, trading)• Funds (ETFs, unit trusts)• Futures

• Generally favoured during periods of perceived high future inflation

*Source: http://commoditiestradingsg.blogspot.sg/2011/04/how-to-invest-in-commodities-in.html

PROPERTIES

Bonds Commodities Properties CashStocks

Underlying

• Types • Residential (HDB, landed, condos)• Retail (shop lots, strata title shops)• Office• Industrial (flatted factories, landed factories)

PROPERTIES

Bonds Commodities Properties CashStocks

Underlying

• Factors • Freehold / Leasehold• Rental yield• Proximity to public transport, shopping malls, good schools• Catalysts (New developments)• Occupancy rate• Feng shui

PROPERTIES

Bonds Commodities Properties CashStocks

Underlying

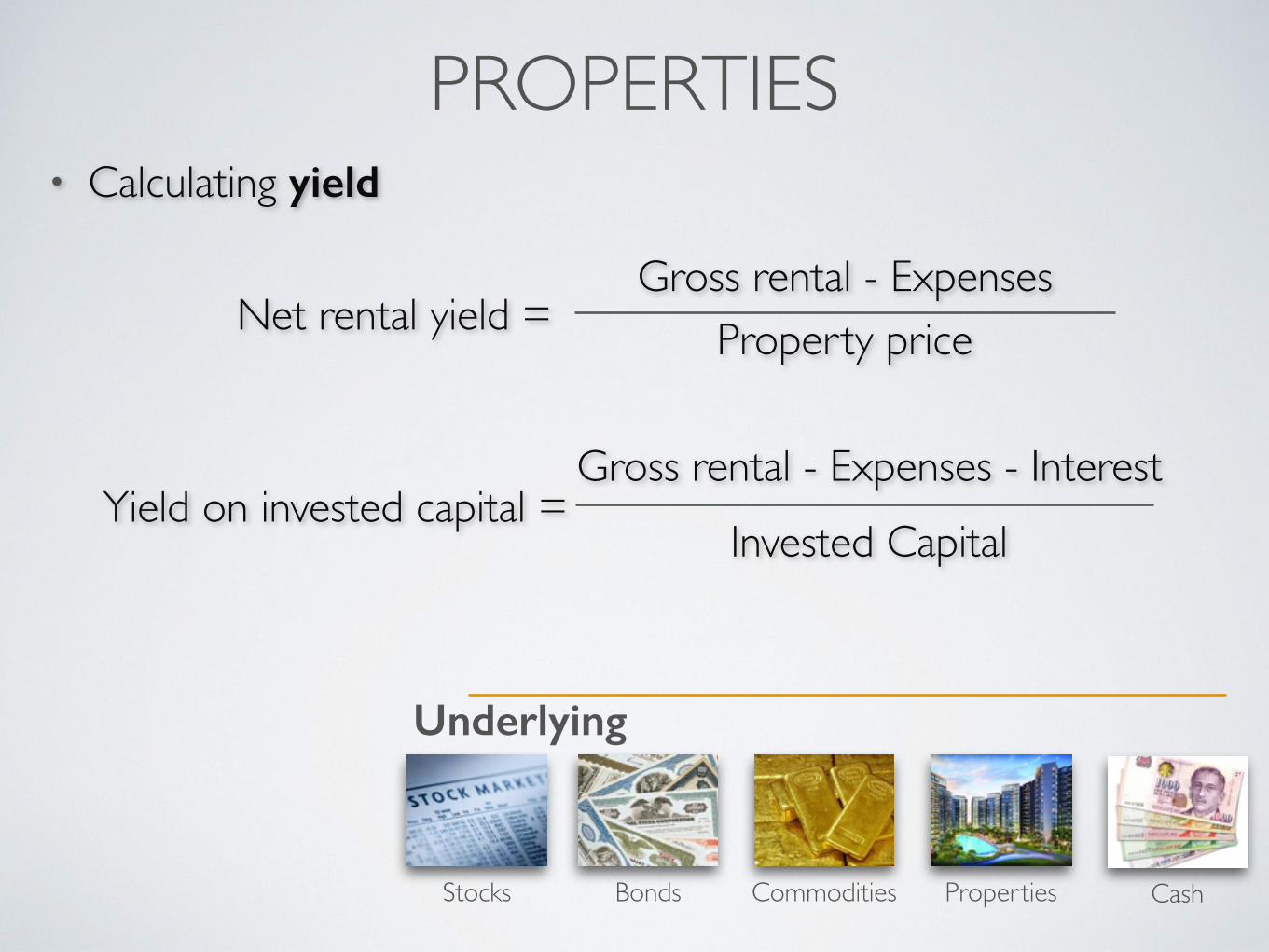

• Calculating yield

Net rental yield = Gross rental - Expenses

Property price

Yield on invested capital = Gross rental - Expenses - Interest

Invested Capital

CASH

Bonds Commodities Properties CashStocks

Underlying

• Bank savings or in fixed deposit• Protected under Singapore Deposit Insurance Corporation

(SDIC) at max $50,000 per bank*• Work towards 3 to 6 times of your monthly expenses for

emergency needs• Retain savings for short term needs (<3 yrs) in cash

*Refer to www.sdic.org.sg for participating banks.

UNIT TRUSTS

Bonds Commodities Properties CashStocks

Underlying

• a.k.a. Mutual Funds• Basket of stocks and/or bonds• Actively managed by a group of fund managers• Every fund has an objective/mandate which the fund

managers are required to adhere to• Benchmarked against an index

UNIT TRUSTS

Bonds Commodities Properties CashStocks

Underlying

• Exercise: How to read a fund fact sheet

ETF

Bonds Commodities Properties CashStocks

Underlying

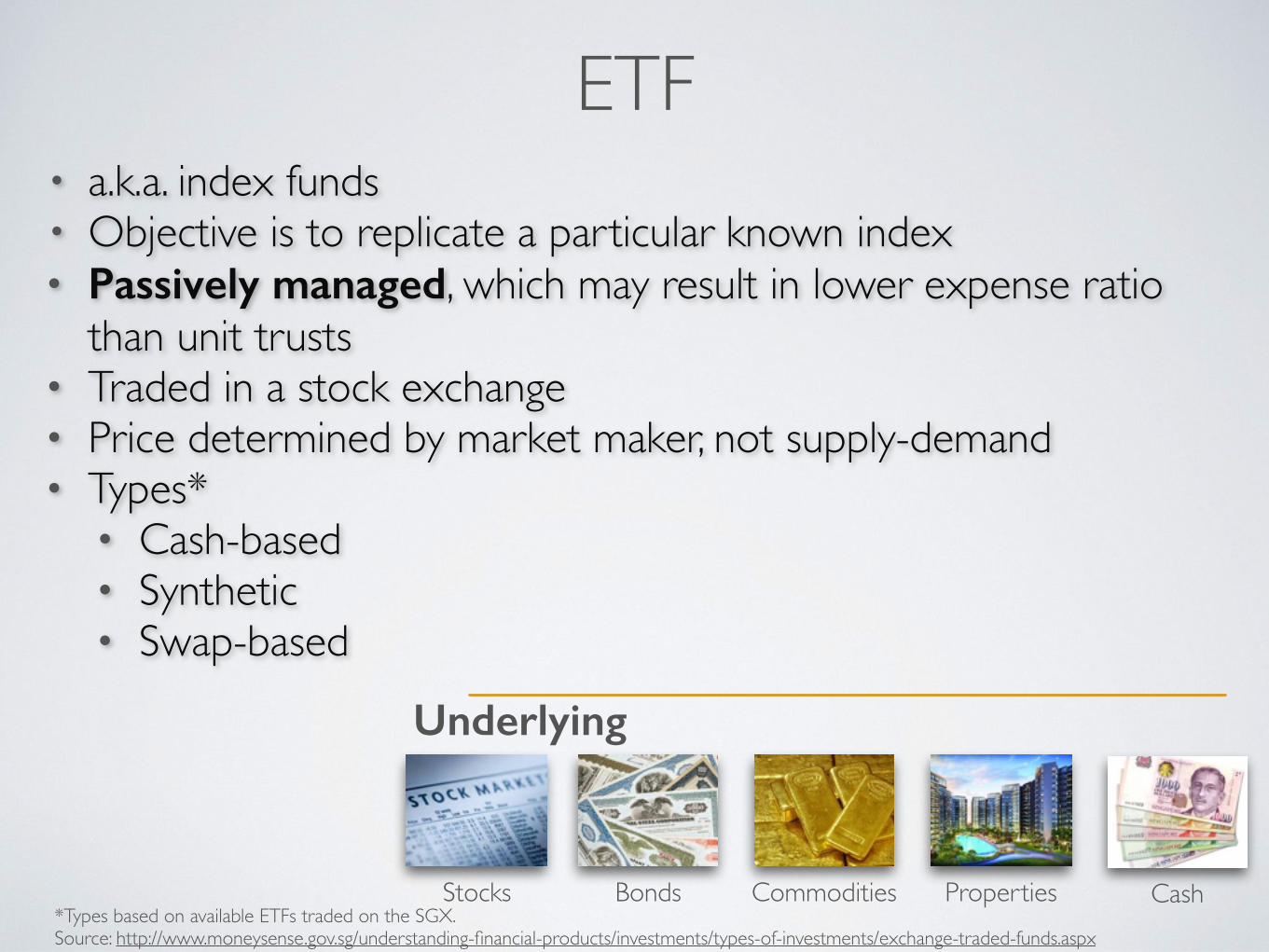

• a.k.a. index funds• Objective is to replicate a particular known index• Passively managed, which may result in lower expense ratio

than unit trusts• Traded in a stock exchange• Price determined by market maker, not supply-demand• Types*

• Cash-based• Synthetic• Swap-based

*Types based on available ETFs traded on the SGX. Source: http://www.moneysense.gov.sg/understanding-financial-products/investments/types-of-investments/exchange-traded-funds.aspx

MONEY MARKET FUNDS

Bonds Commodities Properties CashStocks

Underlying

• Low-risk• Invests in cash equivalent assets• Gives slightly higher interest than bank deposits• Not insured under Singapore Deposit Insurance Corporation

(SDIC)

INVESTMENT LINKED POLICIES

Bonds Commodities Properties CashStocks

Underlying

• Hybrid insurance-investment vehicle• Charges for protection benefits are deducted monthly

according to age and sum assured• Advantage: Flexibility to reduce premium / sum assured• Disadvantage: Protection charges increases exponentially with

age

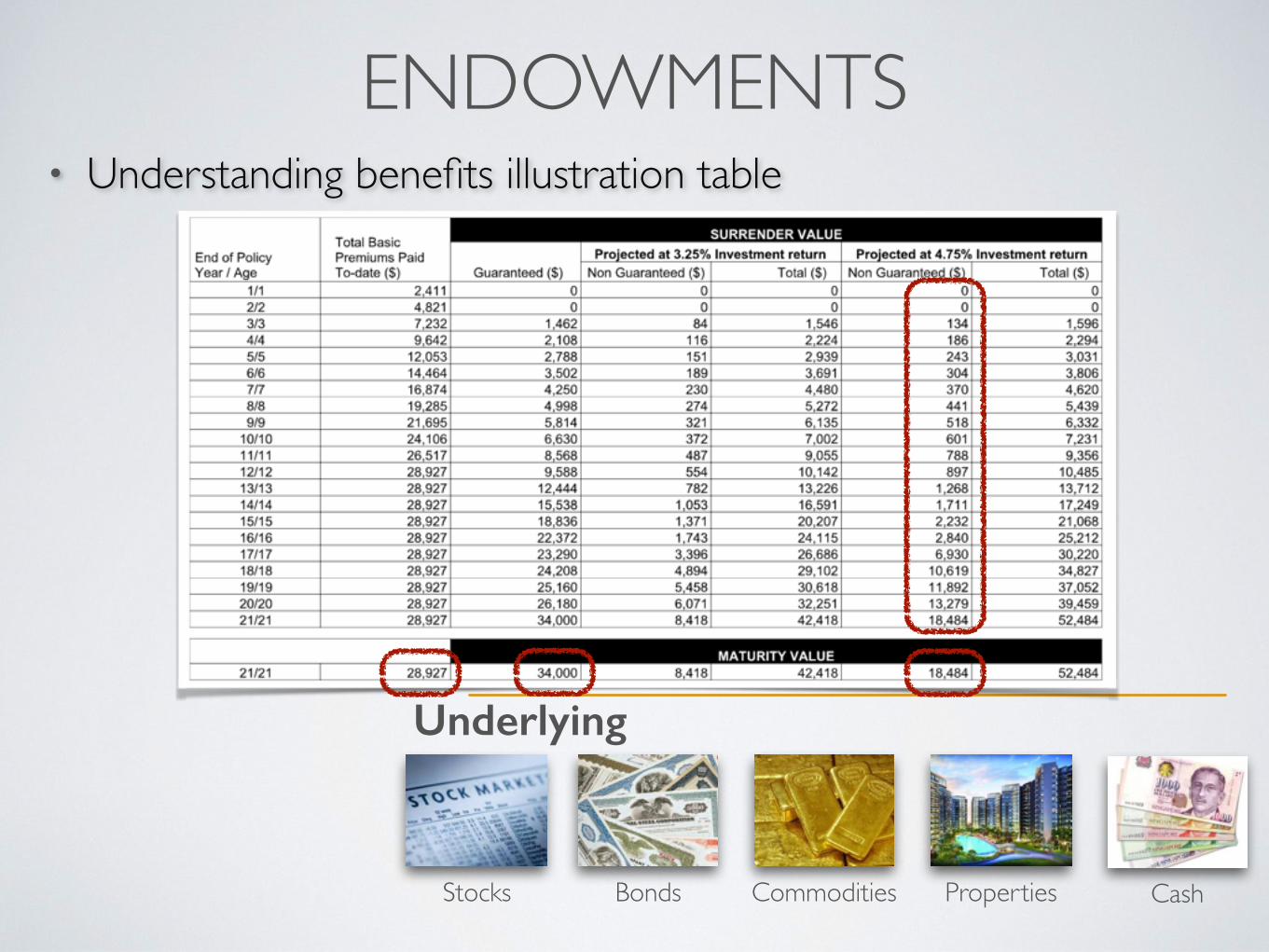

ENDOWMENTS

Bonds Commodities Properties CashStocks

Underlying

• Savings plans by insurance companies• Fixed maturity period determined at start of policy• Maturity benefit consists of a guaranteed and non-

guaranteed portion• Protection benefits varies from plan to plan

• Guaranteed Issuance Offer (no medical underwriting) plans are increasingly popular. Note that their protection benefits are very limited.

ENDOWMENTS

Bonds Commodities Properties CashStocks

Underlying

• Understanding benefits illustration table

ENDOWMENTS

Bonds Commodities Properties CashStocks

Underlying

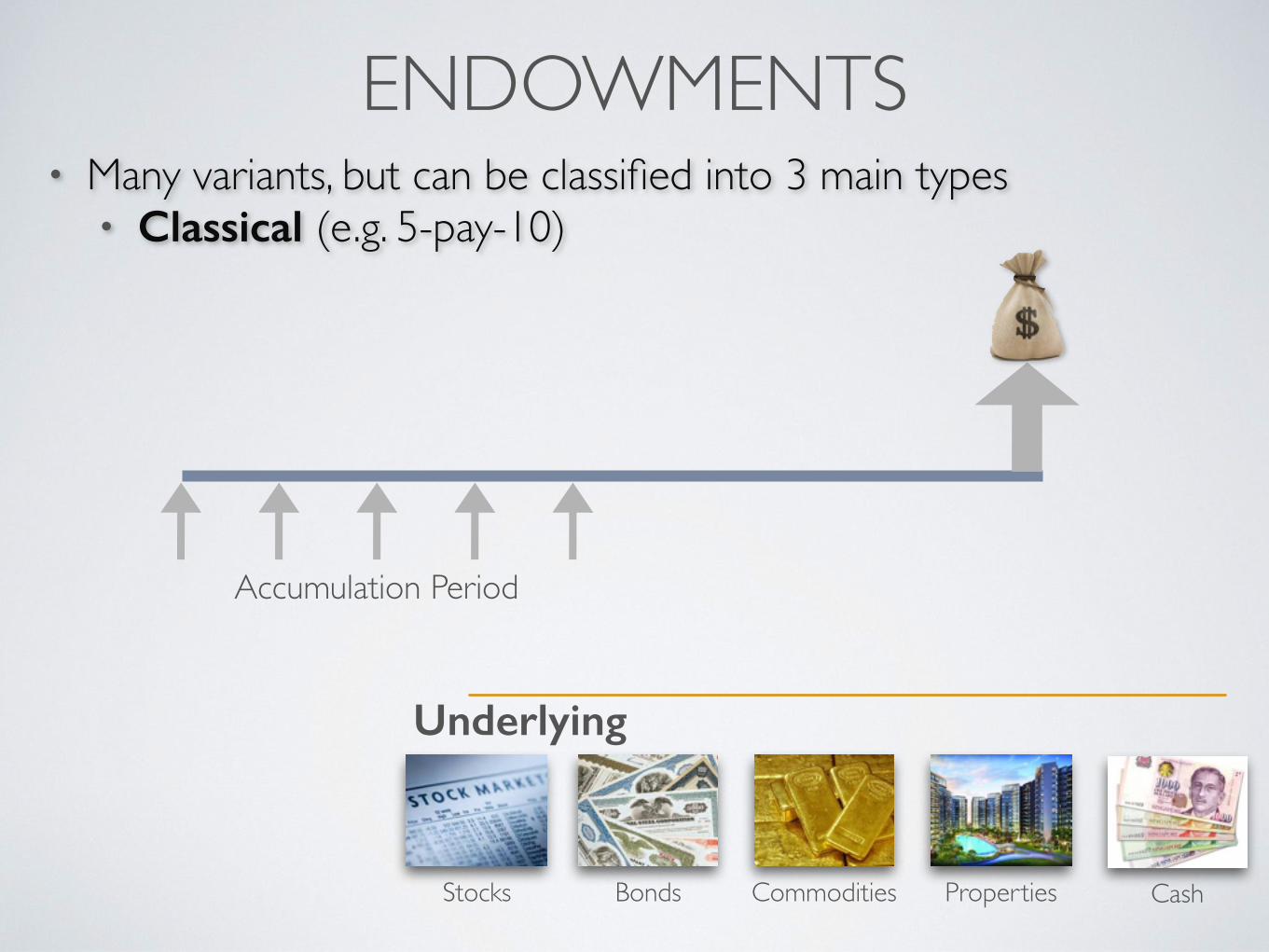

• Many variants, but can be classified into 3 main types• Classical (e.g. 5-pay-10)

Accumulation Period

ENDOWMENTS

Bonds Commodities Properties CashStocks

Underlying

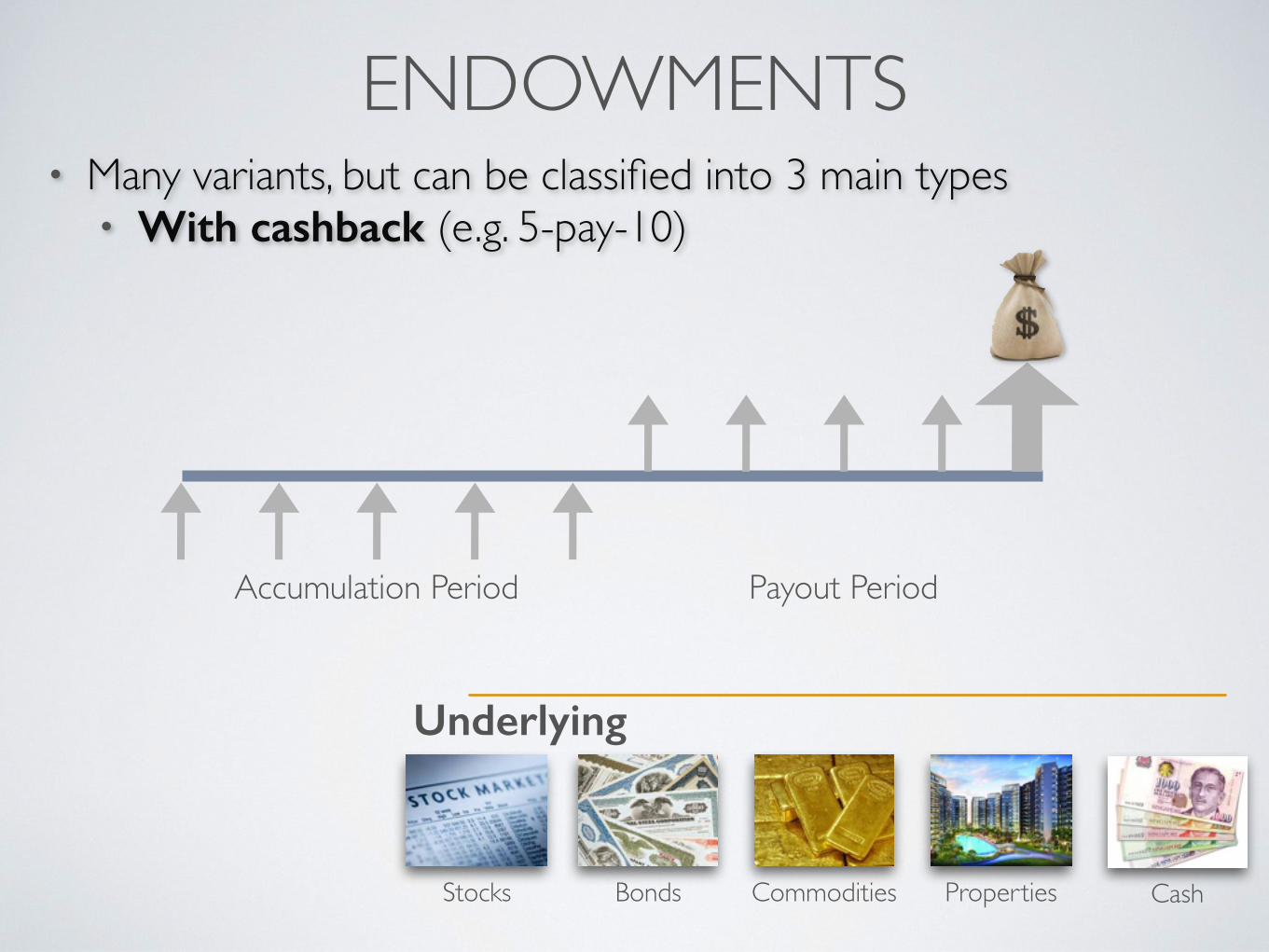

• Many variants, but can be classified into 3 main types• With cashback (e.g. 5-pay-10)

Accumulation Period Payout Period

ENDOWMENTS

Bonds Commodities Properties CashStocks

Underlying

• Many variants, but can be classified into 3 main types• Retirement (e.g. payout at 60, mature at 70)

Accumulation Period Payout Period

INVESTMENT PLANS

Bonds Commodities Properties CashStocks

Underlying

• E.g. Blue chip investment plans• Allows for regular investment of selected stocks using little

amount of money.• Advantage: may be lower cost than unit trusts• Disadvantage: may be less diversified than unit trusts

Risk Level Liquidity Income Suited for

Medium to High

Medium to High

Dividends (if any)

Trading, Capital appreciation

Low to Medium

Low to Medium Coupons Regular fixed

income

Low to High High NIL Hedge against inflation

Low to High Low Rental(if any)

Hedge against inflation, rental

income

Low High Interest Liquidity needs

COMPARISON - UNDERLYING

Bonds

Commodities

Properties

Cash

Stocks

Risk Level Liquidity Income Suited for

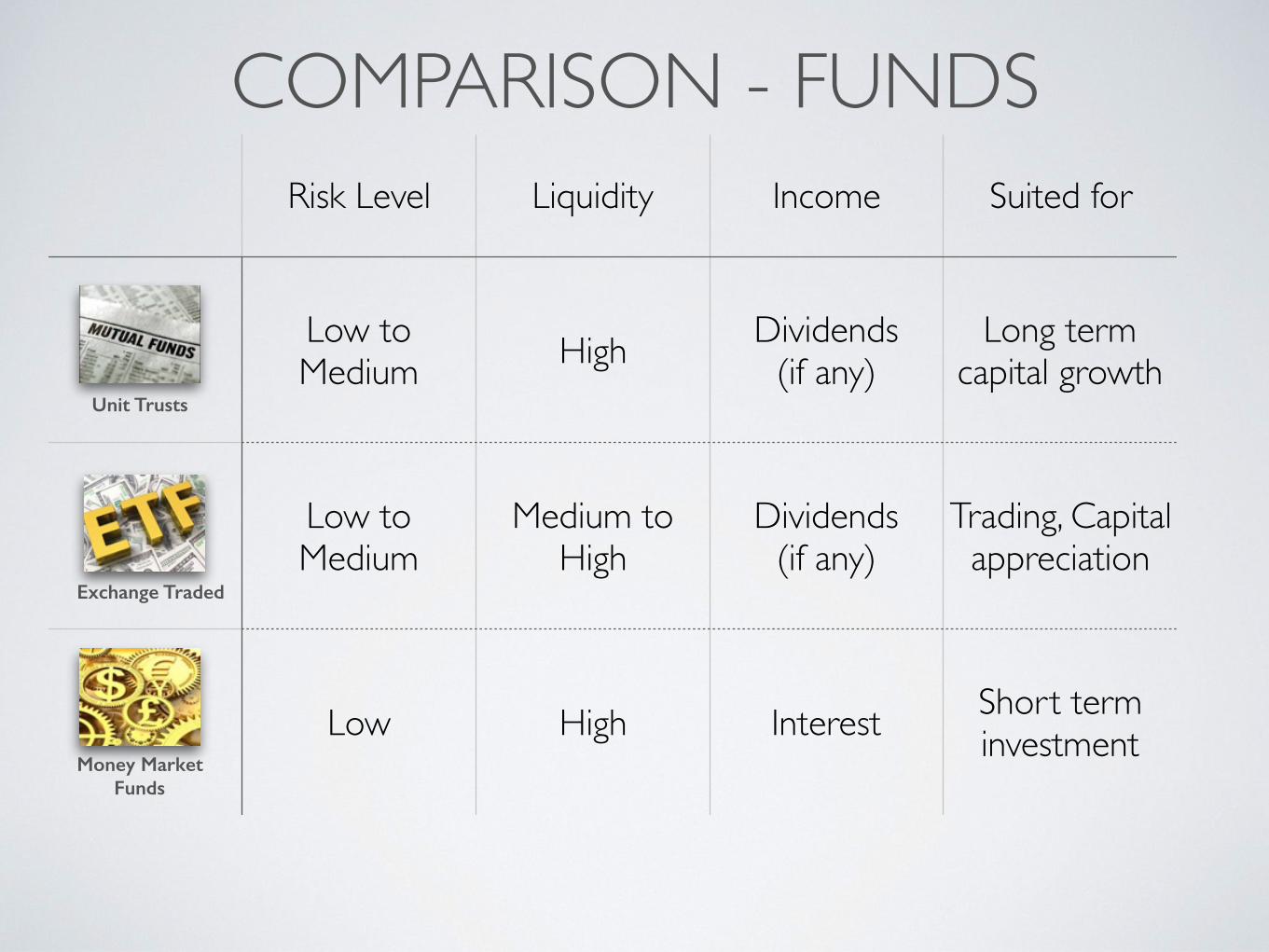

Low to Medium High Dividends

(if any)Long term

capital growth

Low to Medium

Medium to High

Dividends(if any)

Trading, Capital appreciation

Low High Interest Short term investment

COMPARISON - FUNDS

Unit Trusts

Exchange Traded

Money Market Funds

Risk Level Liquidity Income Suited for

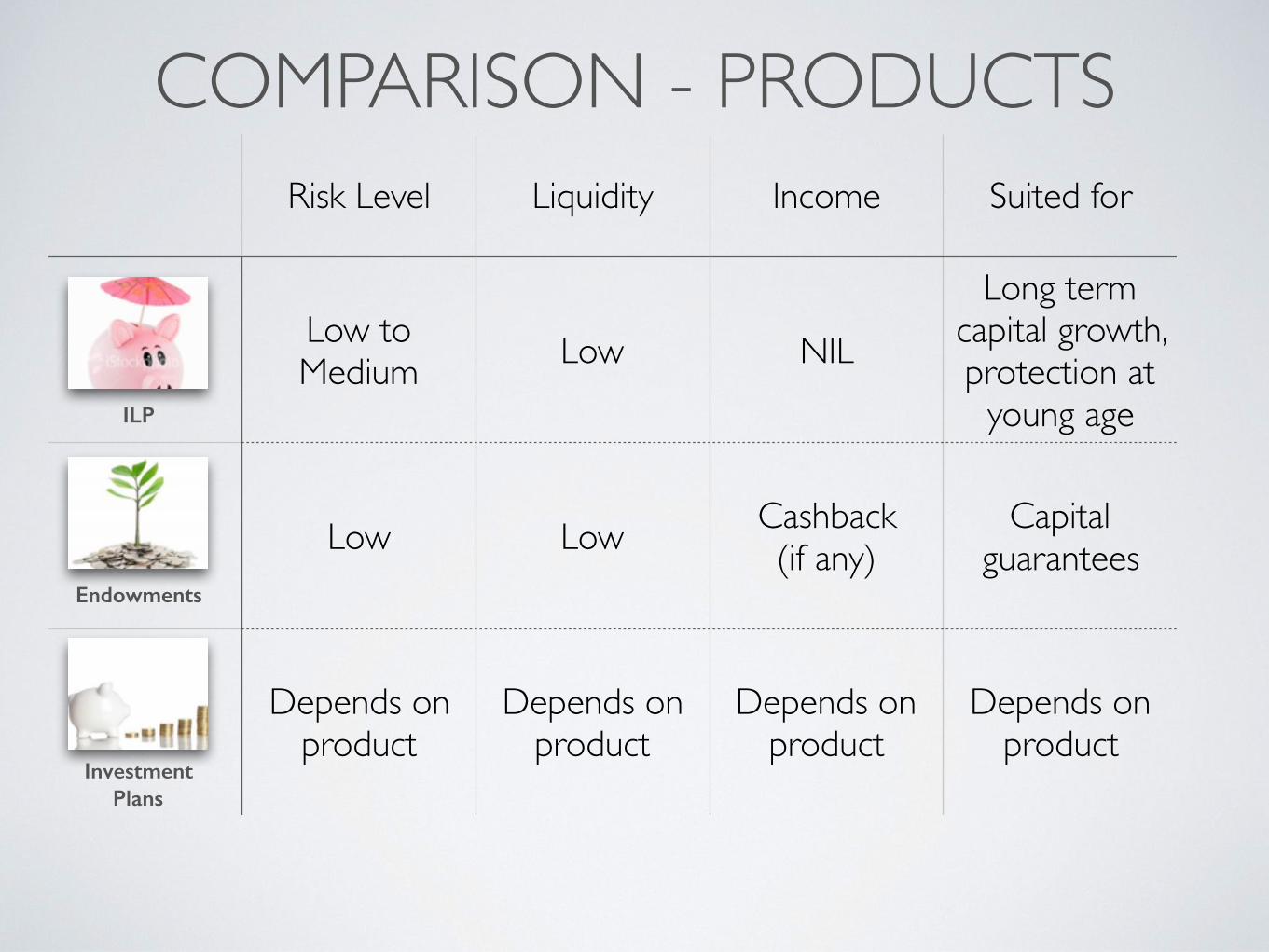

Low to Medium Low NIL

Long term capital growth, protection at

young age

Low Low Cashback(if any)

Capital guarantees

Depends on product

Depends on product

Depends on product

Depends on product

COMPARISON - PRODUCTS

ILP

Endowments

Investment Plans

WHAT SHOULD YOU INVEST IN?

Unit Trusts

FundsExchange

Traded FundsMoney

Market Funds

ILP

ProductsEndowments Investment

Plans

Bonds Commodities Properties CashStocks

Underlying

HOW MANY WAYS TO MAKE COFFEE?

Funds

Products

Underlying

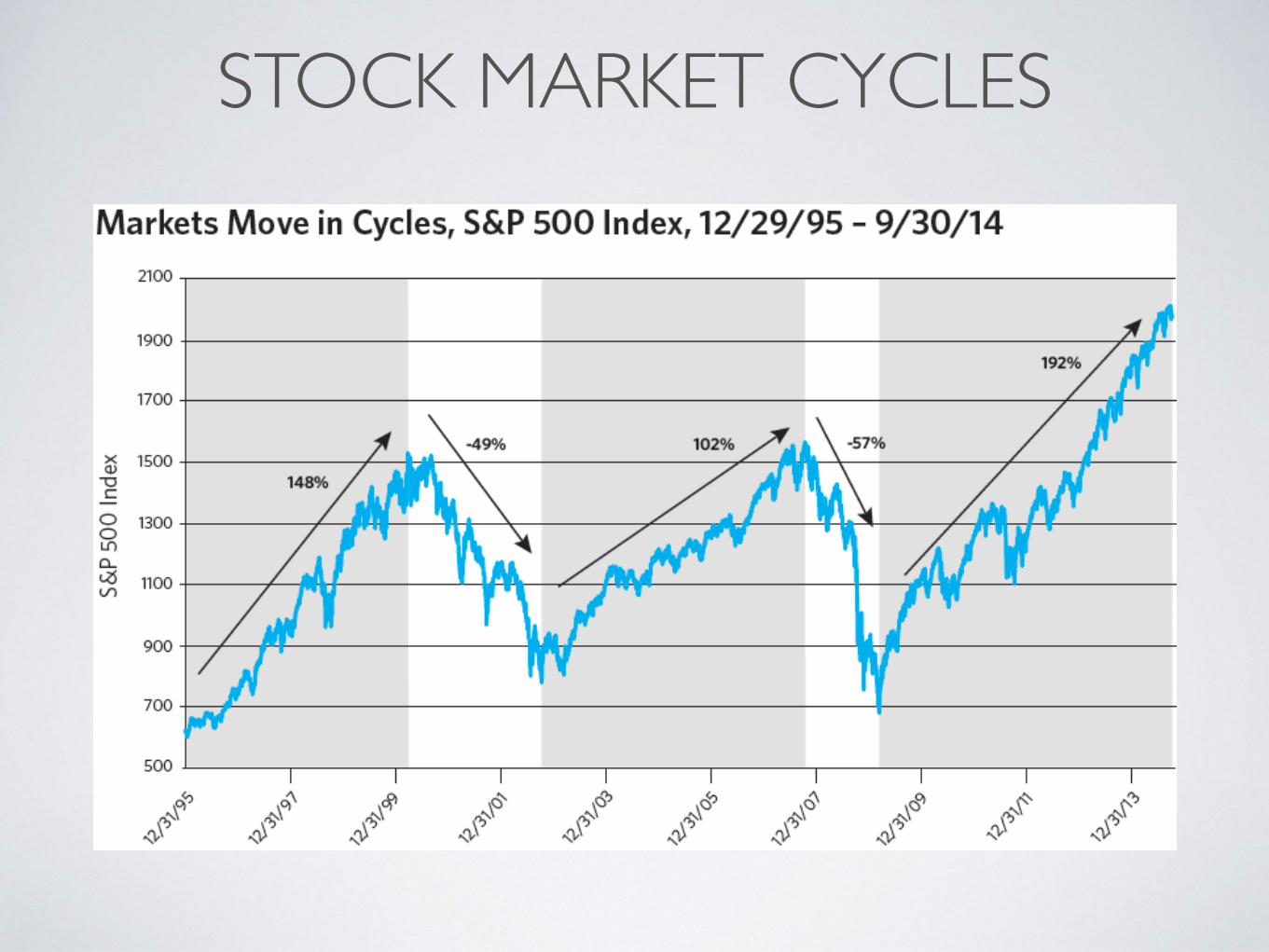

STOCK MARKET CYCLES

LET’S PLAY!

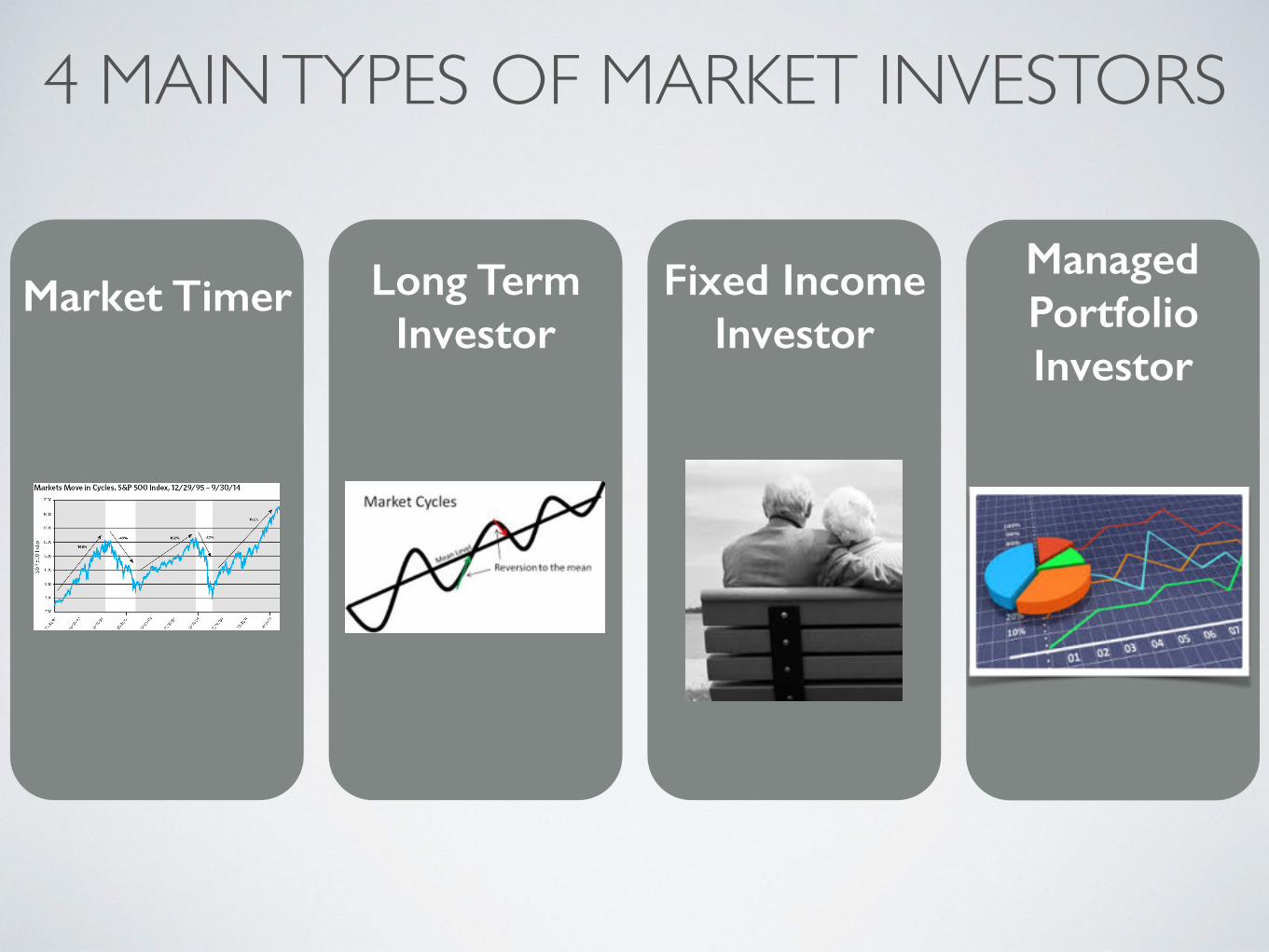

4 MAIN TYPES OF MARKET INVESTORS

Market Timer Long Term Investor

Fixed Income Investor

Managed Portfolio Investor

4 MAIN TYPES OF MARKET INVESTORS• Market Timer (Trader)

• Try to buy at bottom of market cycle and sell at top of market cycle

• Difficulties: • Spotting the top and bottom• Emotions (greed vs fear)• When to cut loss when market moves against you

• Typically alternates between stocks and cash

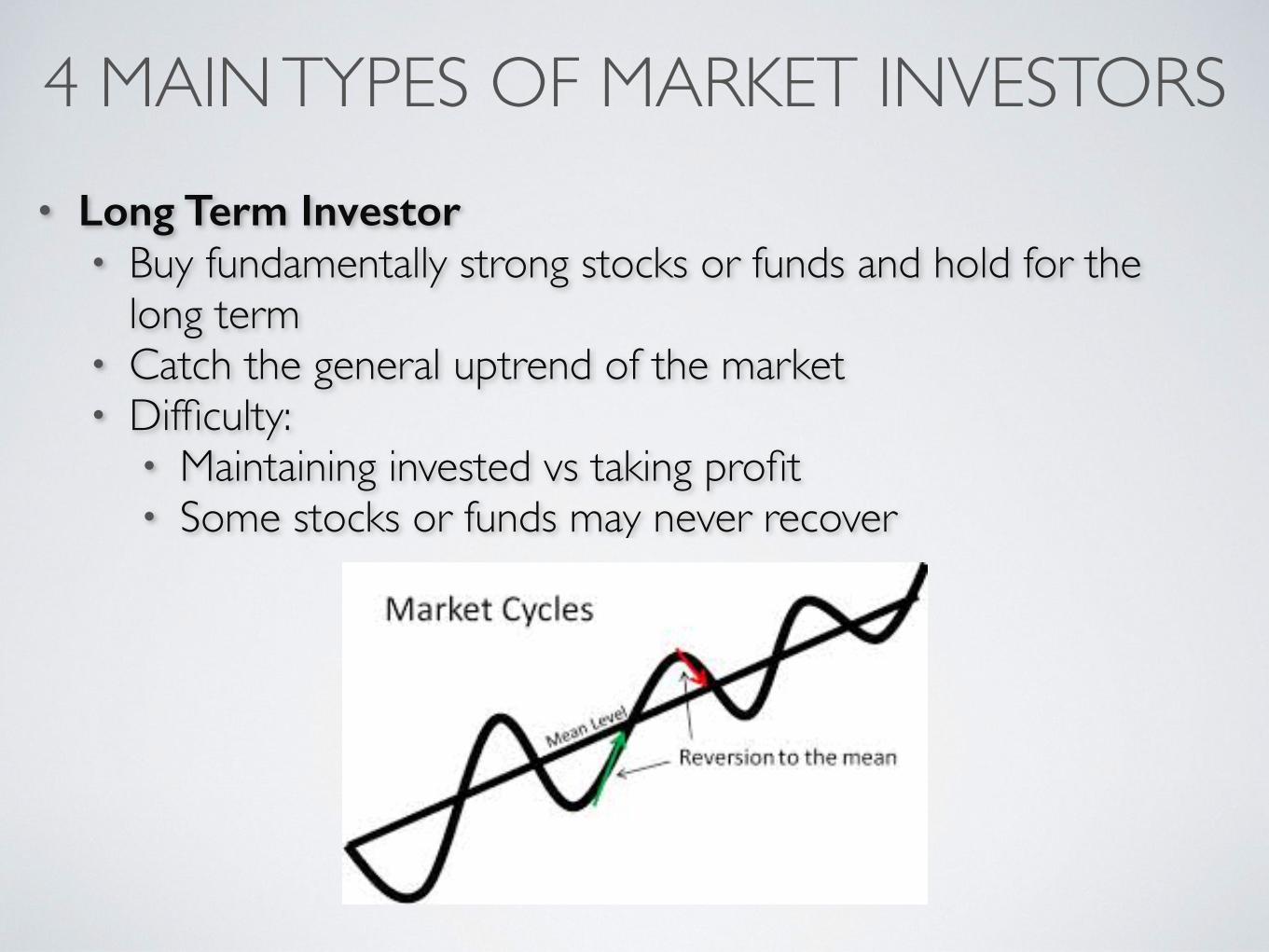

4 MAIN TYPES OF MARKET INVESTORS• Long Term Investor

• Buy fundamentally strong stocks or funds and hold for the long term

• Catch the general uptrend of the market• Difficulty:

• Maintaining invested vs taking profit• Some stocks or funds may never recover

4 MAIN TYPES OF MARKET INVESTORS• Fixed Income Investor

• Buy bonds and hold till maturity, collecting coupons periodically

• Buy bond funds and hold• Typically fuss-free and low risk, but may run the risk of

company defaulting• Popular for retirees• Difficulty:

• Reinvesting coupons

4 MAIN TYPES OF MARKET INVESTORS• Managed Portfolio Investor

• Typically invested in unit trusts and/or ETFs• Strategic allocation ratio: e.g. 70% stocks, 30% bonds• Tactical allocation ratio allows for minor form of market

timing• Tradeoff: Potential returns are trimmed due to fees

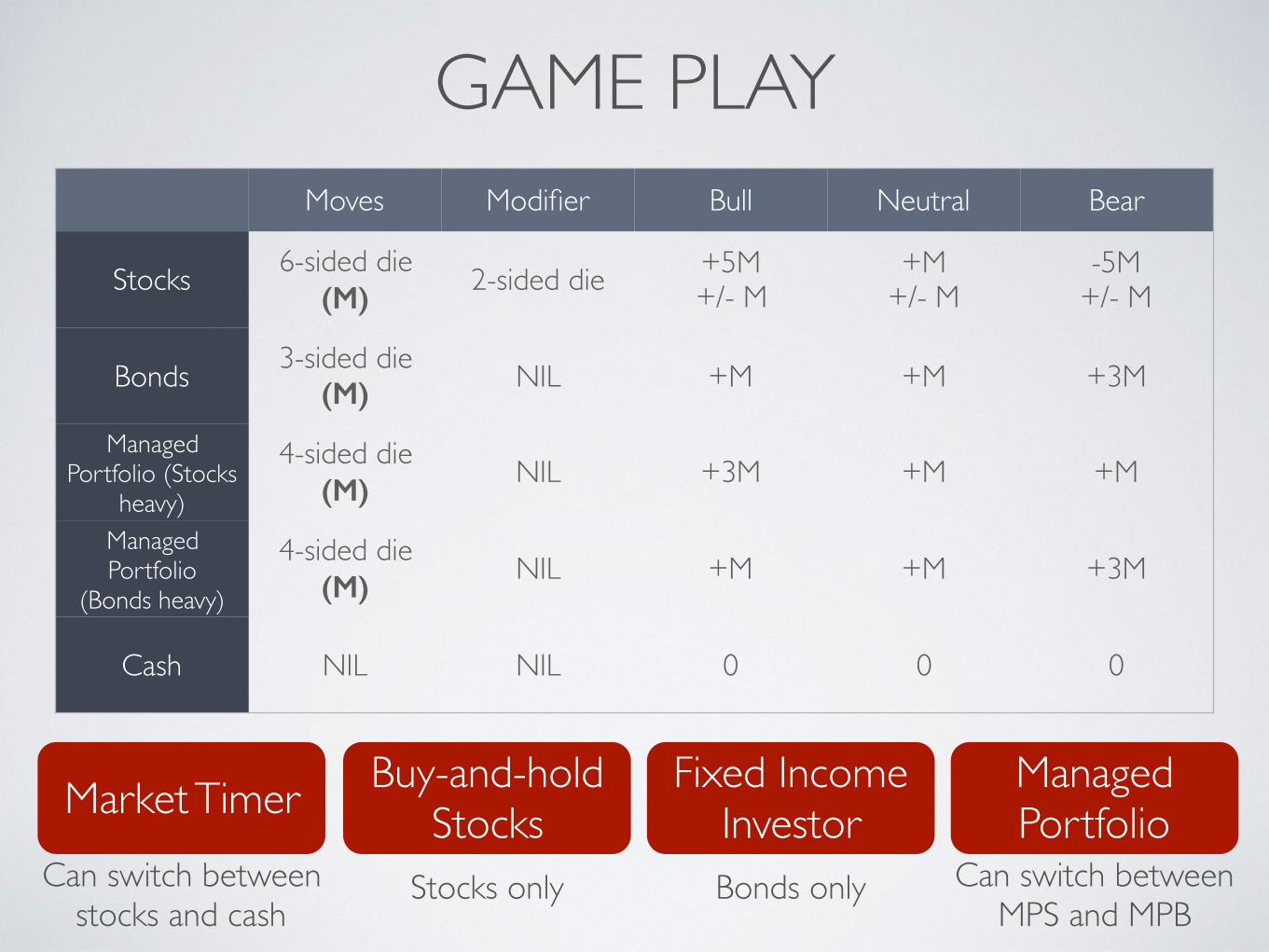

GAME PLAYMoves Modifier Bull Neutral Bear

Stocks 6-sided die (M)

2-sided die +5M +/- M

+M+/- M

-5M +/- M

Bonds 3-sided die(M) NIL +M +M +3M

Managed Portfolio (Stocks

heavy)

4-sided die(M)

NIL +3M +M +M

Managed Portfolio

(Bonds heavy)

4-sided die (M)

NIL +M +M +3M

Cash NIL NIL 0 0 0

Buy-and-hold Stocks

Stocks only

Market TimerCan switch between

stocks and cash

Fixed Income InvestorBonds only

Managed Portfolio

Can switch between MPS and MPB

Moves Bull Neutral Bear

Stocks 6-sided die (M)

+5M +/- M

+M+/- M

-5M +/- M

Bonds 3-sided die(M) +M +M +3M

Managed Portfolio (Stocks heavy)

4-sided die(M)

+3M +M +M

Managed Portfolio (Bonds heavy)

4-sided die (M)

+M +M +3M

Cash NIL 0 0 01 2 3 4 5 6 7 8 9 10

20 19 18 17 16 15 14 13 12 11

21 22 23 24 25 26 27 28 29 30

40 39 38 37 36 35 34 33 32 31

41 42 43 44 45 46 47 48 49 50

60 59 58 57 56 55 54 53 52 51

61 62 63 64 65 66 67 68 69 70

80 79 78 77 76 75 74 73 72 71

81 82 83 84 85 86 87 88 89 90

100 99 98 97 96 95 94 93 92 91

Strategy/ Risk Management

BACK TO THE BIG PICTURE

Plan Execute

Investment Objective

Time Horizon

Financial Goals

Specific Instruments Allocation

Specific Funds / Securities

Target Asset Allocation

Feedback

Changes in Circumstance Market outlook

Risk Appetite

HAVE A PLAN AND STICK TO IT!

Cash

Endowment

Endowment

Bond Fund

Bond Fund

Stocks

PropertyEquity Fund

Gold / Silver

HY Bond Fund

HY Bond Fund