INVESTOR’S GUIDE: THE NEW ZEALAND FOOD & BEVERAGE INDUSTRY 2014February 2014

1

AN INVESTOR’S GUIDE TO THE NEW ZEALAND FOOD & BEVERAGE INDUSTRY

Part of the New Zealand Government’s Food & Beverage Information Project; Feb 2014

www.foodandbeverage.govt.nz

iFAB 2014Photo credit: New Zealand Story

iFAB 2014

The objective of this document is to make a strong, factual case for investment in the New Zealand food and beverage industry

- This investment can come from existing investors or those new to the sector

- This investment can come from global sources or New Zealand

The document acts as an “entry portal” to the wealth of further information available in on the sector in the New Zealand Government’s Food & Beverage Information Project

www.foodandbeverage.govt.nz

iFAB 2014

New Zealand is well positioned to triple its food & beverage exports over the next 15 years; investors will participate in this success

GENERAL

New Zealand is a developed, temperate-climate country in the Asia-Pacific region. It is a stable democracy with strong economic freedoms(Index of Economic Freedom #4), excellent investor protection (WorldBank #1) and low corruption (Transparency International #1). It is byalmost all measures the most attractive investment destination in thetemperate zone of the Southern Hemisphere.

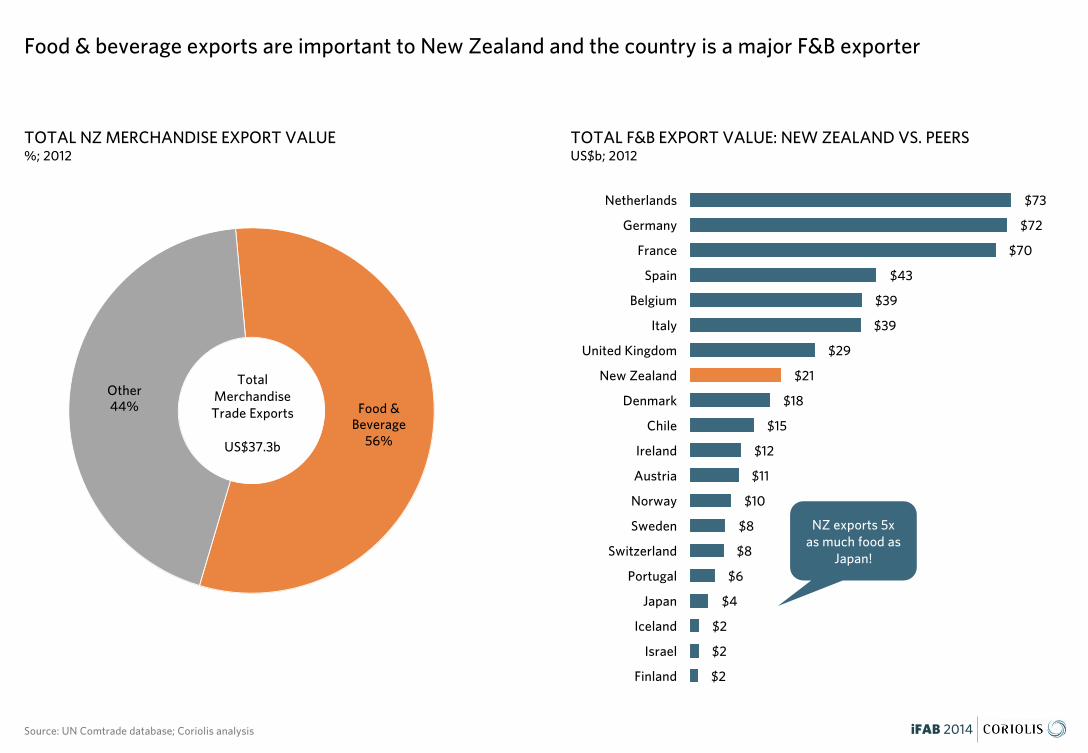

FOOD & BEVERAGEFood and beverage exports are important to New Zealand and thecountry is a major F&B exporter (56% of exports). New Zealand’s F&Bexports are growing strongly and the country’s export performance isstrong and improving relative to peers.The country has demonstrated capability in the production oftemperate-climate food and beverages. It is the largest exporter in theworld of dairy products and lamb and a major exporter of beef,kiwifruit, apples and seafood.

DRIVERS

The success of New Zealand in temperate foods is built around anatural environment conducive to agriculture. New Zealand –surrounded by the Pacific Ocean – has the light of Spain with theclimate of Bordeaux. This climate will also moderate the effects ofglobal warming going forward (relative to large continents).

The country’s farmers are highly productive and efficient. The countryhas no agricultural subsidies and regulation is generally rational andlight handed.New Zealand has a supportive infrastructure for food and beverages

along the total value chain.

New Zealand is a leader in food safety and product traceability.Customers and consumers around the world trust food and beveragesproduced in New Zealand.In science, New Zealand spends more than half a billion dollars a yearon Agri-food research across a wide range of areas, from fruit geneticsto nutraceuticals. The country is also home to four major universitiesrespected globally for their Agri-food research.

OPPORTUNITIES

While New Zealand is a major global F&B exporter, the country hassignificant untapped capacity to export more. New Zealand is acountry the size of Italy with the population of Singapore. HoweverItaly feeds a domestic population of 60m people and exports twice asmuch F&B as New Zealand.

The New Zealand Government has set a target of tripling the country’sfood and beverage exports over the next 15 years. This will beachieved through both growth of existing major sectors and the neweremerging growth stars.

New Zealand is a young country still discovering its comparativeadvantages and new industries continue to emerge. In the past twentyyears New Zealand wine, honey, aquaculture and avocados have allemerged from almost nothing into world leading sectors.New Zealand has attracted investment in F&B manufacturing fromaround the world. Global leaders have already endorsed New Zealandby investing in manufacturing in the country and 25% of the F&Bmanufacturing sector is foreign owned.

iFAB 2014

4.5m people 0.06% of the world

267,710km2 in area Similar to Italy

15,134km coastline More than China

16.6 people/km2500x less than Singapore

US$171b GDP Similar to Kuwait

$38,255 GDP/capita Similar to Hong Kong

NZ$1 dollar US$0.83

Index of Economic Freedom #4 Above Switzerland

Corruption Perceptions Index #1 Tied with Denmark

World Bank Investor Protection #1 Above Singapore

New Zealand is a developed, temperate-climate country in the Asia-Pacific region that is an attractive investment destination

BIGGER… than you think

iFAB 2014

iFAB 2014

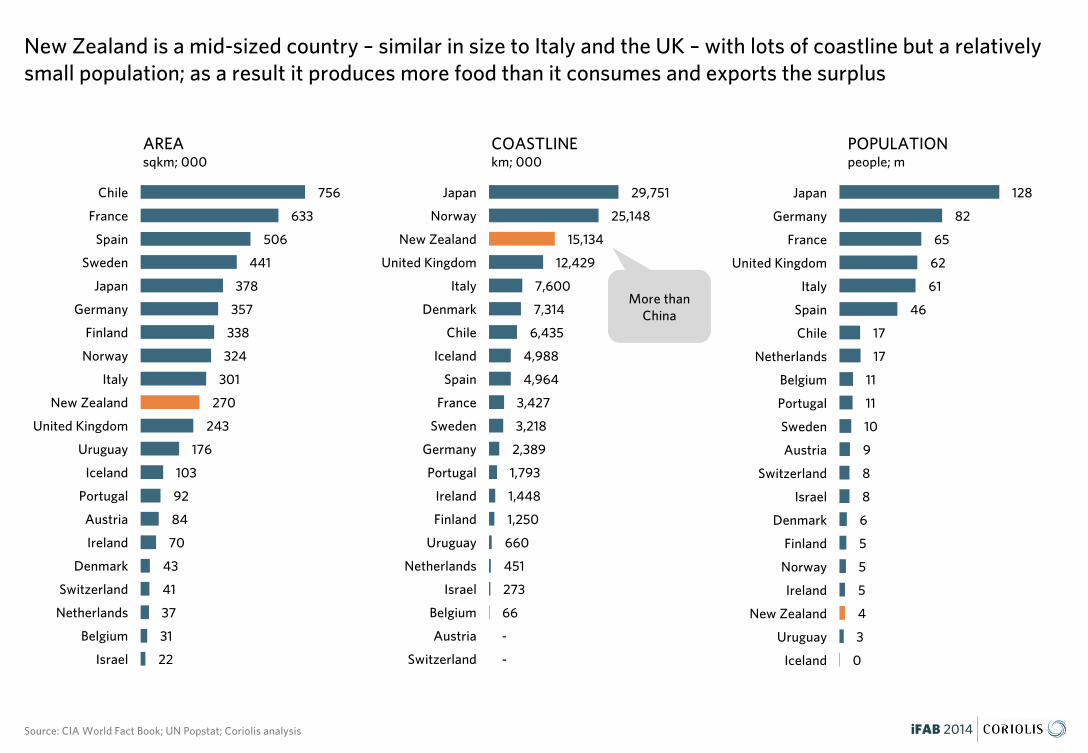

New Zealand is a mid-sized country – similar in size to Italy and the UK – with lots of coastline but a relatively small population; as a result it produces more food than it consumes and exports the surplus

Source: CIA World Fact Book; UN Popstat; Coriolis analysis

756

633

506

441

378

357

338

324

301

270

243

176

103

92

84

70

43

41

37

31

22

Chile

France

Spain

Sweden

Japan

Germany

Finland

Norway

Italy

New Zealand

United Kingdom

Uruguay

Iceland

Portugal

Austria

Ireland

Denmark

Switzerland

Netherlands

Belgium

Israel

POPULATIONpeople; m

128

82

65

62

61

46

17

17

11

11

10

9

8

8

6

5

5

5

4

3

0

Japan

Germany

France

United Kingdom

Italy

Spain

Chile

Netherlands

Belgium

Portugal

Sweden

Austria

Switzerland

Israel

Denmark

Finland

Norway

Ireland

New Zealand

Uruguay

Iceland

AREAsqkm; 000

29,751

25,148

15,134

12,429

7,600

7,314

6,435

4,988

4,964

3,427

3,218

2,389

1,793

1,448

1,250

660

451

273

66

-

-

Japan

Norway

New Zealand

United Kingdom

Italy

Denmark

Chile

Iceland

Spain

France

Sweden

Germany

Portugal

Ireland

Finland

Uruguay

Netherlands

Israel

Belgium

Austria

Switzerland

COASTLINEkm; 000

More than China

iFAB 2014

Food & Beverage

56%

Other44%

TOTAL NZ MERCHANDISE EXPORT VALUE%; 2012

Food & beverage exports are important to New Zealand and the country is a major F&B exporter

Source: UN Comtrade database; Coriolis analysis

TOTAL F&B EXPORT VALUE: NEW ZEALAND VS. PEERS US$b; 2012

NZ exports 5x as much food as

Japan!

Total Merchandise Trade Exports

US$37.3b

$73

$72

$70

$43

$39

$39

$29

$21

$18

$15

$12

$11

$10

$8

$8

$6

$4

$2

$2

$2

Netherlands

Germany

France

Spain

Belgium

Italy

United Kingdom

New Zealand

Denmark

Chile

Ireland

Austria

Norway

Sweden

Switzerland

Portugal

Japan

Iceland

Israel

Finland

iFAB 2014

$3.0

$10.2

$2.1

$4.4

$0.7

$1.2

$0.7

$1.6

$0.0

$0.2

$0.4

$1.7

$0.1

$0.3

$0.2

$1.3

2002 2012

NZ F&B EXPORT VALUE BY MAJOR SEGMENTUS$b; 2012

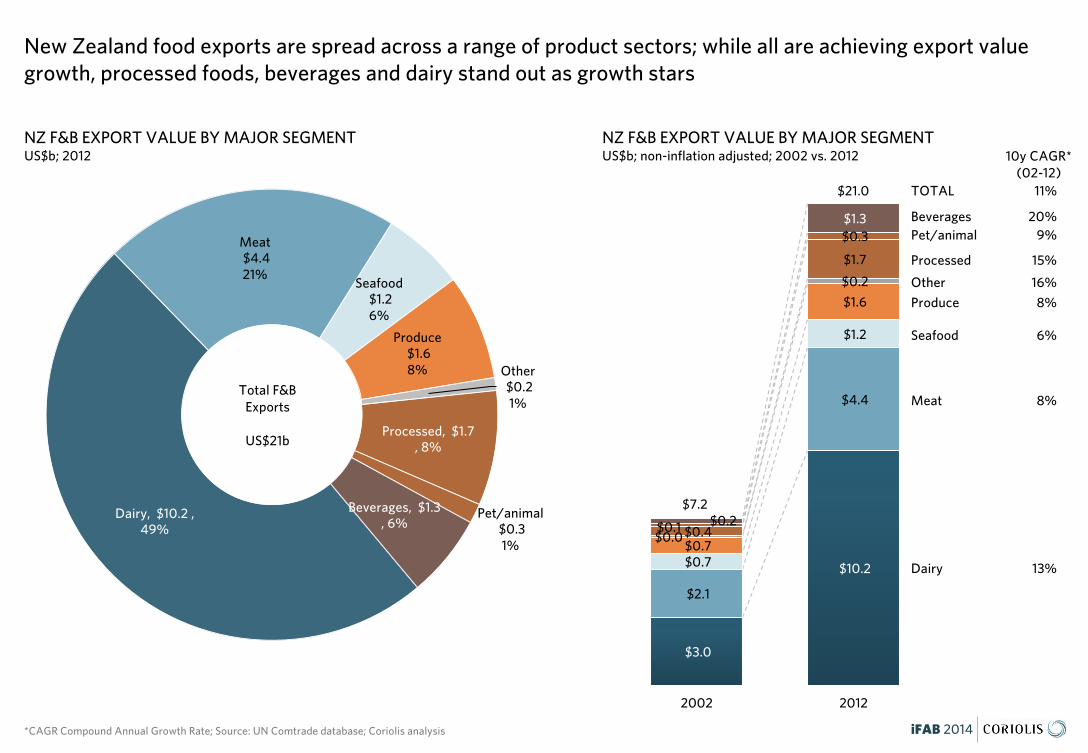

New Zealand food exports are spread across a range of product sectors; while all are achieving export value growth, processed foods, beverages and dairy stand out as growth stars

*CAGR Compound Annual Growth Rate; Source: UN Comtrade database; Coriolis analysis

Dairy

NZ F&B EXPORT VALUE BY MAJOR SEGMENTUS$b; non-inflation adjusted; 2002 vs. 2012

Meat

Seafood

Produce

Other

Processed

Beverages

$21.0

$7.2

13%

8%

6%

8%

16%

15%

9%

10y CAGR*(02-12)

20%

Dairy, $10.2 , 49%

Meat$4.4 21%

Seafood$1.2 6%

Produce$1.6 8% Other

$0.2 1%

Processed, $1.7 , 8%

Pet/animal$0.3 1%

Beverages, $1.3 , 6%

Total F&B Exports

US$21b

Pet/animal

TOTAL 11%

iFAB 2014

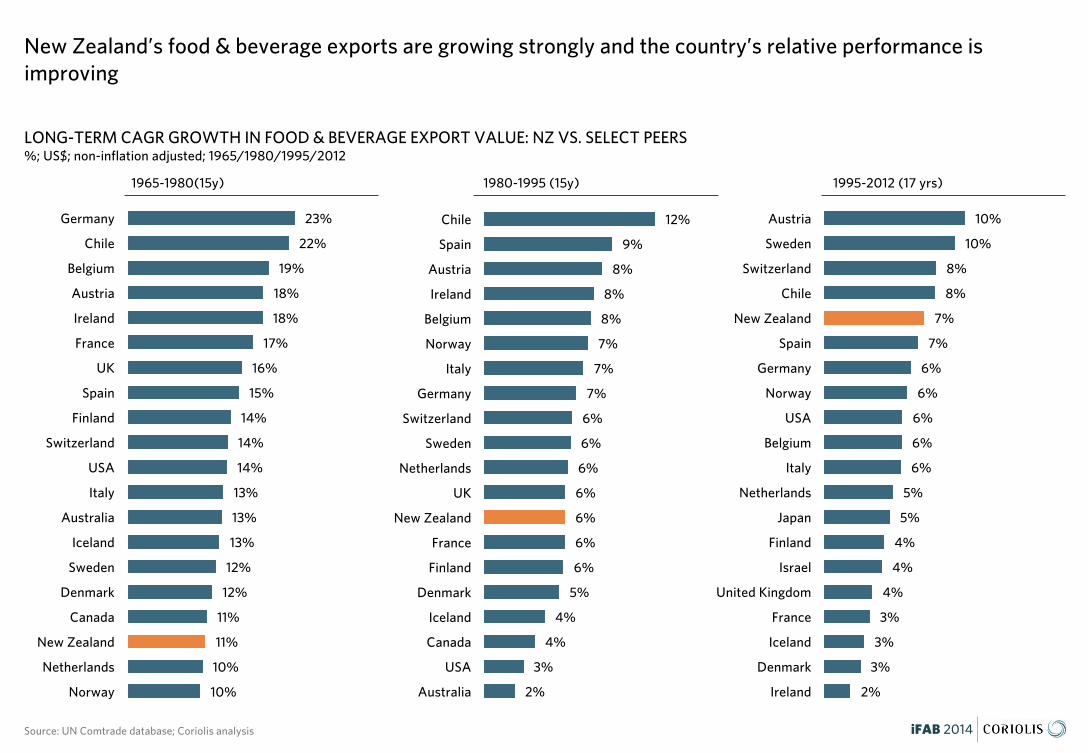

LONG-TERM CAGR GROWTH IN FOOD & BEVERAGE EXPORT VALUE: NZ VS. SELECT PEERS%; US$; non-inflation adjusted; 1965/1980/1995/2012

New Zealand’s food & beverage exports are growing strongly and the country’s relative performance is improving

Source: UN Comtrade database; Coriolis analysis

1965-1980(15y) 1980-1995 (15y) 1995-2012 (17 yrs)

23%

22%

19%

18%

18%

17%

16%

15%

14%

14%

14%

13%

13%

13%

12%

12%

11%

11%

10%

10%

Germany

Chile

Belgium

Austria

Ireland

France

UK

Spain

Finland

Switzerland

USA

Italy

Australia

Iceland

Sweden

Denmark

Canada

New Zealand

Netherlands

Norway

12%

9%

8%

8%

8%

7%

7%

7%

6%

6%

6%

6%

6%

6%

6%

5%

4%

4%

3%

2%

Chile

Spain

Austria

Ireland

Belgium

Norway

Italy

Germany

Switzerland

Sweden

Netherlands

UK

New Zealand

France

Finland

Denmark

Iceland

Canada

USA

Australia

10%

10%

8%

8%

7%

7%

6%

6%

6%

6%

6%

5%

5%

4%

4%

4%

3%

3%

3%

2%

Austria

Sweden

Switzerland

Chile

New Zealand

Spain

Germany

Norway

USA

Belgium

Italy

Netherlands

Japan

Finland

Israel

United Kingdom

France

Iceland

Denmark

Ireland

iFAB 2014

$1,746 $2,019 $2,468 $2,591 $2,549 $2,876 $3,220 $2,834 $2,842 $3,407 $2,891

$1,543 $1,672

$1,950 $2,082 $2,003 $2,130

$2,265 $1,941 $2,026

$2,443 $2,652

$703 $884

$1,135 $1,245 $1,319

$1,661 $1,878

$1,727 $2,175

$2,560 $2,609

$439 $482

$509 $568 $580

$1,001 $1,098

$643 $869

$1,059 $944

$48 $83

$123 $155 $226

$322

$384

$319

$430

$587 $543

$412 $476

$596 $746 $888

$1,192

$1,537

$1,233

$1,584

$2,226 $2,299

$85 $102

$121 $152 $184

$246

$292

$247

$421

$516 $411

$770

$925

$1,078 $1,182 $1,256

$1,933

$2,217

$1,622

$2,272

$2,633 $2,527

$1,483

$1,712

$2,378

$2,557 $2,475

$2,802

$3,220

$3,150

$4,358

$5,434 $6,071

$7,238

$8,364

$10,370

$11,288 $11,497

$14,180

$16,133

$13,736

$16,993

$20,888 $20,955

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

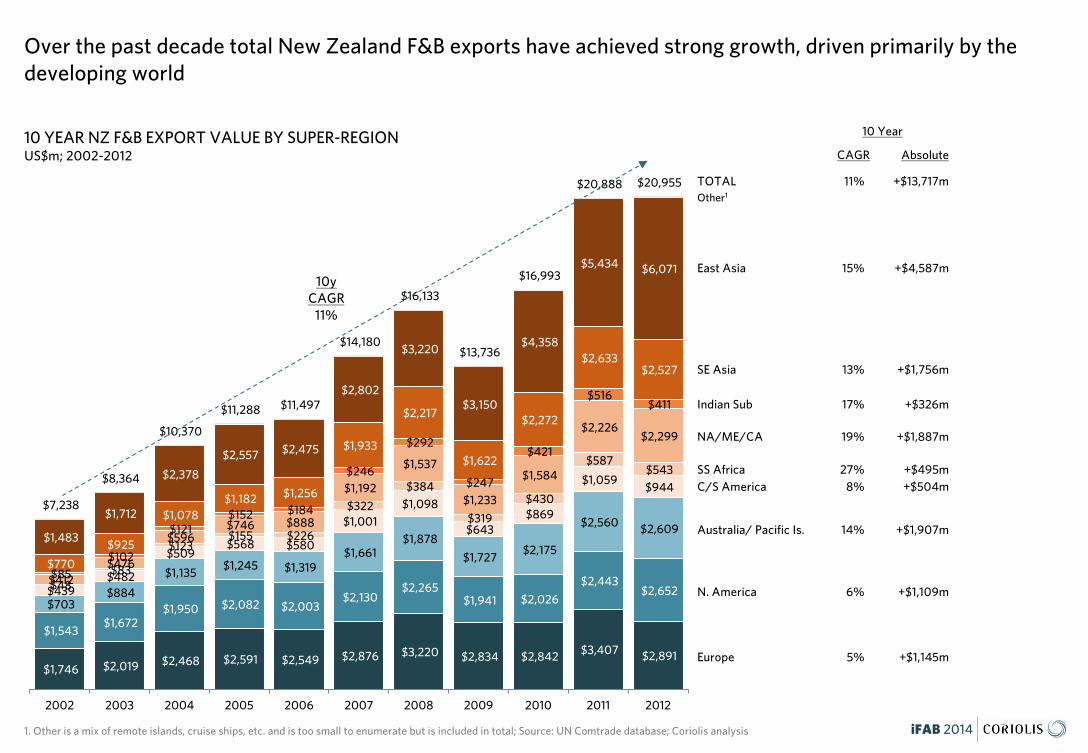

10 YEAR NZ F&B EXPORT VALUE BY SUPER-REGIONUS$m; 2002-2012

Over the past decade total New Zealand F&B exports have achieved strong growth, driven primarily by the developing world

1. Other is a mix of remote islands, cruise ships, etc. and is too small to enumerate but is included in total; Source: UN Comtrade database; Coriolis analysis

Europe 5% +$1,145m

N. America 6% +$1,109m

Australia/ Pacific Is. 14% +$1,907m

NA/ME/CA 19% +$1,887m

Indian Sub 17% +$326m

SE Asia 13% +$1,756m

East Asia 15% +$4,587m

TOTAL 11% +$13,717m

C/S America 8% +$504mSS Africa 27% +$495m

CAGR Absolute

10 Year

10yCAGR

11%

Other1

EMERGING… food bowl of Asia-Pacific

iFAB 2014

iFAB 2014

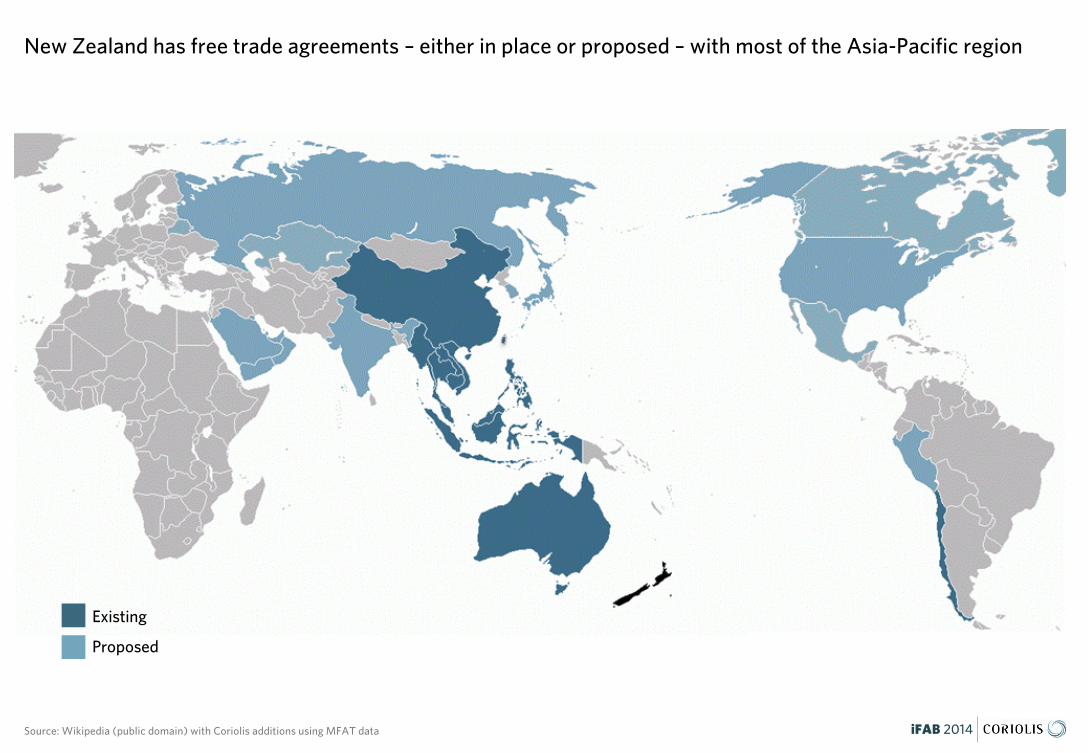

New Zealand has free trade agreements – either in place or proposed – with most of the Asia-Pacific region

Source: Wikipedia (public domain) with Coriolis additions using MFAT data

Existing

Proposed

iFAB 2014

Europe, $2,891 , 14%

N America$2,652 13%

Australia/Pacific $2,609 12%

C/S America$944 4%

SS Africa $543 3%

Indian Sub. $411 2%

NA/ME/CA$2,299 11%

SE Asia, $2,527 , 12%

E Asia, $6,071 , 29%

Total F&B Exports

US$21b

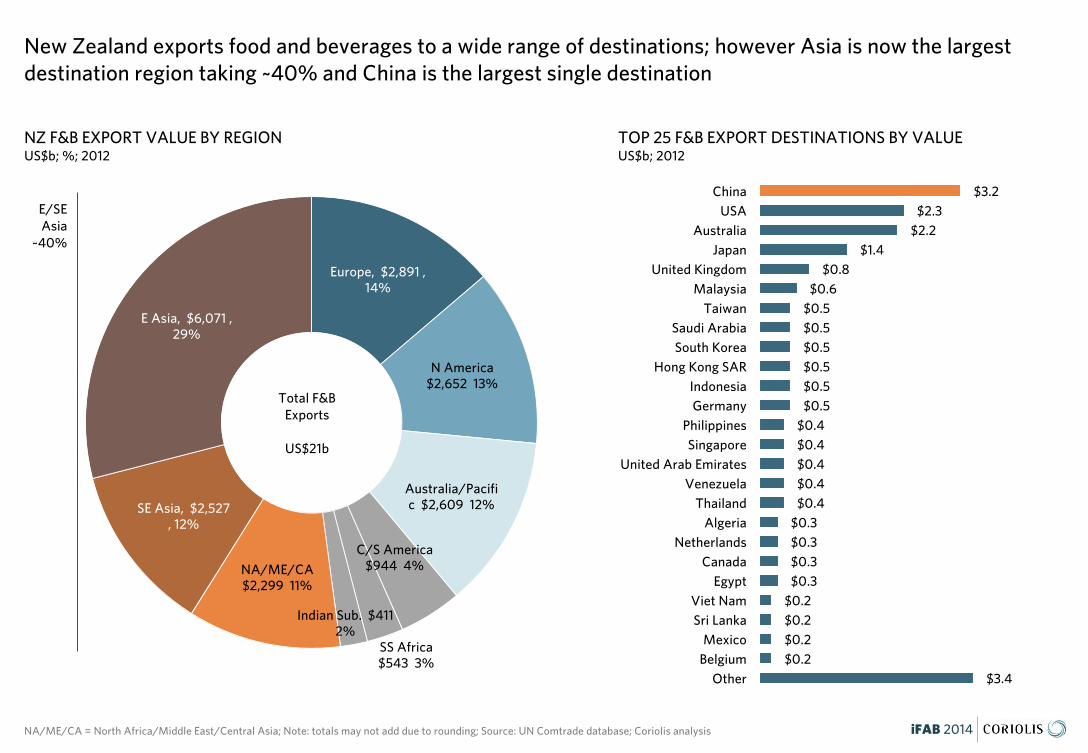

NZ F&B EXPORT VALUE BY REGIONUS$b; %; 2012

New Zealand exports food and beverages to a wide range of destinations; however Asia is now the largest destination region taking ~40% and China is the largest single destination

NA/ME/CA = North Africa/Middle East/Central Asia; Note: totals may not add due to rounding; Source: UN Comtrade database; Coriolis analysis

E/SEAsia

~40%

TOP 25 F&B EXPORT DESTINATIONS BY VALUEUS$b; 2012

$3.2 $2.3

$2.2 $1.4

$0.8 $0.6

$0.5 $0.5 $0.5 $0.5 $0.5 $0.5

$0.4 $0.4 $0.4 $0.4 $0.4

$0.3 $0.3 $0.3 $0.3

$0.2 $0.2 $0.2 $0.2

$3.4

ChinaUSA

AustraliaJapan

United KingdomMalaysia

TaiwanSaudi ArabiaSouth Korea

Hong Kong SARIndonesiaGermany

PhilippinesSingapore

United Arab EmiratesVenezuela

ThailandAlgeria

NetherlandsCanada

EgyptViet NamSri Lanka

MexicoBelgium

Other

iFAB 2014

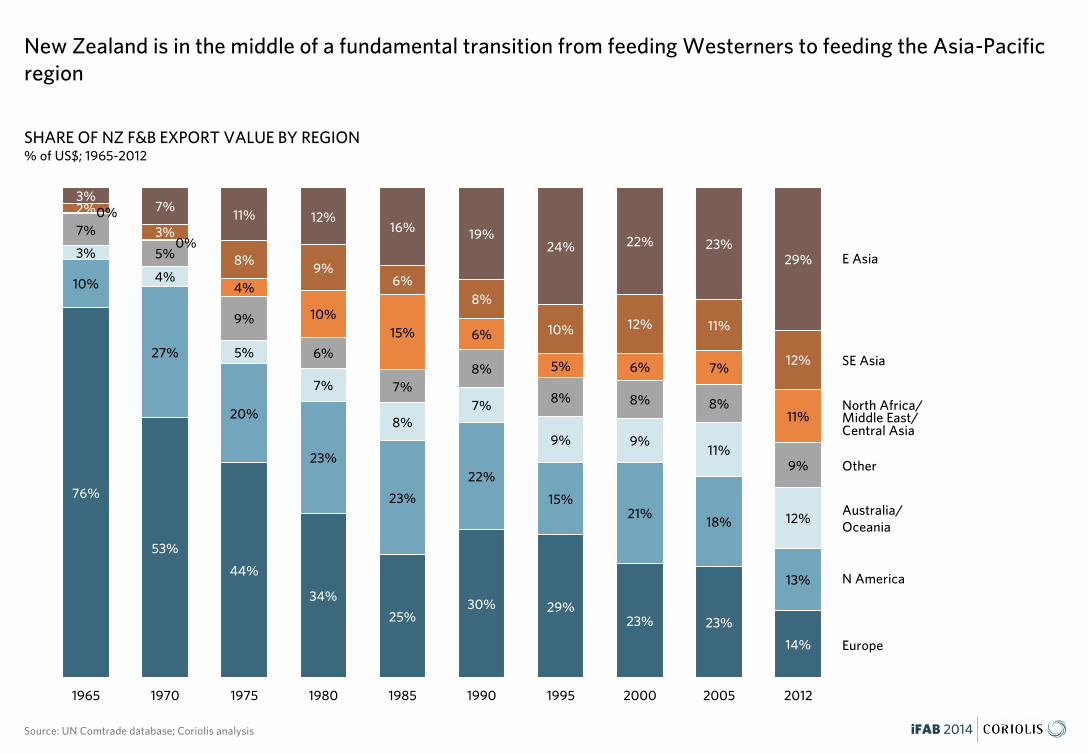

SHARE OF NZ F&B EXPORT VALUE BY REGION% of US$; 1965-2012

New Zealand is in the middle of a fundamental transition from feeding Westerners to feeding the Asia-Pacific region

Source: UN Comtrade database; Coriolis analysis

Europe

Other

Australia/ Oceania

E Asia

SE Asia

N America

North Africa/Middle East/Central Asia

76%

53%

44%

34%

25%30% 29%

23% 23%

14%

10%

27%

20%

23%

23%

22%

15%21%

18%

13%

3%

4%

5%

7%

8%7%

9% 9%11%

12%

7%

5%

9%

6%

7%8%

8% 8% 8%

9%

0%

0%

4%

10%15% 6%

5% 6% 7%

11%

2%

3%

8%9%

6%8%

10% 12% 11%

12%

3%7%

11% 12%16% 19%

24% 22% 23%29%

1965 1970 1975 1980 1985 1990 1995 2000 2005 2012

UPSIDE… capacity to produce much more

iFAB 2014

iFAB 2014

Peers suggest ample capacity to increase or intensify food production volume for the foreseeable future, though this will likely require land use change and more irrigation

AG LAND USE BY TYPE% of ag area; km2; 2012 or as available

TOTAL FOOD PRODUCTION VOLUMETonnes; 000; 1961-2011

1. available data is consented to irrigate not actually irrigated; Source: World Bank; CIA World Fact Book; UN AgStat database; Coriolis analysis

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

196119641967197019731976197919821985198819911994199720

00

200

320

06

200

9

Switzerland

Ireland

Denmark

New Zealand

Netherlands

Japan

United Kingdom

Italy

93%

83%

73%

62%

60%

54%

49%

39%

33%

26%

25%

13%

7%

0%

7%

2%

4%

19%

18%

1%

0%

2%

0%

16%

17%

20%

36%

37%

27%

34%

60%

67%

72%

75%

71%

Japan

Denmark

Slovakia

Belgium

France

Italy

Spain

Netherlands

UK

Switzerland

Ireland

New ZealandArable

landFruit/perm.

cropsPasture/other

agricultural land

AREA IRRIGATEDkm2; 000; 2012 or as available

37,800

27,500

26,000

25,920

10,770

5,650

4,490

1,830

1,700

400

250

-

Spain

Italy

France

Japan

New Zealand

Netherlands

Denmark

Slovakia

UK

Belgium

Switzerland

Ireland

1

377,930

301,336

270,467

242,900

70,273

43,094

41,284

37,354

Japan

Italy

New Zealand

United Kingdom

Ireland

Denmark

Switzerland

Netherlands

COUNTRY AREAkm2; 2013

iFAB 2014

760,805

204,000

179,500

99,584

43,615

34,605

29,300

24,708

14,920

7,362

3,237

France

Chile

Portugal

Germany

Austria

New Zealand

Croatia

Washington

Switzerland

Oregon

British Columbia

AQUACULTURE PRODUCTION VALUEUS$m; 2011

Peers suggest many food & beverages categories have strong growth upside

Source: UN FAO AgStat; UN FAO FishStat FIGIS database; USDA Census of Agriculture; Wine BC; Coriolis analysis

HECTARES IN FRUIT & VEGETABLESha; 000; 2012

GRAPE AREA BY COUNTRY/REGIONha; actual; 2012

3-10x

319 450

39

1,539 1,126

71

319

160

1

Spain Italy New Zealand

Fruit

Nuts

Vegetables

2,177

1,736

110

$6,340

$5,240

$1,102

$987

$923

$846

$770

$572

$414

$279

$174

$148

$120

$81

$60

$59

$53

Chile

Norway

USA

United Kingdom

France

Canada

Australia

Spain

Faroe Islands

New Zealand

Ireland

Denmark

Germany

Portugal

Finland

Sweden

South Africa

3-10x

3-10x

iFAB 2014

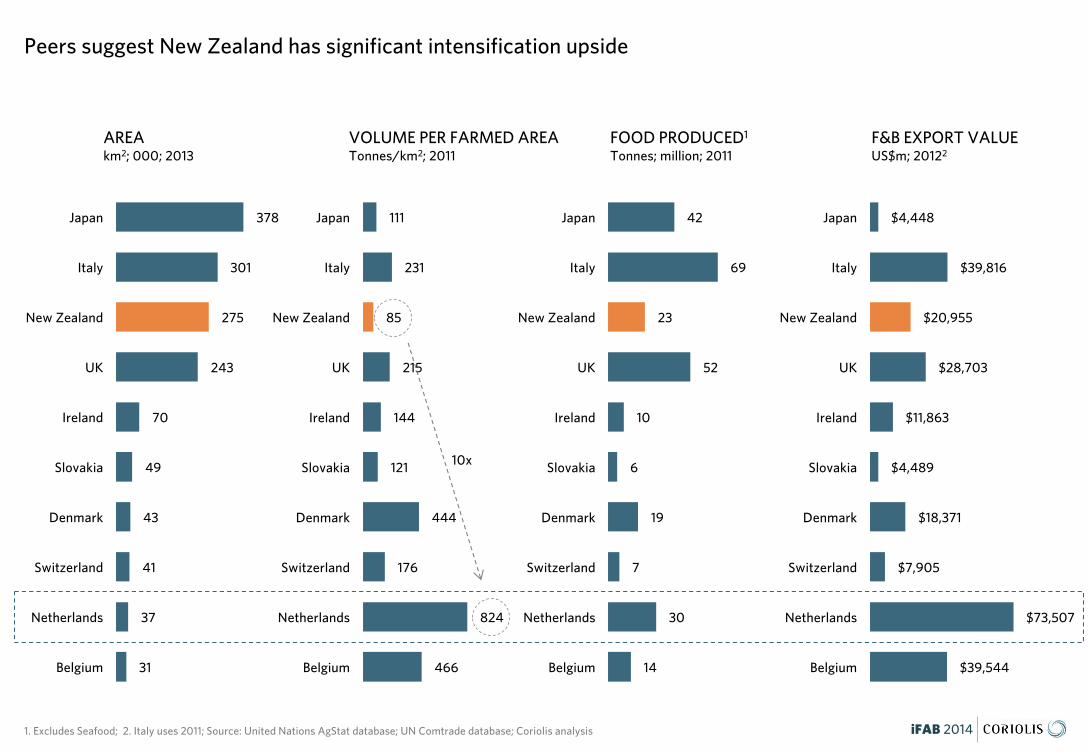

378

301

275

243

70

49

43

41

37

31

Japan

Italy

New Zealand

UK

Ireland

Slovakia

Denmark

Switzerland

Netherlands

Belgium

111

231

85

215

144

121

444

176

824

466

Japan

Italy

New Zealand

UK

Ireland

Slovakia

Denmark

Switzerland

Netherlands

Belgium

AREAkm2; 000; 2013

Peers suggest New Zealand has significant intensification upside

1. Excludes Seafood; 2. Italy uses 2011; Source: United Nations AgStat database; UN Comtrade database; Coriolis analysis

42

69

23

52

10

6

19

7

30

14

Japan

Italy

New Zealand

UK

Ireland

Slovakia

Denmark

Switzerland

Netherlands

Belgium

$4,448

$39,816

$20,955

$28,703

$11,863

$4,489

$18,371

$7,905

$73,507

$39,544

Japan

Italy

New Zealand

UK

Ireland

Slovakia

Denmark

Switzerland

Netherlands

Belgium

FOOD PRODUCED1

Tonnes; million; 2011F&B EXPORT VALUEUS$m; 20122

VOLUME PER FARMED AREATonnes/km2; 2011

10x

iFAB 2014

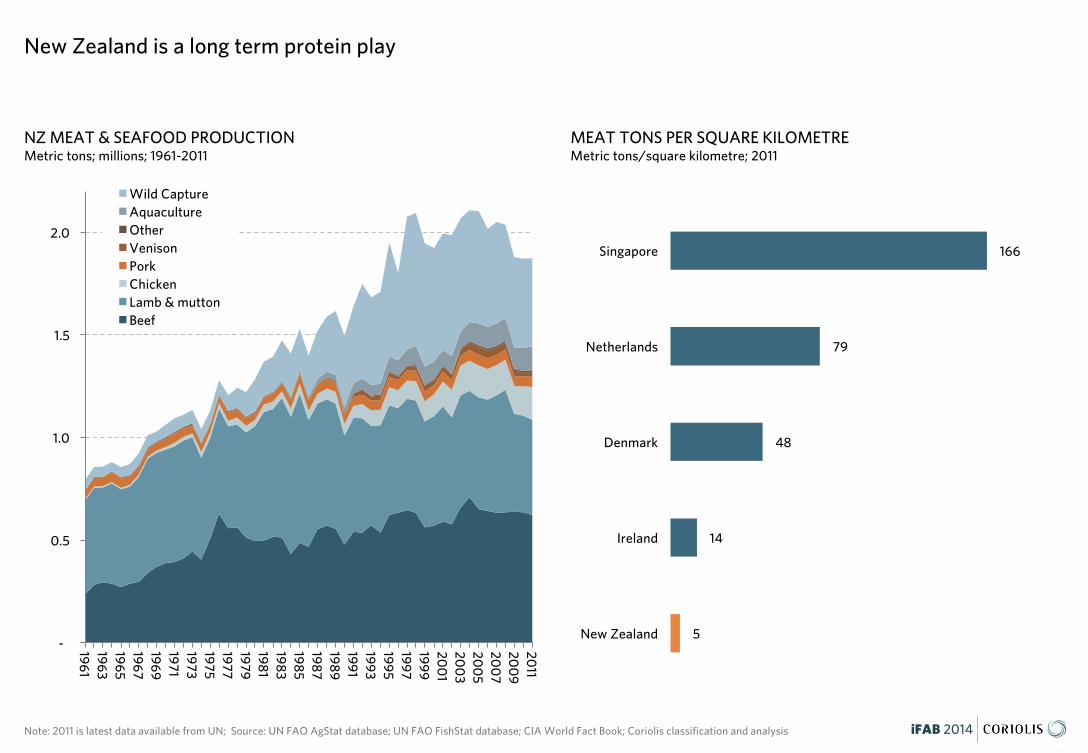

NZ MEAT & SEAFOOD PRODUCTION Metric tons; millions; 1961-2011

New Zealand is a long term protein play

Note: 2011 is latest data available from UN; Source: UN FAO AgStat database; UN FAO FishStat database; CIA World Fact Book; Coriolis classification and analysis

-

0.5

1.0

1.5

2.0

1961196319651967196919711973197519771979198

1198

3198

5198

7198

91991199319951997199920

01

200

320

05

200

720

09

2011

Wild CaptureAquacultureOtherVenisonPorkChickenLamb & muttonBeef

MEAT TONS PER SQUARE KILOMETREMetric tons/square kilometre; 2011

166

79

48

14

5

Singapore

Netherlands

Denmark

Ireland

New Zealand

GREAT… at producing food and beverages

iFAB 2014

iFAB 2014

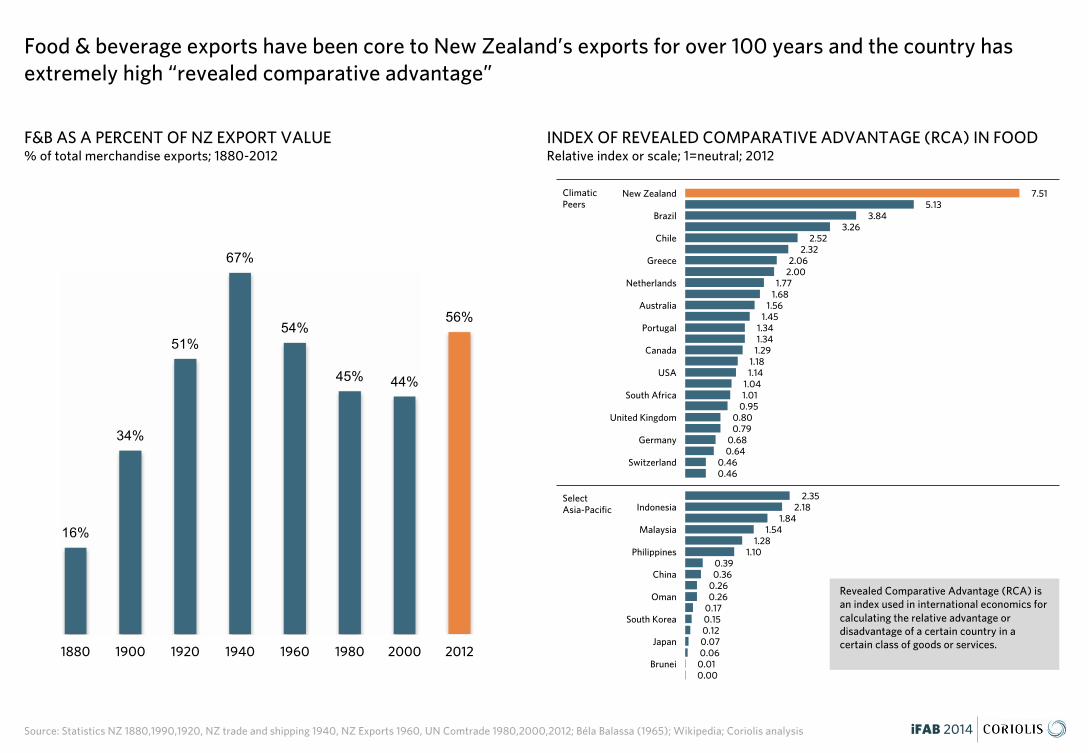

F&B AS A PERCENT OF NZ EXPORT VALUE% of total merchandise exports; 1880-2012

Food & beverage exports have been core to New Zealand’s exports for over 100 years and the country has extremely high “revealed comparative advantage”

Source: Statistics NZ 1880,1990,1920, NZ trade and shipping 1940, NZ Exports 1960, UN Comtrade 1980,2000,2012; Béla Balassa (1965); Wikipedia; Coriolis analysis

16%

34%

51%

67%

54%

45% 44%

56%

1880 1900 1920 1940 1960 1980 2000 2012

7.51 5.13

3.84 3.26

2.52 2.32

2.06 2.00

1.77 1.68

1.56 1.45

1.34 1.34 1.29

1.18 1.14

1.04 1.01

0.95 0.80 0.79

0.68 0.64

0.46 0.46

2.35 2.18

1.84 1.54

1.28 1.10

0.39 0.36

0.26 0.26

0.17 0.15 0.12 0.07 0.06

0.01 0.00

New Zealand

Brazil

Chile

Greece

Netherlands

Australia

Portugal

Canada

USA

South Africa

United Kingdom

Germany

Switzerland

Indonesia

Malaysia

Philippines

China

Oman

South Korea

Japan

Brunei

INDEX OF REVEALED COMPARATIVE ADVANTAGE (RCA) IN FOODRelative index or scale; 1=neutral; 2012

Revealed Comparative Advantage (RCA) is an index used in international economics for calculating the relative advantage or disadvantage of a certain country in a certain class of goods or services.

ClimaticPeers

Select Asia-Pacific

iFAB 2014

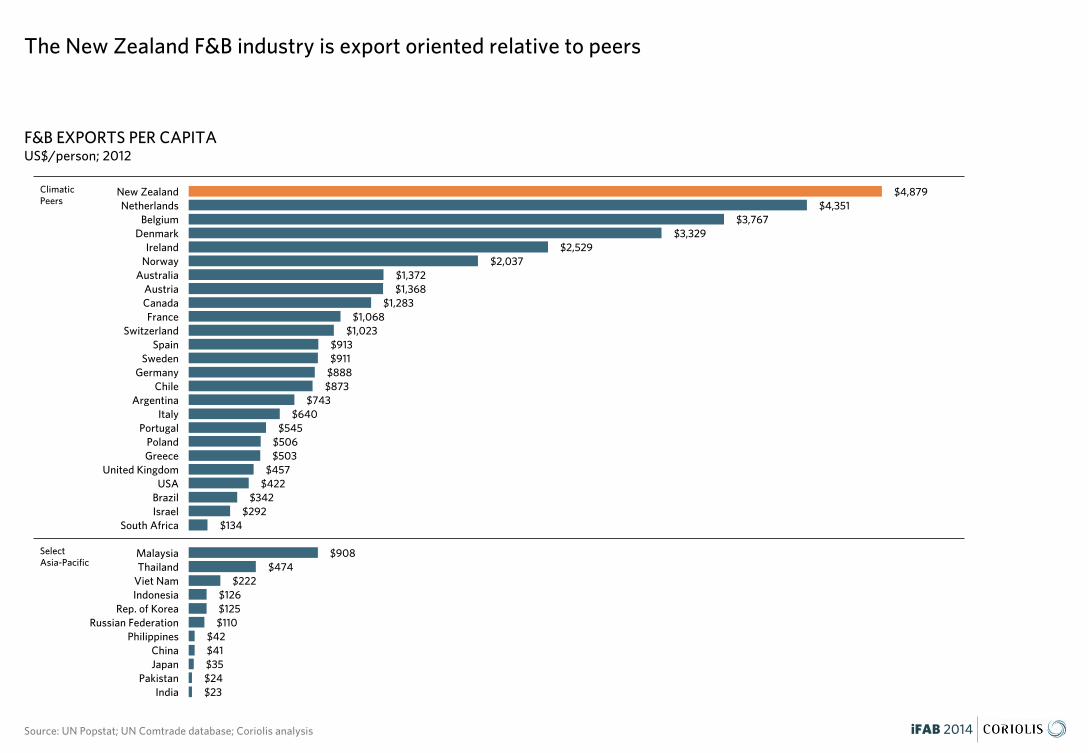

F&B EXPORTS PER CAPITAUS$/person; 2012

The New Zealand F&B industry is export oriented relative to peers

Source: UN Popstat; UN Comtrade database; Coriolis analysis

$4,879 $4,351

$3,767 $3,329

$2,529 $2,037

$1,372 $1,368

$1,283 $1,068

$1,023 $913 $911

$888 $873

$743 $640

$545 $506 $503

$457 $422

$342 $292

$134

$908 $474

$222 $126 $125 $110

$42 $41 $35 $24 $23

New ZealandNetherlands

BelgiumDenmark

IrelandNorway

AustraliaAustriaCanadaFrance

SwitzerlandSpain

SwedenGermany

ChileArgentina

ItalyPortugal

PolandGreece

United KingdomUSA

BrazilIsrael

South Africa

MalaysiaThailand

Viet NamIndonesia

Rep. of KoreaRussian Federation

PhilippinesChinaJapan

PakistanIndia

ClimaticPeers

Select Asia-Pacific

iFAB 2014

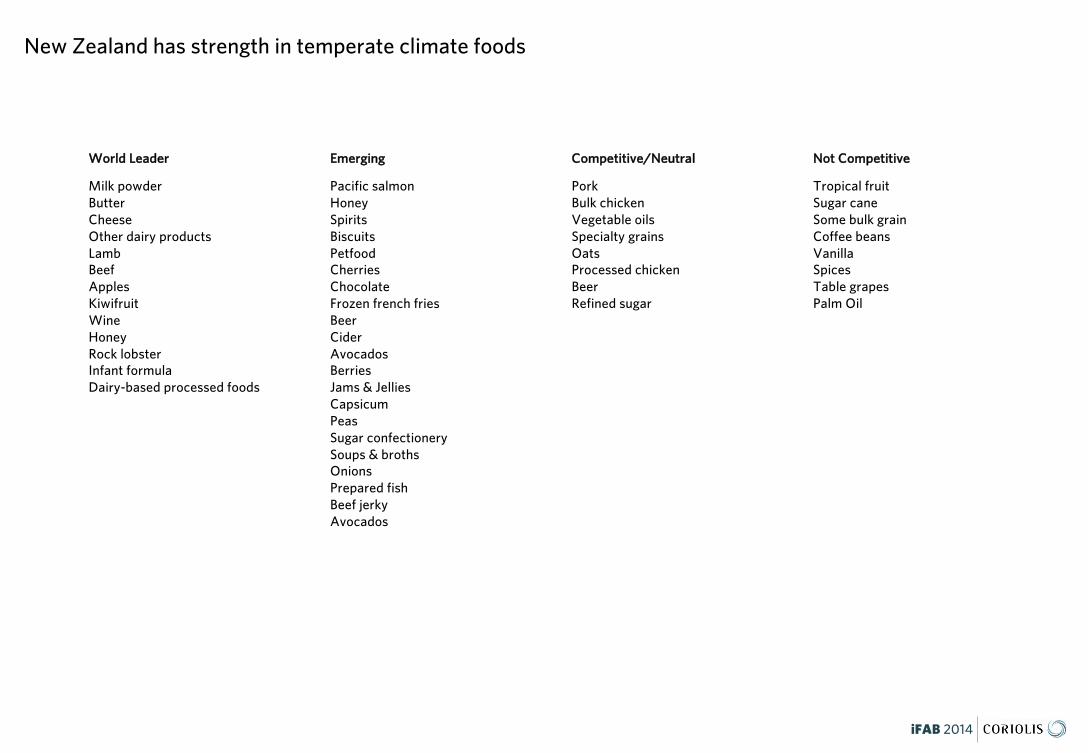

WWoorrlldd LLeeaaddeerr EEmmeerrggiinngg CCoommppeettiittiivvee//NNeeuuttrraall NNoott CCoommppeettiittiivvee

Milk powderButterCheeseOther dairy productsLambBeefApplesKiwifruitWineHoneyRock lobsterInfant formulaDairy-based processed foods

Pacific salmonHoneySpiritsBiscuitsPetfoodCherriesChocolateFrozen french friesBeerCiderAvocadosBerriesJams & JelliesCapsicumPeasSugar confectionerySoups & brothsOnionsPrepared fishBeef jerkyAvocados

PorkBulk chickenVegetable oilsSpecialty grainsOatsProcessed chickenBeerRefined sugar

Tropical fruitSugar caneSome bulk grainCoffee beansVanillaSpicesTable grapesPalm Oil

New Zealand has strength in temperate climate foods

iFAB 2014

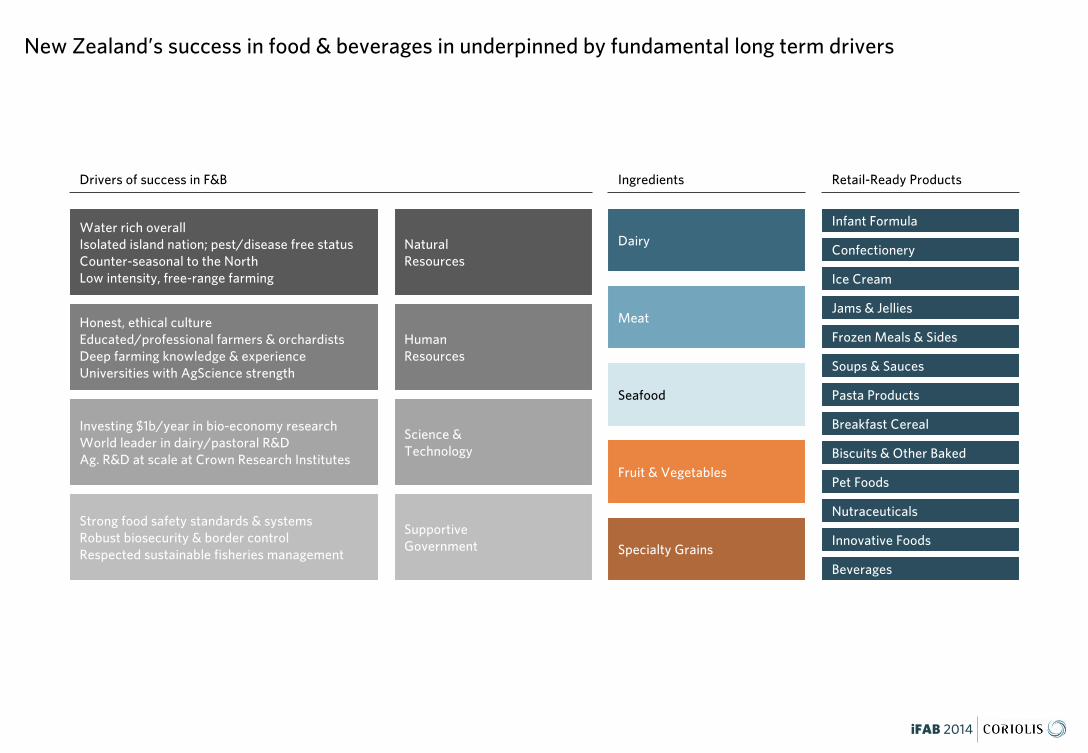

New Zealand’s success in food & beverages in underpinned by fundamental long term drivers

Water rich overallIsolated island nation; pest/disease free statusCounter-seasonal to the NorthLow intensity, free-range farming

Honest, ethical cultureEducated/professional farmers & orchardistsDeep farming knowledge & experience Universities with AgScience strength

Investing $1b/year in bio-economy researchWorld leader in dairy/pastoral R&DAg. R&D at scale at Crown Research Institutes

Strong food safety standards & systemsRobust biosecurity & border controlRespected sustainable fisheries management

Natural Resources

HumanResources

Science & Technology

SupportiveGovernment

Dairy

Meat

Seafood

Fruit & Vegetables

Specialty Grains

Infant Formula

Confectionery

Ice Cream

Jams & Jellies

Frozen Meals & Sides

Soups & Sauces

Pasta Products

Breakfast Cereal

Biscuits & Other Baked

Pet Foods

Nutraceuticals

Innovative Foods

Beverages

Ingredients Retail-Ready ProductsDrivers of success in F&B

iFAB 2014

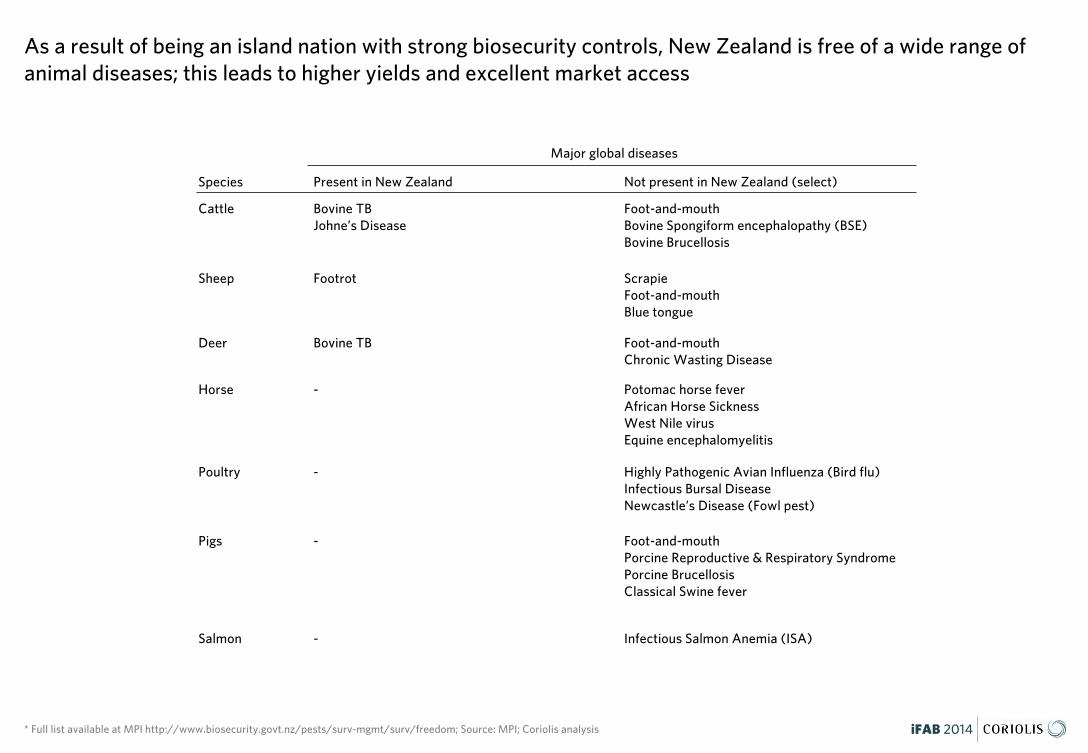

As a result of being an island nation with strong biosecurity controls, New Zealand is free of a wide range of animal diseases; this leads to higher yields and excellent market access

* Full list available at MPI http://www.biosecurity.govt.nz/pests/surv-mgmt/surv/freedom; Source: MPI; Coriolis analysis

Species

Major global diseases

Present in New Zealand Not present in New Zealand (select)

Cattle Bovine TBJohne’s Disease

Foot-and-mouthBovine Spongiform encephalopathy (BSE)Bovine Brucellosis

Sheep Footrot ScrapieFoot-and-mouthBlue tongue

Deer Bovine TB Foot-and-mouthChronic Wasting Disease

Horse - Potomac horse feverAfrican Horse Sickness West Nile virusEquine encephalomyelitis

Poultry - Highly Pathogenic Avian Influenza (Bird flu)Infectious Bursal Disease Newcastle’s Disease (Fowl pest)

Pigs - Foot-and-mouthPorcine Reproductive & Respiratory SyndromePorcine BrucellosisClassical Swine fever

Salmon - Infectious Salmon Anemia (ISA)

iFAB 2014

Canada

Sweden

Switzerland

Australia

Norway

Denmark

NNeeww ZZeeaallaanndd

Finland

Netherlands

Austria

Germany

Ireland

Belgium

Japan

United Kingdom

Italy

France

Spain

Portugal

Singapore

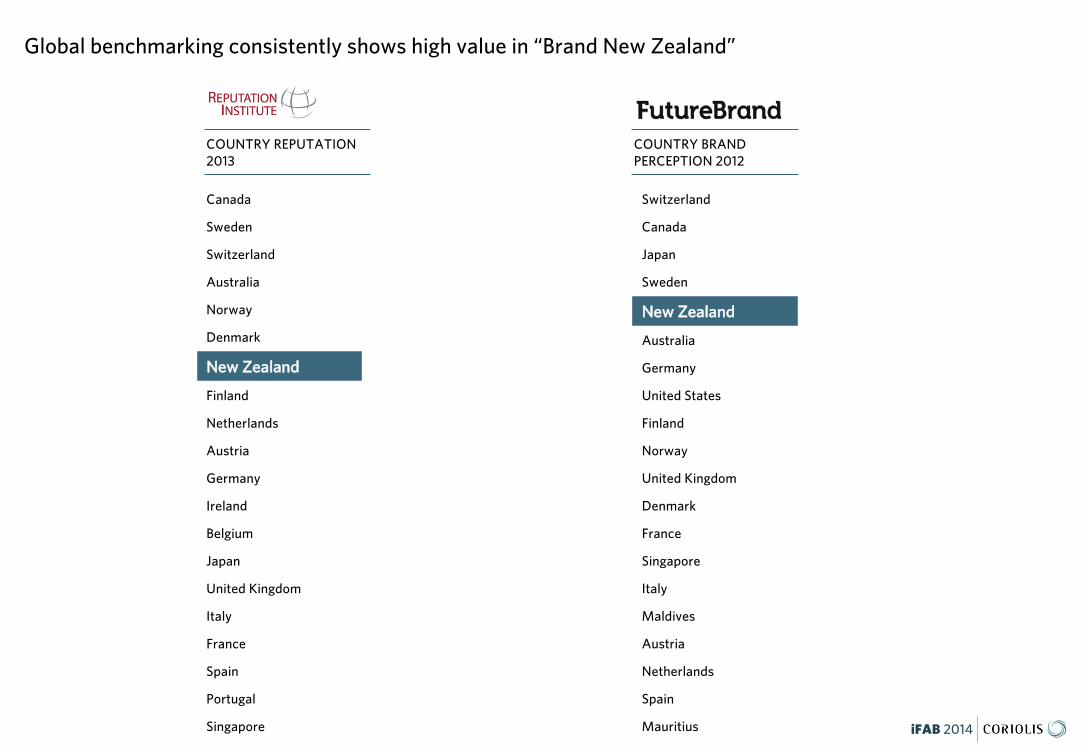

Global benchmarking consistently shows high value in “Brand New Zealand”

Switzerland

Canada

Japan

Sweden

NNeeww ZZeeaallaanndd

Australia

Germany

United States

Finland

Norway

United Kingdom

Denmark

France

Singapore

Italy

Maldives

Austria

Netherlands

Spain

Mauritius

COUNTRY REPUTATION 2013

COUNTRY BRAND PERCEPTION 2012

iFAB 2014

Consumers in key markets – particularly Asia – trust New Zealand food and beverages

Source: Gain report JA8713; Coriolis

-100

-80

-60

-40

-20

0

20

40

60

80

100

-100 -80 -60 -40 -20 0 20 40 60 80 100

EUScandinavia

Japan

USA

Asia (excl. China)

China

Lower cost & trusted

NEW ZEALAND& Australia

SAFE

UNSAFE

EXPENSIVECHEAP

JAPANESE PUBLIC IMAGE OF FOREIGN PRODUCTS 2009

iFAB 2014

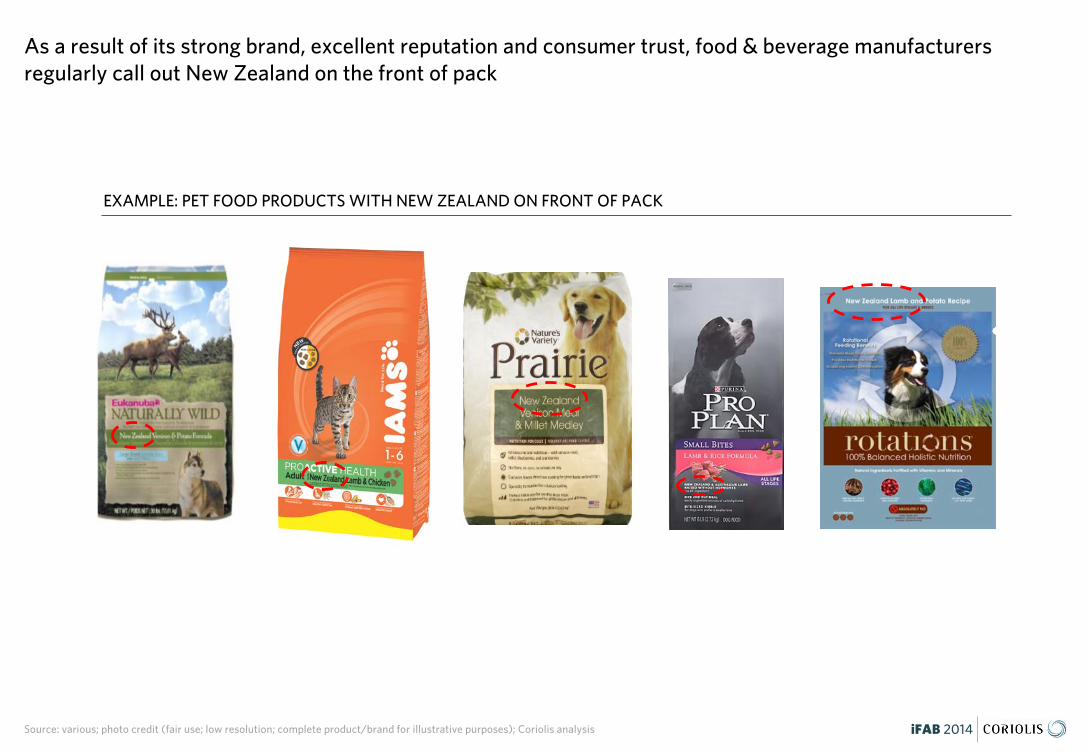

As a result of its strong brand, excellent reputation and consumer trust, food & beverage manufacturers regularly call out New Zealand on the front of pack

EXAMPLE: PET FOOD PRODUCTS WITH NEW ZEALAND ON FRONT OF PACK

Source: various; photo credit (fair use; low resolution; complete product/brand for illustrative purposes); Coriolis analysis

SUPPORTIVE… business ecosystem

iFAB 2014

iFAB 2014

BEST COUNTRIES FOR BUSINESS 2013

Multiple global surveys show NZ Inc. leading in international business friendly rankings

Ireland

NNEEWW ZZEEAALLAANNDD

Hong Kong

Denmark

Sweden

Finland

Singapore

Canada

Norway

Netherlands

Australia

United Kingdom

Belgium

United States

Iceland

Switzerland

Slovenia

Taiwan

France

Portugal

NNEEWW ZZEEAALLAANNDD

Denmark

Finland

Sweden

Singapore

Norway

Switzerland

Netherlands

Australia

Canada

Luxembourg

Germany

Iceland

United Kingdom

Belgium

Barbados

Hong Kong

Japan

United States

Uruguay

Singapore

Hong Kong

NNEEWW ZZEEAALLAANNDD

United States

Denmark

Malaysia

South Korea

Georgia

Norway

United Kingdom

Australia

Finland

Iceland

Sweden

Ireland

Taiwan

Lithuania

Thailand

Canada

Mauritius

NNEEWW ZZEEAALLAANNDD

Singapore

Hong Kong

Canada

Malaysia

Colombia

Ireland

Israel

United States

South Africa

United Kingdom

Mauritius

Thailand

Albania

Slovenia

Belgium

Georgia

Japan

Macedonia

Peru

Hong Kong

Singapore

Australia

NNEEWW ZZEEAALLAANNDD

Switzerland

Canada

Chile

Mauritius

Denmark

United States

Ireland

Bahrain

Estonia

United Kingdom

Luxembourg

Finland

Netherlands

Sweden

Germany

Taiwan

CORRUPTION PERCEPTIONS 2013

EASE OF DOING BUSINESS 2013

INVESTOR PROTECTION 2013

ECONOMIC FREEDOM 2013

iFAB 2014

New Zealand food & beverage sectors have strong and robust industry representation

DAIRY MEAT SEAFOOD PRODUCE PROCESSED FOODS BEVERAGES

iFAB 2014

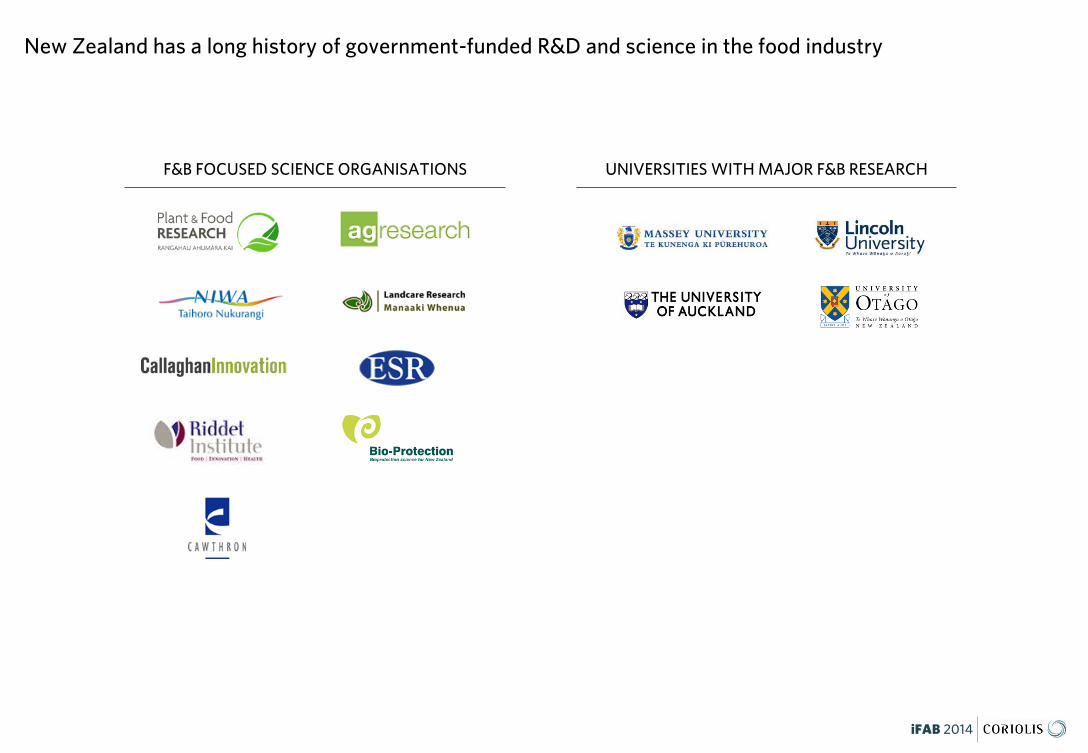

New Zealand has a long history of government-funded R&D and science in the food industry

F&B FOCUSED SCIENCE ORGANISATIONS UNIVERSITIES WITH MAJOR F&B RESEARCH

iFAB 2014

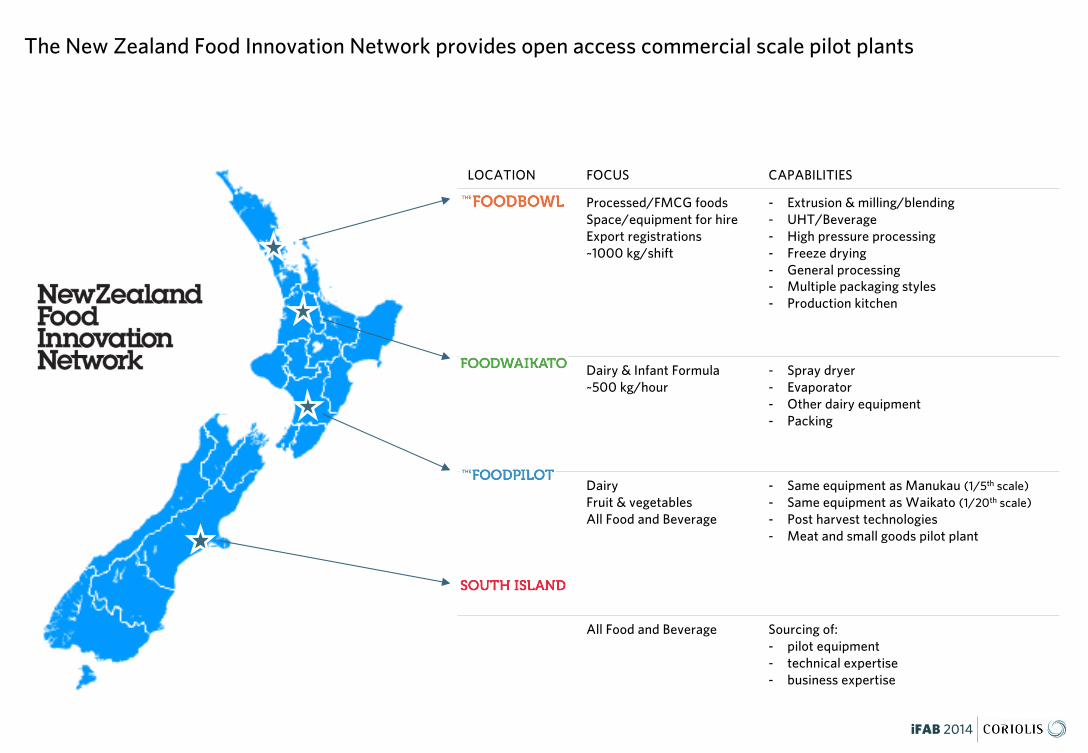

The New Zealand Food Innovation Network provides open access commercial scale pilot plants

LOCATION FOCUS CAPABILITIES

Processed/FMCG foods Space/equipment for hireExport registrations ~1000 kg/shift

- Extrusion & milling/blending- UHT/Beverage - High pressure processing- Freeze drying- General processing- Multiple packaging styles- Production kitchen

Dairy & Infant Formula~500 kg/hour

- Spray dryer- Evaporator- Other dairy equipment- Packing

DairyFruit & vegetablesAll Food and Beverage

- Same equipment as Manukau (1/5th scale)- Same equipment as Waikato (1/20th scale) - Post harvest technologies- Meat and small goods pilot plant

All Food and Beverage Sourcing of: - pilot equipment- technical expertise- business expertise

ATTRACTING… investment

iFAB 2014

iFAB 2014

EUROPE

AMERICAS

AUSTRALIA

ASIA

The New Zealand F&B industry has attracted investment from a wide range of global leaders

iFAB 2014

New investors continue to arrive in New Zealand

2010 2011 2012 2013

iFAB 2014

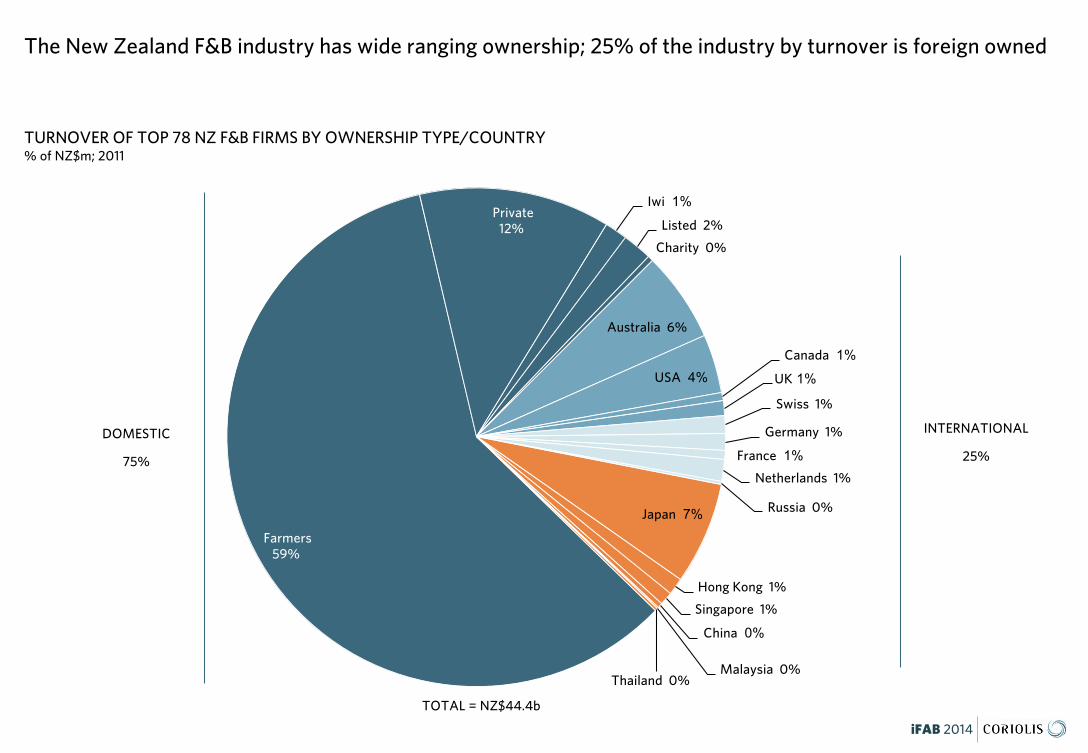

Farmers 59%

Private 12%

Iwi 1%

Listed 2%

Charity 0%

Australia 6%

USA 4%Canada 1%

UK 1%

Swiss 1%

Germany 1%

France 1%Netherlands 1%

Russia 0%Japan 7%

Hong Kong 1%

Singapore 1%

China 0%

Malaysia 0%Thailand 0%

TURNOVER OF TOP 78 NZ F&B FIRMS BY OWNERSHIP TYPE/COUNTRY% of NZ$m; 2011

The New Zealand F&B industry has wide ranging ownership; 25% of the industry by turnover is foreign owned

DOMESTIC

75%

TOTAL = NZ$44.4b

INTERNATIONAL

25%

LEARN… more

iFAB 2014

iFAB 2014

Further information on all the major sectors of the New Zealand food & beverage industry is available in the other reports in this series

Other reports, including those from previous years, are available on the MBIE or Coriolis website…

www.med.govt.nz/sectors-industries/food-beverage/information-project/ www.coriolisresearch.com/reports/

iFAB 2014

Agency Key areas of responsibility Contact details

- Economic Development Policy- Research goals & priorities- Scientific research funding- Labour market/employment relations

www.mbie.govt.nz/contact-uswww.foodandbeverage.govt.nz

- Trade promotion- Export development

www.nzte.govt.nz/about-nzte/pages/new-zealand-offices.aspx

- Trade relationships- Trade policy, including trade negotiations

and offshore market access barriers

mfat.govt.nz/About-the-Ministry/Contact-us/index.php

- Biosecurity- Agricultural production- Food safety

www.mpi.govt.nz/AboutMPI/ContactUs/tabid/94/Default.aspx

For more information or assistance in investing in the New Zealand food and beverage industry contact:

The Food and Beverage Information Project

The Food & Beverage Information Project is the first comprehensive overview of the state of New Zealand’s Food & Beverage (F&B) industry. Part of the Government’s Business Growth Agenda (BGA), it is an integrated programme of work focusing on the six key inputs businesses need to succeed, grow and add jobs; export markets, capital markets, innovation, skilled and safe workplaces, natural resources and infrastructure.

Essentially, the BGA Export Markets goal will require lifting the ratio of exports from today’s rate of 30% of GDP to 40% by 2025. This equates to doubling exports in real terms (or tripling exports in nominal non-inflation adjusted terms). This in turn equates to achieving a 7% per annum growth rate over the next twelve years.

This five-year project analyses the main sectors in F&B, including dairy, meat, seafood, produce, processed foods, and beverages, as well as providing an overview of how the industry is fairing in our major markets. It also conducts in-depth sector reviews on a rotating basis. The information is updated annually and feedback from users shows the project is acting as a vital tool for companies looking to expand and grow exports.

Why Food & Beverage?

The Food & Beverage industry is vitally important to the New Zealand economy. Food & Beverage accounts for 56% of our merchandise trade exports and one in five jobs across the wider value chain. In addition, F&B acts as a vital ambassador for the country, being in most cases the first exposure global consumers get to “Brand New Zealand.”

New Zealand’s F&B exports are growing strongly and the country’s export performance is strong and improving relative to peers. In the 15 years leading up to 2010, New Zealand's food and beverage exports grew at a compound annual rate of 7% per annum. So one way to look at the challenge is to ask – can we continue to grow our food & beverage exports at the same rate? To understand if this is possible we need to know what has been driving our success.

What is the purpose of the food and beverage information project?

The project pulls together the available information on the food and beverage industry into one place, in a form which is familiar and useful to business. The reports contain analysis and interpretation of trends and opportunities to materially assist with business strategy and government policy.

The information will be of vital use to businesses, investors, government, and research institutions as the industry expands and diversifies. This industry view will be very useful to government, enabling better dialogue and the opportunity to address issues collectively.

What benefit will this bring to businesses?

The Project will have many uses for businesses. These include:

– As a base of market intelligence to enable business to be much more targeted in their own market research

– Reviewing and informing offshore market development (including export and investment) strategies

– Assisting in identifying areas of innovation and R&D for the future

– Identifying strategic partners and collaborators– Enabling a company to benchmark performance with that

of its competitors– Monitoring industry activity– Gaining a better understanding of their own industry

sector– Identifying internal capability needs or external inputs

How will government use the reports?

This information will provide much greater insight into the industry, which is useful for a range of policy developments, from regulatory frameworks to investment in science and skills and facilitating access to international markets. In particular, a single source of factual information will enable government agencies to better coordinate their efforts across the system and be more responsive to addressing industry issues.

iFAB 2014

Coriolis is a boutique management consultingfirm that focuses on food, consumerpackaged goods, retailing and foodservice.

Coriolis advises clients on strategy,operations, organization, and mergers andacquisitions. We develop practical, fact-basedinsights grounded in the real world that guideour clients decisions and actions. Founded in1999, Coriolis is based in Auckland, NewZealand and works on projects across theAsia Pacific region.

WHAT WE DO

We help our clients assemble the factsneeded to guide their big decisions. We makepractical recommendations. Whereappropriate, we work with them to makechange happen.

HOW WE DO IT

Our style is practical and down-to-earth. Wetry to put ourselves in our clients’ shoes andfocus on actions. We listen hard, but we aresuspicious of the consensus. We provide anexternal, objective perspective. We are happyto link our fees to results.

WHO WE WORK WITH

We only work with a select group of clientswe trust. We build long term relationshipswith our clients and more than 80% of ourwork comes from existing clients. Our clientstrust our experience, advice and integrity.

Typical assignments for clients include…

FIRM STRATEGY & OPERATIONS:We help clients develop their own strategy forgrowing sales and profits. We have a strongbias towards growth driven by new products,new channels and new markets.

MARKET ENTRYWe help clients identify which countries arethe most attractive – from a consumer, acompetition and a channel point-of-view.Following this we assist in developing a planfor market entry and growth.

VALUE CREATIONWe help clients create value through revenuegrowth and cost reduction.

TARGET IDENTIFICATIONWe help clients identify high potentialacquisition targets by profiling industries,screening companies and devising a plan toapproach targets.

DUE DILIGENCEWe help organisations make better decisionsby performing consumer and market-focuseddue diligence and assessing performanceimprovement opportunities.

EXPERT WITNESSWe provide expert witness support to clientsin legal cases and insurance claims. We assistwith applications under competition/fairtrade laws and regulations.

READ MORE ON OUR WEBSITE.

ABOUT CORIOLIS’ SERVICES

CORIOLIS LIMITEDPO BOX 90-509AUCKLAND, NEW ZEALANDT: +64 9 623 1848www.coriolisresearch.com

ABOUT CORIOLIS’ SERVICES