January, 2018INVESTORS PRESENTATION1

JANUARY, 2018

INVESTORS PRESENTATION

January, 2018INVESTORS PRESENTATION2

DISCLAIMER

Some of the statements contained in this document may be forward-looking statements concerning Vilmorin & Cie SA's financial position,results, businesses, strategy or projects.

Vilmorin & Cie SA considers that such statements are based onreasonable assumptions but cannot and does not give any assurancethat the Group's future performance will be consistent with thosestatements.

Actual results could differ from those currently anticipated in suchstatements due to a certain number of inherent risks and uncertainties,most of which are beyond Vilmorin & Cie SA's control, such as thosedescribed in the documents filed or to be filed by Vilmorin & Cie SA withthe French securities regulator (Autorité des marchés financiers) andmade available for downloading from the Company's website:www.vilmorincie.com

January, 2018INVESTORS PRESENTATION3

AGENDA

VILMORIN & CIE AT A GLANCE s. 04

VILMORIN & CIE GROWTH STRATEGY s. 11

SALES FOR THE 1st QUARTER 2017-2018 s. 22

OUTLOOK FOR 2017-2018 AND MID TERM AMBITIONS s. 30

VILMORIN & CIE ON THE STOCK EXCHANGE s. 34

SCHEDULE AND CONTACTS s. 37

APPENDICES s. 40

January, 2018INVESTORS PRESENTATION4

4

VILMORIN & CIE AT A GLANCE

January, 2018INVESTORS PRESENTATION5

VILMORIN & CIE, 4TH LARGEST SEEDS COMPANY IN THE WORLD

Fourth largest seeds company in the world with leading positions on its core activities

Pure player built up on historical expertise in botany since 1743and on the basis of real proximity with the agricultural world

A long-term vision of the development, strengthened by the consistent support of its reference shareholder, Limagrain, an international agricultural cooperative group

VILMORIN & CIE AT A GLANCE

N°2worldwide

for vegetable

seeds

N°1in Europe

for straw

cereals (1)

N°3in North

America for

corn seeds

N°4in Europe

for corn

seeds

(1) Wheat and barley

January, 2018INVESTORS PRESENTATION6

A FULL CONTROL OF ALL STAGES IN SEEDS BUSINESS

VILMORIN & CIE AT A GLANCE

ANALYZING

NEEDS

CREATING

NEW SEEDS

COLLECTING

GENETIC

RESOURCES

PRODUCING

SEEDS

DISTRIBUTING AND

SELLING SEEDS

AROUND 300 VARIETIES LAUNCHED PER YEAR

A 7 TO 10 YEARS CYCLE

January, 2018INVESTORS PRESENTATION7

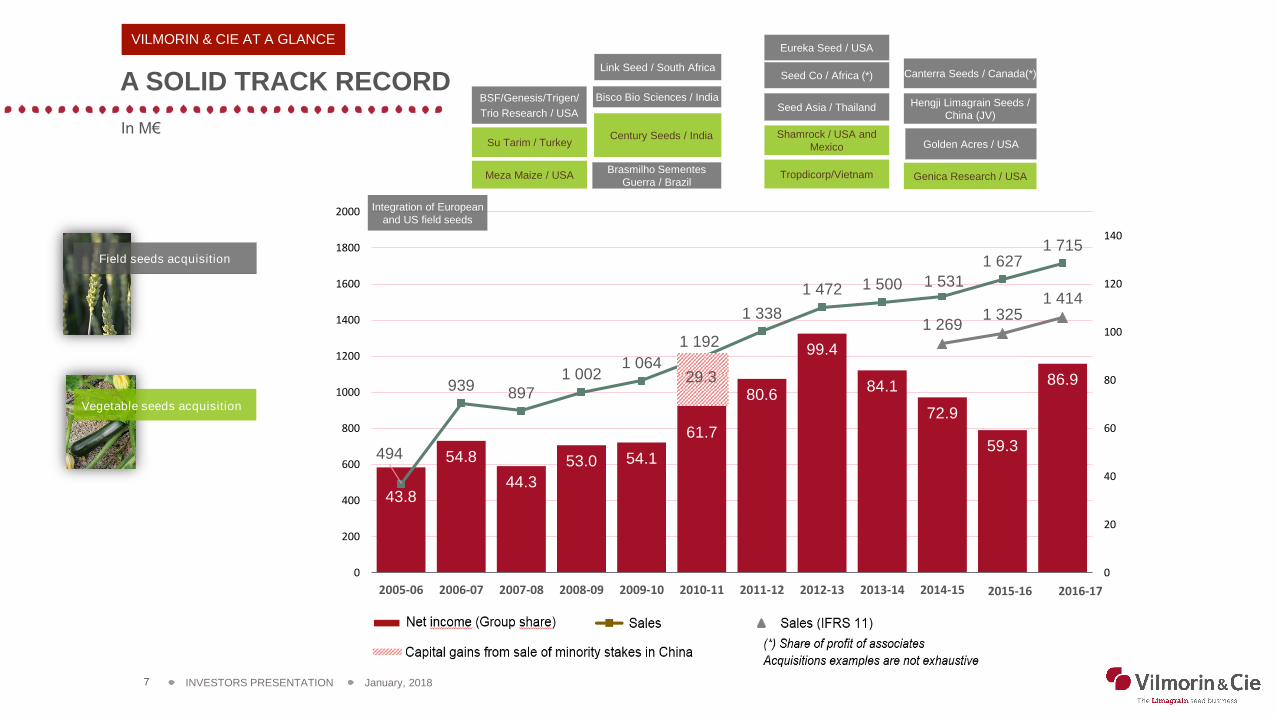

43.8

54.8

44.3

53.0 54.1

80.6

99.4

84.1

72.9

59.3

86.9

494

939897

1 0021 064

1 192

1 338

1 472 1 500 1 531

1 6271 715

1 2691 325

1 414

0

20

40

60

80

100

120

140

0

200

400

600

800

1000

1200

1400

1600

1800

2000

2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16 2016-17

A SOLID TRACK RECORD

VILMORIN & CIE AT A GLANCE

In M€

Integration of European

and US field seeds

Brasmilho Sementes

Guerra / Brazil

Bisco Bio Sciences / IndiaBSF/Genesis/Trigen/

Trio Research / USA

Century Seeds / India

Link Seed / South Africa

Eureka Seed / USA

Seed Co / Africa (*)

Seed Asia / Thailand

Field seeds acquisition

Hengji Limagrain Seeds /

China (JV)

Golden Acres / USA

Vegetable seeds acquisition

Tropdicorp/Vietnam

Shamrock / USA and

Mexico

Canterra Seeds / Canada(*)

Genica Research / USA

Su Tarim / Turkey

Meza Maize / USA

29.3

61.7

January, 2018INVESTORS PRESENTATION8

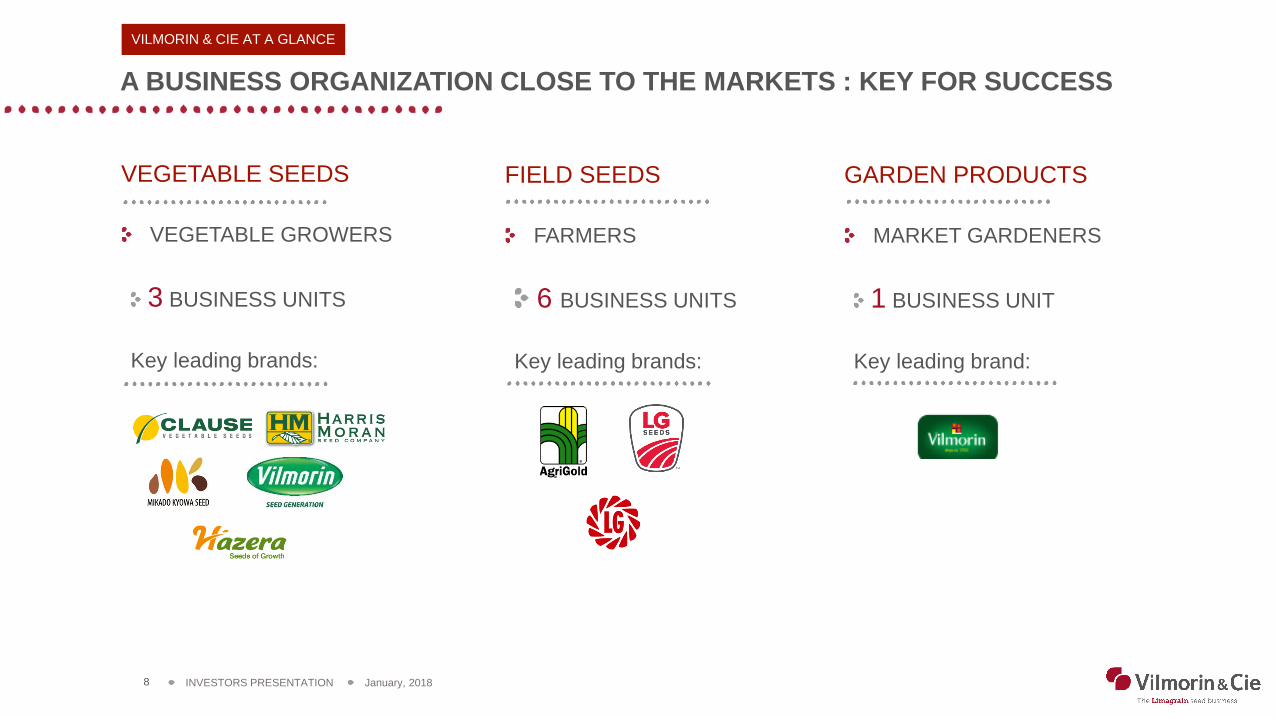

A BUSINESS ORGANIZATION CLOSE TO THE MARKETS : KEY FOR SUCCESS

VILMORIN & CIE AT A GLANCE

VEGETABLE SEEDS

VEGETABLE GROWERS

3 BUSINESS UNITS

Key leading brands:

FIELD SEEDS

FARMERS

6 BUSINESS UNITS

Key leading brands:

GARDEN PRODUCTS

MARKET GARDENERS

1 BUSINESS UNIT

Key leading brand:

January, 2018INVESTORS PRESENTATION9

Investors

(of which ~50%

internationally

based: USA, UK,

Singapore,

Belgium…)

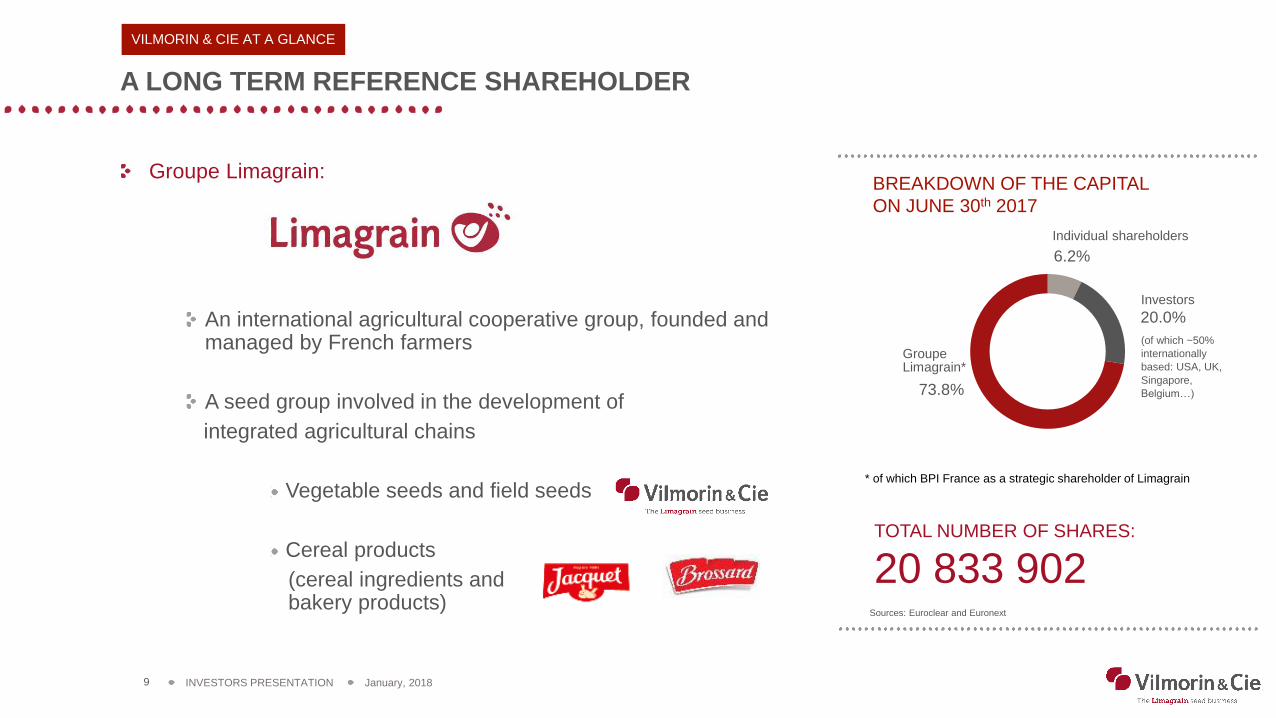

A LONG TERM REFERENCE SHAREHOLDER

Groupe Limagrain:

An international agricultural cooperative group, founded and managed by French farmers

A seed group involved in the development of

integrated agricultural chains

Vegetable seeds and field seeds

Cereal products

(cereal ingredients and bakery products)

BREAKDOWN OF THE CAPITAL

ON JUNE 30th 2017

6.2%

20.0%

73.8%

Groupe Limagrain*

Individual shareholders

* of which BPI France as a strategic shareholder of Limagrain

Sources: Euroclear and Euronext

TOTAL NUMBER OF SHARES:

20 833 902

VILMORIN & CIE AT A GLANCE

January, 2018INVESTORS PRESENTATION10

Moving agriculture forward to meet food challenges

A LONG TERM REFERENCE SHAREHOLDER

Groupe Limagrain, a reference shareholder guaranteeing:

Stable corporate governance

Long term strategy

A perfect knowledge of agriculture, customers and theirs needs

LIMAGRAIN IN BRIEF

MISSION

* Figures for the overall scope of activity worldwide, taking into account data from the

companies AgReliant, AGT, Genective, Seed Co and Soltis.

VILMORIN & CIE AT A GLANCE

STRATEGY

KEY FIGURES

To provide farmers throughout the world with sustainable solutions to improve their farms' profitability

Nearly 2,000 farmer members2.6 billion euros in salesMore than 10,000 employees

January, 2018INVESTORS PRESENTATION11

11

VILMORIN & CIE GROWTH STRATEGY

January, 2018INVESTORS PRESENTATION12

1/ PROMISING WORLD SEEDS MARKETS

VILMORIN & CIE GROWTH STRATEGY

POWERFUL GROWTH FACTORS:

Increase in seeds demand

Growth in the world population (10 bn in 2050)

Improvement in the standards of living

Increase in the use of commercial seeds

Ever greater use of genetically modified

(“GM”) seeds worldwide

Vegetable seeds

(Conventional seeds)

WORLD MARKET

FOR COMMERCIAL SEEDS (2016)

(CAGR between 2011 and 2016)

Field Seeds –

Conventional seeds

Field Seeds –

GM seeds

14,1 %

30,6 %

55,3 %

MARKET VALUE 2016:

$36.9 BN. GLOBAL CAGR: +1,4% / YEAR

Sources: Phillips McDougall 2017 and ISAAA 2017

January, 2018INVESTORS PRESENTATION13

1/ MARKET FOR SEEDS: SLIGHT INCREASE FOR GMO IN 2016

VILMORIN & CIE GROWTH STRATEGY

WORLD MARKET ACREAGE

185.1 million hectares (around 10% of arable land), +3% / 2015,

grown by 18 million farmers in 26 countries

Sources: ISAAA 2017. Phillips McDougall 2017

WORLD MARKET VALUE

More than $20 billion in 2016 (i.e. 55 % of the world market for seeds), +3% / 2015

million ha

185GMO :

ACREAGE PER COUNTRY

-10

10

30

50

70

90

110

130

150

170

190

1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Others

China

India

Canada

Argentina

Brazil

USA

January, 2018INVESTORS PRESENTATION14

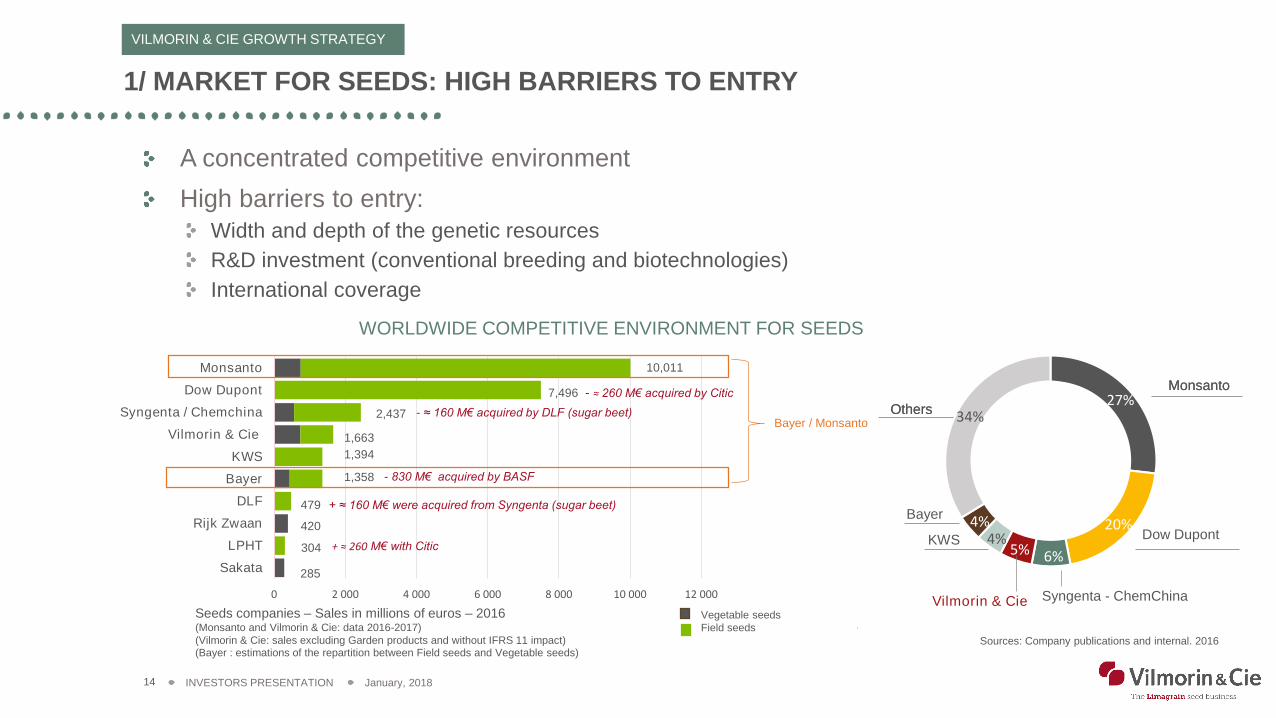

1/ MARKET FOR SEEDS: HIGH BARRIERS TO ENTRY

VILMORIN & CIE GROWTH STRATEGY

A concentrated competitive environment

High barriers to entry:

Width and depth of the genetic resources

R&D investment (conventional breeding and biotechnologies)

International coverage

WORLDWIDE COMPETITIVE ENVIRONMENT FOR SEEDS

Seeds companies – Sales in millions of euros – 2016(Monsanto and Vilmorin & Cie: data 2016-2017)

(Vilmorin & Cie: sales excluding Garden products and without IFRS 11 impact) (Bayer : estimations of the repartition between Field seeds and Vegetable seeds)

Sources: Company publications and internal. 2016

KWS

Monsanto

Others

Vegetable seeds

Field seeds

0 2 000 4 000 6 000 8 000 10 000 12 000

Sakata

LPHT

Rijk Zwaan

DLF

Bayer

KWS

Vilmorin & Cie

Syngenta / Chemchina

Dow Dupont

Monsanto

+ ≈ 260 M€ with Citic

- 830 M€ acquired by BASF

Bayer / Monsanto

+ ≈ 160 M€ were acquired from Syngenta (sugar beet)

7,496 - ≈ 260 M€ acquired by Citic

1,663

1,394

420

479

304

285

2,437 - ≈ 160 M€ acquired by DLF (sugar beet)

10,011

1,358

27%

20%

6%5%4%

4%

34%

Dow Dupont

Syngenta - ChemChina

Bayer

Vilmorin & Cie

Monsanto

Others

January, 2018INVESTORS PRESENTATION15

2/ A STRATEGY OF WINNING MARKET SHARES

VILMORIN & CIE GROWTH STRATEGY

3 strategic priorities

3 strategic foundations

INNOVATION TARGETED POLICY OF

EXTERNAL GROWTHINTERNATIONALIZATION

Vegetable seeds: reinforce world leadership

Corn seeds: become a global actor

Wheat seeds : become the world reference

January, 2018INVESTORS PRESENTATION16

34%

33%

17%

16%

3 / VEGETABLE SEEDS. DIVISION PROFILE

VILMORIN & CIE GROWTH STRATEGY

Tomato

Sweet and hot pepper

Carrot

Melon

SquashBeanOnion

Others

SALES OF VEGETABLE SEEDSPER CROP. 2016-2017

SALES OF VEGETABLE SEEDSPER GEOGRAPHICAL AREA. 2016-2017

Europe

Americas

Africa / Middle East

Asia / Oceania

KEY FIGURES 2016-2017

32736

17.1%

COUNTRIES

WITH

LOCATIONS

M€

SALES

OPERATING

MARGIN

Current operating margin : 17.3%

1

3

1

1

22

1,2,3: worldwide competitive positions

N°2in the

world

- A very strong competitive position addressing worldwide vegetable growers and food processors

- An extremely diversified product line-up with more than 30 species (tomato, carrot, melon, pepper, bean, etc.)

January, 2018INVESTORS PRESENTATION17

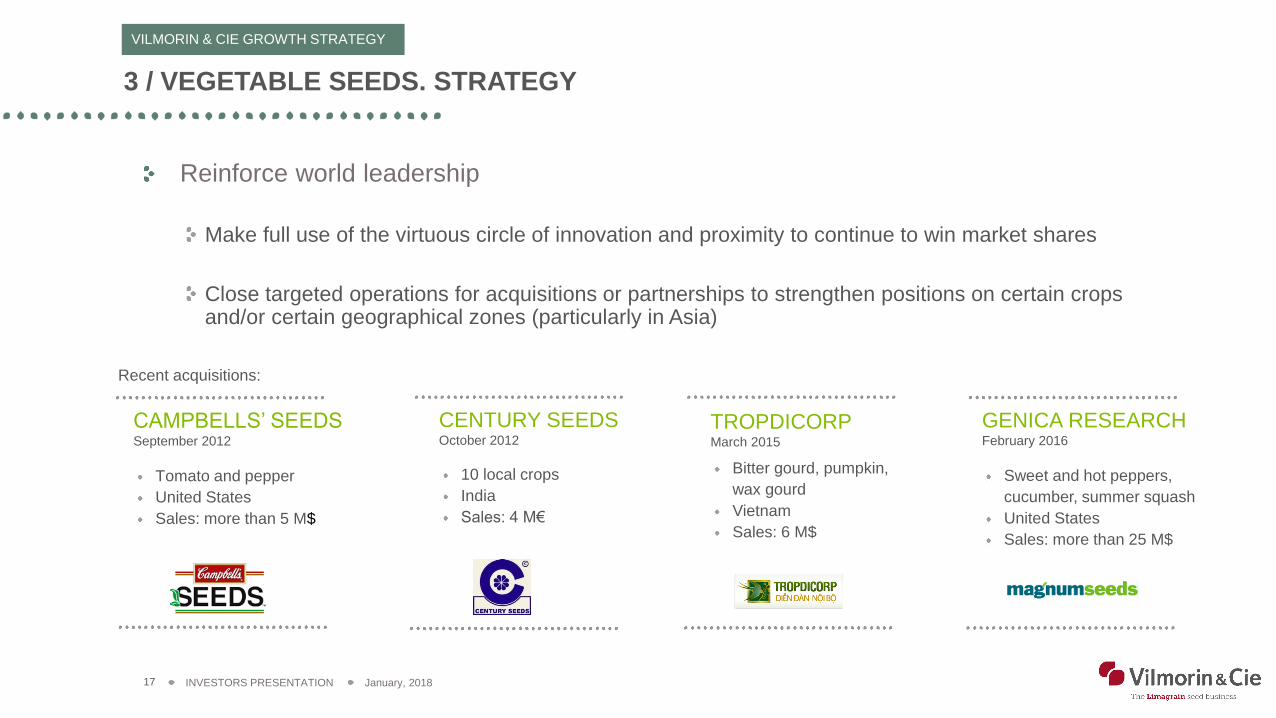

3 / VEGETABLE SEEDS. STRATEGY

VILMORIN & CIE GROWTH STRATEGY

Reinforce world leadership

Make full use of the virtuous circle of innovation and proximity to continue to win market shares

Close targeted operations for acquisitions or partnerships to strengthen positions on certain crops and/or certain geographical zones (particularly in Asia)

CAMPBELLS’ SEEDSSeptember 2012

Tomato and pepper

United States

Sales: more than 5 M$

CENTURY SEEDSOctober 2012

10 local crops

India

Sales: 4 M€

TROPDICORP March 2015

Bitter gourd, pumpkin,

wax gourd

Vietnam

Sales: 6 M$

GENICA RESEARCHFebruary 2016

Sweet and hot peppers,

cucumber, summer squash

United States

Sales: more than 25 M$

Recent acquisitions:

January, 2018INVESTORS PRESENTATION18

52%

42%

3% 3%

4 / FIELD SEEDS. DIVISION PROFILE

VILMORIN & CIE GROWTH STRATEGY

SALES OF FIELD SEEDS*PER GEOGRAPHICAL AREA. 2016-2017

Europe

Americas

Asia / Oceania

KEY FIGURES 2016-2017

33

626

2.7%

COUNTRIES

WITH

LOCATIONS*

M€

SALES

OPERATING

MARGIN

Current operating margin : 3.6%

(928 M€)*

N°1in Europe

for straw

cereals

N°3in North

America

And N°4in Europe

for corn seeds

- One of the top players in strategic crops targeting farmers

- 2 worldwide strategic crops: corn and wheat

- And regional strategic crops: sunflower, rapeseed and barley in Europe, rice in India, and soybean, which Vilmorin & Cie distributes in North and South America and in South Africa

11%

4%

4%

15%

66%

SALES OF FIELD SEEDS*PER CROP. 2016-2017

Cereals (corn,

wheat, barley)

Other field seeds

Rapeseed

Feed grains

Sunflower

(1) Wheat and barley

Africa / Middle East

* Without the application of the standard IFRS 11 (“Joint arrangements”) resulting in certain

activities being consolidated using the “Equity method” since 2014-2015 (in particular AgReliant.

North America. Field Seeds)

(1)

January, 2018INVESTORS PRESENTATION19

4 / CORN SEEDS. STRATEGY

VILMORIN & CIE GROWTH STRATEGY

CORN SEEDS: BECOME A GLOBAL ACTOR

SEED COMinority stake. 2014

#1 African seeds company

Sales: 135 M$

6 factories & 8 research stations in south

east Africa

SEED ASIAMarch 2014

Hybrid tropical corn

Thailand

Sales: 9 M$

HENGJI LIMAGRAIN SEEDSJV. September 2015

Corn

China

Production and distribution

Technological strategic partnership between Vilmorin & Cie and KWS

*Source: USDA

Internationalize activitiesfurther afield from European and North American activities on the largest world seed market in terms of value

(more than $15 bn in 2016*)

GM corn traits licensing agreements with Syngenta (October 2015)

Develop a proprietary portfolio of GM seeds

Recent acquisitions:

January, 2018INVESTORS PRESENTATION20

4 / WHEAT SEEDS. STRATEGY

VILMORIN & CIE GROWTH STRATEGY

WHEAT SEEDS: BECOME THE WORLD REFERENCE

*Source: USDA

Consolidate position of leader in Europe and become the world reference of the first worldwide crop in terms of cultivated surface areas (more than 220 million hectares in 2016*)

Develop more efficient seeds and contributeto converting the market to high yield seeds

Gradually extend the positions to other major wheat markets and develop strong partnerships internationally

NORTH AMERICA

United States

Canada

AUSTRALIA

Australian Grain Technologies

OTHER ZONES

South America

Asia

January, 2018INVESTORS PRESENTATION21

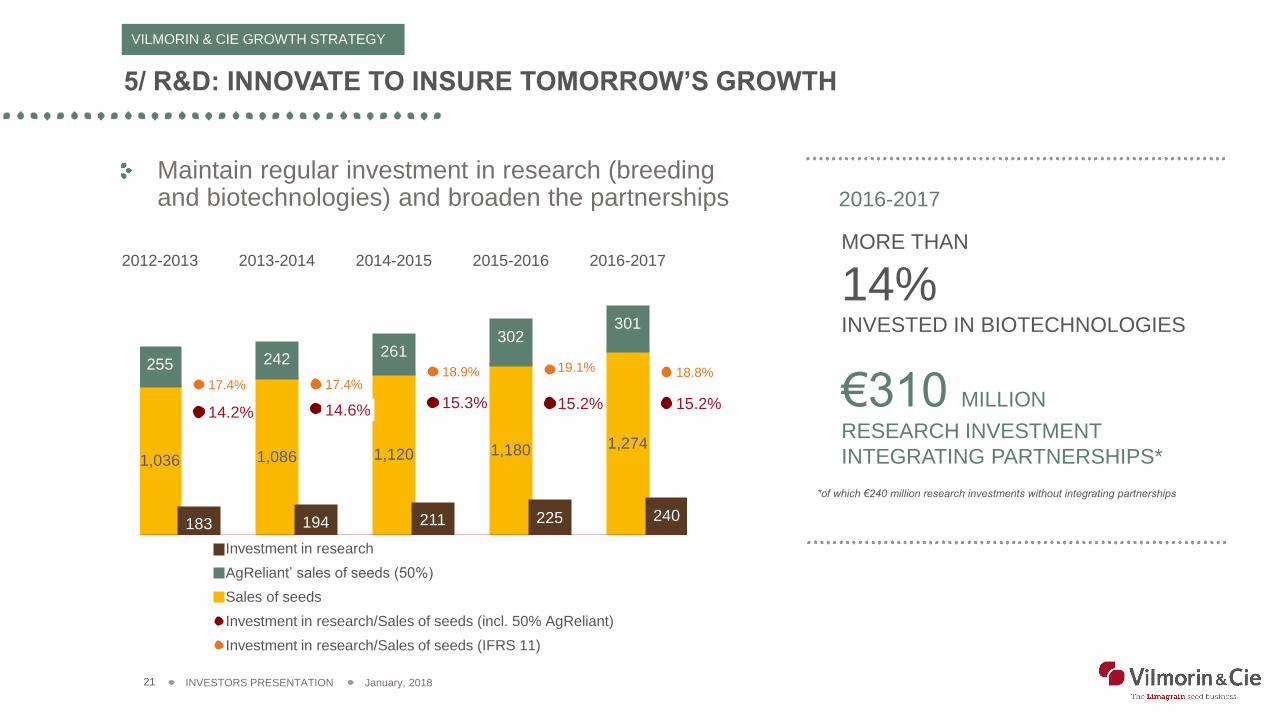

5/ R&D: INNOVATE TO INSURE TOMORROW’S GROWTH

VILMORIN & CIE GROWTH STRATEGY

2016-2017

*of which €240 million research investments without integrating partnerships

€310 MILLION

RESEARCH INVESTMENT

INTEGRATING PARTNERSHIPS*

MORE THAN

14%INVESTED IN BIOTECHNOLOGIES

Maintain regular investment in research (breeding and biotechnologies) and broaden the partnerships

1,036 1,086 1,120 1,180 1,274

255 242261

302301

183 194 211 225 240

14.2% 14.6% 15.3% 15.2% 15.2%

17.4% 17.4%18.9% 19.1% 18.8%

0

200

400

600

800

1 000

1 200

1 400

1 600

1 8002012-2013 2013-2014 2014-2015 2015-2016 2016-2017

Effort de recherche

Chiffre d'affaires semences AgReliant (à 50%)

Chiffre d'affaires semences

Effort de recherche/chiffre d'affaires semences (yc AgReliant 50%)

Effort de recherche/chiffre d'affaires semences (IFRS 11)

Investment in research

AgReliant’ sales of seeds (50%)

Sales of seeds

Investment in research/Sales of seeds (incl. 50% AgReliant)

Investment in research/Sales of seeds (IFRS 11)

January, 2018INVESTORS PRESENTATION22

22

SALES FOR THE 1ST QUARTER 2017-2018 (ON SEPTEMBER 30, 2017)

January, 2018INVESTORS PRESENTATION23

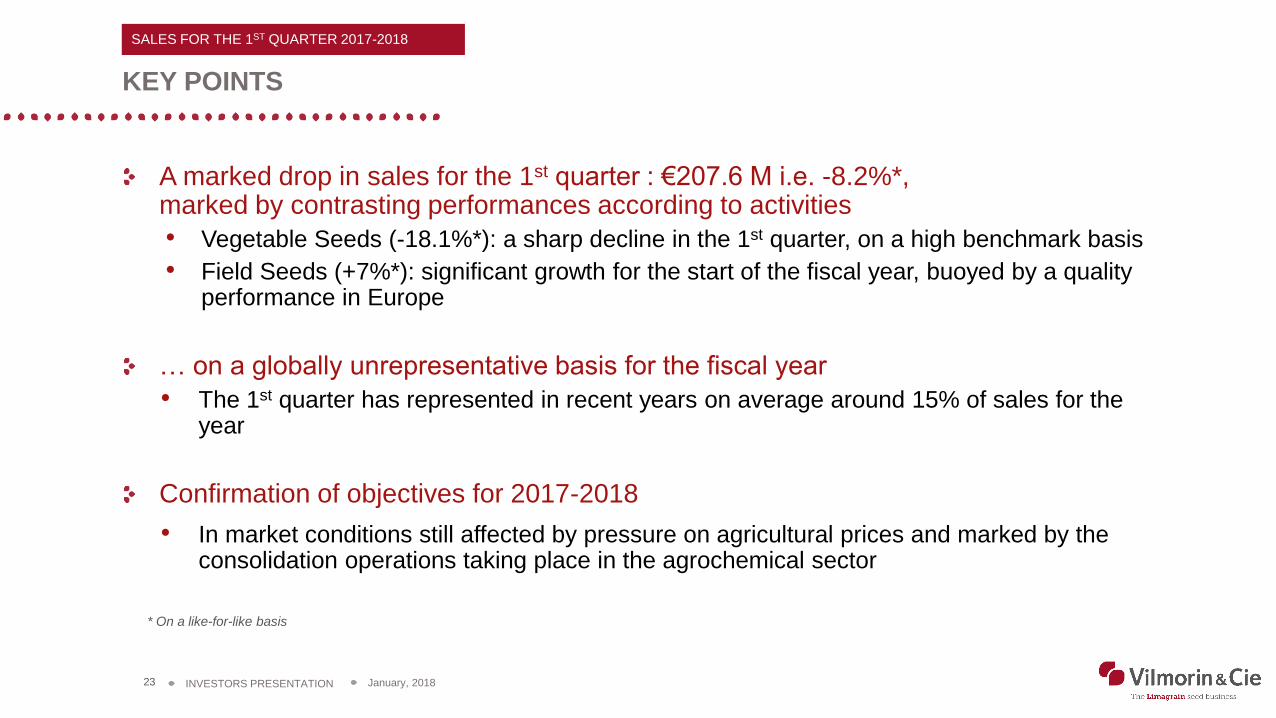

A marked drop in sales for the 1st quarter : €207.6 M i.e. -8.2%*, marked by contrasting performances according to activities

• Vegetable Seeds (-18.1%*): a sharp decline in the 1st quarter, on a high benchmark basis

• Field Seeds (+7%*): significant growth for the start of the fiscal year, buoyed by a quality performance in Europe

… on a globally unrepresentative basis for the fiscal year

• The 1st quarter has represented in recent years on average around 15% of sales for the year

Confirmation of objectives for 2017-2018

• In market conditions still affected by pressure on agricultural prices and marked by the consolidation operations taking place in the agrochemical sector

* On a like-for-like basis

KEY POINTS

SALES FOR THE 1ST QUARTER 2017-2018

January, 2018INVESTORS PRESENTATION24

REFERENCES

SALES FOR THE 1ST QUARTER 2017-2018

2016 2017

$ 1.12 1.17

¥ 114 130

£ 0.85 0.90

TRY 3.31 4.13

ILS 4.25 4.18

BRL 3.62 3.71

INR 75 76

MXN 20.9 20.9

UAH 28.3 30.5

RUB 72.1 69.3

Accounting referenceIFRS on September 30, 2017

Consolidation scopeNo variation

Average rates of the main currencies on September 30, 2017 (and September 30, 2016)

January, 2018INVESTORS PRESENTATION25

CONSOLIDATED SALES*

In M€

53%43%

4%

SALES* FOR THE 1ST QUARTER 2017-2018 PER DIVISION

Vegetable

Seeds

Field

Seeds

Garden Products and

Holdings

SALES FOR THE 1ST QUARTER 2017-2018

* Revenue from ordinary activities

232208

-6 -18

sept.-16 Impactdevises

Activité sept.-17

-10.5%

-8.2%

Currency

impactActivity

January, 2018INVESTORS PRESENTATION26

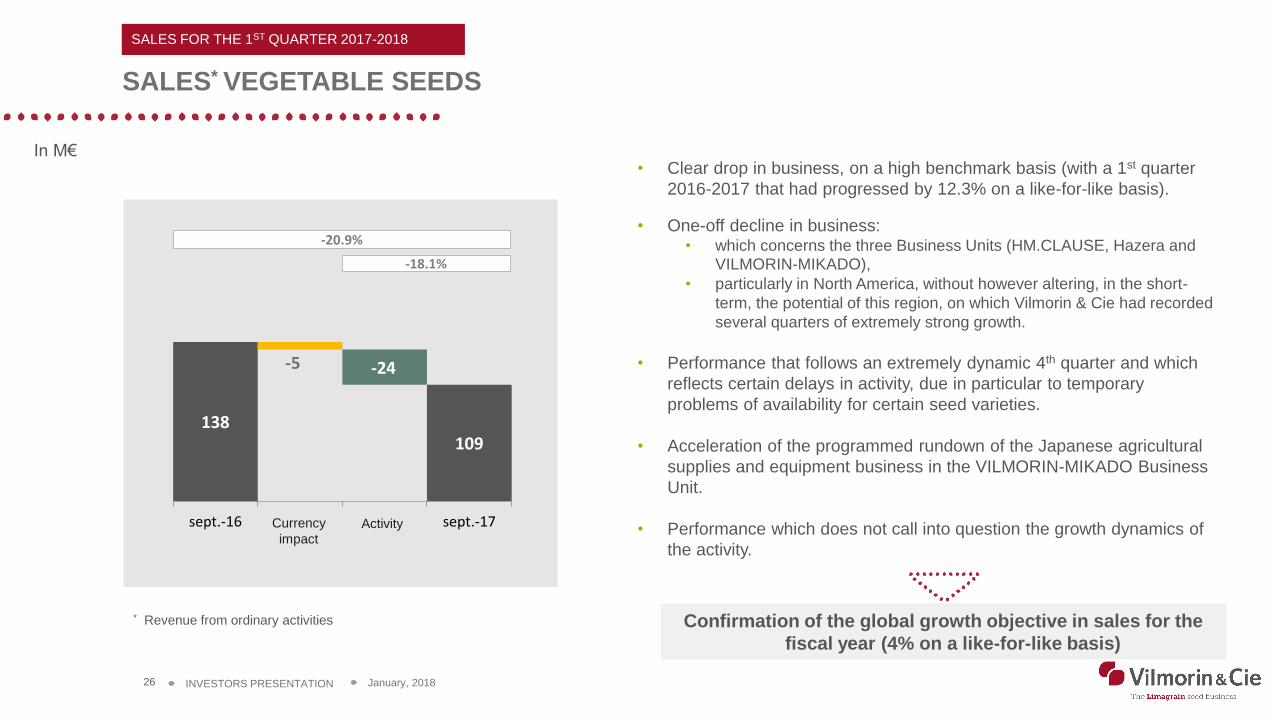

SALES* VEGETABLE SEEDS

In M€

SALES FOR THE 1ST QUARTER 2017-2018

• Clear drop in business, on a high benchmark basis (with a 1st quarter

2016-2017 that had progressed by 12.3% on a like-for-like basis).

• One-off decline in business: • which concerns the three Business Units (HM.CLAUSE, Hazera and

VILMORIN-MIKADO),

• particularly in North America, without however altering, in the short-

term, the potential of this region, on which Vilmorin & Cie had recorded

several quarters of extremely strong growth.

• Performance that follows an extremely dynamic 4th quarter and which

reflects certain delays in activity, due in particular to temporary

problems of availability for certain seed varieties.

• Acceleration of the programmed rundown of the Japanese agricultural

supplies and equipment business in the VILMORIN-MIKADO Business

Unit.

• Performance which does not call into question the growth dynamics of

the activity.

* Revenue from ordinary activities

138109

-5

sept.-16 Impactdevises

Activité sept.-17

-20.9%

-18.1%

-24

Confirmation of the global growth objective in sales for the

fiscal year (4% on a like-for-like basis)

Currency

impactActivity

January, 2018INVESTORS PRESENTATION27

SALES* FIELD SEEDS

In M€

SALES FOR THE 1ST QUARTER 2017-2018

Europe:• Rapeseed: high level of growth (volume and value), particularly in Central Europe,

France and the United Kingdom, leading to significant market shares gains, thanks to a

portfolio of highly efficient products from a technical point of view.

• Straw cereals (wheat, barley): very slight increase in sales, in a market still affected by a

reduction in certified seeds.

• Forage and amenity grass seeds: slight growth in business.

South America:• Increase in sales, particularly for soybean, a relevant complement to the corn offering.

• Drop in sales for the first corn campaign in Brazil (safra), reflecting the current evolution

of cultivated acreage for this crop.

• Promising outlook for orders for the 2nd corn campaign (safrinha), for which acreage

should increase, but with less intensity than during the previous fiscal year.

• Confirmation of the growth objectives fixed for this region.

Asia:• Good start to the fiscal year, with a strong increase in business particularly in India.

Europe and North America:• Procurement of corn seeds is nearly complete, and according to the latest estimates, is

globally in line with production plans objectives.

• Revenue from ordinary activities

after application of IFRS 11 (i.e. excluding AgReliant)

8590

6

-1

sept.-16 Impactdevises

Activité sept.-17

+5.9%

+7.0%

Reaffirmation of the objective to increase sales

for the fiscal year (at least 5% on a like-for-like basis)

Currency

impactActivity

January, 2018INVESTORS PRESENTATION28

CONSOLIDATED SALES* PER GEOGRAPHICAL AREA

Americas

€43 M. -23.6%**

Africa/Middle East €20 M. -16.3% **

Europe

€115 M. +1.4%**

Asia/Oceania

€28 M. -24.0%**

60 %

10 %

* Sales of goods

** Current data compared with 2016-2017

56%

21%

13%

10%

Africa/

Middle East

Americas

Asia/Oceania

Europe

SALES FOR THE 1ST QUARTER 2017-2018

January, 2018INVESTORS PRESENTATION29

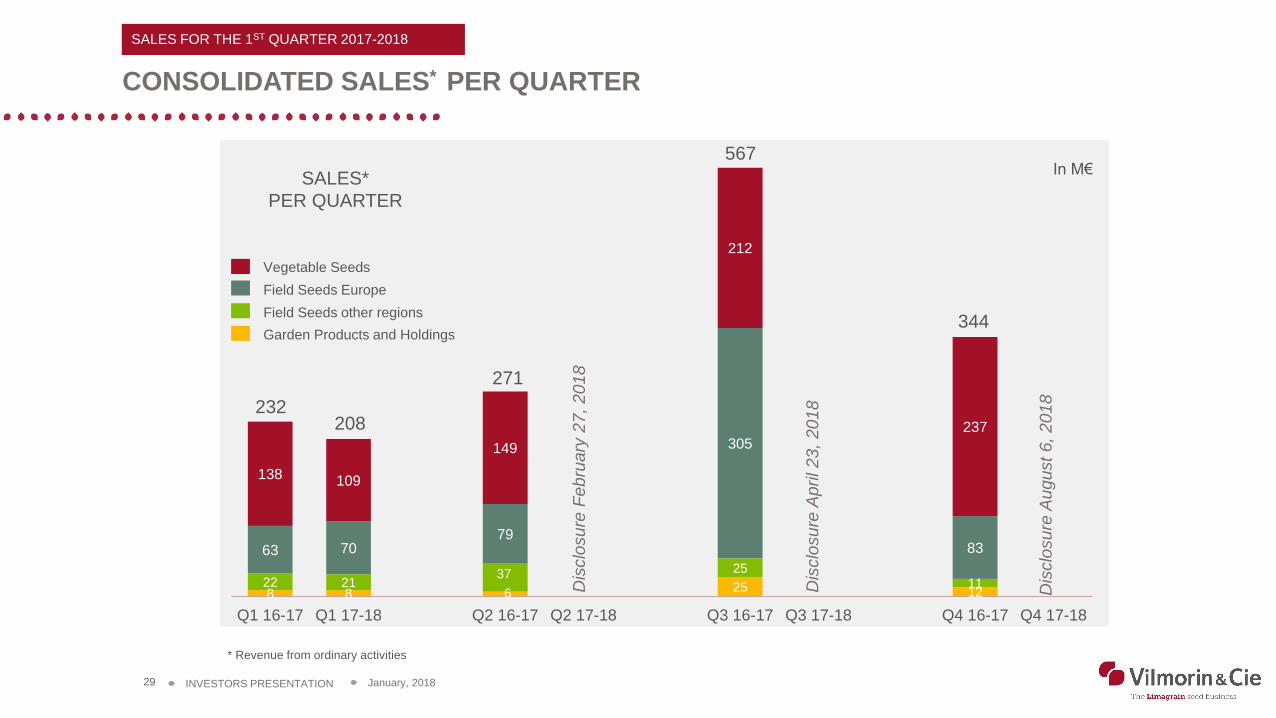

CONSOLIDATED SALES* PER QUARTER

* Revenue from ordinary activities

SALES FOR THE 1ST QUARTER 2017-2018

8 8 6 25 1222 21

37 2511

63 7079

305

83

138 109

149

212

237

Q1 16-17 Q1 17-18 Q2 16-17 Q2 17-18 Q3 16-17 Q3 17-18 Q4 16-17 Q4 17-18

208

In M€

232

271

Vegetable Seeds

Field Seeds Europe

Field Seeds other regions

Garden Products and Holdings

SALES*

PER QUARTER

567

344

Dis

clo

su

re F

eb

rua

ry 2

7,

20

18

Dis

clo

su

re A

pri

l 23,

201

8

Dis

clo

su

re A

ug

ust

6,

20

18

January, 2018INVESTORS PRESENTATION30

OUTLOOK FOR 2017-2018 AND MID-TERM AMBITIONS

January, 2018INVESTORS PRESENTATION31

CONFIRMATION OF OBJECTIVES

OUTLOOK FOR 2017-2018

Vegetable Seeds

Strengthen world leadership:

> By pursuing innovation in plant breeding and close proximity to markets.

> While remaining on the look-out for any external growth opportunity

to consolidate positions for strategic zones and crops.

In Japan, Vilmorin & Cie will pursue its programmed rundown of the agricultural

supplies and equipment activity of the Business Unit VILMORIN-MIKADO.

Objective for 2017-2018

Sales for Vegetable Seeds = +4%on a like-for-like basis

Field Seeds

Strengthen positions in regions where facilities have been established:Objective for 2017-2018

Sales for Field Seeds > +5%on a like-for-like basis

> In market conditions that will probably remain difficult in Europe.

> Pursuing the deployment of the strategic plan for Field Seeds aiming to:

- Become a global player in corn seeds.

- Ultimately become the world reference for wheat seeds.

January, 2018INVESTORS PRESENTATION32

CONFIRMATION OF OBJECTIVES

OUTLOOK FOR 2017-2018

Achieve significant growth in sales and consolidate the current operating margin rate

Aim for a contribution from its associated companies* at least equivalent to that of 2016-2017.

* Mainly AgReliant (North America. Field Seeds), Seed Co (Africa. Field Seeds) and AGT (Australia. Field Seeds).

Consolidated sales +5%

on a like-for-like basis

Current operating margin rate at the

same level as in 2016-2017, taking into

account research investment ≈ €255 M

Pursue deployment of the development and innovation strategy,

in a long-term vision,

over a fiscal year which should continue to be affected

by the pressure on agricultural prices

and will be marked by the consolidation operations in the agrochemical sector.

January, 201833 INVESTORS PRESENTATION

STRATEGIC ORIENTATIONS

MID-TERM AMBITIONS

VEGETABLE SEEDS CORN SEEDS WHEAT SEEDS

ULTIMATELY

BECOME THE

WORLD

REFERENCE

BECOME A

GLOBAL

PLAYER

REINFORCE

WORLD

LEADERSHIP

• Accelerate development to reach business growth higher than market trends and increase

operating margins, both in Vegetable Seeds and Field Seeds

• Materialize the three strategic priorities:

Confirmation of the strategic ambitions for 2020

Fiscal year 2016-2017 fully confirmed these ambitions

Objectives for 2017-2018 firmly in line with these trends

January, 2018INVESTORS PRESENTATION34

VILMORIN & CIEON THE STOCK EXCHANGE

January, 2018INVESTORS PRESENTATION35

(Source: Euronext.com)

€89.70SHARE PRICE

ON JANUARY 5TH, 2018

VILMORIN & CIE ON THE STOCK EXCHANGE

EVOLUTION OF THE SHARE PRICE

Vilmorin & Cie :

Vilmorin & Cie

CAC 40

MARKET CAPITALIZATION

ON JANUARY 5TH, 2018

€1.9 BN.

+ 27.3% 10 years + 26.5% 5 years + 52.3% 1 year

January, 2018INVESTORS PRESENTATION36

VILMORIN & CIE ON THE STOCK EXCHANGE

DIVIDENDS (1)

* Capital gain from the disposal of a minority stake in China.

(1) Data not restated for the allotment of free shares of January 2013 and January 2015.

28.4%Pay-out 35.3% 31.4% 37.2% 44.8% 38.6%

4.37

3.87

4.77

4.04

3.50

2.85

4.17

1.24 1.36 1.50 1.50 1.571.10

1.60

2011 2012 2013 2014 2015 2016 2017

Profit (group share) per share Dividend

1.40*

38.4%

Proposal

January, 2018INVESTORS PRESENTATION37

SCHEDULE AND CONTACTS

January, 2018INVESTORS PRESENTATION38

TUESDAY FEBRUARY 27, 2018

Disclosure of the sales and results for the 1st semester 2017-2018

MONDAY APRIL 23, 2018

Disclosure of the sales for the 3rd quarter 2017-2018

MONDAY AUGUST 6, 2018

Disclosure of the sales at the end for fiscal year 2017-2018

WEDNESDAY OCTOBER 17, 2018

Disclosure of the annual results for fiscal year 2017-2018

SCHEDULE

January, 2018INVESTORS PRESENTATION39

FOR ANY FURTHER INFORMATION:

CONTACTS

Valérie MONSERAT

All our financial information on

www.vilmorincie.com

Vilmorin & Cie

Head Office: 4 quai de la Mégisserie – F-75001 PARIS

Postal address: CS 20001 Saint-Beauzire – F-63360 GERZAT

Tel: +33 (0)473 634 485

Vincent SUPIOT

January, 2018INVESTORS PRESENTATION40

APPENDICESKey financial data for fiscal year 2016-2017Organization chart

January, 2018INVESTORS PRESENTATION41

APPENDICESKey financial data for fiscal year 2016-2017

January, 2018INVESTORS PRESENTATION42

INCOME STATEMENT

In M€ 2015-2016 2016-2017 Variation

Sales 1 325.1 1 414.0 +6.7%

Sales margin 632.2 687.0 +€54.8 M

Sales margin rate 47.7% 48.6% +0.9 pt

Operating income 100.3 118.3 +€18.0 M

Operating margin rate 7.6% 8.4% +0.8 pt

Current operating margin rate 8.4% 9.2% +0.8 pt

Income from associated companies 30.8 33.9 +€3.1 M

Financial income -36.5 -24.5 -(€12.0) M

Income taxes -33.8 -37.6 +(€3.8) M

Net income 60.8 90.1 +€29.3 M

Net income Group share 59.3 86.9 +€27.6 M

RESULTS FOR FISCAL YEAR 2016-2017

January, 2018INVESTORS PRESENTATION43

KEY FIGURES FOR EACH ACTIVITY’S CONTRIBUTION TO CONSOLIDATED SALES

* Revenue from ordinary activities

Sales* Operating income Net income

In M€ 2015-2016 2016-2017 2015-2016 2016-2017 2015-2016 2016-2017

Vegetable Seeds 688.7 735.8 109.3 125.8 71.6 84.9

Field Seeds 581.7 626.0 10.6 17.2 17.3 31.9

Garden Products 53.6 51.2 -4.6 -6.7 -4.6 -6.9

Holdings 1.1 1.0 -15.0 -18.0 -23.5 -19.8

Consolidated 1 325.1 1 414.0 100.3 118.3 60.8 90.1

RESULTS FOR FISCAL YEAR 2016-2017

January, 2018INVESTORS PRESENTATION44

FREE CASH-FLOW

In M€ 2015-2016 2016-2017

Net indebtedness at the beginning of the FY 660 742

EBITDA 278 316

Variation of working capital needs 20 -43

Other operating items -28 -12

Net industrial investments -46 -38

Activated development costs -157 -165

Operating cash-flow 68 57

Net financial investments -116 -5

Capital and other equity contributions -1 -

Dividends -10 -4

Net financial charges -23 -23

Free cash-flow -83 25

Other restatements (IFRS/Currency, etc.) 1 3

Net indebtedness at the end of the FY 742 714

RESULTS FOR FISCAL YEAR 2016-2017

January, 2018INVESTORS PRESENTATION45

BALANCE SHEET STRUCTURE

Total balance sheet 2 159 2 179

of which cash 207 256

In M€

Gearing 55%

Leverage 2.3

742 714

64 7689 80

1 264 1 309

June 2016 June 2017

Equity

Provisions

Net deferred taxes

Net indebtedness

468 492

1 691 1 687

Net fixed assets

Net working capitalneeds

RESULTS FOR FISCAL YEAR 2016-2017

January, 2018INVESTORS PRESENTATION46

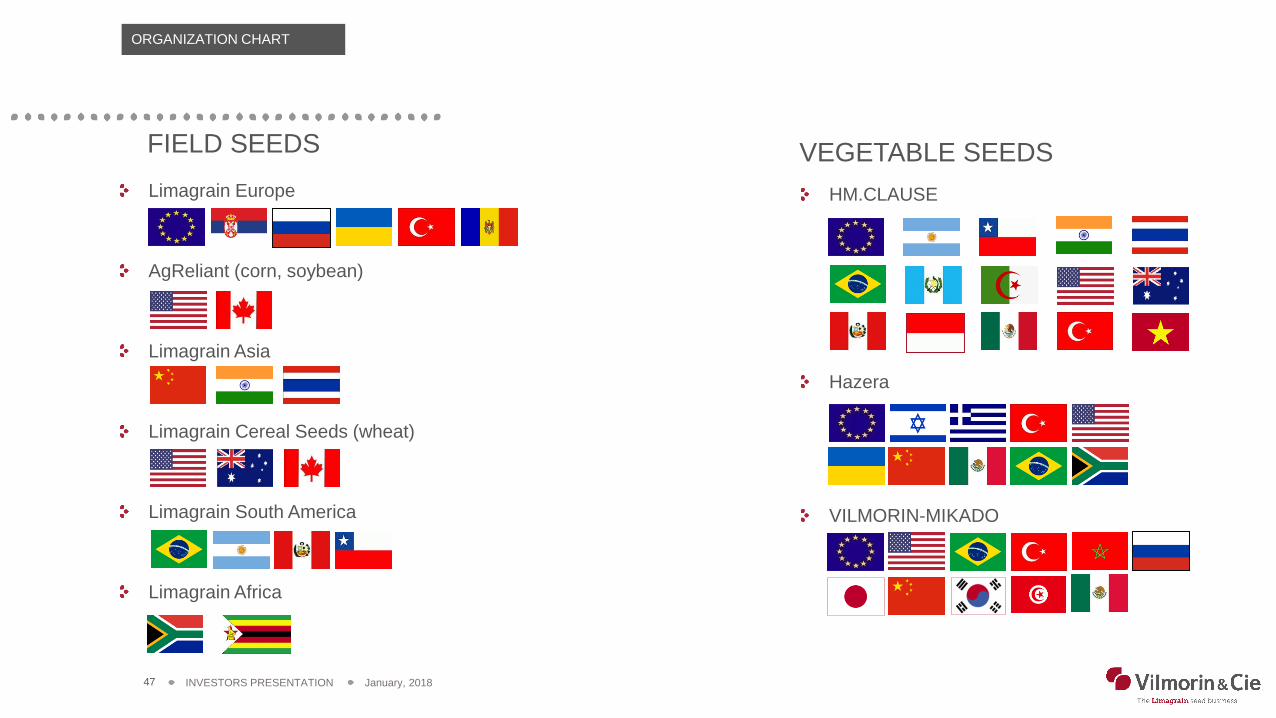

APPENDICESVILMORIN & CIE ORGANIZATION CHART

January, 2018INVESTORS PRESENTATION47

FIELD SEEDS

Limagrain Europe

AgReliant (corn, soybean)

Limagrain Asia

Limagrain Cereal Seeds (wheat)

Limagrain South America

Limagrain Africa

ORGANIZATION CHART

VEGETABLE SEEDS

HM.CLAUSE

Hazera

VILMORIN-MIKADO

January, 2018INVESTORS PRESENTATION48

THANK YOUVILMORIN & CIE

Head office: 4 quai de la Mégisserie – F-75001 PARIS

Postal address: CS 20001 Saint-Beauzire – F-63360 GERZAT

Tel: +33 473 634 485

www.vilmorincie.com