IT & ITeS SECTOR PROFILE

IT & ITeS : Global Scenario

IT & ITeS : Indian Scenario

IT & ITeS : Tamil Nadu Scenario

Investment Opportunities

Government Support

CONTENTS

0

200

400

600

800

1000

1200

1400

BPO PackagedSoftware

Hardware IT services ER&D

153 309

645 605

1125

168

392

996

655

1400

2010 2013

IT, BPM services and software products accounted for more than half the share in Global IT spending, contributing over USD 1.2 trillion which is about 54 per cent of the total IT spend.

IT hardware with growth rate of ~7 percent touched USD 996 billion and accounted for the remaining 46 per cent.

North America (USA and Canada) and Europe have been the fore runners with around 80% Global IT spending coming from them. Asia Pacific region lags behind with only 16% contribution, while others like Latin America, Middle East & Africa are still developing as far as technology is concerned.

46%

34%

16%

2% 1% 1%

North America

Europe

Asia Pacific

Latin America

Middle East

Africa

Global IT Spending (USD Billion)

IT & ITeS Industry: Global Scenario

24 32 32 32 75 50

70 76 86

225

74 102 108 118

300

2009-10 2011-12 2012-13 2013-14 2020-21

Domestic Exports

4X

Indian IT & ITes Revenues earned in USD Billion

Top Company Name % Market share

TCS 10.7%

Wipro 7.2%

Cognizant 6.8%

Infosys 6.3%

HCL Tech 4.2%

Tech Mahindra 1.1%

Total 36%

Indian IT-ITeS industry has shown a consistent growth in past 5 years following a CAGR of 13%. The growth is mainly driven by exports and it contributes to more than 70% of the total revenue earned by the industry. The IT & ITeS sector contribution to Country’s GDP increased from a meagre 1.2% in 1998 to 8.1% in 2013. The industry is poised to reach USD 300 Billion by 2020.

Diverse Suppliers base >15,000 Firms (% Share in

Revenues)

11 Large Players (>40%)

Mid-sized 120-150 players (~35-40%)

Emerging Players ~1000-1200 (~10%)

Small-Sized ~15,000 Players

(~10%)

The supplier’s landscape for the IT-ITeS sector is largely dominated by big players contributing to more than 40% of the revenue share

IT & ITeS Industry: Indian Scenario India has emerged as one of the most important destination for providing world class technology and business services.

31.50%

15.50%

15%

13%

12.50%

6.60%

1.50% 1.50% 1.50% 1.40% Manufacturing

Energy

Government

BFSI

Consumers

Telecom

Retail

Education

Healthcare

Others

38%

9% 13%

36%

IT

ITes/BPO

SoftwareProducts& Engg Services

Hardware

Domestic Market distribution by Business Verticals

Breakup of Domestic Market by Service Lines (2013-14)

The Domestic market is slated to reach USD 75 Billion by 2020. This is will require a CAGR of 15% over the next 6 years.

IT service sector is mainly focused into technology upgrades in BFSI, telecom and State governments, and compliance MIS investments.

The Hardware industry driven by storage and mobile computing devices is the 2nd highest contributor to the domestic market and is targeted to grow further.

Software products generally include vertical specific and SMAC- based solutions.

The advent of Cloud computing will be the next big opportunity for the IT sector specially the SMB’s

50 70 76 86

225

2009-10 2011-12 2012-13 2013-14 2020-21

~5X

Indian IT & ITeS export Revenues Earned in USD Bn

60% 23%

16% 0.5%

IT ITeS/BPO Software Products… Hardware

Breakup of Export Revenues by Service Lines (2013-14)

Exports contribute to more than 70% of the total revenue generated by the sector.

IT services is expected to be the fastest growing segment in the future, currently generating exports of USD 52 billion (60% share in revenues) driven by collaboration, communication, business intelligence projects, and integration of SMAC services with traditional offerings.

With over 3,000 firms, India is emerging as a favorite destination for software products with SMAC.

The global sourcing market grew by USD 11-12 billion in which India accounted for over 90 per cent of the incremental growth.

India’s IT Exports rose at a CAGR of 13%in last 5 years despite the Global economic slowdown.

1114

1780

2004-05 2012-13

The Service Sector has been contributing to>60% of the State’s GSDP since past decade.

According to Software Technology Parks of India(STPI), Chennai, the number of registered software units in Tamil Nadu has increased from 1114 in 2004-05 to 1780 in 2012-13 providing employment to more than 3.75 lakh professionals.

No. of IT Units in Tamil Nadu

IT & ITeS Industry: Tamil Nadu Scenario IT & ITeS industry is the major contributor to the Service sector in the State.

The presence of major IT giants reiterates the fact that it is one of the most preferred destination in India.

14.31%

11.36%

10.80%

8.51%

5.71%

49.31%

Construction andInfrastructureDevelopmentAutomobile Industry

Computer Software &Hardware

Services Sector

Drugs &Pharmaceuticals

Others

Cumulative FDI distribution in Tamil Nadu

The total cumulative FDI inflow in Tamil Nadu for the period 2000-2014 has

been USD 16Billion.

Tamil Nadu State ranks 3rd in IT-ITeS sector investment, accounting for around

~11% of the total.

LP Cube Systems Pvt. Ltd, Singapore is the top investor accounting for more

than 57% of the total FDI received in IT & ITeS Sector in Tamil Nadu.

World Bank

Standard Chartered

41%

1% 6% 9% 7%

1%

1% 1%

2%

1%

30%

Application Software

Engineering Software

BPO

Product Development

System Software

Medical Transcription

Call Centre

E-Publishing

Data Entry

Onsite Consultancy

Others

Tamil Nadu accounts for more than 10% of the total IT exports carried out from India. Software services are the highest contributor to the exports accounting for more than 40%.

Tamil Nadu is the 4th largest software exporter in India

8870

11350 12380

2011-12 2012-13 2013-14

US

D M

illi

on

Export of Computer Software & Elec. Goods from Tamil Nadu in USD million

CAGR 18%

Location of IT SEZs

& IT Parks in Tamil

Nadu

There are 28 operational SEZs for IT-ITeS in the State. Around 234 IT Parks are in the Pipeline with a built-up space of 131 million sq. feet in Tamil Nadu

22 approved IT parks & around 234 in pipeline

Full fledged wide area network and data

centre (largest bandwidth in India –

14.8 Tbps)

Presence of all major Service providers Fibre

Network

TIDEL Park, with a total area of 1.28 million sq. ft is the largest in India

Over 1780 IT software units in the State

Land identified for setting up International Institute of Information

Technology (IIIT)

Presence of STPI multi Fiber backbone and

state of art infrastructure facility for the IT industries

28 operational Special Economic Zones in State

The State Government is establishing an IT Investment Region

near Chennai covering an area of 1600 sq. km with a total

investment of USD 1.7 billion. Land acquisition has been initiated.

Opportunities in the IT & ITeS Sector in Tamil Nadu

ICTACT has forged new partnerships and signed Memoranda of Understanding with leading ICT Companies NVIDIA and IBM, as part of its objectives

Conferences (ICTACT Bridge) in 6 cities and conducted 47 Technical Seminars (ICTACT Power Seminars) for students across the State of Tamil Nadu

Conducted 6 Industry-Institute Interaction

Published 87 research articles

Assessed and certified 23,000 students on Basic Computer Course

Conducted 70 Faculty Development Programmes

Trained 1650 Higher education Faculty from 572 Institutes

1634596

250000

3384

572

0

1000

2000

3000

4000

0

500000

1000000

1500000

2000000

India Tamil Nadu

Total Intake Total No of colleges

Total intake of students in engineering and technical colleges

The annual intake of 572 Engineering institutes at under graduate level is 2.5 lakh students.

Out of this total around 90,000 students specialize in IT, Computer Science & electronics telecommunication.

Tamil Nadu offers the largest pool of technically qualified professionals in India

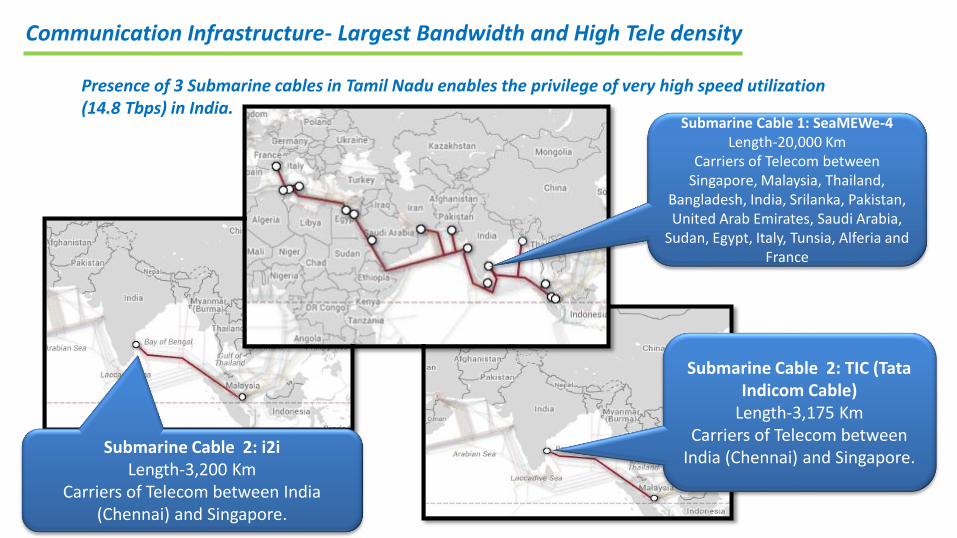

Submarine Cable 1: SeaMEWe-4 Length-20,000 Km

Carriers of Telecom between Singapore, Malaysia, Thailand,

Bangladesh, India, Srilanka, Pakistan, United Arab Emirates, Saudi Arabia,

Sudan, Egypt, Italy, Tunsia, Alferia and France

Submarine Cable 2: TIC (Tata Indicom Cable)

Length-3,175 Km Carriers of Telecom between

India (Chennai) and Singapore. Submarine Cable 2: i2i

Length-3,200 Km Carriers of Telecom between India

(Chennai) and Singapore.

Presence of 3 Submarine cables in Tamil Nadu enables the privilege of very high speed utilization (14.8 Tbps) in India.

Communication Infrastructure- Largest Bandwidth and High Tele density

Cloud based services and

solutions

Hardware manufacturing

Urban and rural planning - using

GIS, remote sensing

Knowledge process outsourcing

Data/computer centers

E-Governance initiatives

IT based education and trainings

Investment opportunities in Tamil Nadu

• Capital subsidy of 20% on Capital Investments subject to employment of atleast 50 trained people in that unit

• Training subsidy of INR 1500 per person per month

• Transport facility for the BPO

• Exemption from payment of SD/EMD and cost of tender

Rural BPO Policy 2012

• Structured package of incentives for IT /ITes facilities being set up/expanded in Chennai, Tiruvallur, Kancheepuram with a minimum investment of INR 250 crores (INR 150 crores for other Districts) in a span of 3 years.

• Special Incentives for facilities in TIER II & III Locations: Backended Capital subsidy and Electricity Tax exemptions based on investment pattern and measure.

• Relaxation Of FSI: Upto 100% FSI Relaxation for IT-ITes Parks

• Exemptions in Stamp Duty and registration fee

• Reduction in Power tariffs

• Administrative Incentives

• Physical Incentives

• Single Window Clearance Mechanism

• Others like Data Security policy, augmenting Civic Infrastructure, etc.

ICT Policy 2008

Government Support

Additional Chief Secretary - Government of Tamil Nadu Industries Department

Phone: 91-44-25671383 Fax: 91-44-25670822 Email: [email protected], [email protected]

Nodal agency

Tamil Nadu Industrial Guidance and Export Promotion Bureau

19-A, Rukmini Lakshmipathy Road, Egmore, Chennai-600 008

Phone: 91-44-2855 3118

Email: [email protected]

Visit us at www.tamilnadugim.com