J. M. COLLINS* , C. K . REID^* C E N T E R F O R F I N A N C I A L S E C U R I T Y, U N I V E R S I T Y

O F W I S C O N S I N - M A D I S O N^ F E D E R A L R E S E RV E B A N K O F S A N F R A N C I S C O

Who Receives a Mortgage Modification? Race and Income Differentials in Loan Workouts

West Coast Poverty Center Seminar January 24, 2011

Overview

Homeownership boom and bustRemedies for Borrowers in DistressPolicy Response: HAMPConcerns about Financial Literacy, Racial &

Income DisparitiesDataFindingsFuture ResearchA bit of a commercial…

Boom and Bust

Janu

ary 19

87

Janu

ary 19

88

Janu

ary 19

89

Janu

ary 19

90

Janu

ary 19

91

Janu

ary 19

92

Janu

ary 19

93

Janu

ary 19

94

Janu

ary 19

95

Janu

ary 19

96

Janu

ary 19

97

Janu

ary 19

98

Janu

ary 19

99

Janu

ary 20

00

Janu

ary 20

01

Janu

ary 20

02

Janu

ary 20

03

Janu

ary 20

04

Janu

ary 20

05

Janu

ary 20

06

Janu

ary 20

07

Janu

ary 20

08

Janu

ary 20

09

Janu

ary 20

100.00

50.00

100.00

150.00

200.00

250.00

National Housing PricesThrough July 2010

National 10 City Composite

National 20 City Composite

Seaso

nall

y A

dju

sted

Case

-Shil

ler

Data

Source: Case-Shiller Index

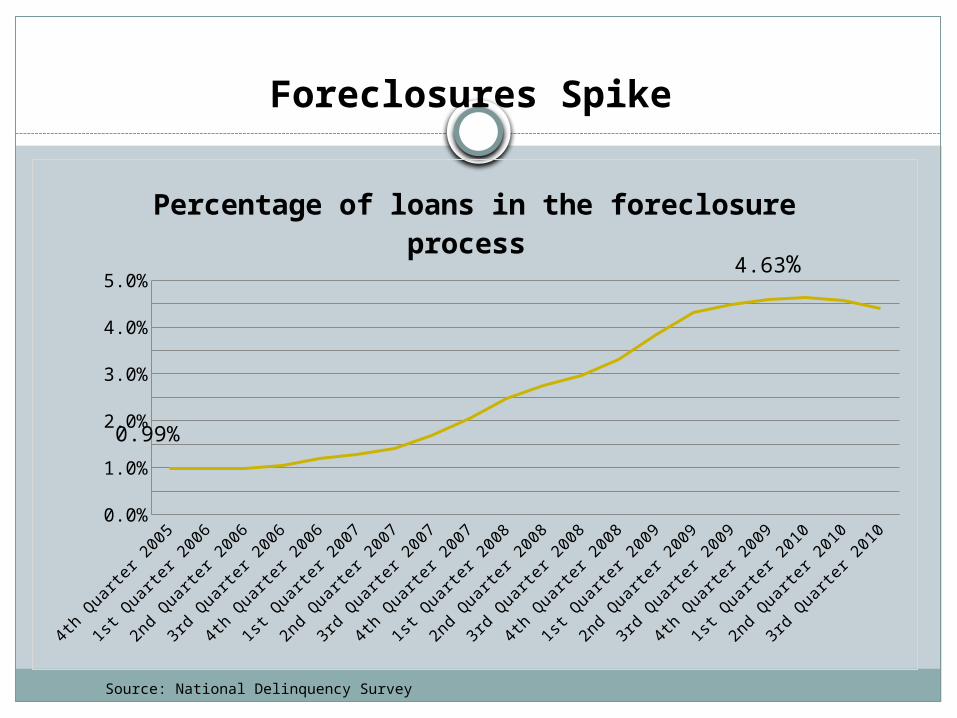

Foreclosures Spike

Source: National Delinquency Survey

4th

Quarter

200

5

1st Q

uarter

200

6

2nd

Quarter

200

6

3rd

Quarter

200

6

4th

Quarter

200

6

1st Q

uarter

200

7

2nd

Quarter

200

7

3rd

Quarter

200

7

4th

Quarter

200

7

1st Q

uarter

200

8

2nd

Quarter

200

8

3rd

Quarter

200

8

4th

Quarter

200

8

1st Q

uarter

200

9

2nd

Quarter

200

9

3rd

Quarter

200

9

4th

Quarter

200

9

1st Q

uarter

201

0

2nd

Quarter

201

0

3rd

Quarter

201

00.0%0.5%1.0%1.5%2.0%2.5%3.0%3.5%4.0%4.5%5.0%

0.99%

4.63%

Percentage of loans in the foreclosure process

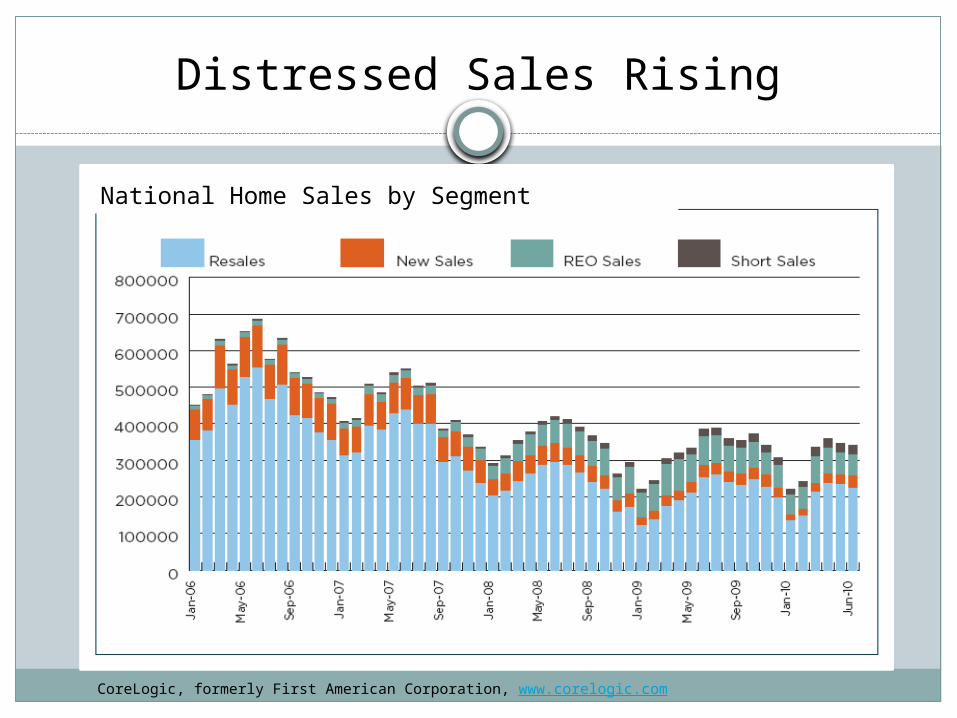

Distressed Sales Rising

National Home Sales by Segment

CoreLogic, formerly First American Corporation, www.corelogic.com

Remedies

Counseling: 888-HOPE & NFMC Program In 2009, received 1.89 million calls and counseled more

than 430,000 distressed homeowners Averages 135,000 calls per month and 5,500 calls per

day Mediation (conciliation)

Out of court meeting with a neutral third party appointed by the court in an attempt to resolve a dispute.

21 states have some form of foreclosure mediation Loan modifications: permanently alter original loan

contract Lower interest rates, Extending loan term, and/or Reducing principal balance owed.

Federal Modification Initiative: HAMP

• Home Affordable Mortgage Program - Federal subsidy

Goal: More lender/servicer modifications Emphasis on ‘waterfall’

Capitalization of arrearages (past payments and fees) Move from ARM to FRM (frozen or reset mod) Reduction in the interest rate (time limited) Reduce principal (very rare)

Goal: bringing monthly payments to 31% of their income

Example

HAMP Goal: 3 Million Loans

3rd Q 2009 4th Q 2009 1st Q 2010 2nd Q 2010 3rd Q 2010Other Modifications 130,464 102,820 129,572 159,073 175,063 HAMP Modifications 783 21,878 100,301 108,257 58,790 Other Trial-Period Plans 127,902 95,250 87,143 88,919 70,264 HAMP Trial-Period Plans 272,709 258,905 184,171 65,484 43,739 Payment Plans 163,551 121,722 120,439 145,157 122,465 Total 695,409 600,575 621,626 566,890 470,321

Source: Office of the Comptroller of the Currency and the Office of Thrift Supervision Mortgage Metrics Report, Third Quarter 2010

Slow to implementMany iterations: much confusionLong delays and overall volume trails projections

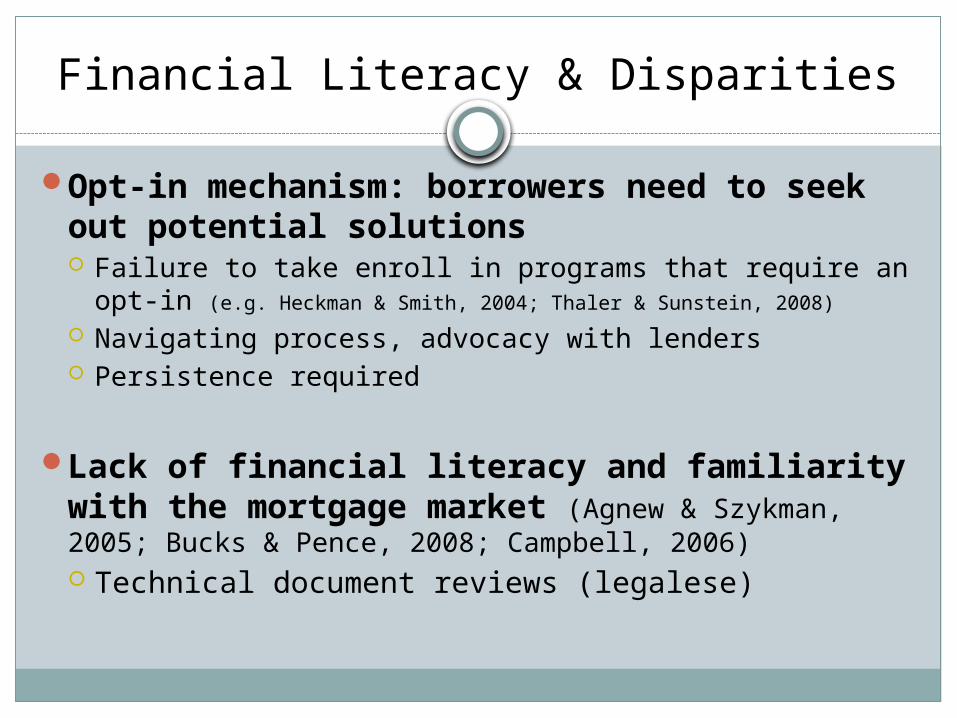

Financial Literacy & Disparities

Opt-in mechanism: borrowers need to seek out potential solutions Failure to take enroll in programs that require an opt-

in (e.g. Heckman & Smith, 2004; Thaler & Sunstein, 2008)

Navigating process, advocacy with lenders Persistence required

Lack of financial literacy and familiarity with the mortgage market (Agnew & Szykman, 2005; Bucks & Pence, 2008; Campbell, 2006) Technical document reviews (legalese)

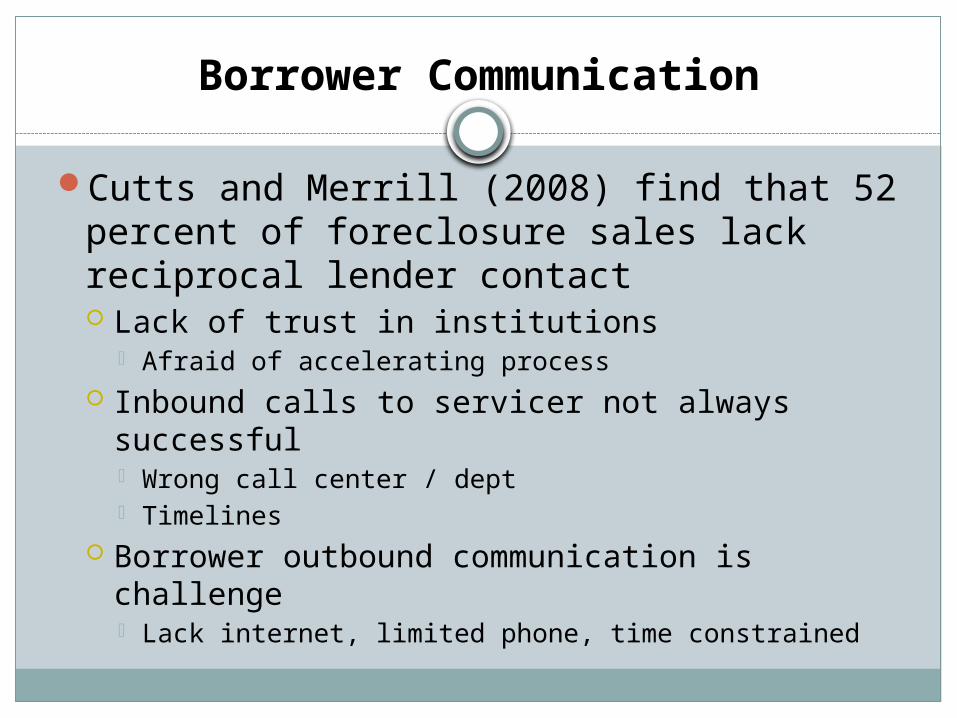

Borrower Communication

Cutts and Merrill (2008) find that 52 percent of foreclosure sales lack reciprocal lender contact Lack of trust in institutions

Afraid of accelerating process Inbound calls to servicer not always successful

Wrong call center / dept Timelines

Borrower outbound communication is challenge Lack internet, limited phone, time constrained

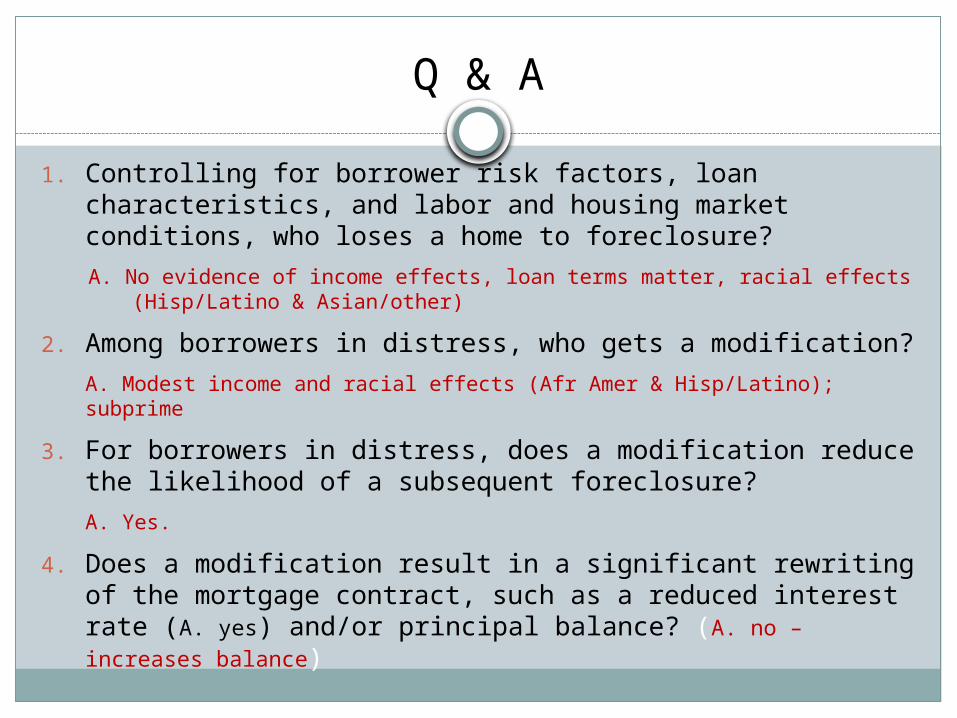

Research Questions

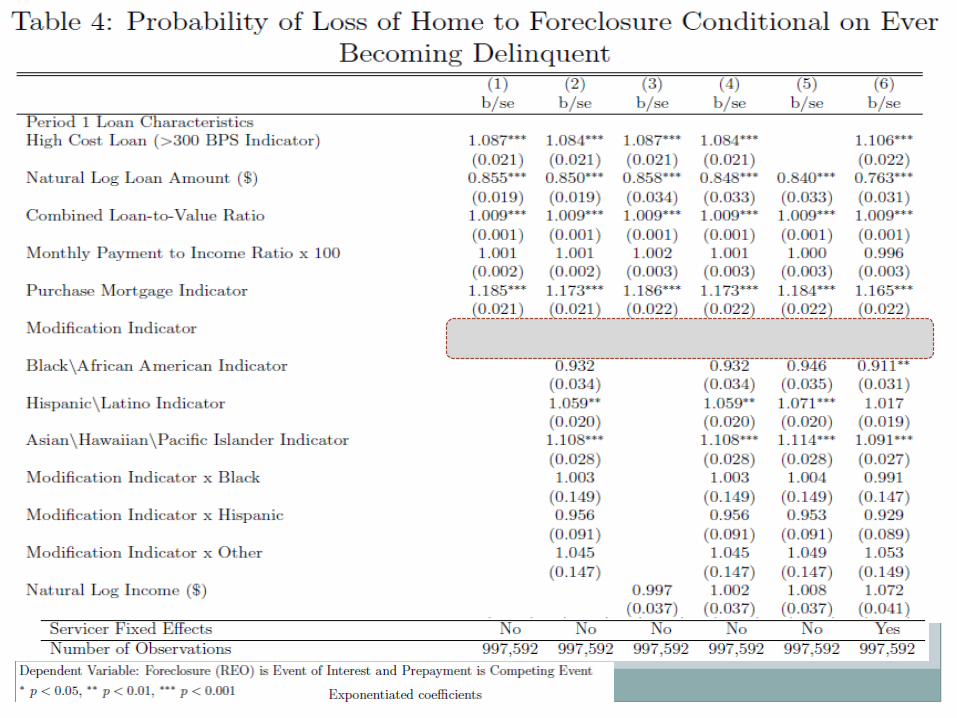

1. Controlling for borrower risk factors, loan characteristics, and labor and housing market conditions, who loses a home to foreclosure?

2. Among borrowers in distress, who gets a modification?

3. For borrowers in distress, does a modification reduce the likelihood of a subsequent foreclosure?

4. Does a modification result in a significant rewriting of the mortgage contract, such as a reduced interest rate and/or principal balance?

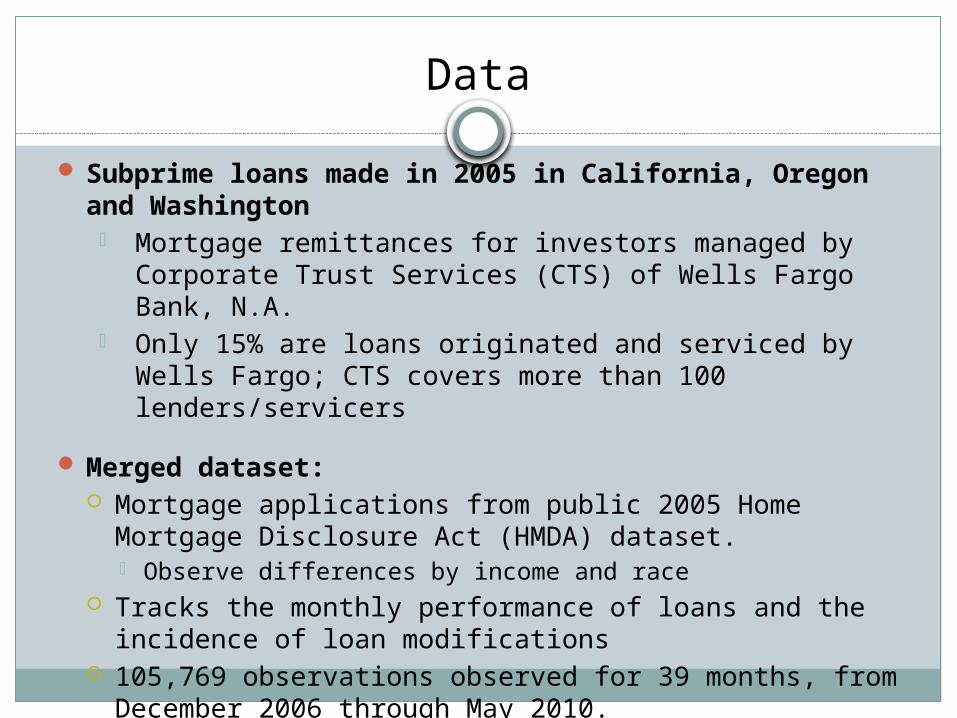

Data

Subprime loans made in 2005 in California, Oregon and Washington Mortgage remittances for investors managed by

Corporate Trust Services (CTS) of Wells Fargo Bank, N.A.

Only 15% are loans originated and serviced by Wells Fargo; CTS covers more than 100 lenders/servicers

Merged dataset: Mortgage applications from public 2005 Home Mortgage

Disclosure Act (HMDA) dataset. Observe differences by income and race

Tracks the monthly performance of loans and the incidence of loan modifications

105,769 observations observed for 39 months, from December 2006 through May 2010.

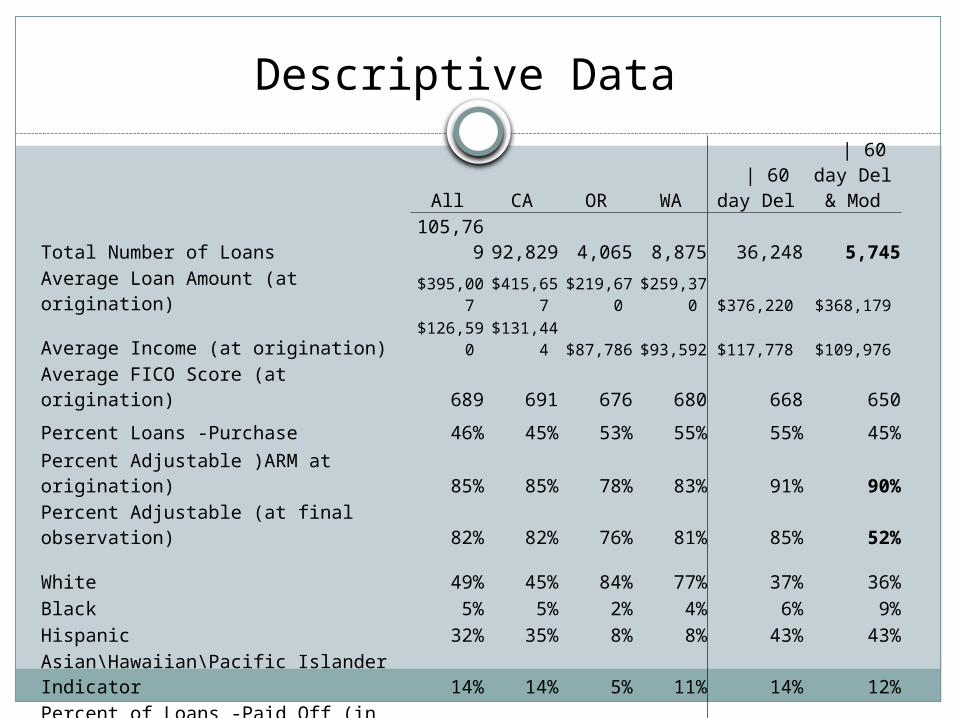

Descriptive Data

All CA OR WA | 60 day

Del | 60 day

Del & Mod

Total Number of Loans 105,769 92,829 4,065 8,875 36,248 5,745

Average Loan Amount (at origination) $395,007 $415,657 $219,670 $259,370 $376,220 $368,179

Average Income (at origination) $126,590 $131,444 $87,786 $93,592 $117,778 $109,976

Average FICO Score (at origination) 689 691 676 680 668 650

Percent Loans -Purchase 46% 45% 53% 55% 55% 45%

Percent Adjustable )ARM at origination) 85% 85% 78% 83% 91% 90%Percent Adjustable (at final observation) 82% 82% 76% 81% 85% 52%

White 49% 45% 84% 77% 37% 36%Black 5% 5% 2% 4% 6% 9%Hispanic 32% 35% 8% 8% 43% 43%

Asian\Hawaiian\Pacific Islander Indicator 14% 14% 5% 11% 14% 12%

Percent of Loans -Paid Off (in final observation) 40% 38% 57% 59% 14% 6%

Percent of Loans -REO (in final observation) 15% 17% 4% 3% 45% 11%

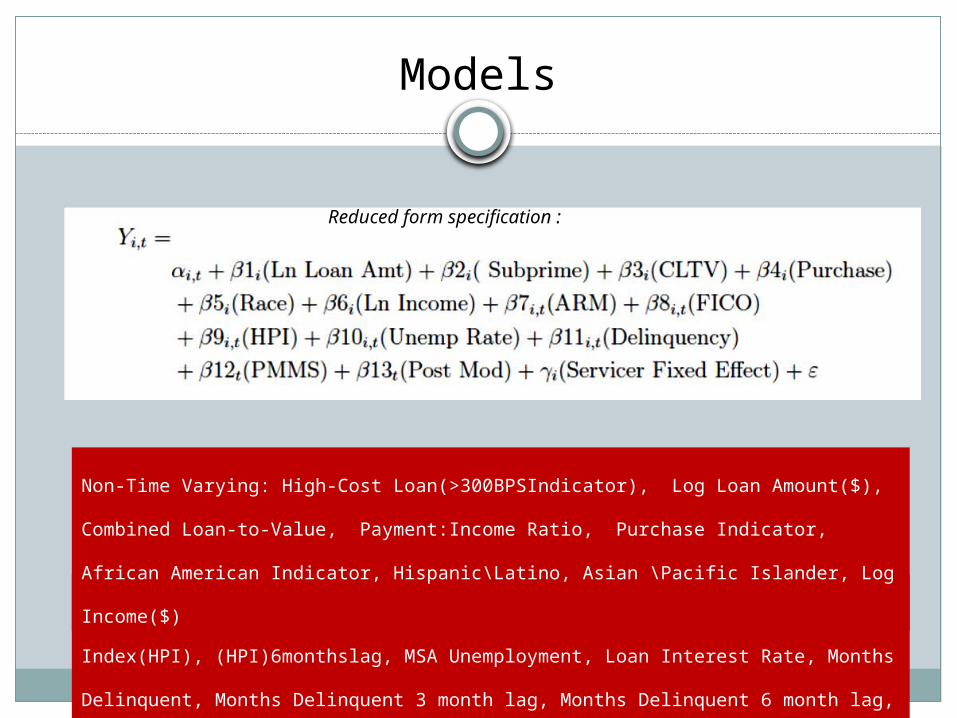

Models

1. Who loses a home to foreclosure? • competing risks (pre-pay, cure, reo)

2. Who gets a modification? • Restricted to those loans being 60+ days delinquent• survival analysis

3. Does a modification reduce the likelihood of a subsequent foreclosure? • Restricted to 60+ days delinquent• competing risks

4. Does a modification result in a significant rewriting of the mortgage contract? • Difference in difference

Models

Reduced form specification :

Time Varying controls: ARM Indicator, FICO, FICO2, Housing Price Index(HPI),

(HPI)6monthslag, MSA Unemployment, Loan Interest Rate, Months Delinquent,

Months Delinquent 3 month lag, Months Delinquent 6 month lag, PMMS

Non-Time Varying: High-Cost Loan(>300BPSIndicator), Log Loan Amount($),

Combined Loan-to-Value, Payment:Income Ratio, Purchase Indicator, African

American Indicator, Hispanic\Latino, Asian \Pacific Islander, Log Income($)

Terms of Modifications: Rate Drops

Growing Balance

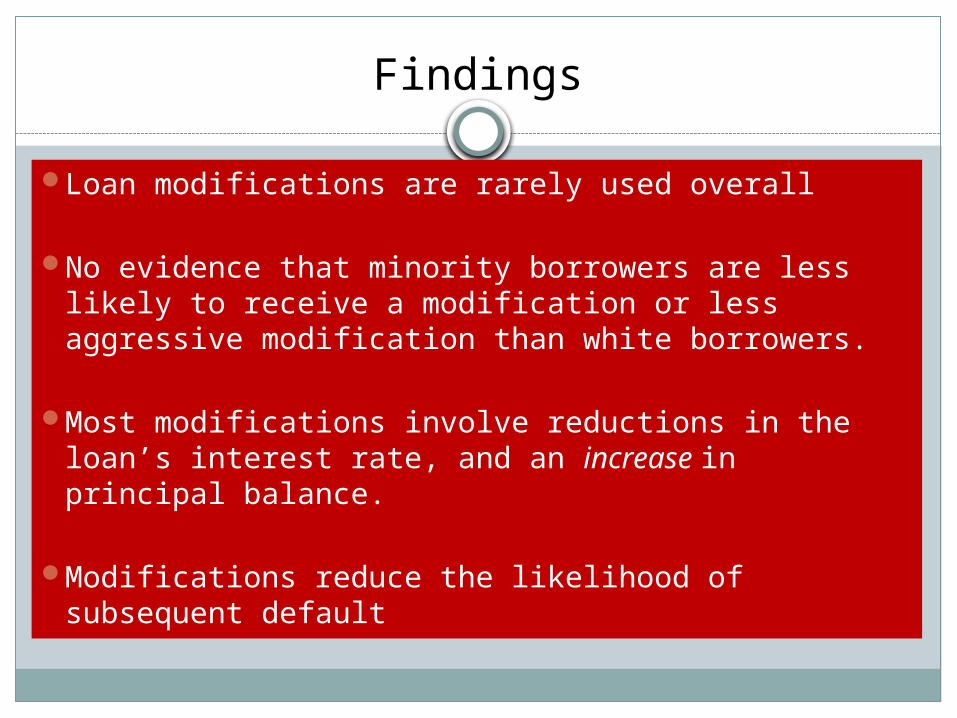

Findings

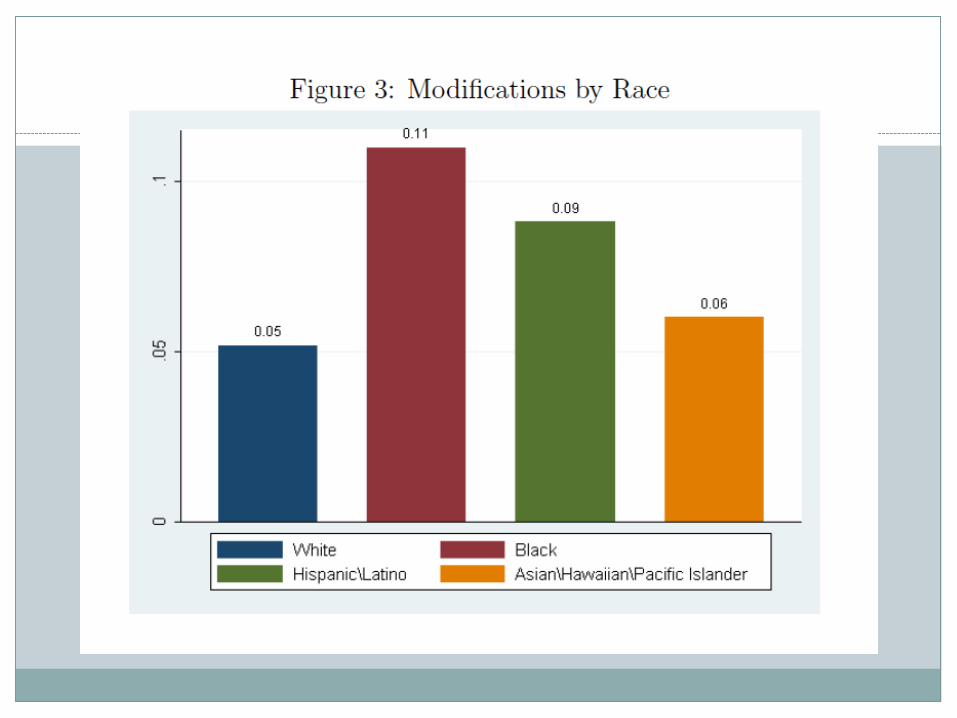

Loan modifications are rarely used overall

No evidence that minority borrowers are less likely to receive a modification or less aggressive modification than white borrowers.

Most modifications involve reductions in the loan’s interest rate, and an increase in principal balance.

Modifications reduce the likelihood of subsequent default

Q & A

1. Controlling for borrower risk factors, loan characteristics, and labor and housing market conditions, who loses a home to foreclosure?

A. No evidence of income effects, loan terms matter, racial effects (Hisp/Latino & Asian/other)

2. Among borrowers in distress, who gets a modification?

A. Modest income and racial effects (Afr Amer & Hisp/Latino); subprime

3. For borrowers in distress, does a modification reduce the likelihood of a subsequent foreclosure?

A. Yes.

4. Does a modification result in a significant rewriting of the mortgage contract, such as a reduced interest rate (A. yes) and/or principal balance? (A. no – increases balance)

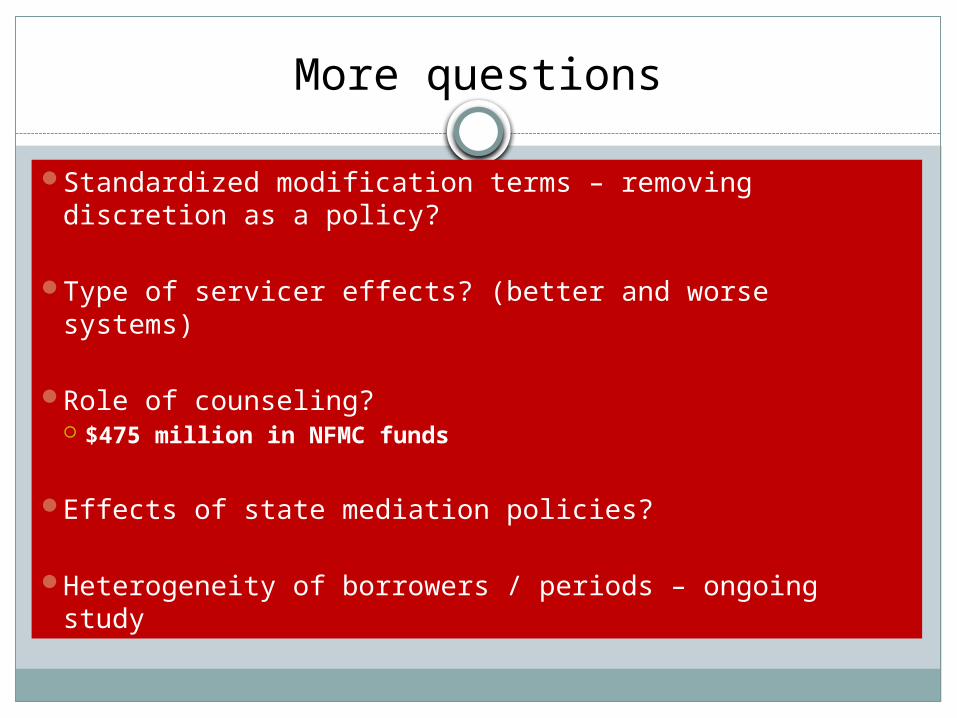

More questions

Standardized modification terms – removing discretion as a policy?

Type of servicer effects? (better and worse systems)

Role of counseling? $475 million in NFMC funds

Effects of state mediation policies?

Heterogeneity of borrowers / periods – ongoing study

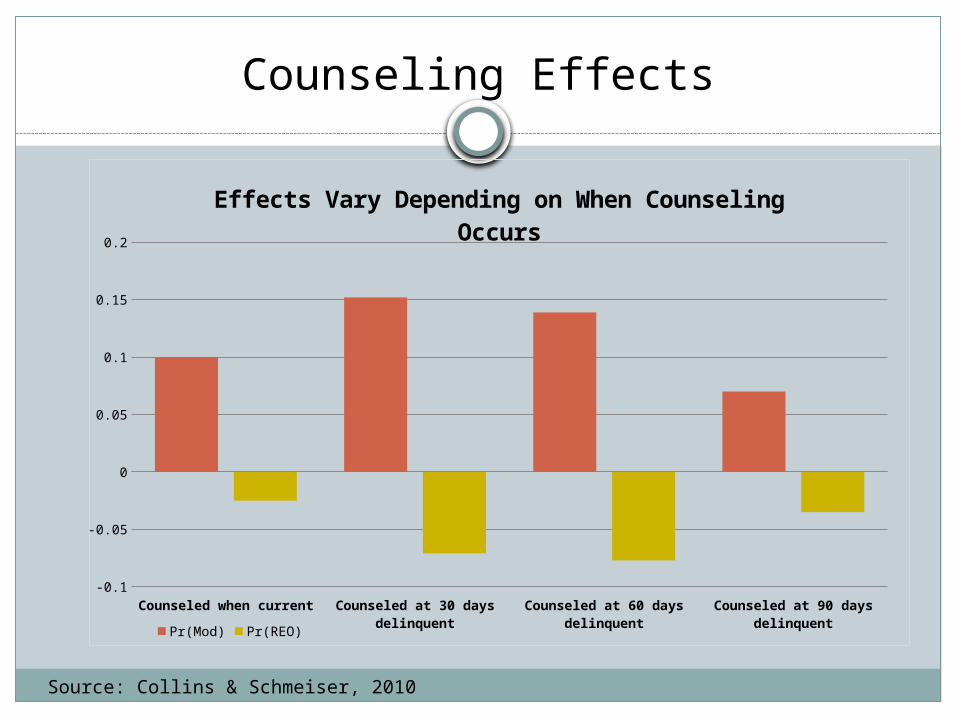

Counseling Effects

Counseled when current Counseled at 30 days delinquent

Counseled at 60 days delinquent

Counseled at 90 days delinquent

-0.1

-0.05

0

0.05

0.1

0.15

0.2

Effects Vary Depending on When Counseling Occurs

Pr(Mod) Pr(REO)

Source: Collins & Schmeiser, 2010

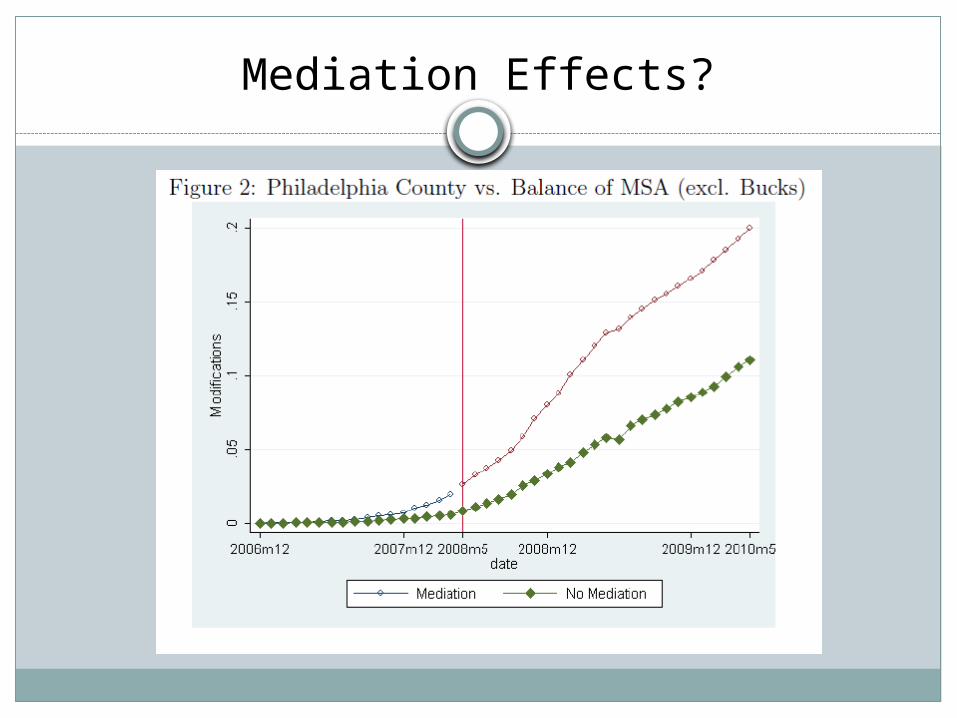

Mediation Policies

Mediation (conciliation) Out of court meeting with a neutral third party appointed

by the court in an attempt to resolve a dispute. If the parties to come to a resolution, foreclosure

dismissed

21 states have some form of foreclosure mediation 13 statewide 8 with county or court-district based

Mediation Effects?

Typology of Borrowers in Default

Income disruption Job loss/cutback (relocation options) Divorce (child support issues) Widow/er (may have limited work options)

Disability Chronic (DI application process)

Health crisis Acute or ongoing expenses (medical debt management)

Investor (not all are speculators) tenant eviction issues subsidized units

Small business failure (non-real estate) Sale / bankruptcy (special issues if farm)

Strategic defaulters

Policies for Homeowners in Distress

Prevention People not in default, but worried

Early Intervention Missed 1-2 payments

Late Intervention Missed 3+ payments

Transitional Support Short sale or foreclosure auction

Center for Financial Security

Financial Literacy Research Consortium of the Social Security Administration Wisconsin, Rand, Boston College FY 12 projects due late spring

Financial capacity building Life course models (not just retirement) Focus on vulnerable populations Balance sheet approach (not just saving)

Counseling, education, advice, disclosures, reminders, etc.

J. Michael CollinsFaculty Director, Center for Financial SecurityUniversity of Wisconsin-Madison7401 Social Science, 1180 Observatory DriveMadison, WI [email protected]

For More Information: cfs.wisc.edu