KEEI

KEEI

KE

EI

Korea Energy Demand Outlook

ISSN 1599-9009

KoreaEnergy

Dem

andO

utlook December 2011

Decem

ber2011

Volume 13, No. 4QUARTERLY ENERGY OUTLOOK

Korea Energy Economic Institute132 Naesonsunhwan-ro, Uiwang-si, Gyeonggi-do

Phone: (031)420-2114

Fax: (031)422-4958

E-mail : [email protected]

Hompage : http://www.keei.re.kr

Korea

Energy

Econom

icInstitute

에너지수요전망 문13-4 2012.3.8 4:9 PM 페이지1 매일3 MAC2PDF_IN 600DPI 175LPI T

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지156 매일3 MAC2PDF_IN 600DPI 125LPI T

ISSN 1599-9009

December 2011

Volume 13, No. 4

KEEIKorea Energy Demand Outlook

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지1 매일3 MAC2PDF_IN 600DPI 125LPI T

·In charge of overall research Choi, Do-young ([email protected])

·Oil/International oil market Kim, Soo-il ([email protected])

·Electricity/Transformation Choi, Do-young ([email protected])

·Coal/International coal market Kim, Tae-heon ([email protected])

·Town gas/Thermal energy Lee, Sang-youl ([email protected])

·International LNG market Lee, Bo-hye ([email protected])

·Material/Research support Hwang, In-wook ([email protected])

·Statistical support Chung, Chang-bong ([email protected])

Phone: +82-31-420-2148, +82-31-420-2234

Fax: +82-31-420-2164

KEEI Korea Energy Demand Outlook

The 「KEEI Korea Energy Demand Outlook」is a report that analyzes trends in theinternational energy market and energy supply/demand trends in Korea, and makesshort-term forecasts on energy demand.

This report quickly identifies recent changes in energy supply and demand, thusproviding various energy supply/demand forecast indexes and information forgovernment policies. It is intended to contribute to government efforts in setting andadjusting an overall policy direction regarding energy supply and demand.

This report was written and edited by the Energy Demand and Supply ForecastTeam under the Center for Energy Information and Statistics of KEEI.

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지2 매일3 MAC2PDF_IN 600DPI 125LPI T

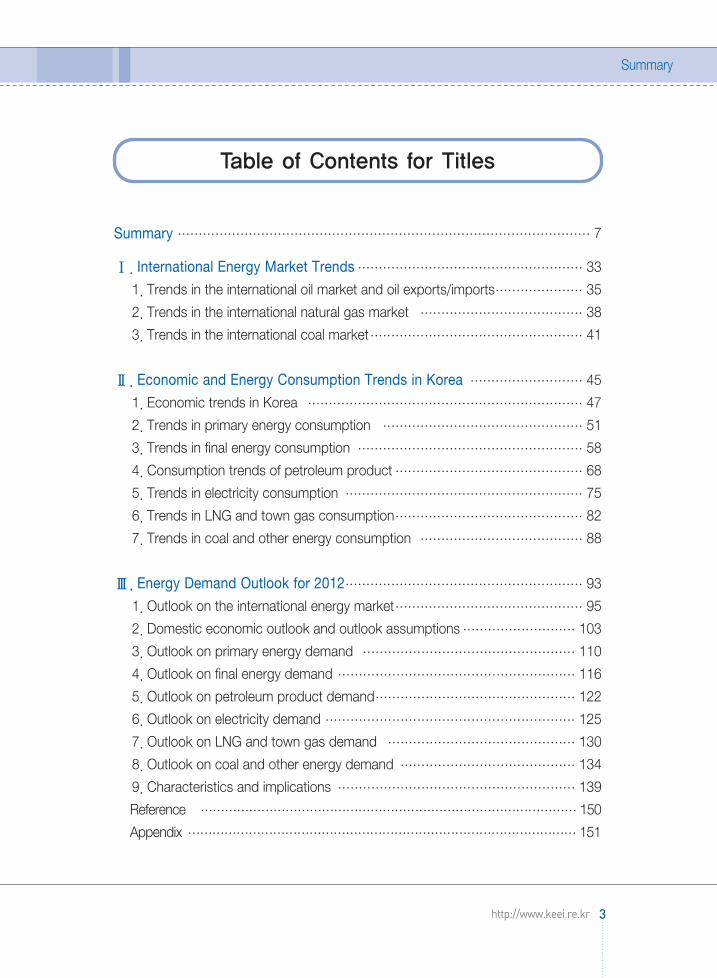

Summary ……………………………………………………………………………………… 7

Ⅰ. International Energy Market Trends……………………………………………… 33

1. Trends in the international oil market and oil exports/imports………………… 35

2. Trends in the international natural gas market ………………………………… 38

3. Trends in the international coal market…………………………………………… 41

Ⅱ. Economic and Energy Consumption Trends in Korea ……………………… 45

1. Economic trends in Korea ………………………………………………………… 47

2. Trends in primary energy consumption ………………………………………… 51

3. Trends in final energy consumption ……………………………………………… 58

4. Consumption trends of petroleum product ……………………………………… 68

5. Trends in electricity consumption ………………………………………………… 75

6. Trends in LNG and town gas consumption……………………………………… 82

7. Trends in coal and other energy consumption ………………………………… 88

Ⅲ. Energy Demand Outlook for 2012………………………………………………… 93

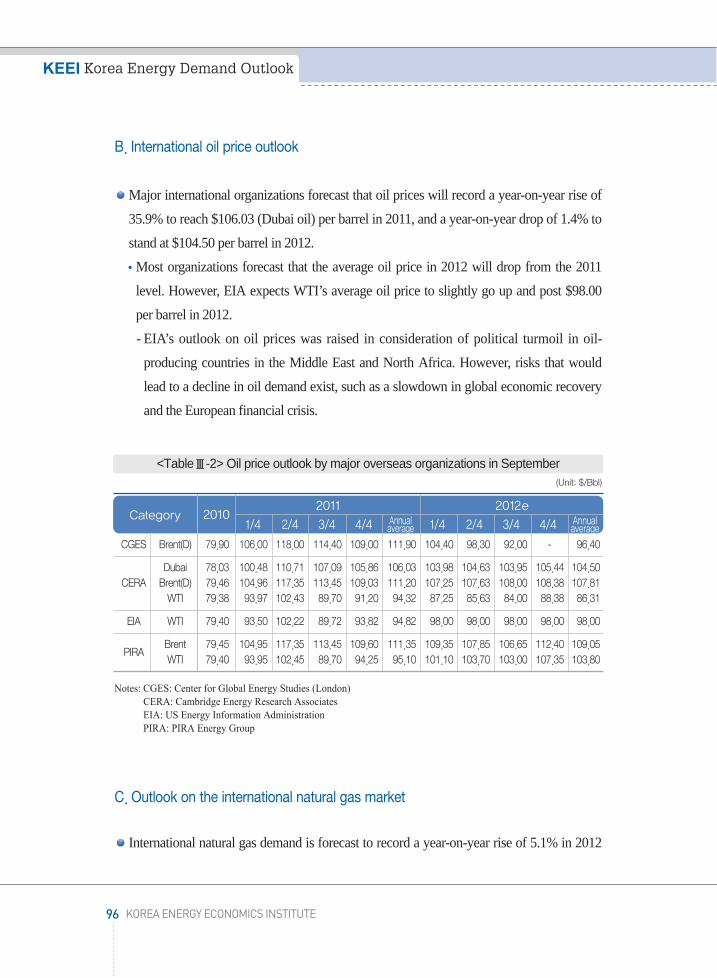

1. Outlook on the international energy market……………………………………… 95

2. Domestic economic outlook and outlook assumptions……………………… 103

3. Outlook on primary energy demand …………………………………………… 110

4. Outlook on final energy demand ………………………………………………… 116

5. Outlook on petroleum product demand………………………………………… 122

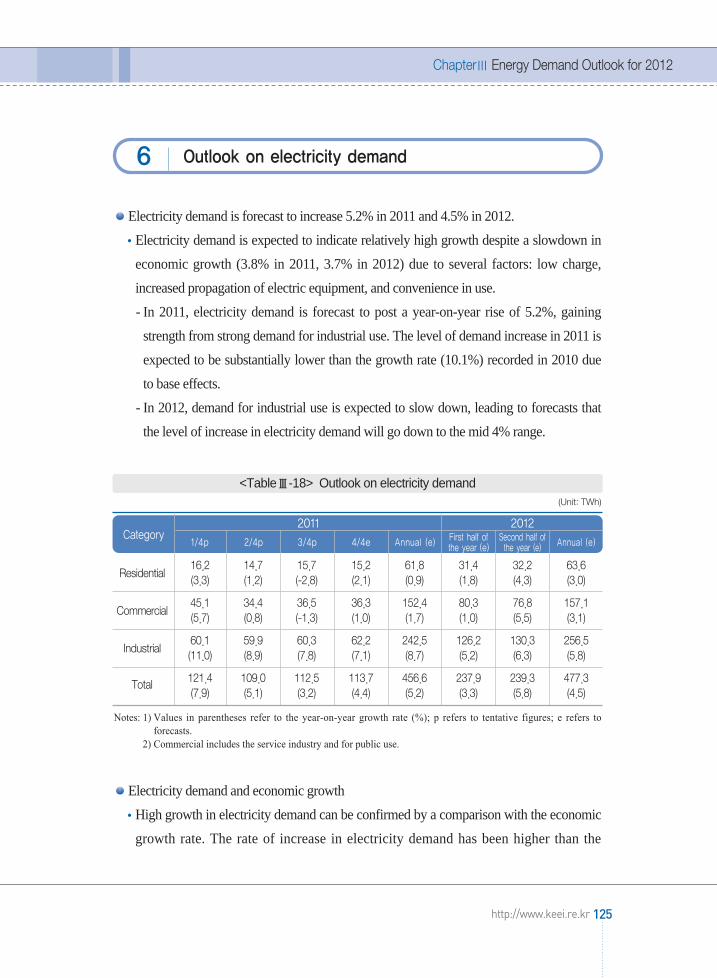

6. Outlook on electricity demand …………………………………………………… 125

7. Outlook on LNG and town gas demand ……………………………………… 130

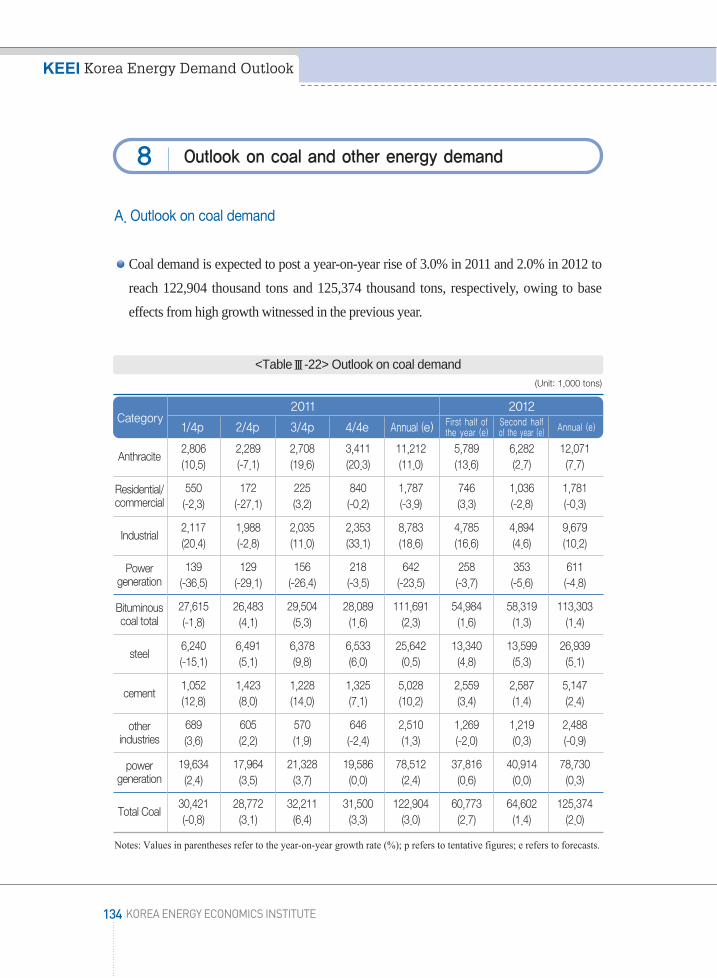

8. Outlook on coal and other energy demand …………………………………… 134

9. Characteristics and implications ………………………………………………… 139

Reference ………………………………………………………………………………… 150

Appendix …………………………………………………………………………………… 151

Contents

3http://www.keei.re.kr

Summary

Table of Contents for Titles

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지3 매일3 MAC2PDF_IN 600DPI 125LPI T

KEEI Korea Energy Demand Outlook

4 KOREA ENERGY ECONOMICS INSTITUTE

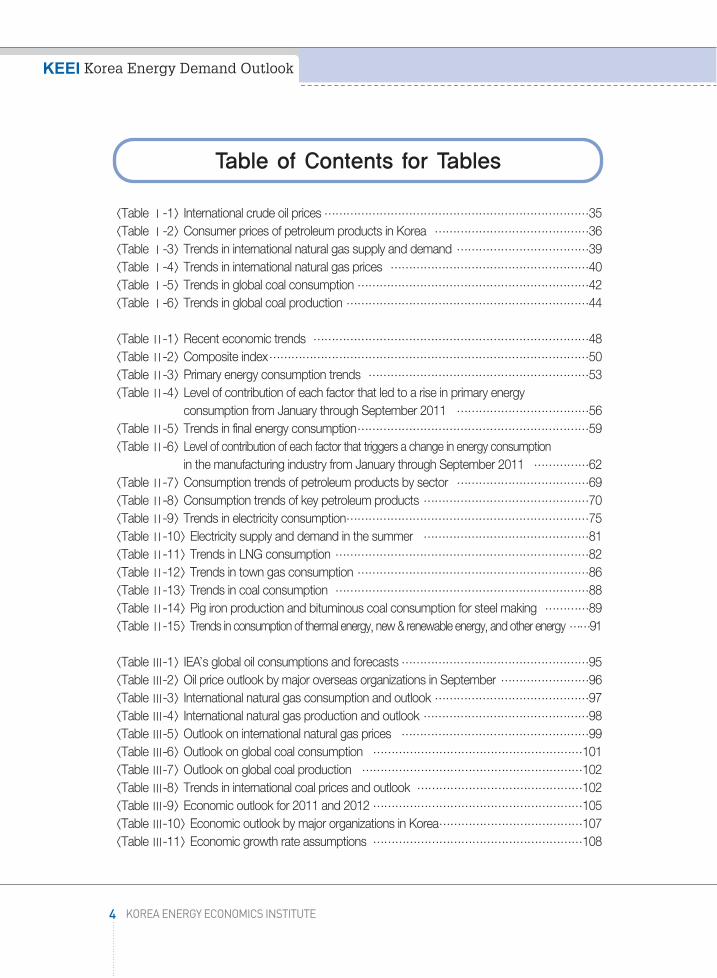

<Table Ⅰ-1> International crude oil prices ………………………………………………………………35<Table Ⅰ-2> Consumer prices of petroleum products in Korea ……………………………………36<Table Ⅰ-3> Trends in international natural gas supply and demand ………………………………39<Table Ⅰ-4> Trends in international natural gas prices ………………………………………………40<Table Ⅰ-5> Trends in global coal consumption ………………………………………………………42<Table Ⅰ-6> Trends in global coal production …………………………………………………………44

<Table Ⅱ-1> Recent economic trends …………………………………………………………………48<Table Ⅱ-2> Composite index……………………………………………………………………………50<Table Ⅱ-3> Primary energy consumption trends ……………………………………………………53<Table Ⅱ-4> Level of contribution of each factor that led to a rise in primary energy

consumption from January through September 2011 ………………………………56<Table Ⅱ-5> Trends in final energy consumption………………………………………………………59<Table Ⅱ-6> Level of contribution of each factor that triggers a change in energy consumption

in the manufacturing industry from January through September 2011 ……………62<Table Ⅱ-7> Consumption trends of petroleum products by sector ………………………………69<Table Ⅱ-8> Consumption trends of key petroleum products ………………………………………70<Table Ⅱ-9> Trends in electricity consumption…………………………………………………………75<Table Ⅱ-10> Electricity supply and demand in the summer ………………………………………81<Table Ⅱ-11> Trends in LNG consumption ……………………………………………………………82<Table Ⅱ-12> Trends in town gas consumption ………………………………………………………86<Table Ⅱ-13> Trends in coal consumption ……………………………………………………………88<Table Ⅱ-14> Pig iron production and bituminous coal consumption for steel making …………89<Table Ⅱ-15> Trends in consumption of thermal energy, new & renewable energy, and other energy ……91

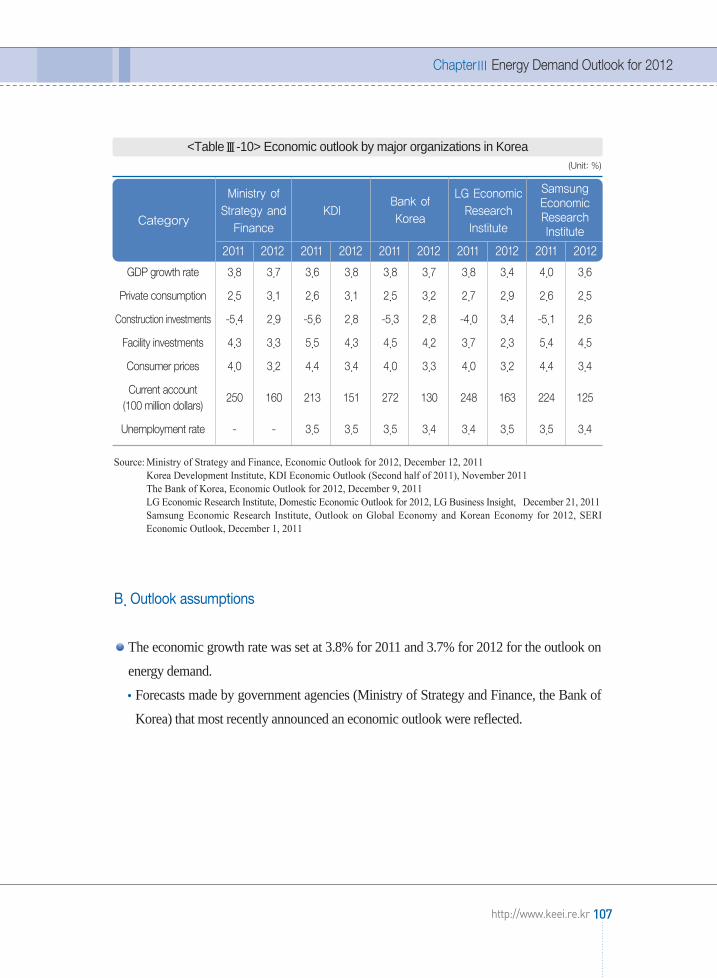

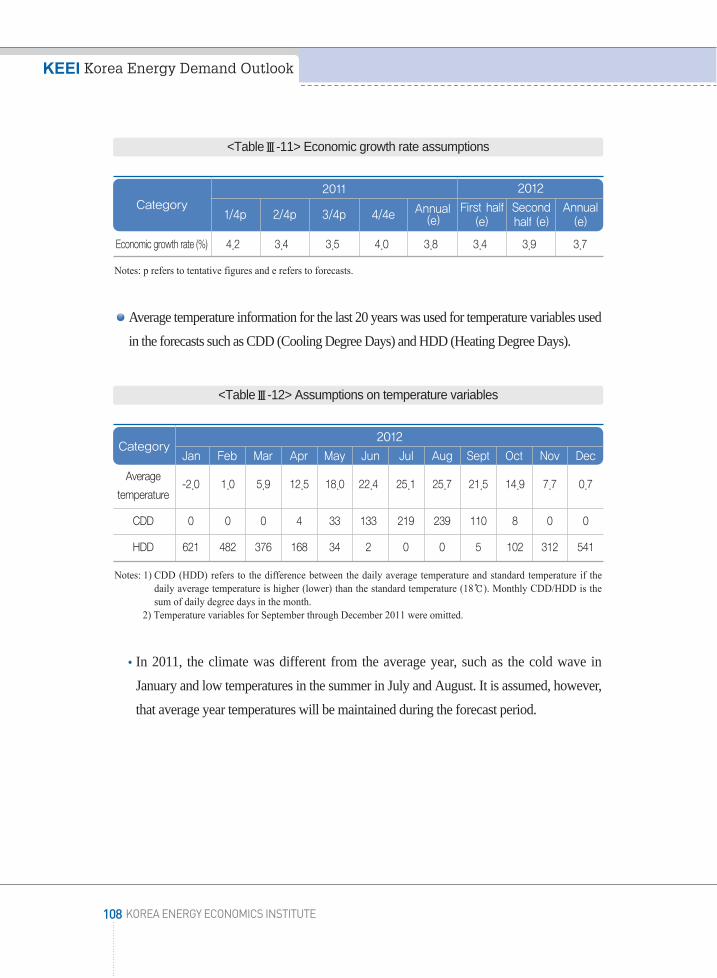

<Table Ⅲ-1> IEA’s global oil consumptions and forecasts……………………………………………95<Table Ⅲ-2> Oil price outlook by major overseas organizations in September ……………………96<Table Ⅲ-3> International natural gas consumption and outlook ……………………………………97<Table Ⅲ-4> International natural gas production and outlook ………………………………………98<Table Ⅲ-5> Outlook on international natural gas prices ……………………………………………99<Table Ⅲ-6> Outlook on global coal consumption …………………………………………………101<Table Ⅲ-7> Outlook on global coal production ……………………………………………………102<Table Ⅲ-8> Trends in international coal prices and outlook ………………………………………102<Table Ⅲ-9> Economic outlook for 2011 and 2012 …………………………………………………105<Table Ⅲ-10> Economic outlook by major organizations in Korea…………………………………107<Table Ⅲ-11> Economic growth rate assumptions …………………………………………………108

Table of Contents for Tables

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지4 매일3 MAC2PDF_IN 600DPI 125LPI T

SummaryContents

5http://www.keei.re.kr

<Table Ⅲ-12> Assumptions on temperature variables ………………………………………………108<Table Ⅲ-13> Outlook on primary energy demand …………………………………………………110<Table Ⅲ-14> Key indices related to energy consumption …………………………………………112<Table Ⅲ-15> Outlook on final energy demand………………………………………………………117<Table Ⅲ-16> Outlook on petroleum product demand by sector …………………………………123<Table Ⅲ-17> Outlook on demand for key petroleum products……………………………………124<Table Ⅲ-18> Outlook on electricity demand…………………………………………………………125<Table Ⅲ-19> Trends in GDP elasticity of electricity demand ………………………………………127<Table Ⅲ-20> Outlook on LNG demand………………………………………………………………131<Table Ⅲ-21> Outlook on town gas demand…………………………………………………………133<Table Ⅲ-22> Outlook on coal demand ………………………………………………………………134<Table Ⅲ-23> Outlook on thermal energy, new & renewable energy, and other energy demand …137<Table Ⅲ-24> Outlook on energy intensity ……………………………………………………………142

[Figure Ⅰ-1] Petroleum product import prices and consumer prices ………………………………37[Figure Ⅰ-2] Trends in international natural gas prices…………………………………………………40[Figure Ⅰ-3] International coal price trends………………………………………………………………43

[Figure Ⅱ-1] Business cycle clock ………………………………………………………………………50[Figure Ⅱ-2] Recent economic and primary energy consumption trends …………………………52[Figure Ⅱ-3] Trends in Dubai spot oil price………………………………………………………………54[Figure Ⅱ-4] Level of contribution to increase in primary energy consumption by each factor

from January through September 2011 …………………………………………………56[Figure Ⅱ-5] Trends in primary energy consumption increase rate …………………………………58[Figure Ⅱ-6] Final energy consumption by energy source from January through October 2011 …60[Figure Ⅱ-7] Rate of increase in value-added of each business type under the manufacturing

industry from January through September 2011 ………………………………………61[Figure Ⅱ-8] Level of contribution made by each factor that triggers a change in energy

consumption in the manufacturing industry from January through September ……63[Figure Ⅱ-9] Trends in consumer prices of oil for transport……………………………………………64[Figure Ⅱ-10] Trends in the rate of final energy consumption increase by sector …………………65[Figure Ⅱ-11] Level of contribution of each energy source to primary energy increase from

January through October 2011 …………………………………………………………67[Figure Ⅱ-12] Increase rate of petroleum product consumption by sector …………………………69[Figure Ⅱ-13] Gasoline consumption and increase rate ………………………………………………71

Table of Contents for Figures

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지5 매일3 MAC2PDF_IN 600DPI 125LPI T

KEEI Korea Energy Demand Outlook

6 KOREA ENERGY ECONOMICS INSTITUTE

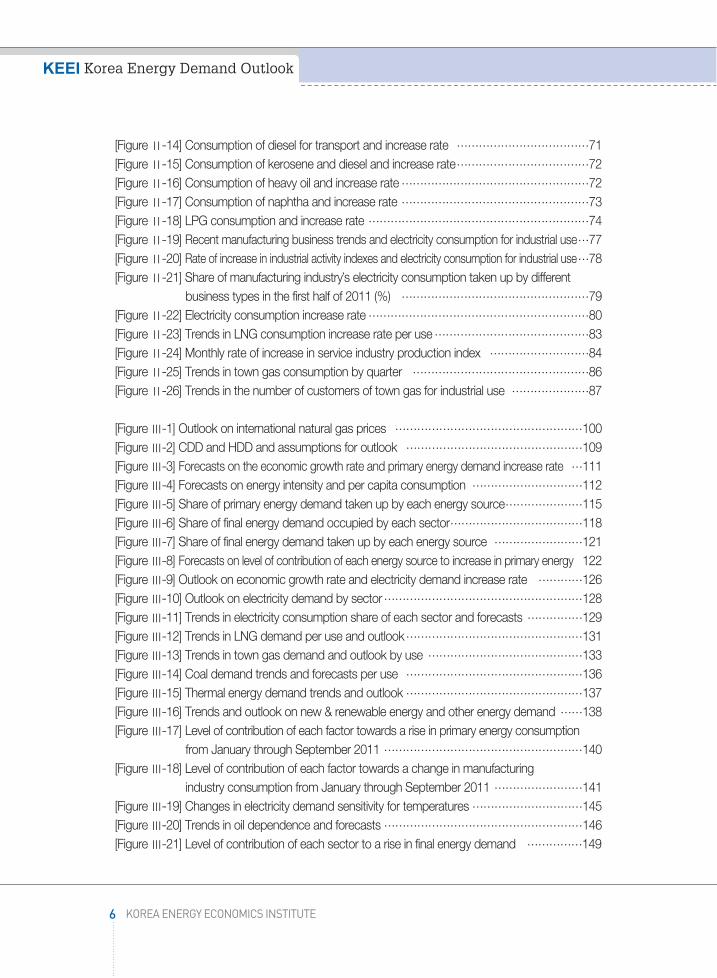

[Figure Ⅱ-14] Consumption of diesel for transport and increase rate ………………………………71[Figure Ⅱ-15] Consumption of kerosene and diesel and increase rate………………………………72[Figure Ⅱ-16] Consumption of heavy oil and increase rate……………………………………………72[Figure Ⅱ-17] Consumption of naphtha and increase rate ……………………………………………73[Figure Ⅱ-18] LPG consumption and increase rate ……………………………………………………74[Figure Ⅱ-19] Recent manufacturing business trends and electricity consumption for industrial use…77[Figure Ⅱ-20] Rate of increase in industrial activity indexes and electricity consumption for industrial use…78[Figure Ⅱ-21] Share of manufacturing industry’s electricity consumption taken up by different

business types in the first half of 2011 (%) ……………………………………………79[Figure Ⅱ-22] Electricity consumption increase rate……………………………………………………80[Figure Ⅱ-23] Trends in LNG consumption increase rate per use……………………………………83[Figure Ⅱ-24] Monthly rate of increase in service industry production index ………………………84[Figure Ⅱ-25] Trends in town gas consumption by quarter …………………………………………86[Figure Ⅱ-26] Trends in the number of customers of town gas for industrial use …………………87

[Figure Ⅲ-1] Outlook on international natural gas prices ……………………………………………100[Figure Ⅲ-2] CDD and HDD and assumptions for outlook …………………………………………109[Figure Ⅲ-3] Forecasts on the economic growth rate and primary energy demand increase rate …111[Figure Ⅲ-4] Forecasts on energy intensity and per capita consumption …………………………112[Figure Ⅲ-5] Share of primary energy demand taken up by each energy source…………………115[Figure Ⅲ-6] Share of final energy demand occupied by each sector………………………………118[Figure Ⅲ-7] Share of final energy demand taken up by each energy source ……………………121[Figure Ⅲ-8] Forecasts on level of contribution of each energy source to increase in primary energy 122[Figure Ⅲ-9] Outlook on economic growth rate and electricity demand increase rate …………126[Figure Ⅲ-10] Outlook on electricity demand by sector………………………………………………128[Figure Ⅲ-11] Trends in electricity consumption share of each sector and forecasts ……………129[Figure Ⅲ-12] Trends in LNG demand per use and outlook…………………………………………131[Figure Ⅲ-13] Trends in town gas demand and outlook by use ……………………………………133[Figure Ⅲ-14] Coal demand trends and forecasts per use …………………………………………136[Figure Ⅲ-15] Thermal energy demand trends and outlook …………………………………………137[Figure Ⅲ-16] Trends and outlook on new & renewable energy and other energy demand ……138[Figure Ⅲ-17] Level of contribution of each factor towards a rise in primary energy consumption

from January through September 2011 ………………………………………………140[Figure Ⅲ-18] Level of contribution of each factor towards a change in manufacturing

industry consumption from January through September 2011 ……………………141[Figure Ⅲ-19] Changes in electricity demand sensitivity for temperatures …………………………145[Figure Ⅲ-20] Trends in oil dependence and forecasts ………………………………………………146[Figure Ⅲ-21] Level of contribution of each sector to a rise in final energy demand ……………149

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지6 매일3 MAC2PDF_IN 600DPI 125LPI T

Summary

7http://www.keei.re.kr

From January through October 2011(in terms of the total), primary energy consumption

tentatively reached 221.3 million TOE, a year-on-year rise of 3.3%.

From January through October, primary energy consumption indicated a gradual

increase in tandem with a slight slowdown in economic growth, despite the record-

breaking cold wave (a 5.4℃ drop from average year temperatures) in January.

- In the first quarter, the Korean economy recorded a growth rate of 4.2%, which is close

to the potential growth rate. However, the economy’s level of growth slowed down to

the mid-3% range in the second quarter and onwards.

- Energy consumption for industrial use led a rise in primary energy consumption from

January through October as a result of continued favorable conditions in industrial

production.

Notes: Values for the fourth quarter of 2011 are forecasts.

Energy consumption trends

Summary▶

[Recent economic and primary energy consumption trends]

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지7 매일3 MAC2PDF_IN 600DPI 125LPI T

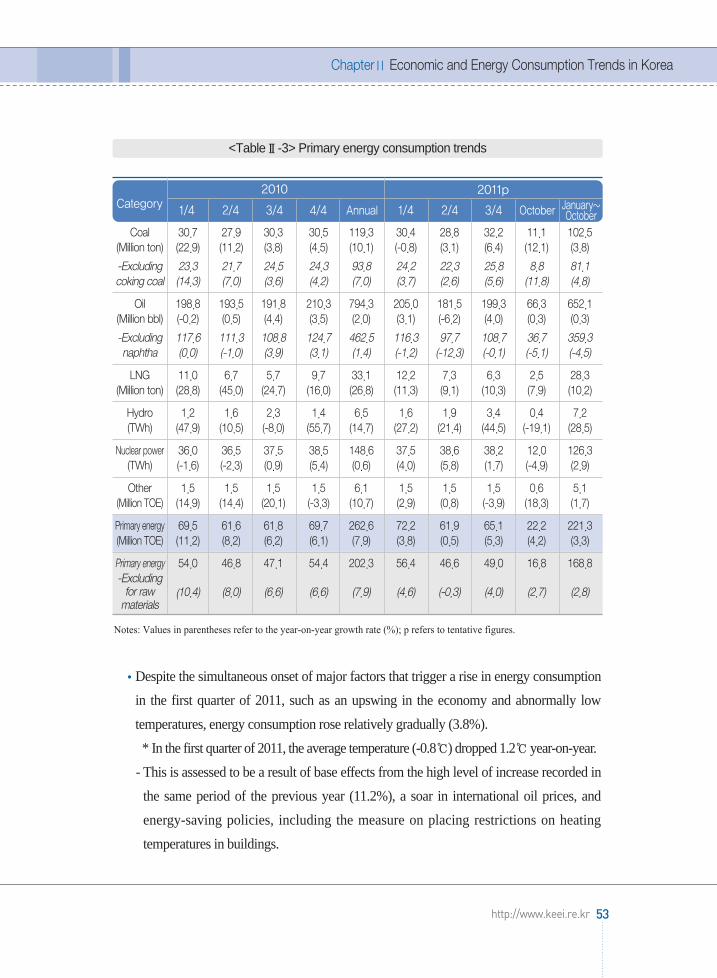

Despite the simultaneous onset of major factors that trigger a rise in energy consumption

in the first quarter of 2011, such as an upswing in the economy and abnormally low

temperatures, primary energy consumption rose relatively gradually.

- This is a result of base effects from the high level of increase recorded in the same period

of the previous year (11.2%), a soar in international oil prices, and energy-saving policies,

including the measure on placing restrictions on heating temperatures in buildings.

Primary energy consumption recorded a year-on-year increase of a mere 0.5% in the

second quarter, but posted relatively high growth of 5.3% in the third quarter.

Notes: Values in parentheses refer to the year-on-year growth rate (%); p refers to tentative figures

8 KOREA ENERGY ECONOMICS INSTITUTE

KEEI Korea Energy Demand Outlook

Category2010 2011p

1/4 2/4 3/4 4/4 Annual 1/4 2/4 3/4 October January~October

<Primary energy consumption trends>

30.7 27.9 30.3 30.5 119.3 30.4 28.8 32.2 11.1 102.5(22.9) (11.2) (3.8) (4.5) (10.1) (-0.8) (3.1) (6.4) (12.1) (3.8)

23.3 21.7 24.5 24.3 93.8 24.2 22.3 25.8 8.8 81.1(14.3) (7.0) (3.6) (4.2) (7.0) (3.7) (2.6) (5.6) (11.8) (4.8)

198.8 193.5 191.8 210.3 794.3 205.0 181.5 199.3 66.3 652.1(-0.2) (0.5) (4.4) (3.5) (2.0) (3.1) (-6.2) (4.0) (0.3) (0.3)

117.6 111.3 108.8 124.7 462.5 116.3 97.7 108.7 36.7 359.3(0.0) (-1.0) (3.9) (3.1) (1.4) (-1.2) (-12.3) (-0.1) (-5.1) (-4.5)

11.0 6.7 5.7 9.7 33.1 12.2 7.3 6.3 2.5 28.3(28.8) (45.0) (24.7) (16.0) (26.8) (11.3) (9.1) (10.3) (7.9) (10.2)

1.2 1.6 2.3 1.4 6.5 1.6 1.9 3.4 0.4 7.2(47.9) (10.5) (-8.0) (55.7) (14.7) (27.2) (21.4) (44.5) (-19.1) (28.5)

36.0 36.5 37.5 38.5 148.6 37.5 38.6 38.2 12.0 126.3(-1.6) (-2.3) (0.9) (5.4) (0.6) (4.0) (5.8) (1.7) (-4.9) (2.9)

1.5 1.5 1.5 1.5 6.1 1.5 1.5 1.5 0.6 5.1(14.9) (14.4) (20.1) (-3.3) (10.7) (2.9) (0.8) (-3.9) (18.3) (1.7)

69.5 61.6 61.8 69.7 262.6 72.2 61.9 65.1 22.2 221.3(11.2) (8.2) (6.2) (6.1) (7.9) (3.8) (0.5) (5.3) (4.2) (3.3)

54.0 46.8 47.1 54.4 202.3 56.4 46.6 49.0 16.8 168.8

(10.4) (8.0) (6.6) (6.6) (7.9) (4.6) (-0.3) (4.0) (2.7) (2.8)

Coal(Million ton)

-Excluding coking coal

Oil(Million bbl)

-Excludingnaphtha

LNG(Million ton)

Hydro(TWh)

Nuclear power(TWh)

Other(Million TOE)

Primary energy(Million TOE)

Primary energy-Excludingfor raw materials

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지8 매일3 MAC2PDF_IN 600DPI 125LPI T

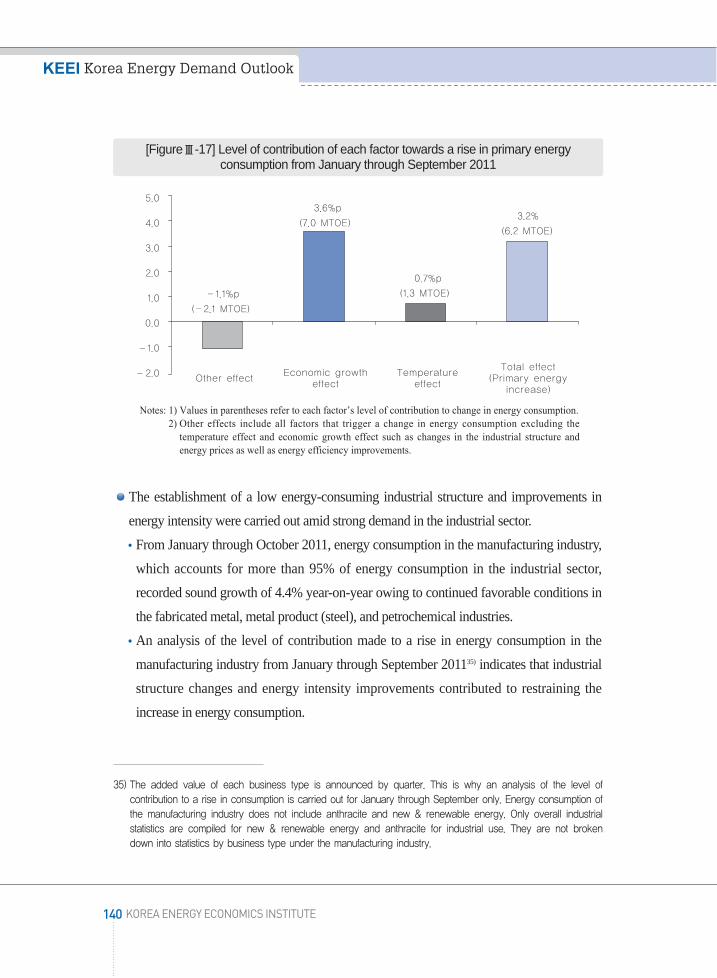

Level of contribution of each factor that led to an increase in primary energy consumption

from January through September 20111)

The level of contribution of economic growth to a rise in primary energy consumption is

estimated at 3.6%p (7.0 million TOE).

- It is assumed that primary energy consumption would have recorded a year-on-year

increase of 3.6% from January through September 2011 as a result of economic growth

if there were no changes in other factors that trigger a change in consumption.

The temperature effect contributed 0.7%p (1.3 million TOE) to a rise in primary energy

consumption.

- It is assumed that energy consumption rose 0.7% from January through September as a

result of a drop (1.2℃↓) in the average temperature in the first quarter, including the

record-breaking cold wave in 48 years that took place in January 2011.

Energy consumption went down 1.1%p as a result of changes in other factors such as

energy efficiency improvements and a rise in oil prices.

Notes: Other effects include all factors that cause changes in consumption, excluding the temperature effect andeconomic growth effect. Examples are improvements in energy efficiency, changes in industrial structure, andchanges in energy prices.

9http://www.keei.re.kr

Summary

1) GDP is announced by quarter. For this reason, an analysis of the level of contribution made to a rise inconsumption is limited to January through September.

CategoryAmount of contribution to a rise in consumption

(1,000 TOE)

Rate of contribution to a rise in

consumption (%)

Level of contribution to rateof increase in primary energy consumption

Growth effect 6,985 112.7 3.6%p

Temperature effect 1,296 20.9 0.7%p

Other effects -2,084 -33.6 -1.1%p

Total effects 6,197 100.0 3.2%

<Level of contribution of each factor that led to a rise in primary energy consumption from January through September 2011>

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지9 매일3 MAC2PDF_IN 600DPI 125LPI T

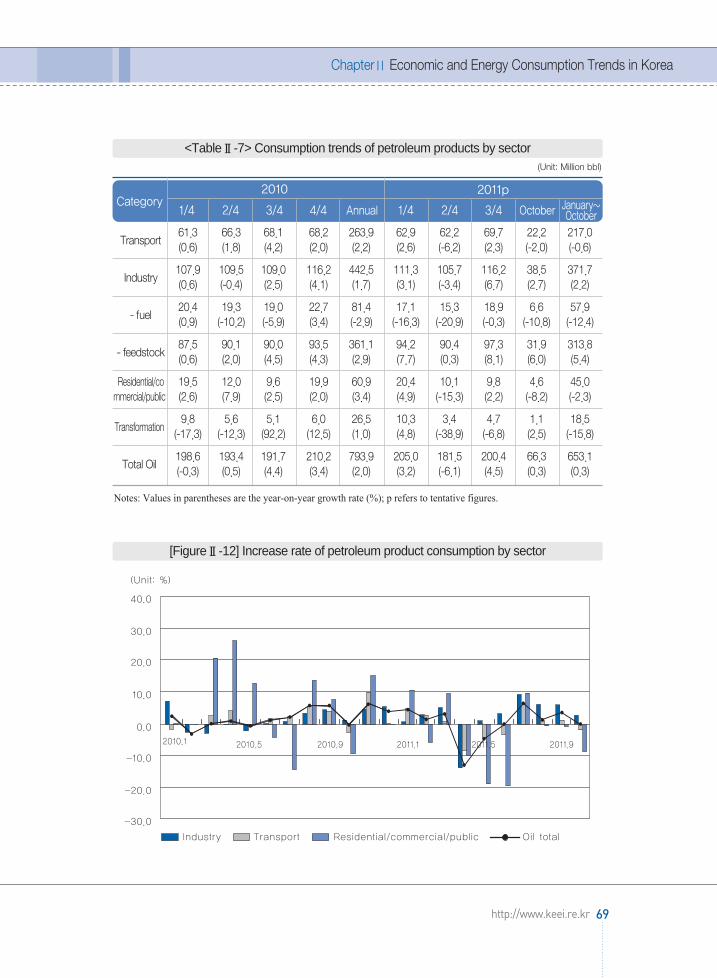

Trends in consumption of each energy source from January through October 2011

Petroleum product consumption showed little change (0.3% increase) from the same

period of the previous year, influenced by sluggish consumption (-6.2%) in the second

quarter.

- Consumption of fuel for transport remained stagnant and consumption of heavy oil for

industrial fuel decreased. In contrast, naphtha consumption for industrial raw material

use went up 7.0% year-on-year as a result of increased production activities in the

petrochemical industry. As of 2010, naphtha consumption for industrial raw material

use accounted for 42% of total oil consumption.

Coal consumption witnessed a year-on-year rise of 3.8%.

- Coal consumption soared (10.1%) in 2010. However, the level of increase substantially

slowed down from January through October 2011 as a result of a mere 0.1% rise in

bituminous coal consumption for steel making, which accounted for 21.4% of total

consumption in 2010.

Natural gas (LNG) consumption rose 26.8% in 2010, followed by two-digit growth

(10.2%) from January through October 2011.

- From January through October, LNG consumption for power generation recorded high

growth of 11.8% year-on-year, attributable to an increase in electricity demand and

shortage of base-load power generation facilities, despite the operation of Singori

Nuclear Power Plant Unit 1.

- LNG consumption for production of town gas increased 9.3%, which meant a

slowdown from the level of increase (12.4%) witnessed in 2010.

From January through October 2011, the level of nuclear power generation rose 2.9%

year-on-year as a result of operation of Singori Nuclear Power Plant Unit 12).

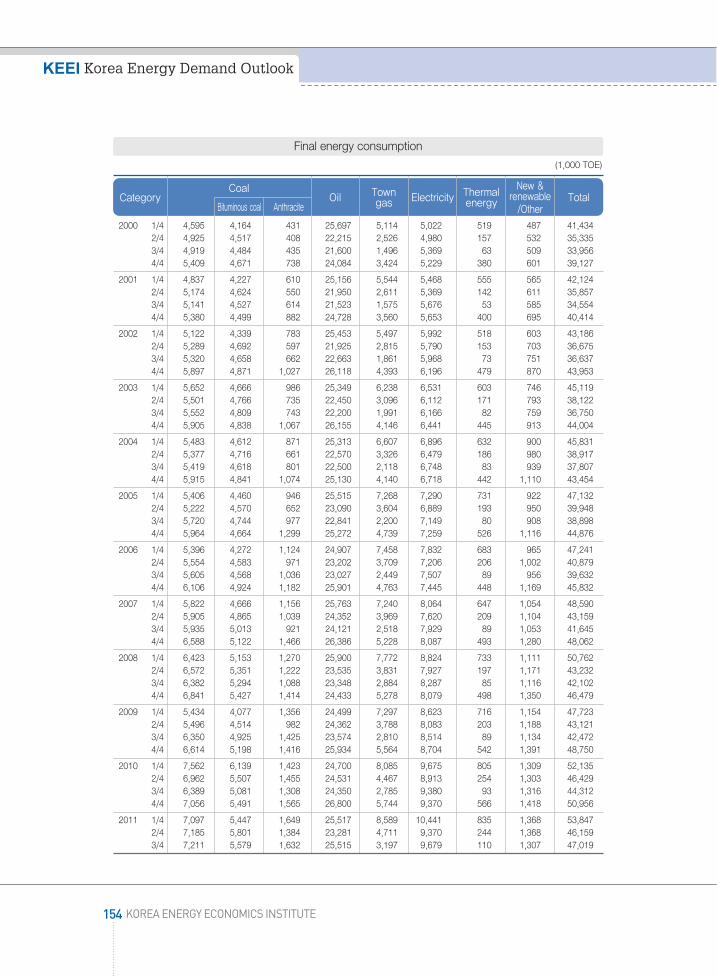

From January through October 2011, final energy consumption rose by 3.1% year-on-year

to stand at 163.2 million TOE, according to tentative figures.

10 KOREA ENERGY ECONOMICS INSTITUTE

KEEI Korea Energy Demand Outlook

2) Korea’s 21st nuclear power plant. Began commercial operation on February 28, 2011.

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지10 매일3 MAC2PDF_IN 600DPI 125LPI T

Notes: Values in parentheses are the year-on-year growth rate (%); p refers to tentative figures.

11http://www.keei.re.kr

Summary

Category2010 2011p

1/4 2/4 3/4 4/4 Annual 1/4 2/4 3/4 October January~October

<Trends in final energy consumption>

29.0 28.5 27.8 29.9 115.2 29.7 29.0 30.1 10.3 99.1(14.2) (9.2) (4.4) (6.7) (8.5) (2.4) (1.8) (8.4) (8.4) (4.6)

13.5 13.7 13.1 14.6 54.8 14.0 13.7 14.0 4.9 46.6(14.1) (9.4) (3.7) (9.0) (9.0) (3.9) (0.4) (7.2) (7.4) (4.1)

8.6 9.3 9.5 9.6 36.9 8.8 8.7 9.8 3.1 30.4(1.2) (2.3) (4.8) (2.8) (2.8) (2.8) (-5.8) (2.6) (-2.0) (-0.4)

13.3 7.6 6.1 10.3 37.3 14.0 7.4 6.1 2.4 30.0

(4.9) (9.6) (3.9) (0.2) (4.3) (5.4) (-2.5) (1.1) (-1.0) (1.9)

1.2 1.0 1.0 1.2 4.5 1.3 1.0 1.1 0.4 3.7(7.6) (2.3) (1.8) (5.2) (4.4) (4.0) (-4.4) (7.7) (-0.8) (2.2)

52.1 46.4 44.3 51.0 193.8 53.8 46.2 47.0 16.1 163.2(9.2) (7.7) (4.3) (4.5) (6.5) (3.3) (-0.6) (6.1) (4.6) (3.1)

36.6 31.6 29.6 35.7 133.5 38.1 30.9 31.0 10.8 110.7

(7.3) (7.0) (4.0) (4.5) (5.7) (4.2) (-2.3) (4.5) (2.3) (2.2)

7.6 4.2 2.6 5.4 20.0 8.1 4.5 3.0 1.3 16.9(10.8) (17.9) (-0.9) (3.2) (8.3) (6.2) (5.5) (14.8) (12.3) (7.9)

188.7 187.7 186.7 204.3 767.4 194.7 178.1 195.7 65.2 633.7(0.8) (0.9) (3.1) (3.2) (2.0) (3.1) (-5.1) (4.8) (0.2) (0.9)

107.6 105.6 103.7 118.7 435.6 106.0 94.2 105.0 35.6 340.9(1.7) (-0.4) (1.6) (2.6) (1.4) (-1.5) (-10.8) (1.3) (-5.4) (-3.9)

112.5 103.6 109.1 109.0 434.2 121.4 109.0 112.5 35.6 378.5(12.2) (10.3) (10.2) (7.7) (10.1) (7.9) (5.1) (3.2) (6.1) (5.5)

11.3 10.4 9.5 10.7 41.8 10.6 10.7 10.7 3.9 36.0(37.0) (26.1) (0.4) (6.5) (16.4) (-5.5) (3.0) (13.0) (15.6) (4.2)

3.9 4.2 3.7 4.5 16.3 4.4 4.2 4.3 1.7 14.6(6.6) (22.0) (-5.4) (7.8) (7.3) (12.5) (-0.1) (17.9) (19.3) (10.7)

2,114 1,557 1,409 1,985 7,064 2,203 1,612 1,417 609 5,841

(13.0) (11.9) (15.2) (2.6) (10.1) (4.2) (3.6) (0.6) (12.4) (3.9)

Industry(Million TOE)

-Excluding forraw materials

Transport(Million TOE)

Residential/commercial(Million TOE)

Public/other(Million TOE)

Total(Million TOE)

Total-Excluding forraw materials

Town gas(Billion m3)

Oil(Million bbl)

-Excludingnaphtha

Electricity(TWh)

Coal(Million ton)

-Excludingcoking coal

Thermal andother

(Thousand TOE)

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지11 매일3 MAC2PDF_IN 600DPI 125LPI T

Energy consumption in the industrial sector indicated a year-on-year rise of 4.6%, thus

leading an increase in final energy consumption. Consumption in the

residential/commercial and transport sector rose 1.9% and -0.4%, respectively.

Energy consumption in the manufacturing industry, which accounts for more than 95%

of energy consumption in the industrial sector, went up 4.4% year-on-year. This is

attributable to a rise in production activities in the fabricated metal, metal product (steel),

and petrochemical industries.

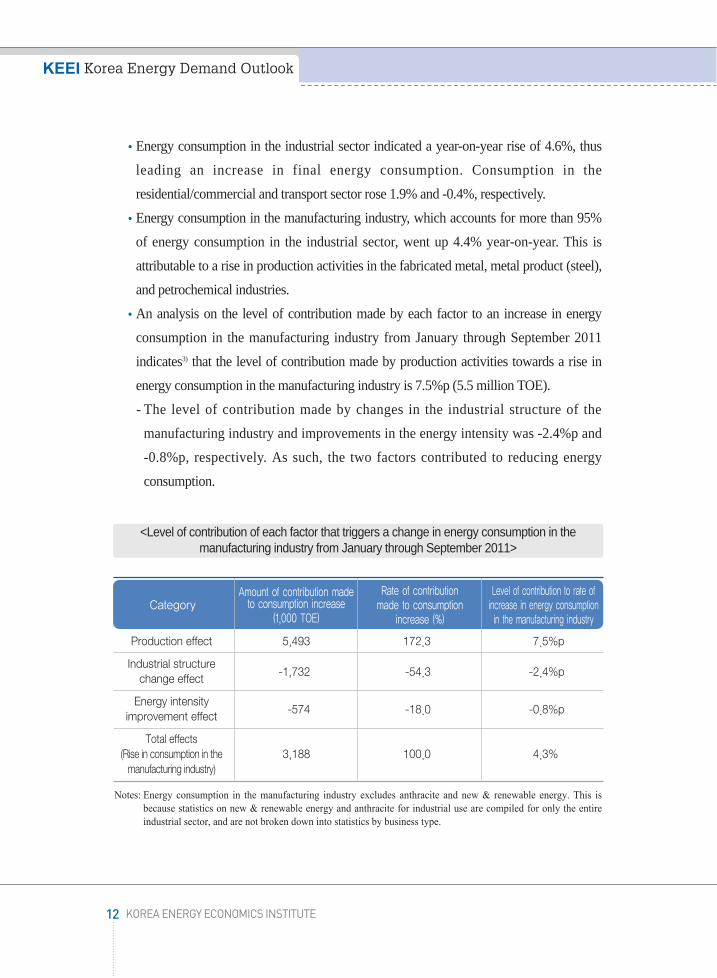

An analysis on the level of contribution made by each factor to an increase in energy

consumption in the manufacturing industry from January through September 2011

indicates3) that the level of contribution made by production activities towards a rise in

energy consumption in the manufacturing industry is 7.5%p (5.5 million TOE).

- The level of contribution made by changes in the industrial structure of the

manufacturing industry and improvements in the energy intensity was -2.4%p and

-0.8%p, respectively. As such, the two factors contributed to reducing energy

consumption.

Notes: Energy consumption in the manufacturing industry excludes anthracite and new & renewable energy. This isbecause statistics on new & renewable energy and anthracite for industrial use are compiled for only the entireindustrial sector, and are not broken down into statistics by business type.

12 KOREA ENERGY ECONOMICS INSTITUTE

KEEI Korea Energy Demand Outlook

CategoryAmount of contribution made

to consumption increase(1,000 TOE)

Rate of contribution made to consumption

increase (%)

Level of contribution to rate ofincrease in energy consumptionin the manufacturing industry

Production effect 5,493 172.3 7.5%p

Industrial structure -1,732 -54.3 -2.4%pchange effect

Energy intensity -574 -18.0 -0.8%pimprovement effect

Total effects(Rise in consumption in the 3,188 100.0 4.3%manufacturing industry)

<Level of contribution of each factor that triggers a change in energy consumption in themanufacturing industry from January through September 2011>

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지12 매일3 MAC2PDF_IN 600DPI 125LPI T

Trends in final energy consumption by energy source from January through October 2011

By energy source, there was a rapid increase in consumption of naphtha for raw material

use in the petrochemical industry (7.0%) and electricity consumption (5.5%), as a result

of continued favorable conditions in industries that consume great amounts of energy

and the cold wave.

- An analysis of the share of final energy consumption taken up by different uses and

energy sources from January through October 2011 indicates that the share taken up by

energy for industrial raw material use (naphtha, coking coal) was the highest at 32.1%.

It was followed by petroleum for fuel (27.8%), electricity (20.0%), and town gas

(10.9%).

In terms of oil, consumption of petroleum products for transport, including gasoline,

diesel for transport, and LPG, declined 0.6%. Consumption for heating in the

residential/commercial sector also went down 2.3%. In contrast, naphtha consumption

went up considerably as a result of favorable conditions in the petrochemical industry.

Town gas consumption for industrial use went up 12.7% to lead an increase in overall

town gas consumption. Consumption for residential/commercial use and public use also

indicated sound growth of 4.9%.

Coal consumption dropped 5.5%, influenced by a decrease (-15.1%) in bituminous coal

consumption for steel making in the first quarter. It turned around afterwards and

indicated a year-on-year rise of 4.2%.

Electricity consumption recorded year-on-year growth of 5.5%, attributable to continued

strong consumption of electricity for industrial use (year-on-year rise of 9.3%).

Level of contribution of each final energy source to an increase in primary energy

consumption from January through October 2011

- The level of contribution of electricity(triggering energy consumption for power

13http://www.keei.re.kr

Summary

3) The added value of each business type under the manufacturing industry is announced by quarter. For thisreason, an analysis of the level of contribution made to a rise in consumption is limited to January throughSeptember.

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지13 매일3 MAC2PDF_IN 600DPI 125LPI T

generation) and energy for industrial raw material use(naphtha, coking coal) stood at

41.4% and 34.8%, respectively, as a result of an upswing in production in industries

that consume great amounts of energy.

- The level of contribution made by town gas, a major source of energy for heating, was

25.0% as a result of the cold weather in the first quarter.

14 KOREA ENERGY ECONOMICS INSTITUTE

KEEI Korea Energy Demand Outlook

[Contribution rate of each energy source to primary energy increase from January through October 2011]

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지14 매일3 MAC2PDF_IN 600DPI 125LPI T

Primary energy demand is expected to rise 3.3% in 2011 and 3.0% in 2012.

Primary energy demand from 2011 to 2012 is expected to become stabilized due to a

slowdown in the nation’s economic growth.

* Economic growth rate assumption: (Year 2010) 6.2% → (Year 2011) 3.8% → (Year

2012) 3.7%

Notes: Values in parentheses refer to the year-on-year growth rate (%); p refers to tentative figures; e refers to forecasts.

15http://www.keei.re.kr

Summary

Outlook on primary energy demand

Category2011 2012

1/4p 2/4p 3/4p 4/4e Annual (e) First half of the year (e)

Second halfof the year (e) Annual (e)

30.4 28.8 32.2 31.5 122.9 60.8 64.6 125.4(-0.8) (3.1) (6.4) (3.3) (3.0) (2.7) (1.4) (2.0)

24.2 22.3 25.8 25.0 97.3 47.4 51.0 98.4(3.7) (2.6) (5.6) (2.7) (3.7) (2.1) (0.4) (1.2)

205.0 181.5 199.3 211.8 797.7 392.9 410.5 803.5(3.1) (-6.2) (4.0) (0.7) (0.4) (1.7) (-0.2) (0.7)

116.3 97.7 108.7 122.2 444.8 214.9 225.8 440.7(-1.2) (-12.3) (-0.1) (-2.1) (-3.8) (0.4) (-2.2) (-0.9)

12.2 7.3 6.3 10.6 36.4 20.2 18.0 38.2(11.3) (9.1) (10.3) (9.4) (10.1) (3.4) (6.7) (5.0)

1.6 1.9 3.4 1.4 8.2 3.6 4.6 8.2(27.2) (21.4) (44.5) (3.2) (27.0) (4.8) (-2.9) (0.3)

37.5 38.6 38.2 40.1 154.4 82.2 86.4 168.6(4.0) (5.8) (1.7) (4.1) (3.9) (8.0) (10.3) (9.2)

1.5 1.5 1.5 1.7 6.2 3.3 3.4 6.7(2.9) (0.8) (-3.9) (11.0) (2.7) (7.1) (6.7) (6.9)

72.2 61.9 65.1 72.3 271.4 138.3 141.3 279.6(3.8) (0.5) (5.3) (3.7) (3.3) (3.2) (2.9) (3.0)

56.4 46.6 49.0 56.2 208.3 106.2 108.2 214.4

(4.6) (-0.3) (4.0) (3.3) (2.9) (3.1) (2.8) (2.9)

<Outlook on primary energy demand>

Coal(Million ton)

-Excludingcoking coal

Oil(Million bbl)

-Excludingnaphtha

LNG(Million ton)

Hydro(TWh)

Nuclear power(TWh)

Other(Million TOE)

Primary energy(Million TOE)

Primary energy-Excludingfor raw materials

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지15 매일3 MAC2PDF_IN 600DPI 125LPI T

Major energy sources for power generation, including nuclear energy and LNG, are

forecast to indicate a relatively high increase in demand, attributable to continually

strong electricity demand and the operation of new nuclear power plants (Singori

Nuclear Power Plant Unit 2, Sinwolseong Nuclear Power Plant Unit 1).

Energy demand for raw material use (naphtha, coking coal) is expected to go up 4.6% in

2011 owing to an upswing in industrial production activities. Its level of increase will

likely drop to 3.4% in 2012, reflecting a downturn in the petrochemical industry.

- Energy for raw material use is forecast to account for 23.3% of primary energy demand

in 2012.

Forecasts on key energy indicators

The energy intensity (TOE/million won) is expected to improve from 0.252 in 2010 to

0.251 in 2011 and 0.249 in 2012.

- The energy intensity deteriorated temporarily in 2009 and 2010, but is expected to turn

around and improve starting from 2011.

Per-capita energy consumption is forecast to rise from 5.37 TOE in 2010 to 5.54 TOE in

2011 and 5.70 TOE in 2012.

Notes: e refers to forecasts.

Forecasts on primary energy demand by energy source

Coal demand is expected to increase 3.0% in 2011 and 2.0% in 2012.

16 KOREA ENERGY ECONOMICS INSTITUTE

KEEI Korea Energy Demand Outlook

Category 2005 2006 2007 2008 2009 2010 2011e 2012e

Economic growth rate (%) 4.0 5.2 5.1 2.3 0.3 6.2 3.8 3.7

Primary energy consumption3.8 2.1 1.3 1.8 1.1 7.9 3.3 3.0 increase rate (%)

Energy intensity (TOE/Million won) 0.264 0.256 0.247 0.246 0.248 0.252 0.251 0.249

Per capita consumption (TOE) 4.75 4.83 4.88 4.95 4.99 5.37 5.54 5.70

<Key indices related to energy consumption>

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지16 매일3 MAC2PDF_IN 600DPI 125LPI T

17http://www.keei.re.kr

Summary

- In 2011, coal demand is expected to show gradual growth of approximately 3.0%,

attributable to a slowdown in coal consumption for power generation (no new

facilities) and base effects from a high increase in coking coal consumption (22.6%) in

the previous year.

- In 2012, coal consumption for power generation is expected to show little change since

no new facilities were built. Coking coal consumption is expected to turn around and

indicate an upward trend in 2012.

Oil demand is expected to indicate extremely gradual growth of 0.4% in 2011 and 0.7%

in 2012.

- In 2011, oil demand is expected to indicate little change despite a rapid rise (6.4%) in

naphtha consumption for raw material use. This is owing to a considerable drop in

demand for use as industrial fuel as a result of continued high oil prices and demand for

heating in the residential and commercial sector.

- A 0.7% rise from 2011 is expected for 2012 to reach 803.5 million barrels, owing to

recovery of demand for transport and a slowdown in the downward trend in fuel for

industrial use.

LNG demand is forecast to record growth of 10.1% in 2011 and 5.0% in 2012.

- LNG demand for power generation, which accounted for 46% of overall consumption

in 2010, is expected to rise 12.5% in 2011 and 5.1% in 2012, thus leading an overall

increase in LNG demand.

- LNG demand for power generation and demand for town gas production both go up in

case of an abnormal cold wave in the winter. For this reason, there is a need to

thoroughly examine LNG supply and demand conditions in the winter.

The amount of nuclear power generation is forecast to go up 3.9% in 2011 and 9.2% in

2012 with the operation of new facilities.

- Following the operation of Singori Unit 1 in (February) 2011, commercial operation of

Singori Unit 2 and Sinwolseong Unit 1 is planned for early 2012.

- At the end of 2012, there will likely be a substantial rise in the amount of nuclear

power generation in tandem with facility expansion of around 2 million kW(10.7%)

from the previous year.

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지17 매일3 MAC2PDF_IN 600DPI 125LPI T

Final energy demand is forecast to record a year-on-year increase of 3.1% in 2011 and

2.9% in 2012.

Energy consumption soared in all demand sectors in 2010. However, the level of

consumption increase is expected to slow down from 2011 to 2012 due to base effects, a

slowdown in economic growth, and continued high oil prices.

- In 2011, consumption in the industrial sector is expected to record relatively high

growth of 4.6%, but consumption in the residential/commercial/public sector and

transport sector is forecast to go up only by a small extent.

- In 2012, the level of increase in demand in the industrial sector is expected to go down

compared to the previous year as a result of a slowdown in the level of increase in

demand for naphtha and electricity for industrial use. The level of increase in demand

in the residential/commercial/public sector is also forecast to be more gradual.

18 KOREA ENERGY ECONOMICS INSTITUTE

KEEI Korea Energy Demand Outlook

Outlook on final energy demand

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지18 매일3 MAC2PDF_IN 600DPI 125LPI T

Notes: Values in parentheses are the year-on-year growth rate (%); p refers to tentative figures; e refers to forecasts.

19http://www.keei.re.kr

Summary

Category2011 2012

1/4p 2/4p 3/4p 4/4e Annual (e) First half of the year (e)

Second halfof the year (e) Annual (e)

29.7 29.0 30.1 31.6 120.5 61.8 63.7 125.4(2.4) (1.8) (8.4) (6.0) (4.6) (5.1) (3.2) (4.1)

14.0 13.7 14.0 15.6 57.3 29.6 30.5 60.2(3.9) (0.4) (7.2) (6.8) (4.6) (6.8) (3.2) (4.9)

8.8 8.7 9.8 9.7 37.0 17.8 19.6 37.3(2.8) (-5.8) (2.6) (1.7) (0.3) (1.2) (0.4) (0.8)

15.3 8.4 7.2 11.5 42.4 24.0 19.0 42.9

(5.3) (-2.7) (2.0) (0.1) (1.6) (1.1) (1.3) (1.2)

53.8 46.2 47.0 52.9 199.9 103.5 102.2 205.7(3.3) (-0.6) (6.1) (3.8) (3.1) (3.5) (2.3) (2.9)

38.1 30.9 31.0 36.9 136.8 71.4 69.1 140.4

(4.2) (-2.3) (4.5) (3.3) (2.5) (4.7) (5.7) (2.7)

8.1 4.5 3.0 5.9 21.5 13.4 9.3 22.6(6.2) (5.5) (14.8) (8.2) (7.7) (5.9) (3.9) (5.1)

194.7 178.1 195.7 206.0 774.4 380.2 401.1 781.3(3.1) (-5.1) (4.8) (0.8) (0.9) (2.0) (-0.1) (0.9)

106.0 94.2 105.0 116.3 421.5 202.2 216.5 418.7(-1.5) (-10.8) (1.3) (-0.2) (-3.2) (1.0) (8.7) (-0.7)

121.4 109.0 112.5 113.7 456.6 237.9 239.3 477.3(7.9) (5.1) (3.2) (4.4) (5.2) (3.3) (5.8) (4.5)

10.6 10.7 10.7 11.7 43.7 22.7 23.3 46.0(-5.5) (3.0) (13.0) (9.6) (4.6) (6.4) (4.1) (5.2)

4.4 4.2 4.3 5.2 18.1 9.4 9.7 19.1(12.5) (-0.1) (17.9) (14.5) (11.0) (8.9) (2.3) (5.5)

2,203 1,612 1,417 2,163 7,395 3,991 3,768 7,758

(4.2) (3.6) (0.6) (9.0) (4.7) (4.6) (5.2) (4.9)

<Outlook on final energy demand>

Industry(Million TOE)

-Excluding forraw materials

Transport(Million TOE)

Residential/commercial/public

(Million TOE)

TotalMillion TOE

Total-Excluding forraw materials

Town gas(Billion m3)

Oil(Million bbl)

-Excludingnaphtha

Electricity(TWh)

Coal(Million ton)

--Excludingcoking coal

Thermal andother

(Thousand TOE)

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지19 매일3 MAC2PDF_IN 600DPI 125LPI T

With regards to final energy demand by energy source, the level of increase recorded by

major energy sources in 2012 will likely maintain the 2011 level or slightly slow down.

Town gas for industrial use is forecast to lead an overall rise in demand. The demand

increase rate is forecast to stand at 7.7% in 2011 and 5.1% in 2012.

Oil demand is forecast to indicate an increase rate of less than 1% in both 2011 and 2012.

- Oil demand for transport is expected to go up 0.1% in 2011 and 0.4% in 2012 despite

continued high oil prices. This is attributable to a steady rise in automobile sales, a rise

in fuel demand for road freight since the second half of 2011, and an increase in

international transport.

- Oil demand in the industrial sector is forecast to go up 2.2% in 2011 and 2.0% in 2012.

Demand for industrial raw material use is expected to lead a rise in overall demand as it

is forecast that there will be an increase in production activities in the petroleum

refining and petrochemical sector in 2012 as well.

Electricity will likely indicate relatively high growth of 5.2% in 2011 and 4.5% in 2012

resulting from several factors: a rise in industrial production activities, low charge,

increased dissemination of equipment that use electricity, and convenience in use.

Coal consumption is forecast to record a sound increase rate that is in the low 5% range

in 2012 as it is expected that the high growth in anthracite demand for industrial use will

continue and coking coal demand will bounce back and slightly go up.

Forecasts on level of contribution made by each final energy source to primary energy

demand

Electricity, which triggers energy input for power generation in the transformation sector,

is forecast to contribute to around half of the amount of primary energy increase

recorded in 2012.

The level of contribution made by energy demand for industrial raw material use is

expected to slightly go down from the 2011 level to stand at 25.9% in 2012.

The level of contribution made by town gas is expected to be 14.7% in 2012. Final

petroleum products for fuel, excluding naphtha, are expected to contribute to a 3.8%

reduction in primary energy demand as decreased consumption is expected in 2012.

20 KOREA ENERGY ECONOMICS INSTITUTE

KEEI Korea Energy Demand Outlook

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지20 매일3 MAC2PDF_IN 600DPI 125LPI T

From January through October 2011, primary energy consumption rose 3.3%, recording a

lower increase rate than the economic growth rate (3.7%) from the first through the third

quarter of 2011.

From January through October, primary energy consumption indicated gradual growth

as the level of economic growth somewhat slowed down. This is despite a rise in energy

demand for heating purposes owing to the record-breaking cold wave in January.

A soar in international oil prices and strengthening of energy-saving policies contributed

to the stabilization of energy consumption.

The speed of industrial production increase (7.4%) exceeded the level of economic

growth (3.7%). Energy consumption for industrial use (4.6% increase) led a rise in

primary energy consumption from January through October.

21http://www.keei.re.kr

Summary

[Forecasts on contribution rate of each energy source to increase in primary energy]

Major characteristics

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지21 매일3 MAC2PDF_IN 600DPI 125LPI T

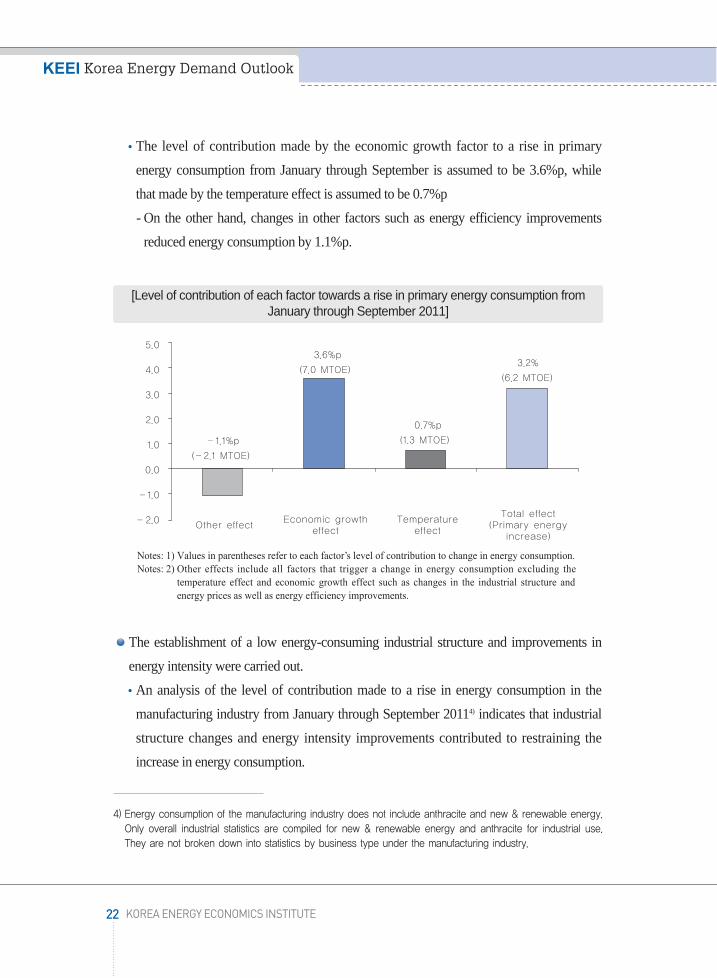

The level of contribution made by the economic growth factor to a rise in primary

energy consumption from January through September is assumed to be 3.6%p, while

that made by the temperature effect is assumed to be 0.7%p

- On the other hand, changes in other factors such as energy efficiency improvements

reduced energy consumption by 1.1%p.

Notes: 1) Values in parentheses refer to each factor’s level of contribution to change in energy consumption.Notes: 2) Other effects include all factors that trigger a change in energy consumption excluding the

temperature effect and economic growth effect such as changes in the industrial structure andenergy prices as well as energy efficiency improvements.

The establishment of a low energy-consuming industrial structure and improvements in

energy intensity were carried out.

An analysis of the level of contribution made to a rise in energy consumption in the

manufacturing industry from January through September 20114) indicates that industrial

structure changes and energy intensity improvements contributed to restraining the

increase in energy consumption.

22 KOREA ENERGY ECONOMICS INSTITUTE

KEEI Korea Energy Demand Outlook

4) Energy consumption of the manufacturing industry does not include anthracite and new & renewable energy.Only overall industrial statistics are compiled for new & renewable energy and anthracite for industrial use.They are not broken down into statistics by business type under the manufacturing industry.

[Level of contribution of each factor towards a rise in primary energy consumption fromJanuary through September 2011]

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지22 매일3 MAC2PDF_IN 600DPI 125LPI T

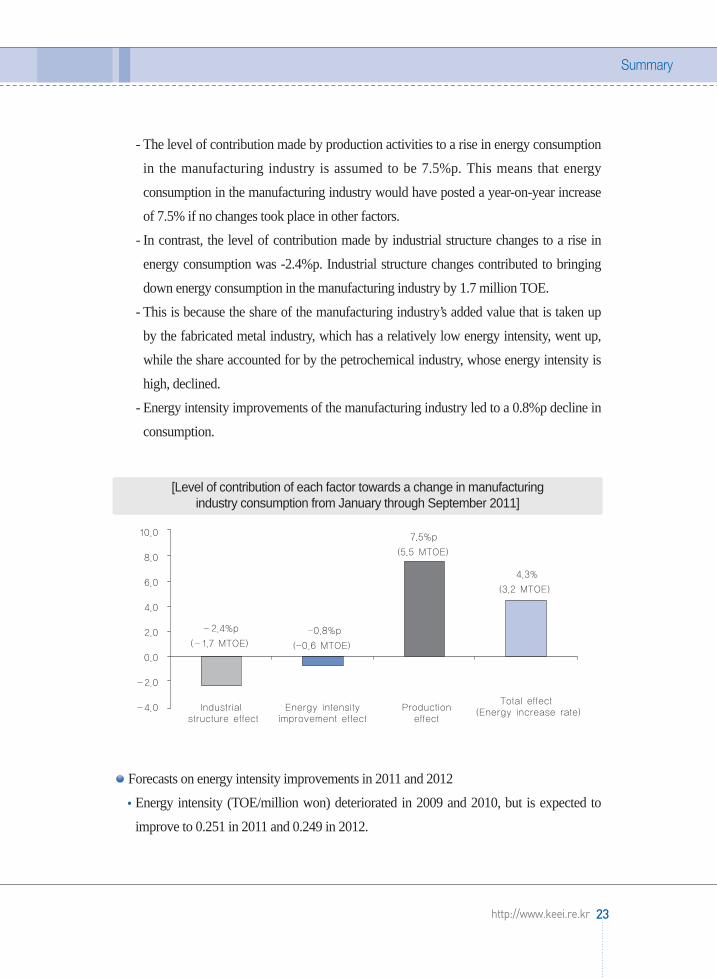

- The level of contribution made by production activities to a rise in energy consumption

in the manufacturing industry is assumed to be 7.5%p. This means that energy

consumption in the manufacturing industry would have posted a year-on-year increase

of 7.5% if no changes took place in other factors.

- In contrast, the level of contribution made by industrial structure changes to a rise in

energy consumption was -2.4%p. Industrial structure changes contributed to bringing

down energy consumption in the manufacturing industry by 1.7 million TOE.

- This is because the share of the manufacturing industry’s added value that is taken up

by the fabricated metal industry, which has a relatively low energy intensity, went up,

while the share accounted for by the petrochemical industry, whose energy intensity is

high, declined.

- Energy intensity improvements of the manufacturing industry led to a 0.8%p decline in

consumption.

Forecasts on energy intensity improvements in 2011 and 2012

Energy intensity (TOE/million won) deteriorated in 2009 and 2010, but is expected to

improve to 0.251 in 2011 and 0.249 in 2012.

23http://www.keei.re.kr

Summary

[Level of contribution of each factor towards a change in manufacturing industry consumption from January through September 2011]

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지23 매일3 MAC2PDF_IN 600DPI 125LPI T

The worsened energy intensity in 2009 and 2010 seems to be temporary amid mid- to

long-term energy efficiency improvements.

- The worsened energy intensity of 2009 resulted from the level of increase in primary

energy consumption (1.1%) exceeding the economic growth rate (0.3%), owing to

operation of new facilities in industries that consume a great amount of energy and a

rise in energy transformation loss as a result of a rapid increase in electricity

consumption5).

- The worsened energy intensity of 2010 mainly resulted from base effects from sluggish

consumption witnessed in the previous year, a soar in energy consumption for

industrial use owing to a rapid economic upswing, and an increase in energy

consumption for cooling and heating purposes as a result of abnormal climate

conditions throughout all seasons.

Continued rapid increase in electricity consumption is expected

Electricity is forecast to maintain a rapid increase in consumption due to several factors:

24 KOREA ENERGY ECONOMICS INSTITUTE

KEEI Korea Energy Demand Outlook

5) Final energy consumption went down 0.3% in 2009 but electricity consumption indicated relatively highgrowth at 2.4%.

[Forecasts on energy intensity and per-capita consumption]

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지24 매일3 MAC2PDF_IN 600DPI 125LPI T

low charge; continued upswing in production in industries that consume a great amount

of electricity; increased propagation of electric equipment; and convenience in use.

- Electricity consumption indicated annual average growth of 6.1% in the 2000s, the

highest among major final energy sources. It is forecast to record relatively rapid

growth of 5.2% in 2011 and 4.5% in 2012.

A rise in electricity consumption expands energy conversion loss, thus triggering an

increase in primary energy demand6).

- The level of contribution made by electricity towards a rise in primary energy

consumption is forecast to be 49.4% in 2011 and 50.9% in 2012. It is forecast that

around half of the primary energy increase will be accounted for by electricity demand.

- Strong electricity demand is expected to continue for the time being as a result of sound

growth of industries that consume great amounts of electricity and changes in lifestyles

triggered by technological development.

The supplied reserve level is steadily decreasing

Since 2000, peak electricity demand has been quickly increasing, faster than the speed at

which power generation facilities were built. For this reason, spare electricity is steadily

declining.

From 2000 through 2011, peak electricity demand in the summer indicated annual

average growth of 5.3%. In contrast, total capacity and supply capacity recorded an

annual average increase of a mere 4.7% and 4.9%, respectively. The supplied reserve

level in the summer substantially dropped.

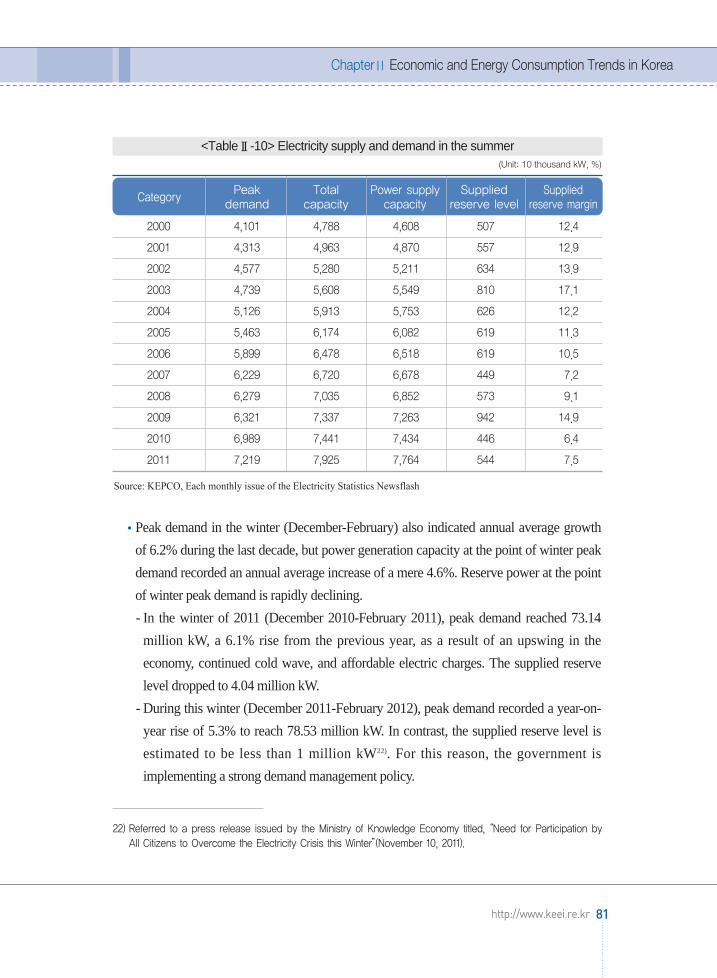

Peak demand in the winter (December - February) indicated annual average growth of

6.2% during the past decade, thus recording a faster increase rate than peak demand in

the summer. Power generation capacity at the point of winter peak demand recorded an

annual average increase of 4.6%. This means that reserve power at the point of winter

peak demand quickly went down.

25http://www.keei.re.kr

Summary

6) There is an energy loss of 63.6% in the power generation sector (as of 2010). This is why 2.74 TOE ofprimary energy is needed to produce 1 TOE of electricity.

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지25 매일3 MAC2PDF_IN 600DPI 125LPI T

Increase in the range of fluctuation in energy demand caused by temperature changes

Temperature changes have had increasing influence on changes in energy consumption

in the 2000s.

- Energy consumption is substantially influenced by temperature changes in tandem with

increased dissemination and use of cooling and heating equipment and frequent

occurrence of abnormal climate conditions.

Electricity demand in the winter is especially becoming more sensitive to temperatures

and the range of fluctuation in demand is widening in tandem with increased

dissemination of electric heating equipment.

- An analysis of how sensitive electricity demand was towards changes in HDD in a 10-

year period after 1985 (movement to recent year by one year on an annual basis)7)

indicates that electricity demand is becoming more sensitive to temperatures as time

passes.

- This shows that electricity is quickly replacing oil as energy for heating.

26 KOREA ENERGY ECONOMICS INSTITUTE

KEEI Korea Energy Demand Outlook

7) Sensitivity analysis model (Monthly data used): InE=α+β1InGDP+β2CDD+β3HDD+e(E refers to electricity, CDD refers to Cooling Degree Days, HDD refers to Heating Degree Days)

[Changes in electricity demand sensitivity for temperatures]

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지26 매일3 MAC2PDF_IN 600DPI 125LPI T

Oil dependence regarding primary energy consumption is forecast to continually drop.

The share of primary energy taken up by oil decreased to less than 40% in 2010, and will

likely go down further to 37.7% in 2012.

When excluding non-energy oil for industrial raw material use (naphtha, asphalt, etc.),

the share of primary energy taken up by oil used as an energy source is expected to

decrease from 21.8% in 2010 to 19.6% in 2012.

The decrease in the Korean economy’s dependence on energy oil is the result of

continued high oil prices and relative prices among energy sources in Korea.

- A rise in oil prices has led to a slowdown in the level of increase in fuel consumption

for transport and continued downward trend in consumption for power generation. Oil

is being steadily replaced by other energy sources such as electricity.

There is a need to examine whether the speed at which the share taken up by energy oil

is dropping is appropriate when Korea establishes energy supply and demand policies.

- Considering Korea’s industrial structure, where the level of contribution of the

petrochemical industry to the economy is high, the nation’s oil dependence target

should be set targeting oil for fuel.

27http://www.keei.re.kr

Summary

[Trends in oil dependence and forecasts]

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지27 매일3 MAC2PDF_IN 600DPI 125LPI T

Continually implement measures to stabilize winter and summer electricity supply and

demand in 2012.

Due to limited expansion of base-load power generation facilities (nuclear power,

bituminous coal), electricity supply and demand conditions that were witnessed in 2011

will likely continue in 2012.

- Commercial operation is planned for two nuclear power plants (Singori Nuclear Power

Plant Unit 2, Sinwolseong Nuclear Power Plant Unit 1) in the first half of 2012, but

there are no plans for additional bituminous coal-based power generation facilities.

- Base-load power generation facility capacity (as of the end of the year) in 2012 will

record a year-on-year rise of a mere 4.8%. The level of increase will be similar to that

of electricity demand (4.5% increase).

As such, strong measures on stabilizing supply and demand need to be continually

implemented in 2012 in order to stabilize electricity supply and demand.

- There is a need to continually move forward with reform into a cost principle-based

charge system. At the same time, there is a need to come up with a mid- to long-term

roadmap that would reduce the economic shock caused by the change in the charge

system and would allow electricity consumers, including the industrial sector, to

prepare for the change.

- There is a need to examine the matter of putting off the shutdown of power plants and

engaging in early construction of new power plants in order to secure more supply

capacity between now and 2015, when there is no spare electricity.

- If needed, current electricity supply/demand stabilization measures (reduce peak

demand, place a restriction on heating temperatures, etc.) should be improved and

continually executed.

- PR activities should be strengthened so that information is delivered to the general

public on how to use electricity efficiently and the importance of reducing energy

consumption.

28 KOREA ENERGY ECONOMICS INSTITUTE

KEEI Korea Energy Demand Outlook

Policy implications

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지28 매일3 MAC2PDF_IN 600DPI 125LPI T

There is a need to pay more caution to electricity supply/demand management when there

is a change in the season.

There is a possibility that difficulties will be experienced in electricity supply in the event

of a soar in electricity demand as a result of abnormal climate conditions when there is a

change in the season.

- The shortage of reserve power in the summer and winter is forecast to continue for the

time being. Repair of power plants needs to be carried out mainly in the spring and

autumn.

- There is a possibility of power load temporarily rising in the event of simultaneous

occurrence of abnormal climate conditions and load shifting of industries when there is

a change in the season.

- In case of simultaneous occurrence of a drop in supply capacity and a rise in power

load, as such was the case on September 15, 2011, there is a possibility of imbalance

between supply and demand in the short term.

There is a need to improve Korea’s industrial structure into a low energy-consuming

structure.

Energy demand in the industrial sector rose 8.5% in 2010. It is forecast to go up 4.6% in

2011 and 4.1% in 2012, thus leading a rise in final energy consumption.

* Rate of increase in final energy demand: (’10) 6.5% → (’11) 3.1% → (’12) 2.9%

- As a result, the share of final energy accounted for by consumption in the industrial

sector is expected to continually increase and reach 61% in 2012.

The rapid increase in demand in the industrial sector is attributable to continued rapid

growth of leading industries that consume a great amount of energy, including the steel

and petrochemical industries, as well as the fabricated metal industry that mainly uses

electricity, including semiconductors, machinery, and automobiles.

- In 2010, there was a substantial rise (12.9%) in electricity demand for industrial use as

a result of construction of large steel making facilities (total capacity of 19,000

thousand tons)8) that consume a great amount of electricity, including Blast Furnace #1

and #2 of Hyundai Steel

29http://www.keei.re.kr

Summary

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지29 매일3 MAC2PDF_IN 600DPI 125LPI T

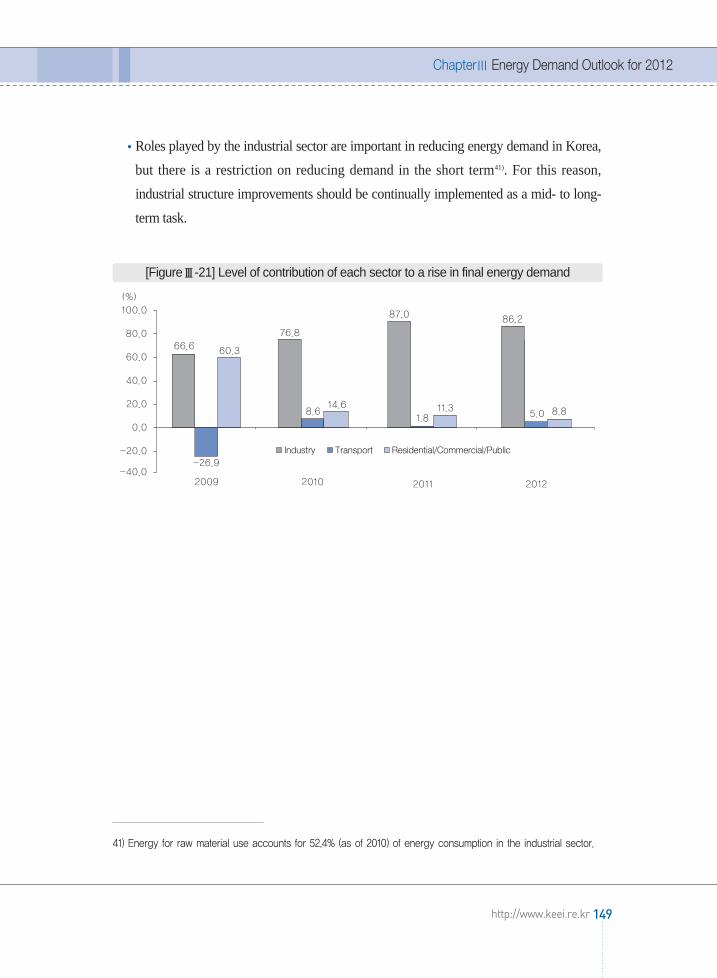

The level of contribution made by the industrial sector to a rise in final energy

consumption has been on an upward trend since 2009.

- In 2012, energy consumption in the industrial sector is expected to increase by 5.0

million TOE, accounting for 86.2% of final energy demand increase (5.8 million TOE).

The level of contribution of energy for industrial raw material use (naphtha, coking

coal) towards a rise in final energy is expected to reach 37.2%.

- In 2012, the level of contribution of the transport sector and residential/commercial and

public/other sector is forecast to be low at 5.0% and 8.8%, respectively.

Roles performed by the industrial sector are important in reducing energy demand in

Korea, but there is a restriction on reducing demand in the short term9). For this reason,

industrial structure improvements should be continually implemented as a mid- to long-

term task.

30 KOREA ENERGY ECONOMICS INSTITUTE

KEEI Korea Energy Demand Outlook

8) This accounts for 8.8% of the total steel making facility capacity (216,667 thousand tons) recorded in 2010.9) Energy for raw material use accounts for 52.4% (as of 2010) of energy consumption in the industrial sector.

[Contribution rate of each sector to a rise in final energy demand]

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지30 매일3 MAC2PDF_IN 600DPI 125LPI T

Energy Demand Outlook for 2012

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지31 매일3 MAC2PDF_IN 600DPI 125LPI T

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지32 매일3 MAC2PDF_IN 600DPI 125LPI T

ChapterⅠInternational Energy

Market Trends

1. Trends in the international oil market and oil exports/imports

2. Trends in the international natural gas market

3. Trends in the international coal market

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지33 매일3 MAC2PDF_IN 600DPI 125LPI T

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지34 매일3 MAC2PDF_IN 600DPI 125LPI T

A. Trends in international oil prices and domestic petroleum product prices

International oil prices have been indicating a downward trend since April. Despite

geopolitical tension in the Middle East and improvements in economic indicators in the

US, international oil prices recorded a 2.2% drop from the previous month to stand at

$105.5/barrel (Dubai oil) in December 2011. This is attributable to anxiety over Europe’s

financial crisis, weak manufacturing industry indicators in China, and a rise in crude oil

inventory in the US.

Notes: Values in parentheses indicate the year-on-year increase rate (%).

ChapterⅠ International Energy Market Trends

35http://www.keei.re.kr

Trends in the international oil market and oil exports/imports1

(Unit: $/Bbl, %)

Category WTI Brent Dubai

2008 99.92 (27.21) 97.47 (24.85) 94.29 (25.86)

2009 61.94 (-37.98) 61.73 (-35.74) 61.92 (-32.37)

2010 79.49 (17.55) 79.66 (17.93) 78.13 (16.21)

January 89.54 (14.30) 96.78 (26.69) 92.55 (20.59)

February 89.66 (17.28) 103.90 (40.75) 100.24 (36.20)

March 102.97 (26.73) 114.64 (45.21) 108.53 (40.33)

April 109.96 (30.13) 123.26 (45.17) 115.76 (38.40)

May 101.29 (37.42) 114.27 (51.91) 108.04 (40.60)

2011June 96.26 (27.85) 113.97 (52.12) 107.50 (45.17)

July 97.30 (27.52) 116.82 (54.32) 110.15 (51.70)

August 86.32 (12.67) 110.11 (42.68) 105.00 (41.57)

September 85.58 (13.73) 111.52 (43.23) 105.75 (40.63)

October 86.51 (5.58) 109.13 (31.20) 103.54 (28.97)

November 97.27 (15.28) 110.53 (28.90) 107.91 (29.11)

December 98.72 (10.72) 107.74 (17.41) 105.51 (18.62)

<Table Ⅰ-1> International crude oil prices

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지35 매일3 MAC2PDF_IN 600DPI 125LPI T

B. Trends in petroleum product prices in Korea

In December 2011, consumer prices of gasoline and diesel in Korea recorded a year-on-

year increase of 9.7% and 14.2%, respectively. Consumer prices of butane for vehicles

went up 8.2%.

The relative price of diesel against gasoline continually dropped after April. As of

December, it skyrocketed to 92.5%, influenced by a rise in international product prices

of diesel.

Notes: Values in parentheses indicate the relative price against gasoline prices (%).

Consumer prices of petroleum products in Korea are roughly 2.4 times (gasoline) and 2.0

times (diesel) higher than prices in the Singapore spot market around two weeks earlier.

36 KOREA ENERGY ECONOMICS INSTITUTE

KEEI Korea Energy Demand Outlook

(Unit: Won/liter, Won/kg, %)

Category Gasoline Diesel Butane for transport

2008 1,692.14 1,614.44 (95.4) 1,009.04 (59.6)

2009 1,600.72 1,397.47 (87.3) 828.70 (51.8)

2010 1,710.41 1,502.80 (87.9) 952.16 (55.7)

January 1,825.4 1,621.7 (88.8) 1,068.1 (58.5)

February 1,850.0 1,651.7 (89.3) 1,068.8 (57.8)

March 1,939.0 1,755.9 (90.6) 1,068.9 (55.1)

April 1,951.2 1,792.8 (91.9) 1,068.3 (54.8)

May 1,938.5 1,772.9 (91.5) 1,068.0 (55.1)

2011June 1,915.4 1,736.3 (90.6) 1,120.9 (58.5)

July 1,934.7 1,754.4 (90.7) 1,099.9 (56.9)

August 1,945.2 1,757.9 (90.4) 1,081.5 (55.6)

September 1,944.4 1,746.3 (89.8) 1,081.1 (55.6)

October 1,978.3 1,772.5 (89.6) 1,080.8 (54.6)

November 1,981.0 1,788.0 (90.3) 1,060.0 (53.5)

December 1,943.0 1,792.3 (92.2) 1,052.4 (54.2)

<TableⅠ-2> Consumer prices of petroleum products in Korea

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지36 매일3 MAC2PDF_IN 600DPI 125LPI T

Notes: Gasoline (92RON) and diesel (0.05%) prices were calculated by using the weekly average price of theSingapore spot market and the weekly average exchange rate.

C. Trends in crude oil and petroleum product exports/imports

In October 2011, the crude oil import volume stood at 83.0 million barrels, recording a

year-on-year rise of 8.3%. The import value (based on CIF) rose 51.4% to reach 9.02

billion dollars.

The import volume from January through October 2011 posted 773.4 million barrels, a

year-on-year rise of 7.8%, while the value posted a rise of 49.5% to stand at 83.14 billion

dollars.

Crude oil imports maintained a high level of increase from the same period of the

previous year, attributable to the Great East Japan Earthquake and the resulting upswing

in oil demand in the region as well as a continued increase in production and exports of

products, triggered by a rise in the refining margin.

From January through October 2011, petroleum product imports recorded a year-on-year

drop of 1.7% to stand at 229.0 million barrels. In contrast, petroleum product exports

ChapterⅠ International Energy Market Trends

37http://www.keei.re.kr

[FigureⅠ-1] Petroleum product import prices and consumer prices

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지37 매일3 MAC2PDF_IN 600DPI 125LPI T

witnessed a year-on-year rise of 19.6% to reach 335.4 million barrels.

Petroleum product imports went down from the same period of the previous year, owing

to a drop in naphtha imports despite a rise in LPG imports. Petroleum product exports

substantially rose as a result of improvements in the refining margin as well as the Great

East Japan Earthquake and the resulting upswing in oil demand in the region.

A. Trends in supply and demand

International natural gas demand went up 7.4% in 2010, but the level of increase slowed

down to 4.1% in 2011 to record total consumption of 3,382.2 billion m3. This is a result of

a slowdown in economic growth of OECD countries and reduced consumption in

Western Europe.

In 2010, Russia’s natural gas consumption reached 467.3 billion m3, a year-on-year

increase of 6.3%, owing to the economic recovery and cold winter. It is estimated that

consumption rose by 3.2% in 2011 to stand at 482.3 billion m3.

Europe’s consumption of natural gas increased 7.5% in 2010, but declined 2.5% in 2011

to stand at 573.5 billion m3, owing to weak economic activity in the eurozone and warm

winter temperatures.

Natural gas consumption in Asia recorded a year-on-year rise of 11.8% to reach 639.1

billion m3 in 2011, attributable to increased consumption in Korea (12.6%), Japan

(10.9%), China (23.3%), and India (18.9%).

International natural gas production went up 7.2% in 2010 to 3,232.1 billion m3, but the

rate of growth slightly went down in 2011 as a result of reduced production in Europe. It

38 KOREA ENERGY ECONOMICS INSTITUTE

KEEI Korea Energy Demand Outlook

Trends in the international natural gas market2

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지38 매일3 MAC2PDF_IN 600DPI 125LPI T

posted year-on-year growth of 4.5% to stand at 3,376.2 billion m3.

In 2011, the US produced 621.9 billion m3 of natural gas, a year-on-year increase of

6.7%, resulting from increased production in the interior regions. Production in Canada

continually went down but turned around and indicated a year-on-year rise of 2.0% to

post 155.4 billion m3.

Natural gas production in Western Europe indicated a downward trend for a long period,

but turned around in 2010 and posted a year-on-year increase of 2.5% to record 305.2

billion m3, owing to increased production in the Netherlands (8.0%) and Norway (2.8%).

However, it dropped 4.5% year-on-year to stand at 291.5 billion m3 in 2011.

Qatar, which is the largest LNG-producing country, indicated high production increase

of 30.7% in 2010. Natural gas production also went up 29.6% in 2011 to reach 151.2

billion m3.

Notes: Values in parentheses indicate the year-on-year growth rate (%), p indicates tentative valuesSource: EIU, World commodity forecasts: Industrial raw materials, January 2012

B. Price trends

The US Henry hub natural gas price began to decline in the second quarter of 2011 as a

result of abundant supply and a warm winter. The annual average price dropped 5.0%

year-on-year to stand at 4.17US$/mBtu.

ChapterⅠ International Energy Market Trends

39http://www.keei.re.kr

(Unit: Billion m3)

Category Consumption Production

2009 3,023.2 (-3.7) 3,014.9 (-3.1)

2010 3,248.2 (7.4) 3,232.1 (7.2)

2011p 3,382.2 (4.1) 3,376.2 (4.5)

<TableⅠ-3> Trends in international natural gas supply and demand

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지39 매일3 MAC2PDF_IN 600DPI 125LPI T

Notes: 1) Values in parentheses indicate the year-on-year growth rate (%), p indicates tentative values.2) Natural gas prices for the US are based on Henry hub, while prices for Europe (excluding the UK) are based

on import border prices. Prices for Japan are LNG import prices. Source: EIU, World commodity forecasts: Industrial raw materials, January 2012

Europe’s natural gas prices continually went up starting from the second quarter of 2010.

In 2011, a year-on-year increase of 25.6% was recorded to reach 10.41US$/mBtu.

Japan’s LNG import prices indicated high year-on-year growth of 21.4% in 2010. In 2011,

Japan’s LNG import prices went up 35.32% to post US$ 14.68/mBtu.

Notes: Natural gas prices for the US are based on Henry hub, while prices for Europe (excluding the UK) arebased on import border prices. Prices for Japan are LNG import prices.

Source: World Bank Commodity Price Data

40 KOREA ENERGY ECONOMICS INSTITUTE

KEEI Korea Energy Demand Outlook

(Unit: US$/mBtu)

Category2010 2011Annual 1/4 2/4 3/4 4/4p Annual (p)

US4.39 4.18 4.37 4.12 4.00 4.17(11.1) (-18.8) (1.2) (-3.7) (5.3) (-5.0)

Europe8.29 9.45 10.31 10.88 11.00 10.41(-4.8) (6.9) (37.3) (31.7) (28.8) (25.6)

Japan10.85 11.99 13.71 16.37 16.65 14.68(21.4) (16.2) (25.2) (45.9) (52.6) (35.3)

<TableⅠ-4> Trends in international natural gas prices

[FigureⅠ-2] Trends in international natural gas prices

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지40 매일3 MAC2PDF_IN 600DPI 125LPI T

International coal prices have been continuing an upward trend since March 2009 owing

to a rise in demand resulting from the global economic recovery. During the last winter

season, international coal prices remained strong, resulting from localized heavy rain in

coal exporting countries and an abnormal cold wave in the northern hemisphere.

What mainly led the rise in prices was the demand in emerging Asian countries such as

China and India.

- Accounting for 46% of global coal consumption, China shifted into a pure importer of

steam coal in 2007. It imported 90 million tons in 2010, and became the world’s No. 2

steam coal importer, following Japan.

- It is assumed that coal consumption in China went up 8% in 2011.

- India witnessed a rise in imports in tandem with a 10.8% increase in coal consumption

in 2010. It imported 45 million tons in 2010 (world’s No. 5 importer).

- It is assumed that India’s coal consumption recorded a year-on-year rise of 8.6% in

2011, resulting in a rapid rise in imports.

ChapterⅠ International Energy Market Trends

41http://www.keei.re.kr

Trends in the international coal market3

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지41 매일3 MAC2PDF_IN 600DPI 125LPI T

Notes: Values in parentheses indicate the year-on-year growth rate. e refers to forecasts.Source: EIU, World commodity forecasts: Industrial raw materials, January 2012

The rise in prices at the end of 2010 and early 2011 is mainly attributable to heavy

rainfall in coal exporting countries and an abnormal cold wave in the northern

hemisphere.

- La Nina caused localized heavy rain in major coal exporting countries - Australia,

Indonesia, Republic of South Africa, and Venezuela. This led to issues in production

and shipment.

- The abnormal cold wave in the northern hemisphere is further aggravating coal

supply/demand conditions. Strengthened export control by the Indonesian government

and a rise in railroad freight charges in the Republic of South Africa also contributed to

the rise in prices.

- The Great East Japan Earthquake in March 2011 resulted in a rise in demand for steam

coal as a replacement for nuclear power generation, leading to continued high prices.

42 KOREA ENERGY ECONOMICS INSTITUTE

KEEI Korea Energy Demand Outlook

(Unit: Million tons)

Category 2009 2010 2011e

China3,152 3,387 3,658(15.6) (7.5) (8.0)

US908 951 937(-10.7) (4.7) (-1.5)

EU719 718 754(-8.6) (-0.1) (5.0)

India622 689 748(8.4) (10.8) (8.6)

Russia202 206 209(-11.0) (2.0) (1.5)

Japan165 188 186(-10.8) (13.9) (-1.1)

Global total6,874 7,289 7,681(3.2) (6.0) (5.4)

<TableⅠ-5> Trends in global coal consumption

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지42 매일3 MAC2PDF_IN 600DPI 125LPI T

Source: IMF (Primary Commodity Price)

In 2010, global coal production went up 6.2% year-on-year owing to high prices and

increased demand. It is estimated that global coal production increased 6.2% in 2011.

China and Indonesia led the increase in production, recording a 8.9% and 18.9% rise,

respectively, in 2010. It is estimated that production rose 11.0% and 10.9%, respectively, in 2011.

ChapterⅠ International Energy Market Trends

43http://www.keei.re.kr

[FigureⅠ-3] International coal price trends

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지43 매일3 MAC2PDF_IN 600DPI 125LPI T

Notes: Values in parentheses indicate the year-on-year growth rate. e refers to forecasts.Source: EIU, World commodity forecasts: Industrial raw materials, January 2012

44 KOREA ENERGY ECONOMICS INSTITUTE

KEEI Korea Energy Demand Outlook

(Unit: Million tons)

구 분 2009 2010 2011e

China3,050 3,321 3,687(8.9) (8.9) (11.0)

US973 985 980(-8.5) (1.2) (-0.5)

India555 569 557(7.6) (2.5) (-2.1)

Australia399 407 415(0.3) (2.0) (2.0)

Russia298 311 322(-2.6) (4.7) (3.5)

Indonesia302 359 398(10.2) (18.9) (10.9)

Global total6,967 7,401 7,861(2.3) (6.2) (6.2)

<TableⅠ-6> Trends in global coal production

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지44 매일3 MAC2PDF_IN 600DPI 125LPI T

ChapterⅡEconomic and Energy

Consumption Trends in Korea

1. Economic trends in Korea

2. Trends in primary energy consumption

3. Trends in final energy consumption

4. Consumption trends of petroleum product

5. Trends in electricity consumption

6. Trends in LNG and town gas consumption

7. Trends in coal and other energy consumption

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지45 매일3 MAC2PDF_IN 600DPI 125LPI T

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지46 매일3 MAC2PDF_IN 600DPI 125LPI T

Outline

According to Industry Activity Trends announced by Statistics Korea in November

2011, total industrial production went up 3.1% year-on-year in November.

- The mining/manufacturing industry, service industry, and retail sales went up from the

same month of the previous year, but slightly declined from the previous month.

The cyclical component of coincident index and leading index’s year-on-year

comparison went down from the previous month.

Production trends

Mining/manufacturing industry production went up 5.6% from the same month of the

previous year, thanks to favorable conditions in semiconductors and parts (21.7%) and in

the automobile industry (14.4%). This is despite a decline in image/sound/communication

equipment (-17.8%) and machinery and equipment (-5.0%).

The average operating rate in the manufacturing industry dropped 0.7%p from the

previous month to stand at 79.0%.

In terms of the service industry, there was a decrease in real estate/lease (-5.6%) and

association/repair/personal (-0.8%), but a rise in finance/insurance (5.2%),

wholesale/retail (2.2%), and health/social welfare (6.2%), etc. led to an overall increase

of 2.6% from the same month of the previous year.

Consumption trends

Retail sales witnessed a year-on-year rise of 0.5% owing to a rise in sales of durables

(5.8%), including computers/telecommunication equipment, despite a drop in quasi-

durables (-2.4%) such as clothes and nondurables (-2.0%) such as car fuel.

ChapterⅡ Economic and Energy Consumption Trends in Korea

47http://www.keei.re.kr

Economic trends in Korea10)1

10) Summary of Industry Activity Trends (November 2011) of Statistics Korea.

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지47 매일3 MAC2PDF_IN 600DPI 125LPI T

Notes: p refers to tentative figures.Source: Statistics Korea, Industrial Activity Trends (November 2011), December 2011The Bank of Korea, Economic

Statistics System (Price index)

48 KOREA ENERGY ECONOMICS INSTITUTE

KEEI Korea Energy Demand Outlook

(Compared to the same period (month) last year, %)

Category2010 2011

Annual 3/4 November 2/4 3/4 September October (p) November (p)

Production

Consumption

Investment

Prices

Sales of consumer goods(compared to the same

month (period))

Consumer prices

Producer prices

Mining/manu

facturingindustry

Production(Compared tosame month(period))

(Automobiles)

Shipment

·Exports

Inventory

Average operating rateProductioncapacity

Facility investmentindex

Domestic ordersfor machinery

Constructioncompleted in Korea

Construction orders in Korea

·Domestic demand

·Manufacturing sector( I C T )

Manufacturingindustry

Facility

Construction

16.2

16.7

25.2

23.1

14.4

11.5

18.2

17.4

81.2

7.2

6.6

25.1

11.2

-3.3

-18.7

3.0

3.8

10.9

11.2

19.1

11.3

9.9

6.6

14.5

19.1

81.2

7.8

7.5

29.3

-0.2

-6.8

-3.6

2.9

3.6

11.2

11.4

13.3

6.9

11.7

9.7

14.5

16.9

80.5

7.5

6.9

13.1

-9.2

-7.6

-48.7

3.0

4.9

7.2

7.4

10.5

12.1

7.2

3.8

11.6

10.0

81.4

5.8

5.7

4.8

8.2

-6.6

-3.3

4.0

6.4

5.1

5.1

5.4

16.2

5.0

2.6

7.9

10.7

81.3

3.9

4.4

-3.5

1.3

-8.4

0.9

4.3

6.2

6.9

7.0

10.1

15.5

7.5

4.2

11.8

10.7

81.3

3.8

2.8

-4.1

3.3

-0.9

-5.0

3.8

5.7

6.3

6.5

17.1

12.0

4.3

0.5

9.2

14.6

79.7

4.0

2.2

-11.4

15.7

2.7

56.3

3.6

5.6

5.6

5.9

13.4

14.4

3.0

-0.9

8.0

18.4

79.0

4.0

0.5

-3.7

31.5

-8.6

15.0

4.2

5.1

<TableⅡ-1> Recent economic trends

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지48 매일3 MAC2PDF_IN 600DPI 125LPI T

- In terms of different retail business types, there was a decrease in department stores and

specialized retail stores, but a rise in convenience stores, nonstore retailing, and large

discount stores.

Investment trends

Facility investments saw a year-on-year drop of 3.7% due to a decrease in investments in

general machinery and automobiles, despite an increase in investments in precision

instruments and other transportation equipment.

The number of domestic orders for machinery went up 31.5% year-on-year, attributable

to a rise in orders in the electricity industry in the public sector, as well as the electronics

and image/sound/communication equipment manufacturing industry and

telecommunications industry in the private sector.

Completed construction witnessed a year-on-year drop of 8.6% owing to decreased

performance in construction and public works.

Construction orders (at current prices) posted a year-on-year rise of 15.0%, owing to

increased orders in the public sector for apartment houses, public offices, roads, and

power generation; and in the private sector for commercial buildings, plants, and

communication.

Business indices

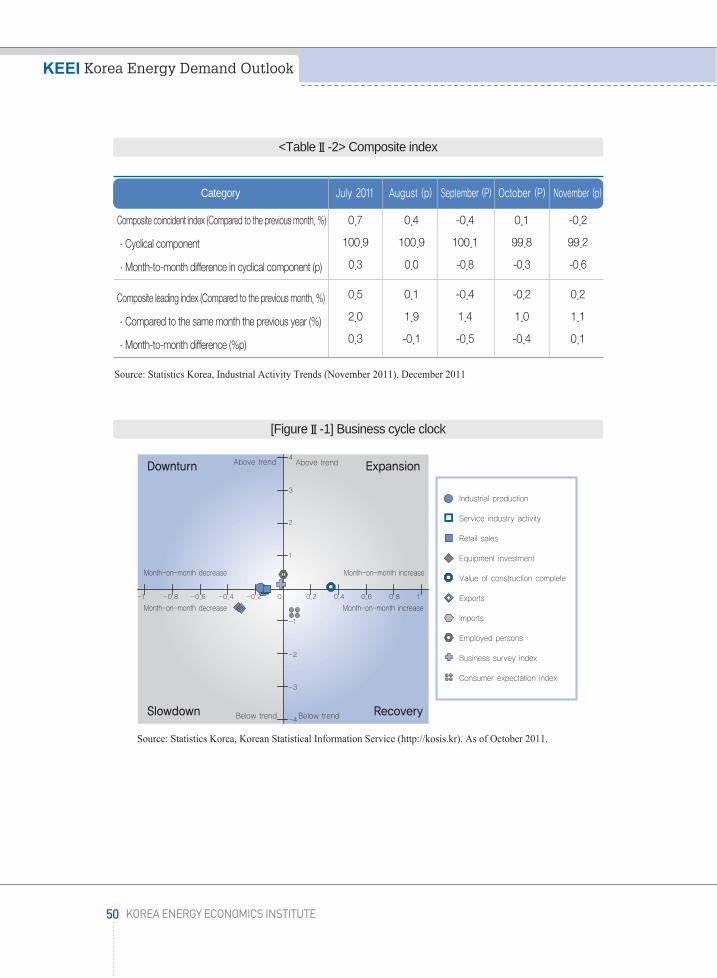

The cyclical component of coincident index went down 0.6p from the previous month,

attributable to a drop in service industry activity, domestic shipment index, and import

value.

The leading index’s year-on-year comparison, which is indicative of future economic

conditions, recorded a 0.1%p increase from the previous month, owing to a rise in the

consumer expectation index, value of orders made for machinery, and liquidity of

financial institutions, despite a drop in the value of construction orders, inventory cycle

index, and net barter terms of trade.

ChapterⅡ Economic and Energy Consumption Trends in Korea

49http://www.keei.re.kr

수요전망 내지13-4 문 2012.3.8 4:2 PM 페이지49 매일3 MAC2PDF_IN 600DPI 125LPI T

Source: Statistics Korea, Industrial Activity Trends (November 2011), December 2011

Source: Statistics Korea, Korean Statistical Information Service (http://kosis.kr). As of October 2011.

50 KOREA ENERGY ECONOMICS INSTITUTE

KEEI Korea Energy Demand Outlook