APMH & Associates LLPChar te red Accountants

KSA VAT IN ASNAPSHOT

APMH & Associates LLPChar te red Accountants

• Legal Framework

• Understanding VAT Model

• A Quick Guide to VAT Registration

• Rates and Input Credit Mechanism

• What is Supply?

• Intra GCC Transactions

• VAT Periodical Compliance

• Transition for Ongoing Contracts

• VAT Impact Areas

• VAT Implementation Roadmap

• GST Implementation Success Story (In India)

• VAT Advisory

Legal Framework forVAT in KSA

GCCAGREEMENT

(finalized andpublished)

VAT LAW

(final law published)VAT IMPLEMENTATION

REGULATIONS

(final regulations published)

TAX RULINGS

(as and when required)

• Sets broad principles and some mandatory elements fo

r VAT in GCC

• Each state responsible for its

own implementation and enforcement

• Prim

ary legislation for VAT in KSA which gives effect to GCC agreement

• Sets out im

plementation and compliance enforcement framework for VAT

• Secondary legislations which provide additio

nal rules and laws for in

terpretation of

GCC Agreement and VAT law

APMH & Associates LLPChar te red Accountants

Value Added Tax (VAT) Model

Manufacturer(SAR 10000 + VAT 500)

Distributor(SAR 11000 + VAT 550)

Retailer(SAR 12100 + VAT 605)

Consumer(Landed Cost SAR 12705)SAR 500

SAR 50 (550-500)SAR 55

(605 – 550)

SAR

(12100+605)

APMH & Associates LLPChar te red Accountants

VAT Impact in KSA Sales Price VAT @ 5% VAT Credit Tax to the Government

Manufacturer to Net Taxable Price 10000.00 500.00 500.00Distributor

Distributor to Net Taxable Price 110% 11000.00 550.00 500.00 50.00Retailer

Retailer to Net Taxable Price 110% 12100.00 605.00 550.00 55.00Consumer Dealer

Total 1655.00 1050.00 605.00

APMH & Associates LLPChar te red Accountants

Registration

Mandatory

Ar ticle 3 & 4

Person has residence inState/ Implementing State

a) Total Value of All supplies exceed the Mandatory Threshold (SAR 375000)”

b) Anticipated that above Threshold will exceed in next 30 Days

a) SAR 187500b) Value of Supplies not

exceeded but expenses incurred exceeded volun-tary threshold limit

If he makes

A) Supplies of goods or services and

B) No other person is obligated to pay the due tax on these supplies

No threshold limit

Voluntary

Ar ticle 7

Person does nothave a place of residence

Threshold limit for mandatory registration as per article 50/51 of GCC Agreement

APMH & Associates LLPChar te red Accountants

Rates and Input Credit MechanismAPMH & Associates LLPChar te red Accountants

5%Input Tax

Deductible

• Standard Rate

Out of Scope (Entities + Type of Transactions

+ Supplies)

• GOVT Or activities of Government and Public authorities (article 9) • Employer , Employed or contracted persons where there is relation of employer & employees with remuneration (article 9)• Transfer in the same entity or group entity (article 18)• Issue or Supply of Voucher (article 19)

0%Input

Tax Deductible

• Expor ts of Goods from KSA (Ar ticle 32)• Services Provided to Non-GCC Residents (Ar ticle 33)• Transportation services for Goods or passengers outside the Kingdom and Supplies relating to transportation (Ar ticle 34)• Medicines and medical equipment (Ar ticle 35)

ExemptNon Deductible

• Finance Services including Life Insurance (Ar ticle 29)• Lease or license of Residential Real Estate (Ar ticle 30)

What is Supply?

DeemedSupply

SupplySupply of ServicesArticle 6 of LawArticle 5 of GCC Agreement

Exempt Supply

Supply of Goods

Supply of Goods Means• Transfer of Ownership• Transfer of right to use• Deferred transfer of

ownership

APMH & Associates LLPChar te red Accountants

Supp

ly(A

rtic

le 1

4 of

the

regu

latio

n) Supply of Goods

Reverse Charge Mechanism

Imports in the state

Supply of Services

Including Non Implementingstates of GCC region

World

Local Sale

KSA VAT

Local Purchase

Suppliers Suppliers

Import PurchaseKSA VAT payable by Importer

Zero RatedExport Sale

You

KSA VAT payable by ImporterIntra GCC purchase

Suppliers

Registered Dealer

UAE VAT payable by Importer

Intra GCC sale

KSA VATIntra GCC sale

Bran

ch T

rans

fer

No T

ax

KSA VAT

KSA Implementing StatesGCC Region

UAEUnregistered

APMH & Associates LLPChar te red Accountants Intra-GCC Transaction

VAT Periodical Compliance

Upto SAR 40MM Above SAR 40MM

Filing frequency : QuarterlyFirst filing period : Jan-Mar 2018First filing deadline : 30-April 2018

Filing frequency : MonthlyFirst filing period : Jan 2018First filing deadline : 28-Feb 2018

APMH & Associates LLPChar te red Accountants

(Article 58 of Regulation)

APMH & Associates LLPChar te red Accountants

Ongoing Contracts(Article 79 of the VAT Regulation)

1st May 2017

31st May 2017VAT is applicable from appointed date

1st Jan 2018 31st Dec 2018

15th April 2017 1st Jan 2018 31st Dec 2018

VAT is Zero Rated VAT is Applicable

* This “Zero Rating” can only be done if the customer provides a written certificate that Input Tax is able to be deducted or refunded in full on the supply

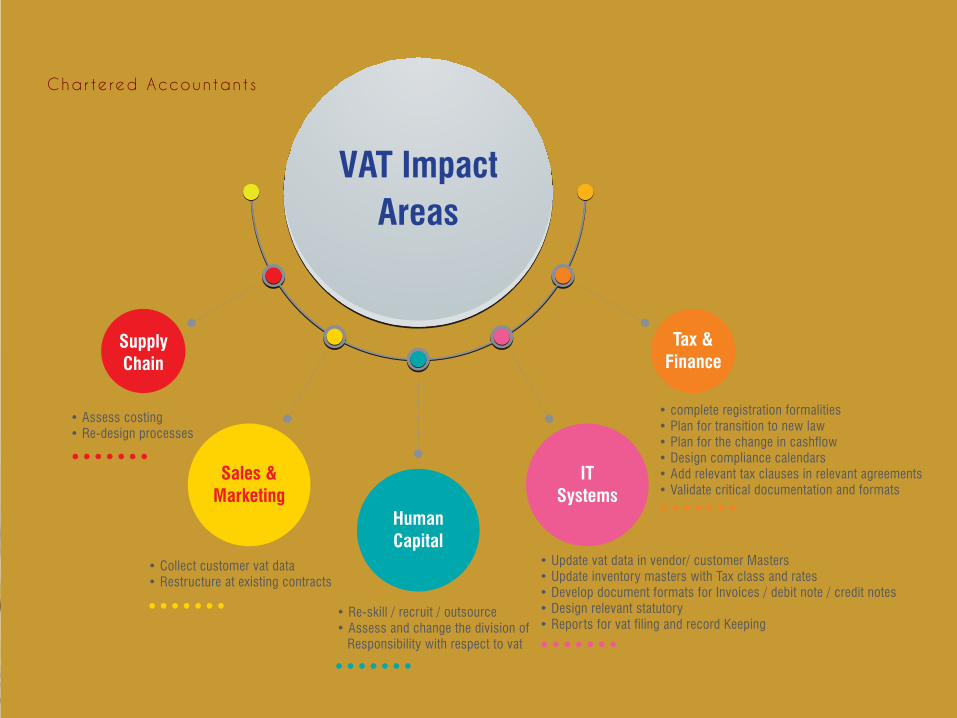

VAT ImpactAreas

• Assess costing• Re-design processes

• Collect customer vat data• Restructure at existing contracts

• complete registration formalities• Plan for transition to new law• Plan for the change in cashflow• Design compliance calendars• Add relevant tax clauses in relevant agreements• Validate critical documentation and formats

• Update vat data in vendor/ customer Masters• Update inventory masters with Tax class and rates• Develop document formats for Invoices / debit note / credit notes• Design relevant statutory• Reports for vat filing and record Keeping

• Re-skill / recruit / outsource• Assess and change the division of Responsibility with respect to vat

SupplyChain

Sales &Marketing

HumanCapital

ITSystems

Tax &Finance

APMH & Associates LLPChar te red Accountants

Post Implementation Support

• Day to day queries

• Handholding team through 3 monthly cycles of VAT filing from an offshore basis

KSA VAT Preparedness

Impact Analysis

• “As is” Study

• Suggesting Tax Optimization Scenarios

• Drawing Change Management Roadmap

PHASE-1

Implementation

• Registrations

• Policy and SOPs

• Team Training

• System Integration support

PHASE-2

• Impact in costing / pricing / cashflow due to VAT

• Objective decision making for optimizing the tax impact

• Approved implementation roadmap

• Clear operating guideline

• Team sensitization

• ERP requirement mapping

• ERP User Acceptance

Testing (UAT)

• Compliance Assurance

• Online issue resolution

• System related feedback

generation

PHASE-3

Roadmap for VAT ImplementationAc

tivity

Key

Outc

ome

APMH & Associates LLPChar te red Accountants

ImpactAnalysis

Nov. 2017 Dec. 2017 1st Jan. 2018 Feb., Mar., April 2018

ImplementationPost

Implementationsupport

GST Implementation Success Story (in India)

Multi-Nationals Trading and Distribution Manufacturing and Ancillaries

Construction and Real-estateLogisticsBanking

Engineering Hospitality Broking e-commerceSAAS

Startups Small and Medium Large

VC / PE Funded

Family Owned

APMH & Associates LLPChar te red Accountants

CA Mitesh Katira Partner APMH

CA Pranav KapadiaPartner APMH

Profile BriefMitesh is a Chartered Accountant and a ISA qualified with specialisation lies in Business Advisory Services with more than 15 years of experience. Mitesh has been focusing on Internal Compliance Outsourcing and Audits, GST implementation. He has been helping corporate and Multinationals on GST Impact Analysis, Implementation and Compliance.

Mitesh has been convenor for Information Technology Committee of the CTC i.e., Chamber of Tax Consultants. He is also a part of IT committee of the WIRC of ICAI. Mitesh has also been a Convenor of the Ghatkopar C A CPE Study Circle.

Specializations• VAT Implementation• VAT Transaction advisory• VAT compliance outsourcing• Corporate Training• Process ImplementationEducation and Certifications• Chartered Accountant• DISA - ICAI• FAFP – ICAI• Certified trainer india GST by ICAI

Profile BriefPranav’s expertise lies in GST Consulting,GST Advance Ruling, GST Transaction Advisory and GST Classification Consulting. He has been an expert consultant to large corporates with presence in Multiple States with complex structures in the Indirect Tax. Pranav lucidly deals in complex legal matters like Works Contracts (WCT), DDQ (Determination Disputed Question) now called Advance Ruling (AR), Assessments and Appeals related to VAT and Allied Tax Laws. Pranav is also an expert consultant on VAT for Corporates and Multinationals in GCC region, mainly Saudi Arabia and UAE. He is the President of The Goods & Service Tax Practitioners Association (GSTPAM) of Maharashtra. Pranav is also part of the Indirect Tax Research Committee of the WIRC of ICAI. He has been past Chairman of Indirect Tax Committee of The Chamber of Tax Consultants for 2014-15 and past Convenor of Ghatkopar CPE Study Circle of ICAI. Pranav has addressed various seminars and lectures on MVAT and CST & GST at the GSTPAM, Chamber of Tax Consultants, WIRC Study Circles of ICAI and various Industrial Associations in Mumbai and across Maharashtra. Specializations• VAT Advisory• VAT Opinion• VAT Advance RulingEducation• Chartered Accountant• DISA - ICAI

APMH & Associates LLPChar te red Accountants

APMH & Associates LLPChar te red Accountants

CA Atul MehtaSenior Partner

Profile BriefAtul focuses on accounting and taxation practice of the firm. He has exposure of more than 17 years in accounts outsourcing and tax advisory side with a specialization in GST Compliance His expertise lies in consultancy, opinions and Tax Planning for Corporates and Individuals. Atul can lucidly handle complex audits, advisory and assessment matters issues related Works Contract matters, CENVAT Credit Rules, Point of Taxation (POT) Rules, Point of Provision of Services (POPS) Rule and so on. Currently Atul is a Convenor for Indirect Taxation Committee of the Chamber of Tax Consultants. He has led the Ghatkopar CA CPE Study Circle of WIRC. Atul has Conducted Training Session organized by WIRC-ICAI and has served at WIRC ICAI Committee for Research and Development and Direct Tax Committee. Atul is appointed as the Vice Chairman of CTC IDT Committe of India.

Specializations• VAT ComplianceEducation• Chartered Accountant• DISA - ICAI

CA Amlesh GuptaManagerAPMH

Profile BriefCA Amlesh Gupta is a Chartered Accountant by profession with more than 5 yrs of experience in Tax Advisory services mainly consisting of GST Implementation and Enterprise Compliance India VAT, Service Tax, Withholding tax and GST Compliance .Amlesh has been handholding India GST Impact Analysis and GST Implementation for various service industries while India went live with GST on 1st July 2017. Apart from domain knowledge, Amlesh has brief understanding of IT Systems ,Project Management and Training Skills. Amlesh has been understanding, learning and tracking development in VAT Laws and Regulations in Saudi Arabia and other GCC Countries.

Specializations• Tax Advisory• VAT Compliances & Consulting• GST Implementation, Compliance and Consulting• Tax Technology

Education• B.Com• Chartered Accountant

APMH & Associates LLPChar te red Accountants

Mehul PawaniSenior IT ConsultantAPMH

Profile BriefMehul is an IT enthusiast with deep understanding about functional aspects of software applications computer systems, networking along with background of accounting and finance. Mehul has been attending various workshops and trainings on data analytics, excel, ethical hacking, cyber forensic, excel and so on. With his ability to understand IT and money trails ie, accounting quickly. Mehul is an expert in systems audit, vulnerability testing, application implementation, etc. Mehul has been important part of IT team of APMH for more than 3 years.

Specializations• VAT IT Implementation• Process Consultant

Mumbai : D-613/614, Neelkanth Business Park, Opp. Near Railway Station,Vidyavihar(W), Mumbai - 400 086. +91-22-2514-6854 / 55 / 56 / 57 / 58 [email protected] www.apmh.in

Get in Touch

Date of Designing : 27/10/2017

Disclaimer: Content published in this book is based on the VAT Acts, Rules and notifications from other sources believed to be reliable, but no representation or warranty is made to its accuracy, completeness or correctness. This is to simplify the legal provisions and procedural aspects of of the law keeping in mind a basic businessman and their accounting team, with the helps of simpler language and graphical representation and so may result into error or omission or interpretation differences. This document is not intended to be a substitute for professional, technical or legal advice or opinion and the contents in this document are subject to change without notice. Whilst due care has been taken in the preparation of this presentation and information contained herein, APMH accept any liability whatsoever, for any direct or consequential loss howsoever arising from any use of this document or its contents or otherwise arising in connection herewith.

APMH & Associates LLPChar te red Accountants