M&A Tax Considerations for Buyers and Sellers Evaluating Tax Issues Impacting Negotiation, Structure and Price

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

THURSDAY, SEPTEMBER 12, 2013

Presenting a live 90-minute webinar with interactive Q&A

Roger Royse, Attorney, Royse Law Firm, Palo Alto, Calif.

Jonathan Golub, Attorney, Royse Law Firm, Palo Alto, Calif.

Michael Kross, Senior Director, BDO USA, LLP, San Francisco

Tips for Optimal Quality

Sound Quality If you are listening via your computer speakers, please note that the quality of your sound will vary depending on the speed and quality of your internet connection. If the sound quality is not satisfactory and you are listening via your computer speakers, you may listen via the phone: dial 1-888-450-9970 and enter your PIN when prompted. Otherwise, please send us a chat or e-mail [email protected] immediately so we can address the problem. If you dialed in and have any difficulties during the call, press *0 for assistance. Viewing Quality To maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key again.

FOR LIVE EVENT ONLY

Continuing Education Credits

For CLE purposes, please let us know how many people are listening at your location by completing each of the following steps:

• In the chat box, type (1) your company name and (2) the number of attendees at your location

• Click the SEND button beside the box

If you have purchased Strafford CLE processing services, you must confirm your participation by completing and submitting an Official Record of Attendance (CLE Form).

You may obtain your CLE form by going to the program page and selecting the appropriate form in the PROGRAM MATERIALS box at the top right corner.

If you'd like to purchase CLE credit processing, it is available for a fee. For additional information about CLE credit processing, go to our website or call us at 1-800-926-7926 ext. 35.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please complete the following steps:

• Click on the ^ sign next to “Conference Materials” in the middle of the left-hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a PDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

M&A TAX CONSIDERATIONS FOR BUYERS AND SELLERS

Royse Law Firm, PC 1717 Embarcadero Road

Palo Alto, CA 94303 www.rroyselaw.com

IRS Circular 230 Disclosure: To ensure compliance with the requirements imposed by the IRS, we inform you that any tax advice contained in this communication, including any attachment to this communication, is not intended or written to be used, and cannot be used, by any taxpayer for the purpose of (1) avoiding penalties under the Internal Revenue Code or (2) promoting, marketing or recommending to any other person any transaction or matter addressed herein.

Roger Royse [email protected] www.rogerroyse.com

Skype: roger.royse

Jonathan Golub [email protected]

September 12, 2013

OVERVIEW OF TRANSACTIONS

• Tax Free Reorganizations: – Type A – Merger – Type B – Stock for Stock – Type C – Stock for Assets – Type D – Spin Off, Split Off, Split Up, and Type D Acquisitive Reorganizations

• Compensation Issues • Taxable Transactions:

– Stock Sale – Asset Sale

• S Corporation Strategies • Foreign Corporations

6

TAXABLE VS. TAX FREE • Type of Acquisition Currency

– Stock – Securities/Debt – Deferred payments, earn outs – Compensatory

• Nature of the Buyers and Seller – Foreign Parties – Tax Attributes of Parties

• Shareholder Level Considerations – Tax Sensitivity of Shareholders – Appetite for Complexity & Risk

7

CONTINUITY OF INTEREST

8

• IRS – 50% Safe Harbor, Rev. Proc. 77-37 • IRS – 40% in Temp. Reg. 1.368-1T(e)(2)(v), example (1) • John A. Nelson – 38% Stock • Miller v. CIR – 25% Stock • Kass v. CIR – 16% Stock is Insufficient • 2011 Regulations address changes in value between the date of

signing and close; – if fixed consideration (Consideration is “fixed” if contract states exact number of shares

and other cash or property to be exchanged) • Consideration is valued as of last business day before the first day the contract is binding and • If a portion of the fixed consideration is other property identified by value, then the specified

value is used for that portion (see Reg. 1.368-1(e)(2)). – 2011 Proposed Regulations (Prop. Reg. 1.368-1(e)(2)(vi)) – consideration that varies as

the value of issuing corporation stock changes prior to closing will not fall below (or above) contractual floor (or ceiling) markers for purposes of continuity of interest. If binding contract uses average value of issuing corporation stock that average value can be used for continuity of interest.

• Post transaction sales and redemptions

TAX FREE REORGANIZATIONS

• Type A – Merger • Type B – Stock for Stock • Type C – Stock for Assets • Type D – Spin Off, Split Off, Split Up, and Type D

Acquisitive Reorganizations • Ruling Guidelines

– Rev. Rul. 77-37 – Rev. Proc. 86-42 – Rev. Rul. 73-54 (terms) – Rev. Proc. 89-50 – Rev. Proc. 96-30 (Type D Checklist)

9

TYPE A REORGANIZATIONS – SECTION 368(a)(1)(A) STATUTORY MERGER

Requirements: • Necessary Continuity of Interest • Business Purpose • Continuity of Business Enterprise • Plan of Reorganization • Net Value Tax Effect: • Shareholders – Gain recognized to the extent of boot • Target – No gain recognition • Acquiror takes Target’s basis in assets plus gain

recognized by Shareholders • Busted Merger – taxable asset sale followed by

liquidation

• Statutory Merger – 2 or more corporations combined and only one survives (Rev. Rul. 2000-5)

• Requires strict compliance with statute

• Target can be foreign; Reg. 1.368-2(b)(1)(ii)

• No “substantially all” requirement

• No “solely for voting stock” requirement

Target Acquiror

Shareholders

10

TYPE B REORGANIZATIONS – SECTION 368(a)(1)(B) STOCK FOR STOCK

11

• Acquisition of stock of Target, by Acquiror in exchange for Acquiror voting stock

• Acquiror needs control of Target immediately after the acquisition

• Control = 80% by vote and 80% of each class

Target Acquiror

Shareholders

• Acquiror’s basis in Target stock is the same as the Shareholder’s Solely for voting stock

• No Boot in a B • Reorganization Expenses – distinguish

between Target expenses and Target Shareholder expenses (Rev. Rul. 73-54)

• Creeping B – old and cold stock purchased for cash should not be integrated with stock exchange

TYPE C REORGANIZATIONS – SECTION 368(a)(1)(C) STOCK FOR ASSETS

12

• Acquisition of substantially all of the assets of Target, by Acquiror in exchange for Acquiror voting stock

• “Substantially All” – at least 90% of FMV of Net Assets and at least 70% of FMV of Gross Assets

• Target must liquidate in the reorganization • 20% Boot Exception – Acquiror can pay

boot (non-stock) for Target assets, up to 20% of total consideration; liabilities assumed are not considered boot unless other boot exists

Target Acquiror

Shareholders

Target Assets

Acquiror Stock

Acquiror Stock

• Reorganization Expenses – Aquiror may assume expenses (Rev. Rul. 73-54)

• Assumption of stock options not boot • Bridge loans by Acquiror are boot • Redemptions and Dividends – who pays

and source of funds

TYPE D REORGANIZATIONS – SECTION 368(a)(1)(D) DIVISIVE SPIN OFF, SPLIT OFF,

SPLIT UP

13

• Divisive – transfer by a corporation of all or part of its assets to another corporation if, immediately after the transfer, the transferor or its shareholders are in control of the transferee corporation. • Stock or securities of the transferee must be distributed under the plan in a

transaction that qualifies under Section 354, 355, or 356.

Transferor Transferee

Shareholders

Transferee Stock

Transferee Stock

Transferor Assets

TYPE D REORGANIZATIONS – SECTION 368(a)(1)(D) NON-DIVISIVE

14

• If shareholders of Transferor stock receive Acquiror stock and own at least 50% of Acquiror stock, the transaction may be treated as a non-divisive D REORG even if it fails as an A REORG for lack of continuity

Transferor Acquiror

Shareholders with 20%

Acquiror Stock

Acquiror Stock

Transferor Assets Merger

Merger Treated as Acquisitive D

Failed Type C Treated as D Shareholders

Transferor Acquiror Assets

Cash & Stock

Liquidation / Reincorporation Shareholders

Transferor Acquiror

NET VALUE RULES

15

• 2005 Proposed Regulation 1.368-1(b)(1): Exchange of no net value (liabilities exceed value) does not qualify as a reorganization

• Example: – Acquiror owns all of the stock of both Merger Sub and Target. Target has assets

with FMV of $100 and liabilities of $160, all of which are owed to B. Target transfers all of its assets to S in exchange for the assumption of Target’s liabilities, and Target dissolves. The obligation to B is outstanding immediately after the transfer. Acquiror receives nothing in exchange for its Target stock.

• Explanation: – Under paragraph (f)(2)(i) of the Reg, Target does not surrender net value

because the FMV of the property transferred by Target ($100) does not exceed the sum of the amount of liabilities of Target assumed by Merger Sub in connection with the exchange ($160). Therefore, under paragraph (f) of the Reg., there is no exchange of net value. See Prop. Reg. 1.368-1(f)(5) Example 3.

• Alabama Asphalt

NON-QUALIFIED PREFERRED STOCK

16

• Preferred Stock – limited and preferred as to dividends; and does not participate in corporate growth if: – (1) shareholder has right to require issuer to redeem – (2) issuer is required to redeem – (3) issuer has right to redeem and is more likely than not to exercise that

right; or – (4) dividend rate varies based on interest rate, or commodity price or

other index • Redemption right exercisable within 20 years and not subject to

contingency that renders likelihood remote • Excludes stock compensation that may be repurchased on

separation from service • Conversion feature not enough to participate in growth • Generally treated as boot to shareholders

TRI-ANGULAR OR SUBSIDIARY MERGERS

17

2. Reverse Subsidiary Merger

Target Acquiror

Merger Sub

Acquiror Target

Merger Sub

1. Forward Subsidiary Merger

TRI-ANGULAR OR SUBSIDIARY MERGERS

18

Section 368(a)(2)(D) Forward Triangular Merger • A statutory merger of Target into Merger Sub (at least 80% owned by Merger

Sub) • Substantially all of Target’s assets acquired by Merger Sub • Would have been a good Type A merger if Target had merged into Merger

Sub

Target Acquiror

Target Shareholders

80%

Tax Consequences • Merger Sub takes Target’s

basis in assets increased by gain recognized by Target

• Acquiror takes “drop down” basis in stock of Merger Sub (same as asset basis) Merger Sub

TRI-ANGULAR OR SUBSIDIARY MERGERS

19

Section 368(a)(2)(E) Reverse Triangular Merger • Merger of Merger Sub into Target where

– (i) Target shareholders surrender control (80% of voting and nonvoting classes of stock) for Acquiror voting stock and

– (ii) Target holds substantially all the assets of Target and Merger Sub

Target Acquiror

Target Shareholders

80%

Tax Consequences • Non-taxable to Target and carryover

basis • No gain to Acquiror and Merger Sub

under Sections 1032 and 361 • No gain to Target shareholders except

to the extent of boot • Acquiror’s basis in Target stock

generally is the asset basis, but Acquiror can choose to take Target shareholders basis in stock (if it is also a B)

• If transaction is also a 351, Acquiror can use Target shareholders’ basis plus gain

Merger Sub

DOUBLE MERGER

20

Acquiror

Target Shareholders

Step 2: A-type Forward Merger Step 1: Reverse Triangular Merger

Target Acquiror

Merger Sub

Target Shareholders

80%

Tax Benefit: A taxable reverse merger has just one tax on the shareholders, while a taxable forward merger has two taxes (one on shareholders and one on corporation). Intended that entire transaction be a tax-free A-type merger (where 20% boot limitation does not exist). Pairing the two reduces the risk of incurring the corporate level tax in the event the entire transaction is not treated as an A-type merger.

REV. RUL. 2001-46

Merger Sub Target+Sub

Merger Sub Survives

DOUBLE MERGER – WHOLLY OWNED LLC

21

Target+Sub

Acquiror

LLC

Merger LLC Survives

Step 2: A-type Forward Merger Step 1: Reverse Triangular Merger

Target Acquiror

Merger Sub

Target Shareholders

80%

Tax Benefit: A taxable reverse merger has just one tax on the shareholders, while a taxable forward merger has two taxes (one on shareholders and one on corporation). Intended that entire transaction be a tax-free A-type merger (where 20% boot limitation does not exist). Pairing the two reduces the risk of incurring the corporate level tax in the event the entire transaction is not treated as an A-type merger.

REV. RUL. 2001-46

Target Shareholders

TARGET DEBT SECURITIES

22

• Exchange of Target securities for Acquiror securities is tax free under Sections 354 and 356, to the extent that the principal amount of Acquiror debt is less than the principal amount of Target debt

• Portion attributable to cash basis accrued interest is taxable

• Possible COD income – Example:

• Target bonds with an issue price (stated principal amount) of $1,000 exchanged for Acquiror stock or debt worth $900; Target has COD of $100

DIVIDEND EQUIVALENCY

23

• Section 356(a)(2) – Boot as dividend or capital gain; post-reorganization redemption test of Rev. Rul. 93-61

• Clark – hypothetical post-reorganization redemption reduced shareholder’s interest from 1.32% to .92% - substantially disproportionate under Section 302(b)(2)

• Section 302(b)(1) – redemption that results in meaningful reduction in voting power is redemption and not essentially equivalent to a dividend

• Section 302(b)(2) – greater than 20% reduction is substantially disproportionate

• E&P Limitation on Dividend – should be Target’s E&P but unclear if Merger Sub’s E&P counted; PLR 9118025, PLR 9041086, and PLR 9039029

CONTINGENT STOCK, ESCROWS, AND EARN-OUTS

24

• Escrows: – Target shareholders usually treated as owner of escrowed Acquiror shares unless

otherwise agreed – Especially true if Target shareholders have right to vote and receive dividends – Not clear who is owner if Target shareholders do not have right to vote or receive

dividends • Earn-Out Stock:

– Target shareholders not considered owners until Acquiror shares are issued – Not treated as boot – Imputed Interest

• Rev. Proc. 84-42 Ruling Guidelines – use of escrow or contingent stock – (1) stock must be distributed within 5 years, subject to escrow or contingency – (2) valid business purpose – (3) maximum number of shares cannot exceed 50% – (4) trigger event not controlled by Target shareholders and not based on tax liability – (5) Formula is objective and readily ascertainable – (6) Restrictions on assignment and substitution – (7) In the case of escrows, Acquiror shares shown as issued to Target shareholders,

current voting and dividend rights, and vested

UNVESTED STOCK RECEIVED IN A TAXABLE OR NON-TAXABLE DEAL

25

• Rev. Rul. 2007-49 - The revenue ruling addresses: – (1) the exchange of fully vested stock for unvested stock of an

acquiring corporation in a tax-free reorganization, and – (2) the exchange of fully vested stock for unvested stock of an

acquiring corporation in a taxable exchange • Under either (1) or (2), the Rev. Rul. provides that the

exchange constitutes a transfer of property subject to Section 83. – The service provider would need to file an 83(b) election to avoid

the recognition of compensation income in the future as the shares vest.

– The Rev. Rul. also provides that the spread will be zero, so there is no downside to the service provider’s 83(b) election.

OPTIONS

26

• Assumption or Substitution – No tax on substitution of NSO – No tax on substitution of ISO, so long as the substitution is

not a modification. There is no “modification” so long as: • (1) the aggregate spread in new option does not exceed the

spread in the old; and • (2) the new option does not have more favorable terms than the

old; see Sections 424(a) and 424(h)(3)

OPTIONS – CASH OUT

27

• Cancel options for cash payment – NSO

• Ordinary income – compensation – withholding or 1099 • Deduction to Target or Acquiror?

– TAM 9024002 – employer deducts based on method of accounting; not clear if cash out at close is pre-acquisition Target deduction or post-close Acquiror deduction in absence of scripting the timing

– Under the cash method, the deduction generally arises when the employer has “paid” the property to the employee. See Regs. §1.461-1(a)(1). Under the accrual method, the deduction arises when the employer's obligation to make the property transfer becomes fixed, the property's value is determinable and economic performance occurs. See Regs. §§1.461-1(a)(2) and -4(d)(2)(iii)(B)

– ISO • FICA • Exercise and disqualifying disposition treated differently

409A

28

• Deferred compensation — A deferral of compensation occurs whenever the service provider (employee) has a

legally binding right during a taxable year to compensation that will be paid to such person in a later year. Treasury Regulation Section 1.409A-1(b)

• Consequences of violating 409A — Amounts which were to be deferred are subject to immediate taxation — Additional 20% penalty on such amounts — Interest penalty — CA state tax penalty

• Bonus or Carve Out Plans • Participation in Earn Outs (Reg. 1.409A-3(i)(5)(iv))

— Payments of compensation in this context may be treated as paid at a designated date or pursuant to a schedule that complies with 409A if the transaction-based compensation is paid on the same schedule and under the same terms and conditions as apply to payments to shareholders generally pursuant to the change in control event

280G GOLDEN PARACHUTE RULES

29

• 20% excise tax and loss of deduction on Excess Parachute Payment – “Excess Parachute Payment” means the amount by which the Parachute Payment

exceeds the Base Amount – “Parachute Payment” means a payment, the present value of which, exceeds three

times the Base Amount – “Base Amount” means the average annual compensation for past 5 years – Must be paid to a disqualified individual (meaning employee, officer, shareholder,

or highly compensated individual) – As compensation, AND – Contingent on a change in control (50% change ownership or effective control, or

ownership change in a substantial portion of the company’s assets)

• Reduce Excess for reasonable compensation • Exclude reasonable compensation for future services • Exception for small business corporation and non publicly traded

corporation that has 75% uninterested shareholder approval • Withholding requirement

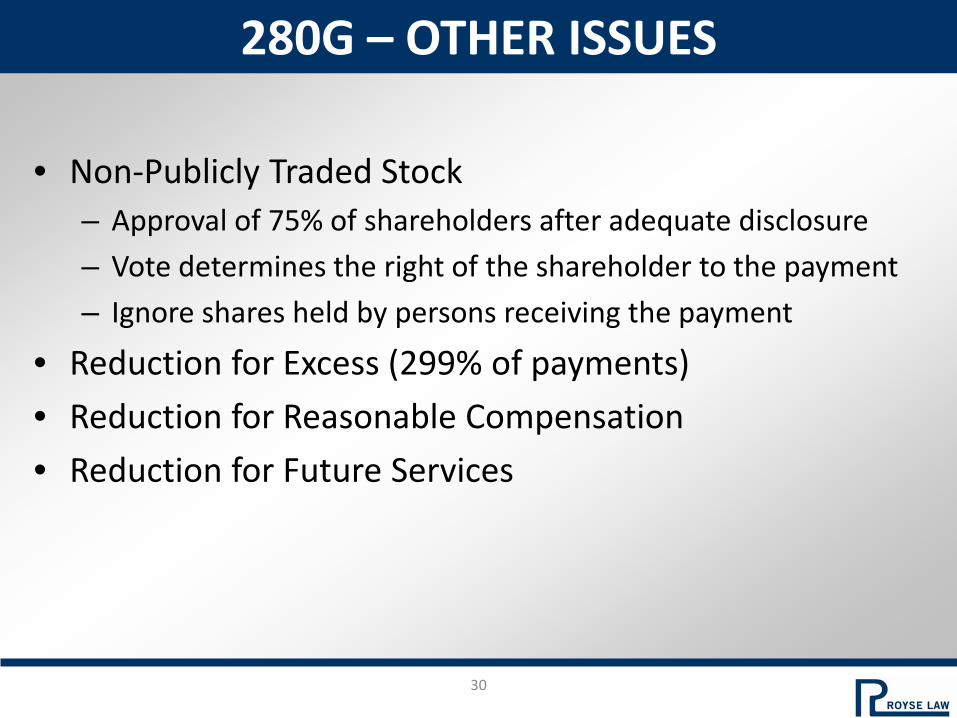

280G – OTHER ISSUES

30

• Non-Publicly Traded Stock – Approval of 75% of shareholders after adequate disclosure – Vote determines the right of the shareholder to the payment – Ignore shares held by persons receiving the payment

• Reduction for Excess (299% of payments) • Reduction for Reasonable Compensation • Reduction for Future Services

TAXABLE STOCK PURCHASES

31

Cash Reverse Triangular Merger • Treated as Stock Sale • Shareholders have gain or loss • Acquiror takes cost basis in Target shares

Merger Sub

Target Shareholders

Target Acquiror

CASH FORWARD MERGER

32

Asset Sale Followed by Liquidation of Target

• Target has gain on sale • Target shareholders have

gain on liquidation (unless 332 applies)

• Acquiror takes cost basis in Target assets

Target Shareholders

Merger Acquiror Survives

Target Shareholders

Variation with Merger Sub:

Target

Target

Acquiror

Acquiror

Merger Sub

SECTION 382 – LIMITATION ON LOSSES AFTER CHANGE IN OWNERSHIP

33

• Section 381 – Survival of Tax Attributes • Section 382

– When there has been an ownership change of a corporation with loss carry forwards, use of Net Operating Losses (NOLs) against future income is limited to the product of the value of the Target and the long term interest rate.

– “Ownership Change” occurs if, within a 3 year testing period, the percentage of stock of Target held by 5 Percent Shareholders increases by more than 50% over lowest percentage held by such shareholders during the test period.

BUSTED 351

34

Shareholders Target Shareholder

Business

Acquiror Target

Stock

Merger

Acquiror Stock

Rev. Ruling 70-140 Step 1: Incorporate Target Step 2: Merge Target into Acquiror

USE OF WHOLLY OWNED LLC

35

Target Acquiror

LLC

T Shareholders

Merger of Corporation into LLC • Reg. 1.368-2(b)(1) – by operation of law, all assets and liabilities of

Target become those of LLC, and Target ceases legal existence • A Type Reorganization

SECTION 351 / 721 ROLLOVER

36

Target

Target Shareholders

PEG

• 80% vote & value • Taxation of boot • Debt + non-qualified

voting stock • Assumption of liabilities

Cash out some and rollover

Target

Target

Target Shareholders PEG

PEG

NewCo NewCo

Target Shareholders

Target Shares

Cash

Cash

Cash

Cash

Cash Assets

Assets

LLC TECHNIQUES

37

Acquiror

Step 1 Step 2

LLC

Former Target Shareholders

Target

$

Target

Target Corp.

LLC

T Shareholders

INSTALLMENT METHOD

38

• Gain on each payment = gross profit ratio times payment – Gross profit ratio = ratio of total gain to purchase price – Pre-transaction planning opportunities to utilize basis

• Section 453A – interest charge to the extent taxpayer holds more than $5 million face amount of Section 453 obligations

• Section 453 Limits – Not available for publicly held stock or securities, or inventory – Not available for sales for demand notes or readily tradable notes – Not available for instruments secured by cash or cash equivalents – Obligor must be purchaser (cannot use parent debt)

• Section 453 applies unless taxpayer affirmatively elects out • Section 453(h) – Target shareholders who receive Acquiror debt

in liquidation of Target allowed to use installment reporting

CONTINGENT PAYMENTS AND EARN-OUTS

39

• Distinguish Equity vs. Debt • 3 Issues

– (1) allocation between interest and sales proceeds; – (2) timing of realization of sales proceeds; and – (3) timing of basis recovery

• Interest – 1.1275-4(b)

• Contingent payment debt for cash or publicly traded property – use non-contingent bond method; projected non-contingent and contingent payments

– 1.1275-4(c) • Contingent debt instrument issued for non-publicly traded property –

bifurcate into non-contingent debt instrument and contingent debt instrument; contingent payment treated as principal based on present value, excess is interest

• Buyer’s basis is non-contingent portion plus contingent payments treated as principal

CONTINGENT PAYMENTS AND GAIN RECOGNITION

40

Reg. 15A.453-1(c) • If capped by maximum amounts, assume maximum for

purposes of gross profit percentage (accelerates gain, backloads basis) – If no cap, but term, basis recovered ratably over term – If neither time nor amount is capped, basis recovered

ratably over 15 years • Election out of Section 453 – FMV of contingent

obligation is amount realized • Open transaction treatment – rare and extraordinary

situations only

SECTION 338 ELECTION

41

• Section 338(g) – Target in stock sale treated as selling all its assets followed by liquidation post close (soaks up NOLs)

• Section 338(h)(10) – Sale and liquidation deemed to occur pre-close; joint election; S corporation or sale out of a consolidated group

• Adjusted Grossed-Up Basis – New Asset basis is basis in recently purchased stock (last 12 months) grossed up to reflect minority shareholder’s basis + liabilities of Target (including taxes in 338(g))

• Adjusted Deemed Sale Price – grossed up amount realized of recently purchased stock plus liabilities of old T (on day after acquisition date)

338(g) ELECTIONS

42

• If there is a US Buyer of a foreign owned foreign target, then 338(g) election steps up basis and eliminates E&P and foreign tax credits

• Target may be able to offset 338(g) gains with NOLs

PURCHASE PRICE ALLOCATION

43

• Asset Sale or 338 Election – Sections 1060 and 338 classes based on FMV – Class I – cash and equivalents – Class II – actively traded personal property under 1092 – Class III – debt instruments and marked to market – Class IV – inventory – Class V – assets other than those in I-IV or VI – Class VI – goodwill and going concern

• Agreement Allocations – Danielson Rule – Parties bound by agreement unless IRS determines that the allocation

is NOT appropriate • SFAS 141R – Purchase Price Allocations

– Assets booked at FMV as of closing date (not signing date) – Bargain purchase results in accounting gain – Earn Outs – estimated and recorded – Deferred tax assets for excess tax deductible goodwill over book value – Transaction related costs recognized (expensed)

S CORPORATIONS AND 338(h)(10)

44

T (S Corp) Acquiror

Merger Sub

Target Shareholders

• Character difference – ordinary income assets

• California 1.5% tax on S corporations

• All Target shareholders must consent on Form 8023

• Deemed 338 election for subsidiaries

• 1374 – BIG Tax • Minority shareholders in rollover • Hidden tax in liquidation or

deemed liquidation in installment sale.

S CORP 338(h)(10) ELECTION AND 453B(h) BASIS ALLOCATION ISSUE

45

• Gain to Shareholders in year of sale: $1 million x 80% = $800,000; A/B of Shareholder = $1.8 million

• No 331 liquidation: $1 million cash decreases A/B by $1 million to $800,000; $800,000 A/B in Note = $3.2 million gain

• 331 liquidation – apportion basis: $1.8 million basis apportioned $360,000 to cash and $1,440,000 to Note; Gain in cash of $640,000 and gain in note of $2,560,000 for a total of $3.2 million gain (GP % on liquidation is 64%)

• Defer cash portion and include in installment obligation: gain on liquidation equal to zero; Shareholder A/B in note of $1 million; profit % is 80%

Target Acquiror

Shareholders

$1 million cash $4 million 453 Note

Stock Sale

$1 million basis

Cash - $1 million / $1 million A/B Assets - $4 million / zero A/B

Reg. 1.338(h)(10) – 1(e) Example 10

S CORP NO 338(h)(10) ELECTION – DISAPPEARING BASIS

46

Liquidate Target into Merger Sub or check the

box Q-Sub

T (S Corp) Acquiror

Merger Sub

T Shareholders

Carryover Basis

Section 336(e)

47

Acquiror

Shareholder $

Target Stock

Basic Model (for stock sales): Target is treated as selling all of its assets to an unrelated person while owned by its former shareholders and then reacquiring same upon acquisition by Acquiror.

$

$ Assets

Assets

= Actual Component

= Deemed Component

Acquiror Shareholder

Target Target 3rd Party

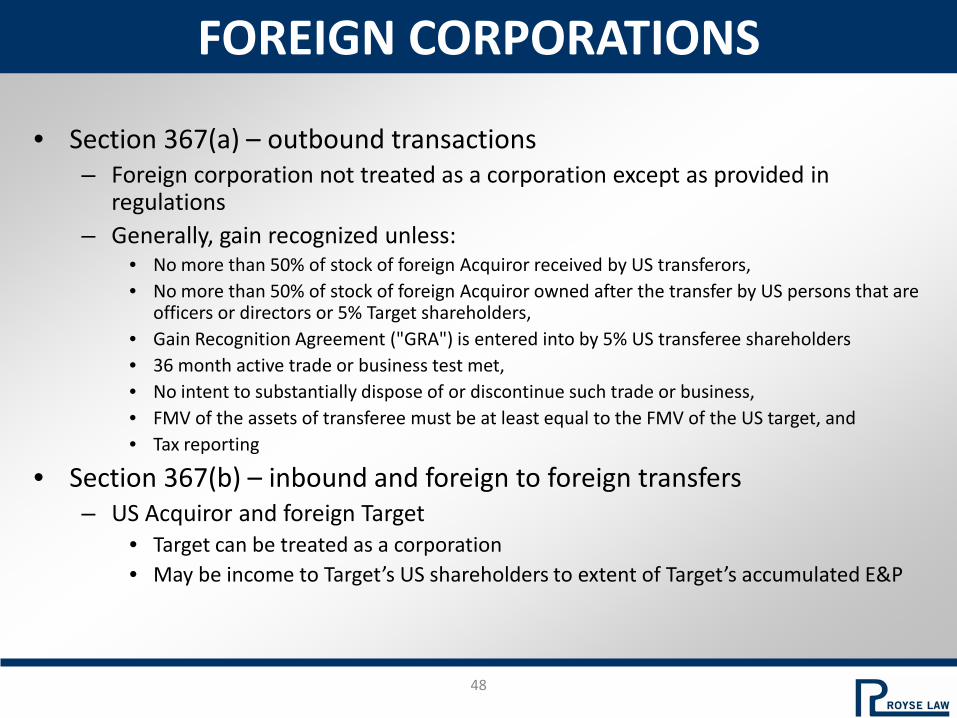

FOREIGN CORPORATIONS

48

• Section 367(a) – outbound transactions – Foreign corporation not treated as a corporation except as provided in

regulations – Generally, gain recognized unless:

• No more than 50% of stock of foreign Acquiror received by US transferors, • No more than 50% of stock of foreign Acquiror owned after the transfer by US persons that are

officers or directors or 5% Target shareholders, • Gain Recognition Agreement ("GRA") is entered into by 5% US transferee shareholders • 36 month active trade or business test met, • No intent to substantially dispose of or discontinue such trade or business, • FMV of the assets of transferee must be at least equal to the FMV of the US target, and • Tax reporting

• Section 367(b) – inbound and foreign to foreign transfers – US Acquiror and foreign Target

• Target can be treated as a corporation • May be income to Target’s US shareholders to extent of Target’s accumulated E&P

FOREIGN CORPORATIONS

49

• Anti-Inversion Rules – tax outbound reorganization and/or tax foreign Acquiror as a U.S. taxpayer; Code Section 7874 – If ownership of former U.S. Target shareholders in foreign Acquiror is 80% or

more; foreign Acquiror is treated as a U.S. company – If ownership continuity is between 60-80%; foreign Acquiror is NOT treated as a

U.S. company, but U.S. tax attributes cannot be used to offset gains – 20% excise tax on stock-based compensation upon certain corporate inversion

transactions – 7874 exception available for companies with “substantial business activities” in

the foreign jurisdiction; facts and circumstances test compares activities of company in foreign jurisdiction with activities of company globally

• Controlled Foreign Corporations (“CFCs”) – A foreign entity is classified as a CFC if it has “United States Shareholders” who

collectively own more than 50% of the voting power or value of the company. For the purposes of the CFC rules, a “United States Shareholder” is defined as US persons holding at least a 10% interest in the foreign corporation.

1248 AMOUNT ON SALE OF CONTROLLED FOREIGN CORPORATION

50

Section 1248 • Seller of Controlled Foreign Corporation (CFC) must

treat as dividend gain to extent of E&P • 1248 inclusion carries foreign tax credits • 1248 amount determined at year end and pro rated

based on day count, so post closing events can have an effect on the 1248 amount

JOINT VENTURE STRUCTURES

51

• Section 367 Issues • Disguised Sale

US Company Foreign Company

LLC

US & Foreign Assets

52

www.rroyselaw.com

PALO ALTO 1717 Embarcadero Road

Palo Alto, CA 94303

LOS ANGELES 11150 Santa Monica Blvd.

Suite 1200 Los Angeles, CA 90025

SAN FRANCISCO 135 Main Street

12th Floor San Francisco, CA 94105

BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee, and forms part of the international BDO network of independent member firms. BDO is the brand name for the BDO network and for each of the BDO Member Firms.

M & A Tax Considerations for Buyers & Sellers Selected Tax Issues Webinar Michael Kross, CPA JD [email protected] September 12, 2013

M&A Tax Considerations for Buyers and Sellers - Selected Tax Issues Page 54

Initial Considerations

Identify Non-Tax and Tax Goals of Each Party

Understand the Economics of the Deal

Buyer’s Perspective vs. Seller’s Perspective

Types of Consideration Continuing Equity Interests?

Installment Payments (Notes/Debt/Contingent)?

M&A Tax Considerations for Buyers and Sellers - Selected Tax Issues Page 55

Basic Tax Structuring Alternatives

Taxable Stock Acquisitions

Taxable Asset Acquisitions

Tax-Free Stock Acquisitions

Tax-Free Asset Acquisitions

Tax-Free Contribution to Capital

This presentation will principally address selected tax issues with respect to taxable stock and taxable asset acquisitions.

M&A Tax Considerations for Buyers and Sellers - Selected Tax Issues Page 56

Tax Considerations in Structuring Acquisitions

Corporate Structure of Target and of Acquirer (or Acquiring Group) Type of Entity of Target such as Corporation or Partnership or LLC

Tax Treatment of Target such as C Corporation, S Corporation, Partnership or Disregarded Entity

Identity of Shareholders (i.e., Corporate, Individual, Tax-exempt)

Overlap in Ownership among Shareholders

Tax Aspects Outside Tax Basis of Stock vs. Inside Tax Basis of Assets

Built-in-Gain or Built in Loss Income or Deduction Items

Tax Attributes, such as Net Operating Losses (NOLs) and Tax Credits

M&A Tax Considerations for Buyers and Sellers - Selected Tax Issues Page 57

Tax Considerations in Structuring Acquisition

Taxable Acquisitions vs. Tax-Free Reorganizations Carry Over Basis to Buyer vs. Deferral of Gain to Seller

Taxable Stock Acquisitions vs. Taxable Asset Acquisitions with C Corporations Double Taxation of C Corporations Liquidations (since 1986 repeal of General Utilities Doctrine)

Double Taxation generally imposed on Buyers in Stock Acquisitions vs. Sellers in Asset Acquisitions

Section 338(h)(10) Elections Qualified Stock Purchase of S Corporation or Corporate Subsidiary Treated as Asset Acquisition for

Income Tax Purposes

Substance vs. Form – Step Transaction Doctrine

M&A Tax Considerations for Buyers and Sellers - Selected Tax Issues Page 58

Consolidated Return Considerations

Consolidated Return Issues when Target is Member of Consolidated Group

Deferred Intercompany Transactions

Excess Loss Accounts

Tax Sharing Agreements

Loss Carrybacks

NOL Elections

Intercompany Loans

Uniform Loss Disallowance Rules

M&A Tax Considerations for Buyers and Sellers - Selected Tax Issues Page 59

Taxable Acquisitions

Asset acquisitions, including Section 1060 Acquisitions Stock acquisitions, without Section 338(h)(10) Election Stock acquisitions, with Section 338(h)(10) Election

M&A Tax Considerations for Buyers and Sellers - Selected Tax Issues Page 60

Financial Accounting (GAAP) Verses Tax Accounting

For Financial Accounting (GAAP) purposes, purchase accounting applies and the purchase price is generally allocated among the assets of Target to determine the beginning balance sheet of the Target.

M&A Tax Considerations for Buyers and Sellers - Selected Tax Issues Page 61

Financial Accounting (GAAP) Verses Tax Accounting For Tax Accounting purposes, the treatment depends on the form of the transaction: In a Stock Acquisition of the Target, the purchase price is generally allocated

only to the stock of the Target and the Target (now owned by Acquirer) retains its existing tax balance sheet and tax attributes (pre-acquisition tax basis in assets, net operating losses (“NOL's”), credits, tax liabilities, etc.).

In an Asset Acquisition of Target, the purchase price is generally allocated to the purchased assets based on fair market values and Target (owned by Seller) retains tax attributes (NOL's, credits, tax liabilities, etc).

It is sometimes possible to elect “deemed” Asset Acquisition treatment for tax purposes in a Stock Acquisition (make an IRC “Section 338 or 338(h)(10) election”).

M&A Tax Considerations for Buyers and Sellers - Selected Tax Issues Page 62

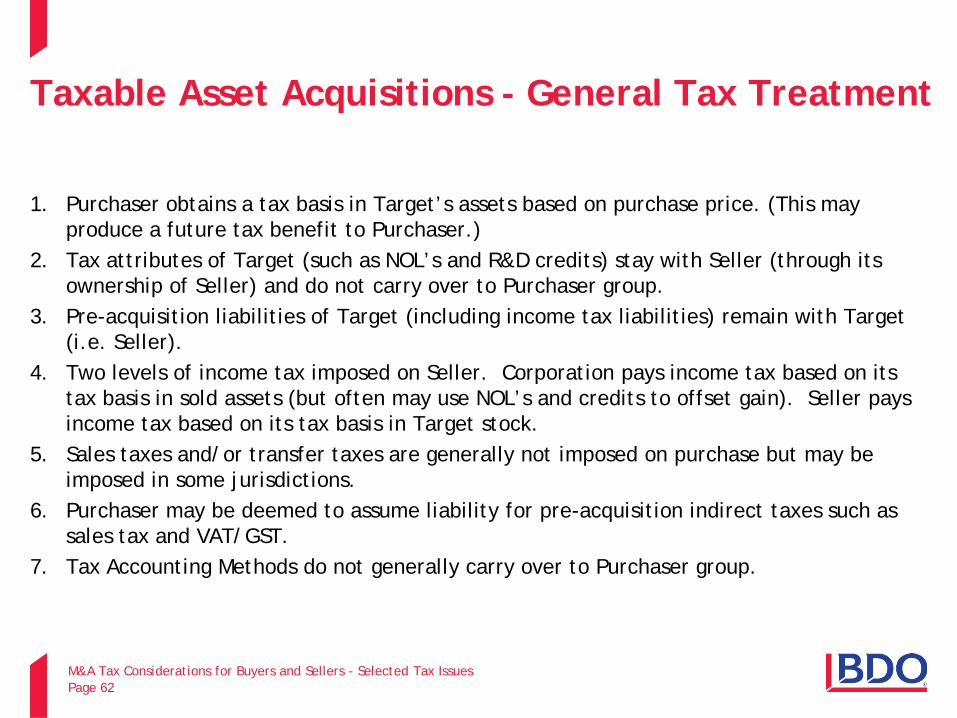

Taxable Asset Acquisitions - General Tax Treatment

1. Purchaser obtains a tax basis in Target’s assets based on purchase price. (This may produce a future tax benefit to Purchaser.)

2. Tax attributes of Target (such as NOL’s and R&D credits) stay with Seller (through its ownership of Seller) and do not carry over to Purchaser group.

3. Pre-acquisition liabilities of Target (including income tax liabilities) remain with Target (i.e. Seller).

4. Two levels of income tax imposed on Seller. Corporation pays income tax based on its tax basis in sold assets (but often may use NOL’s and credits to offset gain). Seller pays income tax based on its tax basis in Target stock.

5. Sales taxes and/or transfer taxes are generally not imposed on purchase but may be imposed in some jurisdictions.

6. Purchaser may be deemed to assume liability for pre-acquisition indirect taxes such as sales tax and VAT/GST.

7. Tax Accounting Methods do not generally carry over to Purchaser group.

M&A Tax Considerations for Buyers and Sellers - Selected Tax Issues Page 63

Tax Considerations with Taxable Asset Acquisitions

Major Tax Considerations for Seller of Assets Amount realized on disposition of each asset Overall gain or loss Character of gain or loss Timing of gain or loss recognition Tax attributes available to offset gain recognized

Major Tax Considerations for Purchaser of Assets Initial cost basis of each asset Potential additional adjustments to the tax basis of each asset due to contingent liabilities Cost recovery for each asset or category

M&A Tax Considerations for Buyers and Sellers - Selected Tax Issues Page 64

Section 1060 as It Applies to Taxable Asset Acquisitions Defined as any transfer (directly or indirectly) Of assets constituting a trade or business; and With respect to which the transferee’s basis in such assets is determined wholly by reference to the

amount of consideration paid for such assets

Consideration allocated to assets in each class subject to fair market value limitation Allocated within each class based on relative fair market values of assets No limitation applies to Class VII (residual class) Form 8594 compliance

M&A Tax Considerations for Buyers and Sellers - Selected Tax Issues Page 65

Identification of Asset Classes for Purchase Price Allocation to Assets under Section 1060

Class I - cash and cash equivalents Class II - marketable securities Class III - accounts receivable Class IV - inventories and other property held for sale to customers Class V - all other assets Class VI - section 197 intangible assets other than Class VII assets Class VII - goodwill and going concern value

M&A Tax Considerations for Buyers and Sellers - Selected Tax Issues Page 66

Taxable Stock Acquisitions (without 338 Elections) - General Tax Treatment of Corporate Target 1. Purchaser obtains a tax basis in Target stock based on purchase price. (Target’s tax basis

in assets is not adjusted due to purchase.) 2. Tax attributes of Target (such as NOL's and research and development (“R&D”) credits)

carry over to Purchaser group (through its ownership of Target) but their use may be limited.

3. Pre-acquisition liabilities of Target (including tax liabilities) attach with Target (i.e. Buyer).

4. One level of income tax imposed on Seller. Seller pays income tax based on Seller’s tax basis in Target stock and tax rate.

5. Sales taxes and/or transfer taxes are generally not imposed. 6. Liability for pre-acquisition taxes, such as income taxes, sales tax and VAT/GST, attach

with Target. 7. Accounting methods of Target generally carry over to Purchaser group (through

ownership of Target) but may not if, for example, Target becomes member of Consolidated Group

M&A Tax Considerations for Buyers and Sellers - Selected Tax Issues Page 67

Taxable Stock Acquisitions (without Section 338 Elections)

Major Tax Considerations for Seller of Stock Generally only one level of taxable gain.

Major Tax Considerations for Purchaser of Stock

Purchased Target Corporation Generally Continues with Existing Assets and Liabilities Tax Attributes generally unaffected by stock transfer

Attributes belong to corporation, and are generally transferred together with other corporate

assets A stock transfer does not affect basis of target corporation’s assets or generally its accounting

methods Sections 382 and 383 may limit purchaser’s ability to use acquired attributes following

ownership change

M&A Tax Considerations for Buyers and Sellers - Selected Tax Issues Page 68

Taxable Stock Acquisitions (without Section 338 Elections) Taxable Year and Accounting Methods generally continue but there are

exceptions.

Consolidated Return Rules apply when Target Joins a Consolidated Group:

Target’s tax year ends (short period, closing of the books treatment of Target) when Target becomes a member of the consolidated group.

Purchase of S Corporations: Target’s tax year ends if Target ceases to qualify as an S corporation (1) For example, if purchaser is a non-qualifying shareholder or Target becomes a member of

a consolidated group.

Pro-rata method of allocating items to pre and post period generally applies, but closing of the books allocation method applies if there an exchange of 50% or more of the stock in the corporation during such year or if all shareholders elect to apply closing of the books method to pre and post acquisition periods.

M&A Tax Considerations for Buyers and Sellers - Selected Tax Issues Page 69

Taxable Stock Acquisitions (without 338 Elections) - General Operation of Section 382 Limitations

Section 382 limitations on use of losses generally apply following an “ownership change”. Use of “pre-change” losses to offset “post-change” income subject to annual section 382 limitation. Limitations may also apply to recognized built-in losses. Limitation generally equals the value of the loss corporation’s stock immediately before the ownership change, multiplied by the long-term tax-exempt rate.

M&A Tax Considerations for Buyers and Sellers - Selected Tax Issues Page 70

Stock Acquisitions (without 338 Elections) - General Policies of Section 382

Anti-trafficking rules - purpose of acquisition is irrelevant An “ownership change” occurs on a testing date when the stock of the loss corporation owned by one or more five-percent shareholders increases by more than 50 percentage points during a testing period when compared with the lowest ownership by each shareholder during that period

Rules for determining applicable testing period can require determining stock ownership and stock transactions from formation of target. Notice 2003-65, Section 338 Approach vs. Section 1374 Approach

M&A Tax Considerations for Buyers and Sellers - Selected Tax Issues Page 71

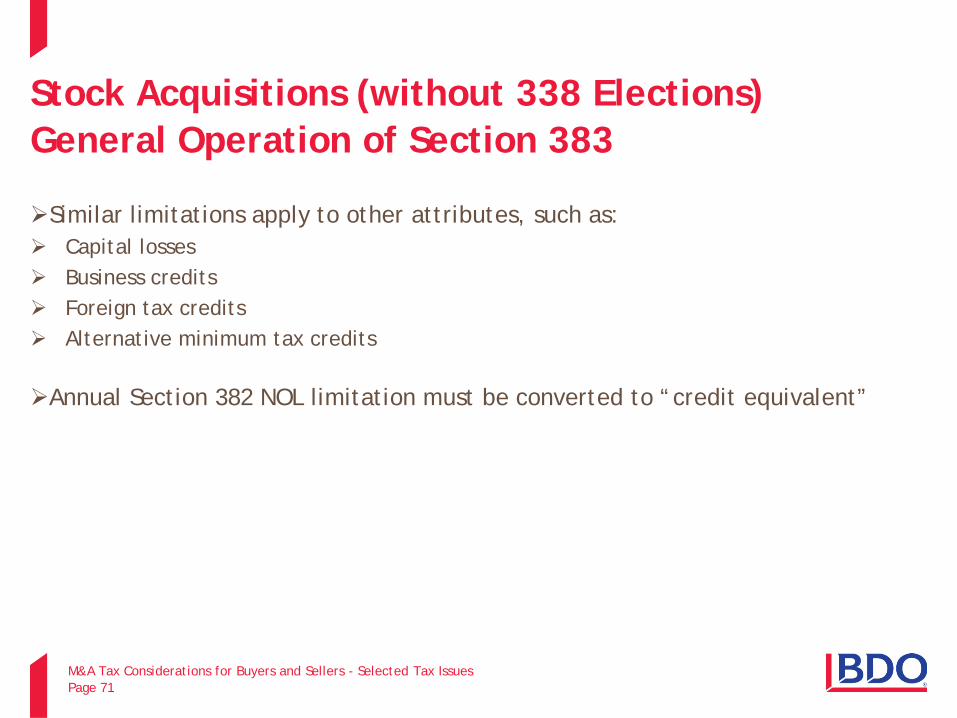

Stock Acquisitions (without 338 Elections) General Operation of Section 383

Similar limitations apply to other attributes, such as: Capital losses Business credits Foreign tax credits Alternative minimum tax credits

Annual Section 382 NOL limitation must be converted to “credit equivalent”

M&A Tax Considerations for Buyers and Sellers - Selected Tax Issues Page 72

Taxable Stock Acquisitions (with Section 338 Elections) Deemed asset purchase and sale treatment requires Qualified stock purchase; and Election on Form 8023

Qualified stock purchase Purchaser must be corporation Stock meeting section 1504(a)(2) requirements must be acquired by “purchase” Requires 12-month acquisition period

Fictions apply for most income tax purposes, but not for — Payroll tax purposes; Information reporting purposes; or Most employee benefit plan purposes.

M&A Tax Considerations for Buyers and Sellers - Selected Tax Issues Page 73

Taxable Stock Acquisitions (Section 338(g) vs. 338(h)(10) Elections) Section 338(g) elections re-characterize old and new target transactions only Purchaser of stock has stock purchase Sellers of stock have stock sale The “old target” and “new target” have deemed asset purchases and sales

Section 338(h)(10) election re-characterize certain seller’s transactions as well Sellers of S corporation stock have deemed taxable liquidation following deemed sale of assets Eligible corporate sellers may have Section 332 treatment for deemed liquidation

M&A Tax Considerations for Buyers and Sellers - Selected Tax Issues Page 74

Taxable Stock Acquisitions (with Section 338(h)(10) Election) 1. Form is a Stock Acquisition. 2. Target is a member of a consolidated group or an “S” corporation. 3. Purchaser and Seller elect to treat acquisition as an Asset Acquisition for income tax

purposes under IRC Section 338(h)(10). 4. Purchaser generally obtains benefits of Purchase Accounting for income tax purposes. 5. Seller is subject to income tax, as if Target had sold assets and liquidated. NOL's and tax

credits remain with Seller and often may be used to offset gains and tax from deemed asset sale.

6. Sales taxes and/or transfer taxes generally do not apply. 7. Pre-acquisition non-income tax liabilities remain with Target (now held by Purchaser).

M&A Tax Considerations for Buyers and Sellers - Selected Tax Issues Page 75

Taxable Stock Acquisitions (Section 338(h)(10) Election Requirements)

Qualified stock purchase of one of the following types of corporations: S corporation Subsidiary member of consolidated group Subsidiary member of non-consolidated affiliated group

Election on Form 8023 Joint election by all S corporation shareholders

Some states require separate state “Section 338” elections

M&A Tax Considerations for Buyers and Sellers - Selected Tax Issues Page 76

Benefits of Section 338(h)(10) Election to Purchaser in a Taxable Stock Acquisition

Cost basis of assets deemed acquired New accounting methods New cost recovery methods New elections Elimination of earnings and profits Eliminate reliance on old tax and accounting records Tax consequences not dependent on form of transaction

M&A Tax Considerations for Buyers and Sellers - Selected Tax Issues Page 77

Taxable Stock Acquisitions (with Section 338(h)(10) Election) Considerations with S Corporation Target Consequences of an S corporation section 338(h)(10) election Deemed sale of assets by “old target” corporation, followed by liquidation Deemed purchase of assets by “new target” corporation

Subject to built-in gains tax for S corporations, only one level of tax is imposed on sale gains Deemed sale gain is allocated to shareholders on Schedule K-1 under normal S corporation rules Basis increase reduces deemed liquidation gain

M&A Tax Considerations for Buyers and Sellers - Selected Tax Issues Page 78

Tax Free Mergers and Acquisitions.

The tax treatment of tax free mergers and acquisitions is not discussed in detail in this presentation. In general, the purchaser in a tax free merger receives a carry over basis in the assets of the target and the seller defers gain with respect to shares of the target it exchanges for shares of the acquirer. The seller generally recognized income, or a taxable gain, with respect to boot it receives in the form or cash or property.

M&A Tax Considerations for Buyers and Sellers - Selected Tax Issues Page 79

Liabilities of Target

In a Stock Acquisition (without a 338(h)(10) election), liabilities of the target generally continue as liabilities of the target and are not included in the purchase price paid for the stock of the target. In an Asset Acquisition, liabilities of the target assumed, or taken subject to, as part of the acquisition are generally included in the purchase price deemed paid for the assets of the target. In a Stock Acquisition (with a 338(h)(10) election), liabilities of the target are generally included in the purchase price deemed paid for the assets of the target. The purchase price paid for target is often subject to adjustment as liabilities of the target are determined or become fixed. Most acquisitions provide for working capital adjustments to the purchase price. Tax liabilities of target are typically among the liabilities taken into account in determining the amount of a working capital adjustment.

M&A Tax Considerations for Buyers and Sellers - Selected Tax Issues Page 80

Transaction Costs Inherently facilitative costs incurred paid by the taxpayer in the process of investigating or otherwise pursuing a “covered transaction” generally must be capitalized as a cost of the transaction. Other than inherently facilitative costs, amounts paid by the taxpayer in the process of investigating or otherwise pursuing a “covered transaction” facilitates the transaction and must generally be capitalized only if the amount relates to activities performed on or after the earlier of the following dates: (1) the date on which a letter of intent, exclusivity agreement, or similar written communication (other than a confidentiality agreement) is executed by representatives of the purchaser and the target; or (2) the date on which the material terms of the transaction, as tentatively agreed to by representatives of the purchaser and the target, are authorized or approved by the taxpayer's board of directors (or its committee) or, for a taxpayer that is not a corporation, are authorized or approved by the appropriate governing officials of the taxpayer. For a transaction that does not require authorization or approval of the taxpayer's board of directors or appropriate governing officials the date determined under the above rules is the date on which the purchaser and the target execute a binding written contract reflecting the terms of the transaction.

M&A Tax Considerations for Buyers and Sellers - Selected Tax Issues Page 81

Transaction Costs

A “covered transaction” includes the following transactions: A taxable acquisition by the taxpayer of assets that constitute a trade or business; A taxable acquisition of an ownership interest in a business entity (whether the taxpayer is the purchaser or the target) if, immediately after the acquisition, the acquirer and the target are related within the meaning of IRC Section 267(b) and IRC Section 707(b); or Most a tax-free corporate reorganizations.

M&A Tax Considerations for Buyers and Sellers - Selected Tax Issues Page 82

Transaction Costs

Success based fees, which are fees contingent on the completion of the transaction, must generally be capitalized, except to the extent the taxpayers satisfies certain documentation requirements. Taxpayers meeting certain requirements may elect a safe harbor allocation. Taxpayers who make the election can treat 70% of the success-based fee as an amount that doesn't facilitate the transaction and is therefore currently deductible. The remaining 30% of the fee must be capitalized. Borrowing costs generally must be capitalized as a cost of the borrowing as opposed to into the cost of the transaction. Certain de-minimis costs need not be capitalized as a cost of the transaction. Costs not capitalized under these rules under IRC Section 263(a) may still be subject to capitalization under IRC Sections 195 or 248.

M&A Tax Considerations for Buyers and Sellers - Selected Tax Issues Page 83

Transaction Costs In a stock acquisition, transaction costs incurred by the target corporation to facilitate the transaction are generally considered incurred by the target on behalf of the selling shareholders and included in the consideration deemed received by the selling shareholders from the sale, increasing their gain from the sale of the target stock. However, these costs are also generally deemed expenditures of the selling shareholders with respect to their sale of stock in the target, which may reduce their gain from the sale of stock in the target. Transaction costs incurred by the purchaser to facilitate the transaction would generally be considered a cost of acquiring the stock and capitalized into the purchaser’s stock basis in the purchased stock.

M&A Tax Considerations for Buyers and Sellers - Selected Tax Issues Page 84

Transaction Costs

In an asset acquisition, transaction costs incurred by the target corporation to facilitate the transaction are generally considered incurred by the target reducing its gain from the sale of assets by the target. Transaction costs incurred by the purchaser to facilitate the transaction would generally be considered a cost of acquiring the assets and capitalized into the purchaser’s basis in the purchased assets.

M&A Tax Considerations for Buyers and Sellers - Selected Tax Issues Page 85

Contingent Liabilities

In an acquisition, the purchaser often assumes (directly or through its ownership of target) certain contingent liabilities of target. For income tax purposes, in an asset acquisition, or a stock acquisition with a 338(h)(10) election, such contingent liabilities are generally to be treated by the seller as an additional amount realized from the sale and by the purchaser as an adjustment to the asset purchase price, as they accrue, or costs with respect to such liabilities are incurred. This means that the purchaser may not generally receive a current income tax deduction, as these liabilities accrue or costs with respect to such liabilities are incurred. While unclear this treatment is often thought to apply to the treatment of deferred revenue, which is a liability commonly found on the balance sheets of targets.

M&A Tax Considerations for Buyers and Sellers - Selected Tax Issues Page 86

Deferred Revenue There is often a difference between the amount of deferred revenue booked for GAAP purposes and the amount of the target’s deferred revenue for income tax purposes. In an asset acquisition, tax deferred revenue assumed by the purchaser in the transaction is generally to be recognized by the seller as an additional amount realized from the sale. For the purchaser, as the purchaser incurs costs with respect to this deferred revenue, the treatment of these costs for income tax purposes is not entirely clear under existing authority. It is often thought that the purchaser should capitalize these costs as they are incurred, into the purchase price of the purchased assets. Under this treatment, often these capitalized costs would be allocated to increased goodwill, under Section 1060, which increase could only be recovered over 15 years. However, the seller and the purchaser may be able to agree to treat the seller as having paid the purchaser a separate payment for agreeing to assume the obligation to perform the services required to generate the deferred revenue. This separate payment should generate a deduction to the seller and income to the purchaser, but the purchaser would then generally be entitled to deduct currently its costs with respect to the deferred revenue. This treatment can be favorable or unfavorable to the purchaser depending on timing and the amounts of the costs to be incurred with respect to the deferred revenue.

M&A Tax Considerations for Buyers and Sellers - Selected Tax Issues Page 87

Deferred Revenue

Further, for income tax purposes, under a line of authorities (mainly dealing with subscription fees and services), a seller might be deemed to have paid to the purchaser, through a deemed reduction in purchase price, a separate payment for agreeing to assume the obligation to perform the services required to generate the deferred revenue. This deemed payment should generates a deduction to the seller and income to the purchaser, but the purchaser would then generally be entitled to deduct currently its costs with respect to the deferred revenue. This treatment can be favorable or unfavorable to the purchaser depending on timing and the amounts of the costs to be incurred with respect to the deferred revenue. In most taxable asset acquisitions, or stock acquisitions with a Section 338(h)(10) election, the parties should consider the tax treatment to the parties resulting from the target’s deferred revenue and their options with respect to the treatment of same. See, New York State Bar Association Tax Section, Report on the Treatment of “Deferred Revenue” by the Buyer in Taxable Asset Acquisitions, January 7, 2013.

M&A Tax Considerations for Buyers and Sellers - Selected Tax Issues Page 88

Accounting Methods

Purchasers and Sellers must generally apply their own method of tax accounting in reporting a transaction.

M&A Tax Considerations for Buyers and Sellers - Selected Tax Issues Page 89

Common Tax Due Diligence Issues 1. Accounting methods including revenue recognition. 2. Limitations on NOL and tax credit use due to prior ownership changes. 3. State income tax compliance and exposure. 4. State sales and use tax compliance and exposure. 5. Foreign income and transfer tax (VAT) Compliance and Reporting. 6. Review prior acquisitions by Target. 7. Compensation and benefits compliance and exposure.

Payroll tax compliance and exposure. Possible IRC Section 409A deferred compensation penalty exposure. IRC Section 280G golden parachute penalty exposure. IRC Section 162(M) exposure. Stock option compliance related to IRC Sec 422.

8. Computational issues on all tax credits previously taken or carried forward. Often it is possible to estimate the possible exposure for several of these items and

negotiate indemnities, holdbacks and purchase price reductions. Possible exposure may result in a restructuring of the acquisition.

M&A Tax Considerations for Buyers and Sellers - Selected Tax Issues Page 90

Disclosure

This outline is for information purposes only. Taxpayers are encouraged to consult their own tax advisors with respect to these issues.

To ensure compliance with Treasury Department regulations, we wish to inform you

that any statements that may be contained in this communication are not intended or written to be used, and cannot be used, for the purpose of (i) avoiding tax-related penalties under the Internal Revenue Code or applicable state or local tax law provisions or (ii) promoting, marketing or recommending to another party any tax-related matters addressed herein.