Maximizing Producer Value through Alliance Pipeline and Aux Sable

Aux Sable Channahon Facility TourSeptember 20, 2012

W.J. (Bill) McAdamCEO, Aux Sable

T.L. (Tim) StauftPresident , Aux Sable

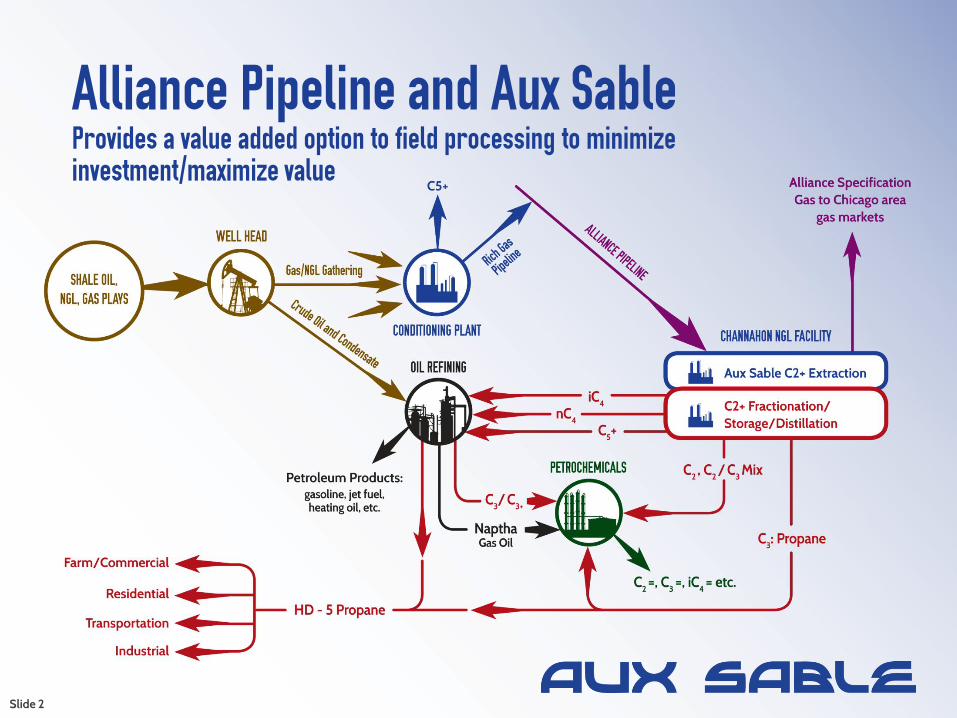

Alliance Pipeline and Aux Sable Provides a value added option to field processing to minimize investment/maximize value

Slide 2

Slide 3

Outline Overview of North American NGL markets Fundamentals of “Rich” Gas Production in North

America Key Attributes of the Alliance and Aux Sable assets What do Producers want? Summary Questions

Natural Gas and NGL Value ChainNatural Gas Production

Processing & Treating

Natural Gas Transmission Straddle Plant Natural Gas

Transmission

NGL Fractionation

NGL Storage

NGL Product Transportation

Natural Gas Storage

Residential/Commercial/

IndustrialPower Plants

Natural Gas Distribution

C2+ or C3+

C2+ or C3+

C2+NGL Raw Mix Transportation

Refined Products

Petrochem Industry

Residential/Commercial

C2+

Slide 4

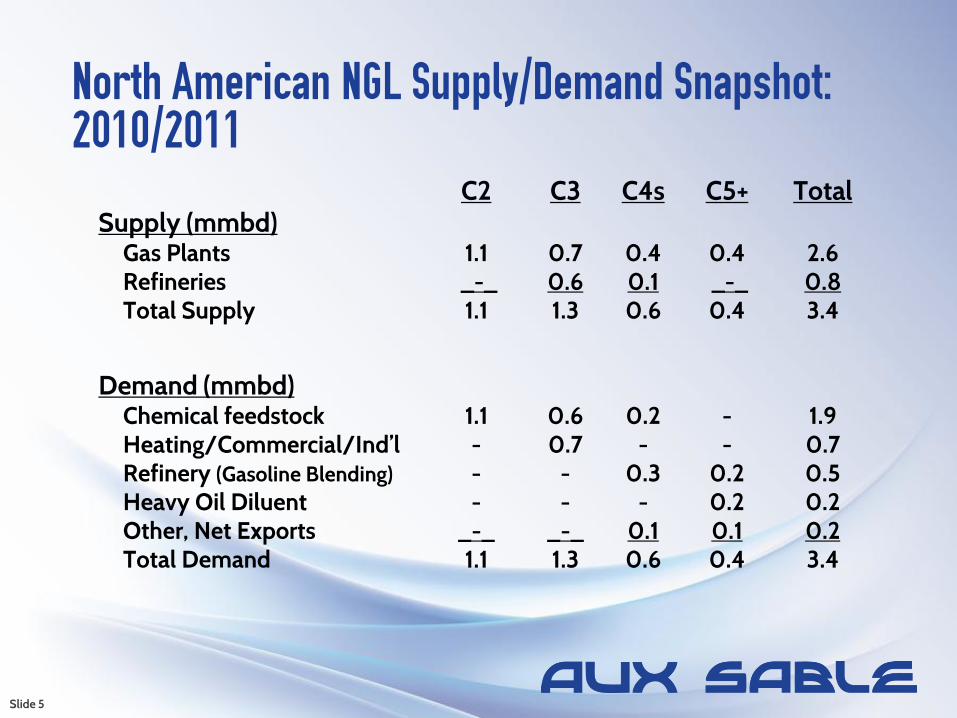

C2 C3 C4s C5+ TotalSupply (mmbd)

Gas Plants 1.1 0.7 0.4 0.4 2.6Refineries _-_ 0.6 0.1 _-_ 0.8Total Supply 1.1 1.3 0.6 0.4 3.4

Demand (mmbd)Chemical feedstock 1.1 0.6 0.2 - 1.9Heating/Commercial/Ind’l - 0.7 - - 0.7Refinery (Gasoline Blending) - - 0.3 0.2 0.5Heavy Oil Diluent - - - 0.2 0.2Other, Net Exports _-_ _-_ 0.1 0.1 0.2Total Demand 1.1 1.3 0.6 0.4 3.4

North American NGL Supply/Demand Snapshot:2010/2011

Slide 5

North American NGL Infrastructure

Slide 6

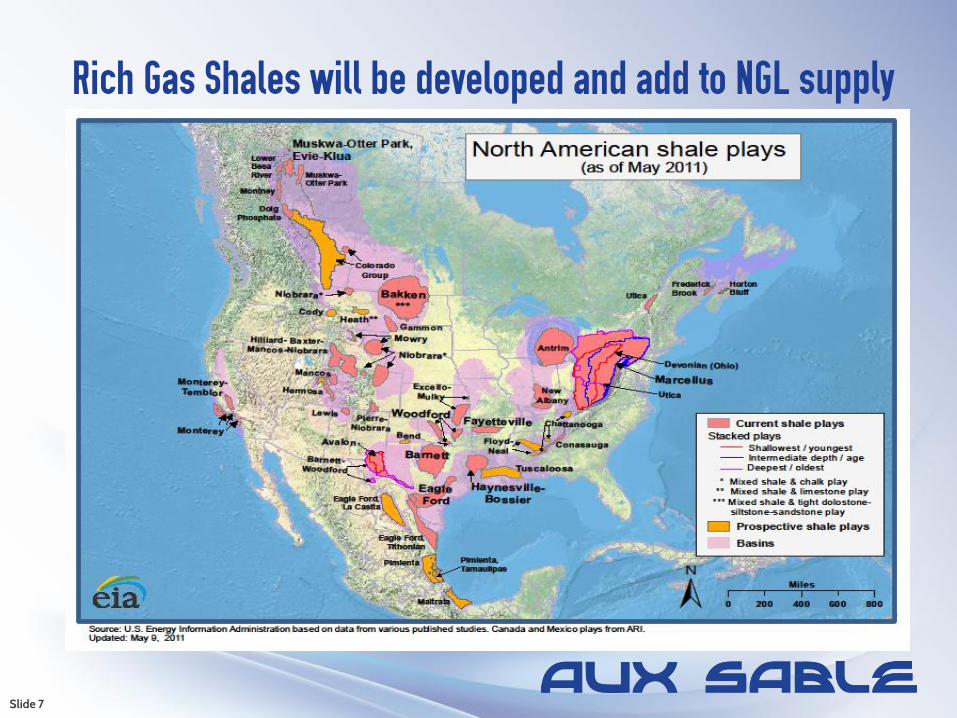

Rich Gas Shales will be developed and add to NGL supply

Slide 7

The Push to Develop Rich Gas and NGLs

-

5

10

15

20

25

30

35

40

2006 2008 2010 2012 2014 2016 2018 2020

Bcf

/d

Western Canada

All Other US

Eagle Ford

Bakken

Utica

Marcellus

Haynesville /1

Fayetteville

Barnett

Woodford

Source: ICF International

Slide 8

Shale gas has driven a dramatic increase in gas production

Low gas netbacks have forced focus on developing oil/rich gas shales deposits

New NGL infrastructure required to recover, process and transport spec product markets to end markets

NGL supply volumes are increasing significantly and will outstrip demand without new markets

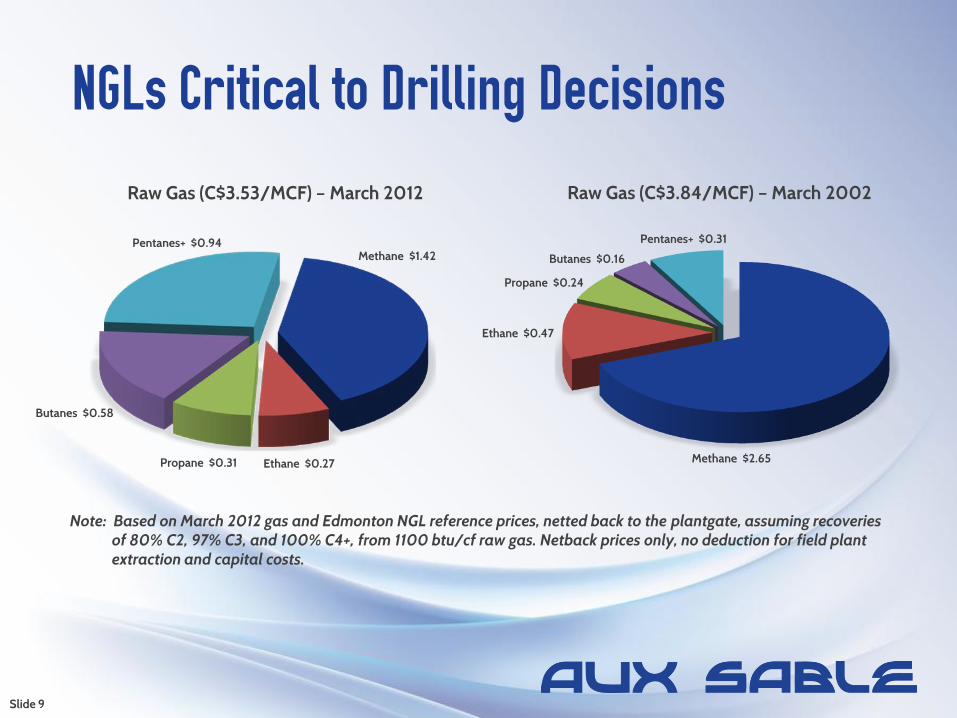

NGLs Critical to Drilling Decisions

Note: Based on March 2012 gas and Edmonton NGL reference prices, netted back to the plantgate, assuming recoveries of 80% C2, 97% C3, and 100% C4+, from 1100 btu/cf raw gas. Netback prices only, no deduction for field plant extraction and capital costs.

Raw Gas (C$3.53/MCF) – March 2012 Raw Gas (C$3.84/MCF) – March 2002

Methane $1.42Pentanes+ $0.94

Ethane $0.27Propane $0.31

Butanes $0.58

Methane $2.65

Pentanes+ $0.31

Ethane $0.47

Propane $0.24

Butanes $0.16

Slide 9

Mont Belvieu

Conway

Sarnia (2.6 B lbs/Yr)

Fort Saskatchewan (2.6 B lbs/Yr)

Chicago

ENTERPRISE ONEOK

COCHIN

ENBRIDGE

ALLIANCE

PTC Empress

Salt Storage

ENTERPRISE

Cochrane

AEGS

North American Ethylene Plants

Slide 10

Extraction Facilities

Ethylene Plant

Joffre (6.0 B lbs/Yr)

USGC (55 B lbs/Yr)

Clinton (1.1 B lbs/Yr)

Morris (1.3 B lbs/Yr) Calvert City

(0.4 B lbs/Yr)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

C2 C3 nC4 Naphtha Gas Oil

Typical Olefins Cracker Yields

Ethylene Propylene Butadiene/Butylenes SC Naphtha SC Gas Oil Fuel Gas

Slide 11

IHS CMAI Global Ethylene Cash Costs

Slide 12

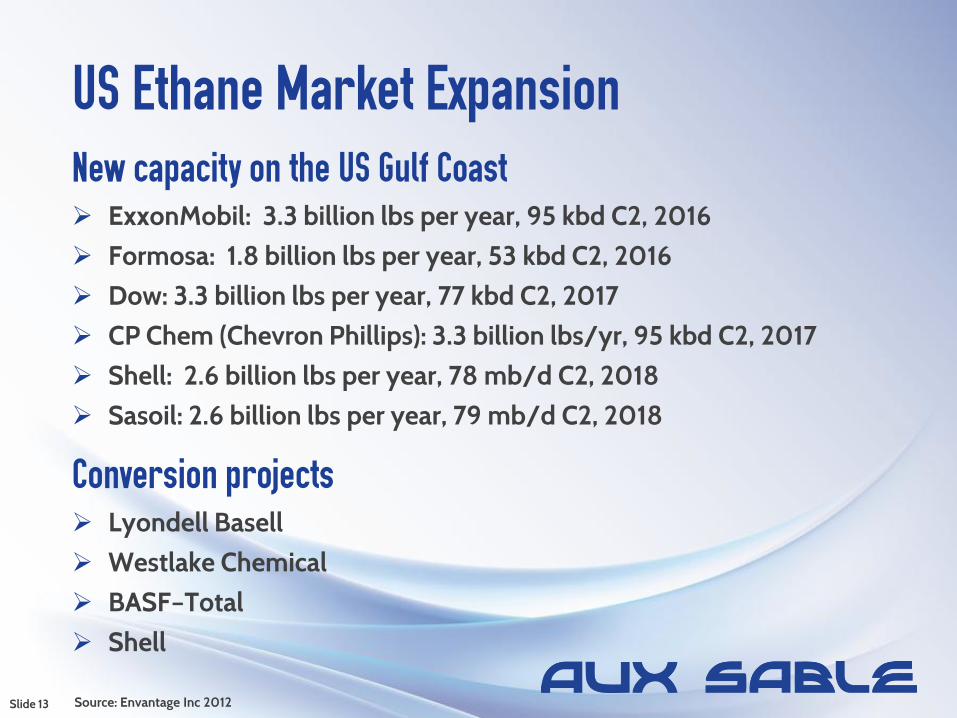

US Ethane Market ExpansionNew capacity on the US Gulf Coast ExxonMobil: 3.3 billion lbs per year, 95 kbd C2, 2016 Formosa: 1.8 billion lbs per year, 53 kbd C2, 2016 Dow: 3.3 billion lbs per year, 77 kbd C2, 2017 CP Chem (Chevron Phillips): 3.3 billion lbs/yr, 95 kbd C2, 2017 Shell: 2.6 billion lbs per year, 78 mb/d C2, 2018 Sasoil: 2.6 billion lbs per year, 79 mb/d C2, 2018

Conversion projects Lyondell Basell Westlake Chemical BASF–Total Shell

Slide 13 Source: Envantage Inc 2012

Max US Ethane Supply vs Max Demand (1000 BPD)

Source: Envantage Inc 2012

US Ethane Supply/Demand Growth

Slide 14

LPG Netbacks from Growing Export Markets

Netbacks (March 2012, US cpg) US Gulf Coast to Japan US Gulf Coast to NWE

C3Market Price

Less:Mont Belvieu PriceTanker LoadingFreight

Subtotal

Margin

201

1261323

162

39

186

1261313

152

34

C4Market Price

Less:Mont Belvieu PriceTanker LoadingFreight

Subtotal

Margin

236

1856

26217

19

211

1856

15206

5

Source: Waterborne LPG Report & Petral, March 2012

Exports of propane from the US Gulf Coast enjoy strong netbacks vs domestic prices.

Slide 15

Purvin and Gertz Survey of US LPG Export Terminal Expansions

Terminal LPG Capacity*(bbl/d)

Notes

Enterprise 156,000 to 312,000 bbl/d

Enterprise is expanding its LPG terminal on the Houston Ship Channel by 4Q12

Load rates for international grade propane will be able to load 3 vessels at one time

Targa 52,200 to 70,000 bbl/d

Expanding at Galena Park Expects to be able to load 3 to 4 VLGCs per month of

international grade propane by 3Q13

Conoco / Occidental / TransMontaigne

240,000 to 480,000 bbl/d

LPG import / export terminal on the Houston Ship Channel operational in 2014

Connections to Mont Belvieu (CP has a fractionator, Oxy has a pipeline corridor and TransMontaigne has the land)

Vitol 100,000 to 200,000 bbl/d

Propane export terminal at Coastal Caverns near Beaumont to start up in 1Q 2013

Will include a 100 MBPD processing facility and salt dome storage at Spindletop

* Assumes loading capacity online from 12 to 24 hrs per day

Slide 16

C2 C3 C4s C5+Supply Direction

Gas Plants UP UP up UPRefineries - flat- flat- flat-

Demand DirectionPetrochemical Feedstock UP balance up up?Heating/Commercial/Ind’l - flat/down - -Refinery (Gasoline Blending) - - down downHeavy Oil Diluent - - up UPDehydro (PDH), MTBE - UP ? -Net Exports - UP up -

Key Trends1. NGL production up from Gas Plants (“oily” gas focus in shales)2. Ethane balanced by increased Petchem feedstock demand3. Propane balanced by increased exports, PDH4. Butanes balanced by increased exports, MTBE

North American NGL Supply/Demand Trends2010 to 2011

Slide 17

Alberta NGL Facilities and Capacity

Major Straddle Plants Estimated Capacity (MMcf/d)Cochrane 2,500Empress 9,700

Other 1,200Total 13,400

Major Fractionators Estimated Capacity (kb/d)

Redwater (C2+) 65 (25/40)Dow (C2+) 70 (35/35)

Keyera (C3+) 35 (C3+ only)

Plains (C3+) 50 (C4+ only)Total 135 C2+, 85 C3/C4+

McMahon/Younger

Judy Creek

Fort SK

Edmonton

West Pembina

Caroline

HarmattanCochrane

Empress

Waterton

AEGS

Alliance

Cochin

Pembina

Enbridge

Slide 18

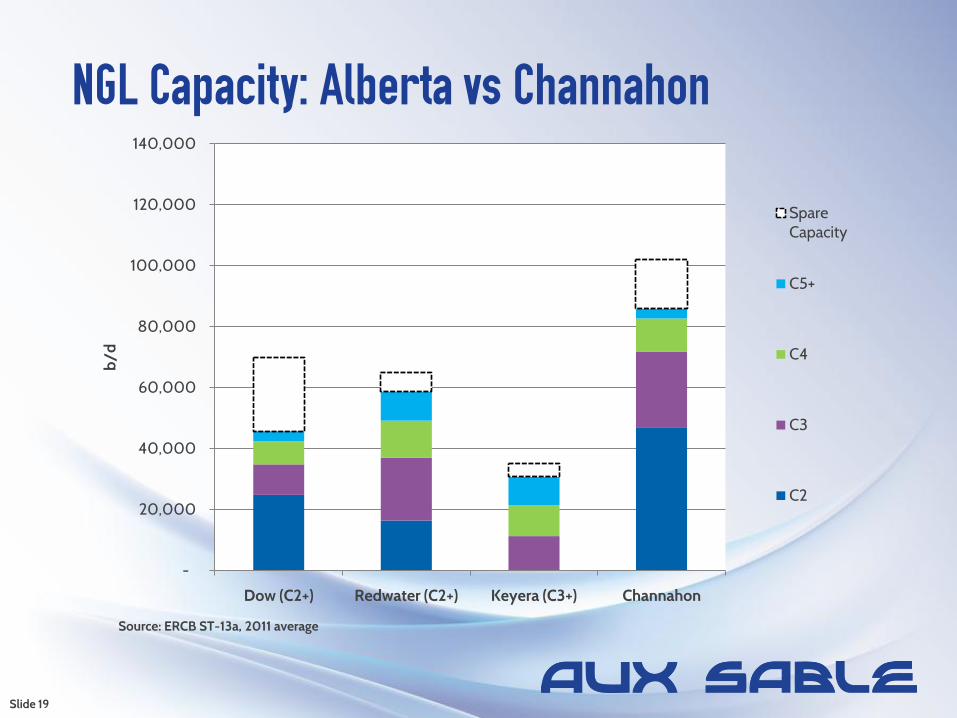

NGL Capacity: Alberta vs Channahon

Source: ERCB ST-13a, 2011 average

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

Dow (C2+) Redwater (C2+) Keyera (C3+) Channahon

b/d

Spare Capacity

C5+

C4

C3

C2

Slide 19

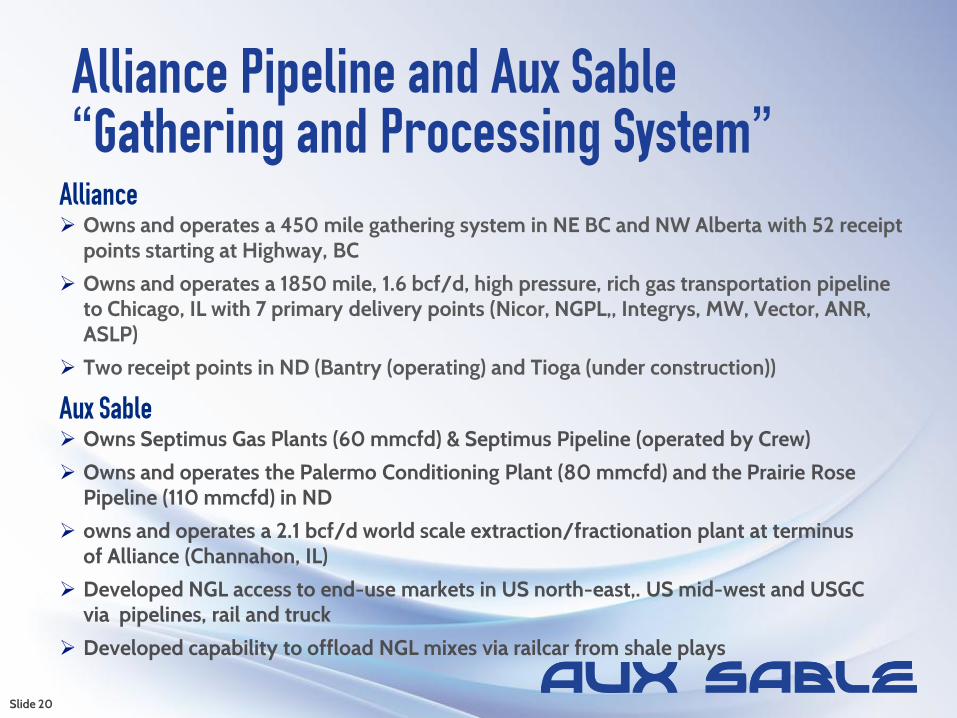

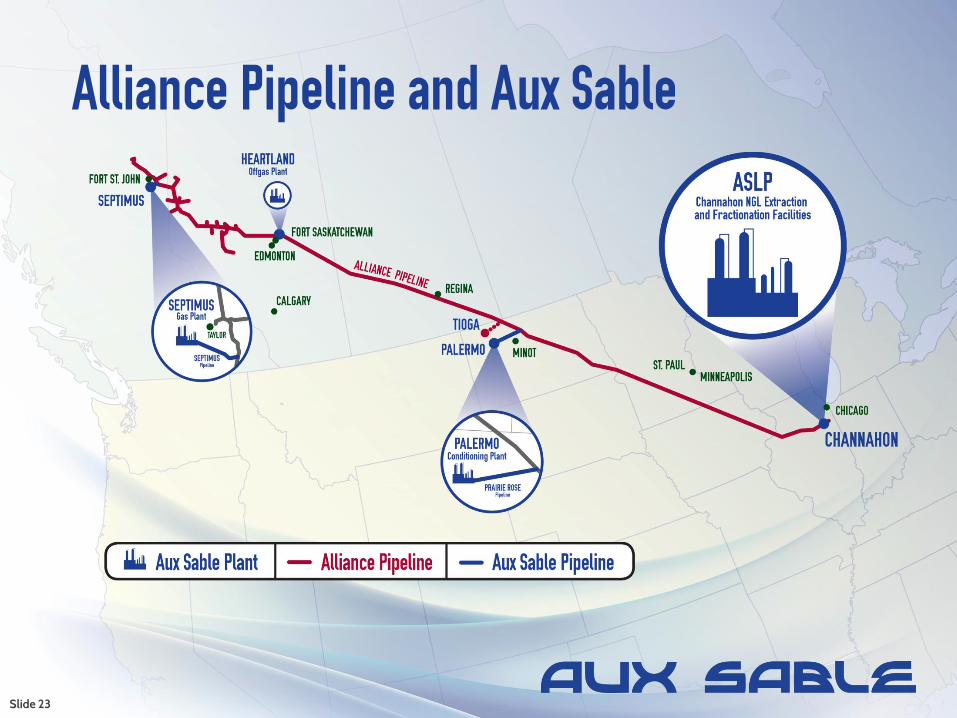

Alliance Pipeline and Aux Sable “Gathering and Processing System”

Alliance Owns and operates a 450 mile gathering system in NE BC and NW Alberta with 52 receipt

points starting at Highway, BC

Owns and operates a 1850 mile, 1.6 bcf/d, high pressure, rich gas transportation pipeline to Chicago, IL with 7 primary delivery points (Nicor, NGPL,, Integrys, MW, Vector, ANR, ASLP)

Two receipt points in ND (Bantry (operating) and Tioga (under construction))

Aux Sable Owns Septimus Gas Plants (60 mmcfd) & Septimus Pipeline (operated by Crew)

Owns and operates the Palermo Conditioning Plant (80 mmcfd) and the Prairie Rose Pipeline (110 mmcfd) in ND

owns and operates a 2.1 bcf/d world scale extraction/fractionation plant at terminus of Alliance (Channahon, IL)

Developed NGL access to end-use markets in US north-east,. US mid-west and USGC via pipelines, rail and truck

Developed capability to offload NGL mixes via railcar from shale plays

Slide 20

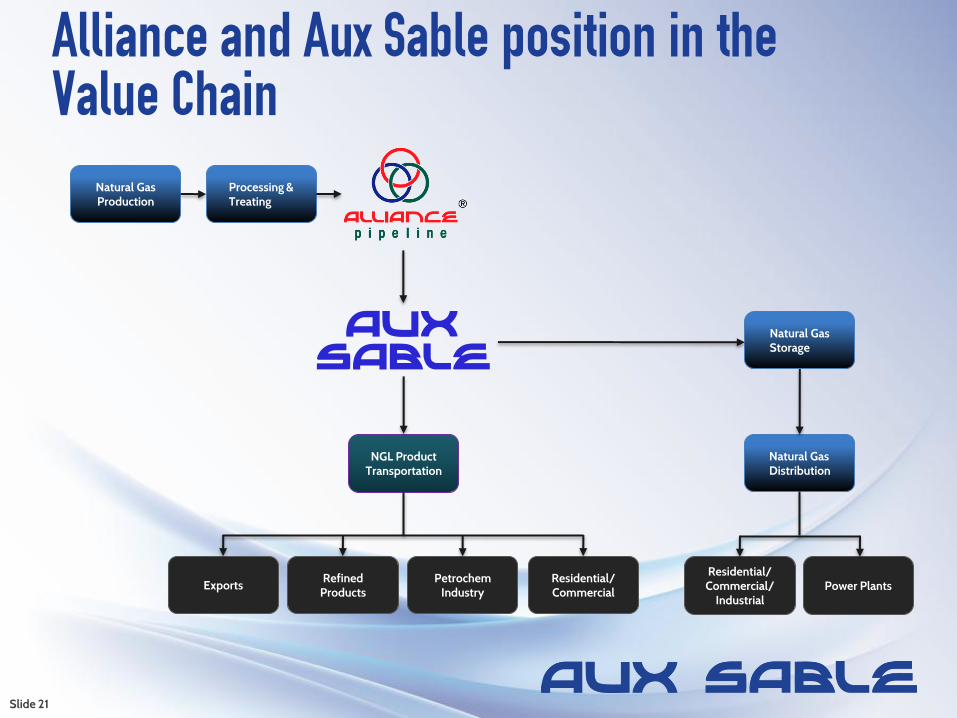

Alliance and Aux Sable position in the Value Chain

Natural Gas Production

Processing & Treating

NGL Product Transportation

Refined Products

Petrochem Industry

Residential/Commercial

Natural Gas Storage

Residential/Commercial/

IndustrialPower Plants

Natural Gas Distribution

Exports

Slide 21

Alliance Pipeline Receipt Points

Slide 22

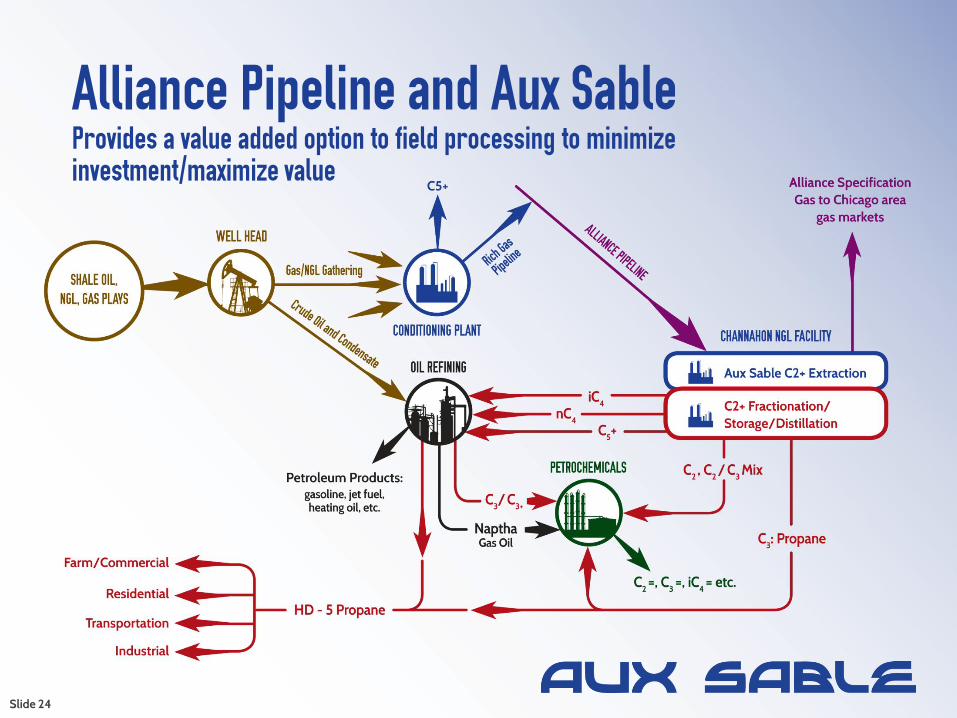

Alliance Pipeline and Aux Sable

Slide 23

Alliance Pipeline and Aux Sable Provides a value added option to field processing to minimize investment/maximize value

Slide 24

What do Producers want? Value for their rich gas production against liquid markets

Access to infrastructure that meets their needs, provides reliable takeaway and is shaped to their production profile as they develop their reserves

Minimum capital investment for field processing and extraction

Minimum commitments to NGL pipeline and processing fees

Access to liquid, transparent markets for pricing and hedging

Recognition of NGLs as liquid production (versus gas equivalent)

Slide 25

Aux Sable rich gas premiums (RGPs) provide value to WCSB gas producers for NGLs, allowing producers to: Avoid costly field plant investments Capture NGL value not available on NGTL system Direct greater resources to gas drilling activities Increase netbacks at plantgate Allows producer to record barrel reserves

The APL-AS system value proposition provides a competitive alternative for producers to maximize value of rich shale gas………also applies to Bakken shale oil play

Greater connectivity for BC/AB & Bakken NGLs/gas to liquid markets increases value of rich gas to producers who commit to use the system

Recent RGP deals in the public domain:— TRILOGY: “Eliminates 2011 and 2012 capital expenditures of approximately $55 Million

for new deep-cut gas plant”— CEQUENCE: “Increase in realized product price”; “Resulting increase to recent netbacks

of approximately $3.00 per boe” — CELTIC: “Eliminates for requirement to incur additional capital expenditures of

approximately 75 MM$”

Aux Sable Rich Gas Premiums

Slide 26

Summary Significant new volumes of NGLs will be produced in North America

driven by high NGL frac spread, low gas prices and rich gas directed drilling activities

Frac spreads have structurally shifted to a new higher level that will can be sustained…..US frac spreads will cycle as supply/demand evolves— Ethane demand increases based on C2=/PE production for export— Propane will be exported via waterborne markets, PD to C3=

Significant midstream infrastructure investments are required in the WCSB, Bakken shale plays to connect gas/NGLs to liquid markets

The Alliance Pipeline and Aux Sable provide a competitive alternative to realize value and meet producers’ needs

Slide 27