Media and content industries

Film industry case

A study for IPTS

Workshop: Economics of MCI

Sophie De Vinck & Sven Lindmark Seville, 31 May 2011

Introduction

• Background • Part of larger study on digital transformation of MCI sector • 1 of 3 (5) case studies

• Objectives • Analysis of the film industry • Main economic developments • Digitisation/Internet -> industry/value network • Implications for European competitiveness • Preliminary conclusions

• Structure of the presentation • Background – characteristics of the “traditional” industry

(value network, EU strengths and weaknesses) • Digital transformation of value network, opportunities and

challenges • Conclusions

The film sector: background • Crossroads of economic and cultural value • Economic characteristics

• Prototype industry (high fixed/production costs, low reproduction costs)

• Competition (value) not reflected in price • Unpredictability of demand • Semi-public goods • -> Hit-driven (blockbuster), • -> Strategies of control, economies of scale and

scope, portfolio approach, versioning, stars, genres, sequels

• -> Copyright

The film sector: background

• Hollywood and European film • Despite public support, European film industries are fragmented

European film production levels on the rise

source: European Audiovisual Observatory (2010). Yearbook 2010 Online Premium Service.

Number of feature films produced

Public support in Europe

European audio-visual (film, TV and other AV works) support funds (of more than €1million, excl. tax incentives) - 2004 budgets Source: Cambridge Econometrics, 2008, p. 25

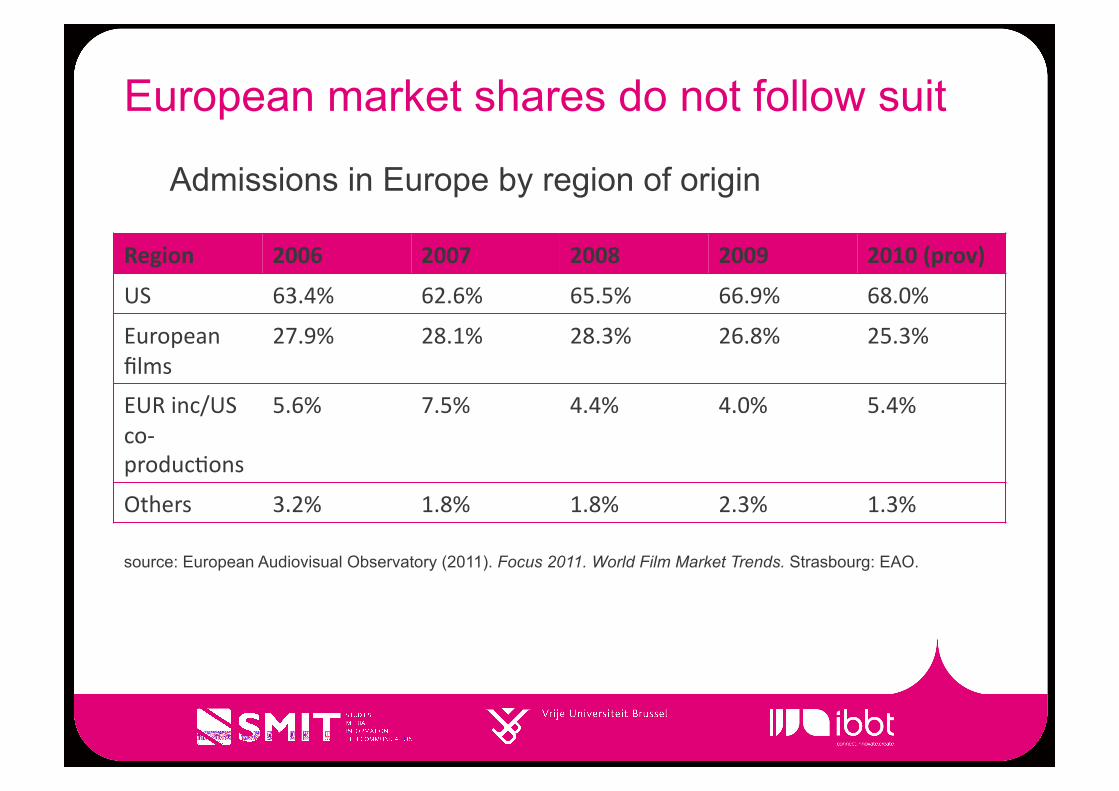

European market shares do not follow suit

Region 2006 2007 2008 2009 2010 (prov)

US 63.4% 62.6% 65.5% 66.9% 68.0%

European films

27.9% 28.1% 28.3% 26.8% 25.3%

EUR inc/US co-‐producBons

5.6% 7.5% 4.4% 4.0% 5.4%

Others 3.2% 1.8% 1.8% 2.3% 1.3%

source: European Audiovisual Observatory (2011). Focus 2011. World Film Market Trends. Strasbourg: EAO.

Admissions in Europe by region of origin

Cross-border circulation is problematic

0.0

50.0

100.0

150.0

200.0

250.0

300.0

2001 2002 2003 2004 2005 2006 2007 2008

Total admisssions for EU produced films

Admissions on national market

Admissions in EU outside national market

source: European Audiovisual Observatory (2010). Yearbook 2010 Online Premium Service.

Admissions in Europe (millions)

Hollywood is common film culture in Europe and beyond

Commission of the European Communities (2009). Commission staff working document. Accompanying document to the proposal for a decision of the European Parliament and of the Council establishing an audio-visual cooperation programme with third countries MEDIA Mundus. Impact assessment report (No. SEC (2009) 3098 final). Brussels: European Commission.

10 leading media groups based on AV-turnover Rank Companies Country Activities Movie subsidiary 2009

1 Sony JP PROD, DIS, VG, REC Sony Pictures, Columbia 30245

2 Walt Disney US PROD, DIS, TV, VID, REC Walt Disney Studios 25482

3 Time Warner US PROD, DIS, TV, VID Warner Bros. 22769

4 News Corporation US PROD, DIS, TV, VID 20th Century Fox 22699

5 DirecTV Group Inc. US TV / 21565

6 Vivendi FR PROD, DIS, TV, VG

Canal + Group (Studio Canal) (and 20% stake in NBC Universal) 17133

7 Nintendo JP VG / 15474

8 NBC Universal US TV, PROD, DIS Universal Studios 15436

9 Viacom US TV, PROD, DIS Paramount Pictures 13619

10 CBS Corp. US TV, RAD / 10684 Source: Adapted from : European Audiovisual Observatory

Film industry value network

Source: adapted from OECD

European strengths and weaknesses Value network Strengths Weaknesses

-‐ Lack of integrated majors

ProducBon -‐ Large and diverse number of companies and films -‐ Auteur cinema tradiBon

-‐ Lack of selecBon and development -‐ Low investment levels -‐ Lack of private funding -‐ Dependent on public support

DistribuBon -‐ Many films distributed -‐ Strong film fesBval tradiBon

-‐ Fragmented and concentrated market -‐ Lack of markeBng tools

ExhibiBon -‐ Large, mature and varied consumpBon

-‐ Theatrical and non-‐theatrical dominated by Hollywood -‐ Lack of cross-‐border circulaBon

Production costs

Average budget per film 2008 Region ($M) North America 22.96 Western Europe 6.13 All Europe 4.73 Far East 4.29 South America 2.86 C/E Europe 0.67 Asia 0.44

Source: Screen Digest (2009)

European strengths and weaknesses Value network Strengths Weaknesses

-‐ Lack of integrated majors

ProducBon -‐ Large and diverse number of companies and films -‐ Auteur cinema tradiBon

-‐ Lack of selecBon and development -‐ Low investment levels -‐ Lack of private funding -‐ Dependent on public support

DistribuBon -‐ Many films distributed -‐ Strong film fesBval tradiBon

-‐ Fragmented and concentrated market -‐ Lack of markeBng tools

ExhibiBon -‐ Large, mature and varied consumpBon

-‐ Theatrical and non-‐theatrical dominated by Hollywood -‐ Lack of cross-‐border circulaBon

Release window system

• Sequenced release • Different times at different

prices • Typically 6-9-12-24 • Shortening (marketing and

piracy)

European strengths and weaknesses Value network Strengths Weaknesses

-‐ Lack of integrated majors

ProducBon -‐ Large and diverse number of companies and films -‐ Auteur cinema tradiBon

-‐ Lack of selecBon and development -‐ Low investment levels -‐ Lack of private funding -‐ Dependent on public support

DistribuBon -‐ Many films distributed -‐ Strong film fesBval tradiBon

-‐ Fragmented and concentrated market -‐ Lack of markeBng tools

ExhibiBon -‐ Large, mature and varied consumpBon

-‐ Theatrical and non-‐theatrical dominated by Hollywood -‐ Lack of cross-‐border circulaBon

(Europe) catching up with the digital impact?

Digital as the latest in a series of innovations

• Innovations affecting film product: • Sound • Colour • Widescreen • 3D

• Innovations affecting film commercialisation: • Television • Home video

Innovations often expanded the market

source: MPA and (Epstein, s.a.)

8.5 4.9 3.3

6.8 6.2 6.5 8.7 8.1 7.0 8.2 8.8 2.2

2.6

6.5 11.9 13.1

21.1 22.8 22.6 19.8 17.9

4.1 7.4

10.1

11.6

15.5

18.7 18.1 16.9

16.1 16.2

0.0

10.0

20.0

30.0

40.0

50.0

60.0

1948 1980 1985 1990 1995 2000 2003 2004 2005 2006 2007

TV (including Pay TV, PPV)

Video/DVD

Theatrical

Worldwide revenues, USD Billion

Digital as the latest in a series of innovations

• Innovations affecting film product: • Sound • Colour • Widescreen • 3D

• Innovations affecting film commercialisation: • Television • Home video

Digital technologies affect all aspects of the film value network

Digitisation effects on the film value network

Source: adapted from OECD

Elements and timeline of digitisation • 1980s and 1990s

• Sound production • Digital imaging (CGI computer generated imagery)

• Jurassic Park and Toy Story (animation)

• Editing • Digital cameras • Digital sounds systems (cinemas) • Home video – DVD

• 2000s – • Digital projectors and D-cinemas (replacing 35 mm reels), DCI

standards • 3D revival • Digital Television, increased # channels, 2012 in EU • (Blue ray) • Internet retailing and ‘rentailing’ • Digital distribution – video on demand, streaming, Youtube etc.

Digitisation effects on the film value network • The production process • The distribution and marketing of films • Film commercialisation:

• Theatrical exhibition • Non-theatrical exhibition • Release window structure

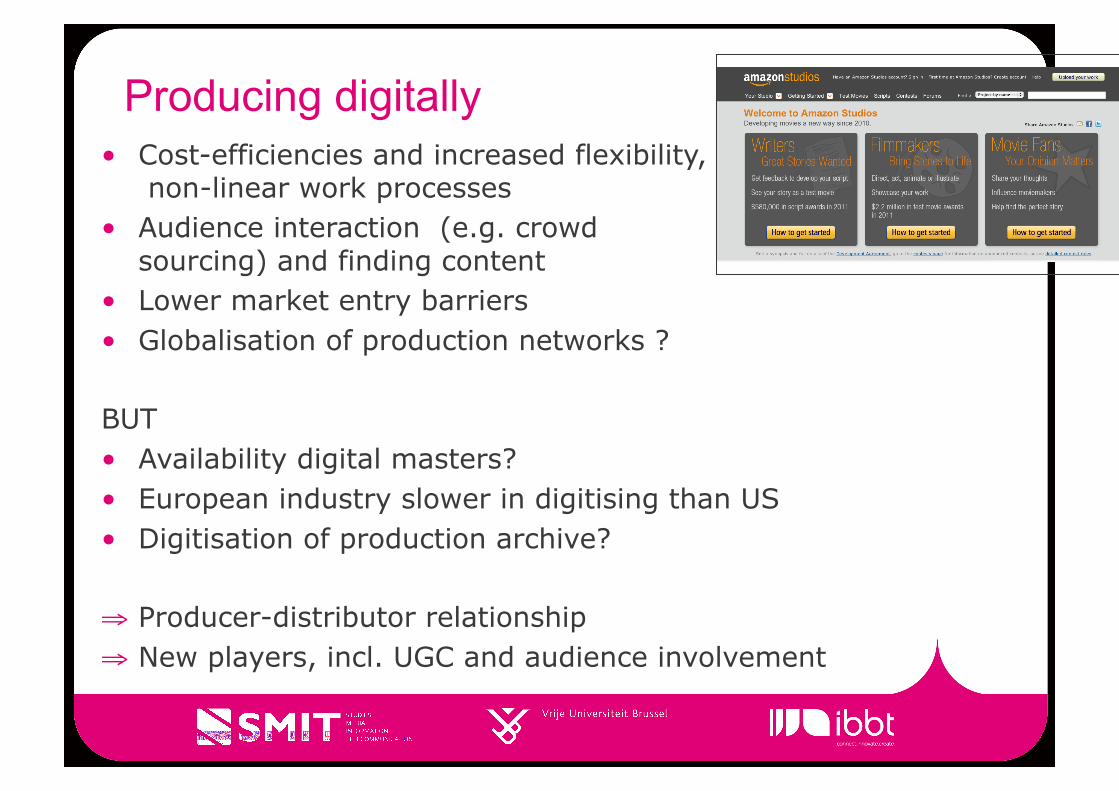

Producing digitally • Cost-efficiencies and increased flexibility,

non-linear work processes • Audience interaction (e.g. crowd

sourcing) and finding content • Lower market entry barriers • Globalisation of production networks ?

BUT • Availability digital masters? • European industry slower in digitising than US • Digitisation of production archive?

⇒ Producer-distributor relationship ⇒ New players, incl. UGC and audience involvement

Digital distribution and marketing

• Cost-savings and easier customisation (Sub-titlling, dubbing) • -> (trans-‐naBonal) distribuBon of European films

• Substantial cost-savings in reproduction and distribution (even for off-line)

• Online and viral marketing strategies • -> may alleviate European weakness in marketing

BUT • Hollywood benefits most from cost-savings? Reinforce

“blockbusterisation”? • How to get attention in a world of abundance? (Brand-names,

intergration, marketing even more important) ⇒ Role distributor reconfigured ⇒ New players specialised in online distribution and rights

management

Theatrical exhibition: digital cinema

• Cost savings (mainly distributors), better quality, programming flexibility

• Flexible programming strategies opportunity for exhibitors

BUT • Costly and difficult roll-out (chicken-and-egg problem) • Smaller exhibitors may disappear

⇒ Emergence of third parties to facilitate roll-out ⇒ Relationship distributor-exhibitor

Evolution of digital screens and sites in Europe

• Transition driven partly by 3D Source: European Audiovisual Observatory (2010). Yearbook 2010 Online Premium Service.

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2004 2005 2006 2007 2008 2009

Digital screens

Africa and Middle East

Asia and Pacific

Europe

Latin America

North America

Source: Gunnarsson, 2010, The outlook for Packaged Media.

Non-theatrical digital/on-line exhibition/consumption

• Dematerialisation -> cost and time of delivery, time and place shifting, linearity of consumption (?)

• VoD model offers opportunities for growth • Opportunities of long tail • Cross-border circulation facilitated

BUT • Slow-down physical home entertainment (blu-ray) not compensated by VoD

revenues – piracy • Continued dominance Hollywood films and US players • Multi-territory licensing not taken up by sector

⇒ New VoD players (Netflix, Apple, Microsoft, etc.) ⇒ Relations between theatrical and non-theatrical ⇒ Illegal marketplace

Online revenue small, but growing

Source: EAO 2010 yearbook

Online revenue small, but growing

Source: KEA European Affairs, & MINES ParisTech Cerna (2010). Multi-territory licensing of audiovisual works in the European Union. Brussels: European Union.

Online film • started to gain some prominence in the mid 2000s when

Apple and other big Internet players (Netflix, Amazon, Google) launched services, followed by Hulu (TV) 2008, Epix 2009

• Difficult to overview the European landscape • Increasing number of providers (200-400) providing

500-1000 services • Often nationally or regionally based • Variety of players

• TV Broadcasters, distributors (operators), content aggregators, content producers

• Variety of modalities • Delivery platforms, delivery and payment models

Looking for business models

pay for films

free models

download-to-own (electronic sell-through)

pay per stream pay per download

subscription models

advertising-based model

sharing model

An online European single market?

Comparison of (consumption) market shares for films in theatrical, video and VoD (France, based on 2008 CNC data) (KEA European Affairs & MINES ParisTech Cerna, 2010, p. 94)

36.6

22.6 30.3

49.2

62.8 58.1

12.2 12.01 11.6

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Theatrical Video VoD

Other

EU

US

French

Release windows under pressure

• Shorter windows: • Piracy • Marketing effects for smaller titles reinforced by cumulative release

• Against shorter windows: • Cannibalization effects • ‘Hit and run’ character blockbuster strategies reinforced

Digital opportunities and challenges Value network Opportuni@es Challenges

ProducBon -‐ Stronger audience Bes -‐ Flexible and more cost-‐efficient producBon networks

-‐ Digital source masters availability -‐ Back catalogue digiBsaBon -‐ Increased (global) compeBBon

DistribuBon -‐ Content customisaBon -‐ Cost-‐savings and flexibility -‐ Online and viral markeBng

-‐ Blockbuster-‐driven character of distribuBon increased -‐ Difficult to draw a`enBon in a world of abundance

ExhibiBon -‐ Flexibility and differenBated theatrical programming -‐ VoD potenBal -‐ Long tail -‐ Increased ‘buzz’ for smaller Btles in shorter release window context

-‐ Digital cinema roll-‐out -‐ Slow-‐down home entertainment market -‐ Lack of strong pan-‐European VoD players -‐ Online licensing problems -‐ Piracy

Conclusions

• Hollywood majors dominate • Despite public support, European film industries

fragmented • Digitisation affecting the whole value network • Value network expanding and reconfiguring • Single market potential not taken up for now • Digital revenues do not offset non-digital losses • New power players are (again) based in US

Suggestions?

Thank you!