MEANINGFULLY DIFFERENT BRANDS

Charles Foster – Millward Brown MEAPraveen Abraham – Millward Brown Egypt

is the set of associations

(ideas, memories and

feelings) in the mind of a

consumer.

What is

a brand?KNOWLEDGE

Facts about the brand

(an understanding of what

it is, what it’s called,

what it looks like)

EMOTIONFeelings,

social values,

desirability

EXPERIENCEWhat the brand experience

is/would be like

(its benefits, how it is

used or found)

Meaningfully different brands,

properly amplified, create sustainable

financial value growth.

W E K N O W T H A T … .

Salient

DifferentMeaningful

The five key inputs…

Meets Needs

Affinity

Unique

Dynamic

Awareness Intensity

The MDS approach has inputs which short, quick, & easier to administer Please drag each brand onto the scale to indicate how different they seem to others in the market. You can place more than one brand in each box or leave a box empty. Please place all brands on the scale before continuing.This type of questioning improved the model fit by 16%

Further development work through BrandZ:

>40 countries, >50,00 brands, >800,000 consumers

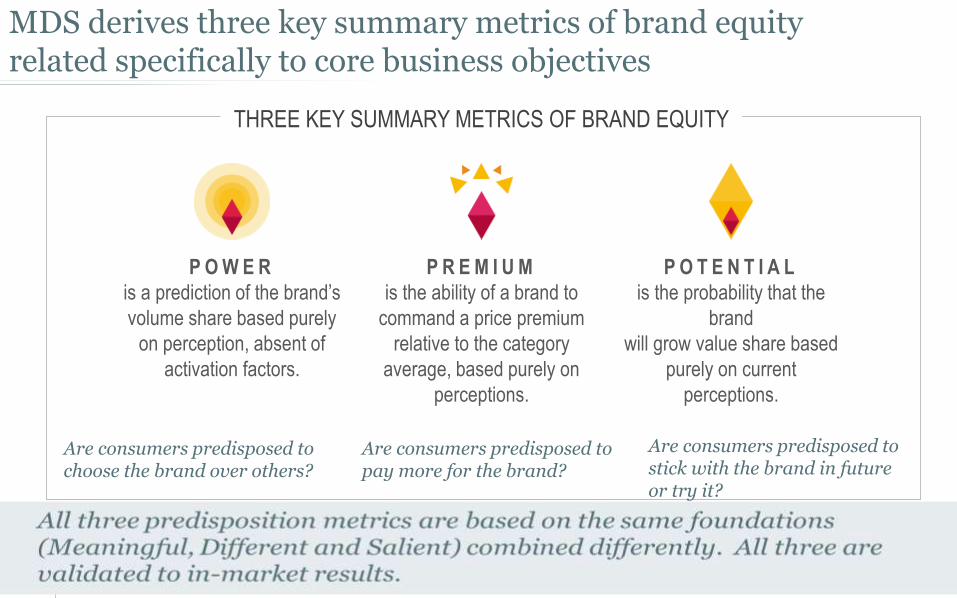

MDS derives three key summary metrics of brand equity related specifically to core business objectives

P O W E R

is a prediction of the brand’s

volume share based purely

on perception, absent of

activation factors.

P R E M I U M

is the ability of a brand to

command a price premium

relative to the category

average, based purely on

perceptions.

P O T E N T I A L

is the probability that the

brand

will grow value share based

purely on current

perceptions.

THREE KEY SUMMARY METRICS OF BRAND EQUITY

Are consumers predisposed to choose the brand over others?

Are consumers predisposed to pay more for the brand?

Are consumers predisposed to stick with the brand in future or try it?

Meaningfully different brands…

7

E A C H O F T H E S E M E T R I C S A R E C R E A T E D F R O M M E A S U R E S O F H O W M E A N I N G F U L , D I F F E R E N T A N D S A L I E N T B R A N D S A R E .

… Have much greater

POTENTIAL to gain

value share in the future

… Can command a

price PREMIUM

… Have the POWER

to capture significantly

MORE VOLUME

POWER

PREMIUM

POTENTIAL

Apple: unique personality and tangible product innovation = differentiation

worth paying for

137 248 131

137 158 272

Avr = 100

$147b

MEANINGFUL DIFFERENT SALIENT

Avr = 100

Coca-Cola: first to mind for billions of thirsty people = dominant volume share

for impulse category

$80b

10

Great metrics, derived from simple, short

questionnaires, need smart data

capturing techniques

Mobile interviewing is the fastest growing methodology in the world, because…

11

Consumers busier

Less accessible housing

Poorer quality ‘traditional’ data

Demand for faster feedback

Why consider mobile surveys?

12

ACTUALLY THE REAL QUESTION SHOULD BE WHY NOT?

1.91 BILLION

37% GROWTH

15% OF WEB

smartphones users by the end of 2015

– overtaking laptops and PCs*

in the number of global 3G subscribers in the past year**

traffic comes via mobile – more than double last year;

Mobile traffic share already over 50% in India and China***

*Source: e.Marketer Global report June 2014 **Source: Informa WCIS;

***Source: StatCounter Global Stats, 9/12

Mobile Internet

13

Mobile Internet

14

Egypt smartphone growth…

15SOURCE : e-marketer Dec 2014

18.2 million users in 2015

Among top 10 on growth rate

16

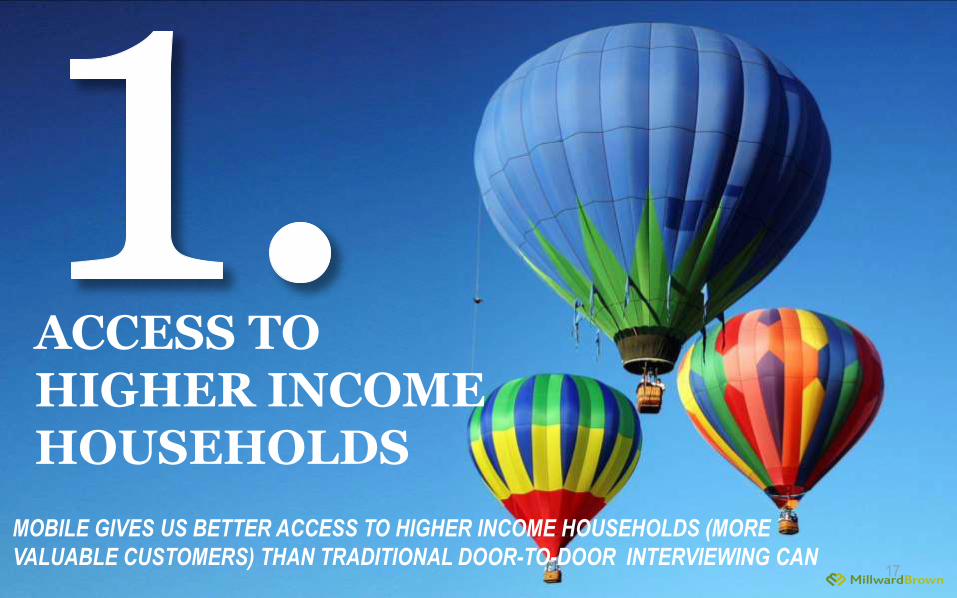

KEY INSIGHTS WE HAVE SEEN FROM MOBILE DATA

17

ACCESS TO HIGHER INCOME HOUSEHOLDS

MOBILE GIVES US BETTER ACCESS TO HIGHER INCOME HOUSEHOLDS (MORE

VALUABLE CUSTOMERS) THAN TRADITIONAL DOOR-TO-DOOR INTERVIEWING CAN

18

MOBILE DATA MATCHES UP TO MARKET SHARE

OVER TIME, MOBILE DATA MATCHES UP TO MARKET REALITY EVEN MORE DUE TO

THE ABILITY TO COVER WIDER GEOGRAPHIES NATIONALLY

19

MORE HONEST FEEDBACKSELF-COMPLETION MODE MEANS THAT RESPONDENTS

ARE MORE DISCRIMINATING TOWARDS BRANDS,

GIVING US MORE HONEST AND USEFUL FEEDBACK

20

NOT AN ISSUE CAPTURING OPEN ENDED RESPONSES

21

SCREEN SIZE DOESN’T MATTER –RESPONSES ARE CONSISTENT

22

MOBILE SURVEYS GIVE YOU GREAT SHORT TERM ADVANTAGES

Consumers are connected to their

mobile phones all the time and find

it comfortable and engaging as a

communication medium better

interview context

Studies have shown that without

interviewers (over)prompting, mobile data is

more discriminating between brands and

reflect market reality better better data

quality

Speed of data access and deliverables

increases significantly.

OUR QUALITY CONTROL MEASURES (all automated)

24

Brand Equity Study

completed via

Mobile in Egypt

Mobile Phone

Brands…

25

Data quality is impressive on

Mobile

Data quality is

impressive on Mobile

26

Increased Engagement

MOBILE CAPI

SYNCING IS MORE THAN JUST GETTING GREATER FREQUENCY

27

Technology

helps

getting

better

coverage

for the study

& proof of

data

capture

It helps us

zoom in into

every

location to

have the

spread of

interviews

Cairo

Alex

Study de ta i l s – Who & What?

29

Males and Females

Between 15 – 40 Years Old

Currently have an active

SIM in Egypt

Samples from Pan Egypt

1. Mobile handset brand

equity

2. Mobile internet behavior

Quick Facts

30

88%answered the surveys

using SMARTPHONE

38%Are from Dual SIM phone

46%Answered using a

SAMSUNG Device

3 DAYSTo conduct

514 interviews

Minutes on

average to

complete

the survey

No environment is 100% mobile-free anymore!!

Relaxing 89% Travelling 61% With Friends 55% Watching TV 54%

While in bed 50% While Eating 23% In a Store In toilet 13%13%

Handsets or Hand sticks?!

32

89% go online on their phone daily

87%I don’t leave their home without their smart phones

I first look into my phone for mails, messages, updates, or

calls once I wake up82%

Says that they would rather sacrifice TV than Smartphone86%

HOW CAN ADVERTISERS TAKE ADVANTAGE

35

The challenge for advertisers is to:

INTRODUCING THE BRAND PROPELLER

36

38.3 17 16.7 13.5 6.5

Meaningful

154

Different

127

Salient

149

135106

168

108

73

88

133

69

87

113

105

80

Take a Guess : Which Brands have higher Power?

Identify the propeller of brands.

37

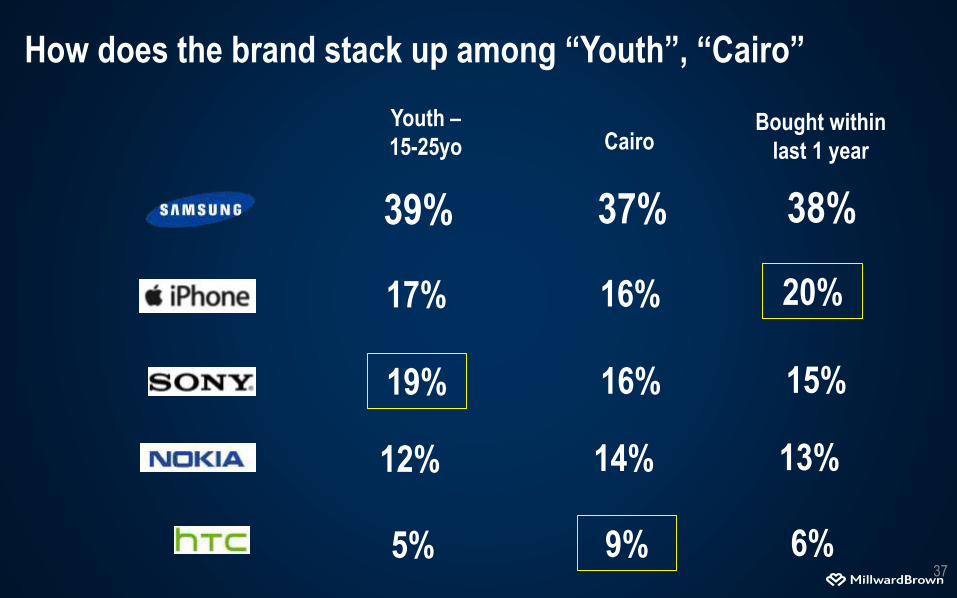

How does the brand stack up among “Youth”, “Cairo”

Youth –

15-25yo Cairo

39%

17%

19%

12%

5%

37%

16%

16%

14%

9%

Bought within

last 1 year

38%

20%

15%

13%

6%

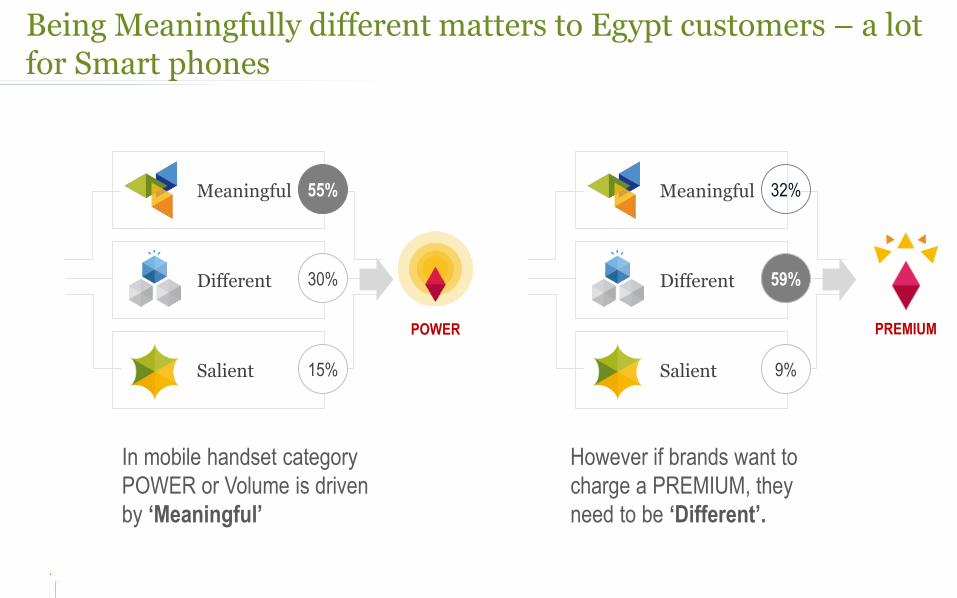

Being Meaningfully different matters to Egypt customers – a lot for Smart phones

Meaningful

Salient

Different

32%

59%

9%

Meaningful

Salient

Different

55%

30%

15%

POWER PREMIUM

In mobile handset category

POWER or Volume is driven

by ‘Meaningful’

However if brands want to

charge a PREMIUM, they

need to be ‘Different’.

Equity Map of mobile brands

39

iPhone along with Samsung and HTC are the meaningfully different brands ;

Microsoft and BB are considered different

Samsung

iPhone

SonyNokia

HTC

Huawei

Other Chinese Brands

Blackberry

LG

G-Tide

Microsoft

35

55

75

95

115

135

155

175

31 51 71 91 111 131 151

MEANINGFUL

DIF

FE

RE

NT

SIZE OF POINT = SALIENT

What contributes to being Meaningful & Different

in smart phone Brands?

40

Image Diagnosis - Marketing Levers

We build models for each study which help us identify how image associations group together

to drive the components of equity.

Emotional

Superior

Relevance

Service

Modern

Makes me feel empowered

Makes me feel always connected

Technologically advanced

Innovative brand

Offers a wide range of products

Easy to use

Best after sales services

Stylish design

Meaningful

Salient

Different

55%

30%

15%

POWER

Which attributes should I focus on to drive equity?

The emotional factors has the highest importance to be able to see the brand as

MEANINGUL and while technical superiority helps the brands to be seen DIFFERENT

31%

22%18%

12%

17%

Meaningful

Contribution to Meaningful

22%

30%18%

15%

15%

Different

11%

3%

57%

27%

2%

Salient

Contribution to SalientContribution to Different

Emotional Superior Relevance Service Style

Tapping in to brand’s potential

45

Potential of brands to grow in future

POWER

POTENTIAL

38.3 17 16.7 13.5 6.5

90 82 56 34 77

Momentum of mobile brands

47

HTC shows high growth potential to its share of equity while Nokia in Cooling off stage…

Samsung

iPhone

Sony

Nokia

HTC

Huawei

Other Chinese Brands

Blackberry

LG

G-TideMicrosoft

0

10

20

30

40

50

60

70

80

90

100

0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0% 35.0% 40.0% 45.0%

PO

TE

NT

IAL

POWER % (share)

Is y

our

bran

d se

t to

grow

in th

e fu

ture

?

Are consumers predisposed

to choose you?

HotHeating Up

Cold Cooling Off

HTC is a hot brand (with high

power and potential) among

high income and older

audience and from Cairo

MS Lumia is having a very

high momentum among lower

income and age audience

But the story doesn't ends here …

48

Predisposition doesn’t always translate to action. Distribution and pricing

factors often intervene in the pragmatic forms of availability, visibility &

affordability – these can be barriers or facilitators to purchase.

Brand

PredispositionBrand Selection

Hence, its necessary to understand the linkage between Predisposition and Volume…

49

Brand Selection

% of market which is

CONVERTED to you at

the point of purchase

(i.e. RISK)

% of market which is

DIVERTED away

from you

(i.e OPPURTUNITY)

The language is aligned to how you, as marketers, intuitively think about your brand’s performance

Samsung and Nokia are the only brand that gained on its market share with more conversion at POS than others…

50

Power Fulfilled

at point of sale

Diverted at

point of sale

To

tal s

har

e o

f cl

aim

ed u

sag

eConverted at

point of sale

Power Score 38.3% 17.0% 16.7% 13.5% 6.5%

25.5%

5.3% 4.8% 8.6%

1.7%

20.7%

2.4% 2.9%

20.7%

1.2%

12.8% 11.6% 11.9%

4.9% 4.9%

1

2

3Net gain/loss +7.9 -9.3 -9.0 +15.8 -4.2

Actual Volume 46.2% 7.7% 7.7% 29.3% 2.3%

51

Power Fulfilled

at point of sale

Diverted at

point of sale

To

tal s

har

e o

f cl

aim

ed u

sag

eConverted at

point of sale

Power Score 38.3%

25.5%

5.3% 4.8% 8.6%

1.7%

20.7%

2.4% 2.9%

20.7%

1.2%

12.8% 11.6% 11.9%

4.9% 4.9%

1

2

3Net gain/loss +7.9

Actual Volume 46.2%

9.13

iPhone Sony Nokia htc others

5.76 6.38 2.18

1. Whom I lost to / gained from?

Samsung gained on volume from iPhone, Sony and htc while losing majorly to Nokia (Lumia)

52

2. Why we gained / lost at POS – Waterfall chart

38.346.2

4.2 -2 -21.5

3.93.1

2.21-2.6

PowerScore

Notavailable

Attractivecolor /design

Salesmanreco

Freeapplications

Bundleoffers

Notdisplayed

User friendly Price ClaimedVolumeshare

Non availability and non display of other pre-disposed brands (iPhone, htc ) made

consumers buy Samsung …

Attractive color/design (of Lumia) coupled with sales man recommendation on windows

platform and price edge made consumers deviate from Samsung …

53

To Sum up

The MDS framework:

Digital data-collection

Helps you build meaningful brands & grow brand value

Holistic in approach, yet can diagnose in detail the

barriers & facilitators to brand growth

Validated and linked to brands’ financial performance.

Consumers are spending more time on digital devices

Gives us better access to different consumer profiles

Better quality data with realistically short questionnaires

54

create meaningful

IMPACT