Download - MO Insights Q1 2012

Page 1 of 10

A N E C O N O M I C A N D M A R K E T C O M M E N T A R Y B Y M I C H A E L O B U C H O W S K I , P H . D .

After the incredible volatility of 2011, the first quarter of

2012 brought back the nearly forgotten sense of

direction to the global markets. Investors’ focus shifted

towards the future and the continually improving US

economy. After being written off by many pundits, the US

is once again the driving force among developed

countries and is likely to drive the global economic

growth in the near future.

As a result, the US equity markets ended the quarter with

the best result since 2009. The Russell 1000 Growth

ended the quarter with a 14.69% return, the S&P 500 with

a 12.59% return and the Russell Top 200 growth with a

14.76% return for the quarter. The quarterly returns were

led by Financials (21.5%) and Information Technology

(21.1%), followed by Consumer Discretionary (15.5%),

Industrials (10.7%), Materials (10.6%), Health Care (8.4%),

Introduction

Global Risks and Global Response

Under another Mario taking over its reins, the European

Central Bank (ECB) finally became much more attuned to

the economic growth risks. Many have argued that ECB’s

prior obsession with real or imaginary inflation under

Jean-Paul Trichet contributed to the European economic

woes with repeated increases in interest rates enacted

with what proved to be the worst timing possible (July

2008 and July of 2011 are just two of the best

examples). In contrast to his predecessor, Mario Draghi’s

first order of business was to reverse the misguided

interest rate increases and to provide support and

increased liquidity to the European banking system that

was hanging on a thread on the edge of the abyss

threatened with significant exposure to the rapidly

deteriorating in value sovereign European debt.

The ECB’s decisive action that roughly followed the Fed’s

blueprint, provided the shock therapy that helped

markets regain composure and pushed many speculators

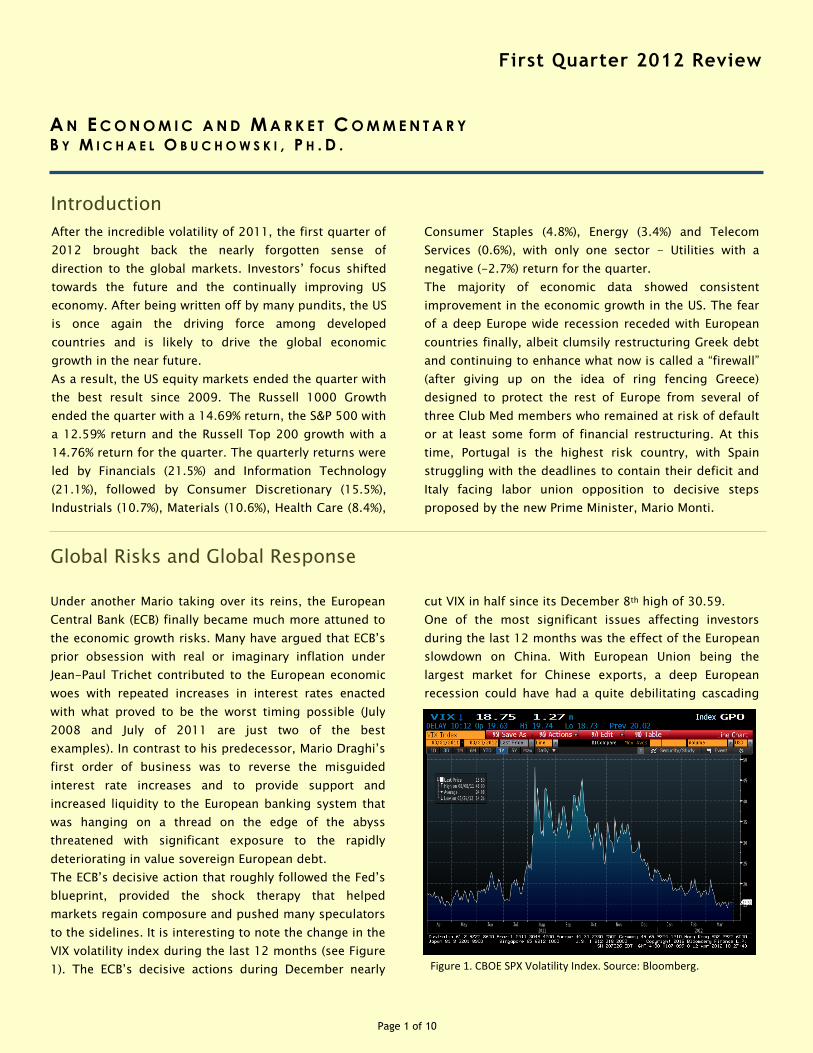

to the sidelines. It is interesting to note the change in the

VIX volatility index during the last 12 months (see Figure

1). The ECB’s decisive actions during December nearly

Consumer Staples (4.8%), Energy (3.4%) and Telecom

Services (0.6%), with only one sector - Utilities with a

negative (-2.7%) return for the quarter.

The majority of economic data showed consistent

improvement in the economic growth in the US. The fear

of a deep Europe wide recession receded with European

countries finally, albeit clumsily restructuring Greek debt

and continuing to enhance what now is called a “firewall”

(after giving up on the idea of ring fencing Greece)

designed to protect the rest of Europe from several of

three Club Med members who remained at risk of default

or at least some form of financial restructuring. At this

time, Portugal is the highest risk country, with Spain

struggling with the deadlines to contain their deficit and

Italy facing labor union opposition to decisive steps

proposed by the new Prime Minister, Mario Monti.

cut VIX in half since its December 8th high of 30.59.

One of the most significant issues affecting investors

during the last 12 months was the effect of the European

slowdown on China. With European Union being the

largest market for Chinese exports, a deep European

recession could have had a quite debilitating cascading

First Quarter 2012 Review

Figure 1. CBOE SPX Volatility Index. Source: Bloomberg.

Page 2 of 10

Page 2

First Quarter 2012 Review

effect around the world. If the Chinese economy slowed

down significantly, that would have affected global

demand for industrial commodities, seriously hurting the

economies of rapidly growing materials exporting

countries. A slowdown in the Chinese economy would

have also had a negative effect on the US economy.

Despite the common perception that US is primarily an

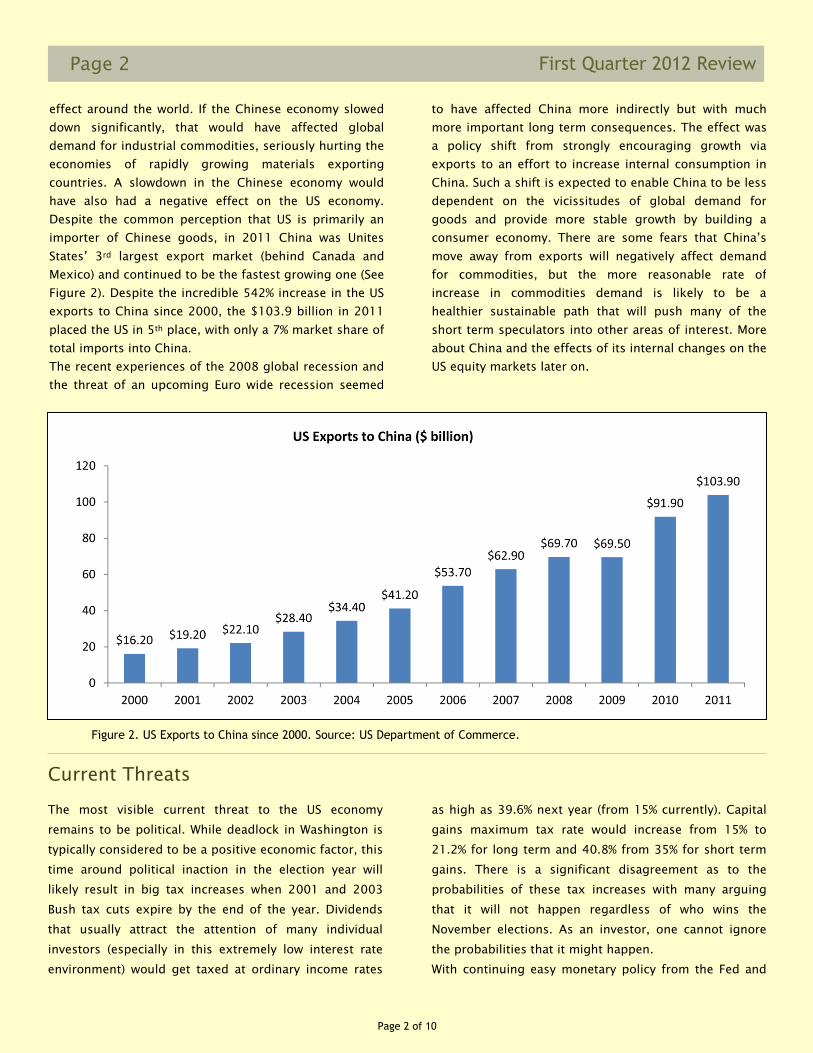

importer of Chinese goods, in 2011 China was Unites

States’ 3rd largest export market (behind Canada and

Mexico) and continued to be the fastest growing one (See

Figure 2). Despite the incredible 542% increase in the US

exports to China since 2000, the $103.9 billion in 2011

placed the US in 5th place, with only a 7% market share of

total imports into China.

The recent experiences of the 2008 global recession and

the threat of an upcoming Euro wide recession seemed

as high as 39.6% next year (from 15% currently). Capital

gains maximum tax rate would increase from 15% to

21.2% for long term and 40.8% from 35% for short term

gains. There is a significant disagreement as to the

probabilities of these tax increases with many arguing

that it will not happen regardless of who wins the

November elections. As an investor, one cannot ignore

the probabilities that it might happen.

With continuing easy monetary policy from the Fed and

to have affected China more indirectly but with much

more important long term consequences. The effect was

a policy shift from strongly encouraging growth via

exports to an effort to increase internal consumption in

China. Such a shift is expected to enable China to be less

dependent on the vicissitudes of global demand for

goods and provide more stable growth by building a

consumer economy. There are some fears that China’s

move away from exports will negatively affect demand

for commodities, but the more reasonable rate of

increase in commodities demand is likely to be a

healthier sustainable path that will push many of the

short term speculators into other areas of interest. More

about China and the effects of its internal changes on the

US equity markets later on.

Current Threats

The most visible current threat to the US economy

remains to be political. While deadlock in Washington is

typically considered to be a positive economic factor, this

time around political inaction in the election year will

likely result in big tax increases when 2001 and 2003

Bush tax cuts expire by the end of the year. Dividends

that usually attract the attention of many individual

investors (especially in this extremely low interest rate

environment) would get taxed at ordinary income rates

Figure 2. US Exports to China since 2000. Source: US Department of Commerce.

Page 3 of 10

Page 3 First Quarter 2012 Review

the future. One of the early measures indicating increase

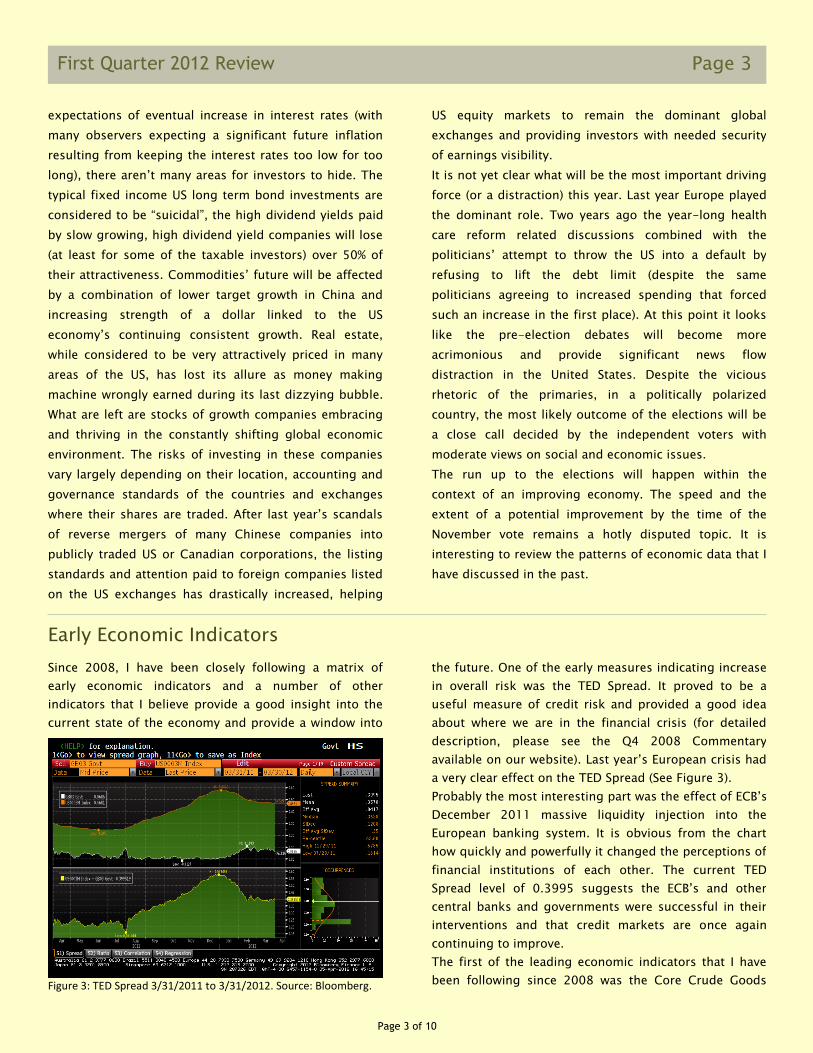

in overall risk was the TED Spread. It proved to be a

useful measure of credit risk and provided a good idea

about where we are in the financial crisis (for detailed

description, please see the Q4 2008 Commentary

available on our website). Last year’s European crisis had

a very clear effect on the TED Spread (See Figure 3).

Probably the most interesting part was the effect of ECB’s

December 2011 massive liquidity injection into the

European banking system. It is obvious from the chart

how quickly and powerfully it changed the perceptions of

financial institutions of each other. The current TED

Spread level of 0.3995 suggests the ECB’s and other

central banks and governments were successful in their

interventions and that credit markets are once again

continuing to improve.

The first of the leading economic indicators that I have

been following since 2008 was the Core Crude Goods

Since 2008, I have been closely following a matrix of

early economic indicators and a number of other

indicators that I believe provide a good insight into the

current state of the economy and provide a window into

expectations of eventual increase in interest rates (with

many observers expecting a significant future inflation

resulting from keeping the interest rates too low for too

long), there aren’t many areas for investors to hide. The

typical fixed income US long term bond investments are

considered to be “suicidal”, the high dividend yields paid

by slow growing, high dividend yield companies will lose

(at least for some of the taxable investors) over 50% of

their attractiveness. Commodities’ future will be affected

by a combination of lower target growth in China and

increasing strength of a dollar linked to the US

economy’s continuing consistent growth. Real estate,

while considered to be very attractively priced in many

areas of the US, has lost its allure as money making

machine wrongly earned during its last dizzying bubble.

What are left are stocks of growth companies embracing

and thriving in the constantly shifting global economic

environment. The risks of investing in these companies

vary largely depending on their location, accounting and

governance standards of the countries and exchanges

where their shares are traded. After last year’s scandals

of reverse mergers of many Chinese companies into

publicly traded US or Canadian corporations, the listing

standards and attention paid to foreign companies listed

on the US exchanges has drastically increased, helping

US equity markets to remain the dominant global

exchanges and providing investors with needed security

of earnings visibility.

It is not yet clear what will be the most important driving

force (or a distraction) this year. Last year Europe played

the dominant role. Two years ago the year-long health

care reform related discussions combined with the

politicians’ attempt to throw the US into a default by

refusing to lift the debt limit (despite the same

politicians agreeing to increased spending that forced

such an increase in the first place). At this point it looks

like the pre-election debates will become more

acrimonious and provide significant news flow

distraction in the United States. Despite the vicious

rhetoric of the primaries, in a politically polarized

country, the most likely outcome of the elections will be

a close call decided by the independent voters with

moderate views on social and economic issues.

The run up to the elections will happen within the

context of an improving economy. The speed and the

extent of a potential improvement by the time of the

November vote remains a hotly disputed topic. It is

interesting to review the patterns of economic data that I

have discussed in the past.

Early Economic Indicators

Figure 3: TED Spread 3/31/2011 to 3/31/2012. Source: Bloomberg.

Page 4 of 10

Page 4

First Quarter 2012 Review

Producer Price Index. The CCG Index provides insight

into the earliest stages of capital goods production and

is especially sensitive to turning points in the economic

activity, as we can see in Figure 4. It proved to be an

important indicator of changes in future industrial

production, suggesting the bottoming of the recession in

early 2009.

Figure 5. The Primary Metals Index (US Durable Goods New Orders) since 3/31/2006. Source: US Census Bureau, Bloomberg.

The Core Capital Goods Order Index is considered to be

one of the best indicators of business investment

spending. Technically known as the New Orders of

Nondefense Capital Goods Excluding Aircraft, it provides

a broad overview of business investing, while controlling

for the volatile aircraft orders and defense spending that

is rarely highly correlated to economic activity or

expectations. Similar to the other indices, it is currently

at a level comparable to its prior peak in 2008 (See

Figure 6).

The Primary Metals Index captures the raw materials

being ordered by large manufacturers and it proved to be

an important indicator of changes in future industrial

production. At its current level of 26955 (see Figure 5),

the PMI is just slightly above its prior peak in 2008,

suggesting a continuing increase in expectations for

industrial production.

Figure 4. Core Crude Goods Producer Price Index. Source: Bureau of Labor Statistics, Bloomberg.

When selecting the Baltic Dry Index in early 2008, I

expected that it was going to be a useful indicator of

global economic activity. The BDI provides an assessment

of the price of moving raw materials by sea. It covers 26

shipping routes worldwide and is a composite of the

Baltic Capesize, Panamax, Handysize ansd Supramax

bulk carrier indices. To my surprise, instead of being an

index of global economic activity, the BDI proved to be

(at least so far) a sensitive index capturing economic

activity in China. Whether this will remain so in the future

(considering China’s efforts to refocus on domestic

consumption) is certainly a question. However, the recent

rebound in the BDI after a sharp decline in early 2012

(see Figure 7) suggests that current worries about a

significant economic slowdown in China might be

incorrect.

The first three indicators presented above showed a

consistently improving economy since early 2009. The

BDI, although very volatile and seemingly driven by the

vicissitudes of Chinese economy has also recovered from

its 2008 lows.

Figure 6. Core Capital Goods Order Index (New Orders of Nondefense Capital Good Excluding Aircraft & Parts). Source: US Census Bureau, Bloomberg.

Page 5 of 10

Page 5 First Quarter 2012 Review

It is no surprise that the indicators that have only

recently started providing a more optimistic pattern are

both related to the real estate. The Architecture Billing

Index (ABI) is a leading indicator of commercial

construction activity, capturing the approximately nine to

twelve months lag time between architecture billings and

construction spending. The ABI is derived from a

monthly “Works-on-the-Boards” survey sent to a panel

of the American Institute of Architects member owned

firms. The ABI is a diffusion index and level of above 50

represents increase in architectural billings. Figure 8

illustrates how, after a recovery from the 2008/2009

doldrums, the index crossed 50 in late 2010 to once

again decline until pretty much the end of 2011, only

stabilizing above 50 during the last few months. It looks

like there is finally some hope for commercial

construction activity. The Private Housing Authorized by Building permits

Index (BPI) provides information about expectations for

residential real estate activity based on the issuance of

building permits. There is no question that the latest

seasonally adjusted BPI of 715 thousand (Figure 9) is far

from its peak of nearly 2 million permits issued per

month in April 2006 and less than half of the 10 year

median of 1,553,000 seasonally adjusted monthly

permits.

However, the relatively consistent increase that started in

early 2011 brought the number of building permits

significantly above its 2009 trough of 513 thousand

permits in March 2009 and is currently at its highest

level since 2008. There are several negative factors

affecting private housing construction (e.g., continuing

foreclosure overhang and difficulty in obtaining

construction loans). Despite some potential effects of

warmer than usual winter (although one would expect

weather to have an effect on actual construction rather

that permits), the pattern is suggesting a continuous if

sluggish improvement. Because of its long term

reliability as an economic indicator and it large multiplier

effect (by some estimates, construction of 1,000 single

family homes generates 2,500 full time jobs and nearly

$100 million in wages), it is an important indicator to

follow.

Figure 7. The Baltic Dry Index since 3/31/2006. Source: Baltic Exchange, Bloomberg.

Figure 8. The Architecture Billings Index. Source: American Institute of Architects, Bloomberg.

Figure 9. Private Housing Authorized by Building Permits Index. Source: US Census Bureau, Bloomberg.

Page 6 of 10

Page 6

First Quarter 2012 Review

It is hardly a surprise that many of the lagging economic

indicators remain depressed despite the significant

improvement over time. In the election year, we are likely

to hear a lot of rhetoric with focus and interpretation

dependent more on political affiliation rather than

objective analyses of available data.

One of the most obvious targets of political spins will be

the data related to employment. The official headline

unemployment measure is the U-3 (total unemployed, as

a percent of civilian labor force). The U-3 rate has

declined significantly from its recession high, but it

remains above 8%.

A necessary part of the continuing decline in

unemployment is jobs creation. Based on the average

population growth and the average Labor Participation

Rate for the last 10 years, it is necessary to add

approximately 150,000 jobs every month just to keep up

with the natural workforce growth. As with many other

economic data, there is a lively discussion about the

reasons for recent declines in the Labor Participation

Rate. Some argue that the retiring baby boomers will

continue to shrink the labor force and help the

unemployment numbers drop even faster. Others argue

that the primary reason for a declining Labor

Participation Rate is that many people give up searching

for work and leave the civilian labor force temporarily,

only until the job prospects improve. According to the

Bureau of Labor Statistics, the number of persons not in

the labor force increased by 2.69% during the last 12

months. At the same time, the number of Persons who

Many argue that the U-3 is too conservative of a measure

and that we should use a more liberal measure to fully

evaluate the labor underutilization, not just strict

unemployment. The most liberal alternative measure

from the Bureau of Labor Statistics is the U-6: Total

unemployed, plus all marginally attached workers, plus

total unemployed part time for economic reasons, as a

percent of the civilian labor force plus all marginally

attached workers. The U-6 rate is always higher than the

U-3 and provides a better picture of the labor utilization

trends. The spread between these two measures typically

widens during the periods of prolonged high

unemployment due to economic contraction. Because the

U-6 includes all marginally attached workers who are not

counted in the civilian labor force and are not included in

the U-3 unemployment, the U-3 vs. U-6 spread can

better illustrate changes in unemployment than either of

the measures alone. As we can see in Figure 11, despite

the decline in U-3 and U-6 measures, the U-3/U-6

Lagging Economic Indicators

Currently Want a Job declined by 3.34%, with a 3.37%

decline in those Marginally Attached to the Labor Force

and a 6.08% decline in the Discouraged Workers

subcategory. These data suggests that the retiring

individuals might be the primary reason for the Labor

Participation Rate decline, although it is possible that

decisions to retire might have been precipitated by the

perceived lack of job opportunities.

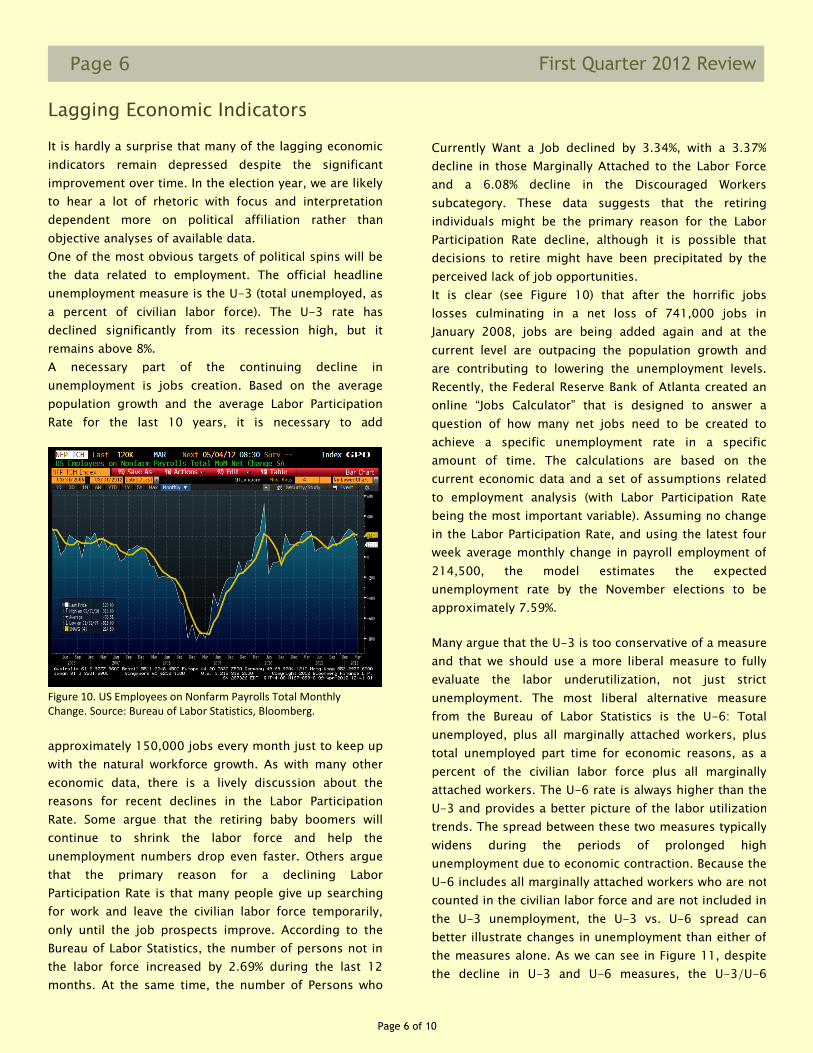

It is clear (see Figure 10) that after the horrific jobs

losses culminating in a net loss of 741,000 jobs in

January 2008, jobs are being added again and at the

current level are outpacing the population growth and

are contributing to lowering the unemployment levels.

Recently, the Federal Reserve Bank of Atlanta created an

online “Jobs Calculator” that is designed to answer a

question of how many net jobs need to be created to

achieve a specific unemployment rate in a specific

amount of time. The calculations are based on the

current economic data and a set of assumptions related

to employment analysis (with Labor Participation Rate

being the most important variable). Assuming no change

in the Labor Participation Rate, and using the latest four

week average monthly change in payroll employment of

214,500, the model estimates the expected

unemployment rate by the November elections to be

approximately 7.59%.

Figure 10. US Employees on Nonfarm Payrolls Total Monthly Change. Source: Bureau of Labor Statistics, Bloomberg.

Page 7 of 10

Page 7 First Quarter 2012 Review

spread stayed close to its high throughout 2011 and

most of 2011. The U-3/U6 spread has only started

declining at the end of 2011 and continued its decline in

early 2012, supporting the data suggesting long awaited

improvements in the labor market.

There are several interesting measures closely related to

the changes in unemployment. One of the more

important measures is the Average Weekly Hours worked

(see Figure 12). With average weekly hours at a level

comparable to 2007, it is likely that companies will have

to increasingly focus on hiring new employees, with

existing employees unable to provide more working time

and reaching limits of productivity improvements (Figure 13).

Throughout the recession we have heard that for

unemployment rates to decline, the Initial Jobless Claims

have to remain below the magical number of 400,000.

This weekly measure is very volatile and is frequently

subject to large revisions. It is best interpreted as a four-

week moving average (See Figure 14). Despite all the

noise in the financial media every time the Initial Jobless

Claims do not match the average expectations of the

economists (which is basically every week), it would be

very difficult to deny that the pattern is strongly

supportive of continuing declines in unemployment.

Similarly to the U-3/U-6 spread, the Initial Jobless

Claims accelerated their decline towards the end of 2011

and in the first quarter of 2012.

Figure 11. U-3 and U-6 Unemployment and U-3/U-6 spread since 1994. Source: Bureau of Labor Statistics, Bloomberg.

Figure 12. Average Weekly Hours of Production of Nonsupervisory Workers on Private Nonfarm Payrolls. Source: Bureau of Labor Statistics, Bloomberg.

Figure 13. US Nonfarm Business Sector Output Per Hour YoY Change. Source: Bureau of Labor Statistics, Bloomberg.

Figure 14. US Initial Jobless Claims. Source: Department of Labor, Bloomberg.

Page 8 of 10

Page 8

First Quarter 2012 Review

With overall improvement in the employment markets,

some commentators focus on the plight of those already

unemployed. The average duration of unemployment has

continued to decline to 39.4 from its high 40.9 weeks at

the end of November 2011. Those unemployed for a

longer period of time typically have a much more difficult

time finding jobs. With that in mind, one would expect

the difference between the average length of

unemployment and the median length of unemployment

to be always positive. An increasing average vs. median

unemployment spread suggests a shift in the distribution

towards longer periods of unemployment, as one might

expect during a recession. Despite the decline in both

the mean and the median length of unemployment, the

percentage of unemployed for 27 weeks or more remains

stubbornly high at 42.5% and the spread between the

mean and median remains close to its recent peak (See

Figure 15).

Another interesting measure of employment is the

Diffusion Index of Employment Change (Figure 16). This

index represents a percentage of industries (within the

347 industries with private nonfarm payrolls) with

increasing employment, plus on-half of the industries

with unchanged employment. Diffusion Index of 50

indicates an equal balance between industries with

increasing and decreasing employment. Despite some

volatility in this monthly measure, the pattern of data

suggests continuing improvement in nonfarm payroll

hiring.

By now there are quite a few tools in our research and

critical thinking toolset. Overall, the early or coincidental

economic indicators suggest continuing economic

growth, at least in the US. Those indicators capturing real

estate markets and unemployment show steady

improvement in the still fragile environment. One issue

that continues to stand out is the structural

unemployment among those who have been out of work

for a long period of time.

There is also quite a disparity of opinions regarding the

rate of growth of the US economy for the rest of 2012.

The pessimists point towards the historically unusual

contribution of exports to the GDP, the potentially

Summary

unsustainable buildup of inventory, the threatening

“fiscal cliff” with expiration of government stimulus and

simultaneous tax increases, potentially deepening

recession in Europe and the economic slowdown in

China. The optimists look at the highly unusual

continuing cuts in government spending that affects the

GDP, the large difference between the Gross Domestic

Income (GDI) and Gross Domestic Product (GDP) that

might explain the acceleration in nonfarm employment,

the outstanding profitability among large companies

(with more than $1.24 trillion in corporate cash

holdings), signs of decisive decision making in Europe

combined with strengthening of German economy and

Figure 15. Mean vs. Median US Unemployment Duration. Source: Bureau of Labor Statistics, Bloomberg.

Figure 16. Employment Diffusion Index 1 Month. Source: Bureau of Labor Statistics, Bloomberg.

Page 9 of 10

Page 9 First Quarter 2012 Review

China’s determination to maintain at least 7.5% GDP

growth rate of their increasingly opening economy.

The emerging markets are rapidly becoming a significant

part of the global economy. Jim O’Neill who in 2001

coined the term BRIC (Brazil, Russia, India and China) to

identify the countries that would significantly growth

their share of the world economy (from combined 8% in

2001), has added the Next Eleven (N-11) group of

countries in 2005 and in early 2011 decided that many

of those countries are no longer “emerging markets” but

rather “Growth Markets” that will increasingly influence

the global economic growth. Adding such framework to

our focus on the G7 will certainly help in the

understanding and analysis of future economic changes.

With China surpassing Japan as the world’s second

largest economy in the second quarter of 2010, the

effects of changes in China’s economic policies are

increasingly felt around the world. One of the interesting

developments that I have been closely following for some

time is the increasing openness to allowing Chinese

citizens to invest outside of mainland China. Until now,

the primary vehicle for individuals who wanted to invest

globally was the Qualified Domestic Institutional Investor

(QDII) program, originally extended to investment fund

firms in 2006. There are many limitations to the QDII

funds, including size quotas, maximum exposure to

stocks and countries where funds can be invested. After

a few aborted attempts, China’s State Council announced

that they are studying allowing residents of Wenzhou

(one of the earliest cities in China to open to the world in

1978 and considered to be the birthplace of China’s

private economy) to invest directly overseas. Although

the details of such a potential approval are not yet clear,

it might become a precursor to expanding it nationwide

after testing it in Wenzhou. With China’s central bank

encouraging Chinese businesses to invest overseas to

diversify its $3.2 trillion of foreign exchange reserves, I

believe that approval for individual investors to invest

overseas is just a question of time. China has the world’s

highest savings rate at more than 50 percent of the

economic activity. Of the more than $12.5 trillion in

deposits, 46% (or $5.75 trillion) comes from households.

With the expected opening of global markets to Chinese

citizens, at least some of those deposits will find their

way overseas and will likely have a significant effect on

the demand for all types of investable assets, providing a

likely boost to the equity markets.

Regardless of the level of optimism and the timing of

potential large inflows into securities markets from the

growth economies, it is clear that the global economy is

still fragile. With ECB joining other central banks, the

monetary policies from every major central bank are

already aggressively easy (Bank of England and Bank of

Japan, ECB and The Fed) or are in the process of easing

(e.g., Bank of China). Those aggressive policies combined

with excess liquidity are likely to continue for the time

being, continuing to boost prices of risky asset classes.

Many of the investors who remain on the sidelines

sooner or later will have to decide on coming back to the

markets and investing more than $7 trillion of assets

invested in money market mutual funds, saving accounts

and CDs. In addition, the lending capacity of depository

institutions is at an all time high and can provide a

significant boost to the economic growth as the

perception of the economy continues to improve. Since

the housing crisis, many depository institutions

continued to build excess cash liquidity. With continuing

slow business and consumer lending combined with fear

of rising interest rates, they have been investing their

rising cash primary into short term instruments that

quickly mature, adding to their cash liquidity. In fact,

$1.5 trillion is currently held by depository institutions in

their accounts at Federal Reserve Banks in excess of their

required reserve and contractual clearing balance.

Until we all agree to adopt a new economic paradigm

focused on Gross National Happiness (as recommended

last year by the UN Resolution 65/309), the differences

of expectations and opinions will remain. After the

prolonged global recession, a rising number of

economists and politicians point out to the lack of

increases in self reported happiness and life satisfaction

in developed countries during several decades of rising

wealth. Hopefully, focus on happiness and satisfaction

will become more important in the future as the global

economy continues its slow and bumpy recovery.

Michael Obuchowski, Ph.D.

Page 10 of 10

Page 10

First Quarter 2012 Review

Disclosures

The foregoing letter is qualified by the following notes:

1. The S&P 500 Index consists of 500 stocks

chosen for market size, liquidity and industry

group representation. It is a market-value

weighted index with each stock’s weight in the

Index proportionate to its market value. The

Index is one of the most widely-used

benchmarks of U.S. equity performance.

2. The Russell Top 200 Growth Index measures the

performance of the especially large cap segment

of the U.S. equity universe represented by stocks

in the largest 200 by market cap that exhibit

growth characteristics. It includes Russell Top

200 Index companies with higher price-to-book

ratios and higher forecast growth values. The

companies also are members of the Russell 1000

Growth Index. The Russell Top 200 Growth Index

is constructed to provide a comprehensive and

unbiased barometer of this larger cap growth

market. The Index is completely reconstituted

annually to ensure new and growing equities are

included and that the represented companies

continue to reflect growth characteristics.

3. The Russell 1000 Growth Index measures the

performance of the large-cap growth segment of

the U.S. equity universe. It includes those Russell

1000 companies with higher price-to-book

ratios and higher forecasted growth values. The

Russell 1000 Growth Index is constructed to

provide a comprehensive and unbiased

barometer for the large-cap growth segment.

The Index is completely reconstituted annually to

ensure new and growing equities are included

and that the represented companies continue to

reflect growth characteristics.

4. The indices referred to herein are unmanaged

and therefore do not have any transaction costs,

advisory fees or similar expenses to which a

client account would be subject. It is not

possible to invest in these indices. The indices

are for comparison purposes only. It should not

be assumed that a composite will invest in any

specific securities that comprise the indices.

Performance for all indices includes the

reinvestment of dividends.

5. There is no guarantee that the matrix of

economic indicators (or each indicator

individually) can accurately predict profits or

losses in the markets or the composite. The

matrix of indicators discussed herein is not

intended to determine investment decisions.

Other indices or economic indicators may reflect

differing or contrary results. There is always the

potential for gains as well as the possibility of

losses.

6. This letter is not an offer or solicitation.