Download - Monetizing the Mobile Channel

2014 Momentum Webinar Series:

Monetizing the Mobile ChannelAin’t it About Time?

April 23, 2014

• Momentum series• Polls• Q/A

Welcome

Katherine Jansen is the Senior Manager, Business Development at Digital Insight, an NCR subsidiary. She is responsible for identifying and executing strategic alliances that extend the company’s mission to its financial institution customers. Katherine previously served as Digital Insight’s leader of corporate strategy, Senior Vice President of Marketing and Senior Manager of Customer Experience.

Introduction

TodayToday’s session will be a success if you:

• Leave thinking that you’ve got to figure out mobile strategy and where you stand

• Rethink the mobile market

• Rethink channel profitability

Source: Federal Reserve, Consumers and Mobile Financial Services 2014

Business as Usual?

Source: Bankrate.com © March 2014 The Financial Brand

Let’s look at it from a different perspective

Mobile is table stakes

Source: Novarica © April 2014 The Financial Brand

And you’ve seen the demographics…

Source: Novarica © March 2014 The Financial Brand

What About Retail?

Source: Pew, January 2013

Mobile Commerce CAGR 2011-2015

Source: Forrester Research, 2013

Mobile POS Payments CAGR 2011-2018

Source: Mercator Advisory Group

• Do you have a defined mobile strategy?

– Yes, and it is well-socialized

– Yes, senior management knows it

– I think so

– No

• How frequently is the strategy updated?

– Every quarter

– Once a year

– When the board asks about it

Polling Questions – Mobile Strategy

P&L View• Revenue

• Income

• Expense reduction

Direct or indirect contribution Lifetime Value View• Customer profitability

• Customer retention

• Infrastructure

Applying the Filter of ROI:Mobile Investments Should Drive:

Showrooming

With mobile device in hand, consumers also consulted their balances in real time before making a purchase, and 50 percent decided against making purchase for lack of available funds.

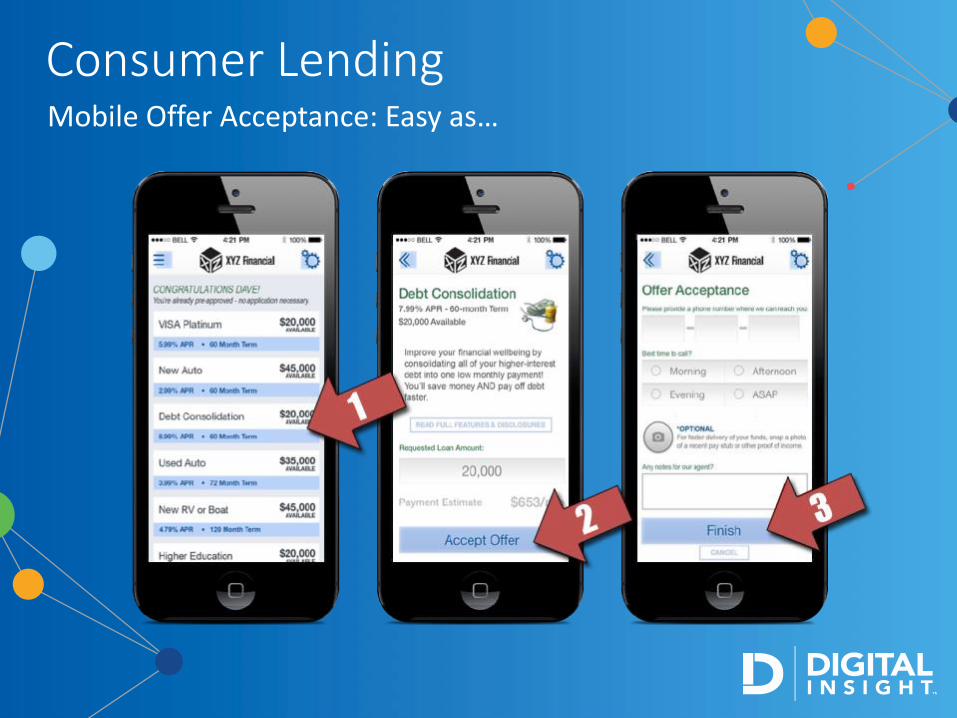

Consumer LendingMobile Offer Acceptance: Easy as…

Merchant POS?

• Similar benefits as retail

• Offers, promotions, pre-staging

• Transactional net promoter

• Appointments and advance check in

iBeacon in the Branch

• Are you evaluating iBeacon for your branches?

- Yes

- No

Polling Question - iBeacon

Reduce Expense

Source: Javelin Strategy & Research, Leveraging an Omnichannel Approach to Drive 1.5B in Mobile Banking Cost Savings, July 2013

Customer Retention

Among younger consumers,

technology and innovation was of

greatest importance, with the reasons for switching primary banks including:

"My previous bank didn't offer the

level of technology/innovation that

I wanted”

"My previous bank didn't offer the

online services that I needed”

"My previous bank didn't offer the

mobile services that I needed"

Source: AlixPartners (March, 2014)

Mobile driving increased engagement and activity; banking no different

Logins / Month

Debit Purchases / Month

Retention Rate

15

85%

10.51

22

93%

17.35

30

93%

Offline Online without Mobile

Online with Mobile

Increase Marketing Traffic:

• Access their financial information

65% more frequently 1

Increase Revenue:

• Conduct 40% more monthly

debit card purchases 2

• 8 additional debit card purchases/month could equal

$32 additional revenue/year

per customer 2

¹ Internal study of 36 Digital Insight FI customers, July 2009 through March 2014; claim based on comparison to Digital Insight online non-mobile consumers. ²Internal study of 29 Digital Insight FI customers, July 2009 through March 2014; claim based on comparison to Digital Insight online non-mobile consumers with an estimated interchange fee of $0.35 current as of 2012.

• Define, regularly update and socialize a living, breathing mobile strategy for your financial institution.

• Identify your points of focus for ROI– P&L view

– Lifetime value view

– Defensive strategy

– Growth strategy

• Measure, analyze, iterate regularly

What is your mobile strategy?

Disruptors

Chase “Quick Checkout”

Barclays Mobile Wallet

Google Mobile Wallet

2929© CELENT

1PayPal’s open wallet

Source: PayPal and the Next Web

Coinbase Mobile - SMS

WyWallet in Sweden• Started by 4 largest

mobile companies• 1.2 million consumers

using (only 9.6 million in all of Sweden)

• Accepted by 4,600 merchants there, including McDonald’s and Burger King.

• Oh – doesn’t run on card rails.

Wearables

Millenials….yup, again

• There is an opportunity to out-innovate

• Identify disruptors & partner with them– Think about your “silos” and where

disruptors can elevate your game

• Drop a pebble and create a ripple

• Disruptors can be your lunch

• Look for innovative partners

• Embrace & cause disruption

If you can’t beat ‘em, join ‘em?

A disruptor/partner story

• Online credit delivery

platform with automated

loan application,

underwriting, origination,

packaging and account

management

• Specifically targeted to

smaller SBA loans.

• Small bank generates 50

loans for over $1M since

testing in October.

Small bank & this company jointly create

Expansion

• New areas of revenue/income

• New ways of doing business that attract more customers or reduce expenses

• Brand evolution

Protection

• Customer retention

• Brand importance

• Expense reduction

• Future revenue streams

Applying the Filter of Innovation/Experiments:

Mobile Investments Should Drive:

Channel Profitability

• Do you measure channel profitability?

– Yes

– No

• Do you have a way to measure “contribution”?

– Yes

– No

Channel Profitability – polling question

• Income– Value of increased balances

– Value of retention

– Interest income

– Fee income

• Expenses– FTEs for creating/maintaining

channel

– Marketing expenses

– Solutions provider’s expense

Channel Profitability: probably looks something like this

Exactly what channel is this?

Before

Exactly what channel is this?

After

What profitability lever does interactive teller push?

Does iBeacon “contribute” or enable?

What Channel is this?

• Decides not to buy yet, but do more research online . . .

• GPS locator sends a push notification with a 20% discount

• Your customer visits an electronics store for washer and dryer

• He’s convinced, downloads coupon, returns to the store and makes purchase with your card

• Goes to OLB to check funds and finds 20% discount again

Apologies to the accountants…• Take a Return on Investment approach

– Define the expected benefits and time period

– Take a lean start up approach if possible to iterate into a solution

– Measure, analyze, iterate

• Take a “Test the Hypothesis” approach– Fund some experiments

– Lean start up, minimum viable product

– Define your learning plan and instrument the experiment so you can analyze.

• Re-evaluate traditional channel profitability and think more of contribution.

Questions?

www.digitalinsight.com

Thank you!

June 2014: Security & Compliance in the Age of IoE

Alan Akahoshi, Product Manager, Digital Insight

Visit Us:

2014 Momentum Webinar Series:

Monetizing the Mobile ChannelAin’t it About Time?

April 23, 2014