N O R T H E R N T R U S T

© 2015 Northern Trust Corporation

June 2, 2015

Catholic Charities and the Archdiocese of Chicago

11th Annual Tax and Estate PlanningSeminar for Professionals

“The Good Giver: An Exploration of Tax-Wise Charitable Giving”

Suzanne ShierWealth Planning Practice Executive andChief Tax Strategist/Tax [email protected]

Rev. 6-1-15 (v13)

2

The Good Giver

“To give away money is an easy matter and in any man’s power. But to decide whom to give it and how large and when and for what purpose and how, is neither in every man’s power nor an easy matter.”

Aristotle

3

The Good Giver

Giving TodayGiving TomorrowGiving Choices – Donees and DonationsGiving Choices – National and InternationalGiving Choices - Giving VehiclesGiving Choices – Transmitting Value(s)

4

The Good Givers’ Giving

Source: Giving USA 2014, The Annual Report on Philanthropy for the Year 2013

Giving by individuals is the greatest source of giving

5

The Good Givers’ Recipients

Source: Giving USA 2014, The Annual Report on Philanthropy for the Year 2013

The majority of giving recipients are religion, education and human services

6

The Good Givers’ Level of Giving

Giving levels are once again increasing

Source: Giving USA 2013: The annual Report on Philanthropy for the Year 2012 (Chicago: Giving USA Foundation, 2013), p. 26

7

The Good Givers’ Generosity

Giving among income groups is greatest at the highest and lowest income levels

Source: IRS 2011 Statistics of Income (SOI)

8

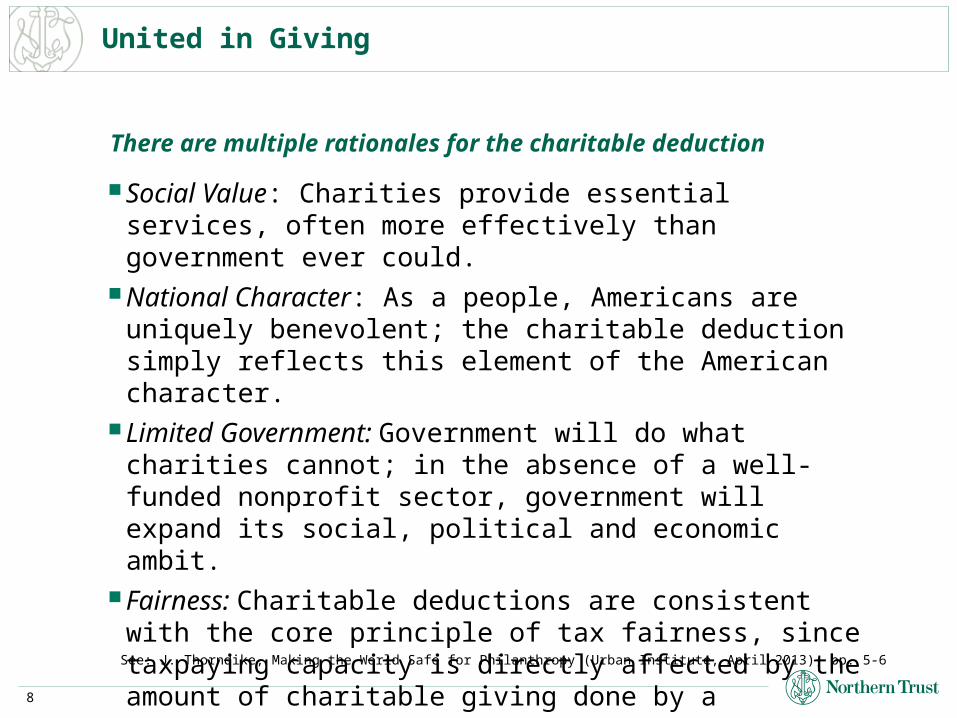

United in Giving

Social Value: Charities provide essential services, often more effectively than government ever could.

National Character: As a people, Americans are uniquely benevolent; the charitable deduction simply reflects this element of the American character.

Limited Government: Government will do what charities cannot; in the absence of a well-funded nonprofit sector, government will expand its social, political and economic ambit.

Fairness: Charitable deductions are consistent with the core principle of tax fairness, since taxpaying capacity is directly affected by the amount of charitable giving done by a taxpayer.

There are multiple rationales for the charitable deduction

See: J. Thorndike, Making the World Safe for Philanthropy (Urban Institute, April 2013), pp. 5-6

9

The Good Givers’ Heritage of Giving

1917 – War Revenue Act of 1917Enacted the individual charitable deduction

1944 – Revenue Act of 1944 1981 – Economic Recovery Act of 1981

Expanded the charitable deduction to non-itemizer individuals 1986 – Tax Reform Act of 1986

Charitable deduction escaped the 2% floor 2006 – Pension Reform Act of 2006

Temporary direct contribution from IRA

The charitable deduction has a long standing history in the tax code

10

What the Good Giver Gives

Non-cash contributions$49 billion in non-cash contributions (22.2 million returns) in 2012One-third of the returns (7.6 million) report $42.9 billion in

contributionsTaxpayers age 65+ gave the most (cash and non-cash)

Asset Value Share

Corporate stock $16.8 billion 39.1%

Mutual funds $1.7 billion 2.8%

Clothing $9.3 billion 21.8%

Household items $3.7 billion 8.7 %

Art and collectibles

$1.2 billion 2.8%

Non-cash contributions remain popular for donations

Source: IRS Statistics of Income, Spring 2015

11

What the Good Giver Gives

Art and collectibles“Making Charitable Gifts of Art – A Primer for Donors”Capital gain or ordinary income propertyUse for a related purpose

Art for a medical school or for liberal arts college?

An income tax deduction consideration, but not a gift or estate tax issue

Art Advisory Panel

344 items reviewed with recommended adjustments for 56%

Giving of art and collectibles is of particular interest

12

What the Good Giver Gives

Individual Retirement AccountsOptimal testamentary giving vehiclePension Protection Act of 2006 direct IRA gift provision

Temporary

Age 70-1/2 or older

Owner’s or inherited IRA

Only IRAs, not 40(k)s

$100,000 maximum per taxpayer per year

Direct to qualified charity

· Public charity (but not donor advised funds or supporting organizations)

· Private operating foundations

Increased income tax rates makes giving from retirement assets even more attractive

13

What the Good Giver Gives

Split-interest charitable trusts and pooled income funds in 2012113,688 split-interest trust returns$11.7 billion in gross income$4.3 billion in charitable distributions93% charitable remainder trusts

80% CRUTs (majority 5-6%)

14% CRATS6% charitable lead trusts1% pooled income funds

Many donors continue to favor giving in trust

Source: Rosenthal, Lisa, Split-Interest Trust, Filing Year 2012, Statistics of Income Bulletin 51 (Winder 2014)

14

The Global Good Giver

Income tax charitable contribution deductionLimited to donees organized within the USQualifications

US charitable donee may use funds abroad for charitable purpose

US charity may make donations to a foreign charity

· “Friends” are permitted· “Conduits” are not

Giving globally is an increasing priority, but it has limitations

15

The Global Good Giver

Gift and estate tax charitable deduction

There is no (US) place of organization requirement

But, there is a Section 501(c)(3) status notice requirement

Exception if foreign organization receives less than 15% of its support from US sources

The estate and gift tax rules for global giving are broader

16

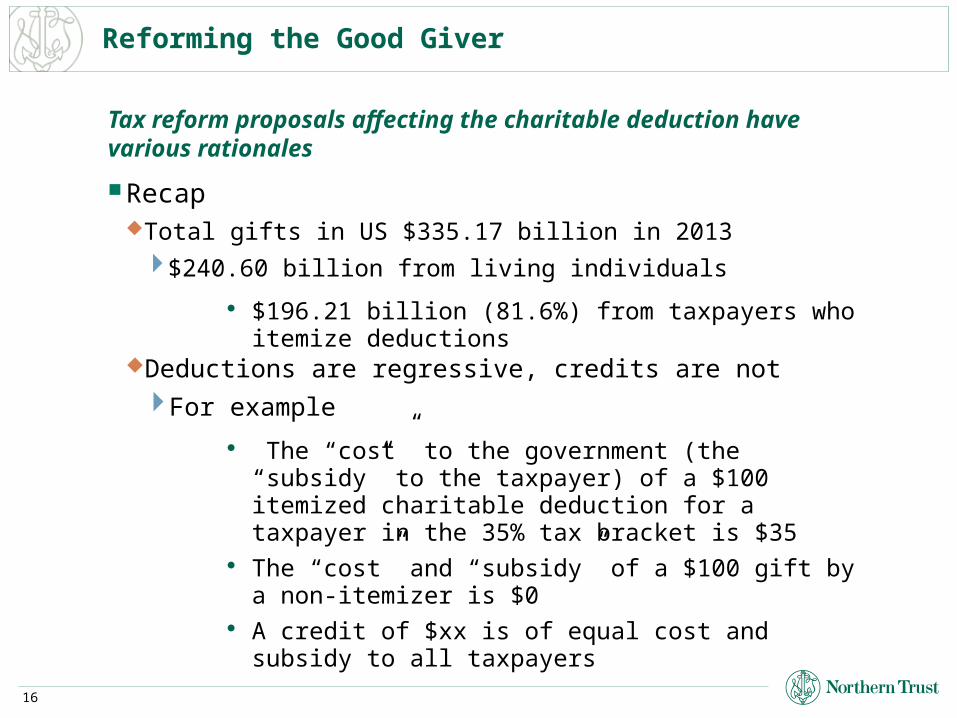

Reforming the Good Giver

RecapTotal gifts in US $335.17 billion in 2013

$240.60 billion from living individuals

· $196.21 billion (81.6%) from taxpayers who itemize deductions

Deductions are regressive, credits are not

For example

· The “cost” to the government (the “subsidy” to the taxpayer) of a $100 itemized charitable deduction for a taxpayer in the 35% tax bracket is $35

· The “cost” and “subsidy” of a $100 gift by a non-itemizer is $0

· A credit of $xx is of equal cost and subsidy to all taxpayers

Tax reform proposals affecting the charitable deduction have various rationales

17

Reforming the Good Giver

Proposals

Administration

Cap the value of all itemized deductions at 28%

Camp proposed Tax Reform Act of 2014

Increase standard deduction

2% floor on itemized charitable deduction

Simplify the rules on deduction limitations

Various reform proposals have been suggested

18

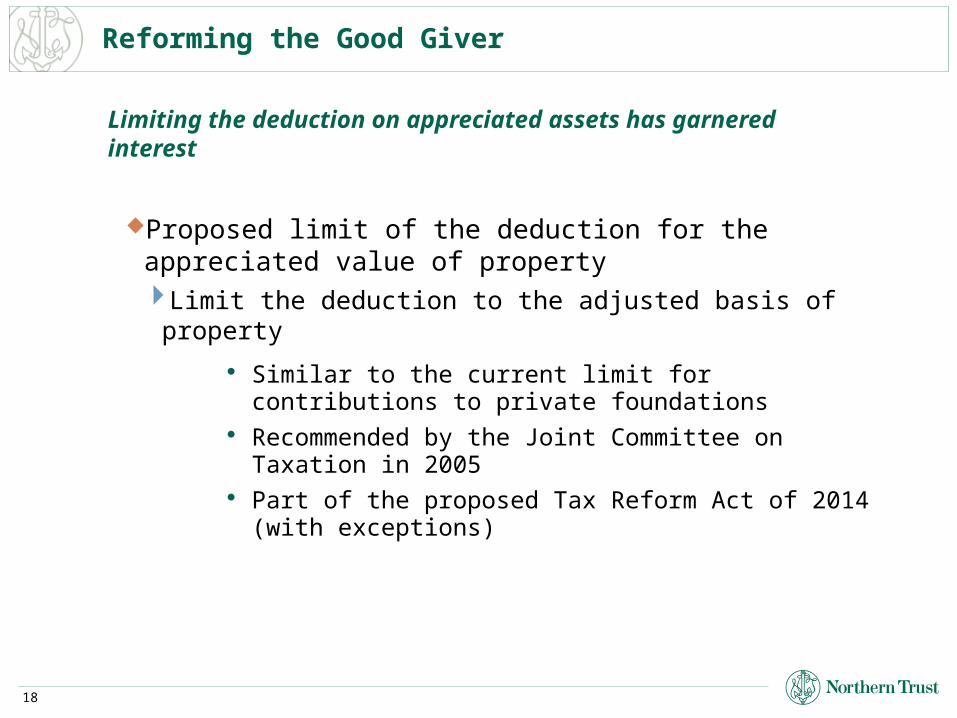

Reforming the Good Giver

Proposed limit of the deduction for the appreciated value of propertyLimit the deduction to the adjusted basis of property

· Similar to the current limit for contributions to private foundations

· Recommended by the Joint Committee on Taxation in 2005

· Part of the proposed Tax Reform Act of 2014 (with exceptions)

Limiting the deduction on appreciated assets has garnered interest

19

Reforming the Good Giver

Recent headlines ask “Who will watch the charities?”

David, Callahan, New York Times, Sunday, May 31, 2015The transparency and accountability of charitable organizations

(private foundations in particular) is under public scrutinyProposed focus of reformsTransparency of charitable donations

Narrower definition of charitable philanthropy focusing on public benefit

Emphasis on the timely use of tax-exempt dollars

· Example – Payout of donor advised fundsBetter accounting of effectiveness of philanthropic dollars

Federal oversight akin to British national Charity Commission

Some have questioned the degree of transparency and accountability of charitable organizations

20

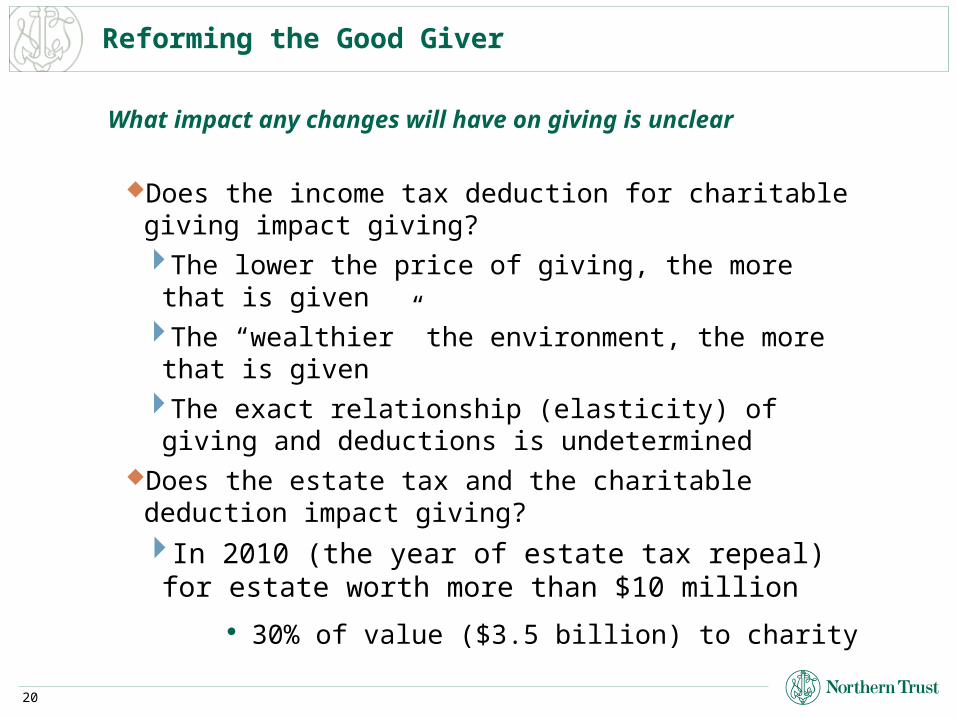

Reforming the Good Giver

Does the income tax deduction for charitable giving impact giving?

The lower the price of giving, the more that is given

The “wealthier” the environment, the more that is given

The exact relationship (elasticity) of giving and deductions is undetermined

Does the estate tax and the charitable deduction impact giving?

In 2010 (the year of estate tax repeal) for estate worth more than $10 million

· 30% of value ($3.5 billion) to charity

What impact any changes will have on giving is unclear

21

The Good Giver’s Tax-Wise Choices

The choice of charity and the gift are important

22

The Good Giver’s Tax-Wise Choices

23

The Good Giver’s Tax-Wise Choices

Planning for gifts makes a difference

24

Direct Donation to Charity

Donor Advised Fund

Supporting Organization

Private Foundation

Charitable Remainder Trust

Charitable Lead Trust

Least Complex Most Complex

The Good Giver’s Giving Options

There are many ways to give, with varying degrees of complexity

Revised April, 2015

Donor Advised FundA Simple and Flexible Way to Promote Family Giving

N O R T H E R N T R U S T

26

At a Glance: Donor Advised Fund

A donor advised fund (DAF) provides an attractive alternative to establishing a private foundation.

A DAF is a charitable giving vehicle that allows you to maintain discretion over your charitable giving without the administrative and financial burdens associated with a private foundation. You can transfer assets to a DAF account during life or at death, and you will receive an immediate charitable tax deduction . You may also appoint family members and friends as "advisors" to the account, thereby promoting family philanthropy and/or charitable giving circles.

Uses: DAFs are less expensive to administer than a private

foundation, and offer a higher income tax charitable deduction

Grants may be made in the name of the DAF account or anonymously

How does it work? Accounts and assets (cash, securities, etc.) are held

by a sponsoring charity, often a community foundation

In year 1, you transfer assets to the DAF

You may be entitled to a charitable income tax deduction in year 1, even though the property may or may not be distributed to charitable organizations in that year

You may make recommendations to the sponsoring charity to make distributions to select charitable organizations

What are the complications? Loss of access to assets for personal needs

Distribution only for the benefit of public charities

While rare, a situation could occur whereby the sponsoring charity may deny a request to direct a charitable gift**

For illustrative purposes only. Not legal or tax advice.

**All DAFs are legally prevented from making certain grants. For more information regarding prohibited grants, please consult a Northern Trust advisor.

DAFYear 1*

Year 2 and beyond:Distributions to Charity

CHARITIES

*Current income tax deduction, subject to deduction limitations

Contribution

Donor Advised Fund Strategy

YOU

27

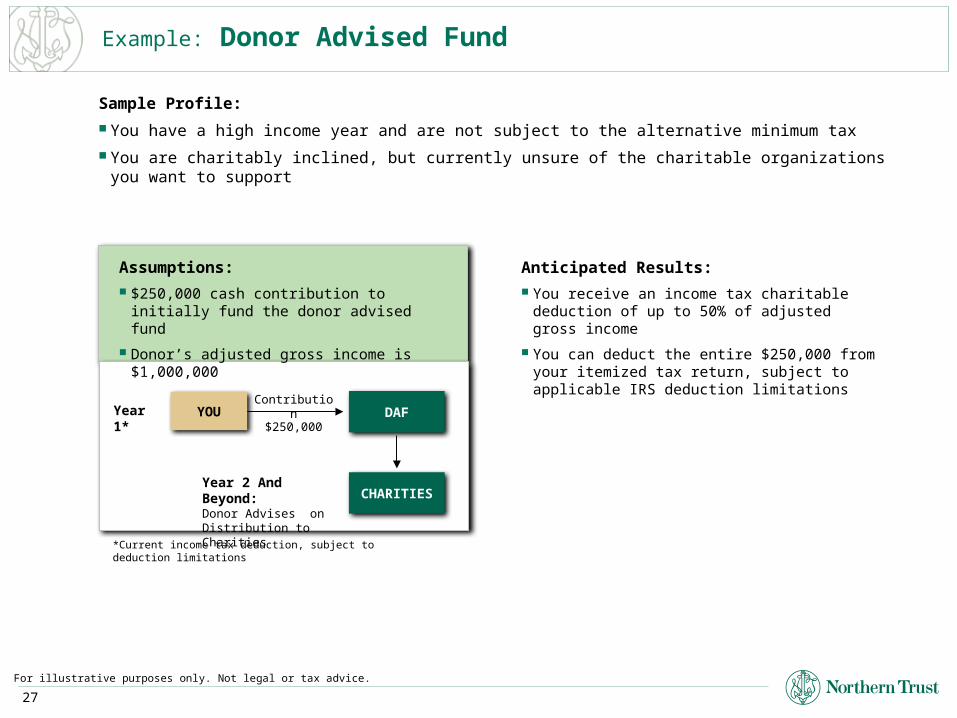

Example: Donor Advised Fund

For illustrative purposes only. Not legal or tax advice.

Sample Profile:

You have a high income year and are not subject to the alternative minimum tax

You are charitably inclined, but currently unsure of the charitable organizations you want to support

Anticipated Results:

You receive an income tax charitable deduction of up to 50% of adjusted gross income

You can deduct the entire $250,000 from your itemized tax return, subject to applicable IRS deduction limitations

Assumptions:

$250,000 cash contribution to initially fund the donor advised fund

Donor’s adjusted gross income is $1,000,000

DAFYear 1*

Year 2 And Beyond:Donor Advises on Distribution to Charities

CHARITIES

*Current income tax deduction, subject to deduction limitations

ContributionYOU

$250,000

Revised April, 2015

Charitable Remainder Trust – "CRT"Fulfill your philanthropic intent while retaining cash flow and deferring capital gains tax

N O R T H E R N T R U S T

29

At a Glance: Charitable Remainder Trust

A charitable remainder trust (CRT) is an irrevocable trust established to provide annual payments to current beneficiaries with the remainder balance distributed to charity. A CRT is typically funded with appreciated assets. You, the grantor, are eligible for an income tax deduction and perhaps a gift or estate tax deduction for the present value of the remainder interest, which will pass to charity.

Payments from the trust may be made to an individual or individuals over time, either for life or for a defined term not to exceed 20 years. Your designated charity (or charities) receives the remaining principal (remainder interest) at the end of the trust term.

Uses:

Appropriate for charitably-inclined persons with highly appreciated assets who desire a defined stream of cash flows for themselves or their beneficiaries

Also provides a method of diversifying appreciated assets while deferring the income taxation, potentially increasing the yield from the assets while gaining a current income tax deduction

How does it work?

A CRT is created in the form of a unitrust (fixed percentage of the trust assets determined and distributed annually) or an annuity trust (fixed dollar amount distributed annually)

Your choice of the term and payout percentage determines both the income tax and gift or estate tax deduction

You and/or your beneficiary(ies) take annual distributions based on the annuity or unitrust amounts

These payments are subject to income tax based upon the character of income earned by the CRT

What are the complications?

Underperforming assets may deplete the trustLoss of control over the contributed assetsGrowth on assets exceeding annuity or unitrust

passes irrevocably to charity If you irrevocably name a beneficiary other than you

or your spouse, the present value of that beneficiary’s interest will be considered a gift for gift tax purposes

Consider generation-skipping transfer tax issues before naming a grandchild or other "skip" person as a beneficiary

For illustrative purposes only. Not legal or tax advice.

CRT

CHARITY

Remainder to charity

CRT Strategy

YOUContribution

ANNUITY OR UNITRUST PAYMENTS

BENEFICIARY

30

Choosing the Charitable Remainder Trust

Charitable remainder trust design presents a number of options

Revised April, 2015

Charitable Lead Trust – "CLT"A Deferred Gift to Minimize Transfer Taxes While Optimizing Annual Charitable Gifts

N O R T H E R N T R U S T

32

At a Glance: Charitable Lead Trust

A Charitable Lead Trust (CLT) makes annual payments to a charity or charities for a term of years, or for a lifetime, before the remaining principal is made available to trust beneficiaries such as children. A CLT can either be testamentary (created by your will or trust upon your death) or inter vivos (created during your lifetime).

Uses: CLTs typically make sense if you want to minimize gift and

estate tax by delaying the transfer of wealth to children or grandchildren, and if you are already making or would like to make annual gifts to charity

How does it work? A CLT is an irrevocable trust with specific annual payments to

charity. Remainder interests pass to or are held for the benefit of non-charitable beneficiaries (typically children)

A CLT is created in the form of a unitrust (fixed percentage of the trust assets determined and distributed annually) or an annuity trust (fixed dollar amount distributed annually)

If structured as a grantor trust, you will be entitled to a current income tax deduction for the present value of the current interest going to charity

You will be taxed on the taxable income during the charitable term

Alternatively, a non-grantor CLT will not tax the grantor on the trust’s income, resulting in the grantor foregoing a current income tax deduction

The CLT, however, will be entitled to a charitable income tax deduction for the amounts passing to charity annually

What are the complications? Loss of control over gifted assets

Loss of access to assets if you or your family have a future need prior to the expiration of the trust’s lead term

Under-performing investments could exhaust the CLT such that the charity may not get its full series of payments and then there will be nothing to pass to the remainder beneficiaries

For illustrative purposes only. Not legal or tax advice.

Charitable Lead Trust Strategy

CLT

TRUST BENEFICIARIES

CHARITY

Annuity Payments to

Charity

Term of Years

Remainder End of Term

YOUContribution

33

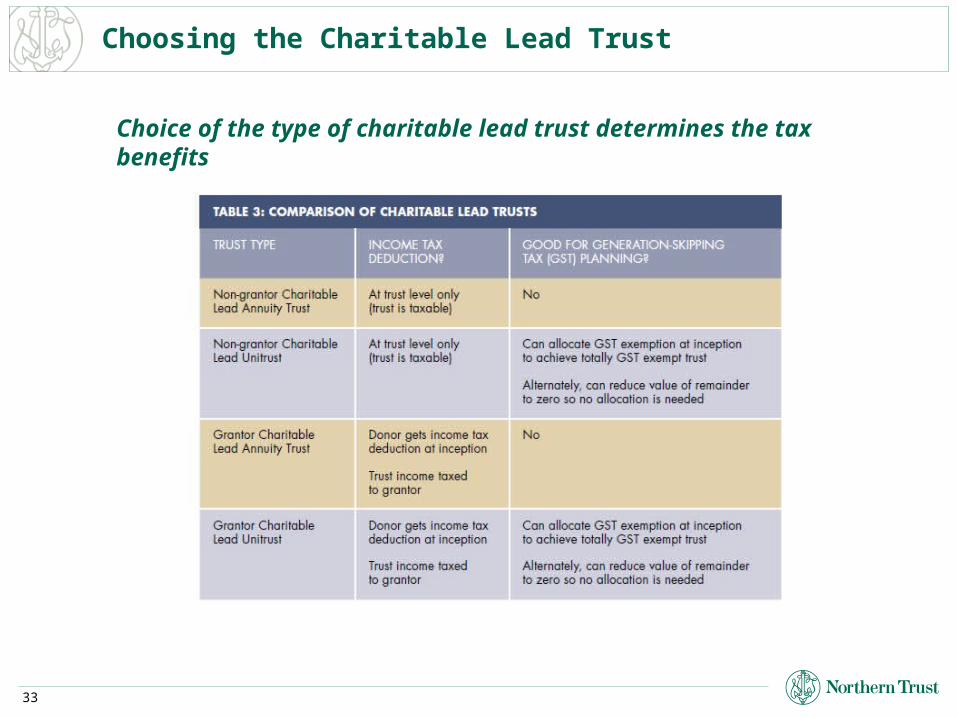

Choosing the Charitable Lead Trust

Choice of the type of charitable lead trust determines the tax benefits

Revised April, 2015

Private Family FoundationMaintain Control of Your Charitable Giving While Promoting Family Philanthropy

N O R T H E R N T R U S T

35

At a Glance: Private Family Foundation

A private family foundation is a tax-exempt charitable vehicle that may be organized as a corporation or a trust. Private family foundations are usually grant-making foundations that make grants to public charities chosen by the foundation’s trustees or directors. A private foundation allows the donor the maximum amount of control and flexibility over a donor’s tax-deductible charitable giving during life and after death.

Multiple generations of family members may be involved in the charitable giving process. Contributions to private foundations are generally deductible for income tax purposes, subject to some limitations.

Uses: A private foundation is effective when you want to

maintain the maximum amount of control over your charitable giving while teaching younger generations about the importance of charitable giving and promoting a family giving legacy

How does it work? A non-profit corporation or a wholly charitable trust

is created Contributions are made to the foundation for future

distributions to charitable causes Private family foundations are generally exempt from

income tax, but must pay an excise tax of 2% on net investment income

Private family foundations must distribute at least 5% of the value of its net assets annually

The donor can maintain control over grant making and investment decisions

What are the complications? Assets must be used for charitable purposes Loss of personal access to assets after transfer to

private foundation Administratively complex Potential loss of privacy due to tax returns being

publicly recorded Subject to complex Internal Revenue Code rules and

close scrutiny by the IRS, particularly as it relates to prohibited transactions

For illustrative purposes only. Not legal or tax advice.

Private Family Foundation Strategy

CHARITIES

AnnualGrants

YOUContribution

PRIVATE FOUNDATION

36

Example: Private Family Foundation

For illustrative purposes only. Not legal or tax advice.

Sample Profile:

Your family would like to contribute $5,000,000 to a charitable giving vehicle to consolidate your charitable giving activities and encourage younger family members (children) to participate in philanthropic activities

Results:

You create a family charitable legacy through the creation and management of the private foundation

You and your spouse/partner and adult children can serve as directors for a corporation or as distribution committee members for a trust and be actively involved in the grant-making process

From a tax perspective, a $5,000,000 income tax charitable deduction is available in the year the contribution is made, subject to the applicable adjusted gross income limitation of 30% for gifts of cash and 20% for gifts of long-term appreciated securities

Assets of the foundation will be subject to the 2% annual excise tax on the net investment income

Assumptions:

Total family assets of $20,000,000

Family is charitably inclined

Family is willing to commit up to $5,000,000 in cash to fund the foundation

CHARITIES

Grants

YOUContribution

FAMILY PRIVATE FOUNDATION$5,000,000

At Least 5% Annually

37

Choosing Between a Private Foundation and Donor Advised Fund

Aligning the type of vehicle with the donor’s goals is essential to planning

Revised April, 2015

Supporting Organizations

N O R T H E R N T R U S T

39

At a Glance: Supporting Organizations

How does it work? A supporting organization is established as either a

nonprofit corporation or a trust One or more donors make contributions to the

supporting organization, making them eligible to take an income tax charitable deduction

The supporting organization makes financial contributions to, or supports the programmatic work of, one or more specified domestic public charities

The donor may continue to have a limited role in the oversight of the supporting organization, including governance and investments

Special Considerations: The rules that govern supporting organizations are

complex The donor(s) and certain related parties (known as

"disqualified persons") may not maintain control over the supporting organization

The supporting organization’s public charity status depends on the involvement of the public charities that are benefitted by the supporting organization. Thus, based on their governance structure, certain supporting organizations are subject to extensive administrative requirements, including minimum required distributions and additional reporting.

For illustrative purposes only. Not legal or tax advice.

Supporting Organization Structure

SPECIFIED CHARITY

Financial or programmatic

support

DONOR(S)

Contribution

SUPPORTING ORGANIZATION

SPECIFIED CHARITY

A supporting organization is a tax-exempt, wholly charitable entity established by one or more donors which provides support to specified public charities. Based on its special relationship to the public charities it supports, the supporting organization is classified as a public charity (rather than as a private foundation).

40

Comparison: Supporting Organizations vs. Private Foundations

Advantages of Supporting Organization Status over Private Foundation status

Tax-free investment income: Because they are classified as public charities, supporting organizations do not pay tax on investment income, whereas private foundations pay a 1-2% excise tax on investment income.

Increased income tax charitable deductions: Contributors to a supporting organization are entitled to greater income tax charitable deductions for such gifts than they would be for identical gifts to a private foundation.

Decreased IRS oversight: Supporting organizations are not subject to the private foundation laws of the Internal Revenue Code, which impose strict rules covering self-dealing, timing of distributions, and types of investments. Failure to fully comply with these rules subjects a private foundation (and, in some cases, its donors or managers) to large excise taxes.

For illustrative purposes only. Not legal or tax advice.

41

Comparison: Supporting Organizations vs. Private Foundations

Disadvantages of Supporting Organization status relative to Private Foundation status

Loss of donor control: The donor of a supporting organization cannot retain control over the entity and may only appoint a minority of the trustees or board of directors.

Loss of grant-making flexibility: A supporting organization is limited to supporting specific public charities that are identified by name or class under the governing instrument, and which cannot be changed at the will of either the donor or the trustee of the supporting organization. By contrast, a private foundation may be established with broad charitable purposes, permitting the trustees to change its grant recipients every year

No compensation to donors or related parties: Disqualified persons related to the donor of a supporting organization may not receive any grant, loan, payment of compensation or similar payments, whereas a private foundation may provide reasonable compensation to such disqualified persons.

For illustrative purposes only. Not legal or tax advice.

42

Comparison of Giving Vehicles

Tax Implications Lifetime gift: Immediate income tax deduction

Cash: up to 50% of AGI Securities: up to 30% of AGI

No capital gains tax on properly structured gifts of

appreciated securities

Bequest: Estate tax deduction for full market

value of donation at death

Lifetime gift: Immediate income tax deduction

Cash: up to 50% of AGI Securities: up to 30% of AGI

No capital gains tax on properly structured gifts of

appreciated securities

Bequest: Estate tax deduction for full market value

of donation at death Investment income is not subject to tax

Lifetime gift: Immediate income tax deduction

Cash: up to 30% of AGI Securities: up to 20% of AGI

No capital gains tax on properly structured gifts of

appreciated securities

Bequest: Estate tax deduction for full market

value of donation at death

Disadvantages Gift acceptance policies vary among charities and may restrict type of

donated property One-time gift vs.continuous grants

Sponsoring charity has final say on grant recommendations and investment

of fund assets

Subject to annual excise tax, quarterly estimated excise

tax payments Annual tax returns

Substantial set-up and ongoing expenses

Complex self-dealing and other private foundation excise tax rules

Outright Donation to Charity Donor Advised Fund Private Foundation

Advantages Immediate benefit to charity No front-end costs or expenses Keep assets until you donate,

investing them as you choose

Contributions deductible in current year Ability to recommend investments

and grants over time Flexible, convenient giving Minimum cost to establish

Involvement of family members and friends

Anonymity, if desired

Contributions deductible in current year

Ability to make grants over time Full control over charitable

distributions Involvement of family members

and friends Anonymity, if desired

43

The Good Giver’s Legacy

$400 billion in taxable gifts were made in 2012Compared to $25 billion per year from 2002 to 2009

Generational wealth transfer over the next 20 years will be unprecedented

Giving the gift of giving has never been more important Positioning as

An heir – to wisdom as well as wealthA steward – responsible for passing the value of generosity

on to the next generationA participant – modeling generosity, as those who follow are

more likely to do as we do than to do as we say

The Good Giver’s greatest gift is transmitting the value of giving

44

The Good-Giver’s Tax-Wise Legacy

Consider a married couple living in Florida with $10 million in assets and two successful children who intend to make a $1 million charitable gift

Alternatives Testamentary charitable gift of $1million and $4.5 million to

each child or $5 million to each child and children make gifts of $500,000

each Assume the children each have $500,000 ordinary income in 2015

and 2016 Estate tax parents

$0 under both alternatives Income savings children

$0 under testamentary gift alternative In excess of $150,000 for each child over two years

Giving with increased estate tax exclusion, portability and higher income tax rates

45

A Closing Thought for the Good Giver (and their Counsel)

The desire of power in excess caused the angels to fall;

the desire of knowledge in excess caused man to fall;

but in charity there is no excess;

neither can angel nor man come in danger by it.

Sir Francis Bacon

46 Presentation Title or Conference (To Edit or Delete: View > Slidemaster)

Insights From Northern Trust Experts

Market UpdatesHelping clients stay abreast of the

latest market challenges and opportunities

MarketScape Video (Weekly)Perspective Publication (Monthly)

Insights from Northern Trust Call/Webcast (Monthly)

Investment Strategy Commentary by Pete Mladina / Katie Nixon

(Quarterly) Investment Strategy Commentary by Jim

McDonald (Timely)

Economic UpdatesCurrent and future economic

conditions and forecasts Weekly Economic Commentary

(Weekly)U.S. Economic Outlook Commentary

(Monthly)Global Economic Outlook Commentary

(Quarterly)The View From Here Video (Timely)

Other PublicationsWealth Planning Insights

News and analysis to help clients navigate the changing wealth planning landscape. (Monthly)

Wealth MagazineFinancial and lifestyle perspectives from Northern Trust. (Quarterly+)

Wealth Advisor Insights Newsletter for professional advisors provides

analysis from our experts. (Quarterly+)

Other Ways to Connect with Northern Trust:

Follow Northern Trust

Wealth Management

Follow @NTWealth

Follow Northern Trust

Videos

Text “NTWealth” to 687878

for text alerts

Download Private

Passport Mobile

Download app for iPad at

northerntrust.com/wealthpath

Followwww.pinterest.com

/northerntrust

4747

LEGAL, INVESTMENT AND TAX NOTICE: This information is not intended to be and should not be treated as legal advice, investment advice or tax advice. Readers, including professionals, should under no circumstances rely upon this information as a substitute for their own research or for obtaining specific legal or tax advice from their own counsel.

This presentation is for your private information and is intended for one-on-one use with current or prospective clients of Northern Trust. The information does not constitute investment advice or a recommendation to buy or sell any security, may not be suitable for all investors and is subject to change without notice.

Securities products and brokerage services are sold by registered representatives of Northern Trust Securities, Inc. (member NASD, SIPC), a wholly owned subsidiary of Northern Trust Corporation.

Not FDIC Insured | No Bank Guarantee | May Lose Value

Disclosures