NYSE: WMB

williams.com

WE MAKE ENERGY HAPPEN

Northwest Pipeline IntroductionGary Venz – Manager, Marketing Services

2© 2017 The Williams Companies, Inc. All rights reserved. WECC Gas/Electric Forum – May 21, 2019

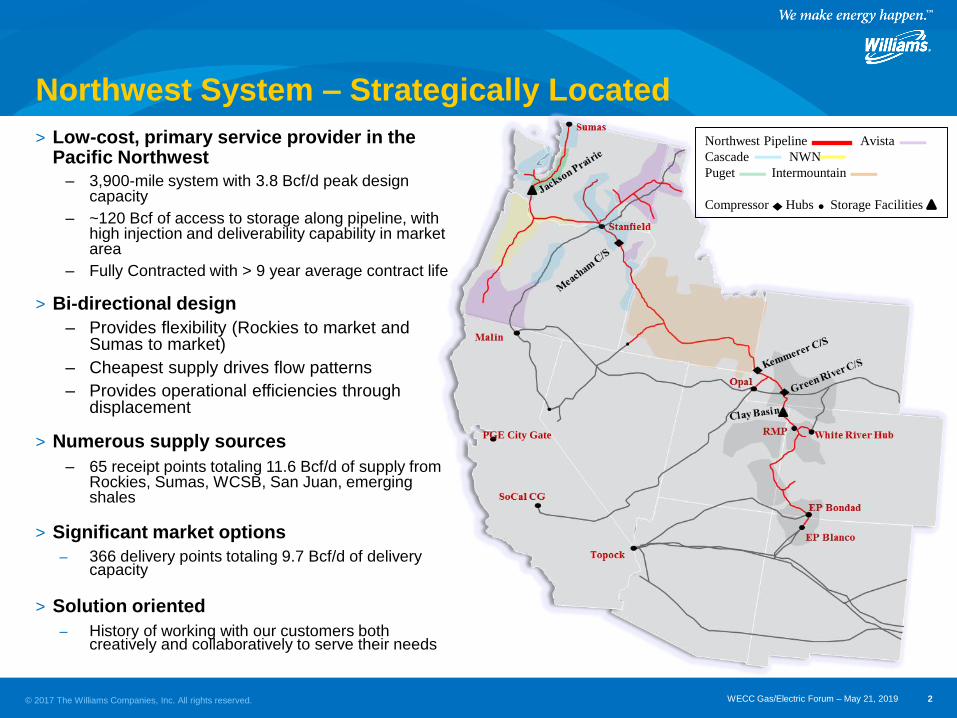

Northwest System – Strategically Located

> Low-cost, primary service provider in the Pacific Northwest

– 3,900-mile system with 3.8 Bcf/d peak design capacity

– ~120 Bcf of access to storage along pipeline, with high injection and deliverability capability in market area

– Fully Contracted with > 9 year average contract life

> Bi-directional design

– Provides flexibility (Rockies to market and Sumas to market)

– Cheapest supply drives flow patterns

– Provides operational efficiencies through displacement

> Numerous supply sources

– 65 receipt points totaling 11.6 Bcf/d of supply from Rockies, Sumas, WCSB, San Juan, emerging shales

> Significant market options

– 366 delivery points totaling 9.7 Bcf/d of delivery capacity

> Solution oriented

– History of working with our customers both creatively and collaboratively to serve their needs

PGE City Gate

Northwest Pipeline Avista

Cascade NWN

Puget Intermountain

Compressor Hubs Storage Facilities

3© 2017 The Williams Companies, Inc. All rights reserved. WECC Gas/Electric Forum – May 21, 2019

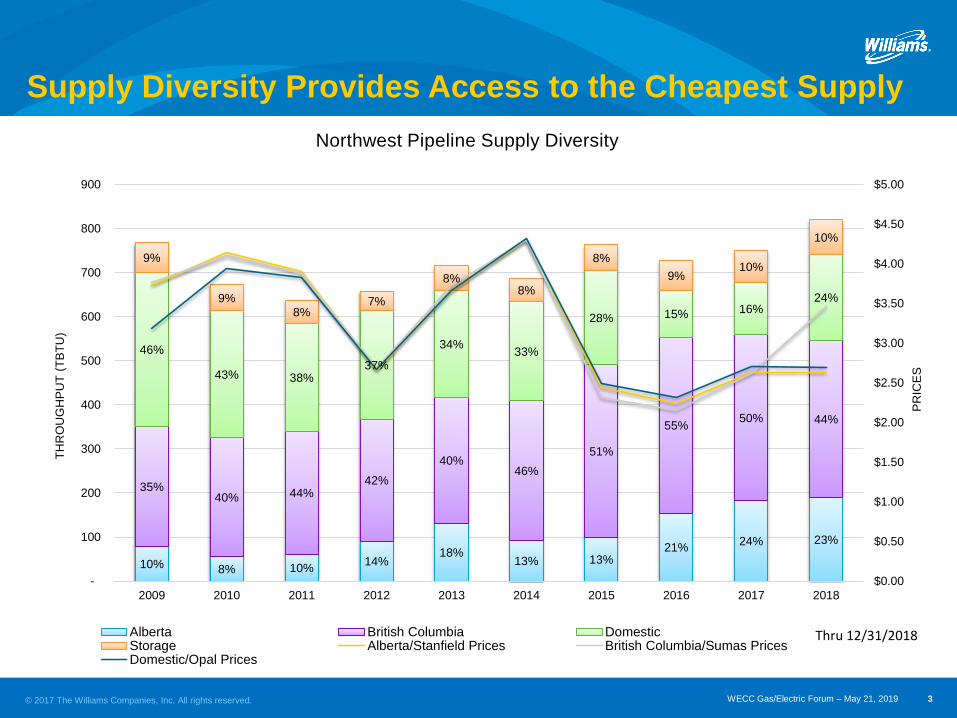

Supply Diversity Provides Access to the Cheapest Supply

10% 8% 10%14%

18%13% 13%

21%24% 23%

35%40% 44%

42%

40%46%

51%

55%50% 44%

46%

43% 38%37%

34%33%

28% 15% 16%24%

9%

9%

8%7%

8%8%

8%

9%10%

10%

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

$5.00

-

100

200

300

400

500

600

700

800

900

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

PR

ICE

S

TH

RO

UG

HP

UT

(T

BT

U)

Northwest Pipeline Supply Diversity

Alberta British Columbia DomesticStorage Alberta/Stanfield Prices British Columbia/Sumas PricesDomestic/Opal Prices

Thru 12/31/2018

4© 2017 The Williams Companies, Inc. All rights reserved. WECC Gas/Electric Forum – May 21, 2019

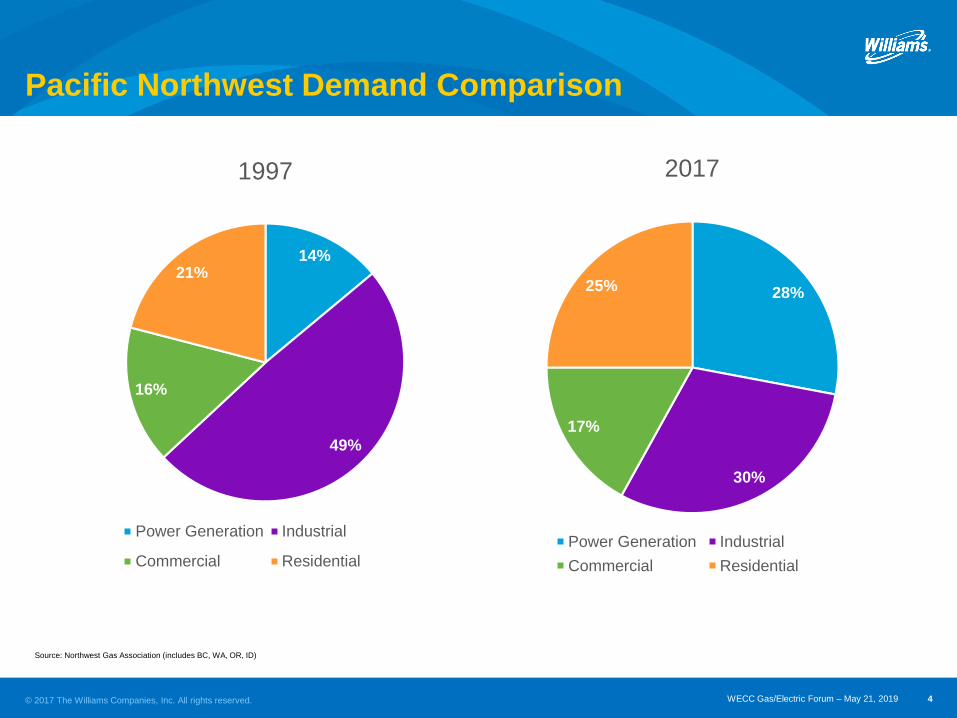

Source: Northwest Gas Association (includes BC, WA, OR, ID)

Pacific Northwest Demand Comparison

14%

49%

16%

21%

1997

Power Generation Industrial

Commercial Residential

28%

30%

17%

25%

2017

Power Generation Industrial

Commercial Residential

5© 2017 The Williams Companies, Inc. All rights reserved. WECC Gas/Electric Forum – May 21, 2019

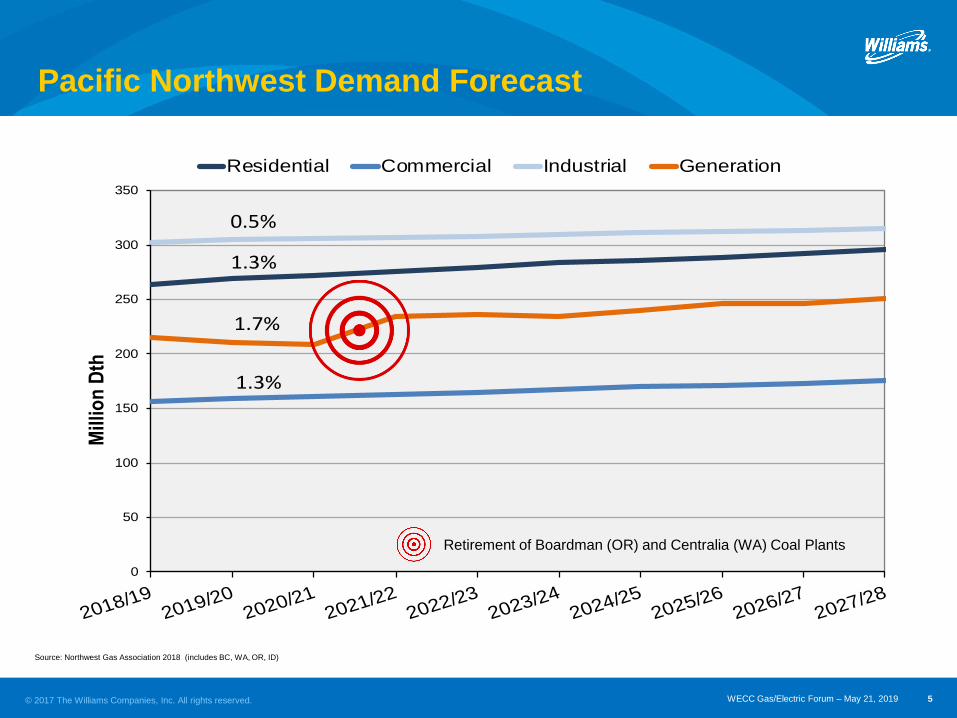

Pacific Northwest Demand Forecast

0

50

100

150

200

250

300

350

2018/192019/20

2020/212021/22

2022/232023/24

2024/252025/26

2026/272027/28

Mil

lio

n D

th

Residential Commercial Industrial Generation

0.5%

1.3%

1.7%

1.3%

Source: Northwest Gas Association 2018 (includes BC, WA, OR, ID)

Retirement of Boardman (OR) and Centralia (WA) Coal Plants

6© 2017 The Williams Companies, Inc. All rights reserved. WECC Gas/Electric Forum – May 21, 2019

Pacific Northwest Natural Gas Generation

7© 2017 The Williams Companies, Inc. All rights reserved. WECC Gas/Electric Forum – May 21, 2019

Aggregate of Northwest On-System Power Demand (Dth/d)

8© 2017 The Williams Companies, Inc. All rights reserved. WECC Gas/Electric Forum – May 21, 2019

Nexus Between Gas and Power on Northwest Pipeline

> Northwest Pipeline offers:

– Flexible balancing

– No uniform hourly takes

– Park and loan services

– Additional post day cycle for realignment purposes

> Northwest Pipeline takes a proactive role in:

– Customers Integrated Resource Planning to understand forecasted demand, peaks and

market drivers

– Participates in regional gas/electric coordination groups to maintain dialogue and education

on how the gas side works

– Mitigates maintenance, to the extent possible, not to impact customers business

> Northwest Pipeline has a history of expanding its system

– Requires long term customer commitment

9© 2017 The Williams Companies, Inc. All rights reserved. WECC Gas/Electric Forum – May 21, 2019

Thank You