Oil & Gas Markets OutlookNational Ocean Industries Association

Dr. Helen Currie, Senior Economist

January 31, 2017

2

3

Oil Market

Global Oil Market: The Past Decade

0

20

40

60

80

100

$0

$25

$50

$75

$100

$125

$150

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Brent Crude Oil Price(left hand scale)

Oil Volatility Index(right hand scale)

Global Oil Prices and VolatilityPrice/Bbl

% Volatility

4 Source: Bloomberg

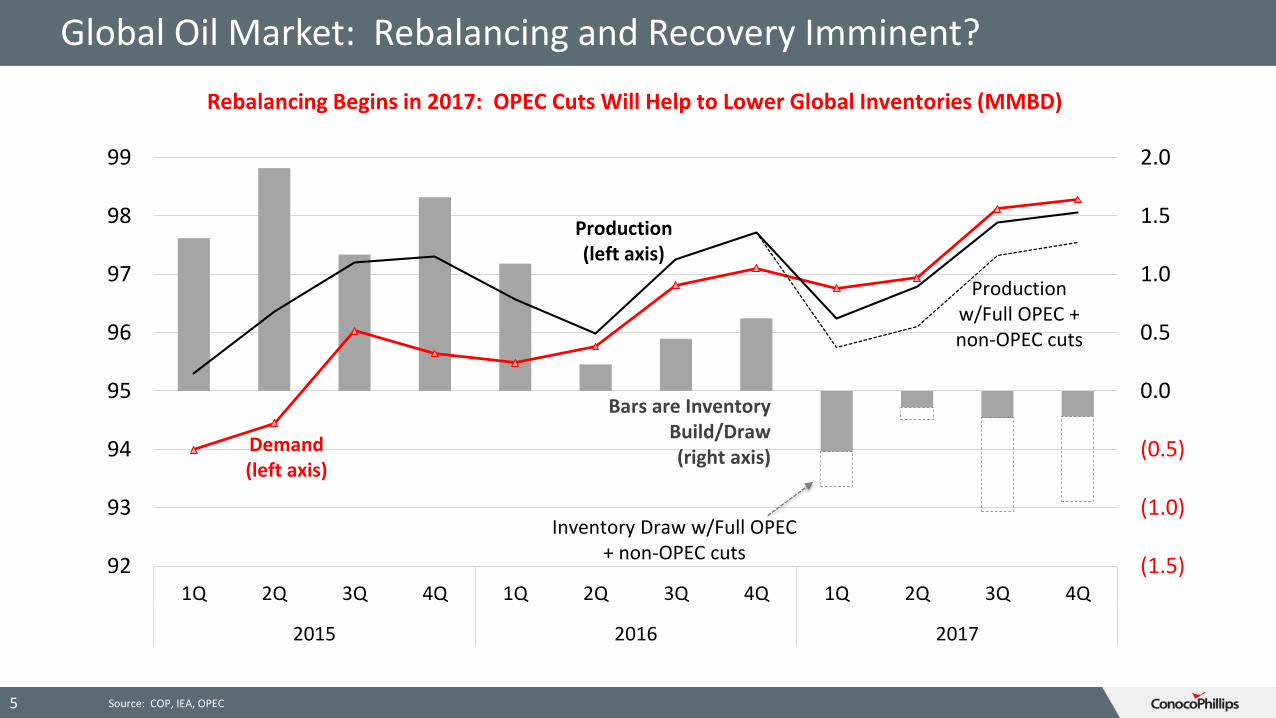

Global Oil Market: Rebalancing and Recovery Imminent?

5

(1.5)

(1.0)

(0.5)

0.0

0.5

1.0

1.5

2.0

92

93

94

95

96

97

98

99

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

2015 2016 2017

Rebalancing Begins in 2017: OPEC Cuts Will Help to Lower Global Inventories (MMBD)

Bars are Inventory Build/Draw (right axis)

Demand (left axis)

Production (left axis)

Production w/Full OPEC + non-OPEC cuts

Inventory Draw w/Full OPEC + non-OPEC cuts

Source: COP, IEA, OPEC

U.S. Crude Oil Production Expected to Grow

EIA Base Case

High Resource & Technology

Prior Base Case

0

5

10

15

2005 2010 2015 2020 2025 2030

EIA Projects Significant Upside to U.S. Oil Production with Additional Efficiency and Technological Improvements (MMBD)

6 Source: U.S. Department of Energy, EIA Annual Energy Outlook 2017

U.S. Crude Oil Production Growth Led by Onshore Fields

Offshore High Case

Onshore High Case

0

2

4

6

8

10

12

14

2015 2020 2025 2030

Lower-48 Offshore vs Onshore Oil Production (MMBD)

Onshore

Offshore

7 Source: U.S. Department of Energy, EIA Annual Energy Outlook 2017

Challenges to Offshore development vs Onshore Unconventional Plays:

• High initial capital

commitments

• Relatively long lead times

• Less flexibility

• Greater complexity

U.S. Unconventional, Light Tight Oil Plays Account for Future Growth

Gulf Coast

Midcontinent

Permian

Bakken, Niobrara/Rockies

East & West Coasts

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2015 2020 2025 2030

Lower-48 Oil Production by Region (MMBD)

High Resource/Technology Cases

8 Source: U.S. Department of Energy, EIA Annual Energy Outlook 2017

Key Issues in Projecting Future Tight Oil Supply:

• Pace and Magnitude of

additional technology &

efficiency improvements

• Cost escalation as activity

accelerates

• Infrastructure needs

• Environmental compliance

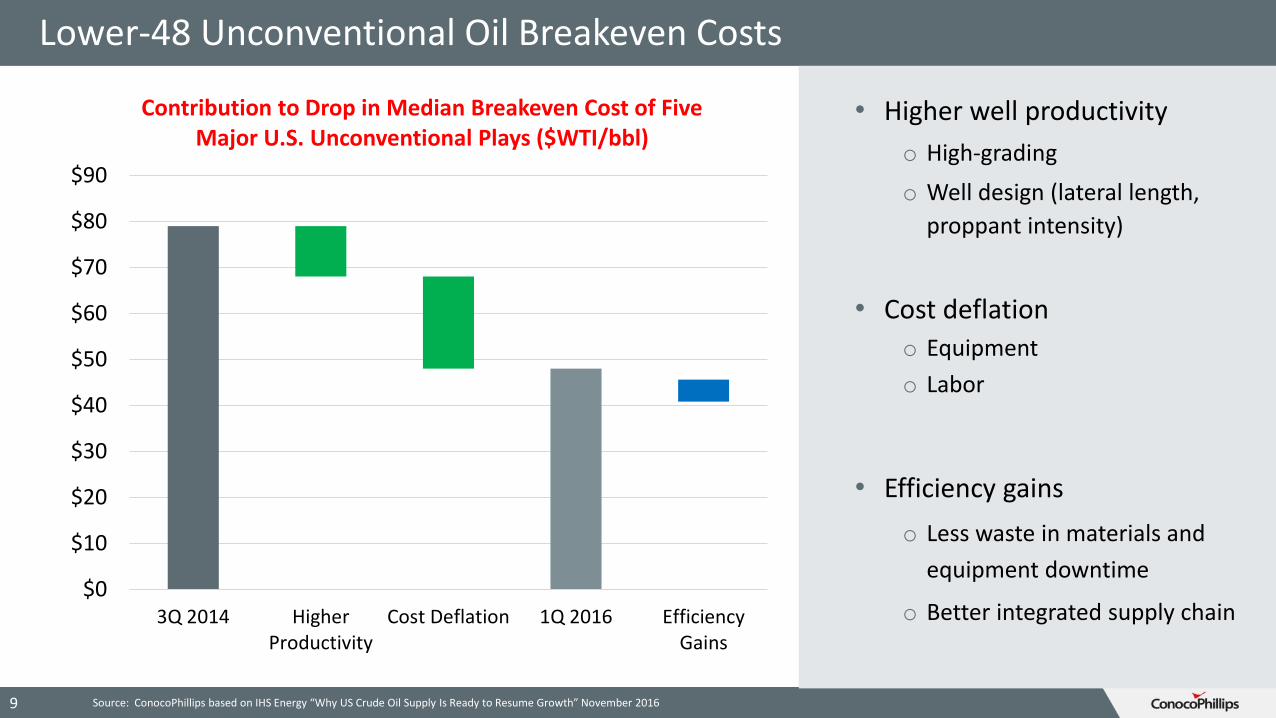

Lower-48 Unconventional Oil Breakeven Costs

9 Source: ConocoPhillips based on IHS Energy “Why US Crude Oil Supply Is Ready to Resume Growth” November 2016

• Higher well productivity

o High-grading

o Well design (lateral length,

proppant intensity)

• Cost deflation

o Equipment

o Labor

• Efficiency gains

o Less waste in materials and

equipment downtime

o Better integrated supply chain$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

3Q 2014 HigherProductivity

Cost Deflation 1Q 2016 EfficiencyGains

Contribution to Drop in Median Breakeven Cost of Five Major U.S. Unconventional Plays ($WTI/bbl)

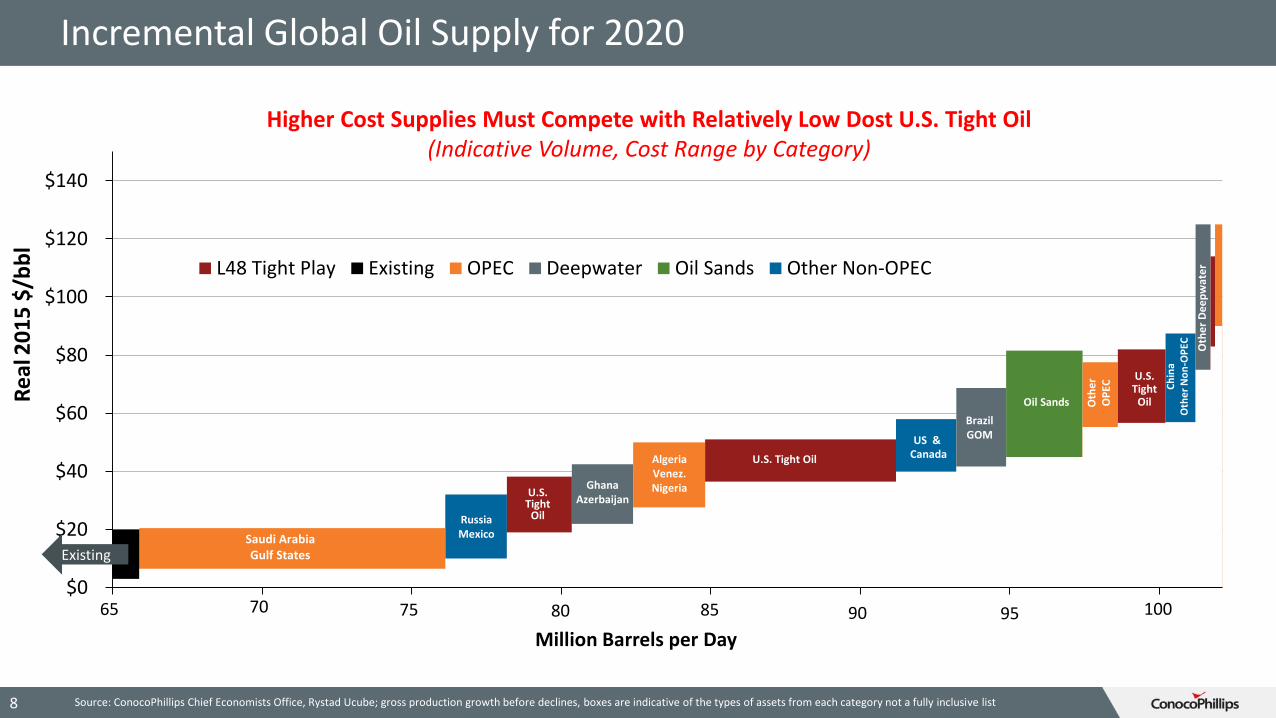

Incremental Global Oil Supply for 2020

65 80 85 90 95 100$0

$20

$40

$60

$80

$100

$120

$140

L48 Tight Play Existing OPEC Deepwater Oil Sands Other Non-OPEC

Existing

U.S. Tight

Oil

U.S. Tight Oil

Russia Mexico

US &Canada

Saudi ArabiaGulf States

Algeria Venez.NigeriaGhana

Azerbaijan

BrazilGOM

Oil Sands

Ch

ina

Oth

er

No

n-O

PEC

U.S. Tight

OilOth

er

OP

EC

Million Barrels per Day

Oth

er

De

ep

wat

er

70 75

Re

al2

01

5 $

/bb

l

Source: ConocoPhillips Chief Economists Office, Rystad Ucube; gross production growth before declines, boxes are indicative of the types of assets from each category not a fully inclusive list 8

Higher Cost Supplies Must Compete with Relatively Low Dost U.S. Tight Oil(Indicative Volume, Cost Range by Category)

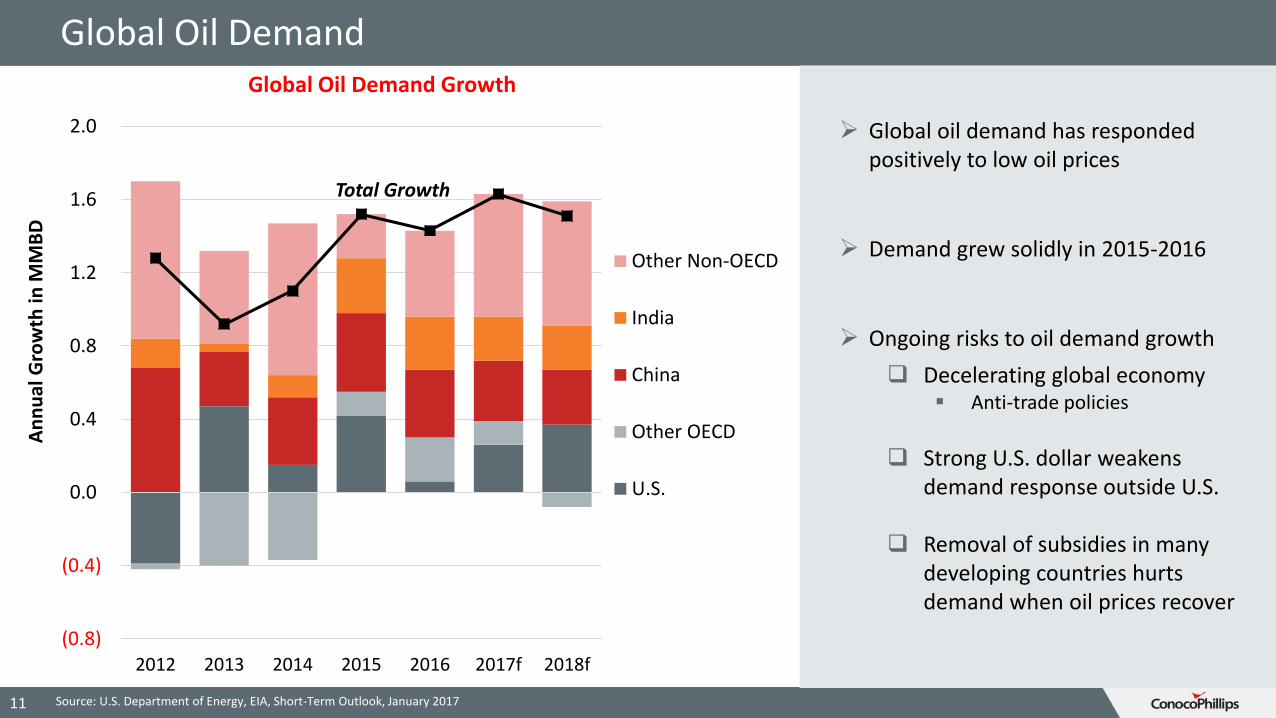

Global Oil Demand

11 Source: U.S. Department of Energy, EIA, Short-Term Outlook, January 2017

(0.8)

(0.4)

0.0

0.4

0.8

1.2

1.6

2.0

2012 2013 2014 2015 2016 2017f 2018f

Global Oil Demand Growth

Other Non-OECD

India

China

Other OECD

U.S.

Global oil demand has responded positively to low oil prices

Demand grew solidly in 2015-2016

Ongoing risks to oil demand growth

Decelerating global economy Anti-trade policies

Strong U.S. dollar weakens demand response outside U.S.

Removal of subsidies in many developing countries hurts demand when oil prices recover

An

nu

al G

row

th in

MM

BD

Total Growth

Slowing Growth in the Global Economy

12

The IMF consistently lowered growth projections for 2015 and 2016

The IMF lowered its GDP forecast for 2016 by 0.2% in its January 2016 forecast.

Downside risks to the economic outlook:

o Secular stagnation

o Hard landing in China’s slowdown

o European immigration crisis and Brexit

o Anti-trade policies

Global Economy: Slowing Growth Prospects

Fiscal Loosening

(10%)

Base (40%)Brexit slows

EU (5%)

Secular Stagnation (10%)

China Tightens (15%)

Strong US Anti-Trade Stance (3%)

2.8

3.0

3.2

3.4

3.6

3.8

4.0

2015 2016 2017 2018 2019 2020

Scenarios for Global Growth

% real GDP, PPP

Sources: Oxford Economics

13

Natural Gas Markets

Resilience of U.S. Shale Gas Production for Major Plays

0

10

20

30

40

50

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Permian

Niobrara

Eagle Ford

Bakken

Utica

Haynesville

Marcellus

Shale Gas Plays

AssociatedGas & Legacy Production

Source: EIA Drilling Productivity Report, January 2017. Type Curves based on data from DrillingInfo

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

1 3 5 7 9 11 13 15 17

0

100

200

300

400

500

600

700

1 3 5 7 9 11 13 15 17

BC

FD

MC

FDM

CFD

Production Month

Marcellus Type Curves

Permian Associated Gas Type Curves

2015 2013 2011

U.S. Shale Gas Production from Top Unconventional Plays

14

Production Month

North American Natural Gas Production Outlook

Source: Wood Mackenzie; U.S. and Canada production combined15

0

20

40

60

80

100

120

140

2015 2018 2021 2024 2027 2030

The Future of North American Production is Shale(Bcf/day)

Shale Gas

Other

Gas from Tight Oil

0

5

10

15

20

Mar

cellu

s

Uti

ca

Can

ada

Eagl

e F

ord

Hay

ne

svill

e

Per

mia

n

Mid

Co

n

Bak

ken

Marcellus is the Growth Leader

Growth in production 2016-2030 (Bcf/day)

LNG exports LNG exports

MexicoMexico

Power

PowerIndustrial

Other

Other

Transport

Res/Comm

0

2

4

6

8

10

12

14

16

18

2016-2020 2020-2030

Demand Growth Led by Export Markets and Power (Bcfd)

16

U.S. Natural Gas Demand Outlook

Source: IHS Energy, December 2016 N.A. Natural Gas Brief. The use of this content was authorized in advance by IHS Markit.Any further use or redistribution of this content is strictly prohibited without written permission by IHS. All rights reserved

Almost 9 Bcfd (70 MTPA) Lower-48 Liquefaction Capacity Online by 2020 (Bcfd)

0

2

4

6

8

2016 2017 2018 2019 2020

Gulf Coast East Coast

Source: Wood Mackenzie

Source: IHS Energy. The use of this content was authorized in advance by IHS Markit.Any further use or redistribution of this content is strictly prohibited without written permission by IHS. All rights reserved

16

(20)

0

20

40

60

80

100

120

140

160

180

Supply Demand Excess Supply

Global Cumulative Growth 2015-2025

U.S.

Australia

Other Pacific

Other Atlantic

Other

Japan, Korea, Taiwan

Other Asia

Europe

Americas

Middle East

New Excess

Existing Excess

Global LNG Supply-Demand BalanceM

TPA

Net growth

Summary

Oil• Prices may continue to experience elevated

volatilityo Uncertain government policies create headwinds for oil

markets

• U.S. production growth expected to be focused onshoreo Ongoing improvements to technology, productivity and

costs will drive growth in U.S. Light Tight Oil

Natural Gas• Shale gas will continue to be a game-changer

o U.S. and Canada will continue to be well supplied by shale resources

• Global gas markets will be more highly linked as LNG trade grows

18