Organised by Ministry of Road Transport & Highways, Government of India

Content

1

2

3

4

5

6

Public Private Partnerships: Multimodal Logistics Parks ................ 01

Urban Transportation in India ............................................................ 15

Freight Corridors for Economic Development ................................... 25

Supply Chain Transformation: Storage Innovations ....................... 35

Gateways and the Role of Digitization ............................................... 47

Standards and Skills for Logistics ....................................................... 55

Foreword

Logistics in India’s rapidly growing economy is supported by the world’s 2nd largest road network, 4th largest

rail network, 14,500 km of navigable waterways, 200+ maritime ports and 125 airports. However, India ranks

35 in World Bank’s Logistics Performance Index (LPI) due to poor modal share - 60% of India’s domestic freight

moves on roads, despite other modes being 50-60% cheaper and 50-90% less polluting. This unfavorable

modal mix is due to lack of seamless intermodal connectivity in the country. This highlights the need for

development of multimodal infrastructure in the country through close coordination between different

agencies involved in planning and developing transport infrastructure.

In this collection of theme papers, six major topics in the logistics sector have been discussed in detail which

provide a brief background of each topic along with actionable recommendations on each. One of the key

solution themes to improve India’s logistics is the development of multimodal logistics parks (MMLPs) which

will enable a hub and spoke model of freight movement by facilitating freight aggregation-disaggregation

and multimodal freight movement. Ministry of Road Transport and Highways (MoRTH) has identified 35

prioritized locations, which account for 50% of total freight movement, for the development of MMLPs.

Additionally, multiple agencies including Container Corporation of India (CONCOR) and Delhi Mumbai Industrial

Corridor Development Corporation (DMICDC) are also developing logistics parks. It is envisaged that these

government agencies shall come together and coordinate with private parties to make a collaborative effort

to set up MMLPs in India and thereby improve India’s logistics efficiency.

The India Integrated Transport and Logistics Summit – 2017 (IITLS), is one such effort to bring together all the

concerned stakeholders, viz. government agencies, logistics service providers, concessionaires, end-users

and investors on one platform. The Summit will highlight the various new development programs in transport

and logistics sector in India

I invite you to peruse this booklet and share your views in the various sessions of the IITLS. This will enable the

government to formulate a comprehensive policy for development of Multimodal Logistics Parks, keeping in

mind the interests of all the concerned stakeholders.

( )Shri Radhakrishnan

dejk ua- 310] ifjogu Hkou] ubZ fnYyh&110001Room No 310, Transport Bhawan, New Delhi-110001

Tel. : 23715159, 23731522 Fax : 23718568

Foreword

The transport and logistics infrastructure in India must be revamped, with a focus on intermodal connectivity

and a network approach, to help bring down the logistics cost and reduce environmental pollution. India needs

to take lessons from modern infrastructure in leading countries, which is tuned to provide seamless

intermodal connectivity and has ensured a favorable modal-mix with more focus on railways and shipping

instead of roads.

Infrastructure Development is one of the top priorities for the NDA Government under the dynamic leadership

of Hon’ble Prime Minister Shri Narendra Modiji. Multiple steps have already been taken by the Ministry of Road

Transport, Highways and Shipping (MoRTH&S) to improve the state of logistics in India. The Sagarmala

Programme is a key initiative which aims to promote port-led development and provide infrastructure to

transport goods to and from ports quickly, efficiently and cost-effectively. The broad objective is capacity

enhancement and modernization of major and non-major ports, establishment of industries and

manufacturing centers to be served by ports in EXIM and domestic trade, simplification of procedures used at

ports for cargo movement and promotion of electronic channels for information exchange.

Inland Waterways Authority of India (IWAI), under the aegis of MoRTH&S, is undertaking the development of

infrastructure on National Waterways which will enable India to achieve the vision of Hon’ble Minister of Road

Transport, Highways and Shipping of using India’s ample waterways in transporting various goods from

production centers to consumption centers in a safe and efficient manner. Through these measures, it is

hoped that freight is shifted from road to coastal, inland and rail routes, which will result in huge savings for the

end-users and will benefit the whole economy.

The India Integrated Transport & Logistics Summit (IITLS) is being organized with a view to promote

collaboration between stakeholders involved in the transport and logistics sector. It is envisaged that this

collection of theme papers, discussing six key areas in which improvement is needed to improve the state of

logistics in India, will be useful to all stakeholders.

Foreword

Although India is among the world's fastest growing economies, its performance in logistics is far behind

compared to other leading countries. This is due to multiple reasons including an unfavorable modal mix,

inadequate transport and logistics infrastructure, and lack of seamless connectivity between different modes

of transport. To address these challenges, a comprehensive and holistic approach towards improving the

state of infrastructure needs to be adopted.

Ministry of Road Transport and Highways (MoRTH) has kicked-off several initiatives including development

of Multimodal Logistics Parks, infrastructure upgradation of freight corridors and IT-based solutions for

facilitating seamless intermodal movement. These initiatives are aimed at making the movement of cargo

on Indian roads more efficient, while at the same time shifting cargo from road to other cheaper and greener

modes including rail, sea and air. To ensure the success of these initiatives, it is hoped that all the relevant

stakeholders, including private parties from India and abroad will come together and join India's logistics

movement under the umbrella of India Integrated Transport and Logistics Summit, 2017 (llTLS). The Summit

is being organized with a view to generate interest and foster partnerships among both public and private

agencies.

This booklet has been prepared to inform the latest trends and happenings in these sectors. I hope that you

will find this material useful and express your valued thoughts over the same in the llTLS.

(Sanjay Mitra)

Foreword

The logistics and transportation scenario in India is poised for a complete makeover. Several important

initiatives have been planned. The Ministry of Road Transport and Highways (MoRTH) had undertaken a

study, called the Logistics Efficiency Enhancement Programme (LEEP), which has identified four key solution

themes to improve the state of logistics in India. These are, freight corridor upgradation, logistics park

development, seamless interstate movement and electronic toll collection systems. Taken together, these

initiatives are expected to reduce India's logistics costs and bring them closer to the accepted global

benchmarks from the current high levels of 13-14% of GDP.

The Ministry plans to develop 35 Multimodal Logistics Parks (MMLPs) in lndia which will, cater to 50% of the

freight movement, enable -10% reduction in transportation costs and -12% reduction in C02 emissions.

Land parcels have been identified and pre-feasibility studies initiated on six of these locations. The parks

will be developed jointly by the National Highways Authority of India (NHAI), the National Highways

Infrastructure. Development Corporation (NHIDCL), other parastatals and the respective state governments.

The government is also working to formulate a uniform policy for the development of MMLPs, It will be our

endeavor to solicit and incorporate the views of all the stakeholders through the India Integrated Transport

and Logistics Summit-2017 (llTLS),

The IITLS will be an excellent platform for all those with interest in transport and logistics sectors to come

together and initiate collaborative partnerships to realize the various greenfield and brownfield opportunities

in logistic parks, freight corridors and IT solutions.

This collection of theme papers has been prepared with a view to inform the readers about the state of

transport and logistics in India, the global best practices and key recommendations to help these sectors

reach world class levels. I hope that our stakeholders will find this useful.

02

Freight movement in India has doubled to ~2,300 Bn Ton Km in FY15, from ~ 1,200 Bn from FY 08 and is expected to continue its growth trajectory, with an expected annual growth rate of 8 - 10% over the next ten years. With this expected growth in freight movement, there is a need to focus on improving the logistics efficiency to reduce the overall cost and time of the freight movement in India.

India’s rankings on global indices related to logistics performance, like the Logistics Performance Index (LPI)of World Bank– where India has moved up in ranking from 54 to 35 – and Ease of Doing Business (EoDB), reflect that the country is heading in the right direction. However, there still is need for focused action – the marginal improvement in key sub-metrics, like Freight movement time and Freight cost parameters of LPI, point towards the same.

India’s freight modal mix is heavily skewed towards roadways with roadways constituting 60% of total freight carried in the country, as against railways which constitutes ~30% of freight movement. The modal share

of railways in India’s freight movement has been decreasing continuously over the years, from 53% in 1990 to 32% in 2015. Modal share of waterways is only 7%. This is in stark contrast to the modal mix of other countries such as China, where both roads and waterways contribute 35-40% each of the total freight carried.

In India, more than 50% of the long-haul freight movement happens by road. Freight movement by road is typically 25 – 30% more expensive than railways for long haul routes. Infrastructure to enable seamless multimodal freight transfer is critical to ensure efficient freight movement in the country.

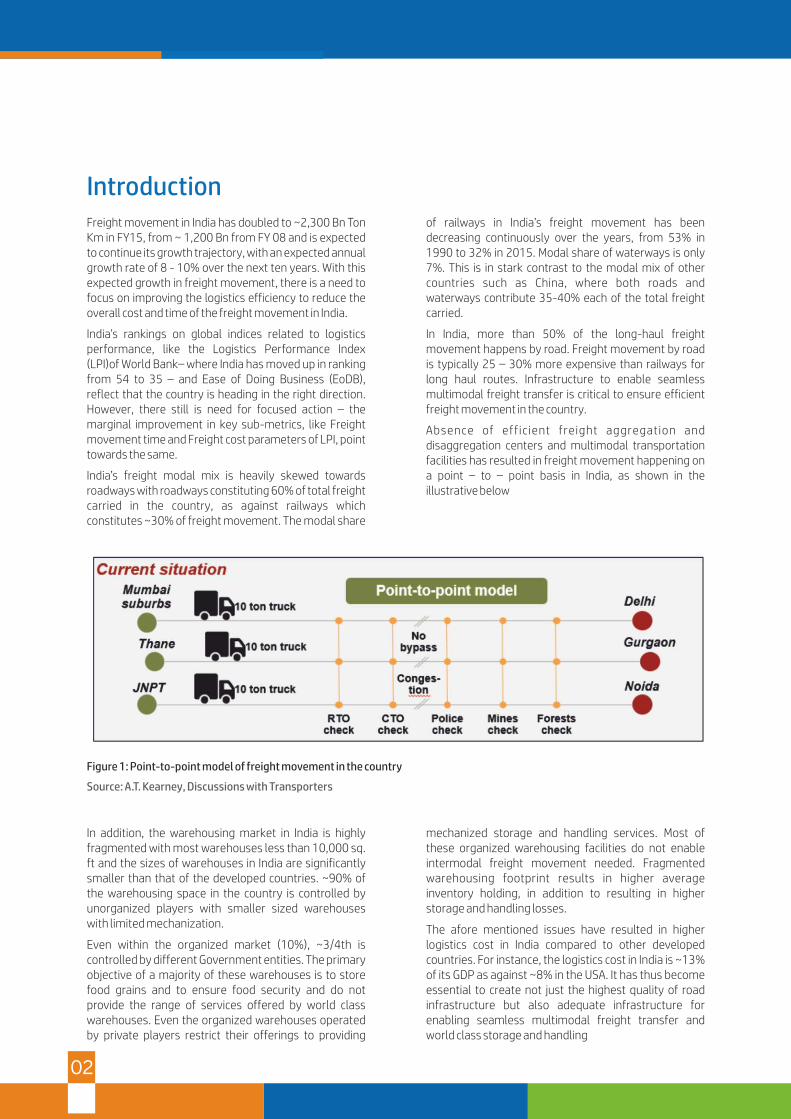

Absence of efficient freight aggregation and disaggregation centers and multimodal transportation facilities has resulted in freight movement happening on a point – to – point basis in India, as shown in the illustrative below

Introduction

Figure 1: Point-to-point model of freight movement in the country

Source: A.T. Kearney, Discussions with Transporters

In addition, the warehousing market in India is highly fragmented with most warehouses less than 10,000 sq. ft and the sizes of warehouses in India are significantly smaller than that of the developed countries. ~90% of the warehousing space in the country is controlled by unorganized players with smaller sized warehouses with limited mechanization.

Even within the organized market (10%), ~3/4th is controlled by different Government entities. The primary objective of a majority of these warehouses is to store food grains and to ensure food security and do not provide the range of services offered by world class warehouses. Even the organized warehouses operated by private players restrict their offerings to providing

mechanized storage and handling services. Most of these organized warehousing facilities do not enable intermodal freight movement needed. Fragmented warehousing footprint results in higher average inventory holding, in addition to resulting in higher storage and handling losses.

The afore mentioned issues have resulted in higher logistics cost in India compared to other developed countries. For instance, the logistics cost in India is ~13% of its GDP as against ~8% in the USA. It has thus become essential to create not just the highest quality of road infrastructure but also adequate infrastructure for enabling seamless multimodal freight transfer and world class storage and handling

With the government increasing focus on developing rail

and waterways infrastructure, and the implementation

of GST turning India into a consolidated market,

developing a network of multimodal logistics parks to

act as logistics hubs will address the afore mentioned

issues

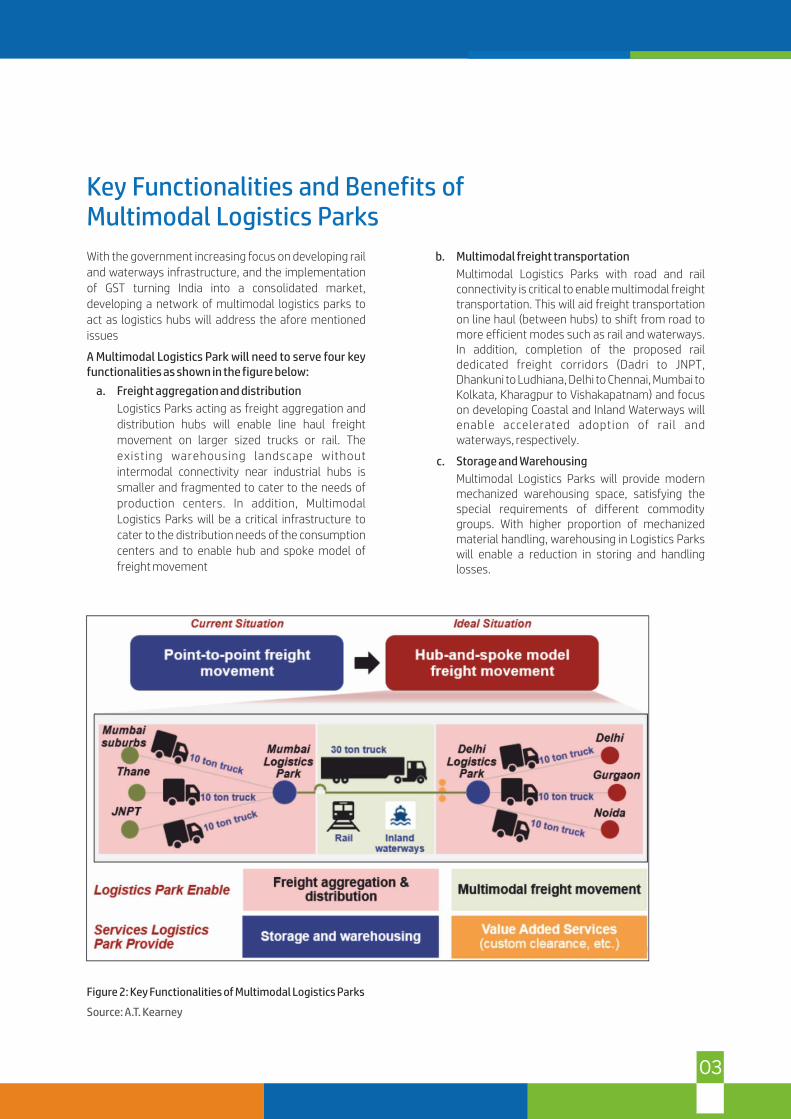

A Multimodal Logistics Park will need to serve four key functionalities as shown in the figure below:

a. Freight aggregation and distribution

Logistics Parks acting as freight aggregation and

distribution hubs will enable line haul freight

movement on larger sized trucks or rail. The

existing warehousing landscape without

intermodal connectivity near industrial hubs is

smaller and fragmented to cater to the needs of

production centers. In addition, Multimodal

Logistics Parks will be a critical infrastructure to

cater to the distribution needs of the consumption

centers and to enable hub and spoke model of

freight movement

b. Multimodal freight transportation

Multimodal Logistics Parks with road and rail connectivity is critical to enable multimodal freight transportation. This will aid freight transportation on line haul (between hubs) to shift from road to more efficient modes such as rail and waterways. In addition, completion of the proposed rail dedicated freight corridors (Dadri to JNPT, Dhankuni to Ludhiana, Delhi to Chennai, Mumbai to Kolkata, Kharagpur to Vishakapatnam) and focus on developing Coastal and Inland Waterways will enable accelerated adoption of rail and waterways, respectively.

c. Storage and Warehousing

Multimodal Logistics Parks will provide modern mechanized warehousing space, satisfying the special requirements of different commodity groups. With higher proportion of mechanized material handling, warehousing in Logistics Parks will enable a reduction in storing and handling losses.

Key Functionalities and Benefits of Multimodal Logistics Parks

Figure 2: Key Functionalities of Multimodal Logistics Parks

Source: A.T. Kearney

03

04

d. Value added services:

Multimodal Logistics Parks are also expected to provide value added services such as customs c learance with bonded storage yards, warehousing management services, etc. Customs clearance at Multimodal Logistics Parks will enable waiting time reduction at the ports and thereby reduce the freight transportation cost and time for cargo. In addition, Multimodal Logistics Parks near the major ports (Chennai, Vishakhapatnam, Mumbai, Kolkata, etc.) will have clearly demarcated Free Trade and Warehousing Zones to enable storage of trans-shipment cargo, without any tax implications.

Multiple benefits exist in developing Multimodal Logistics Parks, over independent warehouses:

a. Seamless inter-modal freight movement

A Multimodal Logistics Park will enable seamless transfer of goods from one mode to another. This

will enable a more efficient hub and spoke model of freight movement.

b. Reduction in inventory holding costs

MultimodalLogistics Parks will provide large modern and mechanized warehousing space. With higher proportion of mechanized material handling, Multimodal Logistics Parks will result in reduction in storage and handling losses. In addit ion, avai labi l i ty of a consol idated warehousing zone will enable reduction in inventory holding costs

c. Reduction in freight transportation lead times

Customs clearance at Multimodal Logistics Parks will enable a reduction in waiting time at the ports. In addition, provisions for packaging/ repacking and return management at the Multimodal Logistics Parks will enable a reduction in overall supply chain lead times.

Lessons from Global Best Practices in Development of Logistics Parks

Case Study 1:Logistics platforms in China

Large scale logistics parks are developed by Government owned entities, either solely or through a Joint venture with private players. Examples of two logistics platforms in China are illustrated below.

GLP Suzhou Park

GLP Suzhou Logistics Park is located within the Suzhou industrial zone, which is the largest free trade zone in the country. Developed in an area of ~ 300 acres, it provides services such as bonded warehousing, customs clearance facilities, facilities for preliminary processing and packaging.

The logistics park is well served by two expressways – Beijing–Shanghai expressway and Nanjing–Shanghai expressway. The logistics park is connected to the Shanghai deep water port (160 km) and Shanghai International Airport (80 km) through these expressways.

GLP Suzhou Park was developed as a 50:50 Joint Venture between Global Logistic Property (GLP), a fund

Multimodal Logistics Parks have been developed in most developed countries and large developing economies to improve the efficiency of freight movement.

A few case studies from global Logistics Parks are highlighted below

manager, developer and operator of logistics parks with a global portfolio of 52 million sq. ft. of warehousing space and SEALL, a government owned entity.

Case Study 2: Logistics platforms in the USA

Large scale integrated logistics parks are typically developed as private limited companies with participation from the Government in the USA. Learning from one such logistics park in Chicago is provided below.

Center Point Integrated Logistics Parks, Chicago

An integrated logistics park was developed by Center Point properties at Joliet, 40 miles southwest of Chicago, covering an area of ~2,200 acres at an investment of USD 1 Billion. The area was formerly a military base which had been c losed, result ing in ~15% unemployment in the area. Department of Defense then released the area for development of Logistics Park, to generate employment and provide an economic boost to the area. Integrated Logistics Park was envisioned to alleviate road congestion within the Chicago metropolitan area and the congestion in Chicago rail

05

interchange. The role of the Government in development of the Logistics Parks is to provide the trunk infrastructure and enabling access to the nearest freeway.

The logistics park location is very well connected by both road and rail. In addition, the Logistics park has advanced infrastructure such as tracks for catering to long double stack trains, GPS enabled cranes, automated cranes. CenterPoint Logistics Park is a huge success driven by excellent rail road connectivity, proximity to a large consumption center and efficient operations. CenterPoint Logistics Park created ~8,000 direct and indirect jobs in the region.

Key lessons from an assessment of Global Logistics Parks are highlighted below

a. Adequate connectivity:

Dedicated trunk infrastructure to connect the Logistics Parks to the arterial network of transportation modes, such as National Highways network, Railways network, port and inland waterway terminals, etc. is essential to ensure efficient freight evacuation from Logistics Parks. Successful logistics parks have railway sidings, dedicated connectivity to the expressway network

There is a need to develop Multimodal Logistics Parks in all the major production and consumption centers in the country. Locations for development of Multimodal Logistics Parks will need to be prioritized based on the amount of freight flow, need for trunk infrastructure connectivity and the extent of competing facilities available.

35 locations which account for ~50% of the road freight movement will be ideal candidates for Investments in Multi modal Logistics Parks in India in the first phase.

The land parcel for development of Multimodal Logistics Parks need to be based on an assessment of freight flows and the connectivity requirement, within each node.

The factors that need to be considered for prioritization of clusters for the development of Multimodal Logistics parks are highlighted below:

a. Freight flow assessment

A detailed assessment of the road and rail freight flow patterns will need to be conducted for each

to improve freight evacuation from the Multimodal Logistics Parks.

b. Multipurpose facilities

M o st s u c c essf u l Lo g i st i c s Pa r ks h a v e multipurpose facilities and are customizable to cater to the needs to different commodities and industries including cold storage, open storage yards, etc. In addition, logistics parks have provisions for late stage manufacturing activities such as kitting and final assembly, grading, sorting, labeling and packaging activities, re-working, return management etc. the customers. The norms for land usage for different activities shall be well defined.

c. Management Model

Logistics parks have been developed by private players as well by the sovereign, through a public private partnership model. The role of the Authority in the PPP model has been restricted to providing the required land and the trunk infrastructure connectivity, while the private concessionaire has been responsible for development and operation of the Logistics Parks.

Location and Design Guidelines for Multimodal Logistics Parks

node to understand the direction of the freight movement. Land parcels along the Highway with maximum freight flows need to be prioritized for development of Multimodal Logistics Parks.

b. Proximity to production and consumption zones

While Multimodal Logistics Parks will ideally need to be located outside the limits of the city to enable congestion reduction in the city, land parcels that are closer to the city limits, preferably along the ring roads/ city bypasses will need to be prioritized. Land parcels near Industrial / Manufacturing parks will need to be prioritized to maximize the network effects of combined logistics and manufacturing activity.

c. Connectivity requirement

Land parcels near National Highways and Railway network with good access to other modes such port and inland waterway terminals will need to be accorded higher priority for development of Multimodal Logistics Parks

06

In addition, the size and facilities needed at each

Logistics Park will depend on the key commodities

produced and consumed by the individual location.

Area required for developing a multimodal logistics park at any location will need to be determined based on the projected commodity wise freight originating and terminating at that node. For instance, a location with higher proportion of perishable agri - commodities will need a higher proportion of warehousing space dedicated to cold storage. Similarly, commodities with higher average inventory holding will need to be allocated higher storage space.

Multimodal Logistics Parks will need to have five broad zones to fulfil the functionalities as highlighted in the previous section viz., Commodity storage zone, Intermodal zone, Value added services zone, Ancillary service zone and Vehicle Parking zone. While majority of the area will need to be dedicated to core logistics activities – Warehousing, Intermodal Areas, Value Added Services and Custom Clearance facilities, provision will need to be made for other ancillary logistics activities such as vehicle sales and service including vehicle service areas, People service areas, office spaces for logistics service providers, transporters etc.

Figure 3: Top 35 clusters identified for development of Multimodal Logistics Park

Source: A.T. Kearney

Private investments in development of Multimodal Logistics Parks have been muted primarily owing to restricted land availability, lack of dedicated trunk infrastructure connectivity to enable efficient freight evacuation. In addition, the potential returns for private players from their investments in development of Multimodal Logistics Parks including land ownership is limited. Also, the availability of long term financing is currently constrained for warehousing sector, as they are treated as a commercial activity, unlike the infrastructure sector, with access to long term project

Management Modelfinancing. Hence, the role of the Government through a Public Private Partnership (PPP) model is essential in enabling private investments in development of Multimodal Logistics Parks. In addition, Government will need to provide infrastructure status for development of Multimodal Logistics Parks to enable easy access to credit and tax benefits for private developers

The large-scale investment requirement for such high-value projects and constrained government resources for physical infrastructure investment highlights the importance of attracting private partnerships in such

Logistics parks will drive a reduction in overall freight cost by enabling freight transportation on higher sized trucks and rail. In addition, multimodal logistics parks will enable reduction in vehicular pollution and congestion in key cities.

Logistics parks are expected to provide four key benefits as summarized below

i. Transportation cost reduction

Logistics parks will drive ~10% reduction in transportation cost for the top 15 nodes by enabling freight movement on higher sized trucks and rail. Larger sized trucks have ~60% lower freight cost on a per ton per km basis compared to lower sized trucks. Further, estimates suggest freight cost by rail is ~45% lower on a per ton per km basis compared to average road freight cost.

ii. Pollution reduction

Increased freight movement on higher sized trucks and rail will enable in ~12% reduction in CO2emissions for the top 15 nodes. Higher sized vehicles, because lower fuel consumption per ton per km, will result in lower CO2 emissions. Further,

Expected Impact of Multimodal Logistics Parks

freight movement by rail has ~ 65% lower CO2 emissions compared to road freight on a per ton per km basis. Similarly, there will be a corresponding reduction in PM, CO and HC+NOx emissions, driven by increased freight movement on higher sized vehicles and rail.

iii. Congestion reduction

Increased freight movement on higher sized trucks and rail will result in ~20% reduction in freight vehicles catering to the demands of the top nodes. In addition, shifting warehouses and wholesale markets, currently being operated inside the city, to logistics parks would free up urban spaces, enabling congestion reduction.

iv. Warehousing cost reduction

Shifting warehouses, currently being operated inside city limits, to logistics parks will enable reduction in warehousing cost, driven by lower rentals in logistics parks situated outside the city limits. In addition, modern and mechanized storage solutions provided by logistics parks will enable reduction in storage and handling losses

projects. Public Private Partnership Models ensure sizeable investments are being made in public infrastructure while ensuring that the global best practices are leveraged through private participation

Since the development and operation of Multimodal Logistics Parks involve multiple Union Government departments handling different modes of travel viz., Roadways, Railways, Inland Waterways, etc., coordinated action between the different departments is critical to ensure efficient planning and development of Logistics Parks. In addition, involvement of the respective state governments is essential to ensure easy land acquisition.

Central Government agencies will need to form a Special Purpose Vehicle (SPV) with the different state

governments, where the state government shall be responsible for land acquisition and the central government agencies shall be responsible for providing road and rail connectivity to the site. The SPV shall then appoint private developers for development and operation of Logistics Parks. In addition, Government need to consider provision of infrastructure status and connectivity to large multimodal Logistics Parks, being developed by private developers.

A draft policy on Multimodal Logistics Parks highlighting the location and design norms, proposed management model, etc. has been drafted by the Ministry of Road Transport and Highways. The draft policy is provided in annexure 1, after this chapter.

07

08

Annexure 1Development of Multimodal Logistics Parks – Draft Policy Document

1.Multimodal Logistics Parks- Location Norms and Design Principles There is a need to develop Multimodal Logistics Parks in all the major production and consumption centres in the country. Locations for development of Logistics Parks shall be prioritized based on the amount of freight flow, need for trunk infrastructure connectivity and the extent of competing facilities available. With a view to the economic viability of the Logistics Parks, Logistics as a sector will be considered for grant of ‘Infrastructure status’. Since customs bonding facil it ies for export/import of cargo, and quarantine facilities for clearance of food items would be mandatory, the requisite provisions will be made by involving the concerned Ministries/ central agencies.

1.1 Norms for Location Identification

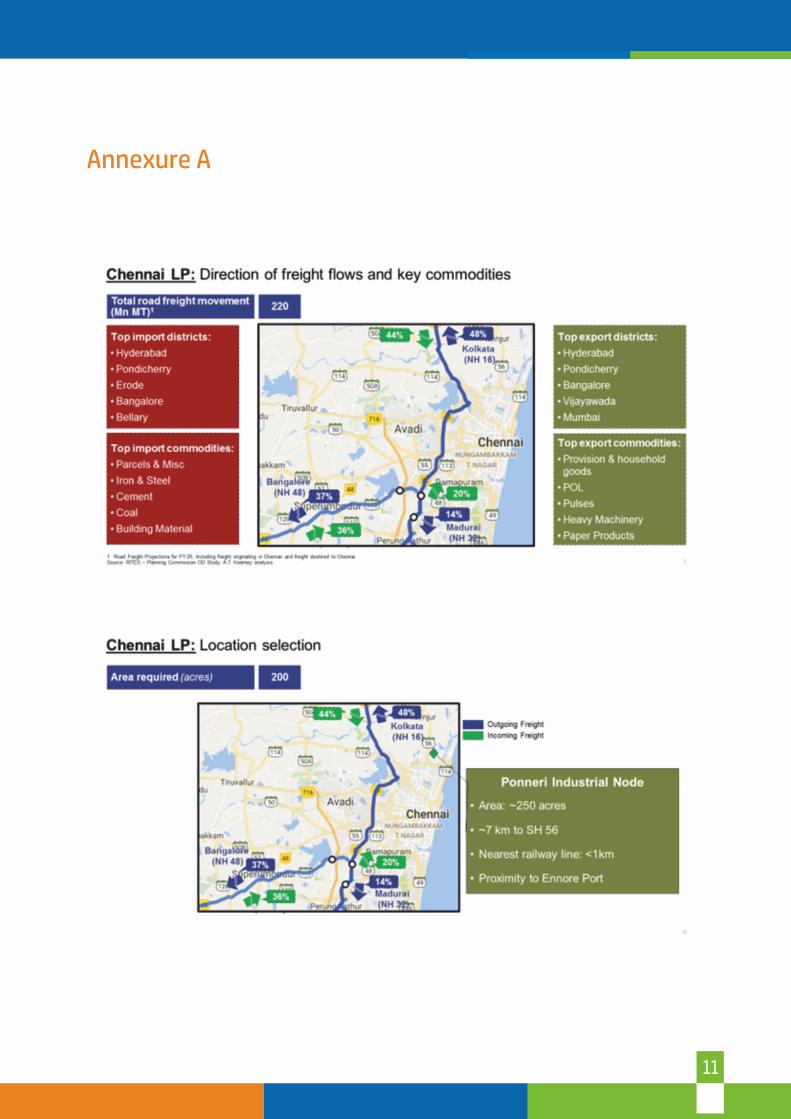

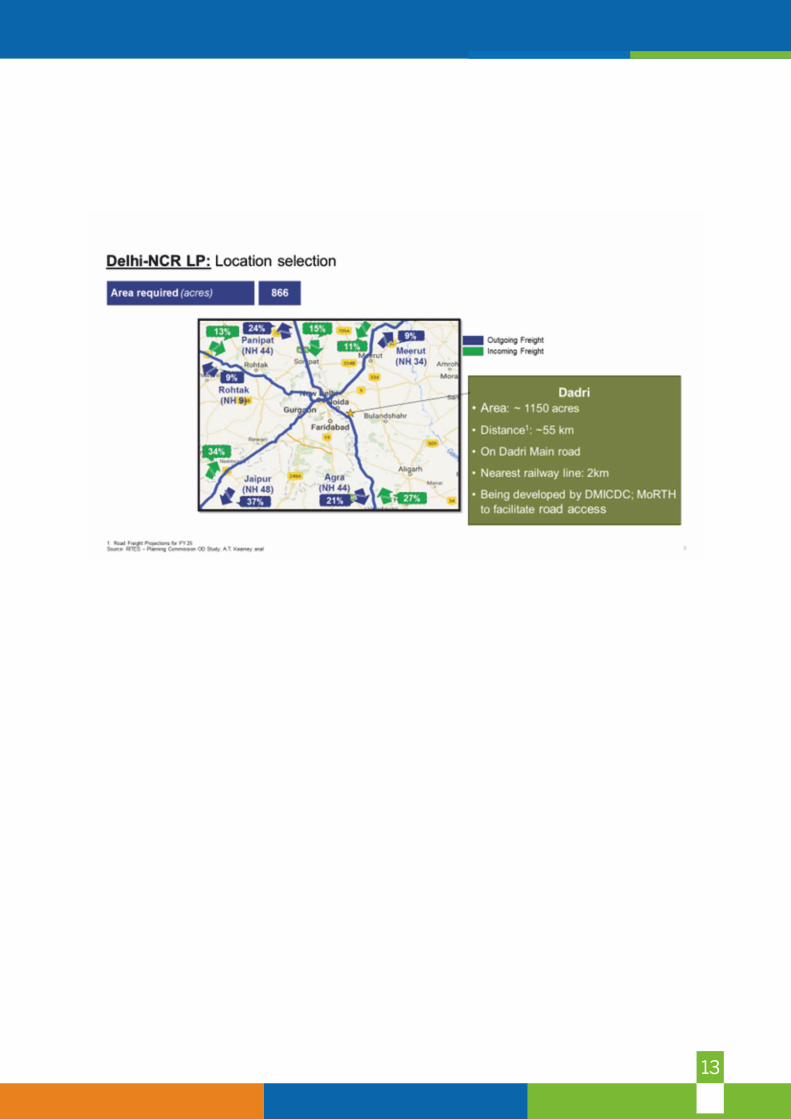

35 locations which account for ~50% of the road freight movement have been identified for developing multimodal logistics parks in phase 1. An indicative list of some locations and their economic potential is at Annexure A. The prioritized list of 35 locations is provided in Annexure B.

The land parcel for development of Logistics Parks shall be finalized based on an assessment of freight flows and the connectivity requirement, within each node.

a. Freight flow assessment

A detailed assessment of the freight flow patterns shall be conducted for each node to understand the direction of the freight movement. Land parcels along the Highway with maximum freight flows from and to the node shall be prioritized for development of Logistics Parks. A network of Logistics Parks shall be developed along the Highways carrying large freight flows to cater to the needs of the node.

b. Proximity to production and consumption zones

While Logistics parks shall be developed outside the limits of the city to enable congestion reduction in the city, land parcels that are closer to the periphery of the city, preferably along the ring roads/ city bypasses shall be prioritized.

c. Connectivity requirement

Land parcels near National Highways and Railway network with good access to other modes such

port and inland waterway terminals shall be prioritized for development of Logistics Parks.

1.2 Design Principles

The size and facilities needed at Logistics Parks Facilities needed at each Logistics Park depend on the key commodities produced and consumed by the individual location. In addition, the extent of competing facilities catering to the needs of the city shall be assessed to evaluate the size of the facility needed.

a. Area required for building a logistics park at any particular location will be determined based on the projected commodity wise freight generating and terminating at that node. The following factors would be considered in estimating the area required

i. Type of storage needed by commodity – covered, open or special storage

ii. Attractiveness of value proposition of the logistics park for each commodity group and hence propensity of using the services offered by logistics parks

iii. Average inventory days and seasonality factor of each commodity

iv. Material bulk density and storage norms for each commodity

v. Competing infrastructure catering to the requirements of the city

b. There will be five broad zones

i. Commodity storage zone – dedicated zones for different types of commodity and bonded storage yard along with vehicle loading ramps, cross docking facilities.

ii. Intermodal zone – rail siding area for intermodal freight transfer; terminals for inland waterways, wherever applicable.

iii. Value added services zone- Package, Re-packaging, Processing, Re-processing.

iv. Ancillary services zone – dedicated area for other value added services such as customs clearance, vehicle service area, office spaces, restaurant, Retail & wholesale, Hotels and entertainment etc.

v. Vehicle parking zone – dedicated area for vehicle parking.

09

d. Multimodal Logistics Parks can be developed on the following suggested lines

• 50 - 55% of the area allocated for Core Logistics Activities, which includes-

- Warehousing Zone: Open Storage, Covered Storage, Regulated Storage, Cross Docking Facilities

- Intermodal Areas: Rail Siding, Loading/ Unloading facilities, Inland Waterway terminal (where applicable) and Air Cargo Terminal (where applicable)

- Value Added Services: Labelling, Packaging, Re-packaging, Processing/ Re-Processing, Kitting, Assembly, Return Management, etc.

- EXIM Clearance: Custom clearance services, bonded storage, testing facilities, quarantine zones

• 10 – 12% of the area allocated for Ancillary Logistics Activities, which includes -

- Vehic le sales and ser v ice: Vehic le maintenance, fuel stations (along with air filling station, puncture repair & pollution check), consumer vehicle sales

- People Service: Lodging, sanitation, dhabas, dormitories for truckers, loaders, unloaders, etc.

- Office spaces: Office space for Logistics Service Providers, Transporters, etc.

• 15 – 17% of the area allocated for truck parking and internal roads for trucks

• 10 – 12% of the area allocated for administrative facilities and commercial zone such as Banks, ATMs, Medical facilities, Retail and wholesale area, Entertainment, convention centres, etc.

• 10 – 12% of the area allocated for landscaping and development of open green zones

• Prevailing standards and norms for safety, operation and maintenance will be applicable

e. Adherence to ‘Green Principles’ will be encouraged. These would include

i. Extensive horticulture and plantation along with adequate sewage treatment

ii. Recycling of water for landscaping and horticulture

iii. Use of natural materials like dry stone cladding for exteriors

iv. Use of bio-methanation for treatment of bio waste and for generation of cooking gas

v. Rainwater harvesting

vi. Provision of single/ double glazed windows with

matched U-Factor for increased energy efficiency

vii. Provision of adequate ventilation and natural day light

2. Management Model Private investment in development of Logistics parks has been muted primarily due to restricted land availability, lack of dedicated trunk infrastructure connectivity to enable efficient freight evacuation. In addition, the potential returns for private players from their investments in end to end development of Logistics Parks including land ownership is limited. Hence, the role of the Government through a Public Private Partnership (PPP) model is essential in enabling private investments in development of Logistics Parks. Participation from private players with prior experience in developing and operating such facilities will ensure that the learning from global best practices in design and operations are leveraged. Participation from the Government will ensure land availability as per land use norms, and trunk infrastructure development, together with fulfilment of regulatory requirements, all of which are critical for the success of Logistics Parks.

The Project Proponents—Central/State Government/ private developer-- can drive the development of Logistics parks by setting up SPVs with the NHAI and/or other related agencies such as Port Trusts, IWAI, CONCOR, AAICLAS, Port-Rail Corporation etc. The proponent can assemble the land required for development of Logistics Parks and the requisite trunk infrastructure would be provided by NHAI. Wherever relevant, the concerned central agency would be a part of the SPV; Railways for providing rail connectivity, Port Trust/IWAI for Port/ Waterways connectivity and AAI for Air Cargo Hubs. The equity participation would be decided by the SPV members, who would also finalise the appropriate PPP model, Concession terms, period etc.

3. Implementation GuidelinesThis section highlights key elements of the execution model, as well as roles and responsibilities of the concessionaire and the government entities viz., NHAI/central agencies and State Industrial Development Corporations.

a. Private developers shall be invited for bidding based on approved RFP and contract document.

b. Bidding for each logistics parks may be done separately.

c. Development, operation and maintenance of Logistics Parks shall preferably be done on a

10

Build Operate Transfer (BOT) model. The Model concession agreement for development of Logistic Parks may be finalised by the stakeholders/State Government and specify the following:

i. Bidding parameters

ii. Concession fee

iii. Service parameters.

iv. Concession period

v. Specification and standards

vi. Monitoring mechanism

vii. Incentives and penalties

viii. Facilities

ix. Blue print

3.2 State Government as the key stakeholder

35 locations which account for ~50% of the road freight movement have been identified for developing multimodal logistics parks in phase 1. An indicative list of some locations and their economic potential is at Annexure A. The prioritized list of 35 locations is provided in Annexure B.

The land parcel for development of Logistics Parks shall be finalized based on an assessment of freight flows and the connectivity requirement, within each node.

• State Government can provide the land required for the Logistics Park or it can be assembled/ mobilised from private developers, with the said land parcel necessarily conforming to all prevailing state legislations. State Government shall also facilitate all the regulatory approvals needed for land use conversion, before an encumbrance free land parcel is provided to the Concessionaire for development of Logistics Parks.

• State Government Authorities shall facilitate utility connections (Power, Water, Sewerage, etc.) for the Logistics Parks in a time bound manner and also ensure seamless movement of trucks into the Logistics Parks with enabling traffic regulations. In addition, the State Government shall make appropriate arrangement to maintain Law and Order within and around the Logistics Parks.

• State Governments should plan and facilitate development of Industrial and Manufacturing Parks adjacent to Multimodal Logistics Parks through appropriate zoning and master planning norms to ensure that network benefits of co-located Industrial and Logistics Parks are realized.

3.3 Role of ConcessionaireThe role of the concessionaire is to be defined in the MCA. Broadly, it may include the following:

i. Funding for the project

ii. D e t a i l e d d e s i g n a n d e n g i n e e r i n g responsibilities

iii. Operation and Maintenance of the multimodal Logistics Parks in line with the service level agreements mentioned in the concession agreement finalized with the Authority

b) While the overall responsibility of development, operation and maintenance of Logistics Parks shall rest with the concessionaire, the concessionaire shall be permitted to engage with third party contractors to outsource certain elements of the Logistics Parks, as needed. The concessionaire shall be responsible for obtaining all requisite permission(s) from the concerned authorities for design, construction, operation and maintenance of the site.

11

Annexure A

12

13

14

Logistics park location

Delhi – NCR (Delhi, Gurgaon, Ghaziabad, Faridabad, Noida)

Mumbai (Mumbai, Mumbai Suburbs, JNPT, Mumbai Port, Raigad District)

North Gujarat (Ahmedabad and Vadodara)

Hyderabad

South Gujarat (Surat and Bharuch)

South Punjab (Ludhiana, Sangrur, Patiala)

North Punjab (Amritsar, Jalandhar, Gurdaspur)

Jaipur

Kandla

Bangalore

Pune

Vijayawada

Cochin

Chennai

Nagpur

Indore

Patna

Kolkata

Ambala

Valsad

Coimbatore

Jagatsinghpur

Nasik

Guwahati

Kota

Panaji

Hisar

Visakhapatnam

Bhopal

Sundargarh

Bhatinda

Solan

Rajkot

Raipur

S.No.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35 Jammu

Locations prioritized for development of Multimodal Logistics Parks in Phase

Annexure B

16

The need to prepare India’s urban mobility for future: Case for passenger mobility

Passenger mobility challenges

Indian cities, especially the populous ones, face

multitude of challenges, many of which are caused by

non-controllable factors like high population density and

historical unplanned construction. Lack of funds with

urban local bodies is another major issue. These

constraints have led to gaps in India’s urban

transportation and mobility which can be classified into 3

areas: Infrastructure, Transport modes and ICT

enablement.

Infrastructure

Infrastructure forms the backbone of transportation.

However, India has visibly poor transportation

infrastructure. Road construction has not matched the

India is going to witness rapid urbanization in coming decades with 50% of India’s population slated to live in urban areas by 2050, up from about 30% today. Urban population during the period 2010-50, is estimated to grow at a CAGR of 2%, while the demand for urban mobility during the same period is estimated to grow at a CAGR of 5%. Growth in urban mobility is outstripping the urban population growth due to: concentration of economic activity in urban areas, increase in affluence level of city dwellers leading to greater use of private vehicles and expansion of cities.

vehicle fleet growth. Vehicle fleet registered an average

decadal growth of 10-12% between 1971 to 2011, but

the corresponding growth of road infrastructure was a

mere 3% during this period.

Transit Modes

Public transport in most Indian cities is inadequate and has not matched the growing mobility needs. This leads to dominance of non-motorized modes among the lower economic strata and an increased propensity towards usage of private vehicles, as the affluence level rises. Delhi has metro penetration which is only about one-fifth of some of the global cities. Suburban rail ridership in Mumbai, though comparable to the global benchmarks, suffers from poor safety standards and is not disabled friendly.

375470 525

815

2010 2020 2025 2050

CAGR 2%

Urban population(2010- 2050, in million)

Urban mobility demand(2010-2050, in BPKM)

2010 2020 2030 2050

800

1,750

3,200

6,000CAGR 5.2%

CAGR 7%

Figure 4: Urban Population and mobility demand (2010-2050)

Source: Transport Scenarios for India: Harmonizing development and Climate benefits, UNEP DTU

17

1Public Bus Fleet(Fleet/ million persons)

Del Mum S’ pore Hong K Tokyo London New York

168 171

765816

163

918

527

13%

60%

40%

61%70%

40%

54%

Del Mum S’ pore Hong K Tokyo London New York

Metro/ suburban rail ridership(avg. daily passengers as % of city population)

Indian cities Global Benchmarks

1. Data for 2016 for mumbai and Delhi and 2012 for other global cities

Figure 5: Comparison of public transport in Delhi and Mumbai with global cities

Source: Review of Urban transport in India by Institute of Urban Transport, Centre for Study of Science technology and Policy (CSTEP), Press sources

ICT Enablement

A robust ICT backbone can have significant impact on

passenger mobility over short term. However, India lags

in digital connectivity for urban transit. Amenities like

multipurpose smart cards, real time passenger

information for city buses, multi modal journey planning

mobile applications etc. are still not available in most

cities.

Consequences of inadequate public transport

Most Indian cities have gaps in passenger mobility

needs. Around 40% of the urban population even in

major Indian cities like Delhi are dependent on non-

motorized modes like walking and cycling. A substantial

proportion of non-motorized commutes could be due to

non-availability of adequate public transit. Experience at

Bogota showed that post BRTS implementation, there

was a drop of almost 6-7% in the non-motorized modes

due to adequate connectivity to public transport.

Inadequate public transport infrastructure and

proliferation of private vehicles leads to: congestion on

city roads, higher greenhouse gas emission.

Economic development of cities and meeting

consumption demand at low prices relies on efficient

urban freight transit. Freight movement, just like

passenger movement, is likely to witness a steeper

increase than urban population growth due to increase in

GDP contribution of cities, expansion of cities and

increase in per capita consumption. Projecting RITES

freight origin destination data for 2008 to 2015 and

2025, shows that both inbound & outbound freight per

capita will increase at a CAGR of 7% during the next

decade, due to increasing consumption and production

in the major Indian cities. Because of higher demand and

production activity, overall demand for freight

movement in India is projected to grow at CAGR of 9%.

The need to prepare India’s urban mobility for future: Case for freight mobility

Freight mobility challengesGaps in urban freight mobility can be classified in a manner like urban passenger mobility i.e. around three factors: Infrastructure, Transit Modes and ICT enablement.

Infrastructure

Most urban cities in India lack an efficient warehousing infrastructure. Warehouse ownership in India is highly fragmented, with 85% of warehouses owned by unorganized players. Warehouses also predominantly exist within the city limits. Fragmented warehouse footprint within city limits precludes freight pooling, leading to higher number of intra-city freight trips while also necessitating entry of HCVs in the city which adds to congestion.

18

Infrastructure for Intermodal connectivity

Integration of city’s transport modes and a seamless

connectivity including last mile passenger connectivity

Global best practices- Passenger mobilityto public transport can facilitate the use of public

transit and development of economic circles, as can be

seen in the case of Miami.

Freight carriage modes

Unlike developed countries, Indian cities still have large number of non-motorized freight carriers like hand carts, pedal carts, bicycles etc. A study by Professor S.L. Dhingra suggests that up to 25% of intra-city freight movement in Indian cities could be through non-motorized modes. In most cities, non-motorized modes routinely use main arterial roads of the cities and congest traffic in case of mixed stream traffic.

ICT enablement

Several solutions around vehicle tracking, fleet

management, packing and route optimization are available. However, these digital solutions have still not picked up in urban freight management. Simple tracking and tracing solutions offer little benefit in the short haul freight carriage. Other technologies like route optimization for tertiary and last mile freight distribution are relatively new and have seen limited adoption due to reasons like: unproven benefits, dominance of point to point movement and unorganized nature of trucking industry.

Case Study 1: Miami Intermodal Center

Situation- Florida Department of Transportation envisaged Miami Intermodal Center to improve

connectivity in Miami Dade County & improve connectivity to International Airport

Solution- Construction of Miami Intermodal Centre brought together the Airport, the central train station

and a major car rental station. Key features of this station are-

• Automated people mover to connect airport, train station and car rental center

• Miami central station and an inter-city bus center

• Metrobus connecting Miami with central station

• Roadway improvement project and a user-friendly car rental center

Impact- Multimodal connectivity reduced congestion on the important corridor connecting airport. Rental

car shuttles were eliminated and replaced with MIA mover, thus reducing unnecessary intra city movement.

It is estimated that 30% traffic was reduced from the roadways.

(Source- MIC, Florida Department of Transport)

While development of Multi modal stations along MRTS

network can shape commuters’ preferences towards

public transit, finding enough land parcels for

development of these stations may prove to be a major

challenge in India. Such challenges call for radical and

innovative solutions. Case study on city of Seoul

describes one such solution.

19

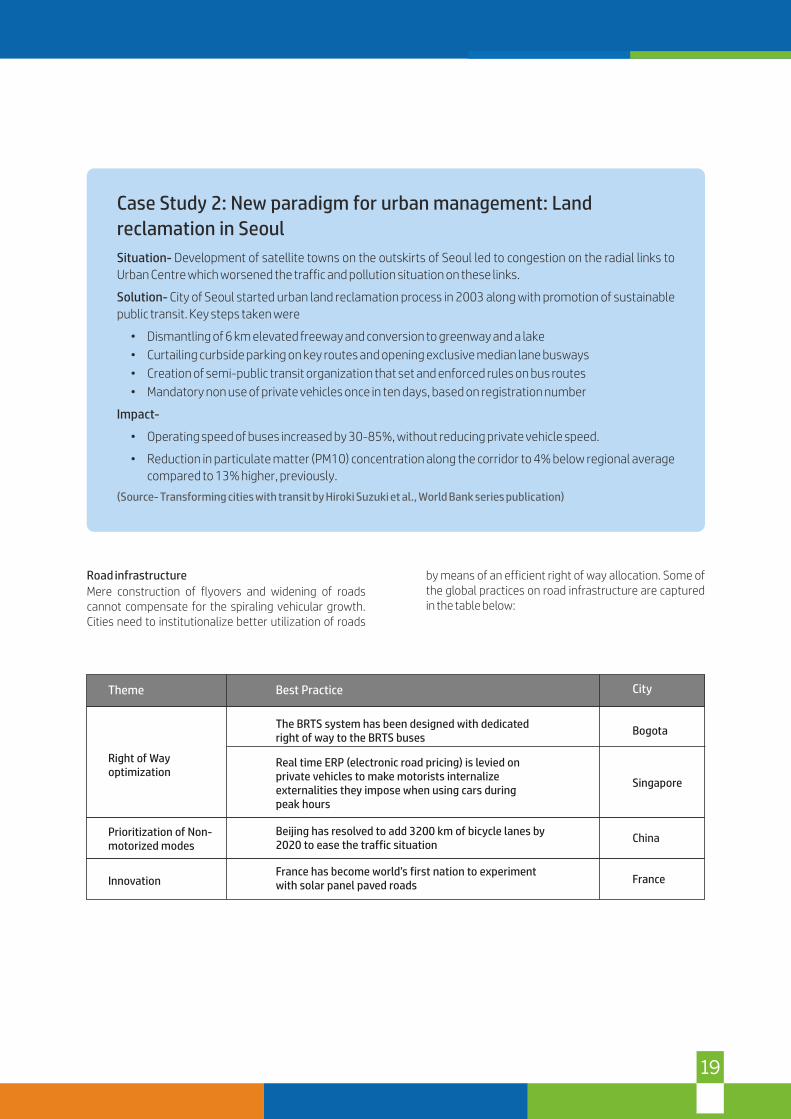

Case Study 2: New paradigm for urban management: Land

reclamation in Seoul

Situation- Development of satellite towns on the outskirts of Seoul led to congestion on the radial links to

Urban Centre which worsened the traffic and pollution situation on these links.

Solution- City of Seoul started urban land reclamation process in 2003 along with promotion of sustainable

public transit. Key steps taken were

• Dismantling of 6 km elevated freeway and conversion to greenway and a lake

• Curtailing curbside parking on key routes and opening exclusive median lane busways

• Creation of semi-public transit organization that set and enforced rules on bus routes

• Mandatory non use of private vehicles once in ten days, based on registration number

Impact-

• Operating speed of buses increased by 30-85%, without reducing private vehicle speed.

• Reduction in particulate matter (PM10) concentration along the corridor to 4% below regional average

compared to 13% higher, previously.

(Source- Transforming cities with transit by Hiroki Suzuki et al., World Bank series publication)

Road infrastructure

Mere construction of flyovers and widening of roads cannot compensate for the spiraling vehicular growth. Cities need to institutionalize better utilization of roads

Theme

Right of Way optimization

Prioritization of Nonmotorized modes

-

Innovation

Best Practice

The BRTS system has been designed with dedicated right of way to the BRTS buses

Real time ERP (electronic road pricing) is levied on private vehicles to make motorists internalize externalities they impose when using cars during peak hours

Beijing has resolved to add 3200 km of bicycle lanes by 2020 to ease the traffic situation

France has become world’s first nation to experiment with solar panel paved roads

City

Bogota

Singapore

China

France

by means of an efficient right of way allocation. Some of the global practices on road infrastructure are captured in the table below:

20

City Bus-stop infrastructure

Global best practices in bus-stop design focus on accessibility and improved passenger amenities. Select

best practices in bus stop design are captured in the graphic below.

Figure 3: Global best practices in bus stop design

Trends in transit modes

With the advent of ride sharing and vehicle sharing platforms, there are early signs of declining propensity of private vehicle use as well as stagnating conventional public transit use in some cities in affluent nations. In US, driving license penetration is declining across age groups. Subway ridership and conventional para transit

ridership is also seeing stagnation or decline in some of the US cities. On the other hand, mobile app based taxi hailing services like Uber have seen huge growth. We expect an increased propensity of users towards personalized service, better connected modes and a shared economy in Indian cities as well:

Figure 4: Trend in urban transit modes for India

21

Trends in transit technologies: New transit technologies are connecting commuters with transit services to provide a seamless mobility experience. Digital solutions

are emerging for each segment of commuter’s journey. Figure 6 below captures some of the ICT solutions.

Figure 6: ICT technologies for passenger transportation

Global best practices in urban freight mobility

Trends in infrastructure

An interface between long haul inter-city and last mile urban freight transport enables freight aggregation. Multi modal logistics hubs at city periphery enable

efficient freight aggregation. Large scale operations of these hubs allow for investments in infrastructure like rail/ road networks and ICT implementation.

Case Study 3: Center Point Intermodal Center- Elwood, Illinois

Situation- Center Point was formerly a military base and it was decided to convert it to a logistics park to provide economic boost to the area.

Solution- Center Point Intermodal Center was set up as a public private investment. Total investment was

around $1 billion. Key features of the intermodal center are

• PPP model with private player managing operations & public authority regulating service

• 2500+ acres integrated logistics center; 1400-acre industrial park

• 100-acre equipment management area

• 12+ million square feet of industrial facilities

• Rail connectivity

Impact- Setting up of logistics park enabled streamlining of long haul as well as short haul freight movement. As per Center Point’s estimate, a 500,000 sq.ft distribution facility in the center could save as much as $500,000 annually in drayage.

22

Recommendations for Passenger mobilityInfrastructure

Improve multimodal connectivity- India has planned to construct a network of multimodal stations, integrating intercity rail and bus as well as the urban transit modes l ike MRTS, paratransit and private vehicles. Development of inter-modal stations was also committed in India’s Union Budget 2017 and the stations

at Nagpur and Varanasi are in DPR stages. Urban transport agencies are also promoting multi modal connectivity. DMRC, for instance, is planning 9 multi modal stations on the under-construction metro lines 7 and 8. In as many as 20-25 cities of India, MRTS networks are under different phases of planning or construction. India should promote multimodality at key stations in

Trends in freight carrying modes

EU nations, with almost 100% motorization of urban transit, are promoting electric and non-motorized freight transit, since these modes produce fewer

emissions, generate less noise and have lower safety risk for pedestrians. The case study below presents the initiatives taken in European Union towards integrating non-motorized modes in urban freight logistics.

Case Study 4: CYCLELogistics in EU

Situation- CYCLELogistics project aims to move 25%-33% urban deliveries through cycles/ non-motorized

modes to cut GHG emissions by integrating the bicycles for last mile delivery.

Solution- EU is actively promotingnon-motorized logistics and has taken following initiatives-

• Cyclelogistics Federation delivered training for cargo bikes usage & setting up IT solutions

• Participating municipalities to set up consolidation-centers, implement low-emission zones

• End users to be made aware of their market shaping powers

Impact-

• These measures have led to setting up and expansion in operations of about 110 specialized cycling

couriers services.

• Multiple EU nations have come up with funding schemes for cargo bikes

(Source- https://ec.europa.eu/energy/intelligent/projects/en/projects/cyclelogistics, ECF website)

Trends in technology

• Fleet management

Fleet management solutions are moving beyond simple tracking and remote diagnostic technologies to advanced solutions like route optimization, truck size selection, improving packing efficiency. These features focus on better monitoring as well as enhanced asset utilization. Apart from the OEMs, startups have devised numerous solutions for fleet management. Some of the prominent global startups in this space are: Zonar systems which provides solutions in pre-post trip inspection and Peloton which provides solutions for improving fuel efficiency and collision avoidance.

• Demand management

Advancements like online freight exchanges, on-demand truck placement etc. have emerged in the market. Some companies like Convoy are already gaining traction in US in this space and disrupting the short-haul, less than truckload ecosystem by providing on-demand, guaranteed trucks as well as shipment management through real-time tracking and billing/ payment through app. Indian trucking eco-system which comprises on manual demand matching through brokers and large number of small trucking firms can gain from these advances. Newer technologies like UAVs/ drones are also emerging.

23

these new MRTS systems. Government should draw a policy framework that ties in relevant government entities and private operators. Framework should specify clear roles and responsibilities along with sources of investment. A coordinating agency (like UTTIPEC- Unif ied Traffic and Transportation Infrastructure Planning & Engineering Centre of Delhi-NCR) should work in close coordination with MRTS corporations, road transport authorities, urban local bodies of the city to develop a blue print of the multi modal stations.

Transit Modes

• Regulatory framework for new transit modes

A decisive policy framework should be adopted that can enable integration of new modes into city transit network. For example, India’s Motor Vehicle (amendment) act, 2016 aims to bridge the existing policy gap for taxi aggregators, by laying out clear guidelines for taxi aggregators as well as the state governments to promulgate laws to regulate the services. A clear regulatory framework should be created to integrate these modes seamlessly with city transport, which can enable collaboration with public transit for efficient last mile connectivity.

• Uptake of innovations in transit modes

Proposed Motor Vehicle (amendment) Act, 2016, could allow for testing of driverless cars in India. India is also exploring option for introduction of innovative modes like electric vehicles. There is also a proposal to set up Private Rapid Transit System in NCR. Timely offtake of these new technologies can be ensured by accelerating regulatory clearances as well as co-development of specifications by Government agencies like NHAI and the OEMs.

ICT Implementation: Multi Modal Mobile application for virtual integration of transit modes

Indian Railways has decided to develop an integrated mobile application which would integrate rail tickets with taxi booking. Ministry of Road Transport and Highways is also in the process of building a multimodal mobile application. India should aim for a systematized approach for full scale virtual integration spanning multimodal scheduling, passenger information and e-reservations. Policy and guidelines are also required to ensure access of private players to travel and real-time information for different government run public transit modes.

Recommendations for freight mobilityInfrastructure: Efficient hub and spoke model

Government has planned to set up 35 large scale Multi

Modal logistics park in India with an investment of INR

50,000 crores, through PPP mode. As next steps, the

Government should incentivize investments by 3PL

operators, road and highway companies, railway freight

operators and end user industries in warehousing sector.

Freight carriage modes

• Integrating non-motorized modes with urban

logistics

Non-motorized modes should be integrated with

the city logistics chain for the last mile delivery.

Some of the interventions that should be

considered are: restricting usage of non-

motorized modes on main arterial roads,

designated lanes for bicycles and cargo cycles,

novel initiatives like freight information portal to

also list available non-motorized modes,

incentivize last mile parcel delivery through non-

motorized modes by means of tax credits etc.

• Promotion of alternate technologies

Promotion of alternate technologies like electric and hybrid vehicles can help India reduce GHG emissions. India should aim to adopt a legislation to facilitate development and use of alternate technologies like electric/ hybrid trucks by means of tax breaks and subsidies.

ICT enablement

Large number of discrete solutions for have come up with the features like fleet tracking, route optimization, loading optimization, RFID tracking, packing efficiency enhancement etc. Creation of strategic plans for these technologies along with joint programs and supporting framework for information sharing can enable accelerated dissemination of these technologies. It is also important to build conducive regulatory environment for new technologies like drones. Indian regulators should designate test sites for drone testing and allow experimental licenses to drone developers. Designated test sites would not only enable regulators to maintain a check but also provide favorable environment for R&D spend.

24

India has a robust transport infrastructure comprising of 5.25 Million km of road network, 1,20,000 km of railway network, 7,500 km coastline with 13 Major Ports and 205 Minor Ports and 125 airports. Additionally, India has a network of 14,500 km of navigable inland waterways. However, Logistics Performance Index (LPI) – a ranking

published by World Bank to measure logistics performance of countries – ranks India at 35, primarily due to suboptimal modal mix and inefficient logistics operations. India not only lags the developed countries on the LPI ranking, but ranks low compared to other Asian countries as indicated below:

Introduction

Germany UK USA japan India

4.23 4.07 3.99 3.973.42

Figure 7: LPI score comparison between India and leading developed countries

Source: LPI Reports

Germany UK USA japan India

4.23 4.07 3.99 3.973.42

Figure 7: LPI score comparison between India and leading developed countries

Source: LPI Reports

26

27

India’s logistics cost as a % of its GDP stands at 13-14%, and the same has doubled over last 15 years. This is very high compared to the other developed countries,

pointing to the inherent inefficiencies in the freight movement in the country:

1. Capital costs include EMI and Depreciation costs

2. Fixed costs include Types and Vehicle Maintenance costs, Driver salaries, annual vehicle & third- party insurance, national permit, road tax and fitness certification fee

3. Operating costs Include fuel, toll and loading and unloading

4. Purchasing Power Party (PPP) 1 USD = INR 17

5. Other Include loading and unloading cost

Freight Cost Benchmarking

Freight cost(as a % of GDP)

13 - 14%

8 - 10% 9 - 10%

India US Other development

countriesFreight cost trend - India(as a % GDP)

Freight Cost Breakup

Freight cost comparison4

(INR/t-km, 20 MT Payload, PPP Basis

Variable3costs

Fixed operating

2costs

1Capital costs

India USA

Fuel Cost

Overheads

Capital costs7-8% 8-9%

10-11%13-14%

2000 2005 2010 2014

5Other

Toll tax

Fuel

Insurance permit, Tax

Maintenance

Salaries

7%

11%

34%

3%12%

15%

17%

28%

50%

22%

1.9

0.9

Figure 3: Freight cost benchmarking

Source: Secondary Research, ISID, TCIL – IIMC Study, Should-Cost model developed for Mumbai – Delhi route for a Full Truck Load

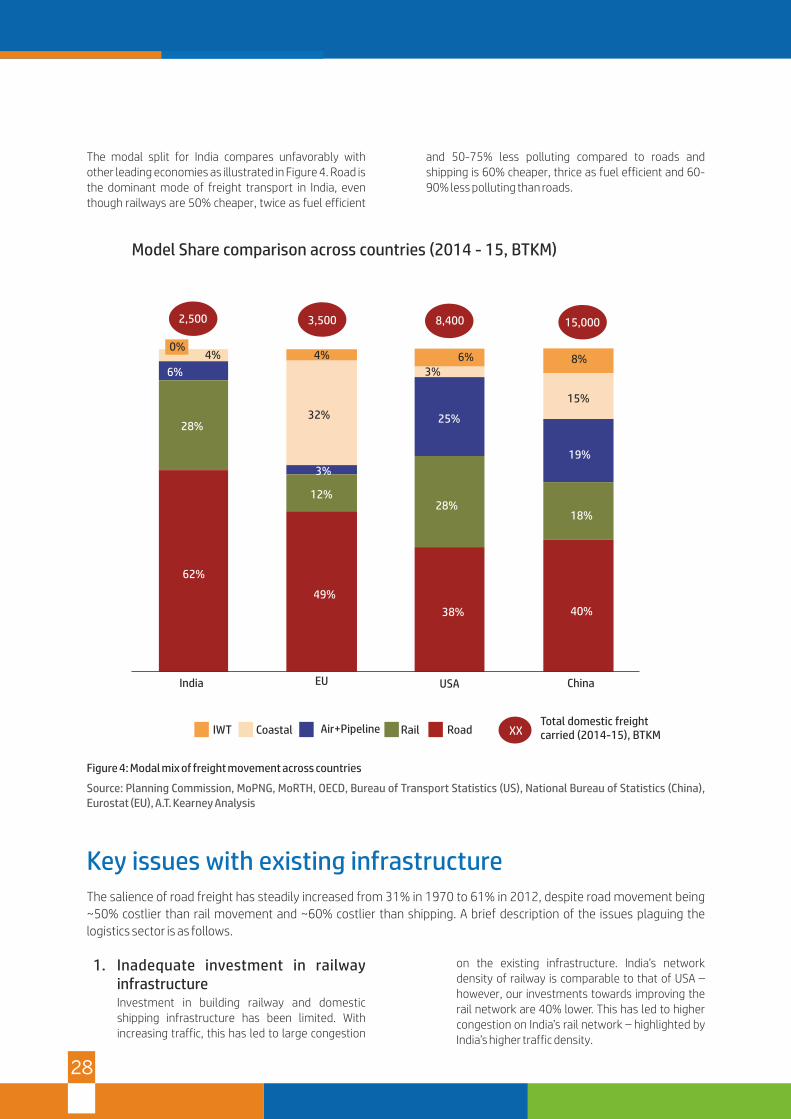

The modal split for India compares unfavorably with other leading economies as illustrated in Figure 4. Road is the dominant mode of freight transport in India, even though railways are 50% cheaper, twice as fuel efficient

and 50-75% less polluting compared to roads and shipping is 60% cheaper, thrice as fuel efficient and 60-90% less polluting than roads.

4%

6%

28%

62%

4%

32%

3%

12%

49%

6%3%

25%

28%

38%

8%

15%

19%

18%

40%

2,500 3,500 8,400 15,000

India EU USA China

XXTotal domestic freightcarried (2014-15), BTKMIWT Coastal Air+Pipeline RoadRail

0%

Model Share comparison across countries (2014 - 15, BTKM)

Figure 4: Modal mix of freight movement across countries

Source: Planning Commission, MoPNG, MoRTH, OECD, Bureau of Transport Statistics (US), National Bureau of Statistics (China), Eurostat (EU), A.T. Kearney Analysis

Key issues with existing infrastructureThe salience of road freight has steadily increased from 31% in 1970 to 61% in 2012, despite road movement being

~50% costlier than rail movement and ~60% costlier than shipping. A brief description of the issues plaguing the

logistics sector is as follows.

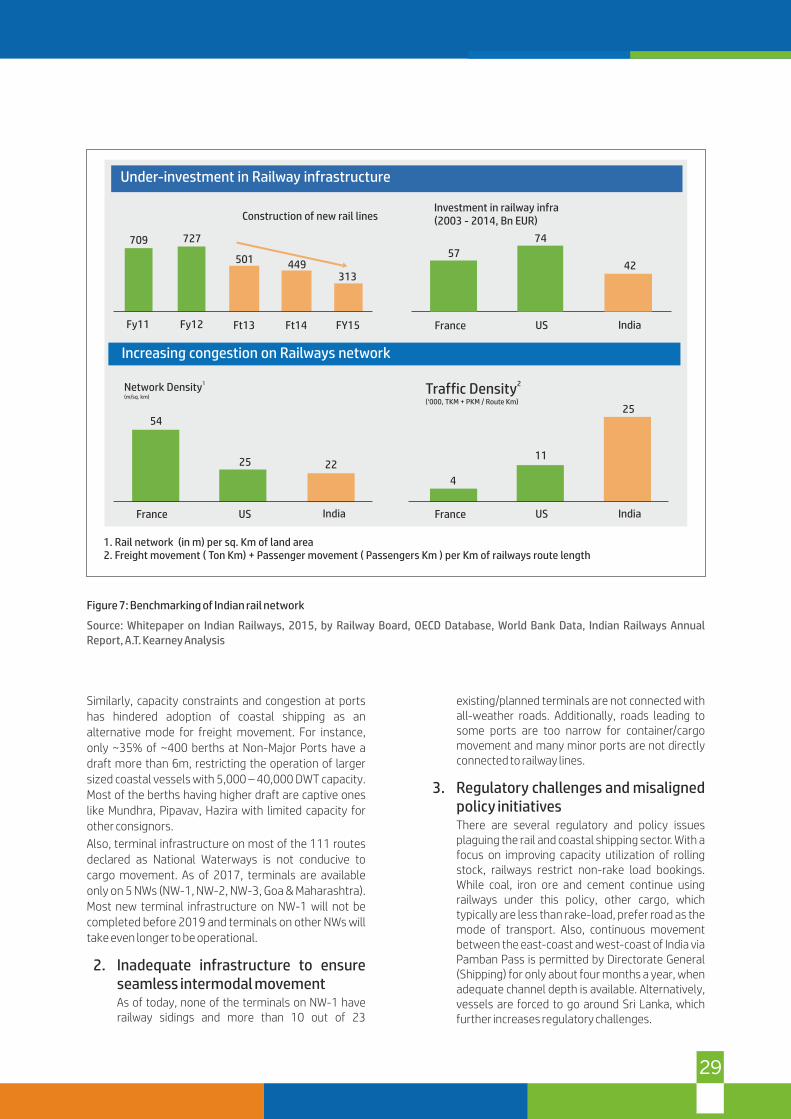

1. Inadequate investment in railway infrastructureInvestment in building railway and domestic shipping infrastructure has been limited. With increasing traffic, this has led to large congestion

on the existing infrastructure. India’s network density of railway is comparable to that of USA – however, our investments towards improving the rail network are 40% lower. This has led to higher congestion on India’s rail network – highlighted by India’s higher traffic density.

28

29

1. Rail network (in m) per sq. Km of land area2. Freight movement ( Ton Km) + Passenger movement ( Passengers Km ) per Km of railways route length

Construction of new rail lines

709 727

501 449313

Fy11 Fy12 Ft13 Ft14 FY15

France US India

54

25 22

2Traffic Density(‘000, TKM + PKM / Route Km)

4

11

25

57

74

42

1Network Density(m/sq. km)

France US India

France US India

Investment in railway infra(2003 - 2014, Bn EUR)

Under-investment in Railway infrastructure

Increasing congestion on Railways network

Similarly, capacity constraints and congestion at ports has hindered adoption of coastal shipping as an alternative mode for freight movement. For instance, only ~35% of ~400 berths at Non-Major Ports have a draft more than 6m, restricting the operation of larger sized coastal vessels with 5,000 – 40,000 DWT capacity. Most of the berths having higher draft are captive ones like Mundhra, Pipavav, Hazira with limited capacity for other consignors.

Also, terminal infrastructure on most of the 111 routes declared as National Waterways is not conducive to cargo movement. As of 2017, terminals are available only on 5 NWs (NW-1, NW-2, NW-3, Goa & Maharashtra). Most new terminal infrastructure on NW-1 will not be completed before 2019 and terminals on other NWs will take even longer to be operational.

2. Inadequate infrastructure to ensure seamless intermodal movementAs of today, none of the terminals on NW-1 have railway sidings and more than 10 out of 23

Figure 7: Benchmarking of Indian rail network

Source: Whitepaper on Indian Railways, 2015, by Railway Board, OECD Database, World Bank Data, Indian Railways Annual Report, A.T. Kearney Analysis

existing/planned terminals are not connected with all-weather roads. Additionally, roads leading to some ports are too narrow for container/cargo movement and many minor ports are not directly connected to railway lines.

3. Regulatory challenges and misaligned policy initiatives There are several regulatory and policy issues plaguing the rail and coastal shipping sector. With a focus on improving capacity utilization of rolling stock, railways restrict non-rake load bookings. While coal, iron ore and cement continue using railways under this policy, other cargo, which typically are less than rake-load, prefer road as the mode of transport. Also, continuous movement between the east-coast and west-coast of India via Pamban Pass is permitted by Directorate General (Shipping) for only about four months a year, when adequate channel depth is available. Alternatively, vessels are forced to go around Sri Lanka, which further increases regulatory challenges.

30

4. Lack of integrated planningWhile the pace of highway construction in the country has gone up in the past few years, the planning for highway upgradation in the country has been ad-hoc and driven primarily by local considerations, with limited focus on large-scale network planning. Corridor approach to road development is in nascent stage in India, with most of the development happening on individual stretches, with limited emphasis on maintaining uniform infrastructure between the origin and the destination of the corridor.

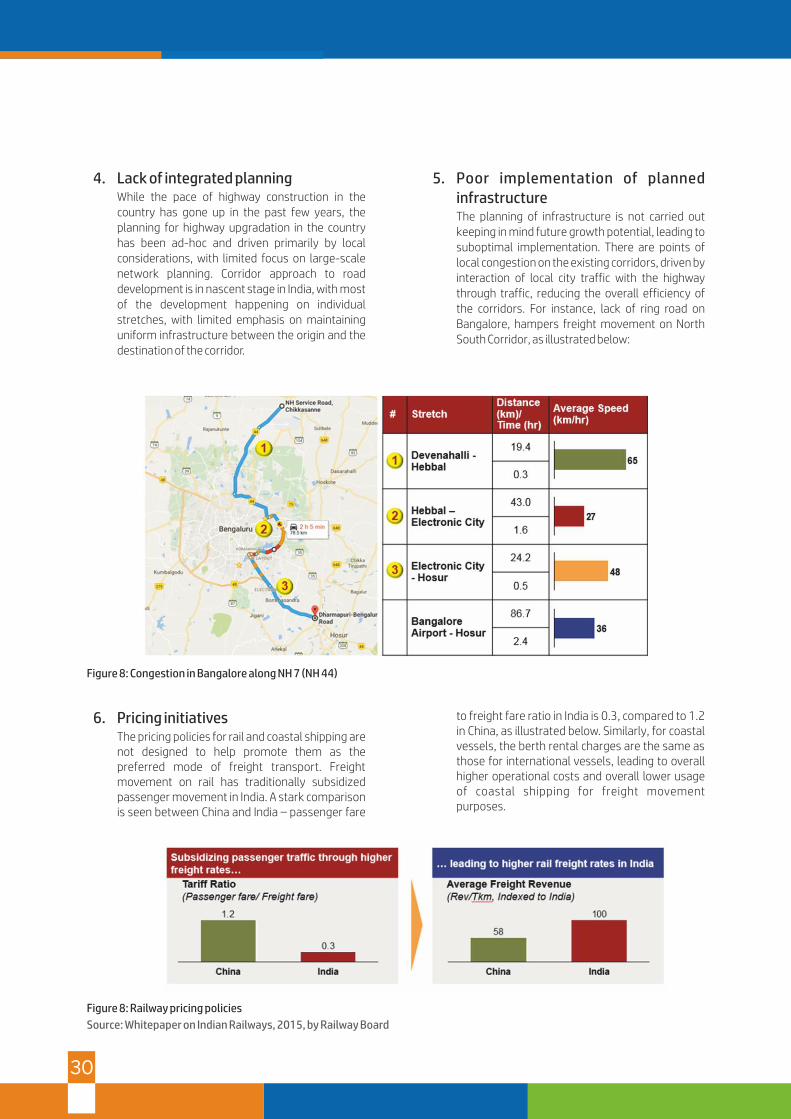

5. Poor implementation of planned infrastructureThe planning of infrastructure is not carried out keeping in mind future growth potential, leading to suboptimal implementation. There are points of local congestion on the existing corridors, driven by interaction of local city traffic with the highway through traffic, reducing the overall efficiency of the corridors. For instance, lack of ring road on Bangalore, hampers freight movement on North South Corridor, as illustrated below:

6. Pricing initiativesThe pricing policies for rail and coastal shipping are not designed to help promote them as the preferred mode of freight transport. Freight movement on rail has traditionally subsidized passenger movement in India. A stark comparison is seen between China and India – passenger fare

Figure 8: Congestion in Bangalore along NH 7 (NH 44)

to freight fare ratio in India is 0.3, compared to 1.2 in China, as illustrated below. Similarly, for coastal vessels, the berth rental charges are the same as those for international vessels, leading to overall higher operational costs and overall lower usage of coastal shipping for freight movement purposes.

Figure 8: Railway pricing policies

Source: Whitepaper on Indian Railways, 2015, by Railway Board

31

There are multiple global examples of successful

implementation of development of road and rail

corridors. Developed economies have also focused on

developing infrastructure to enable shifting of freight

from congested roads onto rail, coastal shipping and

inland waterways. A successful example is the core

network of corridors aimed at providing multi modal

connectivity throughout EU. The following are some of

the network corridors identified:

1. The Rhine-Alpine Corridor is one of the busiest

freight routes in Europe. The corridor connects the

North Sea ports at Rotterdam and Antwerp to the

Mediterranean basin.

2. The Atlantic Corridor links the Western region of

the Iberian Peninsula to Paris and further to

Mannheim with rail lines (conventional and high

speed). This corridor also includes the Seine as an

inland waterway.

3. The Mediterranean Corridor links the Iberian

Peninsula with the Hungary-Ukraine border

region. The 3,000 kilometer corridor provides

multimodal connectivity to the ports of western

Mediterranean region with the Centre of the

European Union.

4. The North Sea-Baltic Corridor – connects the ports

of eastern end of Baltic Sea with the Northern Sea

ports. The corridor provides road and rail transport

links between the Baltic states and Poland,

Germany, Netherlands, Belgium. This corridor also

includes inland waterways. The most important

Global examples of multi-modal corridor developmentproject in this corridor is “Rail Baltic”, which

provides rail connectivity between regions of

Tallinn, Riga, Kaunas and Poland.

5. The North Sea-Mediterranean Corridor stretches

from Ireland to the Mediterranean Sea in southern

France. The multimodal corridor includes inland

waterways in Benelux and France, providing

multimodal connectivity from North Sea ports to

Maas, Rhine, Seine etc.

Countries in Eastern Africa have majorly invested in

development of transportation corridors to facilitate

economic liberalization and trade. The Northern Corridor

is a transport corridor linking the capital cities of Burundi,

Rwanda, Uganda and Kenya with the port of Mombasa in

Kenya. The corridor is a multi-modal corridor integrating

road, rail, inland waterways and pipeline transport.

Following key best practices and lessons emerge from

the assessment of global examples

• Ensure simultaneous development of consistent

infrastructure along the corridor

• Different modes of freight movement should

complement each other instead of competing for

cargo - Allied infrastructure and intermodal

connectivity is essential to improve the overall

efficiency of the corridor

• Most optimum mode of project execution needs to

be finalized based on the economic attractiveness

of different stretches of corridors and market

constraints.

A scientific approach with focus on connecting centers of

economic importance in the most efficient way is needed

to identify and prioritize the next wave of development in

the country. This will enable improvement in the logistics

efficiency of the country through a reduction. In addition,

an integrated multimodal development approach is

essential to ensure a consistent congestion free

carriageway infrastructure along key corridors. Specific

measures need to be taken for each mode to ensure

best-in-class practices are adhered to. However, at the

same time, it is important to ensure there is alignment

on the development plan among different public and

private agencies, to ensure seamless multimodal

connectivity. For this, a central authority for managing

Connectivity Enhancement – Need for Holistic Network Development

the overall infrastructure and facilities is ideal. The

central authority must ensure coordinated planning

across different modes and presence of intermodal

connectivity for seamless movement of freight

throughout the country.

Apart from the measures for ensuring coordination and

complementarity between different modes, including

the development of multimodal logistics parks in key

locations and intermodal connectivity, specific measures

are being taken to improve the state of individual modes

as discussed below.

To improve the road network in the country, a

comprehensive network of corridors and associated

32

feeder routes need to be planned to connect the key

economic centers in the country, to augment the existing

network. A network of 50 corridors along with 175

feeder routes to this network is needed to carry ~70% of

the total national inter district road freight movement in

the country. In addition, a network of such a magnitude is

needed to provide good quality road connectivity to

more than 75% districts.

A summary of the overall network needed to improve

road connectivity is highlighted below:

Table 1: Economic Corridors and Feeder Routes – Profile

In addition to developing new corridors, inter corridor

routes and feeder routes, there is a need to improve the

efficiency of existing and proposed corridors, to ensure a

seamless, well-connected India aiding freight

movement. There are multiple localized congestion

points on the corridors hampering the traffic movement

and thereby reducing the overall efficiency of the

corridor. The right intervention needed to eliminate

congestion and improve corridor efficiency would

depend on the root cause driving the congestion in

these points. Potential interventions could vary from

improving the quality of existing roads to developing

additional carrying capacity through construction

of bypasses, elevated corridors, flyovers, lane

expansion, etc.

Similarly, various interventions are needed to improve

rail freight movement in India, foremost being the

rationalization of rail freight charges. According to a

study on rail freight analysis, revenue maximization for

an average distance of 1,100 kilo-meter is achieved at

INR 15 per TEU per km, a reduction of approximately

33% from the prevailing rates of INR 20 - 22 per TEU per

km. This potential rationalization in freight charges could

be compensated by the premium that could be charged

on dedicated freight corridors. In addition, measures to

increase the priority for freight trains on railways

network need to be explored. Also, an integrated pricing

from the origin to destination covering the road freight

movement on the first and last mile needs to be

explored. For an integrated multi modal transport,