Public Hearings on Local Public Procurement Presentation

Overview of Smith Capital background, capability & VALUE PROPOSITION

Company overview

Value Proposition

We have been in business since 1973 and now a level 2 majority BWO BBBEE company with Proudly SouthAfrican accreditation since November 2015. We have been identified as one of the 100 Black Industrialist by theDepartment of Trade and Industry and recently been invited to showcase our products and solutions to the SouthAfrican Parliament.

After Sales service and maintenance.SCE is a registered LME, No 246, and we employ five LMIs rated for work on MEWPs, more than any other entityin RSA. Between them our LMIs have over 90 years of experience on every type of Truck mounted elevating workplatform. Behind this front row of hands-on expertise stands a company which designs and produces MEWPs tointernational standards, with all the technical skills and experience this necessitates.

We are the only company in South Africa rated to service the most high tech and biggest MEWPs – all those in the 60 – 70 m working height range as well as conventional Municipal units.

We maintain an adequate level of spares needed for product support.

Smith Capital Equipment Value Proposition

Shareholding

Smith Capital Equipment BBBEE Structure post acquisition

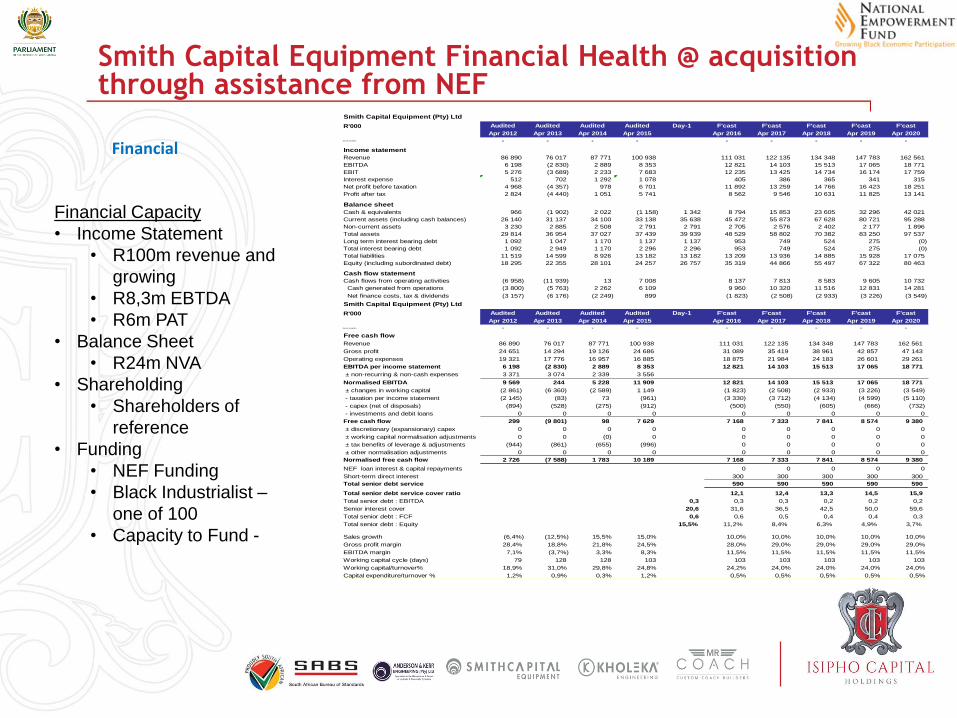

Financial

Financial Capacity

• Income Statement

• R100m revenue and

growing

• R8,3m EBTDA

• R6m PAT

• Balance Sheet

• R24m NVA

• Shareholding

• Shareholders of

reference

• Funding

• NEF Funding

• Black Industrialist –

one of 100

• Capacity to Fund -

Smith Capital Equipment (Pty) Ltd

R'000 Audited Audited Audited Audited Day-1 F'cast F'cast F'cast F'cast F'cast

Apr 2012 Apr 2013 Apr 2014 Apr 2015 Apr 2016 Apr 2017 Apr 2018 Apr 2019 Apr 2020No of months 12 12 12 12 12 12 12 12 12

Income statement

Revenue 86 890 76 017 87 771 100 938 111 031 122 135 134 348 147 783 162 561

EBITDA 6 198 (2 830) 2 889 8 353 12 821 14 103 15 513 17 065 18 771

EBIT 5 276 (3 689) 2 233 7 683 12 235 13 425 14 734 16 174 17 759

Interest expense 512 702 1 292 1 078 405 386 365 341 315

Net profit before taxation 4 968 (4 357) 978 6 701 11 892 13 259 14 766 16 423 18 251

Profit after tax 2 824 (4 440) 1 051 5 741 8 562 9 546 10 631 11 825 13 141

Balance sheet

Cash & equivalents 966 (1 902) 2 022 (1 158) 1 342 8 794 15 853 23 605 32 296 42 021

Current assets (including cash balances) 26 140 31 137 34 100 33 138 35 638 45 472 55 873 67 628 80 721 95 288

Non-current assets 3 230 2 885 2 508 2 791 2 791 2 705 2 576 2 402 2 177 1 896

Total assets 29 814 36 954 37 027 37 439 39 939 48 529 58 802 70 382 83 250 97 537

Long term interest bearing debt 1 092 1 047 1 170 1 137 1 137 953 749 524 275 (0)

Total interest bearing debt 1 092 2 949 1 170 2 296 2 296 953 749 524 275 (0)

Total liabilities 11 519 14 599 8 926 13 182 13 182 13 209 13 936 14 885 15 928 17 075

Equity (including subordinated debt) 18 295 22 355 28 101 24 257 26 757 35 319 44 866 55 497 67 322 80 463

Cash flow statement

Cash flows from operating activities (6 958) (11 939) 13 7 008 8 137 7 813 8 583 9 605 10 732

Cash generated from operations (3 800) (5 763) 2 262 6 109 9 960 10 320 11 516 12 831 14 281

Net finance costs, tax & dividends (3 157) (6 176) (2 249) 899 (1 823) (2 508) (2 933) (3 226) (3 549)

Smith Capital Equipment (Pty) Ltd

R'000 Audited Audited Audited Audited Day-1 F'cast F'cast F'cast F'cast F'cast

Apr 2012 Apr 2013 Apr 2014 Apr 2015 Apr 2016 Apr 2017 Apr 2018 Apr 2019 Apr 2020No of months 12 12 12 12 12 12 12 12 12

Free cash flow

Revenue 86 890 76 017 87 771 100 938 111 031 122 135 134 348 147 783 162 561

Gross profit 24 651 14 294 19 126 24 686 31 089 35 419 38 961 42 857 47 143

Operating expenses 19 321 17 776 16 957 16 885 18 875 21 984 24 183 26 601 29 261

EBITDA per income statement 6 198 (2 830) 2 889 8 353 12 821 14 103 15 513 17 065 18 771

± non-recurring & non-cash expenses 3 371 3 074 2 339 3 556

Normalised EBITDA 9 569 244 5 228 11 909 12 821 14 103 15 513 17 065 18 771

± changes in working capital (2 861) (6 360) (2 589) 1 149 (1 823) (2 508) (2 933) (3 226) (3 549)

- taxation per income statement (2 145) (83) 73 (961) (3 330) (3 712) (4 134) (4 599) (5 110)

- capex (net of disposals) (894) (528) (275) (912) (500) (550) (605) (666) (732)

- investments and debit loans 0 0 0 0 0 0 0 0 0

Free cash flow 299 (9 801) 98 7 629 7 168 7 333 7 841 8 574 9 380

± discretionary (expansionary) capex 0 0 0 0 0 0 0 0 0

± working capital normalisation adjustments 0 0 (0) 0 0 0 0 0 0

± tax benefits of leverage & adjustments (944) (861) (655) (996) 0 0 0 0 0

± other normalisation adjustments 0 0 0 0 0 0 0 0 0

Normalised free cash flow 2 726 (7 588) 1 783 10 189 7 168 7 333 7 841 8 574 9 380

NEF loan interest & capital repayments 0 0 0 0 0

Short-term direct interest 300 300 300 300 300

Total senior debt service 590 590 590 590 590

Total senior debt service cover ratio 12,1 12,4 13,3 14,5 15,9

Total senior debt : EBITDA 0,3 0,3 0,3 0,2 0,2 0,2

Senior interest cover 20,6 31,6 36,5 42,5 50,0 59,6

Total senior debt : FCF 0,6 0,6 0,5 0,4 0,4 0,3

Total senior debt : Equity 15,5% 11,2% 8,4% 6,3% 4,9% 3,7%

Sales growth (6,4%) (12,5%) 15,5% 15,0% 10,0% 10,0% 10,0% 10,0% 10,0%

Gross profit margin 28,4% 18,8% 21,8% 24,5% 28,0% 29,0% 29,0% 29,0% 29,0%

EBITDA margin 7,1% (3,7%) 3,3% 8,3% 11,5% 11,5% 11,5% 11,5% 11,5%

Working capital cycle (days) 79 128 128 103 103 103 103 103 103

Working capital/turnover% 18,9% 31,0% 29,8% 24,8% 24,2% 24,0% 24,0% 24,0% 24,0%

Capital expenditure/turnover % 1,2% 0,9% 0,3% 1,2% 0,5% 0,5% 0,5% 0,5% 0,5%

Smith Capital Equipment Financial Health @ acquisition through assistance from NEF

Our history and main customers:

◦ Ekurhuleni

◦ Have won the back to back contracts for the 3 successive contracts and have 72 units deployed – all locally designed, manufactured and supported products – 58 of SL 125; 11 of 9,2 SSL; and 3 of 18,5 SS Superlift Products.

◦ Eskom

◦ Are the incumbent 5 year contract provider for Aerial Platforms, Drilling Rigs and Truck Mounted Cranes. Have supplied and are maintaining over 500 units currently in their fleet.

◦ Working with Eskom to provide Rental Solutions, Emerging Contractor Funding and Live Line maintenance and Tools.

◦ eThekwini Municipality

◦ Won the last 2 contracts on the supply of Oil and Steel Cherry Pickers and currently have deployed and maintaining 27 of such from the Smith Capital KZN Regional Office.

◦ Tshwane

◦ Have deployed and maintaining 47 Oil and Steel Cherry Pickers and currently awaiting the new contract award through Fleetmatics.

◦ Mogale City

◦ Have deployed and maintaining 17 of the locally manufactured products through Aqua Transport

◦ Africa

◦ Currently pursuing an aggressive African strategy and have deployed several Aerial Platforms and Drilling Rigs

◦ Potential

◦ Transnet, COJ, City of Cape Town, Prasa, AFRICA

Smith Capital Equipment current customer mix

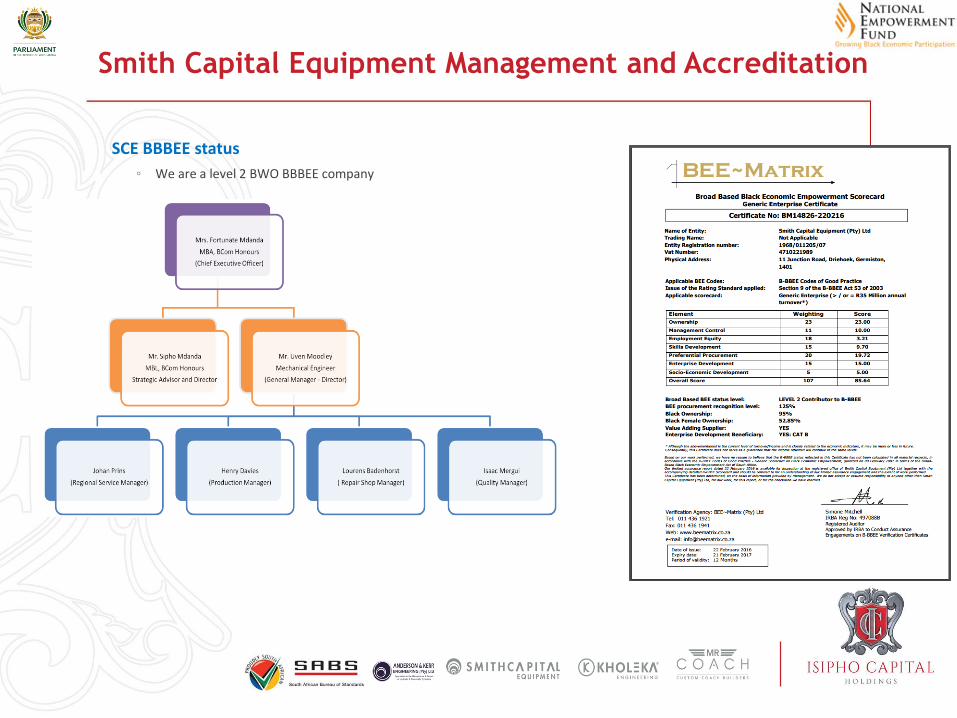

SCE BBBEE status

◦ We are a level 2 BWO BBBEE company

Smith Capital Equipment Management and Accreditation

ISO 9001 : 2008

◦ We are ISO 9001 registered

Smith Capital Equipment Accreditation

Smith Capital Equipment Accreditation

• Lifting Machinery Entity CredentialsThe only majority BWO BBBEE entity with LME

Accreditation. We employ the largest number of

Lifting Machinery Inspectors (LMI’s) by a single

Company and are in the process of accrediting

5 Black LMI’s – submissions already made to the

Institute of Engineering.

Smith Capital Equipment accreditation

Department of Labour Accredited The only majority BWO BBBEE company with the

certification and in the process of including Forklifts and

Reach Stackers and gantry crane

◦ Aerial Platforms

◦ Locally produced Non-insulated (Superlift) –Proudly South African

◦ Locally produced Insulated (Superlift) – Proudly South African

◦ Imported Non-insulated (CTE)

◦ Imported Insulated (Terex Utilities)

◦ Imported Insulated (Bronto Skylift)

◦ Drilling Rigs

◦ Locally produced Pole planter rigs (Hotline) – Proudly South African

◦ Locally produced Exploration rigs (Hotline) – Proudly South African

◦ Locally produced Water well rigs (Hotline) – Proudly South African

◦ Imported Pole planter rigs (Terex Digger Derricks)

◦ Cranes

◦ Imported truck mounted cranes (Effer Cranes)

◦ Imported Marine Cranes (Effer)

◦ Other Products

◦ Kubota Tractors

◦ Forklifts

◦ Reach Stackers

◦ Terminal Tractors

◦ Rail Road Vehicles

◦ Live Line Divisio

Smith Capital Equipment Product Mix

Aerial Platforms (Local)

◦ Locally produced Non-insulated (Superlift)

◦ Locally produced Insulated (Superlift)

Smith Capital Equipment locally produced Aerial Platforms

Drilling Rigs (Local)

◦ Locally produced Pole planter rigs (Hotline)

◦ Locally produced Exploration rigs (Hotline)

◦ Locally produced Water well rigs (Hotline)

Smith Capital Equipment Drilling Rigs

Drilling Rigs (Local Truck and Trailer Mounted Drilling Rigs)

◦ Locally produced Water well rigs (Hotline)

Smith Capital Equipment Drilling rigs variations

Effer Cranes

◦ Imported truck mounted cranes and

◦ Marine Cranes

Smith Capital Equipment Imported Cranes

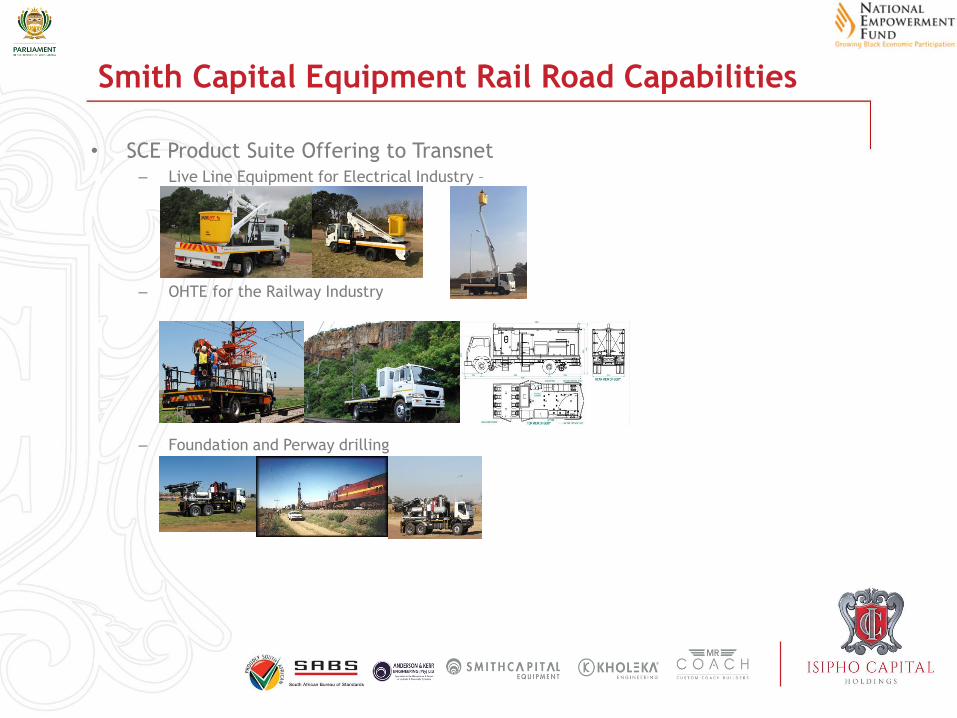

Smith Capital Equipment Rail Road Capabilities

• SCE Product Suite Offering to Transnet– Live Line Equipment for Electrical Industry –

– OHTE for the Railway Industry

– Foundation and Perway drilling

Live Line Division

◦ New division post acquisition

Smith Capital Equipment Live Line Division

Rental Division

◦ Capacitating Emerging Contractors

◦ Removing barriers

Smith Capital Equipment supporting emerging entrepreurs

Our stores

◦ We hold breakdown spares and parts for our equipment

Smith Capital Equipment stores and product support capabilities – R20m inventory

Production Capacity

Our factory capacity for mounting of Aerial devices with their sub-frames and bodywork, electrics and hydraulics, is very large, allowing us to handle volume orders expeditiously. No order so far has proved too large for us. We are an accredited body builder and recommend that we do the whole job. Our long experience includes too many bad examples of split sub-contracts when we have executed only part of the work, leading to errors and incompatibilities, double work, frustrating delays, excessive vehicle transportation between companies and excess axle loads. We can and prefer to do the whole job: just give us the chassis cabs, everything fits as it should and we deliver the finished product!

Smith Capital Equipment production capabilities

ISIPHO CAPITAL MATERIALS HANDLING DIVISION

FORKLIFTS; REACH STACKERS, TERMINAL TRACTORS

AND STACKER RECLAIMERS

SPECIALIZING ON IMPORTING, INSTALLATION,

COMMISSIONING AND REPAIRS TO MHE

Isipho Capital Holding - Materials Handling Division

• Kalmar– Isipho Capital Holdings has partnered with Kalmar who are the current supplier of about 750

units within the South African boarders

– Kalmar will be responsible for the design, supply and maintenance of all machines suppliedto customers

– Kalmar will look at sourcing parts and spares to Isipho Capital Group companies as well astraining these companies in the maintenance of the equipment – transfer of skill andexpertise. This will include the servicing of the current fleet already deployed and ownedby Transnet.

• Product Line

DRT450 REACH STACKER DCF150 /250 -12 FORKLIFT T12 TERMINAL TRACTOR

AGRICULTURAL SOLUTIONS

Smith Capital Equipment value added solutions

Kholeka Engineering (Pty) Ltd

• Head Quartered in KZN with Regional Office in JHB, Polokwane, PE and CT.

• Registered MIB for truck bodies, trailers and specialized terminal trailers.

• Level 1 BBBEE Majority Women Owned and operated business.

• Approved Isuzu Trucks South Africa Body Builder and only BEE that has

Transnet drawings having produced and delivered more than 60 specialized

truck bodies this financial year.

Kholeka Engineering product mix

Mr Coach (Pty) Ltd

• Mr Coach– Head Quartered in KZN with Regional Office in Johannesburg and Polokwane

– Registered MIB for converter of buses, taxis, ambulances, panel van and mobile clinics

– Level 2 BBBEE Majority Black Women Owned and operated business

– Approved Isuzu Convertor for the people transporter 24 seaters and 40 seater buses

and mini buses

Isipho Capital Localization Opportunities

Anderson and Kerr – strategic vertical integration

• Isipho capital acquiring 90% of shares in Anderson and Kerr Engineering.

• This positions Isipho through Anderson to do localization on cylinders, supply

Smith Capital and Kholeka and engineering solutions with the MHE OEM’s –

Komatsu, Kalmar and Manitou.

• It further positions Isipho as a strategic supplier of hydraulic and pneumatic

cylinders to Transnet, Eskom, Prasa, Municipalities in the future.

• Isipho would also collaborate with Transnet School of Engineering in providing

job creation opportunities for students who have passed and looking for

placement.

Financial Health thus capacity to deliver

• Financial Capability– Income Statement

• R80m revenue

• R19m EBITDA

– Balance Sheet• R65m NAV

– Shareholding• Shareholder of reference

– Funding• IDC

Anderson and Kerr (Pty) Ltd

R'000 Audited Audited Audited Audited Day-1 F'cast F'cast F'cast F'cast F'cast

Feb 2013 Feb 2014 Feb 2015 Feb 2016 Feb 2017 Feb 2018 Feb 2019 Feb 2020 Feb 2021No of months 12 12 12 12 12 12 12 12 12

Income statement

Revenue 91 521 100 905 70 622 80 229 85 000 100 000 106 000 112 360 119 102

EBITDA 23 957 30 622 14 081 19 107 20 054 25 336 26 857 28 468 30 176

EBIT 22 113 28 340 11 902 16 940 16 699 21 928 23 390 24 941 26 585

Interest expense 167 187 198 240 7 269 5 974 4 522 2 895 1 070

Net profit before taxation 23 909 30 402 14 809 19 950 11 073 17 426 20 385 23 655 27 235

Profit after tax 14 308 21 858 10 644 14 310 7 973 12 547 14 677 17 032 19 609

Balance sheet

Cash & equivalents 33 481 41 650 55 465 62 573 62 573 56 092 57 787 61 296 65 529 70 510

Current assets (including cash balances) 50 514 55 477 66 821 74 912 74 912 80 078 85 339 90 501 96 486 103 325

Non-current assets 18 514 20 297 18 945 18 845 18 845 15 790 12 700 9 571 6 401 3 189

Total assets 88 220 99 769 106 829 110 212 178 212 180 324 182 494 184 527 187 342 190 969

Long term interest bearing debt 0 0 0 0 68 000 57 323 45 351 31 928 16 876 0

Total interest bearing debt 0 0 0 0 68 000 57 323 45 351 31 928 16 876 0

Total liabilities 11 546 8 033 7 920 8 525 76 525 70 664 60 287 47 643 33 427 17 444

Equity (including subordinated debt) 76 668 91 736 98 909 101 688 101 688 109 660 122 207 136 884 153 916 173 525

Cash flow statement

Cash flows from operating activities (9 852) 23 832 15 181 16 099 4 497 13 985 17 269 19 642 22 236

Cash generated from operations (15 655) 26 078 12 128 16 342 11 646 16 400 18 350 20 788 23 451

Net finance costs, tax & dividends 5 802 (2 246) 3 052 (243) (7 149) (2 416) (1 081) (1 146) (1 215)

Cash flows from investing activities (6 339) (8 873) 2 123 2 540 (300) (318) (337) (357) (379)

Purchase of PPE (net of disposals) (5 238) (4 071) (827) (2 067) (300) (318) (337) (357) (379)

Investments & acquisitions (1 101) (4 802) 2 949 4 607 0 0 0 0 0

Cash flows from financing activities 37 872 (6 790) (3 470) (11 531) (10 677) (11 972) (13 424) (15 051) (16 876)

Interest bearing debt raised/(repaid) 0 0 0 0 (10 677) (11 972) (13 424) (15 051) (16 876)

Other capital raised/(repaid) 37 872 (6 790) (3 470) (11 531) 0 0 0 0 0

Miscellaneous cash flows (99) 0 (18) 0 0 0 0 0 0

Anderson and Kerr (Pty) Ltd

R'000 Audited Audited Audited Audited Day-1 F'cast F'cast F'cast F'cast F'cast

Feb 2013 Feb 2014 Feb 2015 Feb 2016 Feb 2017 Feb 2018 Feb 2019 Feb 2020 Feb 2021No of months 12 12 12 12 12 12 12 12 12

Free cash flow

Revenue 91 521 100 905 70 622 80 229 85 000 100 000 106 000 112 360 119 102

Gross profit 34 862 40 911 29 877 32 271 34 000 42 000 44 520 47 191 50 023

Operating expenses 12 374 12 977 16 803 15 243 16 150 19 000 20 140 21 348 22 629

EBITDA per income statement 23 957 30 622 14 081 19 107 20 054 25 336 26 857 28 468 30 176

± non-recurring & non-cash expenses 0 0 2 339 1 718

Normalised EBITDA 23 957 30 622 16 420 20 825 20 054 25 336 26 857 28 468 30 176

± changes in working capital 5 802 (2 246) 3 052 (243) (7 149) (2 416) (1 081) (1 146) (1 215)

- taxation per income statement (9 601) (8 544) (4 166) (5 641) (3 100) (4 879) (5 708) (6 623) (7 626)

- capex (net of disposals) (5 238) (4 071) (827) (2 067) (300) (318) (337) (357) (379)

- investments and debit loans 0 0 0 0 0 0 0 0 0

Free cash flow 14 920 15 760 12 141 11 156 9 504 17 724 19 731 20 341 20 957

± discretionary (expansionary) capex 0 0 0 0 0 0 0 0 0

± working capital normalisation adjustments 0 0 0 0 0 0 0 0 0

± tax benefits of leverage & adjustments 673 673 18 192 0 0 0 0 0

± other normalisation adjustments 0 0 0 0 0 0 0 0 0

Normalised free cash flow 15 593 16 433 14 499 13 066 9 504 17 724 19 731 20 341 20 957

Ithala Dev loan interest & capital repayments 17 946 17 946 17 946 17 946 17 946

Short-term direct interest 0 0 0 0 0

Total senior debt service 17 946 17 946 17 946 17 946 17 946

Total senior debt service cover ratio 0,5 1,0 1,1 1,1 1,2

Total senior debt : EBITDA 3,4 2,9 1,8 1,2 0,6 0,0

Senior interest cover 2,6 2,8 4,2 5,9 9,8 28,2

Total senior debt : FCF 7,2 6,0 2,6 1,6 0,8 0,0

Total senior debt : Equity 66,9% 52,3% 37,1% 23,3% 11,0% 0,0%

Sales growth 18,4% 10,3% (30,0%) 13,6% 5,9% 17,6% 6,0% 6,0% 6,0%

Gross profit margin 38,1% 40,5% 42,3% 40,2% 40,0% 42,0% 42,0% 42,0% 42,0%

EBITDA margin 26,2% 30,3% 19,9% 23,8% 23,6% 25,3% 25,3% 25,3% 25,3%

Working capital cycle (days) 28 43 42 38 92 92 92 92 92

Working capital/turnover% 9,9% 11,2% 11,6% 10,5% 18,4% 18,0% 18,0% 18,0% 18,0%

Capital expenditure/turnover % 5,9% 4,0% 1,2% 2,6% 0,4% 0,3% 0,3% 0,3% 0,3%

ISIPHO CAPITAL ONSITE MAINTENANCE PRESENTATION

COLLABORATION BETWEEN ISIPHO CAPITAL HOLDINGS ANDISUZU TRUCKS SOUTH AFRICA (ITSA) TO UNLOCK VALUE TOCLIENTS IN THE SERVICE AND REPAIRS TO ISUZU CHASSISDELIVERED AS PART OF THE FULL MAINTENANCE LEASE,SALE AND LEASEBACK AND MANAGED MAINTENACE

• Isipho Capital Holdings (Pty) Ltd through its fleet division – Isipho Capital Fleet, has negotiated with IsuzuTruck South Africa to be an accredited as a Fleet Operator Service Agent thus signing the Fleet OperatorService Agreement. This will see Isipho and group companies to be the only majority African Black WomenOwned Group companies to offer dedicated Service and Maintenance of Isuzu chassis. This competitiveadvantage will bear serious fruits to customers in that it will ensure uptime, allow for SD&D in a big wayand most importantly it’s a way ITSA is contributing to SD&L as an OEM.

• Our collaboration will see us delivering unparalleled service to in the form of ON-SITE MAINTENANCE to allthe ISUZU chassis at Smith Capital, Kholeka Engineering and dedicated On Site Maintenance on strategiclocations to be discussed with Customers to all chassis that:– Will be supplied by Isipho Capital as part of this lease contract,

– Currently supplied to customers by previous FML companies (based on the sale and leaseback), and

– Currently owned by Customers and sitting in their balance sheet.

• This collaboration will go a long way in ensuring:– Improving turnaround times by ensuring chassis availability.

– Improving turnaround times by ensuring one stop solution for Chassis and Upperworks (crane, Aerial Platform,truck body) repairs at the same time and thus reducing machine downtime.

– Creating new competencies and employment opportunities.

– Leveraging on collective infrastructure and countrywide footprint as the ON-SITE WORKSHOP will be locatedat the optimal point where all related services could be absorbed either at Customer workshop, IsiphoCapital Group Companies workshop or ITSA franchised/merchants operations

– Leveraging on the experience curve that ITSA has accumulated on this concept and thus ease ofimplementation and deployment

– Ability to service the entire Customer business.

– Opportunity to employ new persons and thus drive new skill acquisition

– This creates an opportunity to partner with FET Colleges and the Automotive Clusters of which Isipho hasrelationships with.

Isipho Capital Holdings – On Site Maintenance Solutions

Isipho Capital Holdings Super Fleet Concept to Clients

ITSA

Client Identified Depots

FML (Full Maintenance Lease)

Sale and Leaseback

Maintenance labor service on

DEPOs

Isipho Staffed in collaboration with

ITSA

Parts Consignment Stock on site

(Isipho supply and Staffed)

Replenish Parts Stock on usage

and demand

Truck Supply

based on RT57 &

Transnet Spec

Merits to Transnet Off Balance Sheet (Vehicles and Parts)

Lighten cash flow burden

Much less downtime due to on-site maintenance

Focus on core-business by outsourcing non-core vehicle maintenance business

Either through Kholeka,

Smith Capital or

Appointed Agent

manufacture:

• Specialized

Truck Body

• Truck Mounted

Crane

• Specialized

Trailer

This is dependent on the number of

vehicles per region, and proximity of

region to either ITSA or Isipho Capital

Holdings facilities.

ISIPHO CAPITAL COLLABORATION WITH WESBANK

WITH A VIEW OF TRULY TRANSFORMING THE FINANCIAL SERVICESSECTOR – ISIPHO HAS A COLLABORATION WITH WESBANK TO PROVIDEFUNDING, FLEET SOLUTIONS, SALE & LEASEBACK, FML, STR ANDREVERSE LOGISTICS – GIVING MEANINGFUL TRANFER OF SKILLS ANDEXPERTISE AND ALLOWING FOR ENHANCED ONE STOP SOLUTIONS TOCUSTOMERS

• Transformation in the financial service industry is key and Isipho Capital

Holdings is in the forefront of this.

• Having gained the expertise whilst at FNB, Isipho is collaborating with Wesbank

to deliver a total Fleet Solutions to customers on the following:

– Fleet Card

– Sale and Leaseback

– Managed Maintenance

– Short Term Rental

– Reverse Logistics

– FUNDING

• This collaboration will go a long way in ensuring:

– New players in the financial services industry

– One stop solutions to customers (Funding, FML and OEM capabilities)

– Transfer of skill and expertise

Isipho Capital Holdings – Fleet Card, FML, MM, STR and Auctions

INTERVENTION SOUTH FROM THE PORTFOLIO

COMMITTEE

WE BELIEVE THAT OUR COMPANY HAS MADESERIOUS STRIDES WITH THE SUPPORT OF THE NEFBUT BELIEVE THAT THE FOLLOWING SUPPORT ISNEEDED IN TAKING US TO THE NEXT LEVEL

The traditional contracting model has limited benefits flowing through to black

owned companies hence limited development of a competitive local supplier

base

Mid-size Companies, small OEMs

Small Businesses

Large OEM/FML’s &

Multinationals

• Large OEMs have purchasing leverage hence it becomes a compliance exercise resulting in fronting, etc.

• Job creation • Skills development • Direct benefit

of large white

owned

companies

from contract

• Indirect

benefits of

black owned

companies

from contract

• Job creation • Skills development• Small business

promotion

• Rural integration

• SD guidelines through purchasing leverage

Purchasing flow Indirect impact

SOE’s, Government departments, Metros and Municipalities normally go out on

Tender using two main strategies for their fleet.

Direct Procurement

In this case the government departments buy the chassis and upper works (Cherry

Picker) and these sit in their Balance Sheets. Amongst the Metros (Ekurhuleni,

eThekwini and Cape Town) use this type procurement system. We want to

commend the City of Ekurhuleni as the only Metro that always buy locally

manufactured products from us and the competitors. eThekwini and City of Cape

Town have a huge fleet of imported products.

Government and SOE Procurement Systems

FML Procurement

In this procurement process, the Metros award a contract to a Full Maintenance Lease

(FML) company e.g. Bidvest, Eqstra, etc. Amongst the Metros using this system is City

of Johannesburg and Tshwane. In this case the contract is awarded to the FML

company who then procures Cherry Pickers from manufacturers and in this case these

use imported products and their procurement is not governed by the PFMA and PPPF

policies and do not even go out on a public tender but perform a non-transparent

procurement system but mainly buying from local agents importing foreign

products. We also do have imported products but given our experience, the locally

manufactured products are better than these and from a Total Cost of Ownership

concept, the locally manufactured products outweigh the imported products for the

following reasons:

• No forex exposure

• Predictability of supply

• Price stability

• Parts availability locally

• Machine availability is high

Government and SOE Procurement System

FML Procurement (Cont.)

• Manufactured in line with local conditions

• Allow for operator training

• Job creation directly and indirectly from a full value chain of local

suppliers perspective

• Local skills improvement and reliance on local skills

• Contribution toward the GDP

Government and SOE Procurement Systems

Designation of Locally Produced Cherry Pickers/Aerial Platforms

Post - acquisition of the company we engaged the Department of Trade

and Industry with a view of trying to designate the locally produced

Cherry Pickers. Smith Capital is one of two companies that locally

designs and manufactures Cherry Pickers. We compete with imported

products particularly from Europe and China. Our products meet all the

requirements including SABS/SANS accreditation, registered with the

Institute of Working in Heights, Proudly South African and ISO and our

products are more than 90% local content. We employ, train and retain

special expertise and since taking over have embarked on a number of

initiatives including accreditation of Black Staff to qualify as Lifting

Machinery Inspectors (LMI’s). Beyond this we hold about R20m worth of

inventory in our stores at any given point in time and have experienced

staff undertaking service and maintenance on our equipment.

Government and SOE Procurement Systems

- Designation of Aerial Platforms in order to:

- Encourage Local Production

- Ensure retention and new job creation

- Retain and improve competitiveness

- Drive export to Africa

- Create new industries and associated skills

- Price Stability as local products have very little Forex Exposure (95% local content)

- Positioning Local Products with Municipalities in Gauteng

- Excited with how Eskom and Ekurhuleni supports local products including Smith

- Have confidence in public procurement system but have a challenge where

procurement is outsourced to FML’s as they do not adhere to PPPFA

- Invoking Section 9.3 of the PPPFA

- Intervention with current tenders to facilitate local procurement with City of Tshwane

- Smith is well positioned as a MANUFACTURING BUSINESS and not just a trading business -

thus offering real value to you – our valued customer

Proposed Intervention by the Portfolio Committee

CONCLUSION

Contracting Smith Capital/Isipho Capital Holdings is an opportunity for Transnet/Eskom/COJ/Prasa,etc to directly improve the competitiveness of a black women owned business and indirectlyimprove the supplier base and localization. It gives real meaning to transformation in themanufacturing, engineering and financial services sectors.

Small Businesses

Large FML/ OEM’s &

Multinationals

• Job creation • Skills transfer and

development

• Direct

enablement of

black owned

company to

become a

large OEM

• Indirect

benefits of

black owned

companies

from contract

• Localization• Job creation • Skills development• Small business

promotion • Rural integration

• Small business promotion

• Rural integration

• SD guidelines through purchasing leverage

• Isipho Capital will have purchasing leverage to negotiate REAL skills transfer, REAL transfer of technology and REAL IP transfer

Purchasing flow Indirect impact

THANK YOU