Paul Roberts – TIF Technical Manager

Presentation to the TPS – 3 June 2009

Outline of presentation

Growing demand for travel – particularly by car

The impacts of increasing congestion on Traffic conditions Economy Leeds City Centre Buses

Lessons from Manchester

The emerging strategy Schemes Policies Funding

Leeds District employment forecasts(source Yorkshire Forward)

340

350

360

370

380

390

400

410

4202006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

year

000's

fte

jo

bs

December 2007 base March 2009 base

Growth

Demand for car travel

Flow AM peak hour2006

AM peak hour 2016

% increase

PM peak hour 2006

PM peak hour 2016

% increase

Total trips 89,700 105,000 17% 89,900 104,400 16%

Trips to city centre 17,600 19,360 10% 8,400 11,500 37%

Trips to city centre from beyond ORR

8,100 9,100 12% 3,300 4,300 30%

Trips from city centre 8,000 11,300 41% 16,400 19,900 21%

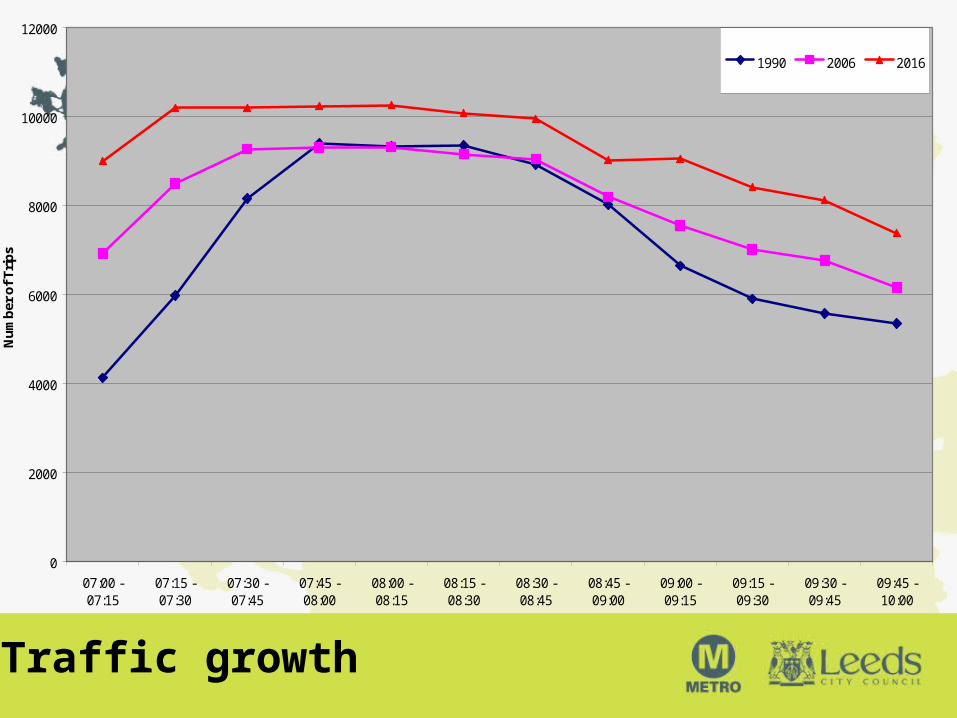

Baseline: Growth in peak period

0

2000

4000

6000

8000

10000

12000

07:00 -07:15

07:15 -07:30

07:30 -07:45

07:45 -08:00

08:00 -08:15

08:15 -08:30

08:30 -08:45

08:45 -09:00

09:00 -09:15

09:15 -09:30

09:30 -09:45

09:45 -10:00

Nu

mb

er o

f T

rip

s

1990 2006 2016

Traffic growth

Distribution of congestion

Within city centre To and from the M621 Around inner loop road On and around Inner Ring Road junctions

On most radial approaches to the city centre and at key radial and Orbital junctions

Junctions along ring road

Key:

Dotted line: current 20 minute drive time.

Shaded green: Future reduction in accessibility due to increasing congestion

Contracting catchments

Buses (main mode for attracting car users)

Downward trend in bus use

Growth in congestion leads to Greater unreliability Slower journey times

In combination with other global factors Fares increases Service reductions Reduced patronage

Do Minimum summary

Growth in congestion – scale, time and locations – especially in and around city centre

Traffic impacts Increases in journey times, queues, variability Deteriorating environment and air quality Increased business costs and reduced markets/opportunities

Significant reduction in city centre catchments (and to other key attractors)

Trip suppression/peak spreading

Many planned new jobs not delivered (12,000 less by 2021) A contracting and more expensive bus network (requiring more subsidy) with

contracting patronage

Lessons from Manchester

City wide pricing scheme cannot be the main policy lever

Non-fiscal demand management must be part of solution

Road pricing may be part of the solution if it is targeted, when and where it may be needed

Must demonstrate significant benefits (net cost of a charge less than the impacts of doing nothing about congestion)

Package needs effective messages and marketing

Bus improvements need to be deliverable (and include fares)

Must have a more ‘acceptable’ package with more winners

Need wide ranging set of objectives

Revised objectives

Delivering the Leeds City Centre Vision

Support the economy (within Leeds and the Region)

Narrowing the gap

Reduce congestion

Sustainable city

Quality of Life

Make Leeds an attractive option for post-recession investment

Raise the importance of transport investment/policy with decision makers

Background to a new Transport Strategy for Leeds

1991 Strategy served its purpose

Produce an updated 20 year Transport Strategy for Leeds

Needs to have identified funding streams

Focus on Phased approach to investment/policy Construction schemes Public transport networks Policy Funding

Emerging Strategy

Four main strands Mode transfer aimed at most significant numbers of trips into city centre, but in

particular commuting and shopping trips From outside ORR – rail, park and ride From inside ORR – bus network, ngt, cycle, walk

Mode transfer for commuting/education trips to the edge of city centre (rim/Aire Valley)

Public transport through interchange in city centre Reduce through car traffic in city centre and within ORR

Mode transfer for local short distance trips Accommodate longer distance orbital highway trips on orbital roads – local

additional orbital capacity (at key junctions)

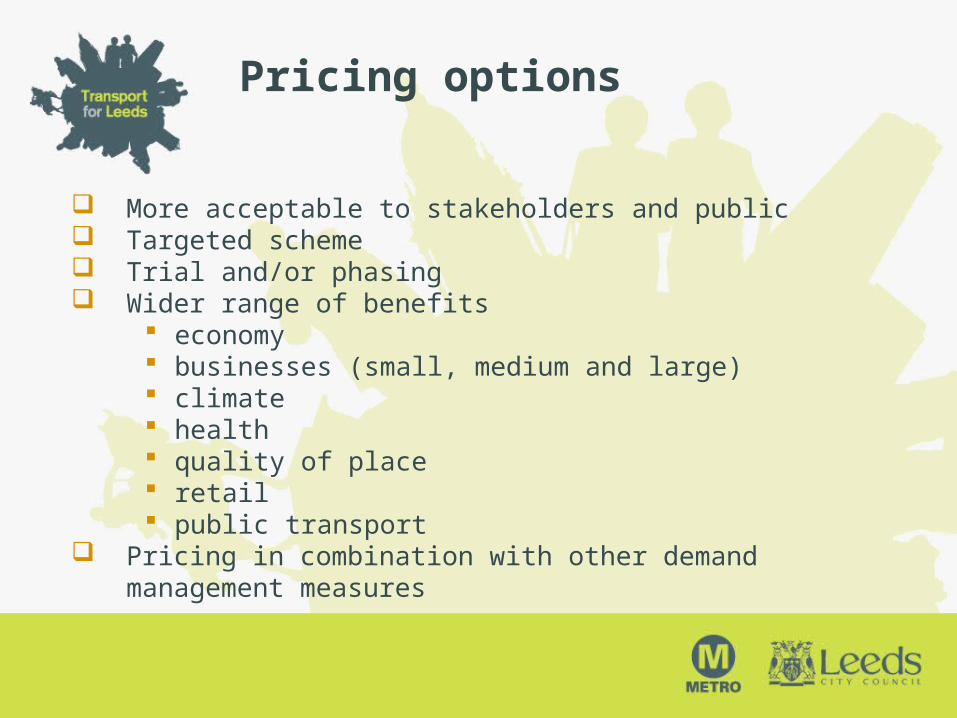

Pricing options

More acceptable to stakeholders and public Targeted scheme Trial and/or phasing Wider range of benefits

economy businesses (small, medium and large) climate health quality of place retail public transport

Pricing in combination with other demand management measures

Reduce CC impact of cars

More bus priority

New bus and rail P&R

Already approved

Eg NGT

Smarter choices, fares and ticketing improvements

Parking policy

Full package

City centre fiscal measures

New NGT routes

Rail package

Area wide fiscal measures

Tipping point for fiscal demand management Orbital highway upgrade

Deliver city centre vision

Support the economy

Reduce congestion

Narrow the gap

Sustainable city

Quality of life

Bus network

Cycle network

New city centre hubs

Emerging transport strategy

Land use policy

Funding Options

Willingness to create a ‘Leeds Transport Fund’ We will be assessing

Regional Funding Allocations – transport and non-transport Highways Agency and Network Rail funding streams Non-transport budgets EU funds TIF - capital Road pricing - revenue Planning Gain Pooling transport income streams Accelerated Development Zones Options for changes to rates

Budget co-ordination, phasing and certainty – A ‘resourced’ Transport Plan

Questions/comments/views?