IT Strategies for an Uncertain Future -

Embracing Change and InnovationScott Lundstrom, GVP

IDC Health Insights

© IDC Health Insights. Reproduction is forbidden unless authorized. All rights reserved.

Who is IDC Health Insights A global provider of research-based advisory

and consulting services focused on market and

technology developments impacting the global

health industry

Part of IDC – the premier global provider of

market intelligence and advisory services for the

information technology, telecommunications, and

consumer technology markets

Research led by a global team of 13 full-time

analysts with deep health industry experience,

and supported by over 1,000 IDC analysts

covering over 110 countries

IDC Health Insights serves a diverse and

growing global client base, including executives in

the payer, provider, and life science industries

and suppliers in the healthcare and life science

industries

2

© IDC Health Insights. Reproduction is forbidden unless authorized. All rights reserved.

Agenda

3

© IDC Health Insights. Reproduction is forbidden unless authorized. All rights reserved.

Health Industry Transformation

More than a small change or a bump in

the road

A significant change in the overall

marketplace

Assets, partnerships, products, and

platforms are all in flux with volatile

value proposition

4

Creates opportunities and risks for all market entrants and participants

© IDC Health Insights. Reproduction is forbidden unless authorized. All rights reserved.

Elements of Transformation

Innovation

Business model change

Changes in channels

Changes in regulations

Changes in buyer behavior and preferences

5

These elements often come together, transforming multiple aspects of an

industry at once

© IDC Health Insights. Reproduction is forbidden unless authorized. All rights reserved.

Industry Transformation on the 3rd Platform

Omni – Channel becomes real

Everything as a service

Customers become suppliers in the mid

market

Internet of Things

6

IT Assets Matter LessIT Agility Matters More

© IDC Health Insights. Reproduction is forbidden unless authorized. All rights reserved.

Technology Fueled Business Transformation Shifts Technology Buying Centers

7

© IDC Health Insights. Reproduction is forbidden unless authorized. All rights reserved.

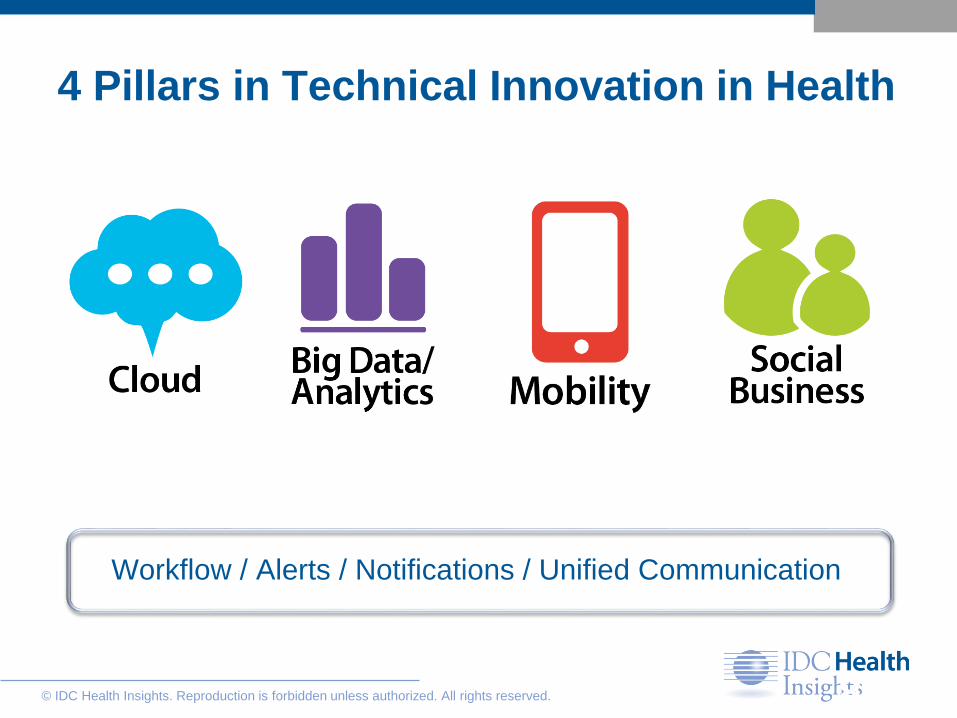

4 Pillars in Technical Innovation in Health

Workflow / Alerts / Notifications / Unified Communication

8

© IDC Health Insights. Reproduction is forbidden unless authorized. All rights reserved.

The Need for Agility On-Demand Turns IT Organizations Inside Out

A shrinking set of “core” competencies are resulting in

expanded BP/IT outsourcing

Public, private and hybrid cloud services have matured

Creating value out of information

is the new IT mantra.

New collaborative business models

are driving IT agility to meet

aggressive transformation demands.

9

© IDC Health Insights. Reproduction is forbidden unless authorized. All rights reserved.

Technology Buying Centers Will Permanently Shift

10

n=1227Source: IDC Business Technology Study, May 2013

© IDC Health Insights. Reproduction is forbidden unless authorized. All rights reserved.

More sourcing/less making– Hybrid dev ops

– Contracting for risk and agility

Analytics as architecture– Data management

– Governance

Commercialization – Information / Process as a

service

– Joint ventures, partnerships,

networks

Organizational Changes

11

40%

60%

Building /implementing ITSystems

Governing andManaging ITSystems

n=131Source: IDC's 2013 IT Staffing Survey - Jun 2013

59%

41%

Technical Skillsare PrimarySkill Set

Business Skillsare PrimarySkillset

© IDC Health Insights. Reproduction is forbidden unless authorized. All rights reserved.

Line of Business Will Outpace Spend by IT Org.US Enterprise IT Spend by Functional Area

12

8.6%

6.4%

5.8%

6.4%

10.4%

5.3%

8.5%

6.3%

6.9%

0%

4%

8%

12%

0% 20% 40% 60%

% Share of Spend, 2014

Security and Risk

Engineering, Architecture & Research

Other Horizontal Operations

Accounting / Finance / Billing

Marketing

Sales

Customer Service

Supply Chain Management

Industry Specific Operations

IT

2013 -

201

4 G

row

th

IT

Functional

Spending 2.2%

© IDC Health Insights. Reproduction is forbidden unless authorized. All rights reserved. 13

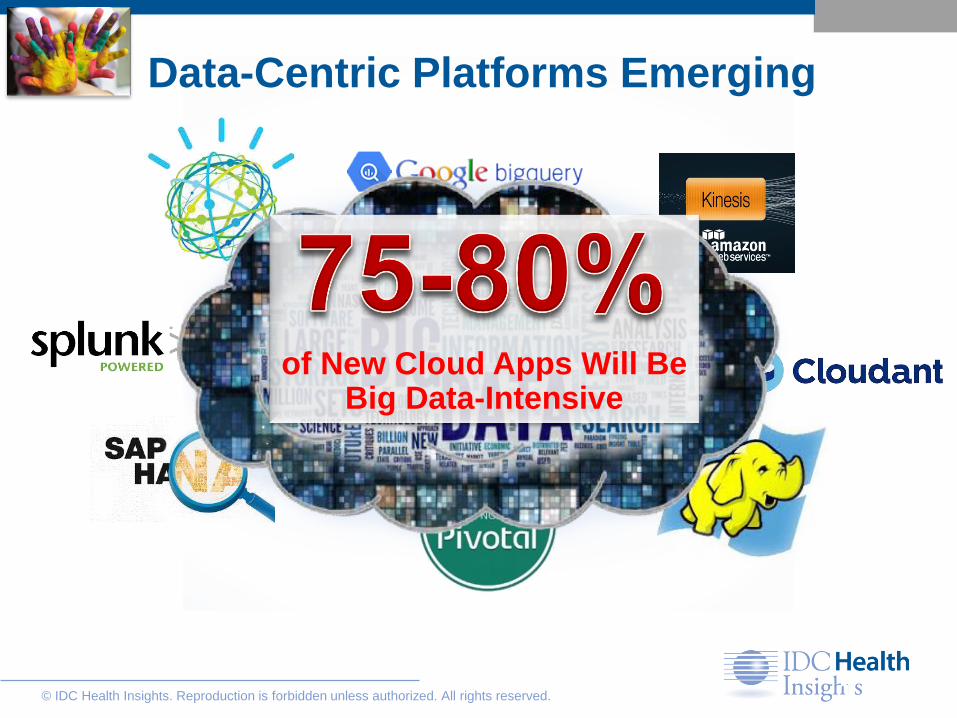

Data-Centric Platforms Emerging

of New Cloud Apps Will Be Big Data-Intensive

© IDC Health Insights. Reproduction is forbidden unless authorized. All rights reserved. 14

Industry Platforms Expanding

The Number of Industry Platforms

Will Expand to

by 2016

© IDC Health Insights. Reproduction is forbidden unless authorized. All rights reserved. 15

ExpandingIndustry Platforms

Industry Platforms Will Disrupt

of the Top 20 Market Leaders

in Most Industries by 2018

© IDC Health Insights. Reproduction is forbidden unless authorized. All rights reserved. 16

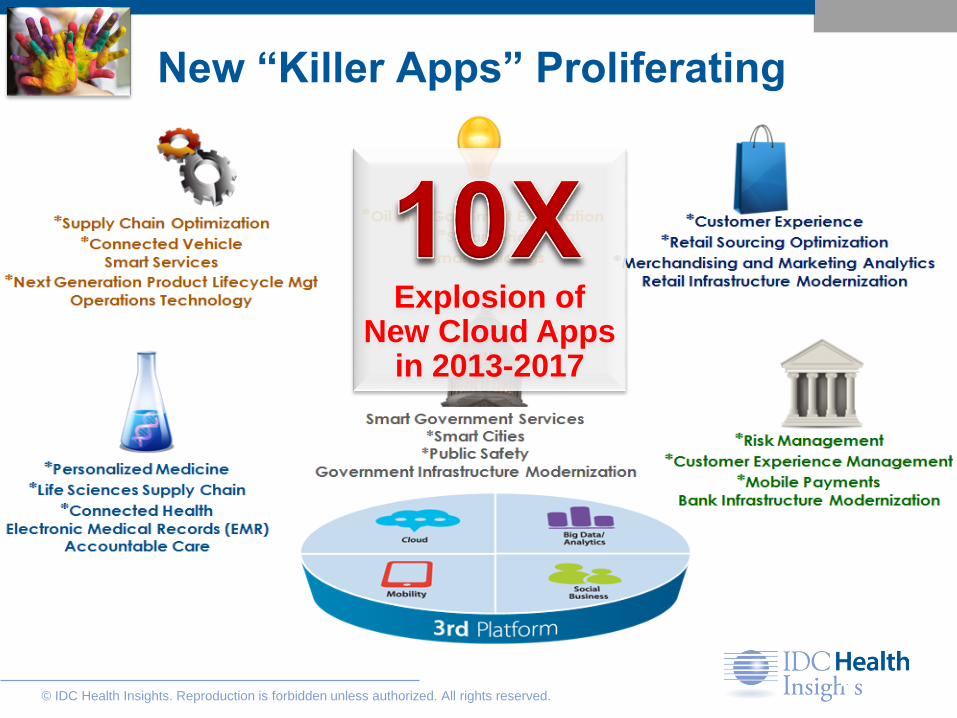

New “Killer Apps” Proliferating

Explosion of New Cloud Apps

in 2013-2017

* Big Data-Intensive

© IDC Health Insights. Reproduction is forbidden unless authorized. All rights reserved.

Cloud First Lives Up to the Hype

17

IDC CloudTrack, October 2013n=177 for manufacturingn=153 for healthcaren=81 for governmentn=80 for bankingN=66 for retailN=23 for utilities

© IDC Health Insights. Reproduction is forbidden unless authorized. All rights reserved.

Health Cloud Adoption

18

© IDC Health Insights. Reproduction is forbidden unless authorized. All rights reserved.

Big Data Healthcare Use Cases

Waste and abuse

Outcomes

Technology

Patient engagement

Fraud detection

Chronic disease

Avoidable deathsRegulatory compliance

Quality of care

Medical research

Drug discovery

Clinical trials

Personalized medicine

Environmental impact

Re-admissions

Translational research

Public health

Adverse health events

Patient compliance

Source: IDC, 2012.

Acti

vit

y

© IDC Health Insights. Reproduction is forbidden unless authorized. All rights reserved.

IDC’s Mobile Maturity Model:5 Stages of Progress

Ad hoc

Opportunistic

Repeatable

Managed

Optimized

Prove value of mobility with proof of concept or pilot projects

Reap early stage benefits and increase constituent buy-in with initial mobility implementations

Improve cost/benefit performance of continued implementations with integrated capabilities in mobility

Drive competitive differentiation with enterprise-wide governance and management in mobility

Sustain leveraged competitive advantage with continuous improvement and innovation in mobility

© IDC Health Insights. Reproduction is forbidden unless authorized. All rights reserved.

Driving Towards Health Systems Reform

Triple Aim Health Reform

5 Year Horizon

Value of Transformation

Patient Experience

Cost

Population Health

EHRHIE

Compliance

Competitive Advantage

Value-BasedPayments

Disease Management

Risk Mgt

Integrated Care + Health / Wellness

Sustainable care

Volume-based Payments

Predictive

Reactive

Prescriptive

At Risk Contracting

Population Health

C

Care Coordination

Now

Case Management

© IDC Health Insights. Reproduction is forbidden unless authorized. All rights reserved.

Essential Guidance

Understand that quality mandates force a

different operating model on IT.

Agility matters more – Assets matter less.

Integration of clinical, operational, and

financial data becomes IT’s biggest

challenge.

Governance and Data Management are

more important than you think.

Non-traditional thinking will be rewarded.

Evaluate new partnering opportunities.

22

© IDC Health Insights. Reproduction is forbidden unless authorized. All rights reserved.

Questions?

23

Scott LundstromGroup Vice President & General ManagerIDC Health Insights, IDC Government Insights, IDC Financial Insights