Presentation to the Allianz SE High Yield Group May 31, 2016

Michael McGillen David Hollander Kathy Mohanna Will Hasten

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

1

Table of Contents Executive Summary ............................................................................................................................. 3

Company ................................................................................................................................................... 6

History & Business Description ............................................................................................... 6

Manufacturing Process & Value Chain ................................................................................. 9

Products ............................................................................................................................................... 9

Management .................................................................................................................................... 11

Shareholder Profile ..................................................................................................................... 13

Capital Structure ........................................................................................................................... 14

Recent Financial Performance .............................................................................................. 18

Segment Financial Analysis ..................................................................................................... 19

Industry .................................................................................................................................................. 22

Market Trends ............................................................................................................................... 22

Competitive Landscape ............................................................................................................. 26

SWOT Analysis ............................................................................................................................... 29

Valuation ................................................................................................................................................ 30

Discounted Cash Flow Analysis ............................................................................................. 30

Comparable Companies Analysis ......................................................................................... 31

Precedent Transactions Analysis ......................................................................................... 33

Historical Prices Analysis ........................................................................................................ 34

Sum-of-the-Parts Analysis ....................................................................................................... 35

Plan of Reorganization ................................................................................................................... 36

Key Challenges to Financial Restructuring ..................................................................... 36

Board Control ................................................................................................................................. 37

Operational Improvements .................................................................................................... 38

Acquisitions & Divestments .................................................................................................... 42

Capital Structure Reorganization ........................................................................................ 44

Recovery Analysis ........................................................................................................................ 47

Allianz Recovery Analysis ........................................................................................................ 49

Appendix ................................................................................................................................................ 50

Exhibit 1: Comparable Trading Multiples .......................................................................... 0

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

2

Exhibit 2: Historical Financials – Income Statement .................................................... 1

Exhibit 3: Historical Financials – Balance Sheet ............................................................. 2

Exhibit 4: Historical Financials – Cash Flow Statement .............................................. 3

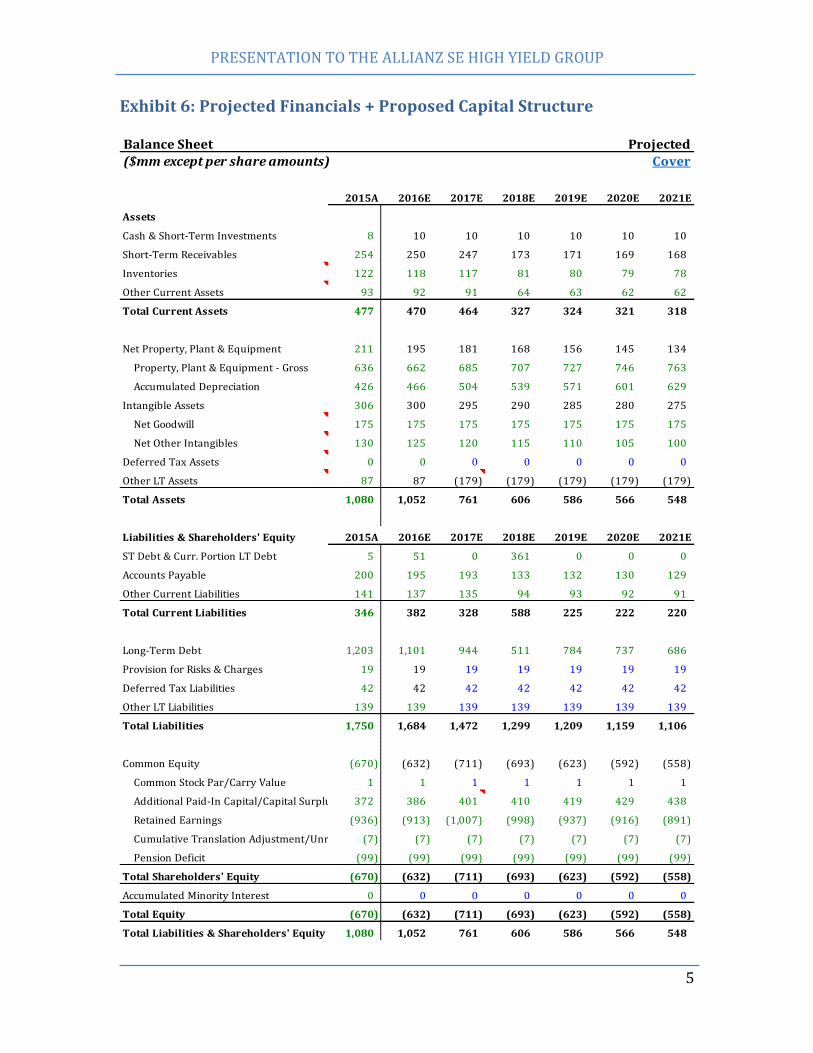

Exhibit 5: Projected Financials + Proposed Capital Structure................................. 4

Exhibit 6: Projected Financials + Proposed Capital Structure................................. 5

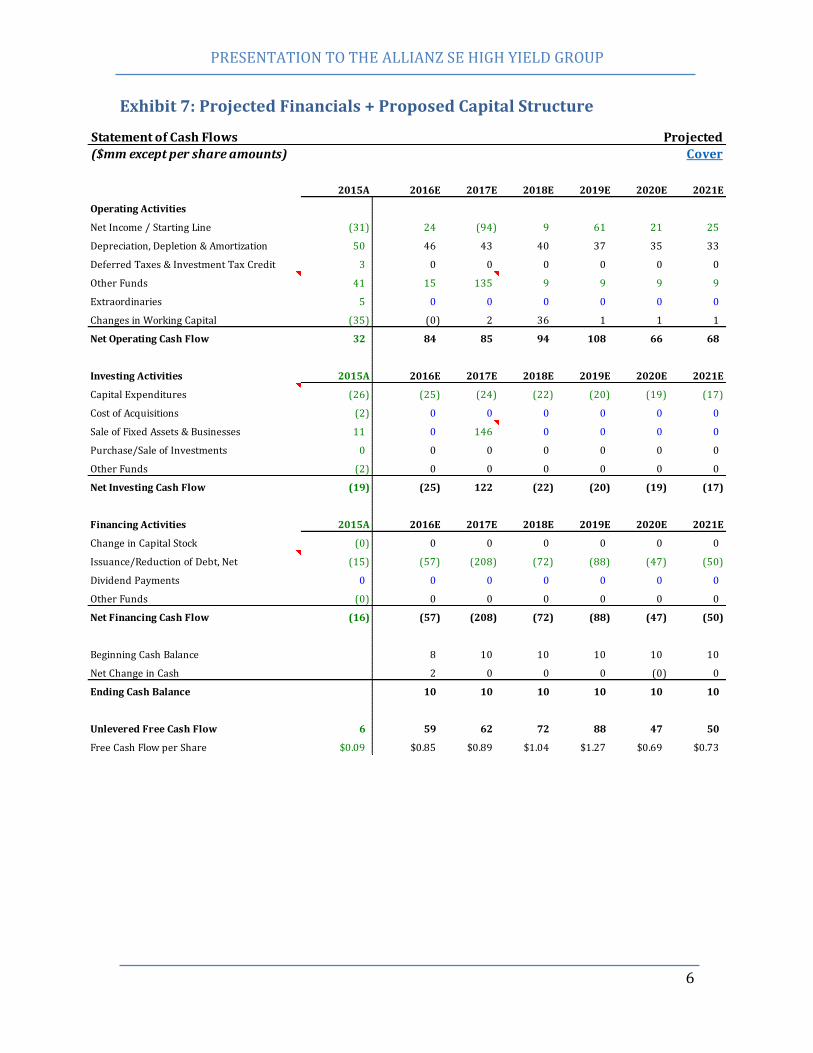

Exhibit 7: Projected Financials + Proposed Capital Structure................................. 6

Exhibit 8: Sum-of-the-parts Valuation .................................................................................. 7

Exhibit 9: Asset Waterfall in Bankruptcy............................................................................ 7

Exhibit 10: Pro-forma Balance Sheet following recapitalization ........................... 8

Exhibit 11: Pre-Restructuring Debt Repayment Schedule ........................................ 8

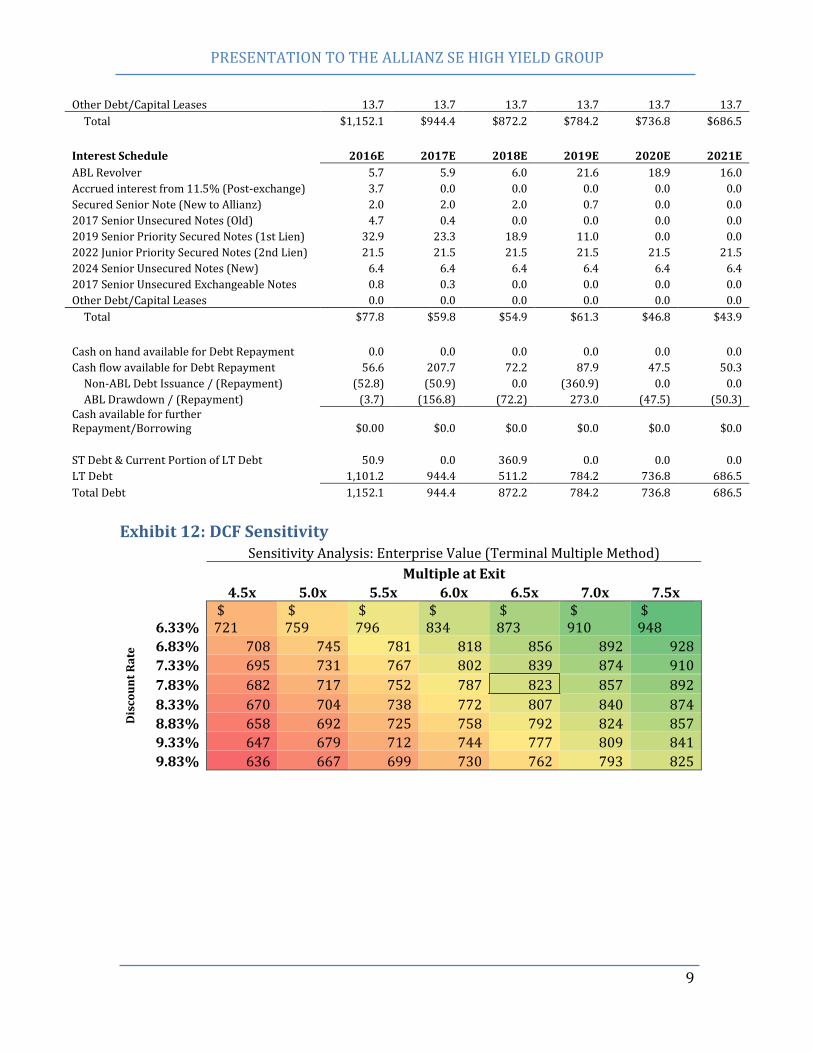

Exhibit 12: DCF Sensitivity ......................................................................................................... 9

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

3

Executive Summary Cenveo Corporation (‘Cenveo’ or ‘the Company’) is a market-leading manufacturer

of envelopes, labels, and commercial print applications. Over the last ten years, it

has been beset by secular declines in nearly all of its businesses. As advertising

spend continues its shift toward digital customer acquisition, direct-mail-dependent

Cenveo has seen pricing and sales volumes worsen. It has attempted three re-

financings in six years and our analysis indicates a likely bankruptcy within three.

Negative revenue growth, untenable 8.7x EBITDA leverage, an ABL facility drawn

dangerously close to its $190mm limit, and $540mm of first-lien notes coming due

in 2019 all spell reorganization for the envelope giant.

There has been a growing trend among private equity and hedge funds with

appetites for equity-like risks/rewards to use debt as a way for acquiring control of

financially distressed companies. The most common approach is to acquire

discounted loans (e.g., second-lien loans, senior subordinated notes, etc.) in the

secondary market or by lending more money to the company to avoid bankruptcy.

Underlying the success of such strategies is growing evidence of creditors effectively

influencing management and the overall direction of a company.1

An effective “loan-to-own” strategy should minimize the risk of litigation, liquidation

(i.e., the target company fails) and valuation that exceeds the investor’s value

proposition. As a result, any firm engaging in a loan-to-own strategy using the

junior debt must account for the interests of other creditors and management.

1 “Creditor Control and Conflict in Chapter 11”, Kenneth Ayotte and Edward Morrison, 2009

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

4

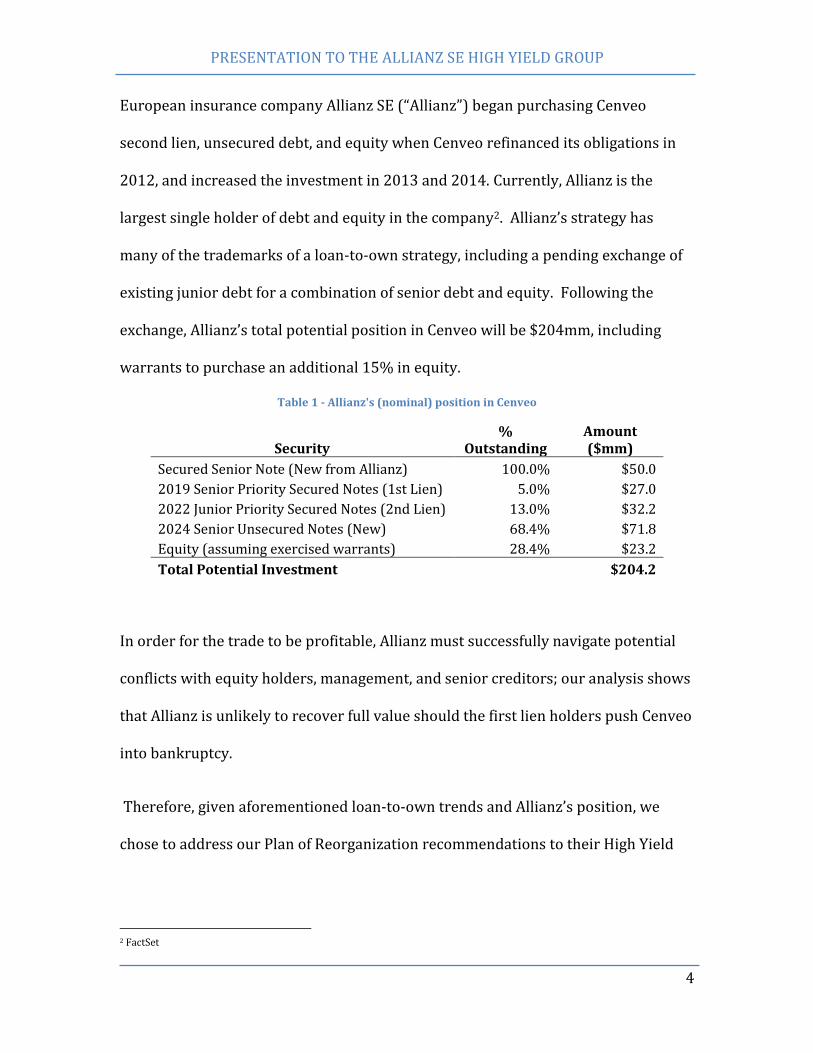

European insurance company Allianz SE (“Allianz”) began purchasing Cenveo

second lien, unsecured debt, and equity when Cenveo refinanced its obligations in

2012, and increased the investment in 2013 and 2014. Currently, Allianz is the

largest single holder of debt and equity in the company2. Allianz’s strategy has

many of the trademarks of a loan-to-own strategy, including a pending exchange of

existing junior debt for a combination of senior debt and equity. Following the

exchange, Allianz’s total potential position in Cenveo will be $204mm, including

warrants to purchase an additional 15% in equity.

Table 1 - Allianz's (nominal) position in Cenveo

Security %

Outstanding Amount ($mm)

Secured Senior Note (New from Allianz) 100.0% $50.0

2019 Senior Priority Secured Notes (1st Lien) 5.0% $27.0

2022 Junior Priority Secured Notes (2nd Lien) 13.0% $32.2

2024 Senior Unsecured Notes (New) 68.4% $71.8

Equity (assuming exercised warrants) 28.4% $23.2

Total Potential Investment $204.2

In order for the trade to be profitable, Allianz must successfully navigate potential

conflicts with equity holders, management, and senior creditors; our analysis shows

that Allianz is unlikely to recover full value should the first lien holders push Cenveo

into bankruptcy.

Therefore, given aforementioned loan-to-own trends and Allianz’s position, we

chose to address our Plan of Reorganization recommendations to their High Yield

2 FactSet

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

5

Group:

1. Operational Improvements: Use equity/debt position to obtain board

control and put in place new management familiar with higher-margin

labeling and modern mailing campaigns, cross-sell Kadena platform, and

expand labeling operations in underpenetrated geographic areas

2. M&A: Divest negative-growth Commercial Print segment to synergy-capable

strategic buyer, using proceeds to pay off 1st lien debt and reduce leverage

ratios

3. Capital Structure Reorganization: Coordinate with 1st and 2nd lien holders

to de-lever Cenveo through debt-to-equity conversion in pre-packaged

bankruptcy, use market position to entice strategic buyer

We estimate that execution of this plan will provide for complete recovery for the

ABL, 1st Lien and 2nd Lien holders and leave a significant stake in equity for Allianz.

Finally, it is important to remember that we believe Allianz has little long-term

interest in managing an envelope company. The recommendations below are aimed

at streamlining Cenveo and paving the way towards a profitable exit.

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

6

Company

History & Business Description Cenveo produces envelopes, labels, and commercial printing products, primarily in

the United States and Canada. Its present structure originates from a Sterling Group

roll-up of Georgia-Pacific’s envelope business as well as other commercial printers.

Sterling took the combined enterprise public in 1995 under the name Mail-Well,

changing its name to Cenveo in 2004.

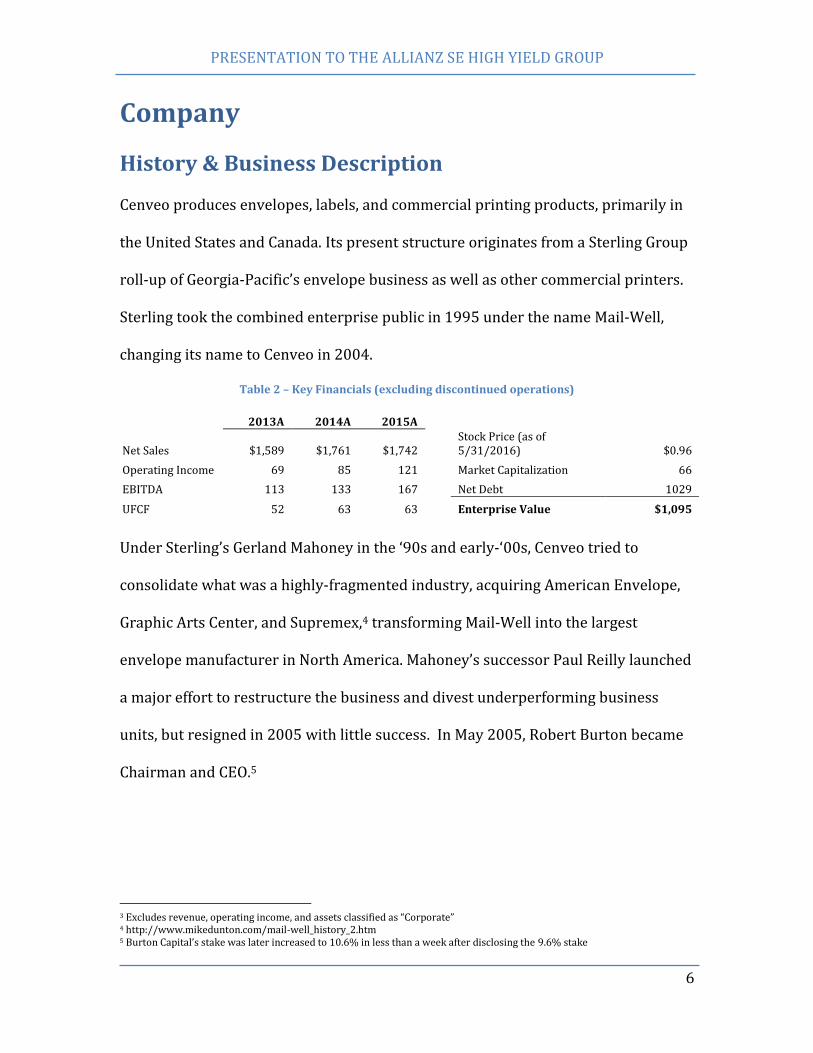

Table 2 – Key Financials (excluding discontinued operations)

2013A 2014A 2015A

Net Sales $1,589 $1,761 $1,742 Stock Price (as of 5/31/2016) $0.96

Operating Income 69 85 121 Market Capitalization 66

EBITDA 113 133 167 Net Debt 1029

UFCF 52 63 63 Enterprise Value $1,095 3

Under Sterling’s Gerland Mahoney in the ‘90s and early-‘00s, Cenveo tried to

consolidate what was a highly-fragmented industry, acquiring American Envelope,

Graphic Arts Center, and Supremex,4 transforming Mail-Well into the largest

envelope manufacturer in North America. Mahoney’s successor Paul Reilly launched

a major effort to restructure the business and divest underperforming business

units, but resigned in 2005 with little success. In May 2005, Robert Burton became

Chairman and CEO.5

3 Excludes revenue, operating income, and assets classified as “Corporate” 4 http://www.mikedunton.com/mail-well_history_2.htm 5 Burton Capital’s stake was later increased to 10.6% in less than a week after disclosing the 9.6% stake

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

7

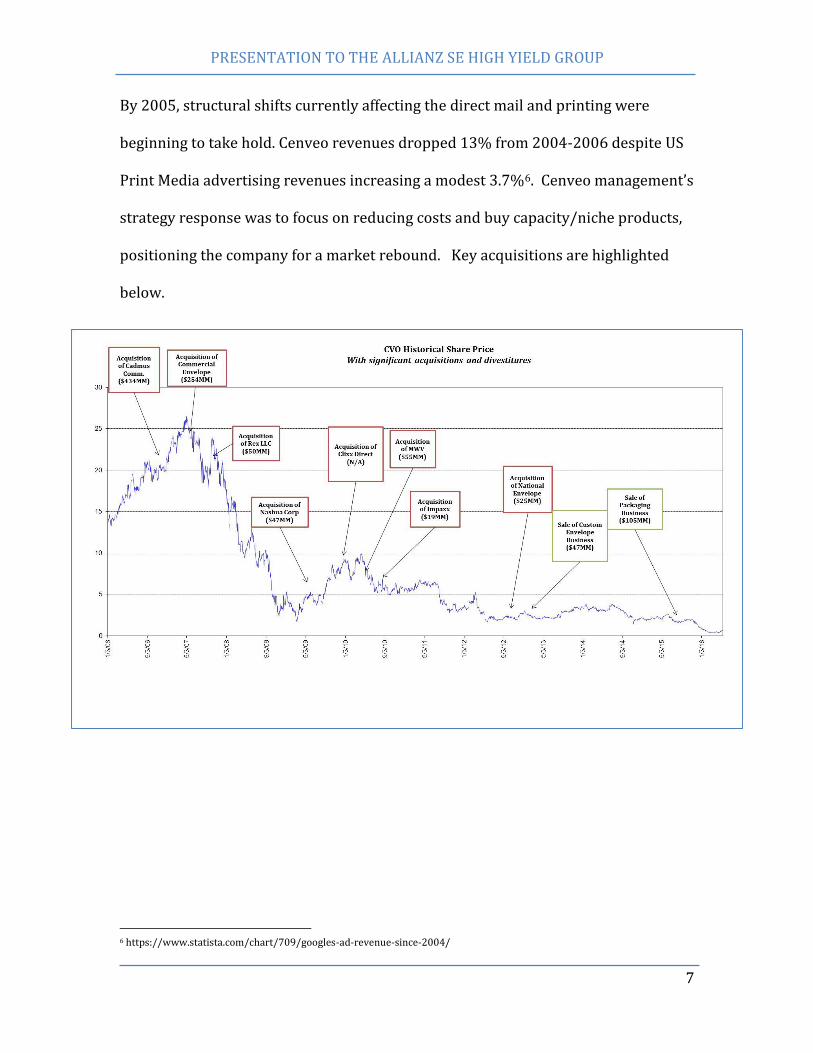

By 2005, structural shifts currently affecting the direct mail and printing were

beginning to take hold. Cenveo revenues dropped 13% from 2004-2006 despite US

Print Media advertising revenues increasing a modest 3.7%6. Cenveo management’s

strategy response was to focus on reducing costs and buy capacity/niche products,

positioning the company for a market rebound. Key acquisitions are highlighted

below.

6 https://www.statista.com/chart/709/googles-ad-revenue-since-2004/

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

8

Cadmus Communications (March 2007): Paid $241mm in cash (12.3x LTM

EBITDA, representing an 18% premium to the prior-day’s closing price) to

expand into scientific and technical journal printing

Commercial Envelope Manufacturing (August 2007): Paid $230mm in

cash (11.3x LTM EBITDA) to expand its envelope manufacturing business

MeadWestVaco’s Envelope Products Group (February 2011): Paid

$55mm in cash to expand direct mail and billing business.

National Envelope (August 2013): Purchased one of Cenveo’s chief

envelope competitors out of bankruptcy for $133mm (including assumption

of debt). This helped solidify Cenveo’s position as the largest North

American envelope manufacturer

Cenveo had expanded its suite of niche products and services but borrowed heavily

to do so. From 2006 to 2009, Cenveo’s net debt ballooned 83% ($676mm to

$1,234mm) while revenue increased only 14% owing to the 2008 recession. As

pricing pressure increased and demand slowed, Cenveo’s interest coverage went

from 1.77x to 1.00x over the same period.

Declining sales in 2012 and 2013 prompted management to change tactics once

more by focusing on the commercial envelope business and reducing exposure to

printing. From 2011-2016, it sold 5 print facilities ($14.6mm), 6 niche envelope

facilities ($9.4mm), its Custom Envelope business ($48mm), and its Packaging

business ($105mm), using the proceeds to pay down debt.

Cenveo has since become increasingly dependent on the high-yield market to

refinance its existing debt obligations, engaging in three exchange offers/issuances

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

9

from 2011-2015. While these have helped reduce overall interest expense by

$20mm per year, Cenveo has struggled to generate cash flow to grow its way out of

debt.

Manufacturing Process & Value Chain Cenveo operates 46 manufacturing facilities (15 owned, 31 leased) and leases its

Stamford headquarters as well as its sales and support facilities. Its primary product

inputs include paper, ink, film, offset plates and chemicals, with paper accounting

for the majority of total material costs. Understandably, Cenveo’s business requires

the use of heavy, capital-intensive machinery—roughly 83% of the Company’s

$636mm in Gross PP&E is devoted to machines like digital presses, which can cost

up to $900,000 and comprise much of one facility’s output. Many of these machines

are highly productive, however (1 W+D 320 envelope converter processes 21,000

units an hour). Cenveo’s 6.26x 5-year fixed asset turnover compares favorably with

RR Donnelly’s 6.71x and Quad/Graphics 2.34x. Only 23% of Cenveo’s 7,300

employees are unionized, which gives them a degree of operational flexibility.

Products

Envelope: Cenveo operates 22 envelope manufacturing and sales facilities, all based

in the US. This manufacturing process consists of “converting” rolls of paper into

envelopes using die-cutting, folding, and gluing. Its Commercial Envelope Group

handles specialized B2B envelope production, while its ‘Quality Park’ brand sells

specialty and stock envelopes through wholesalers, independent dealers and office

product superstores. These operations run hand-in-hand with Cenveo’s Mailing

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

10

Services division, which constructs direct-mail campaigns. These include standard

promotional mailers as well as invoices and billing statements. Key consumers

include the finance/insurance and retail industries.

Print: This segment produces car brochures, journals/books/magazines,

advertising displays, corporate identity/marketing materials and directories. With

16 manufacturing and sales facilities in the US, Cenveo’s commercial printing

process includes electronic prepress, direct-to-plate technology, high-quality color

printing (on web or sheet-fed presses, depending on the volume and quality you

need), and digital printing. This segment caters primarily to the consumer product,

automotive, travel and leisure and telecommunications industries.

Label: The label segment produces custom labels for pharmacies, consumer

product, and food/beverage companies. It specializes in end-to-end production of

custom, overnight packaging, and pressure-sensitive prescription labels. Its ‘Rx

Technology’ brand is the strongest in the pharmacy segment and its ‘Nashua’ brand

is a popular manufacturer of entertainment tickets. The segment has 8

manufacturing and sales facilities and labels are sold directly via the Cenveo

website/sales team or through extensive distributor channels.

Auxiliary: Cenveo also offers services that complement the 3 segments: Fulfillment

software and warehousing/distribution capacity (5 US facilities) offer clients the

ability to input orders automatically and take delivery within days while avoiding

inventory build-up. The Creative Services Group (4 facilities in the US, 4 in India, and

1 in the UK) designs direct-mail and commercial printing campaigns, services

essential to Envelope and Print customers. Cenveo also recently rolled out a

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

11

platform called ‘Kadena’, which is software that allows clients to design and archive

marketing content (both digital and print), manage its production and distribution,

and review campaign analytics.

Management

CEO Robert Burton Sr. has been an officer and director since 2005. Previously the

CEO of Moore Corporation ($2.0bn in sales) and World Color Press ($3.0bn in sales),

Burton had extensive printing industry experience prior to Cenveo. In 2005, Burton

became Cenveo's largest individual shareholder when he acquired a 9.6% stake

through his company Burton Capital Management. His two sons Robert Jr. and

Michael are President and COO, respectively, while CFO Scott Goodwin was an

accountant at Deloitte prior to Cenveo and Ian Scheinmann was a real estate lawyer

prior to becoming their de facto General Counsel.

Table 2 - Cenveo Key Executives

Table 3 - Kadena platform framework

Robert Burton, Sr. 74 Chairman of the Board, CEO 09/12/2005

Robert Burton, Jr. 39 President 08/10/2011

Scott Goodwin 37 CFO 04/2012

Michael Burton 37 COO 07/01/2013

Ian Scheinmann 46 Senior Vice President - Legal Affairs 08/2010

Office Name Age Current PositionOfficer

Since

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

12

The Cenveo Board is composed of three independent directors and Burtons Sr. and

Jr. Gerald Armstrong is a former banker specializing in print finance, Dr. Mark

Griffin is an educator specializing in learning disabilities, and Dr. Susan Herbst is the

president of the University of Connecticut, where Cenveo is based.

While it requires a supermajority for mergers (2/3rds), Cenveo’s board is

remarkably shareholder-friendly. There is no poison pill, classified board or super-

voting requirements for the removal of board members; it has a 1.25/10 FactSet

Bulletproof rating for takeover defenses, which is lax compared to the 3.19 rating

for the Russell 3000.

Table 3 - Cenveo Directorship

There are 3 Cenveo governance-related issues that are cause for concern:

While management equity interests are aligned with the company, the small

number of board members create an unusual amount of control for the

Burton family. This would present some difficulty in a reorganization

scenario.

Excessive Burton family compensation. Each of the Burtons averaged over

$1mm in compensation over a period in which Cenveo’s share averaged a

Robert Burton, Sr. Chairman of the Board 09/12/2005

Gerald Armstrong Independent Director, Chair of Audit Committee and Nominating

Committee

12/31/2007

Robert Burton Director 09/18/2013

Dr. Mark Griffin Independent Director, Chair of HR Committee 09/12/2005

Dr. Susan Herbst, Ph.D Independent Director 09/18/2013

Current PositionsDirector

SinceBoard Member Name

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

13

negative 31% annual return. Cumulatively, they have been paid over $75mm

since 2005 (when shares averaged ~$4.00).

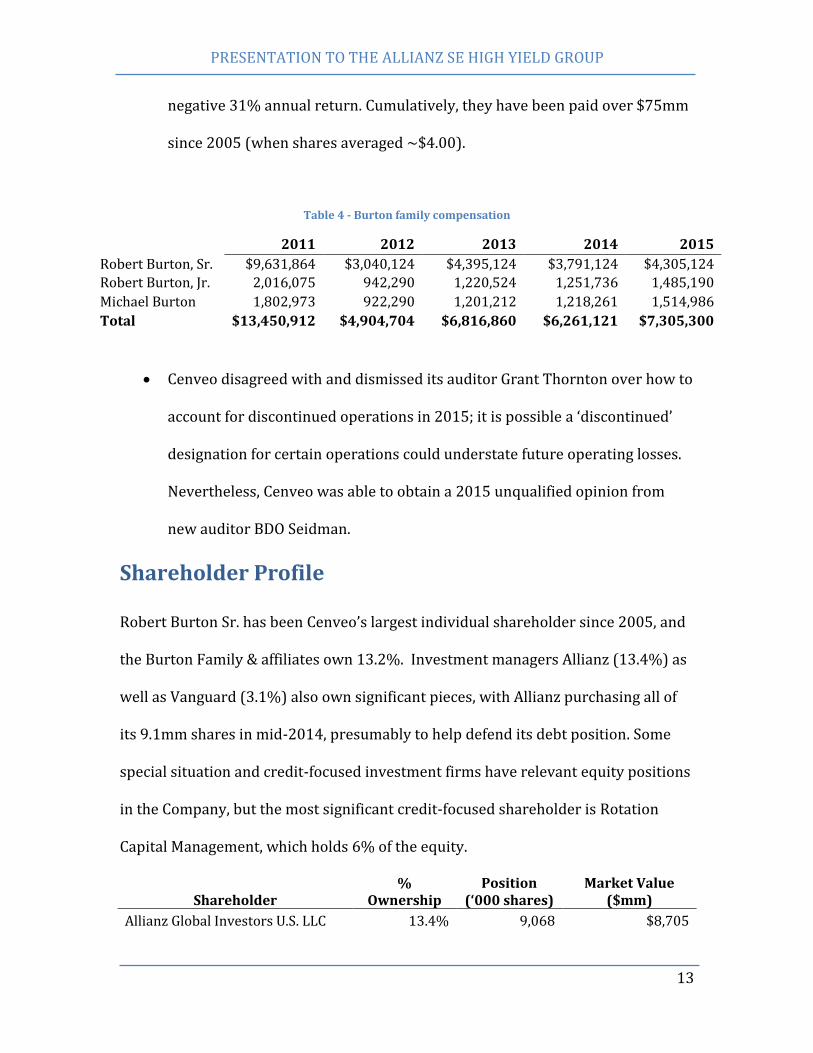

Table 4 - Burton family compensation

2011 2012 2013 2014 2015

Robert Burton, Sr. $9,631,864 $3,040,124 $4,395,124 $3,791,124 $4,305,124

Robert Burton, Jr. 2,016,075 942,290 1,220,524 1,251,736 1,485,190

Michael Burton 1,802,973 922,290 1,201,212 1,218,261 1,514,986

Total $13,450,912 $4,904,704 $6,816,860 $6,261,121 $7,305,300

Cenveo disagreed with and dismissed its auditor Grant Thornton over how to

account for discontinued operations in 2015; it is possible a ‘discontinued’

designation for certain operations could understate future operating losses.

Nevertheless, Cenveo was able to obtain a 2015 unqualified opinion from

new auditor BDO Seidman.

Shareholder Profile

Robert Burton Sr. has been Cenveo’s largest individual shareholder since 2005, and

the Burton Family & affiliates own 13.2%. Investment managers Allianz (13.4%) as

well as Vanguard (3.1%) also own significant pieces, with Allianz purchasing all of

its 9.1mm shares in mid-2014, presumably to help defend its debt position. Some

special situation and credit-focused investment firms have relevant equity positions

in the Company, but the most significant credit-focused shareholder is Rotation

Capital Management, which holds 6% of the equity.

Shareholder %

Ownership Position

(‘000 shares) Market Value

($mm)

Allianz Global Investors U.S. LLC 13.4% 9,068 $8,705

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

14

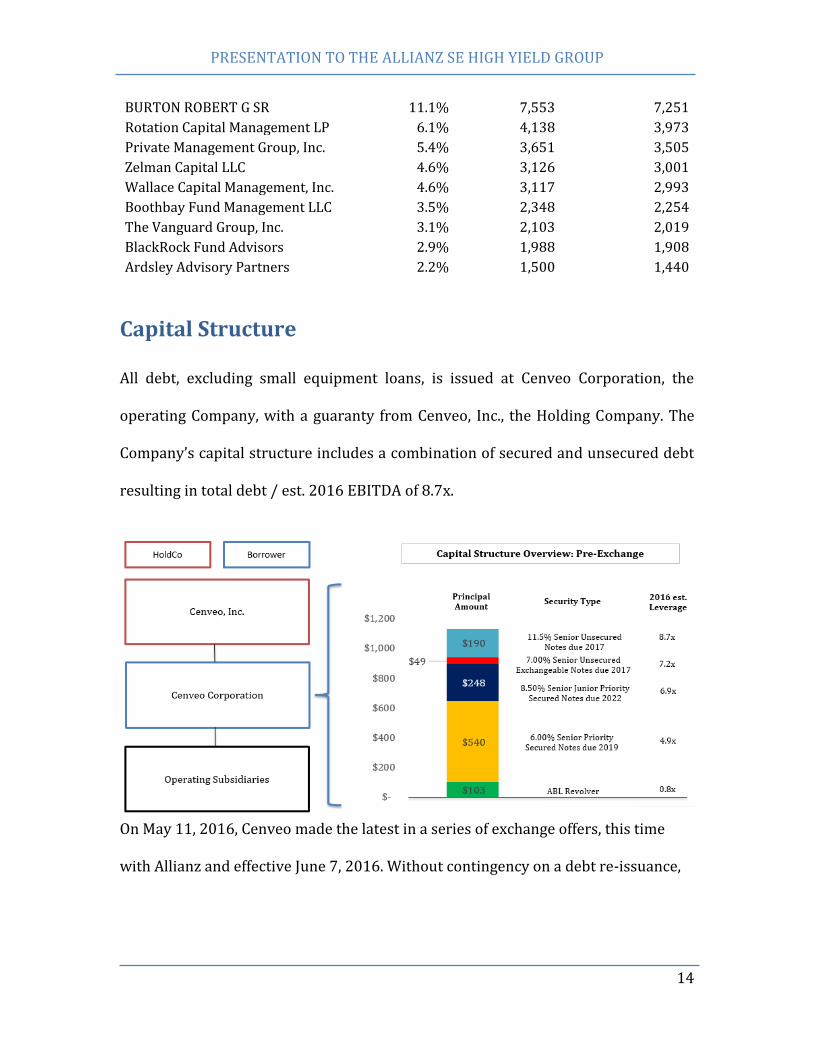

BURTON ROBERT G SR 11.1% 7,553 7,251

Rotation Capital Management LP 6.1% 4,138 3,973

Private Management Group, Inc. 5.4% 3,651 3,505

Zelman Capital LLC 4.6% 3,126 3,001

Wallace Capital Management, Inc. 4.6% 3,117 2,993

Boothbay Fund Management LLC 3.5% 2,348 2,254

The Vanguard Group, Inc. 3.1% 2,103 2,019

BlackRock Fund Advisors 2.9% 1,988 1,908

Ardsley Advisory Partners 2.2% 1,500 1,440

Capital Structure

All debt, excluding small equipment loans, is issued at Cenveo Corporation, the

operating Company, with a guaranty from Cenveo, Inc., the Holding Company. The

Company’s capital structure includes a combination of secured and unsecured debt

resulting in total debt / est. 2016 EBITDA of 8.7x.

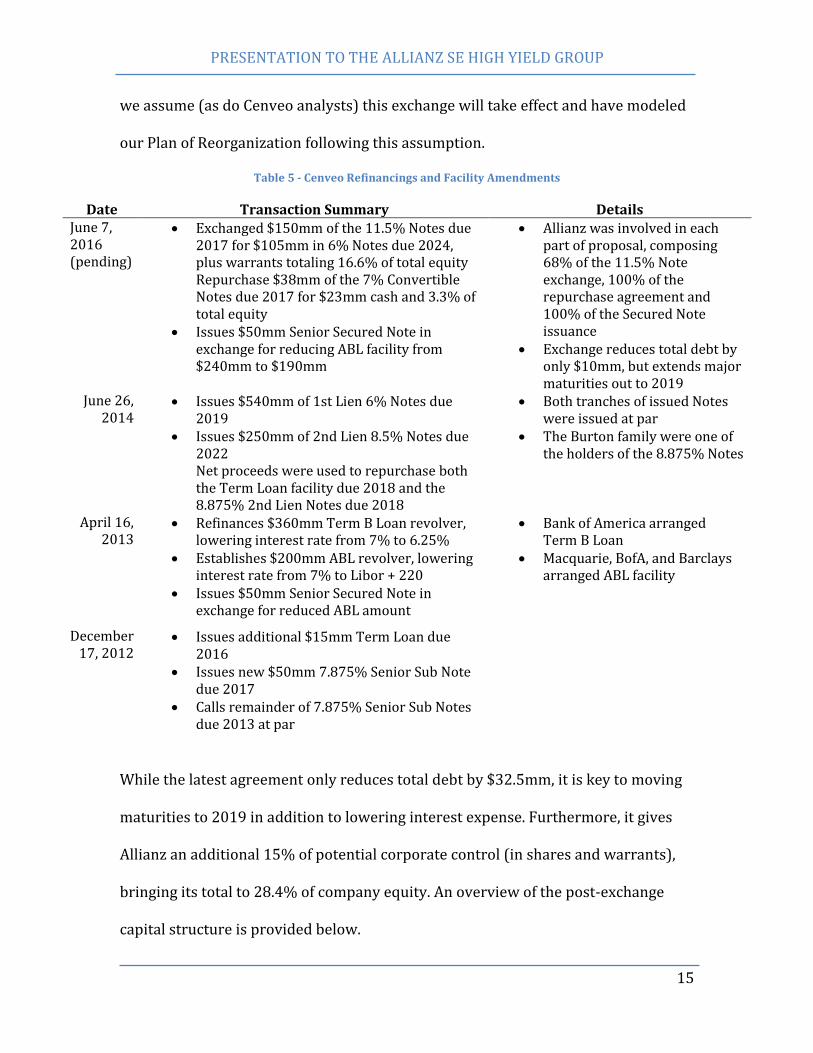

On May 11, 2016, Cenveo made the latest in a series of exchange offers, this time

with Allianz and effective June 7, 2016. Without contingency on a debt re-issuance,

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

15

we assume (as do Cenveo analysts) this exchange will take effect and have modeled

our Plan of Reorganization following this assumption.

Table 5 - Cenveo Refinancings and Facility Amendments

Date Transaction Summary Details June 7, 2016 (pending)

Exchanged $150mm of the 11.5% Notes due 2017 for $105mm in 6% Notes due 2024, plus warrants totaling 16.6% of total equity Repurchase $38mm of the 7% Convertible Notes due 2017 for $23mm cash and 3.3% of total equity

Issues $50mm Senior Secured Note in exchange for reducing ABL facility from $240mm to $190mm

Allianz was involved in each part of proposal, composing 68% of the 11.5% Note exchange, 100% of the repurchase agreement and 100% of the Secured Note issuance

Exchange reduces total debt by only $10mm, but extends major maturities out to 2019

June 26, 2014

Issues $540mm of 1st Lien 6% Notes due 2019

Issues $250mm of 2nd Lien 8.5% Notes due 2022 Net proceeds were used to repurchase both the Term Loan facility due 2018 and the 8.875% 2nd Lien Notes due 2018

Both tranches of issued Notes were issued at par

The Burton family were one of the holders of the 8.875% Notes

April 16, 2013

Refinances $360mm Term B Loan revolver, lowering interest rate from 7% to 6.25%

Establishes $200mm ABL revolver, lowering interest rate from 7% to Libor + 220

Issues $50mm Senior Secured Note in exchange for reduced ABL amount

Bank of America arranged Term B Loan

Macquarie, BofA, and Barclays arranged ABL facility

December 17, 2012

Issues additional $15mm Term Loan due 2016

Issues new $50mm 7.875% Senior Sub Note due 2017

Calls remainder of 7.875% Senior Sub Notes due 2013 at par

While the latest agreement only reduces total debt by $32.5mm, it is key to moving

maturities to 2019 in addition to lowering interest expense. Furthermore, it gives

Allianz an additional 15% of potential corporate control (in shares and warrants),

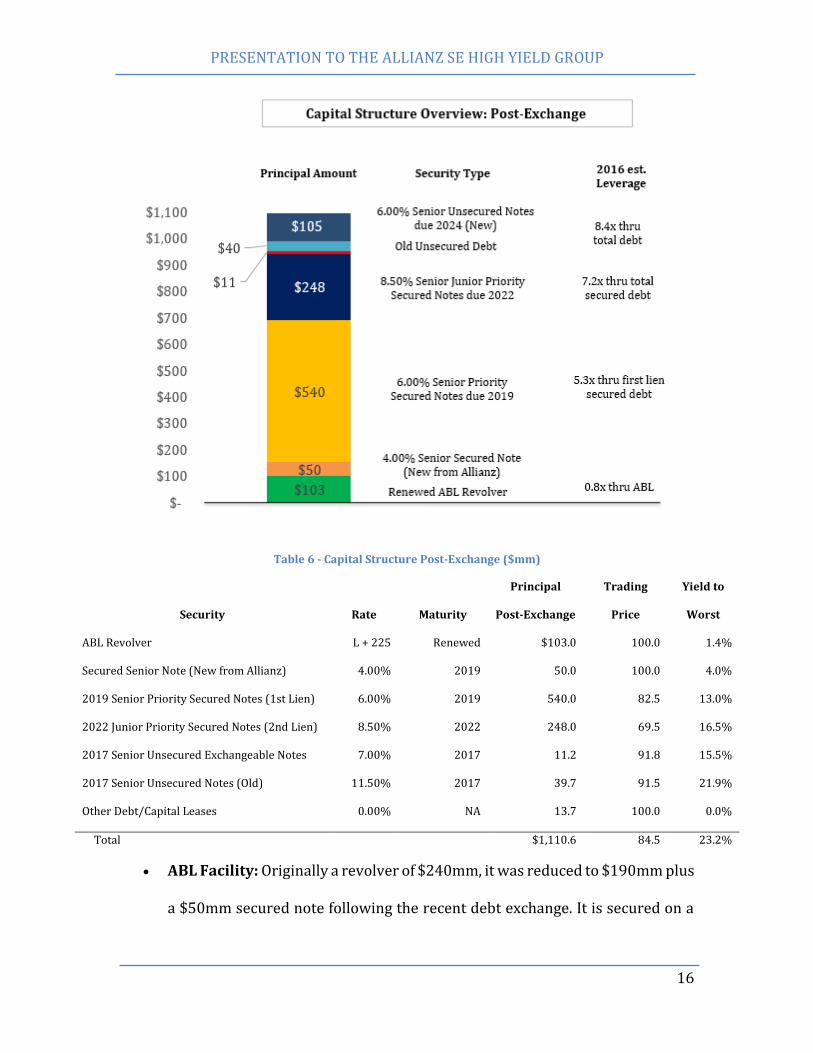

bringing its total to 28.4% of company equity. An overview of the post-exchange

capital structure is provided below.

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

16

Table 6 - Capital Structure Post-Exchange ($mm)

Security Rate Maturity

Principal

Post-Exchange

Trading

Price

Yield to

Worst

ABL Revolver L + 225 Renewed $103.0 100.0 1.4%

Secured Senior Note (New from Allianz) 4.00% 2019 50.0 100.0 4.0%

2019 Senior Priority Secured Notes (1st Lien) 6.00% 2019 540.0 82.5 13.0%

2022 Junior Priority Secured Notes (2nd Lien) 8.50% 2022 248.0 69.5 16.5%

2017 Senior Unsecured Exchangeable Notes 7.00% 2017 11.2 91.8 15.5%

2017 Senior Unsecured Notes (Old) 11.50% 2017 39.7 91.5 21.9%

Other Debt/Capital Leases 0.00% NA 13.7 100.0 0.0%

Total $1,110.6 84.5 23.2%

ABL Facility: Originally a revolver of $240mm, it was reduced to $190mm plus

a $50mm secured note following the recent debt exchange. It is secured on a

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

17

first priority on all Cenveo assets. The syndicate includes Bank of America,

Macquarie, Barclays, GE Capital and Wells Fargo.

Senior Secured Note: Issued by Allianz as part of the agreement to reduce the

ABL facility. Ranked junior to the 1st Lien Notes with respect to the Notes

collateral but senior to the 1st Lien with respect to ABL collateral.

2019 Senior Priority Secured Notes (1st Lien): These are rated Caa1/B- and

secured on a 1st Lien basis by both the parent and subsidiaries of Cenveo. Key

covenants include a restriction on sale of assets (the lien transfers), limit on

further indebtedness (unless it can meet a fixed-charge ratio of at least 2:1—

Cenveo will be at 1.05:1 in 2016), and change of control. Holders include

Allianz (5%), Aberdeen (5%), Fidelity (4%), Unicredit (3%), SEI, State Street,

and Western and Southern (all with 2%).

2022 Junior Priority Secured Notes (2nd Lien): Rated Caa3/CCC-, largely the

same covenants and collateral as the 1st Lien. Holders include Allianz (13%),

Northeast Investors (10%), JPMorgan (5%), SEI (4.7%), Advent, Vertex and

Goldman (all with 1%). Both the 1st and 2nd Lien groups have retained

respective financial and legal counsel.

2017 Senior Unsecured Notes: Allianz formerly held 54% of these, and

together with 2 other holders, a total of 79% were exchanged for the 2024

Notes, leaving the rest with light covenants except for a restriction on asset

sales (unless it’s for at least 75% cash). Ranked pari passu with other

unsecured debt.

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

18

2017 Senior Unsecured Exchangeable Notes: Convertible at $4.41 per

share, these are covenant light. 77% of these (Allianz’s stake) were

repurchased by Cenveo at a 40% discount. Also pari passu with unsecured

debt.

2024 Senior Unsecured Notes: With the same covenants as the 2017

Unsecureds, Allianz and two holders have 97% outstanding.

Leverage & Solvency: The Company’s 2016E ABL, secured, and total leverage will be

an uncomfortable 0.8x, 7.2x, and 8.4x. Based on a fully-diluted market capitalization

of $66mm as of May 31, 2016, Cenveo’s enterprise value is 8.7x EBITDA, which

suggests a debt-to-value at a bankruptcy-level 98%. An Altman Z-Score of 0.8

supports the bankruptcy prediction as well.

Recent Financial Performance

Cenveo reported weaker sales in 2015 (-10.6%) due to the divestiture of its

packaging business and sales slowdowns in its envelope and label segments. That

said, operating margin widened 2.6%; COGS narrowed by 1.3% and SG&A by 0.5%,

demonstrating management’s focus on cost minimization. Interest expense also

declined by $6mm as a result of debt retirement and exchanges. On a same-segment

basis, revenue was down only 1.1%, with EBITDA up 25.6% due to cost-cutting

particularly in the Envelope segment. Management maintained this margin

improvement was due to faster-than-expected integration of the National Envelope

acquisition (they closed redundant facilities in Jacksonville and Ohio) as well as

investments in more efficient labeling machinery.

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

19

Cenveo 2012A 2013A 2014A 2015A

Sales $1,798 $1,778 $1,949 $1,742

Sales Growth (5.8%) (1.1%) 9.6% (10.6%)

COGS excluding D&A as % of Sales 78.4% 80.7% 82.2% 80.9%

SG&A Margin 10.4% 11.6% 11.2% 10.7%

EBIT (Operating Income) 112 29 44 84

Net Income (Loss) (80) (69) (84) (31)

Adjusted EBITDA 187 115 130 142

% Growth (12.3%) (38.3%) 13.0% 9.3%

D&A 62 60 64 50

CapEx 21 29 37 26

Segment Financial Analysis

While the Envelope, Print, and Label segments usually operate out of separate

manufacturing facilities, the company benefits from cross-selling synergies, as

evident by the 130% rise in intercompany sales to $28.3mm from 2013-2015. This

was particularly evident in Print (from $4.9mm to $17.6mm), which provides the

direct-mail inserts to Envelope clients. Additionally, Cenveo benefits from cost

synergies on raw materials supply as well as final product distribution—it

frequently ships multiple products across segments to the same customers.

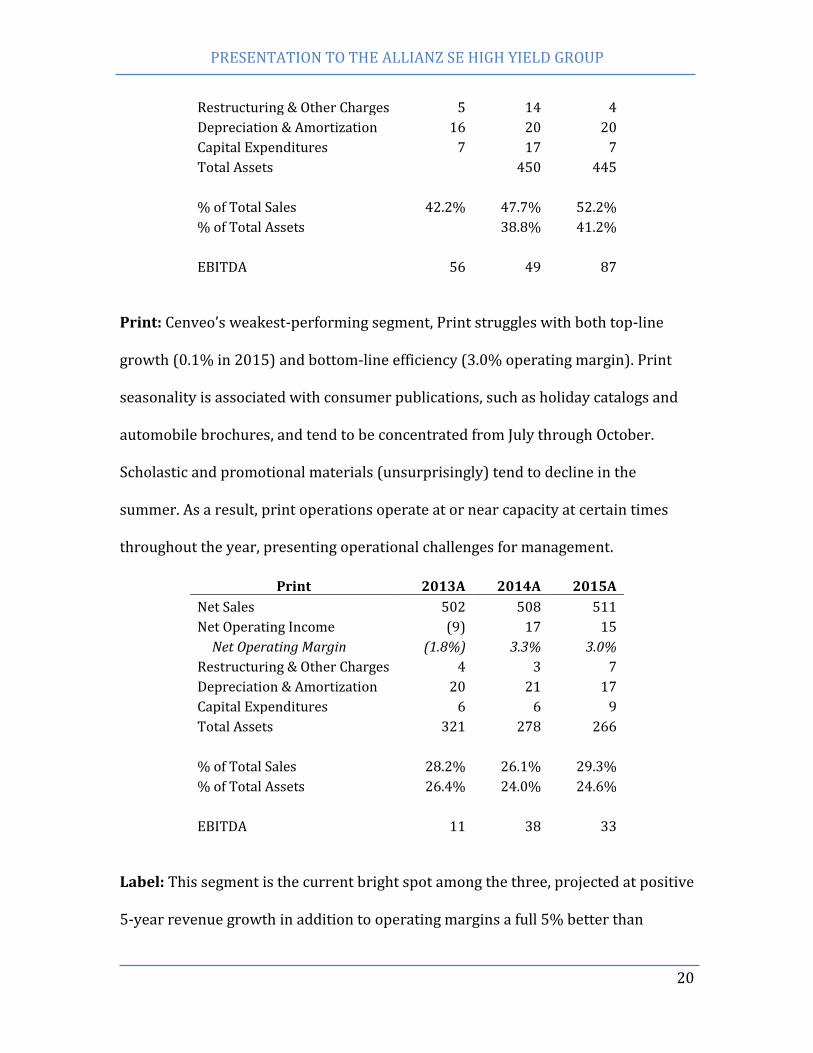

Envelope: The segment typically accounts for 40% of the company’s assets and

33% of its capital expenditure. Historically, Envelope experiences seasonality with a

higher percentage of products sold during Q3 and Q4, primarily related to back-to-

school campaigns and holiday purchases.

Envelope 2013A 2014A 2015A

Net Sales 750 930 909

Net Operating Income 40 30 66

Net Operating Margin 5.3% 3.2% 7.3%

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

20

Restructuring & Other Charges 5 14 4

Depreciation & Amortization 16 20 20

Capital Expenditures 7 17 7

Total Assets 450 445

% of Total Sales 42.2% 47.7% 52.2%

% of Total Assets 38.8% 41.2%

EBITDA 56 49 87

Print: Cenveo’s weakest-performing segment, Print struggles with both top-line

growth (0.1% in 2015) and bottom-line efficiency (3.0% operating margin). Print

seasonality is associated with consumer publications, such as holiday catalogs and

automobile brochures, and tend to be concentrated from July through October.

Scholastic and promotional materials (unsurprisingly) tend to decline in the

summer. As a result, print operations operate at or near capacity at certain times

throughout the year, presenting operational challenges for management.

Print 2013A 2014A 2015A

Net Sales 502 508 511

Net Operating Income (9) 17 15

Net Operating Margin (1.8%) 3.3% 3.0%

Restructuring & Other Charges 4 3 7

Depreciation & Amortization 20 21 17

Capital Expenditures 6 6 9

Total Assets 321 278 266

% of Total Sales 28.2% 26.1% 29.3%

% of Total Assets 26.4% 24.0% 24.6%

EBITDA 11 38 33

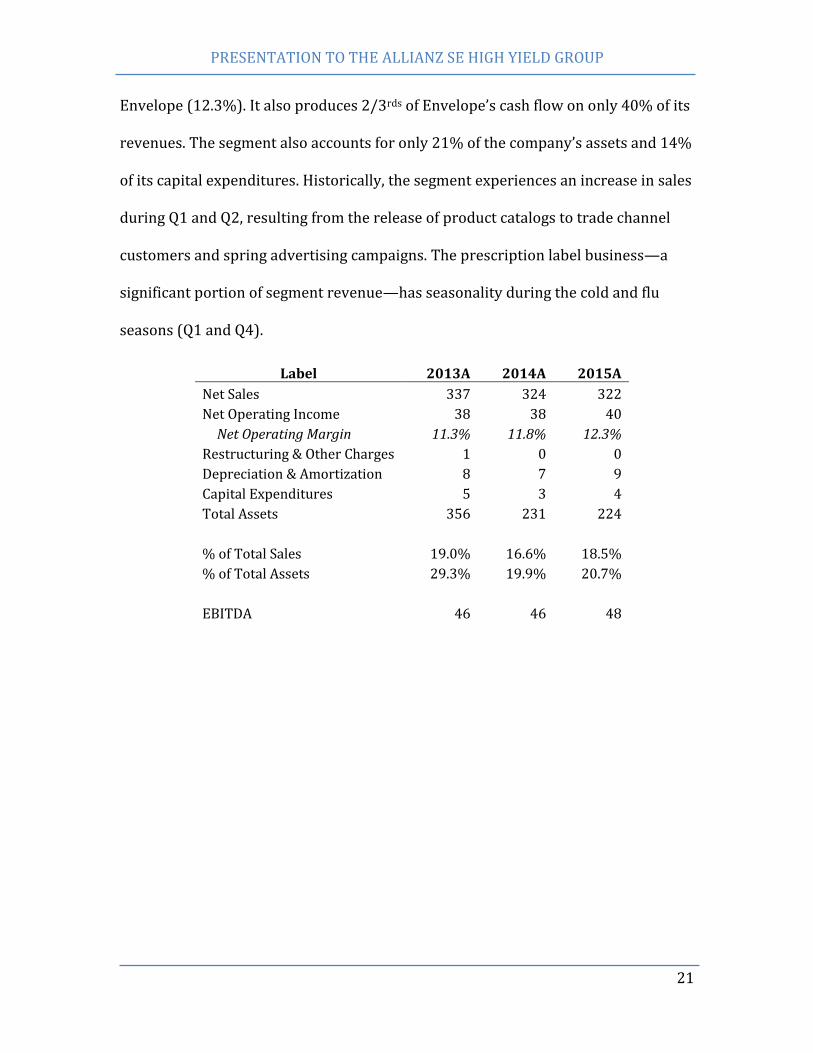

Label: This segment is the current bright spot among the three, projected at positive

5-year revenue growth in addition to operating margins a full 5% better than

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

21

Envelope (12.3%). It also produces 2/3rds of Envelope’s cash flow on only 40% of its

revenues. The segment also accounts for only 21% of the company’s assets and 14%

of its capital expenditures. Historically, the segment experiences an increase in sales

during Q1 and Q2, resulting from the release of product catalogs to trade channel

customers and spring advertising campaigns. The prescription label business—a

significant portion of segment revenue—has seasonality during the cold and flu

seasons (Q1 and Q4).

Label 2013A 2014A 2015A

Net Sales 337 324 322

Net Operating Income 38 38 40

Net Operating Margin 11.3% 11.8% 12.3%

Restructuring & Other Charges 1 0 0

Depreciation & Amortization 8 7 9

Capital Expenditures 5 3 4

Total Assets 356 231 224

% of Total Sales 19.0% 16.6% 18.5%

% of Total Assets 29.3% 19.9% 20.7%

EBITDA 46 46 48

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

22

Industry

Market Trends

Cenveo’s three segments traditionally fall within the following industries: Office

Stationery Manufacturing (or OSM, encompassing Envelopes), Print, and Packaging

& Labelling (PL).

OSM: In the United States (where Cenveo generates 80% of its revenue), OSM

accounts for $6.9bn in sales with a 5-year CAGR of -0.3% (2011-2016) and -2.0%

(2016-2021). Demand for office stationary products is closely correlated with

economic activity and level of unemployment and began to recover following the

most recent crisis supported by favorable levels of business activity and consumer

spending.

Table 7 - Recovery in Demand for OSM

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

23

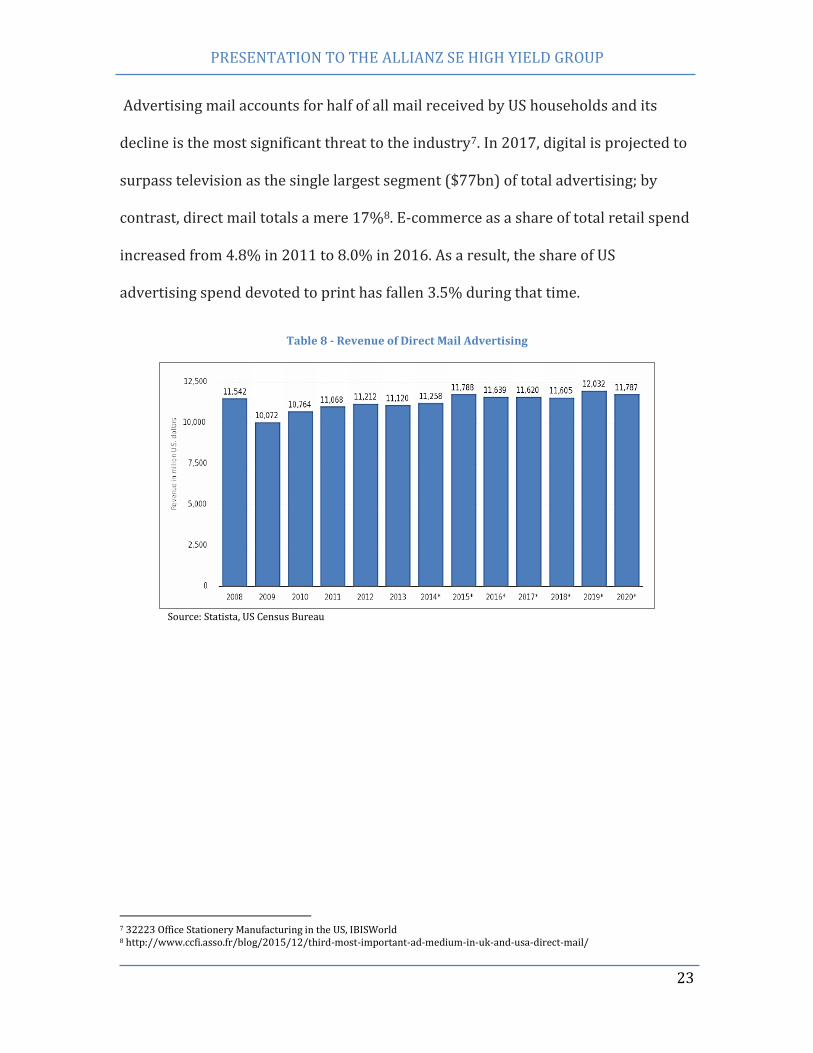

Advertising mail accounts for half of all mail received by US households and its

decline is the most significant threat to the industry7. In 2017, digital is projected to

surpass television as the single largest segment ($77bn) of total advertising; by

contrast, direct mail totals a mere 17%8. E-commerce as a share of total retail spend

increased from 4.8% in 2011 to 8.0% in 2016. As a result, the share of US

advertising spend devoted to print has fallen 3.5% during that time.

Table 8 - Revenue of Direct Mail Advertising

Source: Statista, US Census Bureau

7 32223 Office Stationery Manufacturing in the US, IBISWorld 8 http://www.ccfi.asso.fr/blog/2015/12/third-most-important-ad-medium-in-uk-and-usa-direct-mail/

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

24

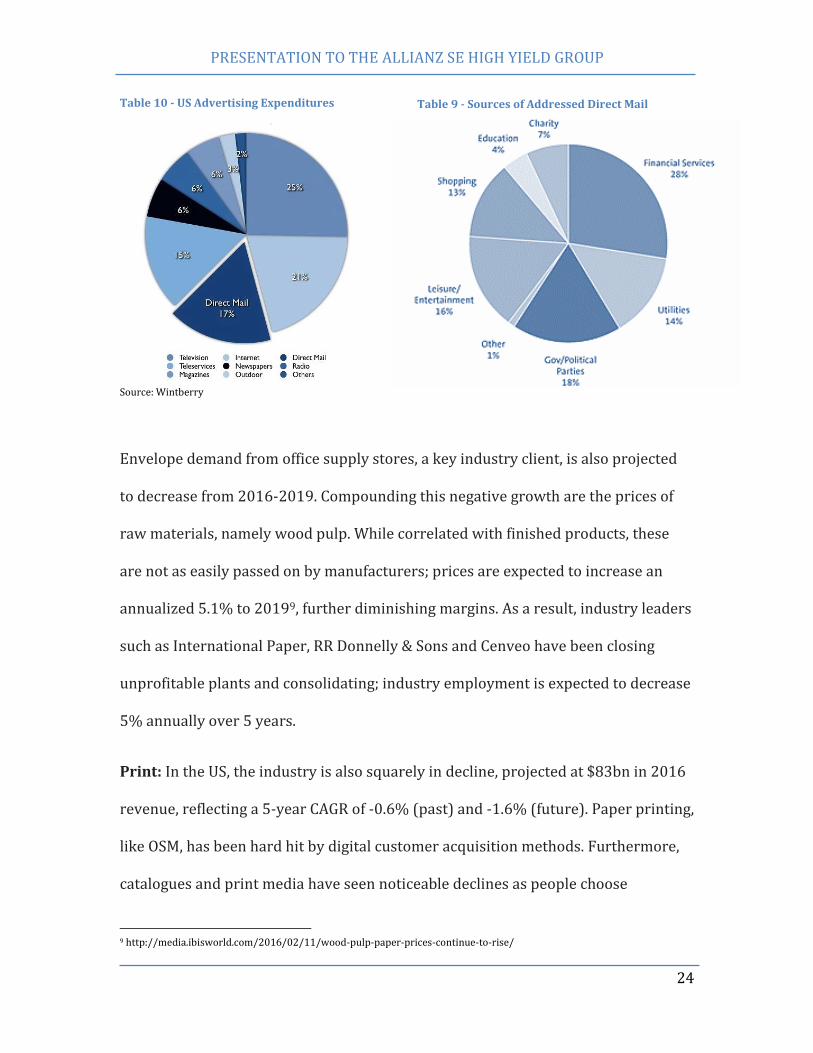

Table 10 - US Advertising Expenditures

Source: Wintberry

Envelope demand from office supply stores, a key industry client, is also projected

to decrease from 2016-2019. Compounding this negative growth are the prices of

raw materials, namely wood pulp. While correlated with finished products, these

are not as easily passed on by manufacturers; prices are expected to increase an

annualized 5.1% to 20199, further diminishing margins. As a result, industry leaders

such as International Paper, RR Donnelly & Sons and Cenveo have been closing

unprofitable plants and consolidating; industry employment is expected to decrease

5% annually over 5 years.

Print: In the US, the industry is also squarely in decline, projected at $83bn in 2016

revenue, reflecting a 5-year CAGR of -0.6% (past) and -1.6% (future). Paper printing,

like OSM, has been hard hit by digital customer acquisition methods. Furthermore,

catalogues and print media have seen noticeable declines as people choose

9 http://media.ibisworld.com/2016/02/11/wood-pulp-paper-prices-continue-to-rise/

Table 9 - Sources of Addressed Direct Mail

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

25

paperless options in a nod to conservation. The sudden demand vacuum has left

excess capacity among the top printers (although their 76% utilization remains

above the 71% manufacturing average10) and resulted in prices averaging an

anemic 0.5% CAGR over the last 5 years.11

To counter these headwinds, printers are attempting to move down the supply

chain to creative and inventory services. Cenveo’s aforementioned Kadena is an

example of this trend, recently signing a 5-year deal to manage National Register

Publishing’s data products (contact lists and museum/financial directories)12;

Cenveo doesn’t release the product’s profitability information, however.

One lone tailwind that may see Cenveo pick up additional clients is the increasing

margin strain affecting newspaper and book publishers. Many of these may be

persuaded to forego the additional investment and outsource their printing needs to

commercial printers such as Cenveo.

PL: PL, unlike OSM and Print, follows consumer purchasing trends, especially in

North America. These have been favorable as of late as North American

consumption recovers from the 2008 recession. The pharmaceutical, food, and

military markets remain strong and annual growth in the $7.4bn US industry has

been 3.1% (2011-2016) and projected at 1.4% (2016-2021)13. Operations have

benefited from the technology boom as processes, especially in labeling, have

10 ISM Q4 2015 Report, U.S. Census Bureau 11 IBISWorld, Printing in the US Industry report, 2016. Bureau of Labor Statistics 12 http://www.prnewswire.com/news-releases/cenveo-announces-five-year-partnership-with-national-register-publishing-300228964.html 13 56191 Packaging & Labeling services in the US, IBISWorld

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

26

become more automated. Such processes often require outsourcing to PL firms in an

arrangement called contract packaging, which is used by cosmetic and

pharmaceutical companies. The high level of automation leads to lower labor costs.

Larger producers do have scale advantages, however label capital intensity remains

below the overall economy and barriers to entry are low. Population trends and

increased pharmaceutical regulation have also worked in the industry’s favor.

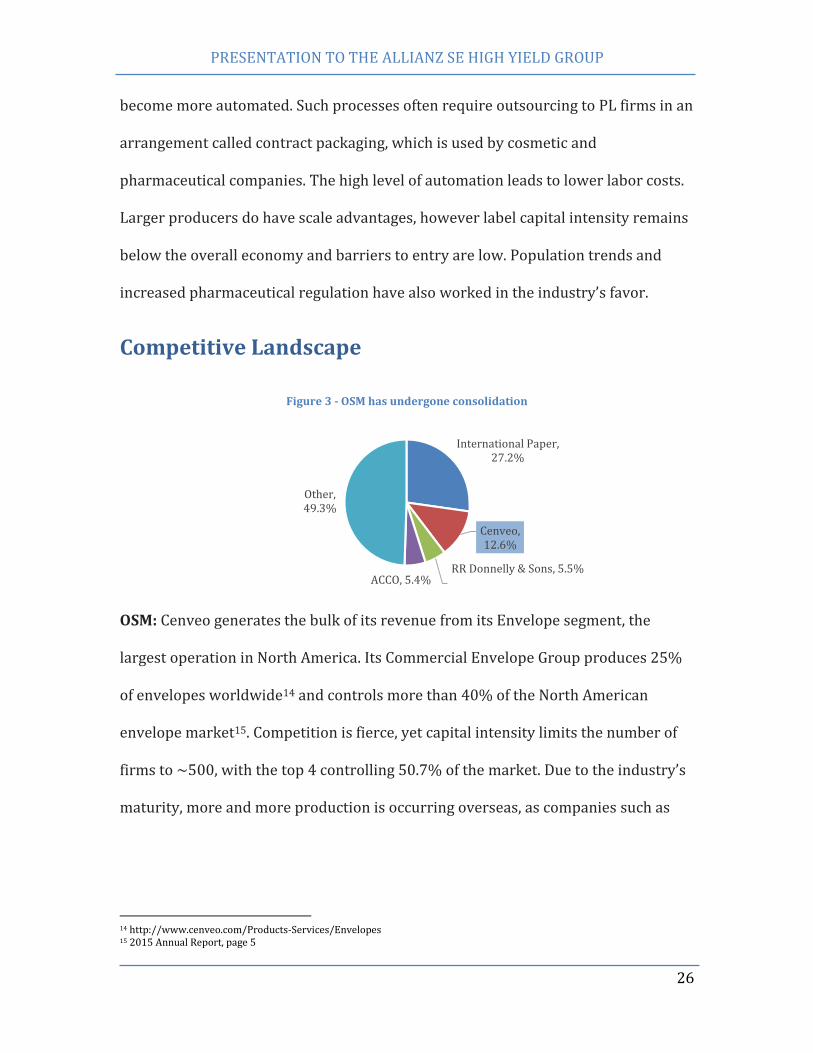

Competitive Landscape

OSM: Cenveo generates the bulk of its revenue from its Envelope segment, the

largest operation in North America. Its Commercial Envelope Group produces 25%

of envelopes worldwide14 and controls more than 40% of the North American

envelope market15. Competition is fierce, yet capital intensity limits the number of

firms to ~500, with the top 4 controlling 50.7% of the market. Due to the industry’s

maturity, more and more production is occurring overseas, as companies such as

14 http://www.cenveo.com/Products-Services/Envelopes 15 2015 Annual Report, page 5

Figure 3 - OSM has undergone consolidation

International Paper, 27.2%

Cenveo, 12.6%

RR Donnelly & Sons, 5.5% ACCO, 5.4%

Other, 49.3%

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

27

International Paper look for growth and lower costs in Brazil and China. The

appreciation of the dollar has hurt exports, however.

Cenveo’s biggest Envelope competitors are RR Donnelly, ACCO, Supremex, and

International Paper. RR Donnelly in particular is structured quite similarly to

Cenveo, with both OSM and Commercial Print operations. However, RR Donnelly is

splitting into 3 separate businesses to free up higher-growth divisions; a restrictive

capital structure and debt covenants limit Cenveo’s annual capital expenditure to

$45mm. Its competitors haven’t pulled back, though: ACCO acquired

MeadWestvaco’s Office Products division (2012, $860mm) and RR Donnelly

acquired Esselte’s North American operations (2014, $97mm).

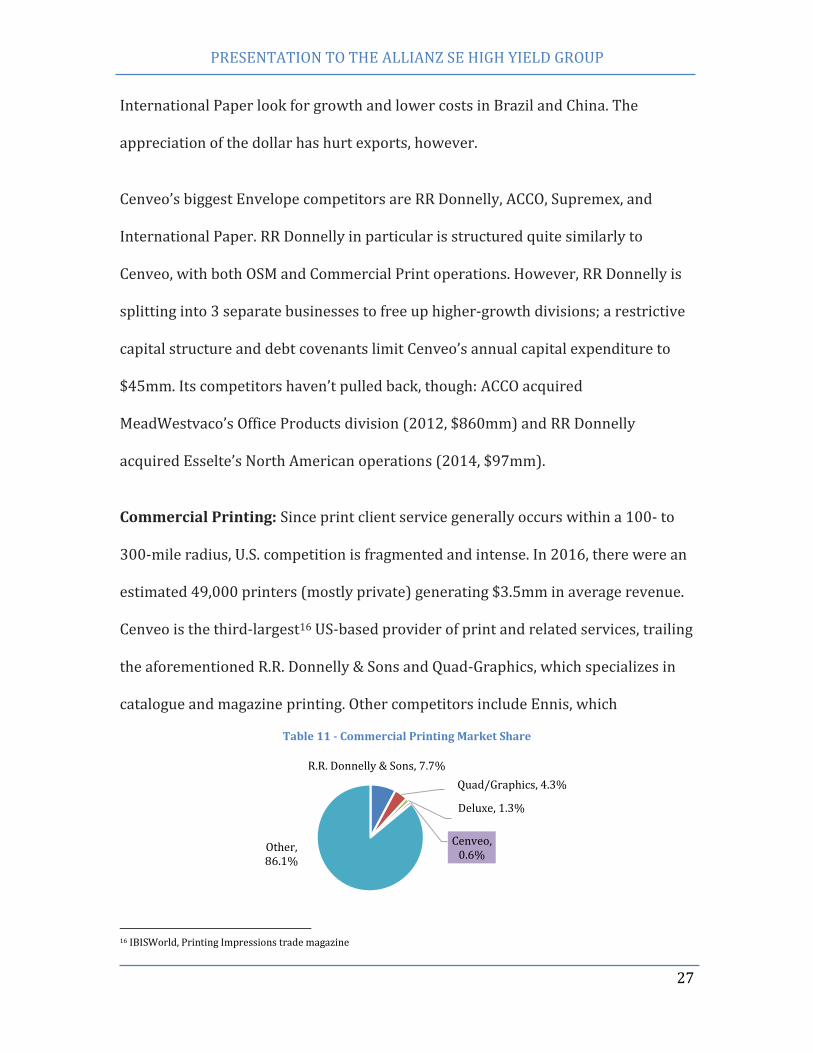

Commercial Printing: Since print client service generally occurs within a 100- to

300-mile radius, U.S. competition is fragmented and intense. In 2016, there were an

estimated 49,000 printers (mostly private) generating $3.5mm in average revenue.

Cenveo is the third-largest16 US-based provider of print and related services, trailing

the aforementioned R.R. Donnelly & Sons and Quad-Graphics, which specializes in

catalogue and magazine printing. Other competitors include Ennis, which

16 IBISWorld, Printing Impressions trade magazine

R.R. Donnelly & Sons, 7.7%

Quad/Graphics, 4.3%

Deluxe, 1.3%

Cenveo, 0.6%

Other, 86.1%

Table 11 - Commercial Printing Market Share

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

28

specializes in advertising and business forms, and Deluxe, which controls over 50%

of the U.S. check-printing market.17

Fragmentation has led to an uptick in M&A: RR Donnelly acquired Consolidated

Graphics (2014, $620mm)18 to bolster print market share and Quad/Graphics

acquired Brown Printing (2014, $100mm)19 to expand its magazine capabilities.

PL: Cenveo’s decision to sell its packaging business to WestRock (2016, $105mm)

was a conscious pivot out of the packaging component of PL. The Company remains,

however, the largest North American pharmacy prescription label manufacturer.

PL’s main player is packaging giant Sonoco, which controls 21.1% of the market.

Other competitors include Berkeley (cosmetic packaging) and Aldelano (display.

While industry experts expect consolidation in the label space, there hasn’t been

much significant activity other than CCL’s acquisitions of Worldmark (2015,

$191mm) and Avery Dennison OCP (2013, $500mm) and Sonoco’s acquisition of

Tegrant (2011, $550mm).

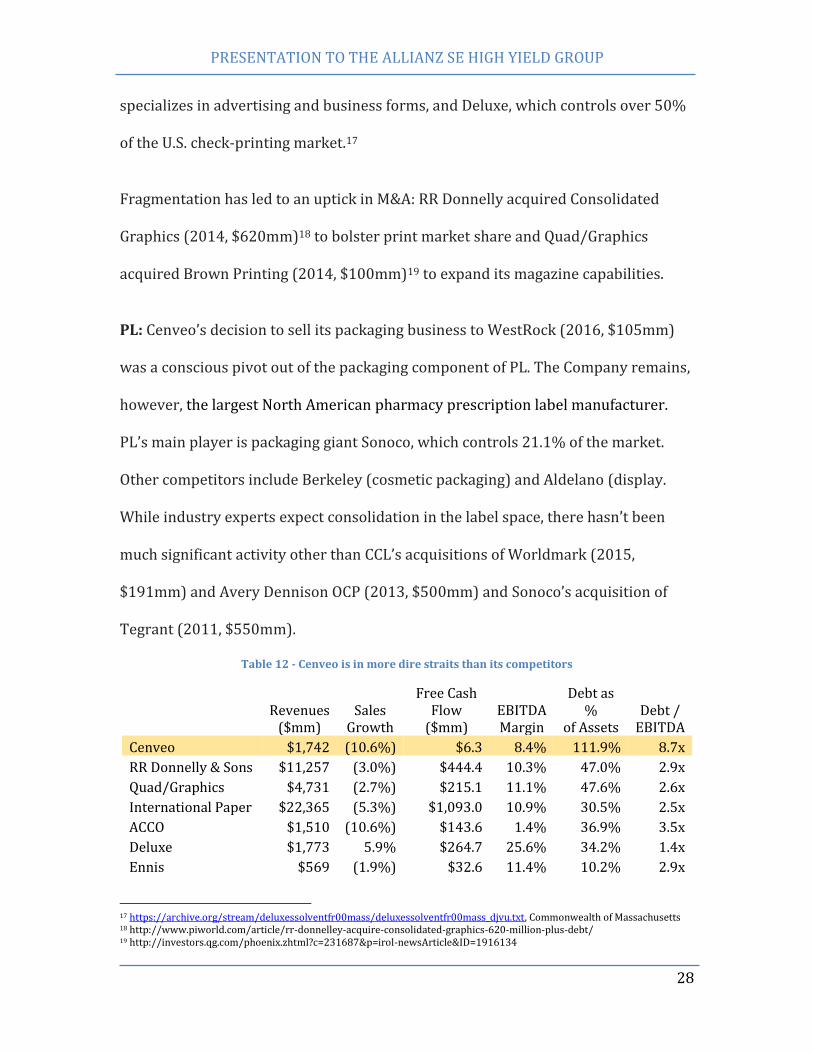

Table 12 - Cenveo is in more dire straits than its competitors

Revenues

($mm) Sales

Growth

Free Cash Flow

($mm) EBITDA Margin

Debt as %

of Assets Debt /

EBITDA

Cenveo $1,742 (10.6%) $6.3 8.4% 111.9% 8.7x

RR Donnelly & Sons $11,257 (3.0%) $444.4 10.3% 47.0% 2.9x

Quad/Graphics $4,731 (2.7%) $215.1 11.1% 47.6% 2.6x

International Paper $22,365 (5.3%) $1,093.0 10.9% 30.5% 2.5x

ACCO $1,510 (10.6%) $143.6 1.4% 36.9% 3.5x

Deluxe $1,773 5.9% $264.7 25.6% 34.2% 1.4x

Ennis $569 (1.9%) $32.6 11.4% 10.2% 2.9x

17 https://archive.org/stream/deluxessolventfr00mass/deluxessolventfr00mass_djvu.txt, Commonwealth of Massachusetts 18 http://www.piworld.com/article/rr-donnelley-acquire-consolidated-graphics-620-million-plus-debt/ 19 http://investors.qg.com/phoenix.zhtml?c=231687&p=irol-newsArticle&ID=1916134

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

29

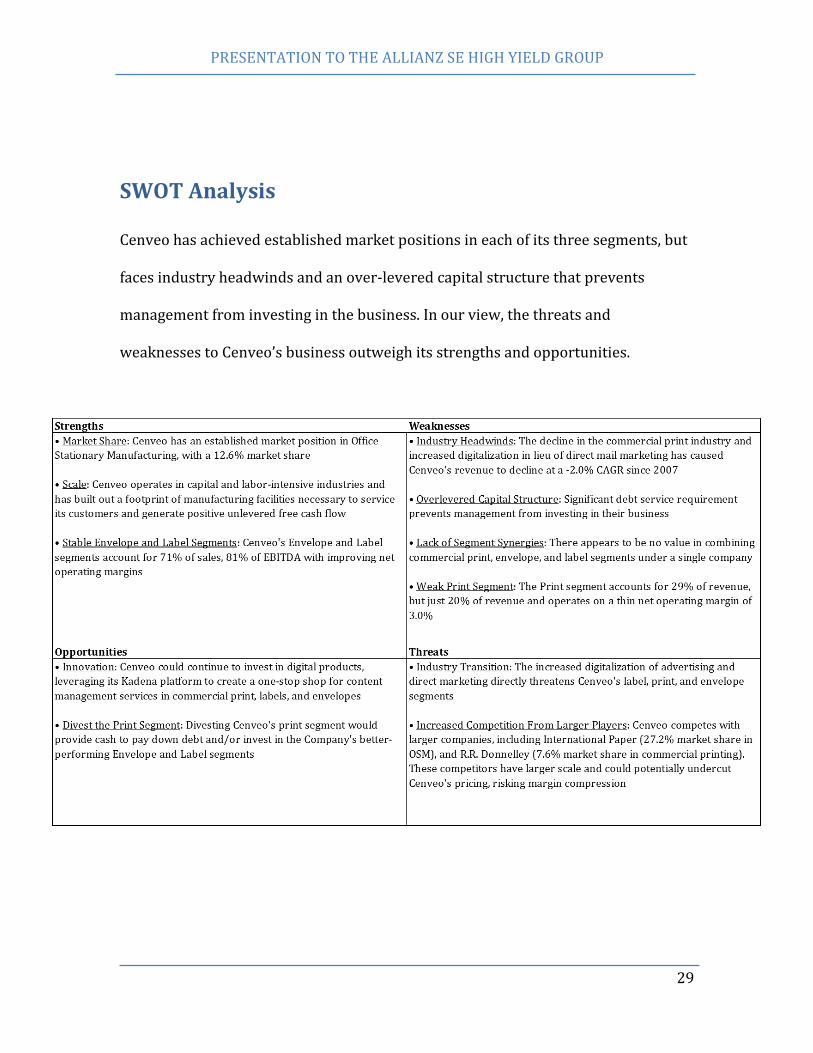

SWOT Analysis

Cenveo has achieved established market positions in each of its three segments, but

faces industry headwinds and an over-levered capital structure that prevents

management from investing in the business. In our view, the threats and

weaknesses to Cenveo’s business outweigh its strengths and opportunities.

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

30

Valuation

To value Cenveo, we used the following methods: discounted cash flow analysis

(Gordon Growth and Terminal Value Methods), publicly traded comparables,

precedent transaction analysis, a sum-of-the-parts analysis, and historical prices. As

exhibited below, these four methods result in a mean and median enterprise value /

2015 EBITDA multiple of 7.1x and 6.9x, respectively, and a mean and median

enterprise value / est. 2016 EBITDA multiple of 7.4x and 6.9x, respectively. These

various valuation methods lead us to conclude that Cenveo’s enterprise value is

approximately $910mm, or 7.0x est. 2016 EBITDA of $130mm, on a run-rate basis.

Discounted Cash Flow Analysis

We used two discounted cash flow methods, the Gordon Growth Model and the

Terminal Multiple Method, to estimate Cenveo’s current value based on discounting

6.0x5.4x

7.0x6.7x

8.3x

9.1x

6.6x5.9x

7.0x6.7x

9.1x 9.1x

0.0x

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x

7.0x

8.0x

9.0x

10.0x

DCF - TerminalMultiple

DCF - GordonGrowth

Publicly TradedComps

PrecedentTransactions

Sum-of-the-parts Historical Prices

Enterprise Value / EBITDA

EV / 2015 EBITDA EV / 2016 est. EBITDA

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

31

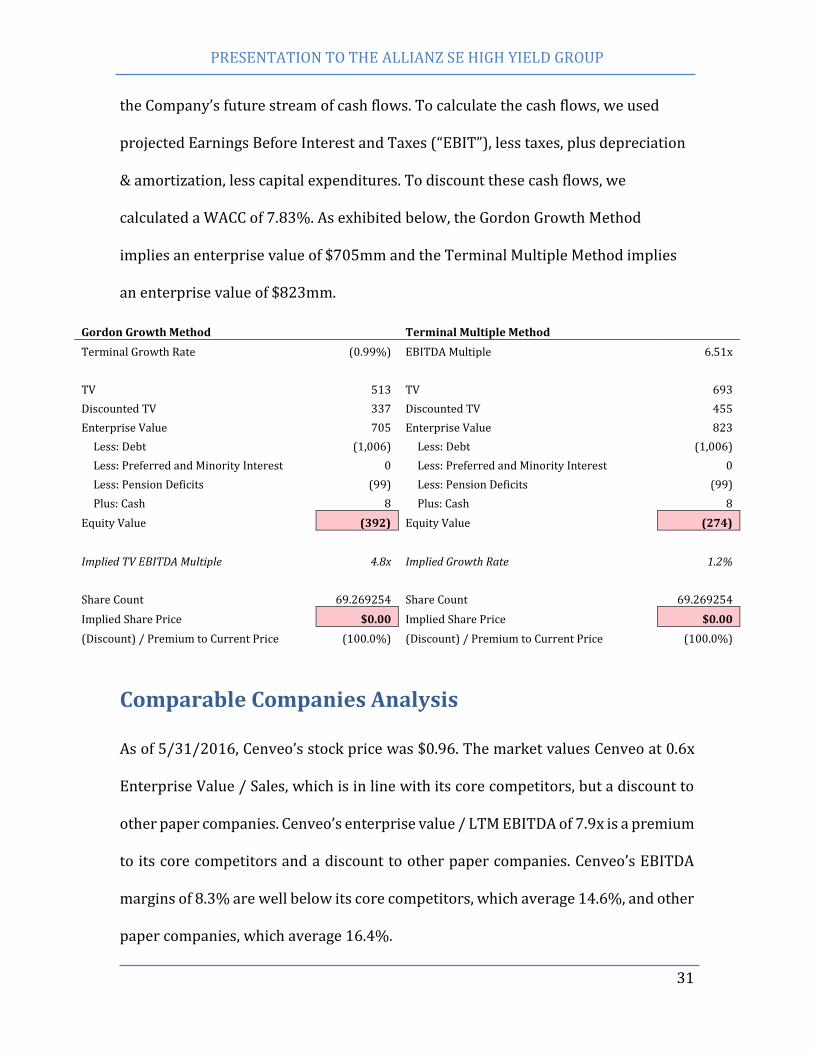

the Company’s future stream of cash flows. To calculate the cash flows, we used

projected Earnings Before Interest and Taxes (“EBIT”), less taxes, plus depreciation

& amortization, less capital expenditures. To discount these cash flows, we

calculated a WACC of 7.83%. As exhibited below, the Gordon Growth Method

implies an enterprise value of $705mm and the Terminal Multiple Method implies

an enterprise value of $823mm.

Gordon Growth Method Terminal Multiple Method

Terminal Growth Rate (0.99%) EBITDA Multiple 6.51x

TV 513 TV 693

Discounted TV 337 Discounted TV 455

Enterprise Value 705 Enterprise Value 823

Less: Debt (1,006) Less: Debt (1,006)

Less: Preferred and Minority Interest 0 Less: Preferred and Minority Interest 0

Less: Pension Deficits (99) Less: Pension Deficits (99)

Plus: Cash 8 Plus: Cash 8

Equity Value (392) Equity Value (274)

Implied TV EBITDA Multiple 4.8x Implied Growth Rate 1.2%

Share Count 69.269254 Share Count 69.269254

Implied Share Price $0.00 Implied Share Price $0.00

(Discount) / Premium to Current Price (100.0%) (Discount) / Premium to Current Price (100.0%)

Comparable Companies Analysis

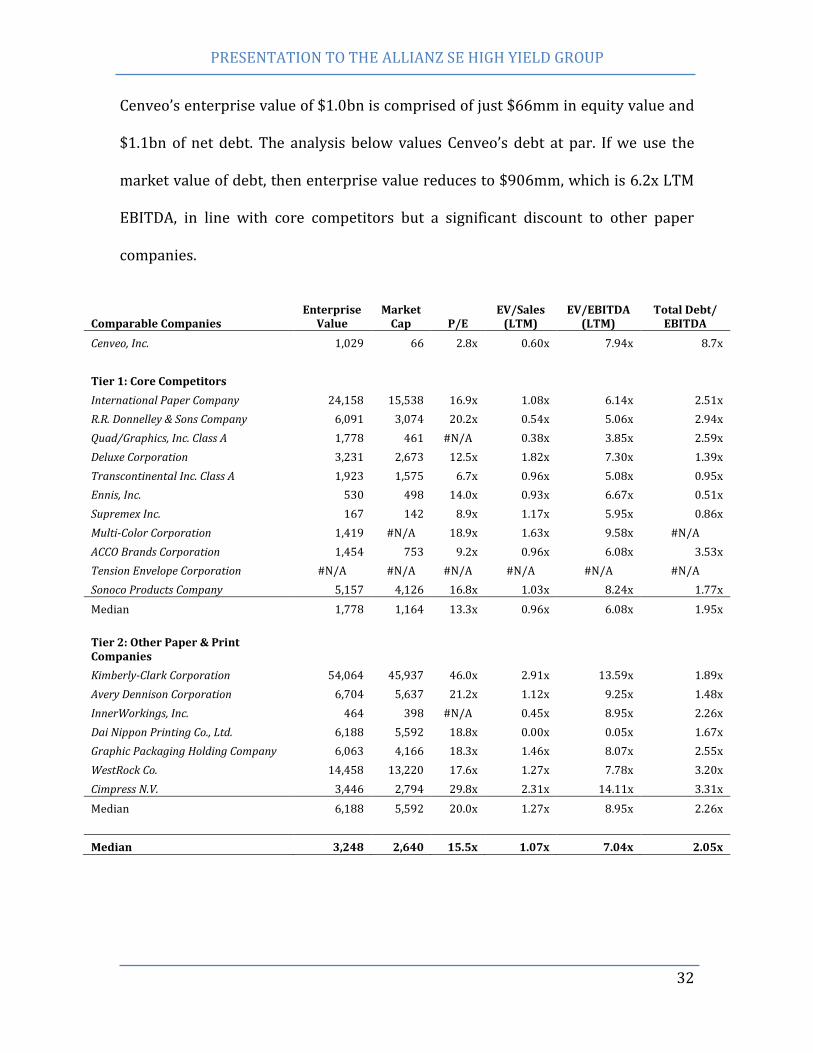

As of 5/31/2016, Cenveo’s stock price was $0.96. The market values Cenveo at 0.6x

Enterprise Value / Sales, which is in line with its core competitors, but a discount to

other paper companies. Cenveo’s enterprise value / LTM EBITDA of 7.9x is a premium

to its core competitors and a discount to other paper companies. Cenveo’s EBITDA

margins of 8.3% are well below its core competitors, which average 14.6%, and other

paper companies, which average 16.4%.

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

32

Cenveo’s enterprise value of $1.0bn is comprised of just $66mm in equity value and

$1.1bn of net debt. The analysis below values Cenveo’s debt at par. If we use the

market value of debt, then enterprise value reduces to $906mm, which is 6.2x LTM

EBITDA, in line with core competitors but a significant discount to other paper

companies.

Comparable Companies Enterprise

Value Market

Cap P/E EV/Sales

(LTM) EV/EBITDA

(LTM) Total Debt/

EBITDA

Cenveo, Inc. 1,029 66 2.8x 0.60x 7.94x 8.7x

Tier 1: Core Competitors

International Paper Company 24,158 15,538 16.9x 1.08x 6.14x 2.51x

R.R. Donnelley & Sons Company 6,091 3,074 20.2x 0.54x 5.06x 2.94x

Quad/Graphics, Inc. Class A 1,778 461 #N/A 0.38x 3.85x 2.59x

Deluxe Corporation 3,231 2,673 12.5x 1.82x 7.30x 1.39x

Transcontinental Inc. Class A 1,923 1,575 6.7x 0.96x 5.08x 0.95x

Ennis, Inc. 530 498 14.0x 0.93x 6.67x 0.51x

Supremex Inc. 167 142 8.9x 1.17x 5.95x 0.86x

Multi-Color Corporation 1,419 #N/A 18.9x 1.63x 9.58x #N/A

ACCO Brands Corporation 1,454 753 9.2x 0.96x 6.08x 3.53x

Tension Envelope Corporation #N/A #N/A #N/A #N/A #N/A #N/A

Sonoco Products Company 5,157 4,126 16.8x 1.03x 8.24x 1.77x

Median 1,778 1,164 13.3x 0.96x 6.08x 1.95x

Tier 2: Other Paper & Print Companies

Kimberly-Clark Corporation 54,064 45,937 46.0x 2.91x 13.59x 1.89x

Avery Dennison Corporation 6,704 5,637 21.2x 1.12x 9.25x 1.48x

InnerWorkings, Inc. 464 398 #N/A 0.45x 8.95x 2.26x

Dai Nippon Printing Co., Ltd. 6,188 5,592 18.8x 0.00x 0.05x 1.67x

Graphic Packaging Holding Company 6,063 4,166 18.3x 1.46x 8.07x 2.55x

WestRock Co. 14,458 13,220 17.6x 1.27x 7.78x 3.20x

Cimpress N.V. 3,446 2,794 29.8x 2.31x 14.11x 3.31x

Median 6,188 5,592 20.0x 1.27x 8.95x 2.26x

Median 3,248 2,640 15.5x 1.07x 7.04x 2.05x

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

33

Publicly traded comparables suggest that Cenveo, as a going concern, should be

valued at 7.0x enterprise value / est. 2016 EBITDA, or $910mm.

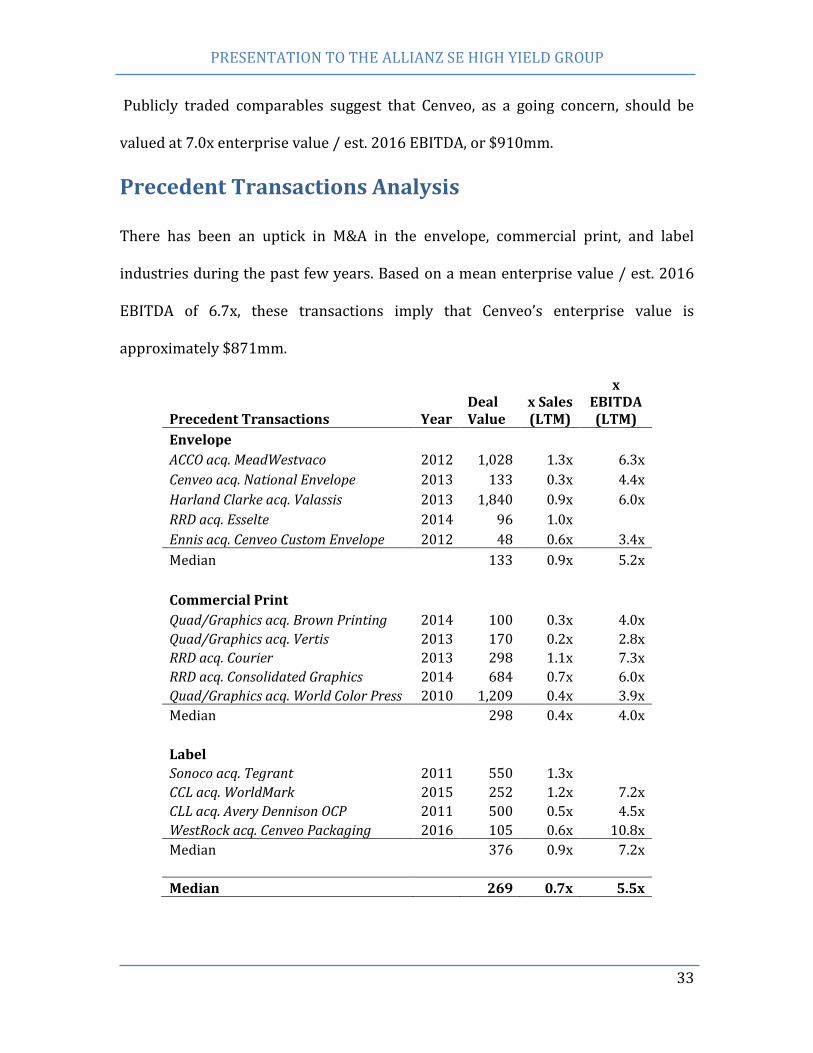

Precedent Transactions Analysis

There has been an uptick in M&A in the envelope, commercial print, and label

industries during the past few years. Based on a mean enterprise value / est. 2016

EBITDA of 6.7x, these transactions imply that Cenveo’s enterprise value is

approximately $871mm.

Precedent Transactions Year Deal Value

x Sales (LTM)

x EBITDA (LTM)

Envelope

ACCO acq. MeadWestvaco 2012 1,028 1.3x 6.3x

Cenveo acq. National Envelope 2013 133 0.3x 4.4x

Harland Clarke acq. Valassis 2013 1,840 0.9x 6.0x

RRD acq. Esselte 2014 96 1.0x

Ennis acq. Cenveo Custom Envelope 2012 48 0.6x 3.4x

Median 133 0.9x 5.2x

Commercial Print

Quad/Graphics acq. Brown Printing 2014 100 0.3x 4.0x

Quad/Graphics acq. Vertis 2013 170 0.2x 2.8x

RRD acq. Courier 2013 298 1.1x 7.3x

RRD acq. Consolidated Graphics 2014 684 0.7x 6.0x

Quad/Graphics acq. World Color Press 2010 1,209 0.4x 3.9x

Median 298 0.4x 4.0x

Label

Sonoco acq. Tegrant 2011 550 1.3x

CCL acq. WorldMark 2015 252 1.2x 7.2x

CLL acq. Avery Dennison OCP 2011 500 0.5x 4.5x

WestRock acq. Cenveo Packaging 2016 105 0.6x 10.8x

Median 376 0.9x 7.2x

Median 269 0.7x 5.5x

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

34

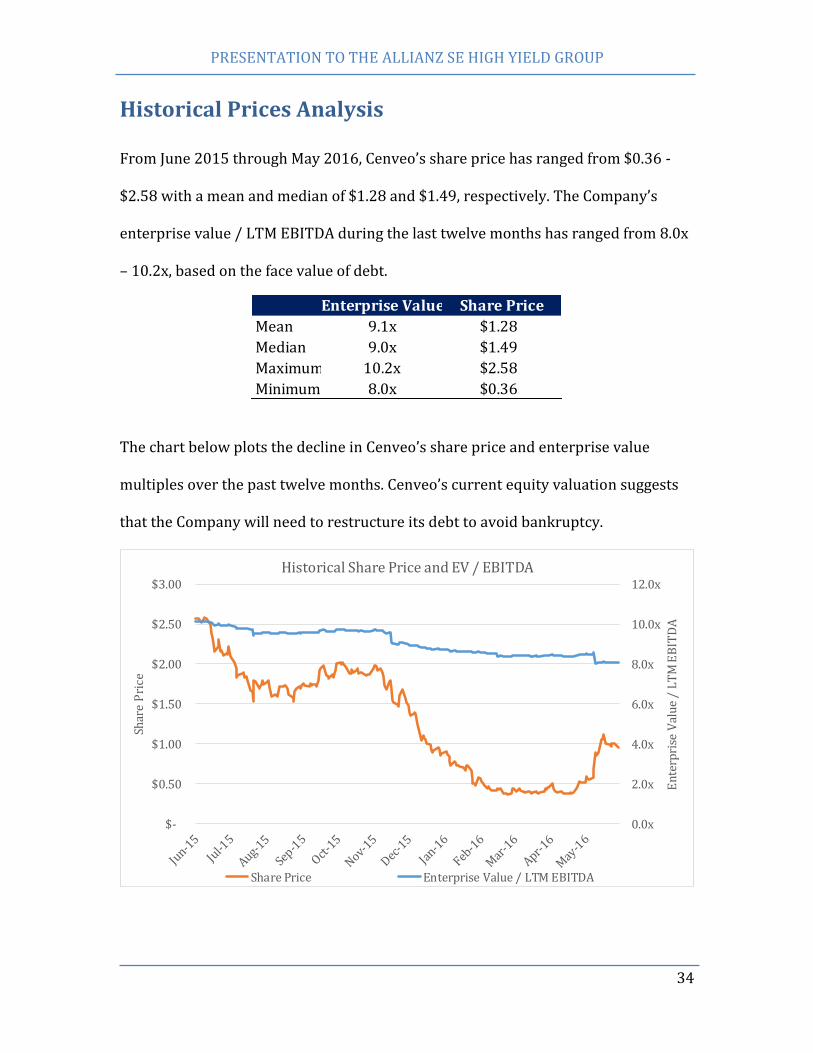

Historical Prices Analysis

From June 2015 through May 2016, Cenveo’s share price has ranged from $0.36 -

$2.58 with a mean and median of $1.28 and $1.49, respectively. The Company’s

enterprise value / LTM EBITDA during the last twelve months has ranged from 8.0x

– 10.2x, based on the face value of debt.

The chart below plots the decline in Cenveo’s share price and enterprise value

multiples over the past twelve months. Cenveo’s current equity valuation suggests

that the Company will need to restructure its debt to avoid bankruptcy.

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

$-

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

En

terp

rise

Val

ue

/ L

TM

EB

ITD

A

Shar

e P

rice

Historical Share Price and EV / EBITDA

Share Price Enterprise Value / LTM EBITDA

Enterprise Value Share Price

Mean 9.1x $1.28

Median 9.0x $1.49

Maximum 10.2x $2.58

Minimum 8.0x $0.36

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

35

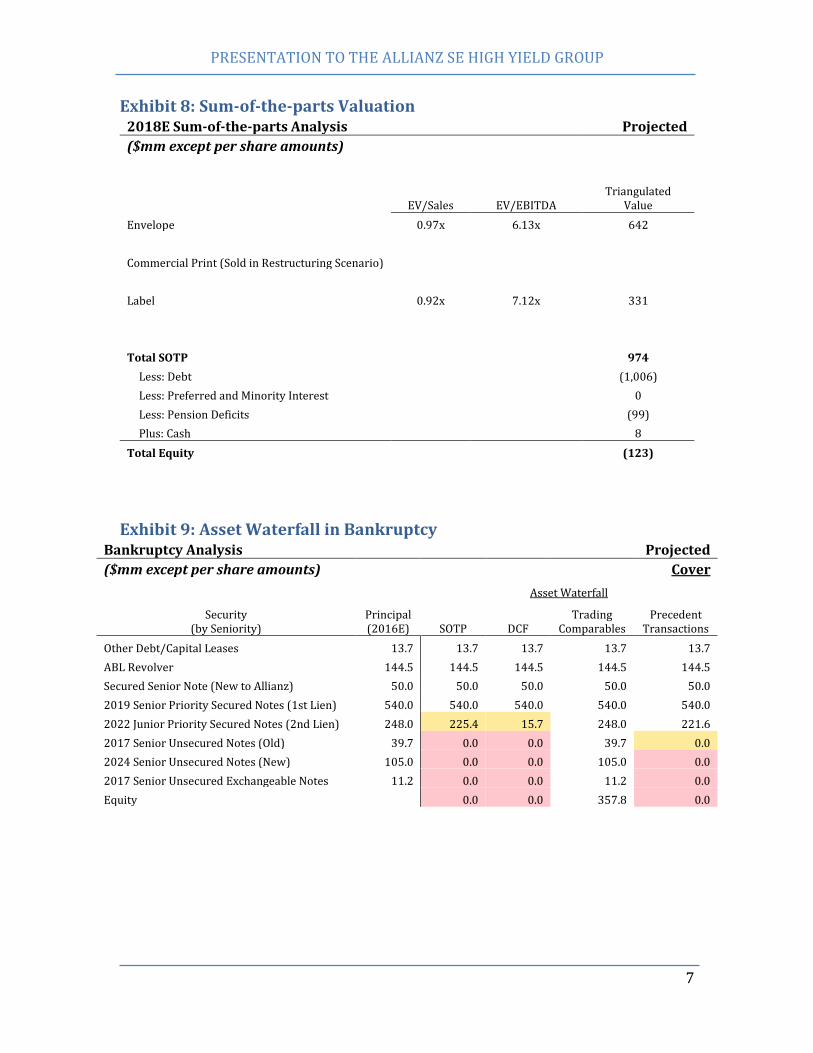

Sum-of-the-Parts Analysis

Cenveo operates three distinct segments: envelope, commercial print, and label, each

with their own intrinsic value. Therefore, we thought it useful to conduct a sum-of-

the-parts analysis on each segment. We valued the envelope segment at 6.1x

enterprise value / EBITDA and the label segment at 8.9x enterprise value / EBITDA.

We recommend divesting the commercial print segment, which we believe would

yield a sale price of $146mm, or 4.9x estimated 2016 commercial print segment

EBITDA of $30mm. Adding up the value of each segment yields an implied enterprise

value of $1.2bn, or 9.1x enterprise value / est. 2016 EBITDA.

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

36

Plan of Reorganization

Key Challenges to Financial Restructuring While Allianz is invested throughout the capital structure,20 some its largest

positions are in second lien and unsecured debt. We believe that liquidation under

Chapter 11 would significantly jeopardize Allianz’s more-junior positions. Allianz

would be better able to negotiate more equity for its junior debt by leveraging its

current investment in Cenveo rather than negotiating with senior creditors during

bankruptcy.

First Lien Creditors - Allianz’s loan-to-own strategy must address the

conflict that often arises between senior creditors, who may be more inclined

to impose liquidation, and junior creditors, who hope to receive equity in the

restructured company. In Cenveo’s case, first lien creditors have significant

bargaining power because they are covered in a liquidation scenario based

on our valuation in addition to holding the nearest maturity. With significant

concentrations of second lien and unsecured notes, Allianz would likely cede

any influence it had over the reorganization process to the first lien holders

in a Chapter 11 scenario.21

Second Lien Creditors – Allianz must convince the remaining second lien

creditors who may believe that they will receive a better package in Chapter

20 Its $50mm Secured Note is classified as an ABL 21 Academic research shows that, for companies reorganizing in bankruptcy, senior creditors exhibit “pervasive” control through the reorganization process with equity-holders and managers exerting little to no leverage. However, the “zone of insolvency” theory has been recently by Delaware Chancery courts. Cenveo is incorporated in Colorado. “Creditor Control and Conflict in Chapter 11”, Kenneth Ayotte and Edward Morrison, 2009

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

37

11, especially if they become the fulcrum security. In bankruptcy, second lien

holders will not be inclined to distribute a significant amount of equity to

creditors holding unsecured debt, of which Allianz owns ~$72mm.

Cenveo Management/Board - The Burton family still has significant control

over Cenveo operations, including whether to sell existing business lines or

how best to pay back its creditors. They also present legal risks to Allianz.

Holders of distressed debt acquired in the open market are increasingly

becoming the target of litigation for fraudulent transfer/preference claims,

recharacterization of debt to equity, equitable subordination and breach of

fiduciary duty22.

Board Control

Key to any reorganization will be Allianz’s ability to influence the process,

potentially contrary to the wishes of the current Burton-controlled board. It is thus

essential that Allianz seek control in 2 ways:

1.

a. Ally with creditors that have significant equity stakes. Hedge fund

Rotation Capital Management is an example of such a holder, with

6.1% equity. These creditors likely wish to see a swift and sustainable

resolution to debt issues, which is one of the reasons they may have

purchased an equity stake in the first place. They are also likely to

22 The pending bankruptcy of The Dolan Company in Delaware demonstrates how an equity committee can hold up the process by claiming the “excessive fees,” “reduced availability,” “management control” and “lender coercion” on the part of creditors. http://www.natlawreview.com/article/attacks-loan-to-own-strategies-continue

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

38

have purchased their position below par, which would make them

more likely to agree to a quick, painless restructuring to ensure

profitable exit.

b. Exercise its warrants and purchase equity on the open market. With

warrants struck at approximately $0.50 above market price, it would

cost Allianz an additional $4.3mm to achieve its 28.4% stake. That

plus Rotation’s portion leaves ~14% equity to achieve a majority

equity position, which can be had at a minimal cost given recent stock

declines.

2. Given Allianz’s past cordial relationship with the Burtons (as demonstrated

by its most recent debt exchange), we believe a more likely scenario is a

Burton family more amenable to Allianz recommendations as they recognize

the inevitable restructuring. In return, Allianz can offer a minimal post-

restructuring portion of the equity (less than it would cost them in option

#1). Furthermore, our recommendation would likely pass the “business

judgment” test required by a board’s fiduciary standard.

Operational Improvements

Once Allianz board control is secure, there are 3 operational improvements to

achieve:

1. Management led by Robert Burton has focused on low-growth segments

(envelope, print) in an ‘empire-building’ strategy to achieve rational pricing

and economies of scale. This strategy has been haphazard at best: From

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

39

2005-2011, Cenveo acquired 13 companies with a variety of brands and

niche products to “enhance our existing global packaging network” and

“expand our reach.23” The Company then turned around and sold those

businesses to “focus on core operations.” Burton also divested segments like

Custom Envelope to a competitor (Ennis) in 2012 only to rebuild virtually

the same group in-house from 2014-2016. In the meantime, Cenveo has

experienced no improved pricing power or margins and the stock has fallen

87%.

We therefore believe this team is not suitable to lead a nimbler Cenveo

focused on higher-growth initiatives. We see a path for sustained growth

through expansion of modern labeling capabilities as well as a transition

from traditional to integrated online-and-mail campaigns. Therefore, we

recommend the Company recruit a new management team familiar with

these ideas. They should also be incentivized with equity post-

recapitalization rather than significant cash payments.

Table 13 - Potential senior executive candidates

Dan Knotts COO, RR Donnelley ● Leads all of RR Donnelley’s

business worldwide ● 30 years of experience in

the industry ● Responsible for global

sales, operations, logistics, and strategic outsourcing

David McRae President, Infogroup ● Leads direct marketing business

and tech solutions ● 20 years of experience in the

industry ● Responsible for building customer

relationships by leveraging marketing, data, and technology

23 http://www.cenveo.com/getattachment/d9f71559-fa17-44fd-a37f-4c11542fee9d/News

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

40

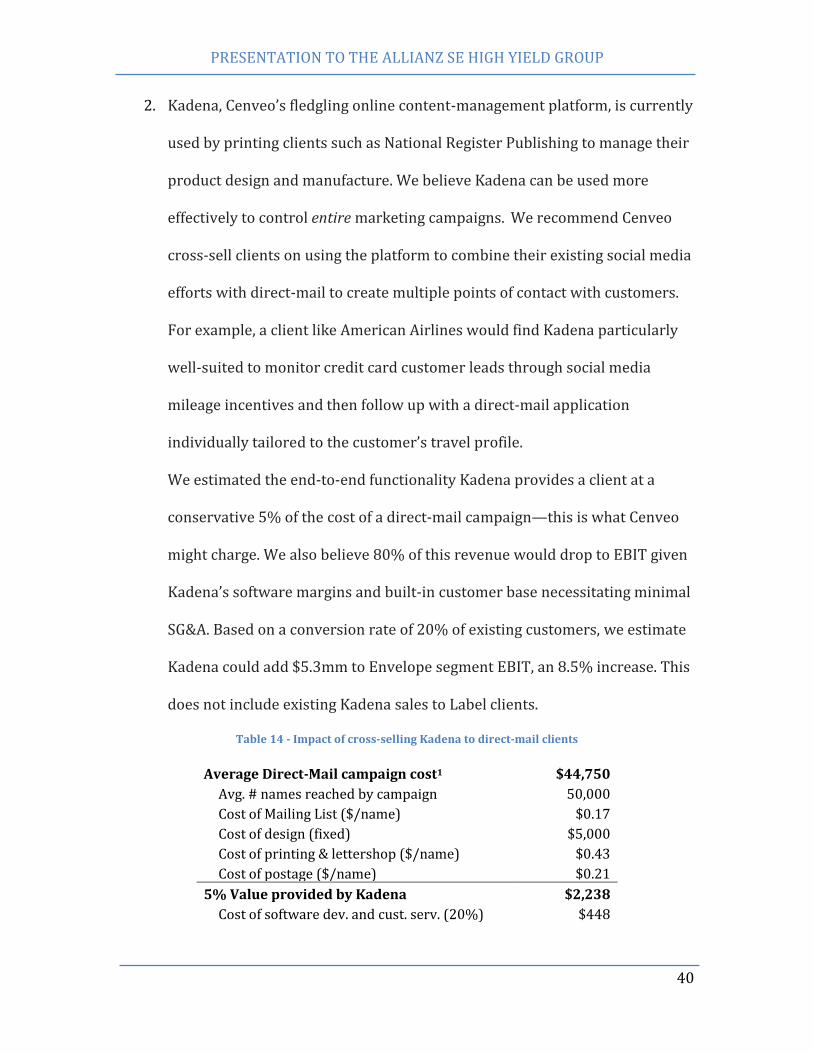

2. Kadena, Cenveo’s fledgling online content-management platform, is currently

used by printing clients such as National Register Publishing to manage their

product design and manufacture. We believe Kadena can be used more

effectively to control entire marketing campaigns. We recommend Cenveo

cross-sell clients on using the platform to combine their existing social media

efforts with direct-mail to create multiple points of contact with customers.

For example, a client like American Airlines would find Kadena particularly

well-suited to monitor credit card customer leads through social media

mileage incentives and then follow up with a direct-mail application

individually tailored to the customer’s travel profile.

We estimated the end-to-end functionality Kadena provides a client at a

conservative 5% of the cost of a direct-mail campaign—this is what Cenveo

might charge. We also believe 80% of this revenue would drop to EBIT given

Kadena’s software margins and built-in customer base necessitating minimal

SG&A. Based on a conversion rate of 20% of existing customers, we estimate

Kadena could add $5.3mm to Envelope segment EBIT, an 8.5% increase. This

does not include existing Kadena sales to Label clients.

Table 14 - Impact of cross-selling Kadena to direct-mail clients

Average Direct-Mail campaign cost1 $44,750

Avg. # names reached by campaign 50,000

Cost of Mailing List ($/name) $0.17

Cost of design (fixed) $5,000

Cost of printing & lettershop ($/name) $0.43

Cost of postage ($/name) $0.21

5% Value provided by Kadena $2,238

Cost of software dev. and cust. serv. (20%) $448

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

41

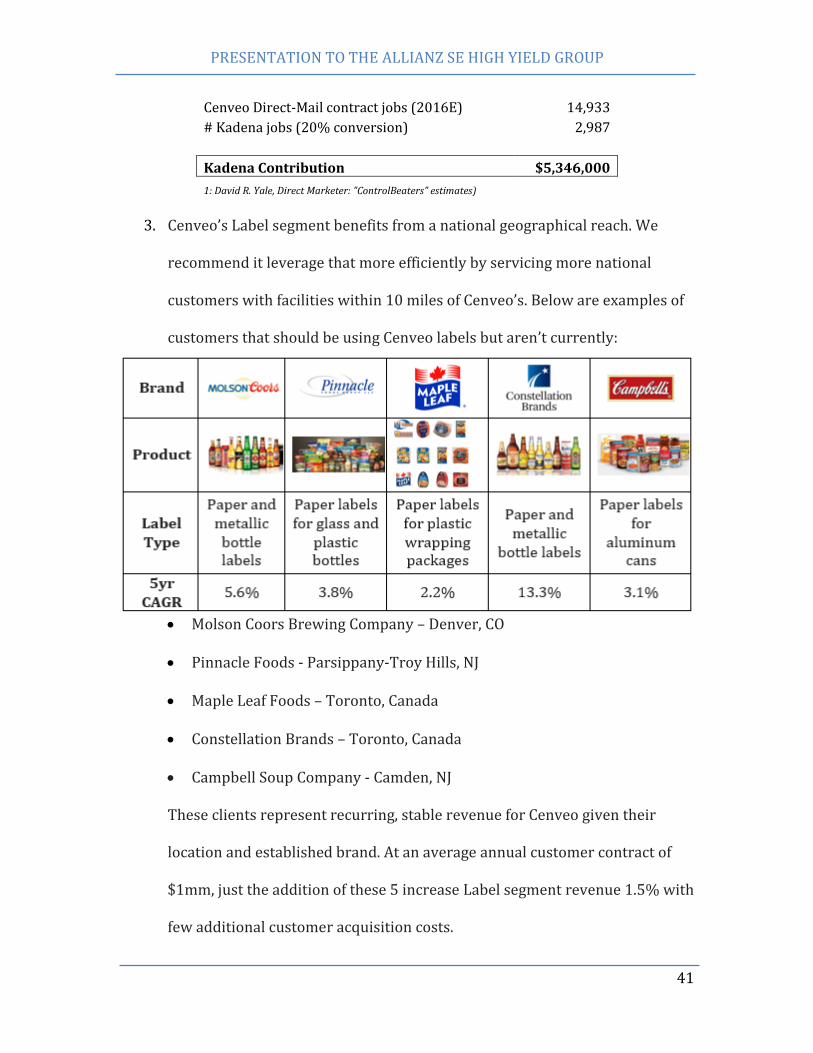

Cenveo Direct-Mail contract jobs (2016E) 14,933

# Kadena jobs (20% conversion) 2,987

Kadena Contribution $5,346,000

1: David R. Yale, Direct Marketer: "ControlBeaters" estimates)

3. Cenveo’s Label segment benefits from a national geographical reach. We

recommend it leverage that more efficiently by servicing more national

customers with facilities within 10 miles of Cenveo’s. Below are examples of

customers that should be using Cenveo labels but aren’t currently:

Molson Coors Brewing Company – Denver, CO

Pinnacle Foods - Parsippany-Troy Hills, NJ

Maple Leaf Foods – Toronto, Canada

Constellation Brands – Toronto, Canada

Campbell Soup Company - Camden, NJ

These clients represent recurring, stable revenue for Cenveo given their

location and established brand. At an average annual customer contract of

$1mm, just the addition of these 5 increase Label segment revenue 1.5% with

few additional customer acquisition costs.

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

42

Acquisitions & Divestments

The Commercial Print division has deteriorated to a greater extent than

Envelope/Label for reasons outlined above. It also has the weakest operating

margins. We therefore believe that, given Cenveo’s lax debt covenants, it is no longer

necessary to keep Print’s EBITDA (with little accompanying cash flow) on the books

purely for leverage ratios. It is important that Cenveo de-lever as soon as possible,

and preferably with the sale of a division in decline and with few areas for growth.

Indeed, throwing good money after bad is one of the reasons for Cenveo’s current

capital structure.

That said, it is important to recognize the synergistic nature of the Print division,

especially through direct-mail inserts that are critical to Envelope clients. Therefore,

Table 15 - Cenveo's national reach should leverage nearby national brands

Molson

Pinnacle

Maple Leaf Constellation

Campbell

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

43

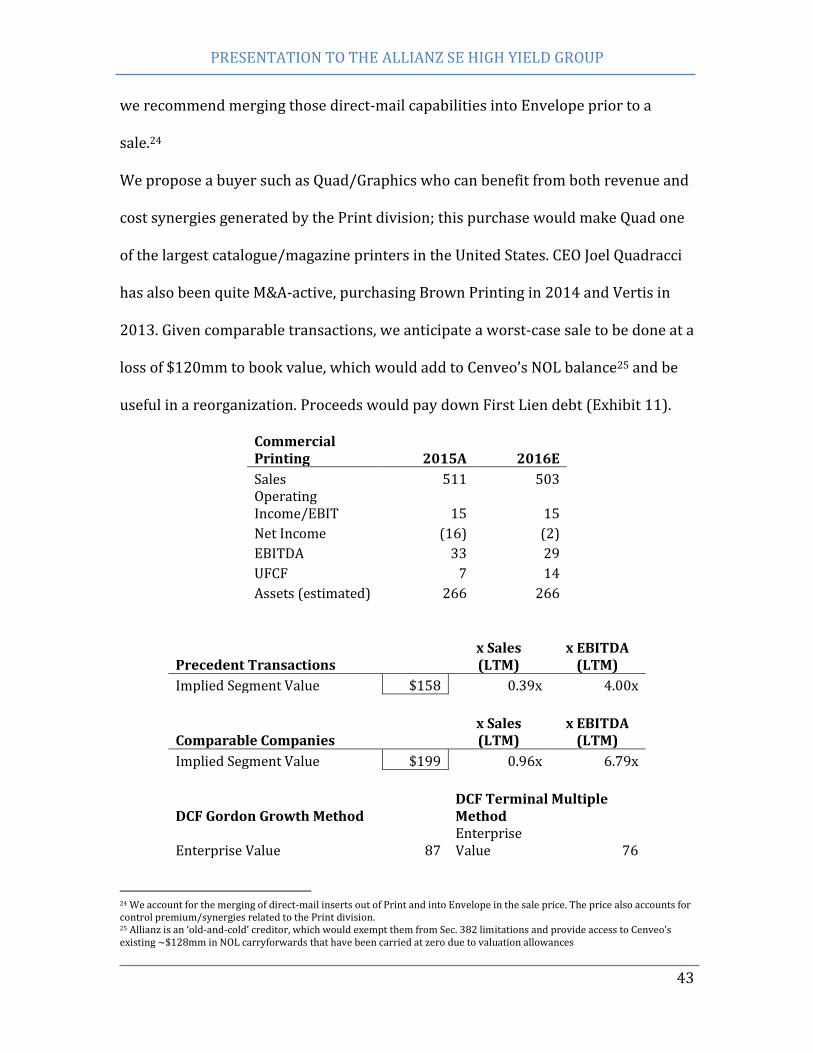

we recommend merging those direct-mail capabilities into Envelope prior to a

sale.24

We propose a buyer such as Quad/Graphics who can benefit from both revenue and

cost synergies generated by the Print division; this purchase would make Quad one

of the largest catalogue/magazine printers in the United States. CEO Joel Quadracci

has also been quite M&A-active, purchasing Brown Printing in 2014 and Vertis in

2013. Given comparable transactions, we anticipate a worst-case sale to be done at a

loss of $120mm to book value, which would add to Cenveo’s NOL balance25 and be

useful in a reorganization. Proceeds would pay down First Lien debt (Exhibit 11).

Commercial Printing 2015A 2016E

Sales 511 503 Operating Income/EBIT 15 15

Net Income (16) (2)

EBITDA 33 29

UFCF 7 14

Assets (estimated) 266 266

Precedent Transactions x Sales (LTM)

x EBITDA (LTM)

Implied Segment Value $158 0.39x 4.00x

Comparable Companies x Sales (LTM)

x EBITDA (LTM)

Implied Segment Value $199 0.96x 6.79x

DCF Gordon Growth Method DCF Terminal Multiple Method

Enterprise Value 87 Enterprise Value 76

24 We account for the merging of direct-mail inserts out of Print and into Envelope in the sale price. The price also accounts for control premium/synergies related to the Print division. 25 Allianz is an ‘old-and-cold’ creditor, which would exempt them from Sec. 382 limitations and provide access to Cenveo’s existing ~$128mm in NOL carryforwards that have been carried at zero due to valuation allowances

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

44

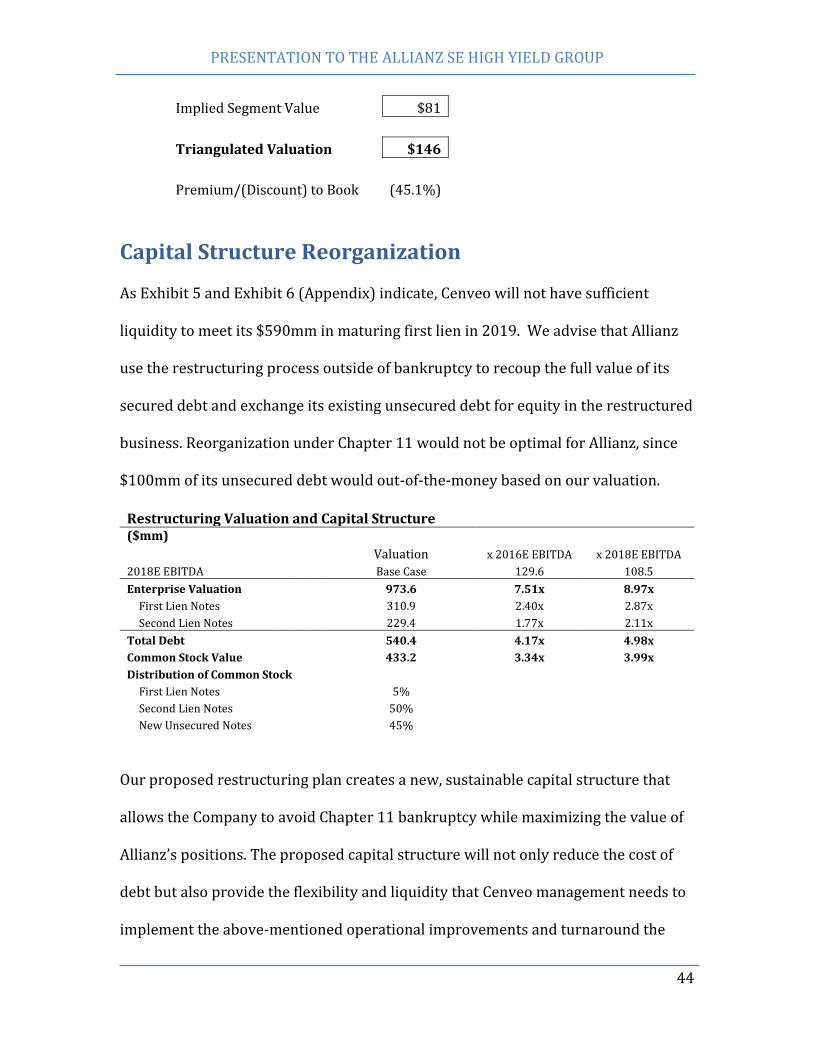

Implied Segment Value $81

Triangulated Valuation $146

Premium/(Discount) to Book (45.1%)

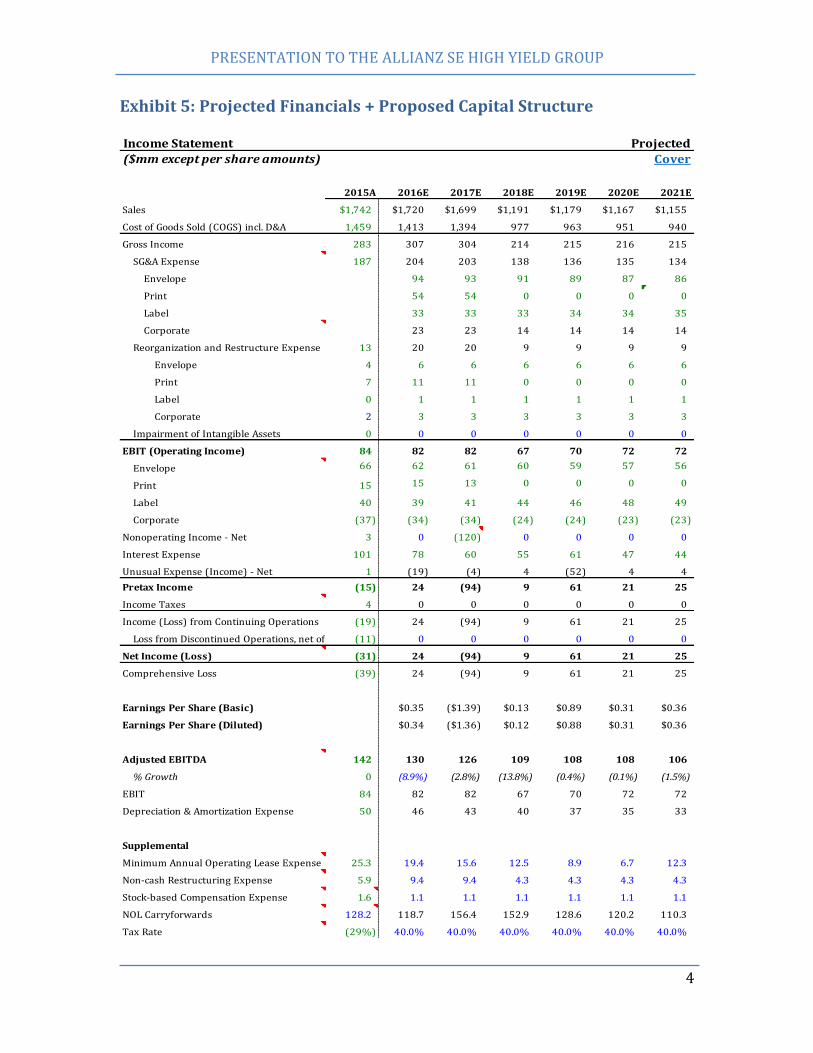

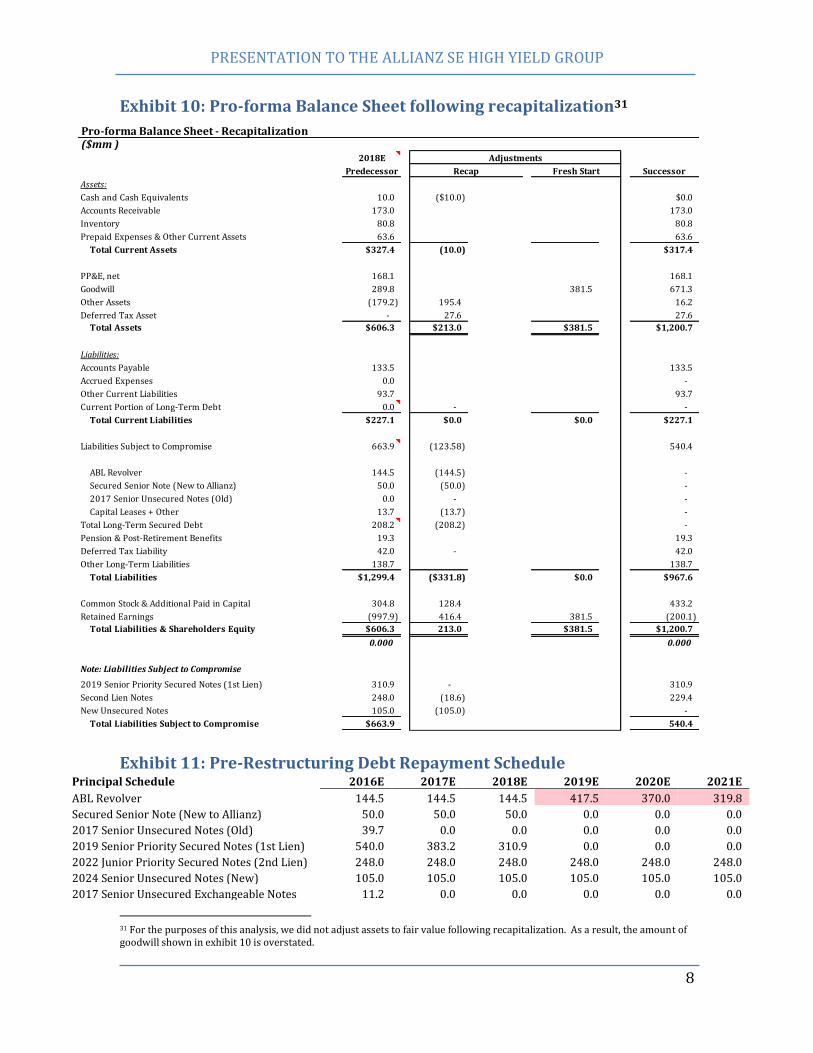

Capital Structure Reorganization As Exhibit 5 and Exhibit 6 (Appendix) indicate, Cenveo will not have sufficient

liquidity to meet its $590mm in maturing first lien in 2019. We advise that Allianz

use the restructuring process outside of bankruptcy to recoup the full value of its

secured debt and exchange its existing unsecured debt for equity in the restructured

business. Reorganization under Chapter 11 would not be optimal for Allianz, since

$100mm of its unsecured debt would out-of-the-money based on our valuation.

Restructuring Valuation and Capital Structure ($mm)

Valuation x 2016E EBITDA x 2018E EBITDA

2018E EBITDA Base Case 129.6 108.5

Enterprise Valuation 973.6 7.51x 8.97x

First Lien Notes 310.9 2.40x 2.87x

Second Lien Notes 229.4 1.77x 2.11x

Total Debt 540.4 4.17x 4.98x

Common Stock Value 433.2 3.34x 3.99x

Distribution of Common Stock

First Lien Notes 5%

Second Lien Notes 50%

New Unsecured Notes 45%

Our proposed restructuring plan creates a new, sustainable capital structure that

allows the Company to avoid Chapter 11 bankruptcy while maximizing the value of

Allianz’s positions. The proposed capital structure will not only reduce the cost of

debt but also provide the flexibility and liquidity that Cenveo management needs to

implement the above-mentioned operational improvements and turnaround the

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

45

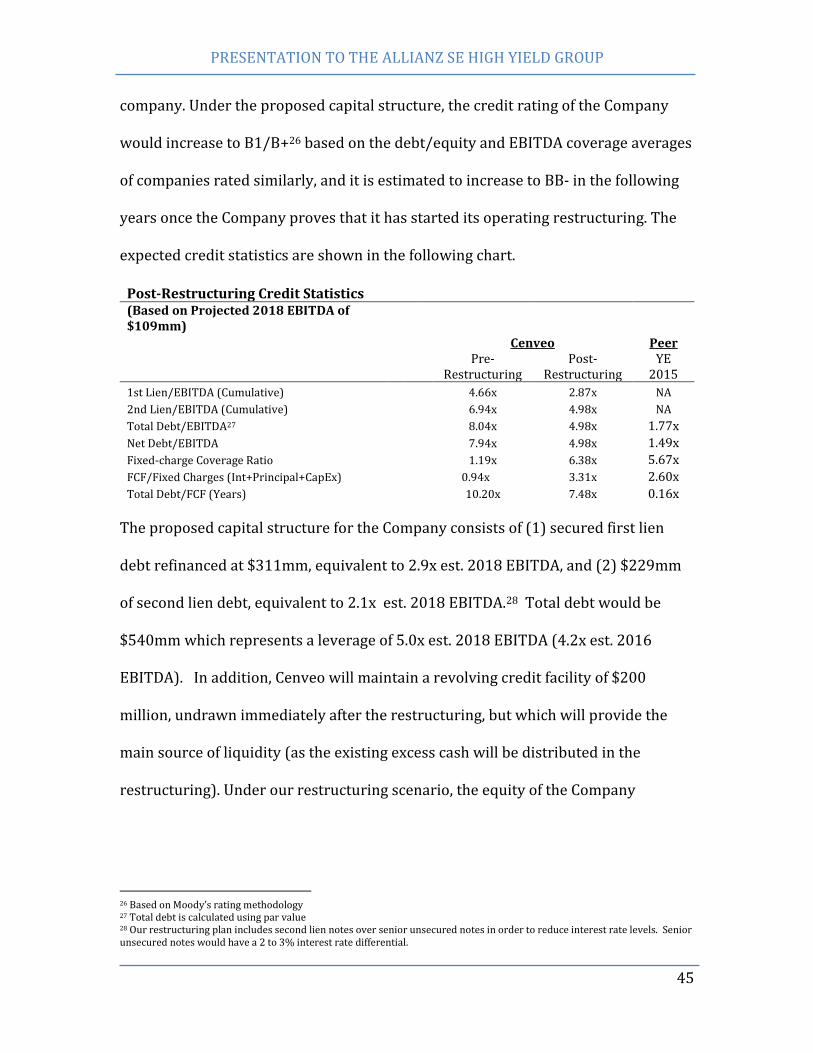

company. Under the proposed capital structure, the credit rating of the Company

would increase to B1/B+26 based on the debt/equity and EBITDA coverage averages

of companies rated similarly, and it is estimated to increase to BB- in the following

years once the Company proves that it has started its operating restructuring. The

expected credit statistics are shown in the following chart.

Post-Restructuring Credit Statistics (Based on Projected 2018 EBITDA of $109mm)

Cenveo Peer

Pre-

Restructuring Post-

Restructuring YE

2015

1st Lien/EBITDA (Cumulative) 4.66x 2.87x NA

2nd Lien/EBITDA (Cumulative) 6.94x 4.98x NA

Total Debt/EBITDA27 8.04x 4.98x 1.77x

Net Debt/EBITDA 7.94x 4.98x 1.49x

Fixed-charge Coverage Ratio 1.19x 6.38x 5.67x

FCF/Fixed Charges (Int+Principal+CapEx) 0.94x 3.31x 2.60x

Total Debt/FCF (Years) 10.20x 7.48x 0.16x

The proposed capital structure for the Company consists of (1) secured first lien

debt refinanced at $311mm, equivalent to 2.9x est. 2018 EBITDA, and (2) $229mm

of second lien debt, equivalent to 2.1x est. 2018 EBITDA.28 Total debt would be

$540mm which represents a leverage of 5.0x est. 2018 EBITDA (4.2x est. 2016

EBITDA). In addition, Cenveo will maintain a revolving credit facility of $200

million, undrawn immediately after the restructuring, but which will provide the

main source of liquidity (as the existing excess cash will be distributed in the

restructuring). Under our restructuring scenario, the equity of the Company

26 Based on Moody’s rating methodology 27 Total debt is calculated using par value 28 Our restructuring plan includes second lien notes over senior unsecured notes in order to reduce interest rate levels. Senior unsecured notes would have a 2 to 3% interest rate differential.

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

46

following the capital structure restructuring would be $433mm, which represents

45% of the estimated enterprise value.

We estimated a restructuring enterprise valuation of $974mm (Exhibit 8) using an

est. 2018 sum-of-the-parts valuation. Our valuation indicates that first lien

creditors would be fully covered in Chapter 11. As a result, a restructuring scenario

that avoids Chapter 11 has to include at least a 100% recovery rate for first lien

creditors. Allianz would use its control to require Cenveo to pay down as much debt

as possible using excess free cash flow and the sale of the print business.

Restructuring would likely occur at the end of 2018 or early 2019, giving Cenveo

over 2 years to implement operational improvements and reduce its debt burden.

Over this period, we estimate that Cenveo can generate between $108mm and

$337mm in cash flow from 2016 to year-end 2018 that can be used to reduce first

lien principal. These steps would lower overall leverage and be sufficient for first

lien creditors to extend their 2019 maturities.

In a base case scenario, the remaining $311mm in first lien debt would be rolled

over to a later maturity date. The refinanced notes would include stronger

covenants intended to strengthen the claim of first lien lenders, including a cash

sweep clause guarantying the distribution of any excess cash as a prepayment of the

debt. The restructured balance sheet would also include $229mm in new second

lien notes with an estimated interest rate in the area of 6.0%. Overall, the blended

interest rate would be close to 5.8%, in line with peers and B1/B+ rated companies.

The above credit statistic table shows that the Company is able to cover its debt cost

and that the proposed capital structure is sustainable. Free cash flow to fixed

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

47

charges (interest payments, principal payments and capital expenditures) would

increase from 0.97x to 3.31x.

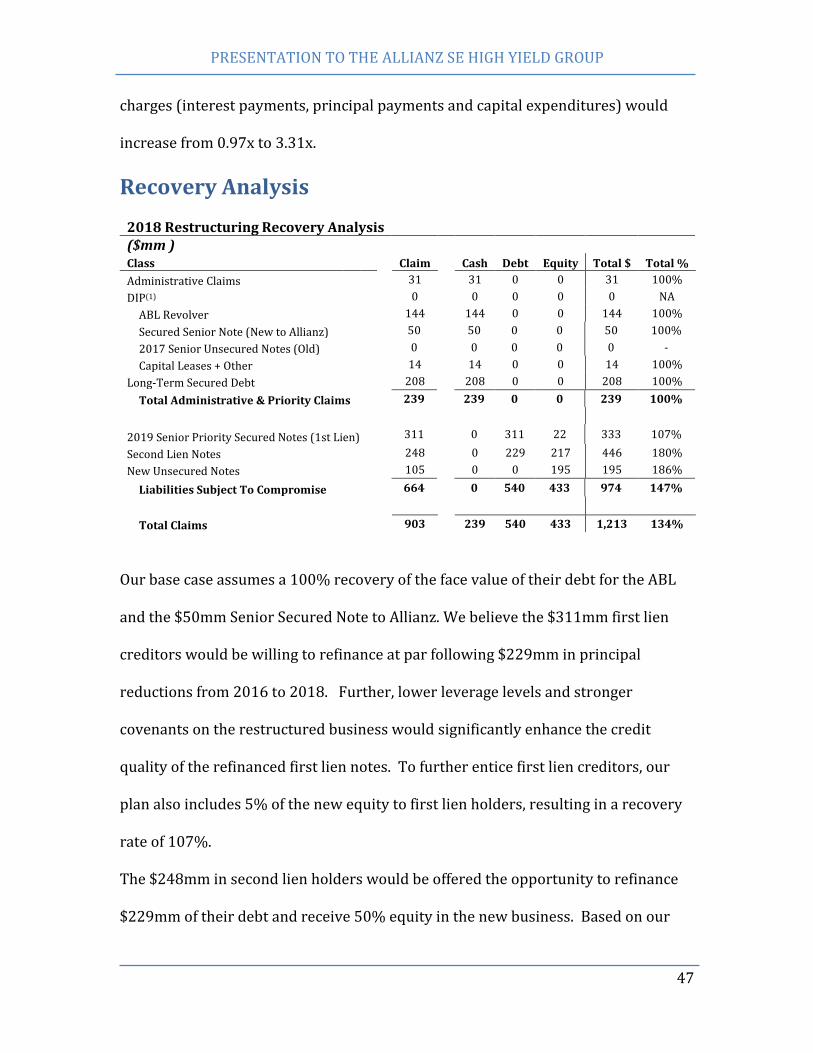

Recovery Analysis

2018 Restructuring Recovery Analysis

($mm )

Class Claim Cash Debt Equity Total $ Total %

Administrative Claims 31 31 0 0 31 100%

DIP(1) 0 0 0 0 0 NA

ABL Revolver 144 144 0 0 144 100%

Secured Senior Note (New to Allianz) 50 50 0 0 50 100%

2017 Senior Unsecured Notes (Old) 0 0 0 0 0 -

Capital Leases + Other 14 14 0 0 14 100%

Long-Term Secured Debt 208 208 0 0 208 100%

Total Administrative & Priority Claims 239 239 0 0 239 100%

2019 Senior Priority Secured Notes (1st Lien) 311 0 311 22 333 107%

Second Lien Notes 248 0 229 217 446 180%

New Unsecured Notes 105 0 0 195 195 186%

Liabilities Subject To Compromise 664 0 540 433 974 147%

Total Claims 903 239 540 433 1,213 134%

Our base case assumes a 100% recovery of the face value of their debt for the ABL

and the $50mm Senior Secured Note to Allianz. We believe the $311mm first lien

creditors would be willing to refinance at par following $229mm in principal

reductions from 2016 to 2018. Further, lower leverage levels and stronger

covenants on the restructured business would significantly enhance the credit

quality of the refinanced first lien notes. To further entice first lien creditors, our

plan also includes 5% of the new equity to first lien holders, resulting in a recovery

rate of 107%.

The $248mm in second lien holders would be offered the opportunity to refinance

$229mm of their debt and receive 50% equity in the new business. Based on our

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

48

valuation this amounts a 180% recovery rate, which is a significant improvement

from the exchange offer Cenveo’s unsecured lenders agreed to in May 2017.

Allocating a portion of the equity is designed to sweeten the proposal and encourage

them to vote in favor of the plan. Our analysis shows that second lien creditors

would be significantly impaired in a liquidation scenario.29 Also, recent

bankruptcies also show that junior creditors are unlikely to recover all of their debt

through Chapter 11 reorganization.30 With these examples in mind, we believe

second lien creditors will vote in favor of the plan.

Allianz holds 68% of the unsecured credit and would agree to receive equity in the

plan. Unsecured creditors receive $195mm of equity value, nearly double the face

value of their debt, which represents 45% of the equity of the new company. Given

that unsecured debt traded below 50% prior to the 2016 exchange, we believe these

creditors would accept an offer of all equity that achieves full recovery of their debt.

Further, the unsecured creditors would be the first to be hit in a bankruptcy

scenario. We believe that the unsecured creditors would vote favorable to the plan.

The company that emerges from this restructuring would carry a much healthier

leverage level. At year-end 2016, Cenveo’s net debt to EBITDA is 8.7x. After this

restructuring plan, the leverage level falls to 4.9x est. 2018 EBITDA. While this post-

restructuring leverage level is on the high-side, many of Cenveo’s peers are highly

levered, including RR Donnelly (3.8x) and International Paper (4.1x).

29 Using National Envelope’s bankruptcy as a proxy, we calculated a liquidation value between $500mm and $680mm. Assuming there is $550mm in senior claims at bankruptcy, second lien lenders could at most hope to receive $130mm, representing a recovery rate of 53%. 30 In Verso Paper’s 2016 bankruptcy reorganization plan, creditors below the first lien notes received a combined 2.85% of the equity, well below the face value of their debt.

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

49

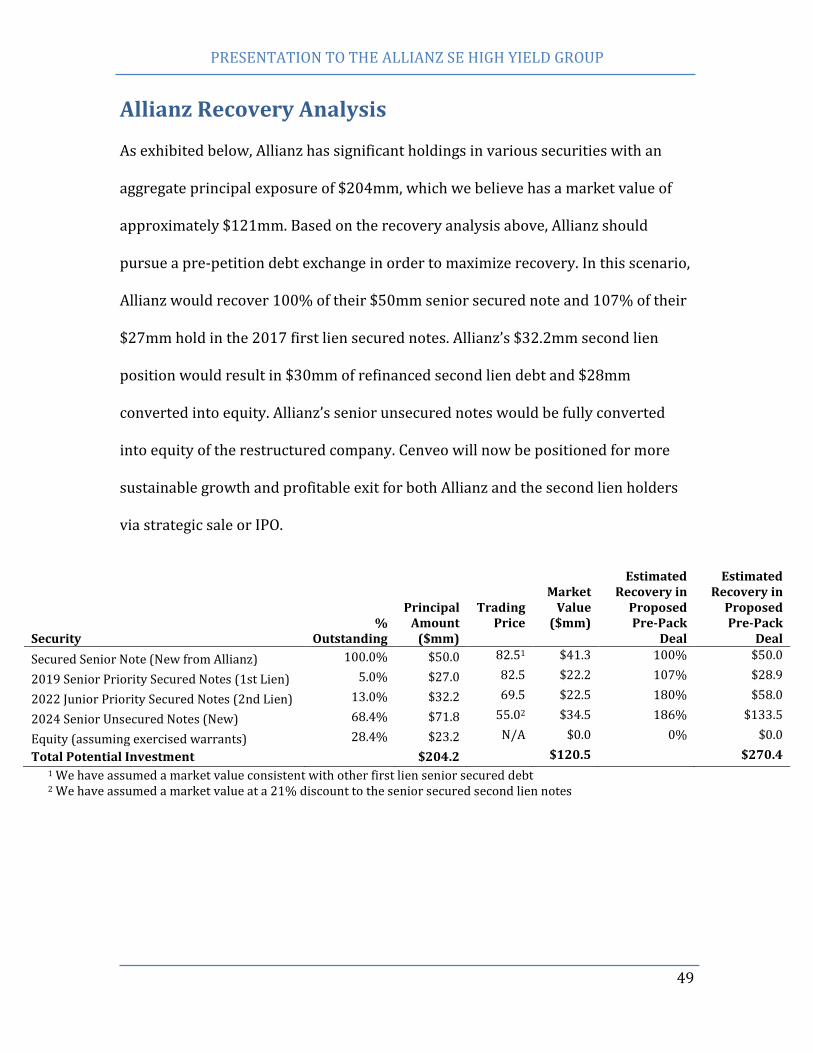

Allianz Recovery Analysis As exhibited below, Allianz has significant holdings in various securities with an

aggregate principal exposure of $204mm, which we believe has a market value of

approximately $121mm. Based on the recovery analysis above, Allianz should

pursue a pre-petition debt exchange in order to maximize recovery. In this scenario,

Allianz would recover 100% of their $50mm senior secured note and 107% of their

$27mm hold in the 2017 first lien secured notes. Allianz’s $32.2mm second lien

position would result in $30mm of refinanced second lien debt and $28mm

converted into equity. Allianz’s senior unsecured notes would be fully converted

into equity of the restructured company. Cenveo will now be positioned for more

sustainable growth and profitable exit for both Allianz and the second lien holders

via strategic sale or IPO.

Security %

Outstanding

Principal Amount

($mm)

Trading Price

Market Value

($mm)

Estimated

Recovery in Proposed Pre-Pack

Deal

Estimated

Recovery in Proposed Pre-Pack

Deal

Secured Senior Note (New from Allianz) 100.0% $50.0 82.51 $41.3 100% $50.0

2019 Senior Priority Secured Notes (1st Lien) 5.0% $27.0 82.5 $22.2 107% $28.9

2022 Junior Priority Secured Notes (2nd Lien) 13.0% $32.2 69.5 $22.5 180% $58.0

2024 Senior Unsecured Notes (New) 68.4% $71.8 55.02 $34.5 186% $133.5

Equity (assuming exercised warrants) 28.4% $23.2 N/A $0.0 0% $0.0

Total Potential Investment $204.2 $120.5 $270.4

1 We have assumed a market value consistent with other first lien senior secured debt 2 We have assumed a market value at a 21% discount to the senior secured second lien notes

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

50

Appendix

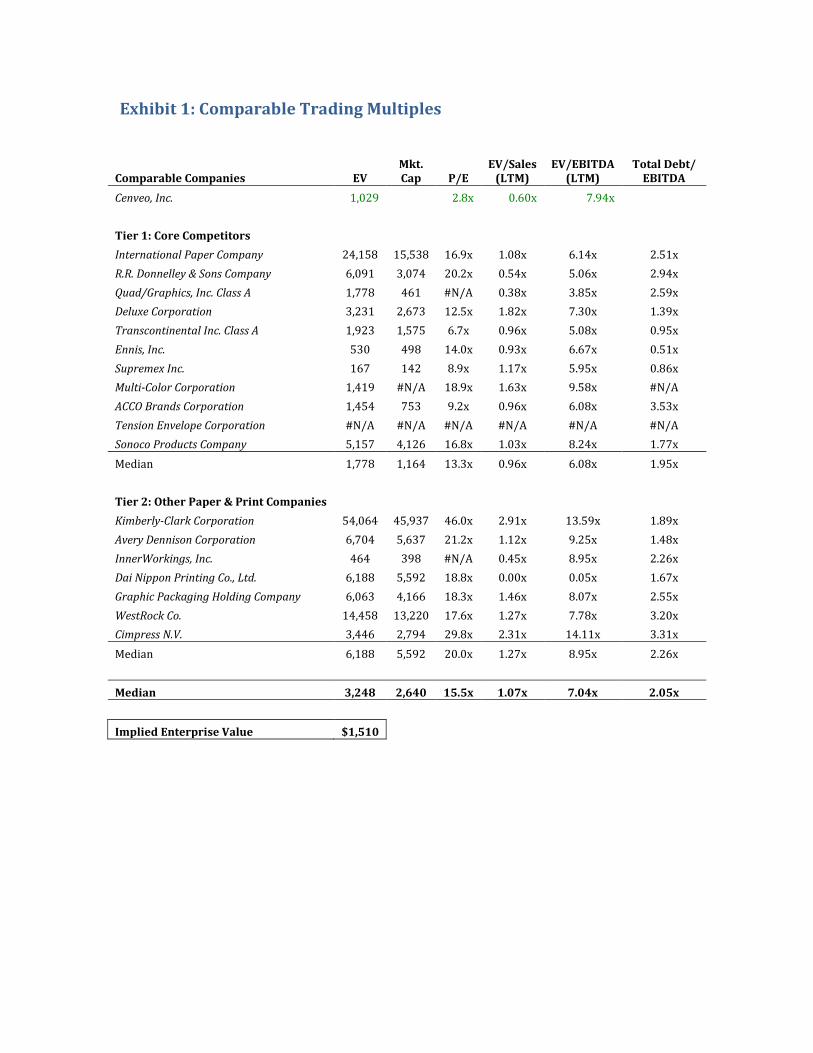

Exhibit 1: Comparable Trading Multiples

Comparable Companies EV Mkt. Cap P/E

EV/Sales (LTM)

EV/EBITDA (LTM)

Total Debt/ EBITDA

Cenveo, Inc. 1,029 2.8x 0.60x 7.94x

Tier 1: Core Competitors

International Paper Company 24,158 15,538 16.9x 1.08x 6.14x 2.51x

R.R. Donnelley & Sons Company 6,091 3,074 20.2x 0.54x 5.06x 2.94x

Quad/Graphics, Inc. Class A 1,778 461 #N/A 0.38x 3.85x 2.59x

Deluxe Corporation 3,231 2,673 12.5x 1.82x 7.30x 1.39x

Transcontinental Inc. Class A 1,923 1,575 6.7x 0.96x 5.08x 0.95x

Ennis, Inc. 530 498 14.0x 0.93x 6.67x 0.51x

Supremex Inc. 167 142 8.9x 1.17x 5.95x 0.86x

Multi-Color Corporation 1,419 #N/A 18.9x 1.63x 9.58x #N/A

ACCO Brands Corporation 1,454 753 9.2x 0.96x 6.08x 3.53x

Tension Envelope Corporation #N/A #N/A #N/A #N/A #N/A #N/A

Sonoco Products Company 5,157 4,126 16.8x 1.03x 8.24x 1.77x

Median 1,778 1,164 13.3x 0.96x 6.08x 1.95x

Tier 2: Other Paper & Print Companies

Kimberly-Clark Corporation 54,064 45,937 46.0x 2.91x 13.59x 1.89x

Avery Dennison Corporation 6,704 5,637 21.2x 1.12x 9.25x 1.48x

InnerWorkings, Inc. 464 398 #N/A 0.45x 8.95x 2.26x

Dai Nippon Printing Co., Ltd. 6,188 5,592 18.8x 0.00x 0.05x 1.67x

Graphic Packaging Holding Company 6,063 4,166 18.3x 1.46x 8.07x 2.55x

WestRock Co. 14,458 13,220 17.6x 1.27x 7.78x 3.20x

Cimpress N.V. 3,446 2,794 29.8x 2.31x 14.11x 3.31x

Median 6,188 5,592 20.0x 1.27x 8.95x 2.26x

Median 3,248 2,640 15.5x 1.07x 7.04x 2.05x

Implied Enterprise Value $1,510

PRESENTATION TO THE ALLIANZ SE HIGH YIELD GROUP

1

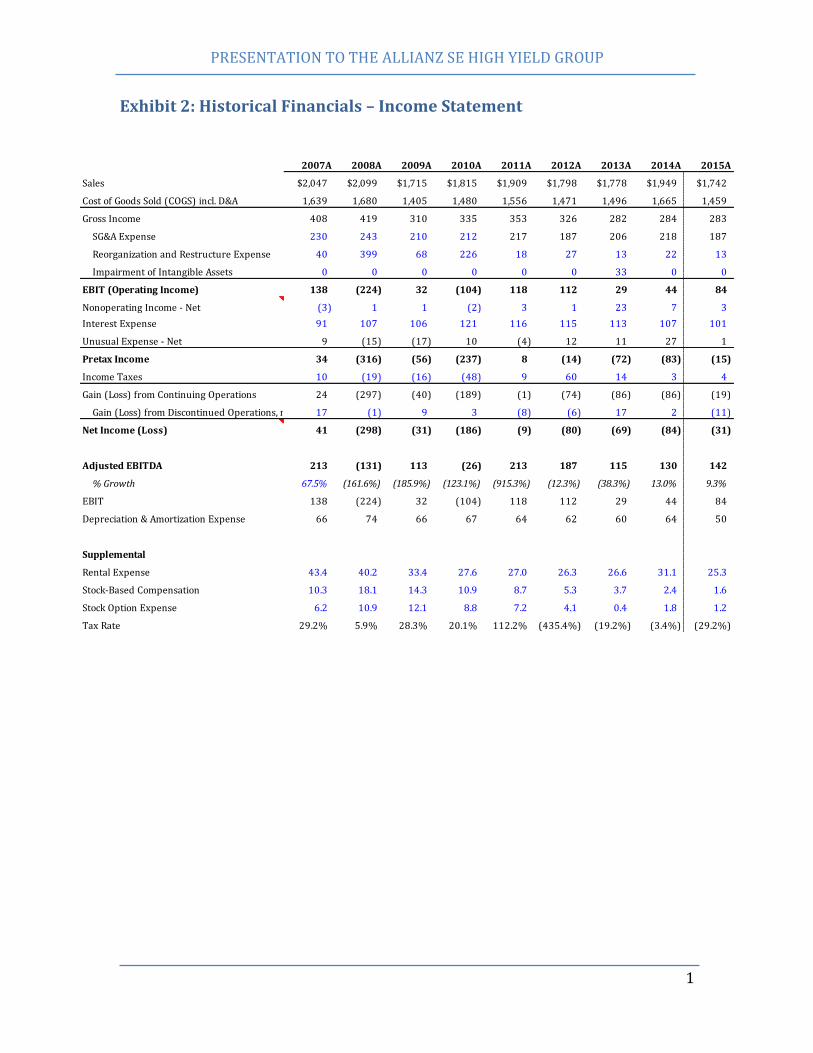

Exhibit 2: Historical Financials – Income Statement

2007A 2008A 2009A 2010A 2011A 2012A 2013A 2014A 2015A

Sales $2,047 $2,099 $1,715 $1,815 $1,909 $1,798 $1,778 $1,949 $1,742

Cost of Goods Sold (COGS) incl. D&A 1,639 1,680 1,405 1,480 1,556 1,471 1,496 1,665 1,459

Gross Income 408 419 310 335 353 326 282 284 283

SG&A Expense 230 243 210 212 217 187 206 218 187

Reorganization and Restructure Expense 40 399 68 226 18 27 13 22 13

Impairment of Intangible Assets 0 0 0 0 0 0 33 0 0