SUMMARY ANNUAL REPORT2005

19, avenue Montaigne75008 Paris - France

Shareholders’ relations:+33 (0)1 56 88 78 [email protected]

Investors’ relations:+33 (0)1 56 88 78 [email protected]

www.sequanacapital.fr

This is a summary of information contained in the reference document. SequanaCapital’s reference document has been fi led with AMF, the French marketregulator, and is available only in French on request from the company. It can also be downloaded at www.sequanacapital.fr.

Sequana CapitalSA Share capital €158,938,536 383 491 446 RDC PARIS

Stock exchange listingEuronext Paris Eurolist Market, Compartment A

Stock market codesReuters: VORP. PABloomberg: VOR FPISIN and Euronext: FR0000063364Mnemonic: VORPListing: Eurolist SRD (Compartment A)

Ordinary and Extraordinary General Shareholders’ Meeting10 May 2006 – 10:30 a.m.

Shareholders’ relationsSophie CormaryTel: +33 (0)1 56 88 78 38Fax: +33 (0)1 56 88 78 50E-mail: [email protected]

Investors’ relationsThibaut HyvernatTel: +33 (0)1 56 88 78 67Fax: +33 (0)1 56 88 78 72E-mail: [email protected]

Graphic design, coordinationPublicis Consultants

Photo creditsAntalis,Antonin Rodet,Arjowiggins, Blue Line Pictures/Iconica,Getty Images,Musée du Louvre – 5 Continents,Musée du Louvre – Gallimard, Musée du Louvre – Ph. Sebert,Neil Selkirk/Stone,SGS,Yann Arthus-Bertrand

Printed byImprimerie SIC on Arjowiggins papersCover: Sensation Tactile, extra blanc, 270 gInside: Absolut Mat,160 g

The 2005 annual report is also published in French and available on our website: www.sequanacapital.fr

Printed in France, June 2006© Sequana Capital ®. All rights reserved

PROFILE AND STRATEGY

02 Message from the Chairman and Chief Executive Offi cer04 Organization – Highlights05 Key consolidated fi gures 06 Corporate governance07 Shareholding structure and share performance 08 Net asset value 10 Environment and partnerships

PRINCIPAL INVESTMENTS

14 Arjowiggins18 Antalis22 SGS26 Permal Group28 Antonin Rodet

FINANCIAL INFORMATION

30 Financial review 31 2005 balance sheet and income statement (Equity method)34 Key 2005 consolidated fi nancial items (IFRS)

SE

QU

AN

A C

AP

ITA

L >

20

05

SU

MM

AR

Y A

NN

UA

L R

EP

OR

T

COUVERTURE_SEQUANA_ANG.indd 1COUVERTURE_SEQUANA_ANG.indd 1 29/05/06 16:22:1429/05/06 16:22:14

SUMMARY ANNUAL REPORT2005

19, avenue Montaigne75008 Paris - France

Shareholders’ relations:+33 (0)1 56 88 78 [email protected]

Investors’ relations:+33 (0)1 56 88 78 [email protected]

www.sequanacapital.fr

This is a summary of information contained in the reference document. SequanaCapital’s reference document has been fi led with AMF, the French marketregulator, and is available only in French on request from the company. It can also be downloaded at www.sequanacapital.fr.

Sequana CapitalSA Share capital €158,938,536 383 491 446 RDC PARIS

Stock exchange listingEuronext Paris Eurolist Market, Compartment A

Stock market codesReuters: VORP. PABloomberg: VOR FPISIN and Euronext: FR0000063364Mnemonic: VORPListing: Eurolist SRD (Compartment A)

Ordinary and Extraordinary General Shareholders’ Meeting10 May 2006 – 10:30 a.m.

Shareholders’ relationsSophie CormaryTel: +33 (0)1 56 88 78 38Fax: +33 (0)1 56 88 78 50E-mail: [email protected]

Investors’ relationsThibaut HyvernatTel: +33 (0)1 56 88 78 67Fax: +33 (0)1 56 88 78 72E-mail: [email protected]

Graphic design, coordinationPublicis Consultants

Photo creditsAntalis,Antonin Rodet,Arjowiggins, Blue Line Pictures/Iconica,Getty Images,Musée du Louvre – 5 Continents,Musée du Louvre – Gallimard, Musée du Louvre – Ph. Sebert,Neil Selkirk/Stone,SGS,Yann Arthus-Bertrand

Printed byImprimerie SIC on Arjowiggins papersCover: Sensation Tactile, extra blanc, 270 gInside: Absolut Mat,160 g

The 2005 annual report is also published in French and available on our website: www.sequanacapital.fr

Printed in France, June 2006© Sequana Capital ®. All rights reserved

PROFILE AND STRATEGY

02 Message from the Chairman and Chief Executive Offi cer04 Organization – Highlights05 Key consolidated fi gures 06 Corporate governance07 Shareholding structure and share performance 08 Net asset value 10 Environment and partnerships

PRINCIPAL INVESTMENTS

14 Arjowiggins18 Antalis22 SGS26 Permal Group28 Antonin Rodet

FINANCIAL INFORMATION

30 Financial review 31 2005 balance sheet and income statement (Equity method)34 Key 2005 consolidated fi nancial items (IFRS)

SE

QU

AN

A C

AP

ITA

L >

20

05

SU

MM

AR

Y A

NN

UA

L R

EP

OR

T

COUVERTURE_SEQUANA_ANG.indd 1COUVERTURE_SEQUANA_ANG.indd 1 29/05/06 16:22:1429/05/06 16:22:14

PROFILE

Sequana Capital is a financial holding company with majority or minority investments in listed and unlisted companies operating worldwide. Although it changed its name in 2005, the company’s mission remains the same: to create value for the shareholders through dynamic management of its investment portfolio, and to seek new opportunities for internal and external growth.

Sequana Capital maintains an ongoing dialogue with the teams overseeing operations at its subsidiaries’ level in view of optimizing management, adapting the resources to their needs and the market environment, and taking appropriate measures to support their development, while respecting their individual corporate culture.Sequana Capital manages an investment portfolio in excess of €3 billion at 31 December 2005, with a net asset value of €2.8 billion and a market capitalisation of nearly €2.5 billion.

01 SEQUANA CAPITAL > 2005 SUMMARY ANNUAL REPORT

MESSAGE FROM THE CHAIRMAN AND CEO

In 2005, your Company underwent several major changes: a change of name, the transformation of its corporate structure, and the reshuffling of its executive management team. These measures were designed to create a new momentum, and they have already started to pay off.

In 2005, our consolidated net profit was at €348 million, versus a loss of €28 million in 2004; €350 million of cash was accumulated at the holding company level, while net consolidated debt was reduced by more than 70%, or nearly €600 million, to €266 million; and our net asset value rose by 6.2%, despite €300 million in asset depreciation and provisions, which were largely attributable to the past.

As a result, we currently are in a position to fulfil our last year’s promise: to propose a significant dividend increase to €3.30 per share, of which €0.60, versus €0.40 in 2004, for its ordi-nary part, and an exceptional dividend of €2.70. The total dividend payment will therefore amount to €350 million, corresponding to our consolidated net profit for the year as well as to the holding company’s current cash position.

These performances are obviously largely attributable to Permal, whose disposal was realized under optimal conditions last November. Our other portfolio companies have also contributed to the favourable 2005 outcome: Arjowiggins’s performances have been disappointing, but they have been quite satisfactory at Antalis and excellent at SGS.

Due to the markets’ appetite for new forms of financial instru-ments and products and thanks to the talent of its managers and employees, Permal has gradually become one of the world leaders in the management of funds of alternative funds, a business that has expanded very rapidly over the past three years. In 2005, we therefore decided that the time was right for finding a partner for Permal, one who could amplify its growth potential and, in particular, provide further access to the American market.

Legg Mason, one of the largest American asset management companies, seemed a perfect fit and thus became Permal’s natural buyer.As far as Sequana Capital which founded this company many years ago, its long lasting efforts and patience have been rewarded with a €450 million capital gain, to which it seems reasonable to expect that further gains will be added in the upcoming two years, under the form of earn-out payments linked to Permal’s future performances which at present, continue to be outstanding.

As regards our two main other subsidiaries, they are active in the manufacturing and distribution sides of the paper industry, which has experienced major difficulties over the last few years: chronic surplus production capacity in Europe has prevented sales price increases, despite a very steep inflation in energy and other raw material costs.

Arjowiggins has nevertheless demonstrated some resilience: operating income declined to €83 million, down 22% com-pared to 2004, which altogether was a respectable achieve-ment compared to its main competitors. Arjowiggins however, had to report a net loss for the second consecutive year as a consequence of impairments, provisions and reserves that had to be acknowledged again in 2005. Given all the risks and uncer-tainties surrounding the company and its market, its net asset value was inevitably affected. Last October, Charles Dehelly was named Chief Executive Officer of Arjowiggins, and has begun implementing an action plan aiming at restoring profitable growth. The company’s weak-nesses must be rapidly identified and overcome, while capi-talizing on Arjowiggins’s numerous strengths, among whicht is significant technological innovation capabilities, the high-quality of its products, its wide brands recognition and the professionalism of its employees. Patience is needed until this new management strategy will bear its fruits. In the meantime 2006 unfortunately shows every sign of being another difficult year.

Ladies and Gentlemen,

I am however convinced that Charles Dehelly and his teams have all it takes to succeed in their endeavour.

Antalis, one of Europe’s largest distributor of communications support materials, significantly improved for the third consecutive year its operating income and net profit, which was up 75.7% in 2005. The Company also continued to enjoy one of the highest operating margins in its sector. Thanks to the strengthening of its presence in key emerging markets, particularly in Eastern Europe, South America and South Africa, to better cost controls and improvements over its operating systems, Antalis has consolidated further its positions in 2005. Pierre Darrot and his teams must now continue on their path to growth, by seizing every opportunity coming their way so as to forge new alliances and win new market shares.

Among our other reasons for satisfaction, I shall of course men-tion our investment in SGS, the world leader in inspection, verifi-cation, testing and certification, notably in the fields of agriculture, mining, petrochemicals and health care. After three years of strong growth, the company reported another excellent year in 2005, with a 14.7% sales increase, a 35% jump in net profit, and bright future growth prospects in all of its markets. Our 23.8% stake, makes us one of SGS’s two core shareholders, and this investment now accounts for over 40% of Sequana Capital’s NAV. In light of SGS’s stock market performance since the beginning of 2006, the company’s value should rise even further in the short to medium term.

With a portfolio of over €3 billion today, Sequana Capital obviously has the necessary resources to ensure its future growth. We must continue to devote time and energy to the monitoring of our existing subsidiaries and participations, particularly those operating under tough market conditions. Yet we must also explore new investment opportunities, a task we are actively pursuing today.

Our vision as an investment holding company boils down to one simple ambition, easier to be expressed than to be achieved: to create long-term value for our shareholders. The recent example of the successful Permal disposal shows us the way: to identify promising new activities, to acquire them at the right price, to sell them at the right moment and, in the meantime, to devote as much energy as necessary to make them prosper over the long run.

The investment market is currently characterized by large liquidities chasing after a limited number of good investment opportunities. As a consequence, valuations are high, meaning that we must act cautiously, and find the right balance between imagination, daring and rigour.

To succeed, we know we can count on the full commitment of Sequana Capital’s personnel, as well as on all the existing talents within our subsidiaries and participations. I would like to seize this occasion to thank all of the Group’s employees for their dedicated efforts as well as for the quality of their accomplish-ments in 2005.

Tiberto Ruy Brandolini d’Adda

“The concept we have of our business as an investment holding company […] : to create long-term value for our shareholders, to identify promising new activities, to acquire them at the right price, to sell them at the right moment and, in the meantime, to devote as much energy as necessary to make them prosper.”

02/03 SEQUANA CAPITAL > 2005 SUMMARY ANNUAL REPORT

ORGANIZATION Principal investments at 31 December 2005

March 2005Disposal of all shares in Pechel Industries.

May 2005 Worms & Cie changes its name to Sequana Capital and adopts the status of a French registered company (société anonyme) with a board of directors. Tiberto Ruy Brandolini d’Adda is named Chairman and Chief Executive Officer of the new entity, with Pascal Lebard and Pierre Martinet as Deputy Managing Directors.

October 2005Charles Dehelly is named Chairman of Arjowiggins’ Executive Board. A complete strategic review of the company is launched.

Antalis acquires two companies – in South Africa and Italy – to consolidate its positions. Creation of a new subsidiary in Brazil.

HIGHLIGHTS

ARJOWIGGINS(100% owned) The world’s leading manufacturer of creative and high-tech materials based essentially on paper

ANTALIS(100% owned) Europe’s leading distributor of paper and visual communication media

Unlisted companies

SGS(23.77% owned) The world’s leading inspection, verification, testing and certification company

Listed company

PERMAL GROUP (6.36% owned) One of the world’s leading fund management companies specialising in alternative investment

ANTONIN RODET (100% owned) Owner, vintner and merchant of premium Burgundy wines

Other investments

November 2005Disposal of a 70.5% stake in the Permal Group (out of a total shareholding of 77%) to Legg Mason for a capital gain of €450 million. Sequana Capital still holds a 6.36% stake in Permal, which will be sold in 2007 and 2009.

March 2006Change in Sequana Capital’s shareholding structure: unwinding of the shareholding agreement between the Worms, Barnaud, Meynial and Taittinger families, which lifts the free float to 27.44% from 12.4%.

Attributable Group net profit –Group share in millions of euros

Net cash position (debt) (1) (2) in millions of euros

NAV of portfolio investments

Net profit before exceptional –Group share in millions of euros

Shareholders’ fund – Group sharein millions of euros

KEY CONSOLIDATED FIGURESat 31 December 2005

2004

2005

(28)

348

Net asset valuein euros per share

Arjowiggins 30.1%

Antalis 15.7%

SGS 40.2%

Other 2.4%

Holding cash and equivalent 11.6%

Total: €3,017 M

2004 2005

173 168

2004 2005

1,8182,190

2004 2005

24.926.4

2004

2005

(235)

350 (2)

(1) Consolidated balance sheet for operating companies (equity method). (2) Including Legg Mason shares received as partial payment for the disposal of Permal, valued at €169 million at 31 December 2005 and sold in Q1 2006.

Net asset value

In millions of euros 2005

NAV of portfolio investments 3,017

Holding companies’ liabilities (222)

Net asset value 2,795

04/05 SEQUANA CAPITAL > 2005 SUMMARY ANNUAL REPORT

CORPORATE GOVERNANCEas of 3 May 2005

Following the General Shareholders’ Meeting of 3 May 2005, Sequana Capital was transformed into a French registered company with a Board of Directors, replacing the previous structure governed by an Executive Board and a Supervisory Board.

Board of Directors

Tiberto Ruy Brandolini d’Adda Chairman and Chief Executive Officer

Laurent Mignon Vice-Chairman

Pascal Lebard Deputy Managing Director

Pierre Martinet Deputy Managing Director

Luc Argand Member

Paul Barnaud Member

Gianluigi Gabetti Member

Michel Taittinger Member

Alessandro Potestà Member

AGF represented by Jean-François Lequoy Member

IFIL Investissements SA represented by Daniel Winteler Member (replaced by Carlo Sant’Albano on 2 March 2006)

Alain Fauchier Delavigne Non-voting Director

Aldo Osti Non-voting Director

Committees

Audit CommitteeAlessandro Potestà Chairman

Paul Barnaud AGF represented by Jean-François Lequoy

Nominations and Remunerations CommitteeGianluigi Gabetti Chairman

Luc ArgandTiberto Ruy Brandolini d’AddaLaurent Mignon

Strategy CommitteeIFIL Investissements SA represented by Daniel Winteler (replaced by Carlo Sant’Albano on 2 March 2006)Chairman

Luc ArgandTiberto Ruy Brandolini d’AddaPascal LebardPierre MartinetLaurent MignonMichel Taittinger

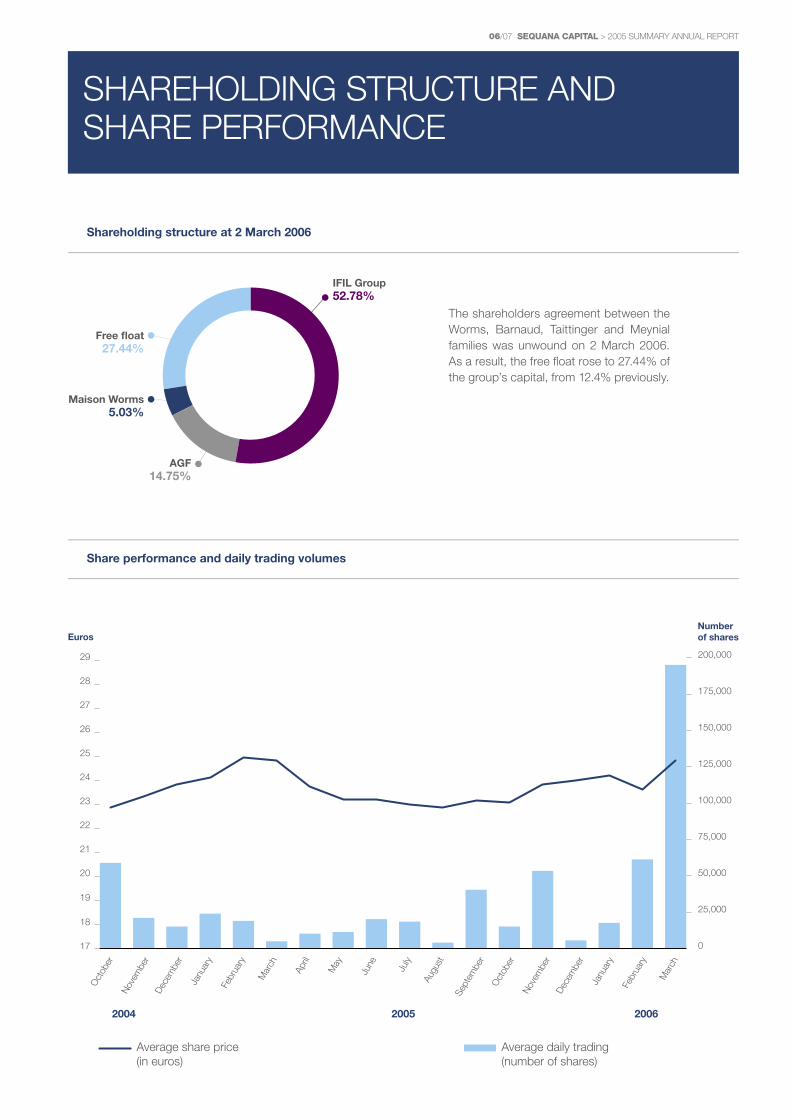

IFIL Group52.78%

AGF 14.75%

SHAREHOLDING STRUCTURE AND SHARE PERFORMANCE

Shareholding structure at 2 March 2006

The shareholders agreement between the Worms, Barnaud, Taittinger and Meynial families was unwound on 2 March 2006. As a result, the free float rose to 27.44% of the group’s capital, from 12.4% previously.

Free float 27.44%

Maison Worms5.03%

Share performance and daily trading volumes

Page 37

25

26

27

28

29

24

23

22

21

20

19

18

17

Euros

0

200,000

Numberof shares

150,000

100,000

50,000

175,000

125,000

75,000

25,000

Janu

ary

Febr

uary

Mar

ch

Janu

ary

Febr

uary

Mar

ch

April

May

June July

Augu

st

Sept

embe

r

Oct

ober

Nov

embe

rDe

cem

ber

Oct

ober

Nov

embe

r

Average share price(in euros)

Dece

mbe

r

2004 2005 2006

Average daily trading(number of shares)

06/07 SEQUANA CAPITAL > 2005 SUMMARY ANNUAL REPORT

Value of portfolio investments

The same principles were used to calculate the value of each of the Group’s investments at 31 December 2005 as at 31 December 2004. These principles are detailed below:

> SGS (company listed on the SWX Swiss Exchange,23.77% owned)To take into account the size of this investment as a share of Sequana Capital’s investment portfolio and the rise in share price in recent months, we calculated its value on the basis of the average share price for the past 45 trading days, rather than on the spot price, minus a 5% discount for lack of liquidity, which reflects Sequana Capital’s significant stake in

the company’s share capital, notably with regard to the daily trading volumes normally observed for SGS. On this basis, we raised SGS’s NAV by 37%.

> Arjowiggins and Antalis (unlisted companies,100% owned)The 3-year business plans established by the executive management of each company and approved by Sequana Capital, served as the basis for a valuation using a multi-criteria approach: essentially discounted cash flow (DCF) and peer group comparisons. Final valuations were based on an equal weighting between DCF, EBITDA and EBIT multiples and the Price Earnings Ratio (market capitalization/net profit before exceptional items).PER is used only for Arjowiggins.

2005 NET ASSET VALUE

Net Asset Value (NAV) is the main indicator of Sequana Capital’s value creation. It represents management’s understanding of the value of the company, using conservative assumptions, based on the aggregate value of Sequana Capital’s assets and liabilities. NAV is reviewed every six months.Since 31 December 2004, management’s NAV calculations have been validated by BNP Paribas, acting as an independent expert. At 31 December 2005, there were no changes in the methods used to calculate the value of portfolio investments compared to 31 December 2004. The methods used were reviewed and approved by the Statutory Auditors.

Summary of NAV

In millions of euros 31 December 2005 31 December 2004 Change

Arjowiggins 909 1,081 (172)

Antalis 475 413 +62

SGS 1,212 886 +326

Permal Group 48 607 (559)

Pechel Industries 6 17 (11)

Antonin Rodet 17 21 (4)

Net value of investments 2,667 3,025 (358)Net cash of holding company 181 (235) +416

Legg Mason shares 169 0 +169

Total cash and equivalent 350 (235) +585

Fox River provision (140) (66) (74)

Fox River deposit 100 100 0

DG IV provision (199) (195) (4)

DG IV deposit 92 92 0

Other assets and liabilities 0 10 (10)

Total financial assets & liabilities (147) (59) (88)

UK pension fund reserve (38) - ns

Holding company expenses (30) - ns

Defferred taxes (7) - ns

Central reserve (75) (100) +25Net Asset Value (NAV) 2,795 2,631 +164

NAV per share (€) 26.4 24.9 +1.5

Change in NAV: ArjowigginsEnterprise Value (EV) was lowered by 19% because the Group’s 2005 results fell short of expectations and the targets of the previous 3-year plan. Market prospects are still sluggish and the execution risk is very high for the new management team’s business plan. The decline in Arjowiggins’ EV was partially offset by a sharp reduction in debt, down €113 million (including €95 million in the second half of 2005), thanks to tighter control over investments and working capital requirements.

Change in NAV: AntalisNAV was raised by 7% because Antalis continues to improve earnings and profitability still ranks among the best in the sector.

> Permal Group (unlisted company, 6.36% owned)As part of the agreement to sell most of this investment in November 2005, the disposal price for the remaining 6.36% stake in Permal is now known. It will be calculated on the basis of $1 billion for 100% of the company’s equity. A 5.36% stake will be sold in November 2007 and the remaining 1% in November 2009. For NAV, we thus used the discounted value of $64 million, or €48 million. In contrast, the potential earn-outs based on the future performances of the Permal Group were not incorporated in NAV.

> Net cash and equivalentNet cash and equivalent of holding companies was added to assets at book value. Legg Mason shares, received in partial payment for the disposal of Permal and valued at market value, were also considered as net cash and equivalent because they were to be sold at the end of 2005 (and effectively sold in first-quarter 2006).

Non-current assets and liabilities

These are the medium and long-term assets and liabilities held by the Group’s holding companies, which were valued at book value at 31 December 2005. As in 2004, these items included:

> Fox River risk The Group is implicated in an environmental issue concerning a river in Wisconsin, USA, which is described in detail in note 15b in the appendix of the consolidated financial statements (Document de référence). A provision was reported in 2001 and raised by $88 million at the end of December 2005, bringing the total to $165 million, to take into account several new factors arising in 2005. A deposit was made at the end of 2001 to cover potential costs relating to the Fox River risk. This represented $118 million at 31 December 2005 and is used to finance incurred expenses (legal expenses, expertise, compensation, etc).

> DG IV riskIn 2001, the European Commission fined AWA Ltd €184 million for alleged price fixing in the carbonless paper market in Europe (1992-1995). Although proceedings for annulment have been filed, we have fully provisioned the fine in our financial statements.

Half of the fine was paid through a deposit in May 2002 and is reported under Sequana Capital’s financial assets. The case was argued before the EU Court of First Instance in Luxembourg in June 2005 and a ruling is expected during 2006.

Changes in the central reserve

A central reserve of €75 million was deducted from NAV at 31 December 2005 (vs €100 million at year-end 2004) to take into account certain liabilities that cannot be quantified using a standard accounting analysis: management’s cautious assumptions of certain economic risks that cannot be taken directly into financial account, of the capitalization of holding company expenses and of deferred taxes.

> UK pension fundsSince 2003, Sequana Capital has valued its pension commitments each year in compliance with IFRS and reported the corresponding provision to its consolidated statements. For the Group’s main UK pension fund, Wiggins Teape Pension Scheme (WTPS), future commitments have now been 99.6% financed in application of IAS 19, which places it among the best financed pension funds in the UK. Yet, the trustee in charge of managing the fund has demanded, as it is in his power, the payment of an additional £30 million over 3 years (or a discounted €38 million) above the accounting obligations obtained under IFRS. Considering this to be a definite economic liability for the company, the amount was deducted from 2005 NAV.

> Holding company expensesTwo years of normal operating costs for the holding companies were also deducted from 2005 NAV.

> Deferred taxesThis is calculated on the basis of tax values less deferred taxes already booked, after taking into account the long-term tax loss carry forwards held by Sequana Capital. At 31 December 2005, the only potential tax liability deducted from NAV (€7 million) were for the planned disposal of Legg Mason shares received in partial payment for the disposal of the Permal Group, and which have been held for less than 2 years (the shares were sold in first-quarter 2006).

08/09 SEQUANA CAPITAL > 2005 SUMMARY ANNUAL REPORT

ENVIRONMENT AND PARTNERSHIPS:RESPONSIBLE, CONSTRUCTIVE COMMITMENTS

Sequana Capital is concerned with investing in businesses that show a strong sense of ethics and corporate social responsibility. In a business that makes heavy demands on nature – especially air and water – Arjowiggins is taking significant steps to preserve the environment. Thanks to the company’s partnerships, the world of Art and Publishing can benefit from the excellence of its products.For its part, Antalis, active in numerous markets around the globe, is multiplying its humanitarian projects in response to the real needs of local communities.

We invest in businesses that respect the environment...

For years, Arjowiggins has made saving energy and managing natural resources, especially water, an integral part of its business. Environmental protection lies at the heart of its strategy.

Founding member of AERES since 2002, the French association for the reduction of greenhouse gas emissions, Arjowiggins introduced a new Environmental Char-ter in 2004, demonstrating the company’s commitment to prevent pollution and improve its environmental performances. To achieve a more equitable use of natural resources, emphasis was given in priority to reduce water consumption, optimizing treatment of effluents, managing waste and pursuing efforts to establish recycling systems. Arjowiggins strives to strike a balance between economic constraints and environmental protection throughout the industrial chain, from the supply of pulp to the management of waste, and including in the selection of its partners. In 2005, Arjowiggins continued to invest in the environment, spending a total of €17.2 million on such efforts, including €5.7 million for waste treatment.A growing number of Arjowiggin’s plants have received ISO 14001 certification, demonstrating the quality of the company’s Environmental Management System. By the end of 2006, the majority of the group’s paper mills will have obtained ISO 14001 certification.

Engaged likewise for many years in such efforts, Antalis has developed a spe-cial product line guaranteeing its customers that environmental standards were respected.

...place priority on humanitarian efforts...

Particularly active in humanitarian projects, Antalis has participated in numerous initiatives both in Europe and around the world that aim to overcome diseases and disabilities, and to help needy children. For example, in the UK it supports the cause of underprivileged children and the fight against cancer; in Poland, educa-tion and mobilization programmes for autistic children; in Spain, sponsorships for cancer associations and development assistance projects; and in Germany, an association helping children who are victims of paedophiliac acts...to cite but a few initiatives.

> Keen to promote a philosophy of sustainable development, Arjowiggins and Antalis were partners in the public awareness campaign Sustainable development: Why? launched by Yann Arthus-Bertrand in 50,000 schools in France. By contributing the paper needed for making the pedagogical kit’s 22 posters, the two companies affirm their commitment to being responsible players in the paper industry, and to engage themselves fully in environmental issues.

Sustainable development

© Y

ann

Art

hus-

Ber

tran

d

For more information, please visit the project website: www.ledeveloppementdurable.fr

10/11 SEQUANA CAPITAL > 2005 SUMMARY ANNUAL REPORT

...and are devoted to cultural partnerships

Since February 2005, Arjowiggins has become a mecene of the Louvre Museum, and a founding member of the Cercle Louvre Entreprises. This partnership with the Art and Publishing world is ineluctable, since the company’s premium papers offer high-performance supports, backed by research conferring them a wide range of properties – from appearance and resistance, to conservation and inviolability. As a result, Arjowiggins now participates in the realization of all catalogues co-published by the Louvre for its temporary exhibitions. Arjowiggins also made it possible for a drawing by Ingres – the Portrait of Charles Marcotte d’Argenteuil, recognized as a National Treasure – to be added to the Louvre’s collections. The association between Jean-Auguste-Dominique Ingres and Arjowiggins first began when Ingres asked the paper manufacturer to create a specific type of paper, one that has been called Ingres paper ever since.

Along the same lines, Arjowiggins sponsored the Louvre’s exhibition L’Atelier de David, as well as the Ateliers de la modernité show at the Maeght Foundation in Saint-Paul-de-Vence – an event to which Antalis also lent its support, by contributing all of the stationary and envelopes needed to make the 15,000 invitations that were sent out worldwide. Arjowiggins, in partnership with the Centre des Monuments Nationaux, has also inaugurated a collection of audio-tactile books called Sensitinéraires that allow people with visual disabilities to ‘tour’ France’s most representative historical monuments: the first audio-tactile book is devoted to the Sainte Chapelle. This partnership has allowed Arjowiggins to demonstrate its creative and innovative abilities.

Among its other efforts in support of culture, Arjowiggins became the first company to offer a special award in recognition of a young painter’s work at the Biennale d’Art Contemporain, held in Issy les Moulineaux (France).Through its AW-4U project, the company invites students in design, communication and the arts to develop a better understanding of materials, while offering them a space in which to exchange and express ideas thorough works they have created using the Group’s paper products. Finally, through its Canson brand, Arjowiggins sponsors one of the 7 official awards attributed during Angoulême’s International Comics Festival, to support talent in this popular art form.

> Portrait of Charles Marcotte d’Argenteuil by Ingres, National treasure acquired for the collections of Le Louvre, thanks to Arjowiggins (donor).

© M

usée

du

Louv

re –

Ph.

Seb

ert

© M

usée

du

Louv

re –

Gal

limar

d©

Mus

ée d

u Lo

uvre

– 5

Con

tinen

ts

© M

usée

du

Louv

re –

Gal

limar

d

PRINCIPAL INVESTMENTS

14 Arjowiggins (100%), the world’s leading manufacturer of creative and high-tech materials based

essentially on paper

18 Antalis (100%), Europe’s leading distributor of paper and visual communication media

22 SGS (23.77%), the world’s leading inspection, verification, testing and certification company

26 Permal Group (6.36%), one of the world’s leading fund management companies specializing

in alternative investment

28 Antonin Rodet (100%), owner, vintner and merchant of premium Burgundy wines

12/13 SEQUANA CAPITAL > 2005 SUMMARY ANNUAL REPORT

ARJOWIGGINS100% owned subsidiary

THE WORLD’S LEADING MANUFACTURER OF CREATIVE AND HIGH-TECH MATERIALS BASED ESSENTIALLY ON PAPER

Sales of €2,004 million / 7,800 employees / 35 production sites worldwide 3 R&D centres / 215 engineers

The world’s leading producer of premium papers and high-tech materials, Arjowiggins is not a conventional paper manufacturer, for it integrates the latest technological advances into all of its products, providing customers with original solutions adapted to their needs. Its strategy: innovation for customers. This effort is supported by the 215 engineers in the Technology and Innovation Department, whose contributions have enabled the company to patent over 1,500 products and solutions.

4 core lines of business

> Communications Paper and other materials for professionals in the design, communications, marketing and publishing industries.

> Creative hobby Art supplies for professional and amateur artists alike, through such well-known brands as Canson and Arches.

> Security High-tech materials for banknotes, security documents such as biometric passports (secured chips, covers and interior pages) and smart product labelling (certification of origin, traceability).

> Technology Special materials for a wide range of industries, from health care (medical papers, bacteriological barriers) to interior design (decorative papers used in making furniture and flooring), automobiles and fashion (transfer papers and synthetic leather support materials)

A portfolio of famous brands: Arches, Canson, Conqueror, Maine Gloss, Rives

Arjowiggins’ Executive Board Charles Dehelly – Chairman and CEOMichel Durand – Chief Operating OfficerMel de Vogue – Chief Financial Officer

14/15 SEQUANA CAPITAL > 2005 SUMMARY ANNUAL REPORT

Faced with a tough market environment and new competition...

The year 2005 was characterized by feeble economic growth in Europe and sluggish demand, chronic surplus production capacity in numerous markets, a rise in Asian competition and lacklustre growth in volumes, up only 1%. As a result, prices continued to be squeezed throughout the year. Consequently, sales rose a feeble 1.4% to over €2 billion, up from €1.9 billion in 2004. Operating profit before exceptional items declined 22% from the 2004 level to €82.6 million, with an operating margin of 4.1%.

The decline in operating profit is mainly due to higher commodity costs and the energy bill in Europe, which rose 23% or €46 million. These costs were not offset by the additional €11.6 million in operating profit generated by sales growth and the €18 million reduction in fixed costs.

Arjowiggins nevertheless generated abundant free cash flow (up €124 million, inclu-ding €95 million in the second half), thanks to significant efforts to reduce working capital requirements, and a strict control of investments. Management reduced net debt by 28% to €291 million at the end of 2005, down from €404.4 million in 2004.

Moreover, the company reported a €210 million charge in 2005, following a charge of over €109 million in 2004, corresponding mainly to the impact of impairment tests at the end of the year in compliance with IFRS.

Arjowiggins launched a strategic review in the second half of 2005 after Charles Dehelly took the helm as chairman of the executive board. This review brought to light the group’s strengths and weaknesses.

“Our challenge lies in innovation, and in adapting ourselves at every turn to meet the needs of our customers.”

ARJOWIGGINS

A NEW ORGANIZATION TO SERVE A STRATEGY OF CONQUEST

Faced with new challenges from global competition, and in order to resume profitable growth, the management team has decided to put the customer and innovation once again at the heart of its strategy. With the markets for paper still looking tough in 2006, it is indispensable to create new dynamics.

Key consolidated figures

In millions of euros 2005 2004

Sales 2,003.6 1,977.1

Operating profit before exceptionals 82.6 106.4

Operating margin 4.1% 5.4%

Attributable group net profit (loss) (156.8) (45.5)

Net debt 291.0 404.4

Capital employed 902.1 1,130.1

Return on capital employed (ROCE) 9.2% 9.4%

Net debt: algebraic sum of bank borrowing and loans, cash and cash equivalent, and trading investments.Capital employed: sum of net fixed assets and working capital requirements.Operating profit before exceptionals: algebraic sum of operating profit, net investment income/(expense), the corresponding corporate tax and the share of associates.

...Arjowiggins responds with a plan of action to meet the challenges

Arjowiggins first plans to capitalize on its strengths, by relying notably on its world-renowned brands and leadership positions in numerous niche markets, its R&D, and its purchasing power. It will then work to correct its weaknesses, due essentially to its organisational structure as a federation of small and medium-sized enterprises with limited synergies, investments that are unsuitably sized or poorly positioned geographically, and a “tonnage-driven” culture that fails to give sufficient importance to marketing and innovation.

To achieve these goals, Arjowiggins has established an action plan that will enable it to switch from a business plan geared for the production and marketing of commodities, to a customer-oriented approach based on comprehensive solutions.

With this aim in mind, the company defined four top priorities to be implemented as of 2006:> step up innovation: increase the R&D budget by 20% a year, with a focus on markets where positions are well established,> seek new sources of growth, notably in Eastern Europe and Asia,> use a cross-functional approach to increase synergies within the Group,> rethink the “go to market model”, using an approach built on strategic partnerships.

To reach these goals, the company was reorganised as follows:> 3 regional divisions focused on industrial, marketing and operating issues, to improve sales productivity while fostering geographic synergies: AW Europe/ Middle East/Africa; AW North & South Americas; and AW Asia-Pacific.> 9 branches focused on strategic issues and product development: AW Printing & Publishing Europe; AW Printing & Publishing North America; AW Business Forms; AW Visual Communication; AW Business Forms; AW Consumer/Retail/ SOHO; AW Labelling & Security; AW Industrial Solutions; AW Medical & Hospital; and AW Advanced Applications.> 4 corporate departments to support the regional and branch organisations: Human Resources; Technology; Finance/Legal; and Business Performance.

> Charles Dehelly was named Chairman and CEO of the Executive Board.

> Launch of a new organization.

> Creation of a joint-venture with China’s leading paper manufacturer to build a new production unit.

> Arrival of Emeric Thibierge as the Group’s Art Director.

Highlights

16/17 SEQUANA CAPITAL > 2005 SUMMARY ANNUAL REPORT

ANTALIS100% owned subsidiary

EUROPE’S LEADING DISTRIBUTOR OF PAPER AND VISUAL COMMUNICATION MEDIA

Sales of €2,344 million / 6,500 employees / Present in 35 countries (in Asia, South America and South Africa) including 23 in Europe / 78 distribution centres / 22,000 deliveries daily 2 million tonnes of paper distributed annually

Serving over 180,000 customers, business professionals and printers, Antalis is the market leader or co-leader in each of its markets.

4 core distribution activities

> Print & Office12,000 paper and envelope products

> Visual communication1,200 products

> PackagingPackaging materials to protect goods during transport

> Promotional products2,000 items

Top-quality advice and specialised services

High-performance logistics

Antalis’ Executive BoardPierre Darrot – Chairman and CEOXavier Roy-Contancin – Chief Financial OfficerHervé Poncin – Director, Western Europe Henry Cubbon – Director, UK, Ireland and South Africa Gilles Raynaud – Director, Human ResourcesStephane Courtot – Director, Marketing and Purchasing

18/19 SEQUANA CAPITAL > 2005 SUMMARY ANNUAL REPORT

Solid results in a tough market environment

Volumes did not rebound in 2005, as expected in late 2004. The European commu-nications materials distribution market declined by 2% in value in 2005, compared to the previous year.

In this unfavourable market environment, Antalis nonetheless continued to improve its operating performances, reaping the benefits of better customer relations management (CRM). Thanks to CRM tools installed last year, Antalis provided customers with appropriate and profitable services, thereby consolidating its market share while boosting operating margins.

At the same time, it continued to pursue cost-cutting programmes, notably in logistics and sales, which fuelled new earnings growth in 2005.

Antalis reported sales of over €2.3 billion, a slight increase over the previous year, while the operating margin gained 0.5 percentage points to 2.3%. Operating profit before exceptional items was €53 million, up 27.4% compared to 2004.

The Iberian Peninsula, South Africa, France, Switzerland and Asia posted good performances. Italy, in contrast, experienced some difficulties, due notably to problems collecting accounts receivable. Performances were generally satis-fying in other countries, as well as in Promotional Products and Packaging.

Ongoing improvements in the overall financial situation resulted in a consolidated net profit of €26.7 million, up strongly from €11.5 million the previous year.

“With its integrated approach, Antalis offers customers products that are continually adapted to their needs, regardless of market trends.”

ANTALIS

CONSOLIDATION OF POSITIONS AND AFFIRMATION OF AN EFFECTIVE BUSINESS MODEL

Once again, and despite a mediocre market for communications media, Antalis strongly improved its operating performances this year. With its focus on creating value for customers, the Group’s commercial policy has proven itself effective and paves the way for optimising Antalis’ geographical redeployment.

Key consolidated figures

In millions of euros 2005 2004

Sales 2,344 2,337

Operating profit before exceptionals 53.0 41.6

Operating margin 2.3% 1.8%

Attributable group net profit 26.7 15.2

Net debt 316 327

Capital employed 647 613

Return on capital employed (ROCE) 8.2% 6.8%

Net debt: algebraic sum of bank borrowing and loans, cash and cash equivalent, and trading investments.Capital employed: sum of net fixed assets and working capital requirements.Operating profit before exceptionals: algebraic sum of operating profit, net investment income/(expense), the corresponding corporate tax and the share of associates.

New footholds in promising markets

Continuing its growth strategy of expanding into fast-growing geographic regions and market segments, Antalis entered the distribution market for pre-press and printing materials in South Africa and Brazil.

In South Africa, Antalis acquired First Graphics Ltd in July 2005. First Graphics is the leading distributor of technical materials and graphic supplies for printers and publishers, with a 40% market share and 2004 sales of €25 million. With this acquisition, Antalis bolsters its leadership position in the South African market by offering customers an integrated product line.

At the same time, capitalizing on its strong presence and experience in the distribution of pre-press and printing materials in Chile, Antalis signed an exclusive distribution agreement with Fuji and opened a subsidiary in Brazil. Building on this base, Antalis plans to expand into the paper distribution market and become a leading player in this major South American market.

Customer-oriented logistics

To satisfy customer demands, Antalis has developed a logistics system that guarantees same-day service in major European cities, and next-day service – generally before noon – for all other destinations. The logistics system is formed by a network of 19 national distribution centres located in proximity to the main European capitals, as well as 59 regional centres handling only a portion of the product line to ensure a high level of service at lower cost. The market outlook for 2006 still looks tough, with limited growth prospects in volume and ongoing pressure on prices.

Yet Antalis plans to capitalize on its internal resources to boost profitability by:> relying on partnerships with strategic suppliers,> pursuing the optimization of its logistics organization and customer relations management,> continuing its expansion in geographic regions and market segments offering strong growth potential.

> Acquisition of First Graphics Ltd, South Africa’s leading distributor of technical materials and graphic supplies, with a 40% market share.

> Opening of a Brazilian subsidiary, Antalis dos Brasil, and the signing of an exclusive distribution agreement with Fuji for the distribution of graphics supplies in Brazil.

> Acquisition of Antaréa, a promotional products company in Italy.

Highlights

20/21 SEQUANA CAPITAL > 2005 SUMMARY ANNUAL REPORT

SGS23.77% owned

THE WORLD’S LEADING INSPECTION, VERIFICATION, TESTING AND CERTIFICATION COMPANY

Sales of CHF 3,308 million / 43,000 employees / 1,000 offices and laboratories

SGS, listed on the SWX Swiss Exchange, is the undisputed world leader in the increasingly sophisticated areas of inspection, verification, testing and certification. In these fast growing markets, the Group is renowned for its leadership, particularly with regard to its high value-added services.

10 business divisions

> Agricultural Services

> Mineral Services

> Oil, Gas and Chemical Services

> Life Science Services

> Consumer Testing Services

> Systems and Services Certification

> Industrial Services

> Environmental Services

> Automotive Services

> Trade Assurance Services

Worldwide presence

22/23 SEQUANA CAPITAL > 2005 SUMMARY ANNUAL REPORT

Another record-breaking year...

The climate of uncertainty that is rapidly spreading amongst consumers, institutions and companies alike is fuelling very strong demand for security, protection and testing in the short and medium term.

SGS benefited fully from these excellent market conditions in 2005, with buoyant demand, strong prices and robust trade in agriculture, energy, construction and manufactured goods. SGS reported strong growth in all regions, headed by Asia with 30% growth.

The group reported a significant increase in sales, up 14.7% to over CHF3.3 billion. This growth is due to the diversification of services and to geographic expansion, notably in Asia. Sales growth was also driven by the successful integration of acquisitions made during the year: Aquatic Health, X-Per-X, Auto Sécurité, MinnovEx, Casco and Paradigm.

The operating margin rose to 15.2%, from 13.6% in 2004 (up 11.5%). Operating profit was CHF502 million, a CHF109 million increase over 2004. Consumer Testing Services, Oil, Gas & Chemical Services and Industrial Services are the three divisions generating the highest operating margins (20.3%, 15.7% and 11.8%, respectively), representing increases of between 11.7% and 17.8% compared to the year-earlier period.

Group net profit rose 33.5% to CHF371 million. The share price rose an average of 37.5% during the year.

“The unrivalled expertise, experience and commitment of its employees are SGS’s greatest assets.”

SGS

GROWTH AND PROFITABILITY IN ALL MARKETS

2005 was another historic year for SGS as it lined up new records, with all of the key items on the income statement showing double-digit growth, buoyed by the dynamic momentum of its activities in all regions.

Key consolidated figures

In millions of CHF 2005 2004

Sales 3,308 2,885

Operating profit before exceptionals 502 393

Operating margin 15.2% 13.6%

Attributable group net profit 371 278

Net cash 430 439

Capital employed 1,477 1,126

Return on capital employed (ROCE) 34.0% 34.9%

Net debt: algebraic sum of bank borrowing and loans, cash and cash equivalent, and trading investments.Capital employed: sum of net fixed assets and working capital requirements.Operating profit before exceptionals: algebraic sum of operating profit, net investment income/(expense), the corresponding corporate tax and the share of associates.

An ambitious strategic development plan

SGS has launched a strategic development plan, based on three growth vectors that build on its competitive advantages:

> continue enriching the services offered in its business portfolio, and expand its geographic range,> accelerate the Group’s growth by focusing on the three divisions whose underlying markets offer strong growth potential: Life Science Services, Consumer Testing Services and Industrial Services, and by exploring acquisition opportunities,> launch strategic initiatives by offering tailor-made services in under-exploited but fast-growing strategic markets, be it for governments, energy infrastructures or financial services.

This strategic development plan aims to reach three targets by 2008:

> sales of CHF5 billion,> an operating margin of 17%,> earnings per share of CHF80.

> April 2005: Dan Kerpelman is named CEO of SGS.

> Acquisitions of small and medium-sized enterprises: - In the first half of 2005: Aquatic Health Chile SA (Chile) was added to the Consumer Testing division; X-Per-X Inc. (Canada) joined Industrial Services; and Auto Marine Services Ltd (UK) was acquired for Automotive Services. - In the second half of 2005: MinnovEX Technologies Inc. (Canada), the world leader in exclusive metallurgical technologies; Casco Australia Pty Ltd (Australia), a complete network of coal inspection services and laboratories in Australia; by acquiring Groupe Auto Sécurité (France), SGS became the clear leader in statutory vehicle inspection business in France; and Paradigm Analytical Laboratories Inc., which has an excellent reputation for innovation in the environmental testing market.

> Disposal of SGS Cortex NV (Belgium).

> March 2006: Sergio Marchionne is named Chairman of the Board of Directors of SGS.

Highlights

> Some of the visuals from SGS’ media campaign.

24/25 SEQUANA CAPITAL > 2005 SUMMARY ANNUAL REPORT

Thanks to Permal’s strong performances in recent years, it was sold to Legg Mason on excellent terms.

Rare expertise in buoyant markets

Permal is one of the world leaders in the management of funds of alternative funds, with over $20 billion in assets under management. Using a multi-manager and multi-style approach, Permal funds are marketed over the main private banking networks worldwide. Created in 1973, Permal has six main offices, in New York, London, Boston, Singapore, Geneva and Nassau.

A win-win merger

Under the terms of the agreement signed on 23 June 2005, Sequana Capital sold a 70.5% stake in the Permal Group (out of a total shareholding of 77%) to Legg Mason Inc. in November 2005 for $718 million, 75% of which was paid in cash ($542 million, including $13 million in January 2006). The remaining 25%, equivalent to $176 million, was paid in Legg Mason shares. Before completing the disposal, Permal Group SCA paid the Sequana Capital group an exceptional dividend of $66 million.

PERMAL GROUP6.36% owned

A DISPOSAL TO FOSTER GROWTH

Key consolidated figures

In millions of dollars 2005 (1) 2004 (2)

Sales 292.4 348.4

Operating profit before exceptionals 75.3 83.2

Operating margin 25.6% 23.9%

Attributable group net profit 54.5 59.5

(1) For the period 1 January to 31 October 2005.(2) For the year to 31 December 2004.

Through this operation, the Permal Group receives the backing of a major American asset management company, which should enable it to significantly develop its North American business and so round out its asset management activities, originally concentrated in Europe, the Middle East and Asia. In exchange, Sequana Capital posted a net capital gain on the disposal of €455 million in 2005 (€450 million attributable to the group).

After this disposal, Sequana Capital still holds a 6.36% stake in Permal Group Ltd. Of this remaining shareholding 5.36% will be sold in November 2007 for a total of $56.3 million. A performance-based supplement, worth a maximum of $146 million, could be paid to Sequana Capital depending on the financial performances of the Permal Group Ltd at that date.

The remainder of Sequana Capital’s holding in the Permal Group, or a stake of about 1%, will be sold in November 2009 for $10 million, along with a maximum of $30 million in performance-based supplements, based on the financial performance of Permal Group Ltd at that date.

Consequently, the total proceeds on the disposal of the Permal Group Ltd are at least $782 million, and could reach a maximum of $958 million if all performance-based supplements are paid.

“Sequana Capital’s business is to create value by investing regularly, and by hedging between investments based on their maturity. Our strategy is to support and enhance the value of companies in which we invest over the long term: this was the case with Permal.

This disposal fits perfectly within our strategy. It represents an excellent opportunity for everyone concerned. With backing from a powerful American financial partner, and thanks to its professionalism and extremely successful management, the Permal Group will be able to pursue its development in the United States. For its part, Sequana Capital has realised an excellent operation.” Tiberto Ruy Brandolini d’Adda

26/27 SEQUANA CAPITAL > 2005 SUMMARY ANNUAL REPORT

Premiers crus and other prestigious wines: a passion for the terroir

Founded in 1875, Antonin Rodet belongs to that very exclusive club of négociant houses dealing in great Burgundy wines: it produces and distributes wines from a range of terroirs, originating in the best vineyards of the Côte d’Or and the Côte Chalonnaise, as well as Macon and Chablis regions. Today, with holdings totalling more than 100 hectares, Antonin Rodet distributes wines from its own domaines (Domaine Jacques Prieur, Domaine du Château de Rully, Domaine du Château de Mercey and Domaine de l’Aigle), as well as those of Château de Chamirey and Domaine des Perdrix. The house also produces a line of premium vins de négoce, of which the best Premiers Crus and Grands Crus are marketed under its special Cave Privée label.

Antonin Rodet generates a significant share of sales from exports and distributes its products in the world’s predominate markets, including the United States, the UK, Japan and Belgium.

Turning around profitability in a market hit by surplus production

Antonin Rodet reported 2005 sales of €14.9 million, down from €16.1 million in 2004. The net loss narrowed to €0.6 million, from a €3.5 million loss in 2004.

In a market environment marked by oversupply worldwide and increasing compe-tition from New World wines, Antonin Rodet has been redefining its strategy and reorganising its sales networks over the past two years, enabling it to turn around profitability after several tough years. These ongoing efforts should begin to pay off in 2006, with renewed sales growth and an operating profit near breakeven.

ANTONIN RODET100% owned subsidiary

OWNER, VINTNER AND MERCHANT OF PREMIUM BURGUNDY WINES

FINANCIAL INFORMATION

30 Financial review

31 2005 balance sheet and income statement (Equity method)

34 Key 2005 consolidated financial items (IFRS)

28/29 SEQUANA CAPITAL > 2005 SUMMARY ANNUAL REPORT

Foreword

The consolidated financial statements of Sequana Capital have been prepared in compliance with IFRS as adopted by the European Union. Data for the year 2004 is also presented using IFRS.

The entities in which Sequana Capital has exclusive control are therefore fully consolidated.

To provide shareholders with the fullest and clearest information possible, and to present a more relevant view of the portfolio and the weight of each line of business in the group’s balance sheet, financial statements have also been prepared using the equity method.

These statements are simply an analytical presentation of the income statement and balance sheet and are not intended to replace the consolidated financial statements submitted to shareholders for approval. For each of the main investments, they provide a clear view of the cost price, the contribution to Group net profit and ROCE. Since the presentation of financial statements using the equity method does not comply with IFRS, we have provided a correspondence table showing the transition between “operating profit before exceptionals” (fully consolidated) and “net profit before exceptionals” (equity method).

FINANCIAL REVIEW

Consolidated balance sheet at 31 December 2005 (Equity method)

In millions of euros 2005 2004

Companies valued at cost:

Arjowiggins 898 1,026

Antalis 442 405

SGS 623 585

Permal Group - 133

Other investments 22 37

Total 1,985 2,186

Other financial assets 245 185

Other assets 18 9

Legg Mason shares 169 -

Net cash 181 -

Total Assets 2,598 2,380

Shareholders’ equity 2,190 1,818

Provisions 356 292

Net debt - 235

Other liabilities 52 35

Total Liabilities 2,598 2,380

30/31 SEQUANA CAPITAL > 2005 SUMMARY ANNUAL REPORT

Dividends paid

Given the size of attributable Group net profit in 2005, Sequana Capital’s Board of Directors is proposing an ordinary dividend of €0.60 per share and an exceptional dividend of €2.70 per share for the year 2005, bringing the total dividend to €3.30 per share. This represents a total dividend payout of €349.7 million, and fulfils the promise Sequana Capital’s Board of Directors made to shareholders in 2005.

Consolidated income statement: 2005 (Equity method)

In millions of euros 2005 2004

Share of earnings of operating companies:

Arjowiggins 57 61

Antalis 31 17

SGS 58 47

Permal Group 41* 46

Other (1) 4

Total 186 175

Net financial income/(expense) 2 8

Administrative expenses (17) (17)

Taxes (3) 7

Net profit before exceptionals 168 173

Net exceptional income/(expense) after tax 180** (76)

Goodwill impairment - (125)

Attributable Group net profit 348 (28)

* For the period 1 January to 31 October 2005.** The €180 million net exceptional income after tax consists mainly of the €450 million gain on the disposal of Permal, €197 million in exceptional charges for Arjowiggins, and an additional provision of €70 million for Fox River litigation. In 2004, the net exceptional expense consisted mainly of exceptional charges for Arjowiggins.

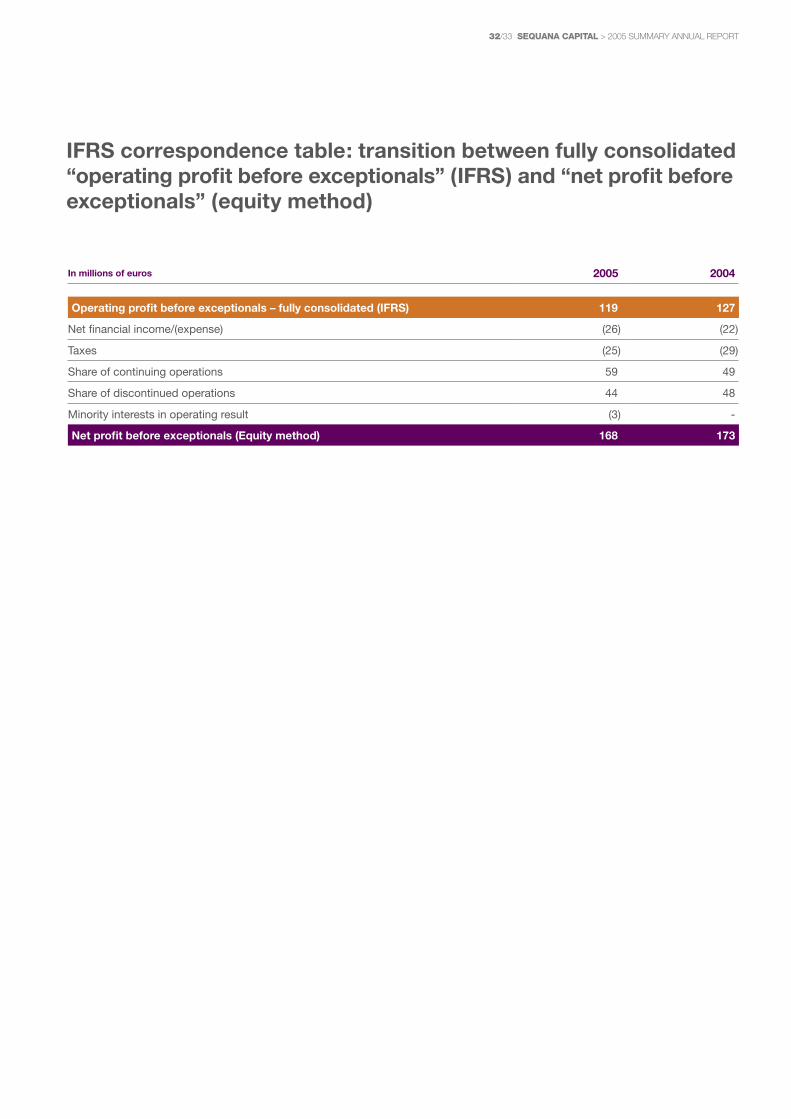

IFRS correspondence table: transition between fully consolidated “operating profit before exceptionals” (IFRS) and “net profit before exceptionals” (equity method)

In millions of euros 2005 2004

Operating profit before exceptionals – fully consolidated (IFRS) 119 127

Net financial income/(expense) (26) (22)

Taxes (25) (29)

Share of continuing operations 59 49

Share of discontinued operations 44 48

Minority interests in operating result (3) -

Net profit before exceptionals (Equity method) 168 173

32/33 SEQUANA CAPITAL > 2005 SUMMARY ANNUAL REPORT

Consolidated balance sheet at 31 December 2005 (IFRS)

In millions of euros 31 Dec. 2005 31 Dec. 2004

Non-current assets:

Goodwill 815 848

Other intangible assets 64 53

Property plant and equipment 784 961

Interests in associates 626 597

Non-current financial assets 262 231

Deferred tax assets 10 31

Other non-current assets 20 14

Total non-current assets 2,581 2,735

Current assets:

Inventories 550 571

Trade receivables 856 870

Other debtors 150 169

Current financial assets 366 51

Cash and cash equivalents 496 431

Total current assets 2,418 2,092

Assets classified as held for sale 3 17

TOTAL ASSETS 5,002 4,844

In millions of euros 31 Dec. 2005 31 Dec. 2004

Equity: Share capital 159 161

Share premium account 1,068 1,104

Translation reserves 30 (39)

Reserves directly associated with assets classified as held for sale 9

Retained earnings and other consolidated reserves 576 620

Attributable Group net profit for the year 348 (28)

Equity attributable to equity holders of the parent 2,190 1,818

Minority interests 3 3

Total equity 2,193 1,821

Non-current liabilities: Long-term provisions 554 468

Bank loans and financial debts 700 393

Deferred tax liabilities 66 66

Other non-current liabilities 5 13

Total non-current liabilities 1,325 940

Current liabilities: Short-term provisions 38 49

Bank overdrafts and bank loans 417 989

Trade payables 721 732

Other creditors 308 313

Total current liabilities 1,484 2,083

Liabilities directly associated with assets classified as held for sale

TOTAL LIABILITIES 5,002 4,844

ASSETS

LIABILITIES

KEY CONSOLIDATED FINANCIAL ITEMS

34/35 SEQUANA CAPITAL > 2005 SUMMARY ANNUAL REPORT

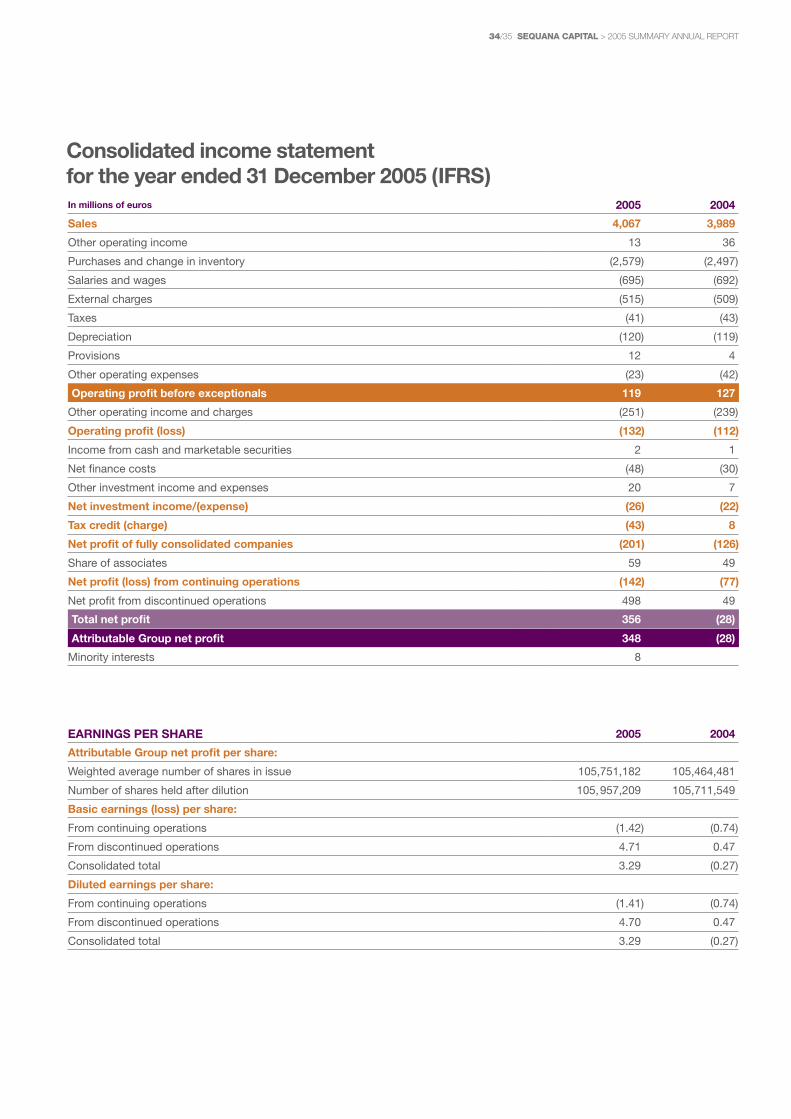

Consolidated income statement for the year ended 31 December 2005 (IFRS)In millions of euros 2005 2004

Sales 4,067 3,989

Other operating income 13 36

Purchases and change in inventory (2,579) (2,497)

Salaries and wages (695) (692)

External charges (515) (509)

Taxes (41) (43)

Depreciation (120) (119)

Provisions 12 4

Other operating expenses (23) (42)

Operating profit before exceptionals 119 127

Other operating income and charges (251) (239)

Operating profit (loss) (132) (112)

Income from cash and marketable securities 2 1

Net finance costs (48) (30)

Other investment income and expenses 20 7

Net investment income/(expense) (26) (22)

Tax credit (charge) (43) 8

Net profit of fully consolidated companies (201) (126)

Share of associates 59 49

Net profit (loss) from continuing operations (142) (77)

Net profit from discontinued operations 498 49

Total net profit 356 (28)

Attributable Group net profit 348 (28)

Minority interests 8

EARNINGS PER SHARE 2005 2004

Attributable Group net profit per share:

Weighted average number of shares in issue 105,751,182 105,464,481

Number of shares held after dilution 105, 957,209 105,711,549

Basic earnings (loss) per share:

From continuing operations (1.42) (0.74)

From discontinued operations 4.71 0.47

Consolidated total 3.29 (0.27)

Diluted earnings per share:

From continuing operations (1.41) (0.74)

From discontinued operations 4.70 0.47

Consolidated total 3.29 (0.27)

In millions of euros 2005 2004

Cash flow from operating activities:

Attributable Group net profit 348 (28)

Minority interests 8

Elimination of non-cash and non-operating items:

+/- Depreciation, amortisation and provisions (excluding current assets) 311 321

+/- Profit (loss) on disposals (465) (6)

+/- Other income and charges 6 (1)

+/- Tax credits and charges (including deferred taxes) 43 (8)

- Share in profits (losses) of associates (59) (49)

Cash provided by fully consolidated companies 192 229

- Dividends received from associates (1)

- Taxes paid (13) (17)

Change in operating working capital 27 15

Net cash from operating activities 206 226

Cash flow from investing activities:

- Acquisitions of tangible and intangible fixed assets (97) (155)

+ Disposals of tangible and intangible fixed assets 36 18

- Acquisition of investments (3) (3)

+ Disposal of investments 2 44

+/- Impact of changes in the scope of consolidation 366 (19)

+/- Change in loans and deposits 3 280

+/- Other cash inflows and outflows 15 (12)

Net cash from investing activities 322 153

Cash flow from financing activities:

Dividends paid to shareholders of the parent company (42) (63)

Dividends paid to minority interests of subsidiaries (4)

Dividends received from associates 14 12

+ Payments received on exercise of stock options 7 3

+/- Acquisitions and disposals of own shares 1

+ Inflows from new loans 340 448

- Repayment of loans (557) (497)

+/- Movements of marketable securities held over 3 months (163) 16

- Net interest paid (2) (1)

+/- Other cash inflows and outflows for financing activities (11) -

Net cash used in financing activities (414) (85)

Impact of exchange rate fluctuations 14 (11)

Change in cash and cash equivalent 128 283

Cash at beginning of year 272 (11)

Cash at end of year 400 272

Net increase (decrease) in cash and cash equivalents 128 283

Consolidated cash flow statement (IFRS)

Analysis of cash at closing:

Cash and cash equivalents 496 431

Current bank overdrafts (96) (159)

Cash and cash equivalents at end of year 400 272

SUMMARY ANNUAL REPORT2005

19, avenue Montaigne75008 Paris - France

Shareholders’ relations:+33 (0)1 56 88 78 [email protected]

Investors’ relations:+33 (0)1 56 88 78 [email protected]

www.sequanacapital.fr

This is a summary of information contained in the reference document. SequanaCapital’s reference document has been fi led with AMF, the French marketregulator, and is available only in French on request from the company. It can also be downloaded at www.sequanacapital.fr.

Sequana CapitalSA Share capital €158,938,536 383 491 446 RDC PARIS

Stock exchange listingEuronext Paris Eurolist Market, Compartment A

Stock market codesReuters: VORP. PABloomberg: VOR FPISIN and Euronext: FR0000063364Mnemonic: VORPListing: Eurolist SRD (Compartment A)

Ordinary and Extraordinary General Shareholders’ Meeting10 May 2006 – 10:30 a.m.

Shareholders’ relationsSophie CormaryTel: +33 (0)1 56 88 78 38Fax: +33 (0)1 56 88 78 50E-mail: [email protected]

Investors’ relationsThibaut HyvernatTel: +33 (0)1 56 88 78 67Fax: +33 (0)1 56 88 78 72E-mail: [email protected]

Graphic design, coordinationPublicis Consultants

Photo creditsAntalis,Antonin Rodet,Arjowiggins, Blue Line Pictures/Iconica,Getty Images,Musée du Louvre – 5 Continents,Musée du Louvre – Gallimard, Musée du Louvre – Ph. Sebert,Neil Selkirk/Stone,SGS,Yann Arthus-Bertrand

Printed byImprimerie SIC on Arjowiggins papersCover: Sensation Tactile, extra blanc, 270 gInside: Absolut Mat,160 g

The 2005 annual report is also published in French and available on our website: www.sequanacapital.fr

Printed in France, June 2006© Sequana Capital ®. All rights reserved

PROFILE AND STRATEGY

02 Message from the Chairman and Chief Executive Offi cer04 Organization – Highlights05 Key consolidated fi gures 06 Corporate governance07 Shareholding structure and share performance 08 Net asset value 10 Environment and partnerships

PRINCIPAL INVESTMENTS

14 Arjowiggins18 Antalis22 SGS26 Permal Group28 Antonin Rodet

FINANCIAL INFORMATION

30 Financial review 31 2005 balance sheet and income statement (Equity method)34 Key 2005 consolidated fi nancial items (IFRS)

SE

QU

AN

A C

AP

ITA

L >

20

05

SU

MM

AR

Y A

NN

UA

L R

EP

OR

T

COUVERTURE_SEQUANA_ANG.indd 1COUVERTURE_SEQUANA_ANG.indd 1 29/05/06 16:22:1429/05/06 16:22:14

SUMMARY ANNUAL REPORT2005

19, avenue Montaigne75008 Paris - France

Shareholders’ relations:+33 (0)1 56 88 78 [email protected]

Investors’ relations:+33 (0)1 56 88 78 [email protected]

www.sequanacapital.fr

This is a summary of information contained in the reference document. SequanaCapital’s reference document has been fi led with AMF, the French marketregulator, and is available only in French on request from the company. It can also be downloaded at www.sequanacapital.fr.

Sequana CapitalSA Share capital €158,938,536 383 491 446 RDC PARIS

Stock exchange listingEuronext Paris Eurolist Market, Compartment A

Stock market codesReuters: VORP. PABloomberg: VOR FPISIN and Euronext: FR0000063364Mnemonic: VORPListing: Eurolist SRD (Compartment A)

Ordinary and Extraordinary General Shareholders’ Meeting10 May 2006 – 10:30 a.m.

Shareholders’ relationsSophie CormaryTel: +33 (0)1 56 88 78 38Fax: +33 (0)1 56 88 78 50E-mail: [email protected]

Investors’ relationsThibaut HyvernatTel: +33 (0)1 56 88 78 67Fax: +33 (0)1 56 88 78 72E-mail: [email protected]

Graphic design, coordinationPublicis Consultants

Photo creditsAntalis,Antonin Rodet,Arjowiggins, Blue Line Pictures/Iconica,Getty Images,Musée du Louvre – 5 Continents,Musée du Louvre – Gallimard, Musée du Louvre – Ph. Sebert,Neil Selkirk/Stone,SGS,Yann Arthus-Bertrand

Printed byImprimerie SIC on Arjowiggins papersCover: Sensation Tactile, extra blanc, 270 gInside: Absolut Mat,160 g

The 2005 annual report is also published in French and available on our website: www.sequanacapital.fr

Printed in France, June 2006© Sequana Capital ®. All rights reserved

PROFILE AND STRATEGY

02 Message from the Chairman and Chief Executive Offi cer04 Organization – Highlights05 Key consolidated fi gures 06 Corporate governance07 Shareholding structure and share performance 08 Net asset value 10 Environment and partnerships

PRINCIPAL INVESTMENTS

14 Arjowiggins18 Antalis22 SGS26 Permal Group28 Antonin Rodet

FINANCIAL INFORMATION

30 Financial review 31 2005 balance sheet and income statement (Equity method)34 Key 2005 consolidated fi nancial items (IFRS)

SE

QU

AN

A C

AP

ITA

L >

20

05

SU

MM

AR

Y A

NN

UA

L R

EP

OR

T

COUVERTURE_SEQUANA_ANG.indd 1COUVERTURE_SEQUANA_ANG.indd 1 29/05/06 16:22:1429/05/06 16:22:14