Project Finance and Debt EquitySolar Thermal Projects

Presented by:Mr. Barin SarkarExecutive Director

LSI Financial Services Private LimitedMarch 14, 2012

AGENDA

National Solar Mission

Targets and Achievements: Phase I

Status‐ Grid Connected Plants

Financing of Solar Projects in India

Forms of Debt Funding

Broad terms of Loan & Financial Indicators

Private Equity Funding

Lessons Learnt

Possible Solutions/ Way Forward

Suggestions

CSP Projects‐Under‐development, Operational & Others Nationally and Internationally

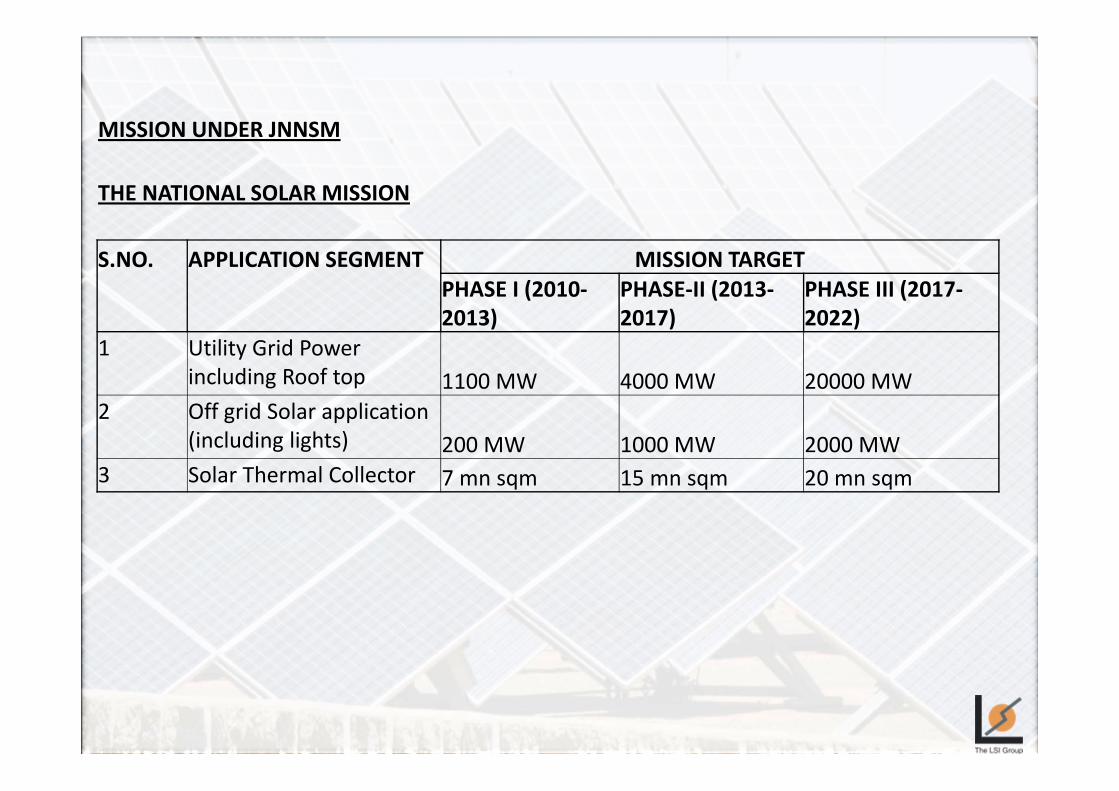

MISSION UNDER JNNSM

THE NATIONAL SOLAR MISSION

S.NO. APPLICATION SEGMENT MISSION TARGETPHASE I (2010‐2013)

PHASE‐II (2013‐2017)

PHASE III (2017‐2022)

1 Utility Grid Power including Roof top 1100 MW 4000 MW 20000 MW

2 Off grid Solar application (including lights) 200 MW 1000 MW 2000 MW

3 Solar Thermal Collector 7 mn sqm 15 mn sqm 20 mn sqm

TARGETS AND ACHIEVEMENTS: PHASE 1

S.NO. APPLICATION SEGMENT

MISSION TARGET

Target (2010‐13)Status January 2012

Achievement Expected by March 2012

1 Grid Solar Power 1000 MW 1054 MW capacity allocated, 170 MW capacity commissioned

350 MW

Roof top & distribution grid connected plants

100 MW 98 MW allotted 60 MW

2 Off grid Solar application (including lights)

200 MW 83.5 MW sanctioned

120 MW

3 Solar Thermal Collector 7 mn sqm 4.88 million sq meters

5.7 mn sqm

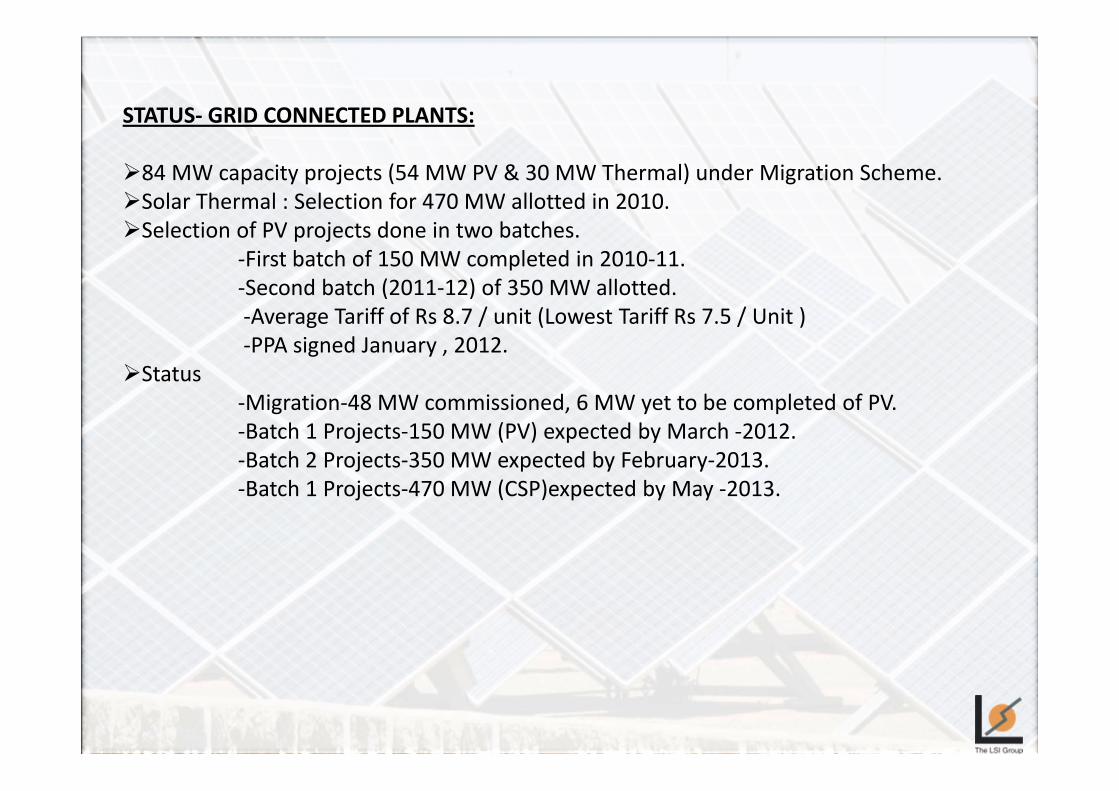

STATUS‐ GRID CONNECTED PLANTS:

84 MW capacity projects (54 MW PV & 30 MW Thermal) under Migration Scheme.Solar Thermal : Selection for 470 MW allotted in 2010.Selection of PV projects done in two batches.

‐First batch of 150 MW completed in 2010‐11.‐Second batch (2011‐12) of 350 MW allotted.‐Average Tariff of Rs 8.7 / unit (Lowest Tariff Rs 7.5 / Unit )‐PPA signed January , 2012.

Status‐Migration‐48 MW commissioned, 6 MW yet to be completed of PV.‐Batch 1 Projects‐150 MW (PV) expected by March ‐2012.‐Batch 2 Projects‐350 MW expected by February‐2013.‐Batch 1 Projects‐470 MW (CSP)expected by May ‐2013.

FINANCING OF SOLAR PROJECTS IN INDIA:

To achieve this target of 500 MW of solar thermal plants by 2013 and further generation ofpower through solar thermal route, projects have to reach financial closure. Projects arefunded by Debt and Equity:

1) DEBT FUNDINGSolar power is only beginning in India. Solar CSP projects can be financed through thefollowing routes:

A) BALANCE‐SHEET BASED FINANCING

• Available for large conglomerates with a healthy balance sheet that can support projects.

• This option can put the company balance sheets at risk.

• Entire burden of the project under‐performing falls on the developers.

• It may allow large industrial houses to get lower rates of finance using their existingrelations with the banks.

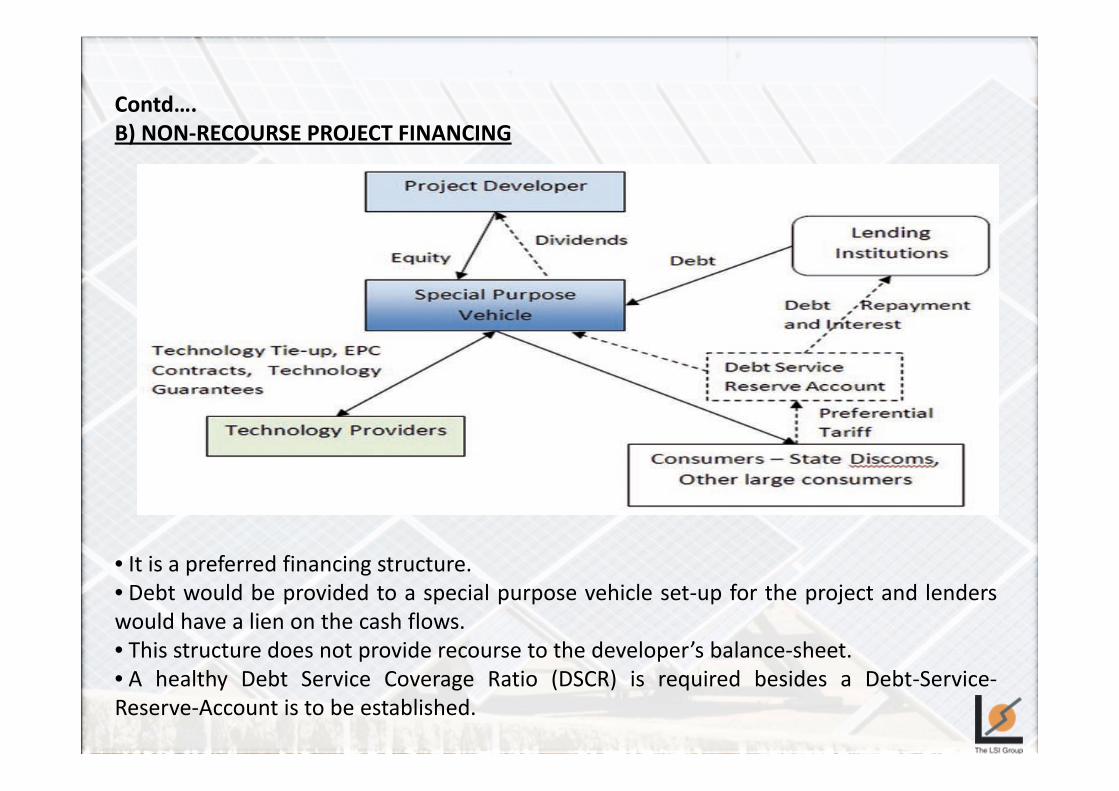

Contd….B) NON‐RECOURSE PROJECT FINANCING

• It is a preferred financing structure.• Debt would be provided to a special purpose vehicle set‐up for the project and lenderswould have a lien on the cash flows.• This structure does not provide recourse to the developer’s balance‐sheet.• A healthy Debt Service Coverage Ratio (DSCR) is required besides a Debt‐Service‐Reserve‐Account is to be established.

FORMS OF DEBT FUNDING:

Funds to be raised for solar thermal project should have longer maturity period of over 15 years otherwise there will be an asset liability mismatch. Funds can be raised from:

Infrastructure Financing Companies (IFC) like, PFC, REC, IREDA, etc.

Banks.

External Commercial Borrowings (ECBs).

Corporate Bonds.

Insurance and Pension Funds: In future, we expect the insurance and pension fundsto come forward which an access to long tenor funds are still not the major lenders to solar sector. This institutions can be attracted by further developing the corporate bond market and putting prudent credit rating mechanism in place.

EXIM Funding: The US export‐import bank provides finance to corporates which import a substantial part of the project components from US. This is a good option in case the main technology provider is from the US and has relations with the EXIM BANK.

Foreign Funding: Large project developers can tap international banks to get lower rates of finance. However, hedging can put a substantial dent in the rate differential and only someone ready to take the currency risk should resort to this option.

Green Energy Funds:There are many green energy funds currently in the market and these can provide equity, quasi‐equity and mezzanine financing.

For success of any project and solar thermal is no exception the following has to be in place for funding a project:

PROMOTERS‐ Promoters should be capable of completing the project.

TECHNOLOGY‐The technology should be a proven technology. Contractual guarantees from proven technology providers with a track record for the long‐term performance of the plant to be obtained.

PROJECT VIABILITY‐ Financial viably should be assessed.

MARKET: There should be a ready market for the products.

REVENUES‐ Long‐term PPA with credible consumers, i.e. direct power sale to large consumers, State Discoms, etc.

ENERGY CERTIFICATE‐ Developers can forego the preferential tariff and trade the RECs on the energy exchange.

Developers must convince lenders that projects are technically and financially viable and have the capability of repaying debt without outside assistance.

BROAD TERMS OF LOAN AND FINANCIAL INDICATORS FOR CSP PROJECT

Interest Loan % 12.35%‐14%Debt Equity Ratio 70:30Repayment 12 years (excluding construction and grace period)

Construction Period 28‐36 monthsMoratorium Period COD + 6 months subject to a maximum of 4 years

from first disbursement

Cost (with storage of 6‐7 hours) Rs. 20‐ Rs. 25 crs per MWCost (without storage) Rs. 15 – Rs. 20 crs per MWLand 8‐10 acres / per MW

KEY PERFORMANCE INDICATORS:

IRR >=12%

DSCR 1.2

FACR 1.2

2) PRIVATE EQUITY (PE) FUNDING

PE investment in the Indian renewable energy space surged ahead in 2011, with bothdeal volumes and average deal values years.

PE funds and venture capitalists have become active in the Indian renewable energyspace over the past one to two years.

Some of PE funds and venture capitalists have also launched clean energy‐specificfunds targeted at the sector. These include Climate Change Capital, IDFC Private Equity,FE Clean Energy, and ADB’s Clean Resources Asia Growth Fund and Renewable EnergyAsia Fund.

A significant emerging trend is that PE funds are floating their own renewable energystart‐ups. For example, IDFC Private Equity was one of the first funds to set up acleantech company, Green Infra.

The International Finance Corporation, the Acumen Fund, New Silk Route, BessemerVentures, Argonaut Venture Partners, IDFC Private Equity and the FE Clean Energy Groupare some of the entities active in the solar energy space in India.

PE has become the preferred route to set up and expand operations.PE funds to be attracted by bringing more transparency in the profitability and credit

rating where by private equity funds would be attracted.At the same time, “Exit” route for the private funds should be attracted.

LESSONS LEARNTDelay in Land Acquisition/conversion to commercial use .

Improper assessment of site conditions in the beginning.

Inexperienced developers leading to delay in finalization of technology.

Inadequate co‐ordination among the stakeholders while creating evacuation system.

Delay in getting State/Local clearances.

Delay in legal documentation resulting in delay in project implementation.

Lack of experience of developers leads to delay in raising equity.

In the absence of authentic critical data's like DNI (Direct Normal Irradiance) leads tounrealistic projections of CUF(Capacity Utilization Factor) and hence IRRs for projects.

Lack of experience EPC contractors.

Non–factorization of grid penetration levels/strength/availability.

Weak Credit rating of State Utilities/Discoms.

POSSIBLE SOLUTIONS/ WAY FORWARD

Select proven technology suitable for Indian condition at the time of DPR preparation.

Proper due diligence to be carried out in selection of site and creation of evacuation facilities.

Suitable arrangements should be planned for raising equity before financial closure.

Simplification of land acquisition procedures for solar thermal projects.

Setup Single window clearance system for solar projects.

Take adequate steps for completion of legal documents with FI s for release of funds to avoid delay in project progress.

Select experienced EPC contractors with track record.

Realistic assessment of Radiation data and to project practically achievable CUFs. Developers should project realistic Capex and IRRs.

Proper assessment for grid strength must be conducted before site selection.

SUGGESTIONS:

Since there is no solar thermal plant in India. The government should set up a demonstration plant so that:

Acceptance of technology will be established.

Performance would be established to the lender.

Since the technology is new in India, assessment of credit risk is must.

Plain Vanilla funding may not be sufficient. Each infrastructure project has been differently structured.

Foreign lenders are more comfortable lending to projects near completion. Refinancing of rupee loans through ECB is restricted at 25 % of total debt and this cap needs to be removed to let firms raise funds through ECB.

Power firms will certainly benefit if they are able to borrow from international leaders as their overall cost is around 8‐9% as against 13‐14% domestically.

CSP Projects Under‐Development

S.NO

COMPANY NAME

LOCATION SIZE TECHNOLOGY EPC CONTARCTOR

COMPLETION DATE

FIXED TARIFF PER KW (Rs.)

1 Lanco Infratech Ltd

Jaisalmer district of Rajasthan

100MW

Parabolic Trough

LANCO Solar & INITEC Energía

13‐Mar 10.49

2 KVK Energy Ventures Pvt Ltd Project

Jaisalmer district of Rajasthan

100MW

Parabolic Trough

N/A 13‐Mar 11.2

3 Megha Engineering & Infrastructres Ltd

Andhra Pradesh

50 MW

Parabolic Trough

MEIL Green Power Limited

13‐Mar 11.31

4 Godawari Power & Ispat Ltd

Rajasthan 50 MW

Parabolic Trough

Lauren‐Jyoti 20‐Mar‐13 12.2

5 Corporate Ispat Alloys Ltd

Rajasthan 50 MW

Parabolic Trough

Shriram EPC Ltd

13‐Mar 12.24

OPERATIONAL PLANTS

COMPANY NAME LOCATION SIZE TECHNOLOGY EPC CONTARCTOR DEVELOPER PARTNE

1 ACME Bikaner Rajasthan 10MW Power Tower ACME eSolar 2 MNRE R&D Project Gwal

Pahari, Haryana

1 MW Parabolic Trough Abener

OTHER PROJECTS UNDER‐DEVELOPMENT

COMPANY NAME LOCATION SIZE TECHNOLOGY DEVELOPER PARTNER

1 Rajasthan Solar One Rajasthan 10 MW Parabolic Trough Entegra Techint, Archimede Solar Energy, Ronda Reflex and Duplomatic Oleodinamica

2 Bap Solar Power Plant Rajasthan 10 MW Parabolic Dish Sterling

Dalmia Cements N/A

3 NTPC Pilot Project Rajasthan 15MW Parabolic Trough NTPC

4 Andhra Pradesh Project Andhra Pradesh

50MW Parabolic Trough Sunborne Energy Khosla Ventures & General Catalyst Partners

5 Thermal Power Project, Kutch Kutch, Gujarat

25MW Parabolic Trough with Thermal Storage

Cargo Solar Power Gujarat Private Limited

GEMASOLAR ‐ 24 HOURS OF UNINTERRUPTED SUPPLY:

Gemasolar is the first high‐temperature solar receiver with molten salt, which provides 15 hours of thermal storage and an annual capacity factor of about 75%.BACKGROUNDTechnology: Power towerCountry: SpainLand Area: 195 hectaresSolar Resource: 2,172 kWh/m2/yrSize: 19.9 MWCompany: SenerStart Production: Apr‐11Developer(s): Torresol EnergyOwner(s) (%): SENER (60%) AND MASDAR (40%)EPC Contractor: UTE C.T. Solar TresOperator(s): Gemasolar 2006, S.A.THERMAL STORAGEStorage Type: 2‐tank directStorage Capacity: 15 hour(s)Thermal Storage Description:

One cold‐salts tank (290ºC) from where salts are pumped to the tower receiver and heated up to 565ºC, to be stored in one hot‐salts tank (565ºC). Annual equivalent hours = 6,500.