Main differences betweenMain differences betweenoperating leasingoperating leasing

and pure rental*and pure rental*

*connectedthinking

Catalin AlexandruCatalin Alexandru

Lawyer, D&B David si BaiasLawyer, D&B David si Baias

Main differences between operating leasing and pure rental PricewaterhouseCoopersD&B David si Baias

Slide 219 October 2005

Contents

Preliminary comments

Distinction criteria between operating leasing and pure rental

Legal consequences

Main differences between operating leasing and pure rental PricewaterhouseCoopersD&B David si Baias

Slide 319 October 2005

Preliminary comments

Designed to satisfy similar economic needs

Similar CAEN codes

Do rules governing the rental agreement apply to operating leasing ?

– Broad definition of the rental agreement in the Civil Code

– Draft Civil Code

– Recommended approach - separate agreements with separate rules under the legislation in force

Main differences between operating leasing and pure rental PricewaterhouseCoopersD&B David si Baias

Slide 419 October 2005

Distinction criteria

Title of the agreement – not binding on the court (merely indicative)

Option right

Essential element of any leasing agreement under Romanian law

Distinction between option right and the first refusal right occasionally included in rental agreements

The option right is compatible with pure rental

The lessor – always a leasing company in operating leasing

Main differences between operating leasing and pure rental PricewaterhouseCoopersD&B David si Baias

Slide 519 October 2005

Distinction criteria

Term of the agreement – minimum 1 year for operating leasing agreements

Scope of the agreement – restrictions for operating leasing

audio and video recordings, plays, manuscripts, patents and copyright, save for computer programmes

“durable assets” – property capable of being depreciated

Other criteria

The parties’ references to specific legal provisions

Computation of consideration

Main differences between operating leasing and pure rental PricewaterhouseCoopersD&B David si Baias

Slide 619 October 2005

Legal consequences

Lessor’s obligations

Delivery obligation

Operating leasing – the lessor is not liable for failure to deliver – even though the law refers only to financial

leasing, it also applies to operating leasing

Rental – the landlord is liable for failure to deliver

Warranties

Operating leasing – the lessor warrants the quiet use of the leased asset, provided that the lessee has

observed all the clauses of the agreement

Main differences between operating leasing and pure rental PricewaterhouseCoopersD&B David si Baias

Slide 719 October 2005

Legal consequences

Lessor’s obligations

Warranties (cont.)

Operating leasing

Is the lessor liable for hidden defects in the leased asset ?

Rental

The landlord warrants both the quiet use of the assets and their conformity

Obligation to maintain the asset fit for use

Operating leasing – not applicable (the lessee may bring a court action against the supplier)

Rental – applicable

Main differences between operating leasing and pure rental PricewaterhouseCoopersD&B David si Baias

Slide 819 October 2005

Lessee’s obligations

Use of the asset

Operating leasing

Use in accordance with the supplier’s instructions

Rental

Use in accordance with the purpose of the asset

Return of the asset

Operating leasing– subject to lessee’s option right

Rental – mandatory unless the landlord agrees otherwise

Legal consequences

Main differences between operating leasing and pure rental PricewaterhouseCoopersD&B David si Baias

Slide 919 October 2005

Legal consequencesOther consequences

Writ of execution

Operating leasing

Writ of execution in respect of lessee’s obligation to return the leased asset

Writ of execution for movable assets under Law No. 99/1999 (Title VI)

Writ of execution if concluded before a notary public and ascertains a receivable that is documented, determined/determinable and due for payment (less practical)

Rental

Writ of execution for movable assets under Law No. 99/1999 (Title VI)

Writ of execution if concluded before a notary public and ascertains a receivable that is documented, determined/determinable and due for payment

Main differences between operating leasing and pure rental PricewaterhouseCoopersD&B David si Baias

Slide 1019 October 2005

Legal consequences

Other consequences

Contract risk

Operating leasing – under the law, the lessee should bear the risk of loss, destruction and damage to the leased asset and continue to pay the leasing installments – inconsistent with the definition of financial leasing

– should not apply to operating leasing

Rental – the tenant is no longer required to pay rent for the period following destruction of the rented asset

Main differences between operating leasing and pure rental PricewaterhouseCoopersD&B David si Baias

Slide 1119 October 2005

Legal consequences

Termination

Bankruptcy proceedings against the lessee

Operating leasing – the lessor is entitled to terminate the agreement – leasing legislation departs from the

bankruptcy legislation

Rental – the landlord is not entitled to terminate the agreement

– the parties may stipulate automatic termination

Failure to pay the leasing installments / rent

Operating leasing – the lessee must have failed to pay the leasing rate for at least two consecutive months

Rental – the court may assess the extent of the breach

Main differences between operating leasing and pure rental PricewaterhouseCoopersD&B David si Baias

Slide 1219 October 2005

Legal consequences

Termination

Damages in the event of termination / breach

Operating leasing – liquidated damages in the event of lessor’s failure to observe the lessee’s option right

Rental – liquidated damages where the rental agreement is terminated as a result of the

tenant’s breach

Leasing – Movable goods and Leasing – Movable goods and means of transportmeans of transport * *

*connectedthinking

Cristian RadulescuCristian Radulescu

Assistant Manager, PricewaterhouseCoopersAssistant Manager, PricewaterhouseCoopers

Main differences between operating leasing and pure rental PricewaterhouseCoopersD&B David si Baias

Slide 1419 October 2005

Current treatment:

• Supply of services

• Split of capital from interest

• VAT applies to capital element at the VAT rate for goods

• VAT does not apply to the finance element

• VAT is deductible

• Account for VAT at time of instalments

EU Accession

Supply of services – main rule

May be deemed as delivery of goods

Case by case analysis of the leasing contract

VAT Standard rated

Treatment unclear and varies between countries

Supply of services vs. delivery of goods

Main differences between operating leasing and pure rental PricewaterhouseCoopersD&B David si Baias

Slide 1519 October 2005

Country Supply of services Delivery of goods Austria Leasing – VAT under reverse charge Belgium Operational and financial leasing Purchase and rental contracts Czeck Republic

Operational leasing (the user does not have the option to buy)

Financial leasing (the user has the option to buy)

France Leasing with/without option to buy The selling of vehicles and the transfer of ownership (including the case where that transfer occurs at the moment of the final payment)

Germany Leasing – when the vehicle is part of the lessor’s assets

Leasing – when the vehicle is part of the lessee’s assets

Hungary If the transfer of ownership to the vehicle is optional and occurs as a result of a mutual agreement between the parties

If ownership will be automatically transferred in the future

Italy Financial and operational leasing The Netherlands

Operational leasing Financial leasing contracts and rental – purchase contracts

Spain Leasing with an option to buy at the end of the contract up to the moment the vehicle is actuallybought

Leasing with a mandatory option to buy at the end of the contract. The exertion of the option to buy the vehicle, mentioned in the leasing contract.

Sweden Leasing The purchase of the vehicle as a result of a leasing contract

Supply of services vs. delivery of goods in different EU countries

(*) VAT treatment for leasing of means of transport

Main differences between operating leasing and pure rental PricewaterhouseCoopersD&B David si Baias

Slide 1619 October 2005

Cross border leasing

Current treatment

Cross-border leasing + option to buy => importation by the beneficiary

EU Accession

Cross-border leasing + option to buy =>

1) within the Community

Intra-Community acquisition by the leasing company

Obligation to register for VAT purposes

2) with parties outside the Community

Importation

Main differences between operating leasing and pure rental PricewaterhouseCoopersD&B David si Baias

Slide 1719 October 2005

Place of supply

Current treatment

Leasing of:

movable tangible property – where the beneficiary is located

immovable property – where the property is located

EU Accession

New rules:

movable tangible property except means of transport – where the beneficiary is located

means of transport – where the supplier is located

immovable property – where the property is located

Use & enjoyment for leasing transactions with non-EU parties

Main differences between operating leasing and pure rental PricewaterhouseCoopersD&B David si Baias

Slide 1819 October 2005

Place of deliveryCurrent treatment

Transport – where the goods are when the transport begins

No transport – where the goods are put at the disposal of the client

Installation – where the installation is carried out

EU Accession

Transport – where the goods are when the transport begins

No transport – where the goods are put at the disposal of the client

Installation – where the installation is carried out

Distance sales

1. where transport ends (>threshold / option)

2. Where transport begins (<threshold)

Excise goods & new means of transport– where transport ends

Second-hand scheme – MS of origin

Main differences between operating leasing and pure rental PricewaterhouseCoopersD&B David si Baias

Slide 1919 October 2005

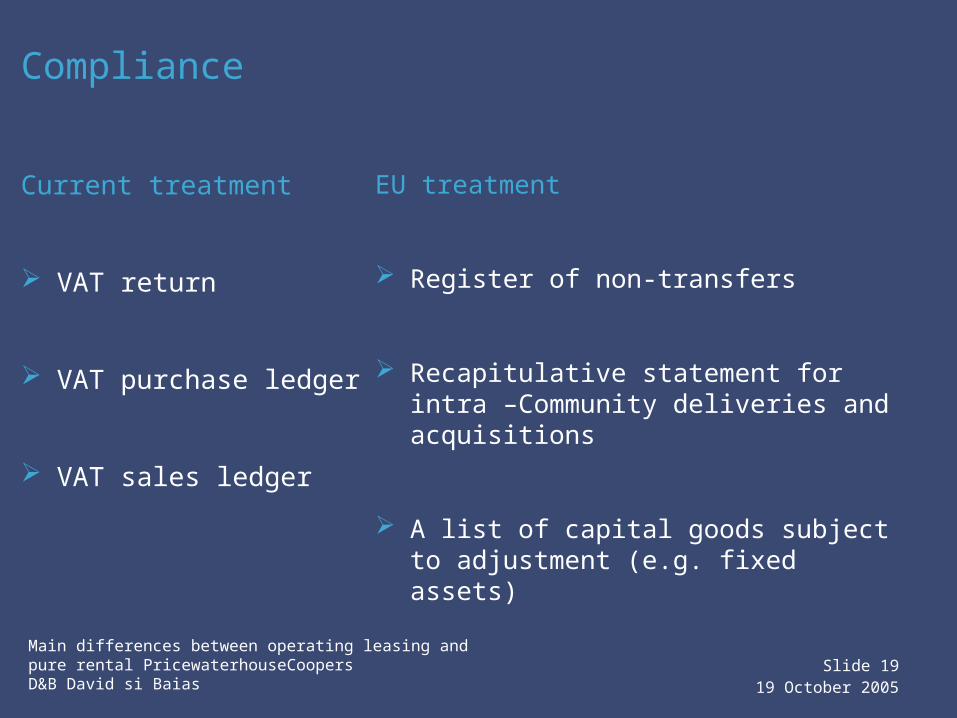

Compliance

Current treatment

VAT return

VAT purchase ledger

VAT sales ledger

EU treatment

Register of non-transfers

Recapitulative statement for intra –Community deliveries and acquisitions

A list of capital goods subject to adjustment (e.g. fixed assets)

Main differences between operating leasing and pure rental PricewaterhouseCoopersD&B David si Baias

Slide 2019 October 2005

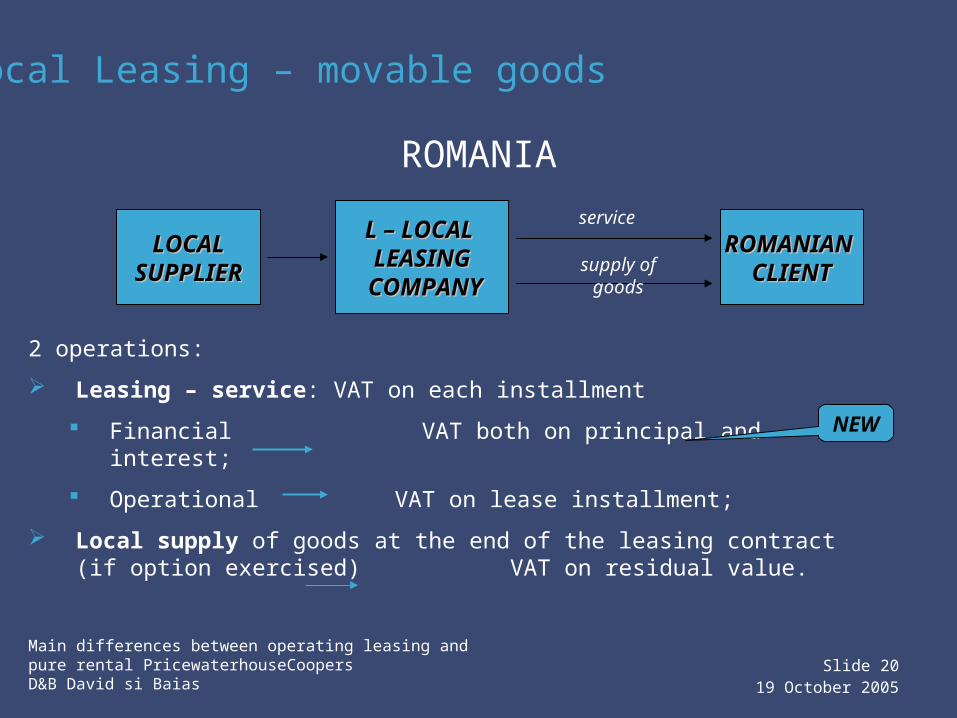

LOCALLOCALSUPPLIERSUPPLIER

L – LOCAL L – LOCAL LEASINGLEASING

COMPANYCOMPANY

ROMANIAN ROMANIAN CLIENTCLIENT

service

supply of goods

ROMANIA

Local Leasing – movable goods

2 operations:

Leasing – service: VAT on each installment

Financial VAT both on principal and interest;

Operational VAT on lease installment;

Local supply of goods at the end of the leasing contract (if option exercised) VAT on residual value.

NEW

Main differences between operating leasing and pure rental PricewaterhouseCoopersD&B David si Baias

Slide 2119 October 2005

supply of goods

RO

EU EU SUPPLIERSUPPLIER

L – LEASINGL – LEASING COMPANYCOMPANY

CLIENTCLIENTservice

HU

ICD ICA

Delivery

3 operations:

Intracommunity acquisition (ICA) in RO / VAT R/C;

Leasing - service: VAT on each installment

Local supply at the end of the contract (if option exercised)

VAT on residual value.

NEW

Local Leasing – movable goods

Main differences between operating leasing and pure rental PricewaterhouseCoopersD&B David si Baias

Slide 2219 October 2005

RORO

FOREIGN FOREIGN SUPPLIERSSUPPLIERS(outside EU) (outside EU)

L – LEASINGL – LEASING COMPANYCOMPANY

CLIENTCLIENTservice

supply of goods

TRTR

export import

Local Leasing – movable goods

3 operations:

Import by L

Import duties (import VAT, customs duties) at the moment of import

Leasing - service: VAT on each installment

Local supply at the end of the contract (if option exercised) VAT on residual value.

Main differences between operating leasing and pure rental PricewaterhouseCoopersD&B David si Baias

Slide 2319 October 2005

ROMANIAN ROMANIAN CLIENTCLIENT

L – LEASINGL – LEASING COMPANYCOMPANY

RO

EU SUPPLIEREU SUPPLIER

service

supply of goods

HU L’

3 operations:

Leasing - service (except MS where leasing = supply of goods!)

always VAT of country of origin (HU)

VAT registered person refund on 8th Directive, subject to limitation in the

Client country of origin

Non-registered person no refund

If option exercised:

Intracommunity acquisition (ICA) in RO by L / VAT R/C

L registration in RO (L’)

Local supply (no transport)

NEW

NEW

NEW

Cross Border Leasing – Means of transport

Main differences between operating leasing and pure rental PricewaterhouseCoopersD&B David si Baias

Slide 2419 October 2005

3 operations:

Leasing - service (except for MS where leasing = supply of goods!);

VAT in RO if Romanian client is a taxable person

R/C if Romanian client is a VAT registered person

If option exercised:

Intracommunity acquisition (ICA) in RO by L / VAT R/C

- L registration in RO

Local supply (no transport)

L – LEASINGL – LEASING COMPANYCOMPANY

serviceMOVABLE GOODS MOVABLE GOODS (except for means(except for means

of transport)of transport)

ROMANIAN ROMANIAN CLIENTCLIENTsupply of goods

ROHU

L’

NEW

Cross Border Leasing – Means of transport

Main differences between operating leasing and pure rental PricewaterhouseCoopersD&B David si Baias

Slide 2519 October 2005

3 operations:

Import performed by L

L registration in RO by FR

Leasing service

Always VAT in RO

Local supply of goods (no transport)

L – LEASINGL – LEASING COMPANYCOMPANY

ROMEANS OF MEANS OF TRANSPORTTRANSPORT

ROMANIAN ROMANIAN CLIENTCLIENT

service

supply of goods

TR L’

NEW

NEW

Cross Border Leasing – Means of transport

Main differences between operating leasing and pure rental PricewaterhouseCoopersD&B David si Baias

Slide 2619 October 2005

service

L – LEASINGL – LEASING COMPANYCOMPANY

MOVABLE GOODS MOVABLE GOODS (except for means(except for means

of transport)of transport)

ROMANIAN ROMANIAN CLIENTCLIENTsupply of goods

ROTR

L’

NEW

Cross Border Leasing – Means of transport excepts means of transport

3 operations:

Import performed by L

L registration in RO by FR

Leasing service

VAT in RO if Romanian client is a taxable person

R/C if Romanian client is a VAT registered person

Local supply of goods (no transport)

NEW

Main differences between operating leasing and pure rental PricewaterhouseCoopersD&B David si Baias

Slide 2719 October 2005

PricewaterhouseCoopers services

Training

Pre-accession review (tailored training included)

Pre-accession Forum

Main differences between operating leasing and pure rental PricewaterhouseCoopersD&B David si Baias

Slide 2819 October 2005

Your worlds Our people

© 2005 PricewaterhouseCoopers. All rights reserved. PricewaterhouseCoopers refers to the network of member firms of PricewaterhouseCoopers International Limited, each of which is a separate and independent legal entity. *connectedthinking is a trademark of PricewaterhouseCoopers.