Recent developments in corporate and partnership p p pplanning

Domestic Tax ConferenceDomestic Tax Conference

May 1, 2013

Disclaimer

► Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young LLP is a client-serving member firm of entity. Ernst & Young LLP is a client serving member firm of Ernst & Young Global Limited located in the US.

► This presentation is ©2013 Ernst & Young LLP. All rights reserved. No part of this document may be reproduced, transmitted or p y potherwise distributed in any form or by any means, electronic or mechanical, including by photocopying, facsimile transmission, recording, rekeying or using any information storage and retrieval system without written permission from Ernst & Young LLP Anysystem, without written permission from Ernst & Young LLP. Any reproduction, transmission or distribution of this form or any of the material herein is prohibited and is in violation of US and international law. Ernst & Young and its member firms expresslyinternational law. Ernst & Young and its member firms expressly disclaim any liability in connection with use of this presentation or its contents by any third party.

► The views expressed by panelists in this webcast are not

Eighth Annual Domestic Tax Conference2

p y pnecessarily those of Ernst & Young LLP.

Circular 230 disclaimer

► Any US tax advice contained herein was not intended or written to be used and cannot be used for the purpose ofwritten to be used, and cannot be used, for the purpose of avoiding penalties that may be imposed under the Internal Revenue Code or applicable state or local tax law provisions.

► These slides are for educational purposes only and are not intended and should not be relied upon asnot intended, and should not be relied upon, as accounting advice.

Eighth Annual Domestic Tax Conference3

Today's presenters

► Phillip Gall► Phillip Gall► Michael Kaibni► Brian Peabody

F W► Franny Wang

Eighth Annual Domestic Tax Conference4

Topics

► Section 355 Monetization Strategies & New No-rule PolicyS ti 355 & REIT El ti► Section 355 & REIT Election

► Partnership IPO Structures► Virtual Incorporations► Virtual Incorporations► Gone & Back Strategy► Key Divestiture Tax Concepts and Complexitiesy p p► Chairman Camp’s Small Business Tax Reform Draft

Proposal

Eighth Annual Domestic Tax Conference5

Section 355 Monetization Strategies & New IRS No-rule Positions

Eighth Annual Domestic Tax Conference6

Background

► A frequent objective in Section 355 transactions is to optimize the capital structures of the businesses of the distributing corporationcapital structures of the businesses of the distributing corporation (“D”) and the controlled corporation (“C”), providing each business with a capital structure tailored to how it operates.

► Another frequent objective is for a corporate group to divest itself of one or more lines of business in order to focus on a core business (or business) However D may want or need to receive compensationbusiness). However, D may want or need to receive compensation for the divestiture but, for a variety of reasons, a sale of the unwanted business may not be possible or practical.

Eighth Annual Domestic Tax Conference7

General Methods

► Generally, there are six methods by which the value can be extracted from a non-core business in connection with the tax-free separation of core and non-core operations. ► Controlled Assumption of Liabilities: assumption of liabilities of the

distributing corporation (D) by the controlled corporation (C);distributing corporation (D) by the controlled corporation (C);► Controlled Cash Distribution: distribution of C’s cash in exchange for

assets transferred by D;► Controlled Cash Purchase: C’s purchase of D’s assets for cash;► Controlled Cash Purchase: C s purchase of D s assets for cash;► Controlled Securities Exchange: exchange of C securities (long-term

debt) for D debt;► Controlled Stock Exchange: exchange of a portion of C stock for D debt; g g p ;

and ► Reverse Direction Spin-off: leverage the non-core business and spin the

core business (together with the proceeds of leveraging)

Eighth Annual Domestic Tax Conference8

Controlled Assumption of Liabilities and Distribution of Cash: Mechanics & Limitations

Mechanics

D S/Hs

Mechanics► D transfers Business 2 to newly formed C in exchange

for C stock, cash (debt funded), and C’s assumption of some of D’s outstanding liabilities and D distributes the stock of C to its shareholders.

C stock, cash, & assumption of D

liabilitiesD

CBusiness 2

Limitations

C

Limitations► Basis Limitation: Assumed liabilities and distributed cash are cumulatively limited to the

basis of the assets transferred by D to C.► To the extent that the liabilities assumed by C and cash distributed to D exceed the basis in the

transferred assets D will recognize gaintransferred assets, D will recognize gain.► Contingent liabilities generally excluded.

► Use of Cash: Cash must be used by D (i) to repay its debt* OR ii) for distribution to its shareholders (i.e., dividends or redemptions).

Eighth Annual Domestic Tax Conference9

shareholders (i.e., dividends or redemptions).

Controlled Securities & Stock Exchange Prior to No-Rule: Mechanics

Mechanics

► D issues $600M principal amount short-term debt (ST debt) to

D S/Hs

$600M ► D issues $600M principal amount short term debt (ST debt) to a financial institution (FI), which holds the debt for its own account, in exchange for cash.

► D transfers Business 2 to a newly formed C in exchange for ► $300M of C securities (long term debt) and

DFIST debt

$600M cash

► $300M of C securities (long term debt), and ► Two classes of C common stock – Class A high vote

(80% vote & 60% value) and Class B low vote (20% vote & 40% value).

D t f th C iti (300M) d Cl B l t

Bus 2

$300M C► D transfers the C securities (300M), and Class B low vote

shares to FI in exchange for the $600M ST debt and distributes the C Class A stock to D’s shareholders in a distribution intended to qualify under Sections 355 and 368(a)(1)(D).D

D S/HsC stock

FI

$300M C securities & C

Class B shares

$600M D Bus 2► FI sells the C securities & Class B shares for cash in a public

offering.C

Bus 2

$600M D Debt

Bus 2

Eighth Annual Domestic Tax Conference10

Bus 2

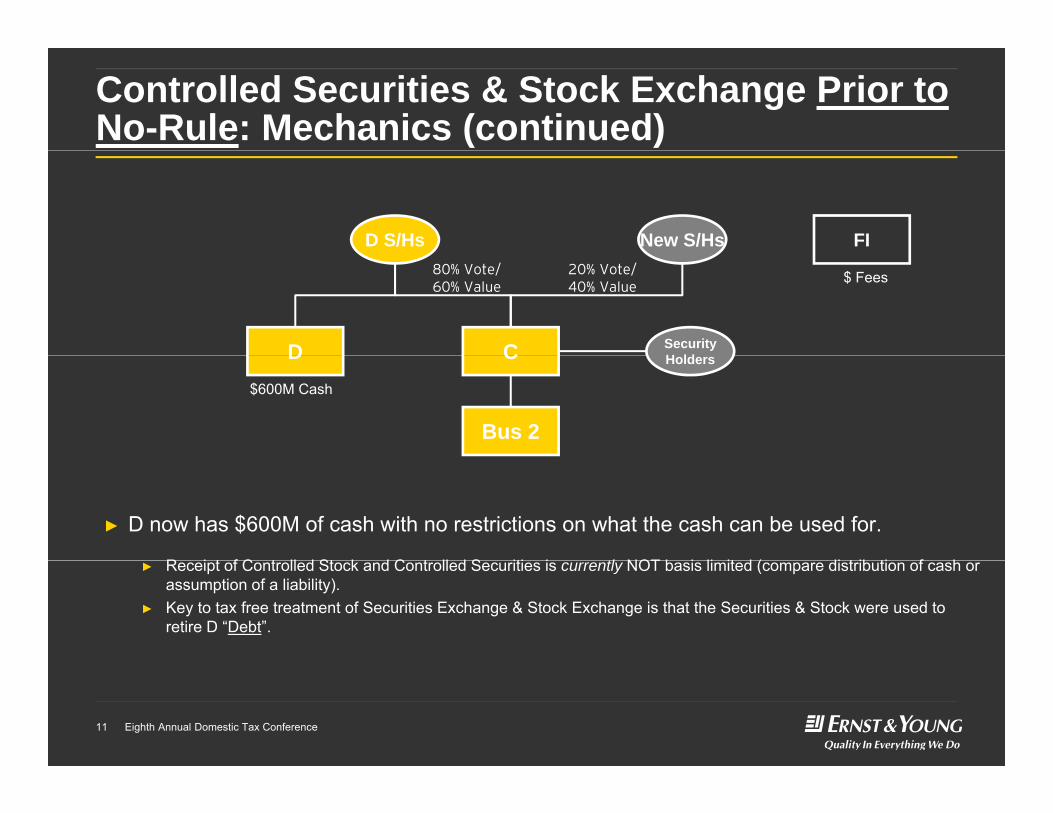

Controlled Securities & Stock Exchange Prior to No-Rule: Mechanics (continued)

D S/Hs New S/Hs FI

D C

80% Vote/60% Value

20% Vote/40% Value

SecurityH ld

$ Fees

D C

Bus 2

$600M Cash

Holders

► D now has $600M of cash with no restrictions on what the cash can be used for.

R i t f C t ll d St k d C t ll d S iti i tl NOT b i li it d ( di t ib ti f h► Receipt of Controlled Stock and Controlled Securities is currently NOT basis limited (compare distribution of cash or assumption of a liability).

► Key to tax free treatment of Securities Exchange & Stock Exchange is that the Securities & Stock were used to retire D “Debt”.

Eighth Annual Domestic Tax Conference11

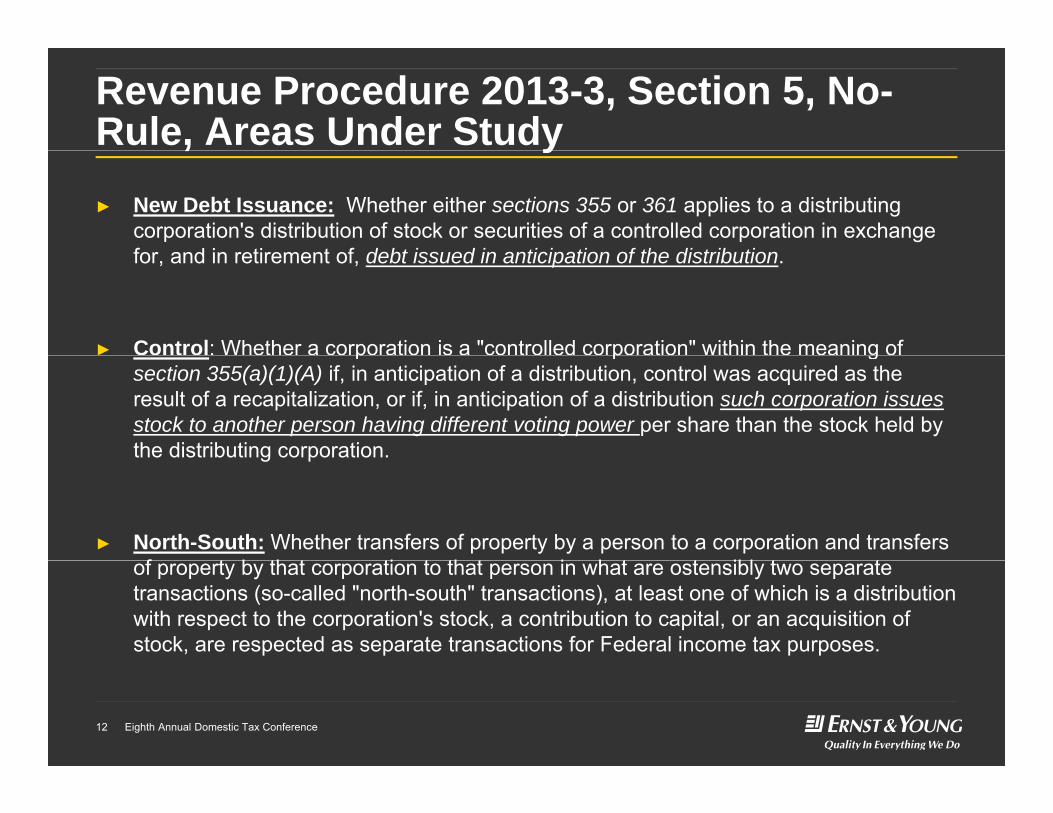

Revenue Procedure 2013-3, Section 5, No-Rule, Areas Under Study, y► New Debt Issuance: Whether either sections 355 or 361 applies to a distributing

corporation's distribution of stock or securities of a controlled corporation in exchange for and in retirement of debt issued in anticipation of the distributionfor, and in retirement of, debt issued in anticipation of the distribution.

► Control: Whether a corporation is a "controlled corporation" within the meaning of p p gsection 355(a)(1)(A) if, in anticipation of a distribution, control was acquired as the result of a recapitalization, or if, in anticipation of a distribution such corporation issues stock to another person having different voting power per share than the stock held by the distributing corporation.g p

► North-South: Whether transfers of property by a person to a corporation and transfers f t b th t ti t th t i h t t ibl t tof property by that corporation to that person in what are ostensibly two separate

transactions (so-called "north-south" transactions), at least one of which is a distribution with respect to the corporation's stock, a contribution to capital, or an acquisition of stock, are respected as separate transactions for Federal income tax purposes.

Eighth Annual Domestic Tax Conference12

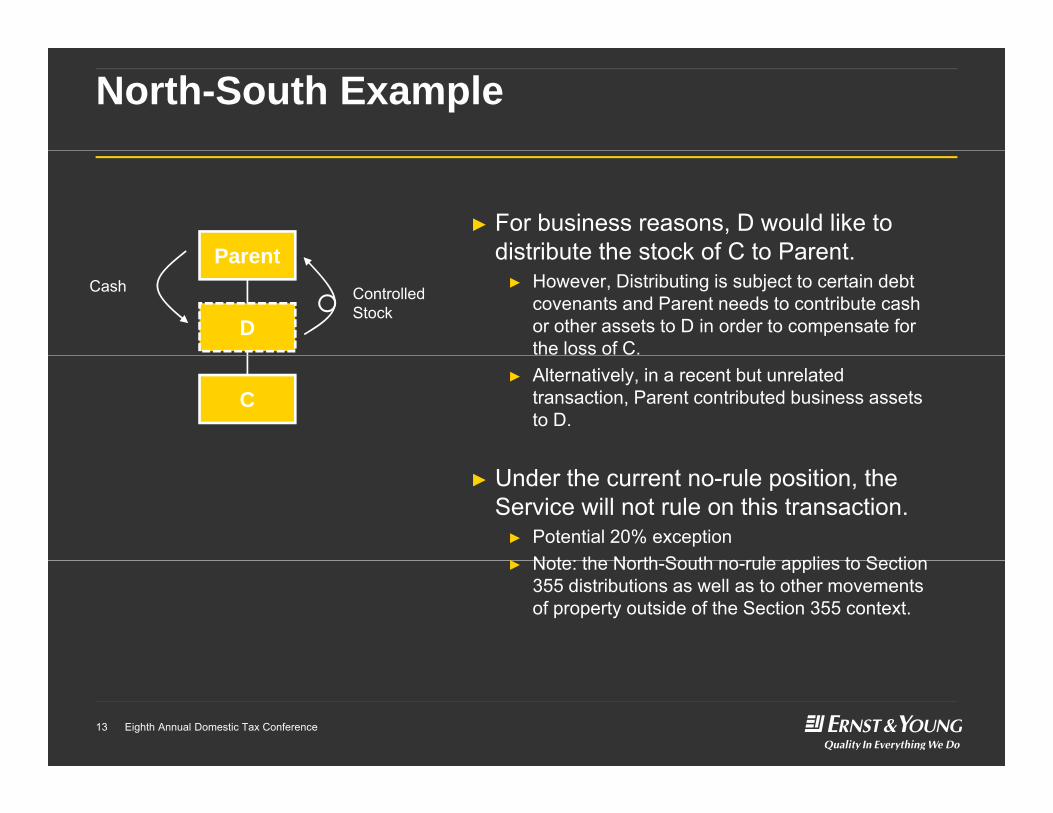

North-South Example

Parent► For business reasons, D would like to

distribute the stock of C to ParentParent

D

Cash Controlled Stock

distribute the stock of C to Parent.► However, Distributing is subject to certain debt

covenants and Parent needs to contribute cash or other assets to D in order to compensate for the loss of C.

C► Alternatively, in a recent but unrelated

transaction, Parent contributed business assets to D.

► Under the current no-rule position, the Service will not rule on this transaction.► Potential 20% exception► Note: the North South no rule applies to Section► Note: the North-South no-rule applies to Section

355 distributions as well as to other movements of property outside of the Section 355 context.

Eighth Annual Domestic Tax Conference13

Section 355 & REIT Election

Eighth Annual Domestic Tax Conference14

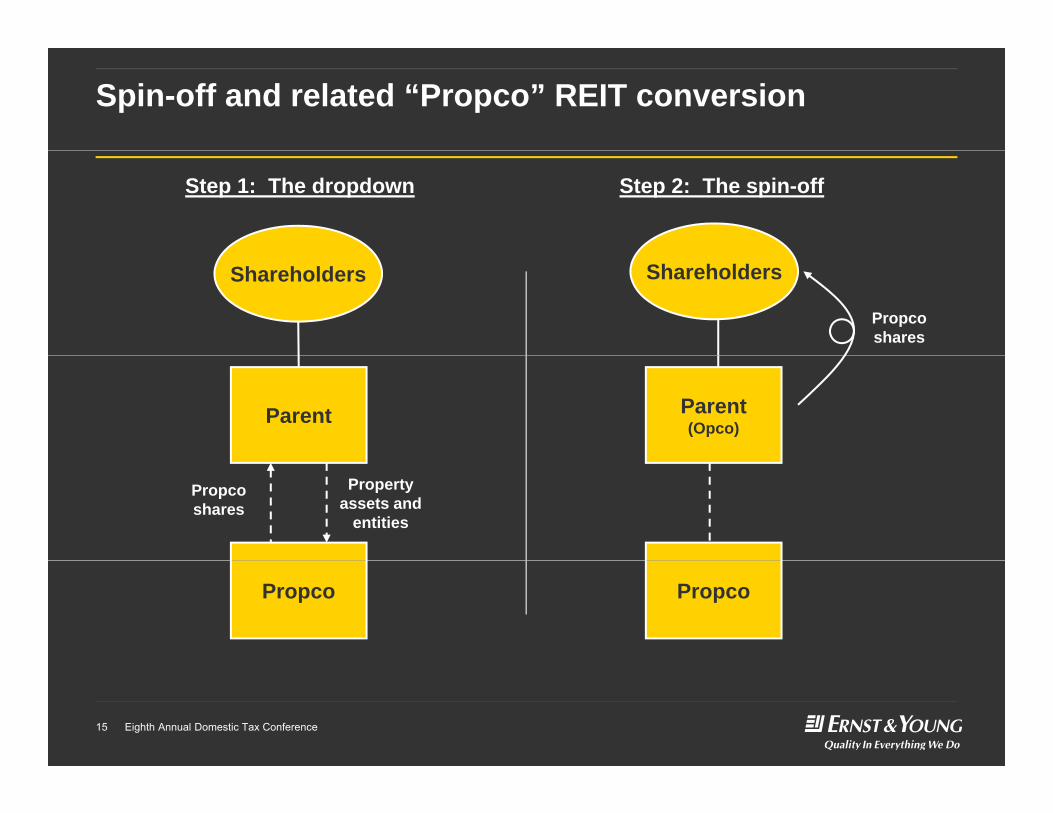

Spin-off and related “Propco” REIT conversion

Step 1: The dropdown Step 2: The spin-off

Shareholders

Propcoshares

Shareholders

Parent Parent(Opco)

Propertyassets and

entities

Propcoshares

Propco Propco

Eighth Annual Domestic Tax Conference15

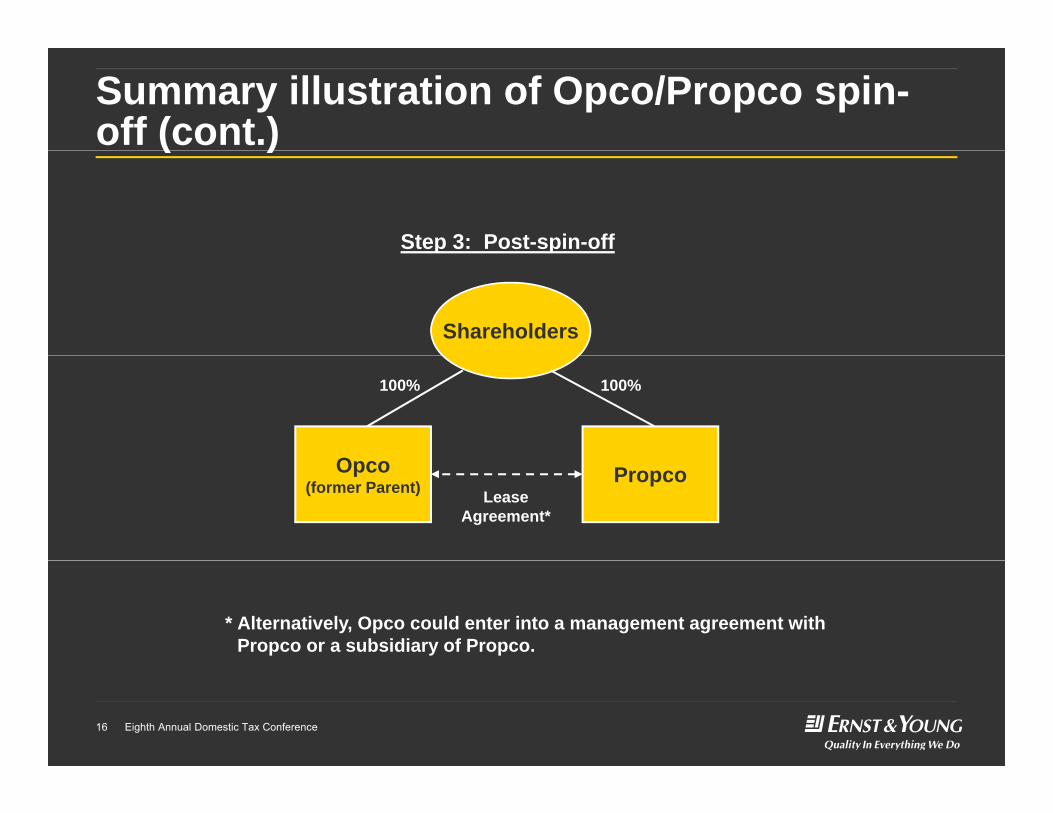

Summary illustration of Opco/Propco spin-off (cont.)( )

Step 3: Post-spin-offp p

Shareholders

O

100% 100%

PropcoOpco(former Parent) Lease

Agreement*

* Alternatively, Opco could enter into a management agreement with Propco or a subsidiary of Propco.

Eighth Annual Domestic Tax Conference16

Partnership IPO Structures

Eighth Annual Domestic Tax Conference17

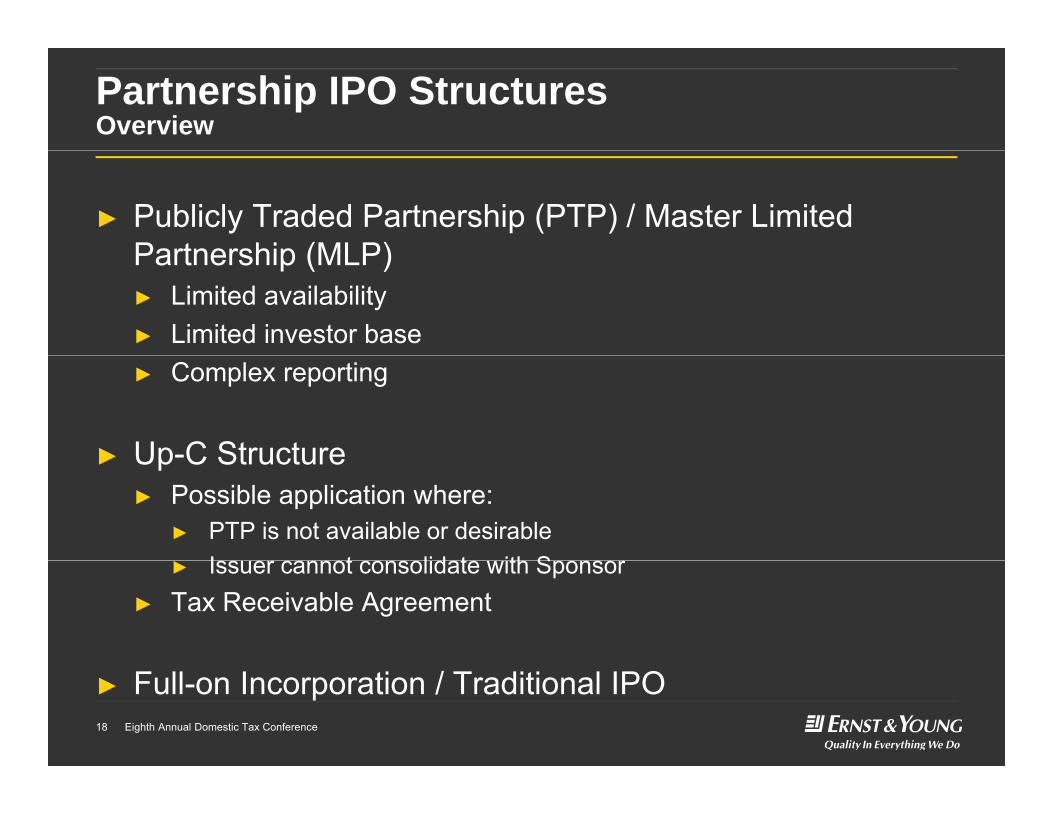

Partnership IPO StructuresOverview

► Publicly Traded Partnership (PTP) / Master Limited Partnership (MLP)Partnership (MLP)► Limited availability► Limited investor base► Complex reporting

► Up-C Structure► Up C Structure► Possible application where:

► PTP is not available or desirableI t lid t ith S► Issuer cannot consolidate with Sponsor

► Tax Receivable Agreement

Eighth Annual Domestic Tax Conference18

► Full-on Incorporation / Traditional IPO

Partnership IPO StructuresPTP/MLP vs. Up-C vs. Traditional

PTP/MLP Up-C Traditional IPO

PublicSponsor PublicSponsorHigh-Vote Sh

PublicSponsor

PubCo

Shares

IPO CoPTP/MLP OpCo

IPO Co.

NonqualifyingIncome

QualifyingIncome

Qualifying & Nonqualifying

Income

Qualifying & Nonqualifying

Income

Eighth Annual Domestic Tax Conference19

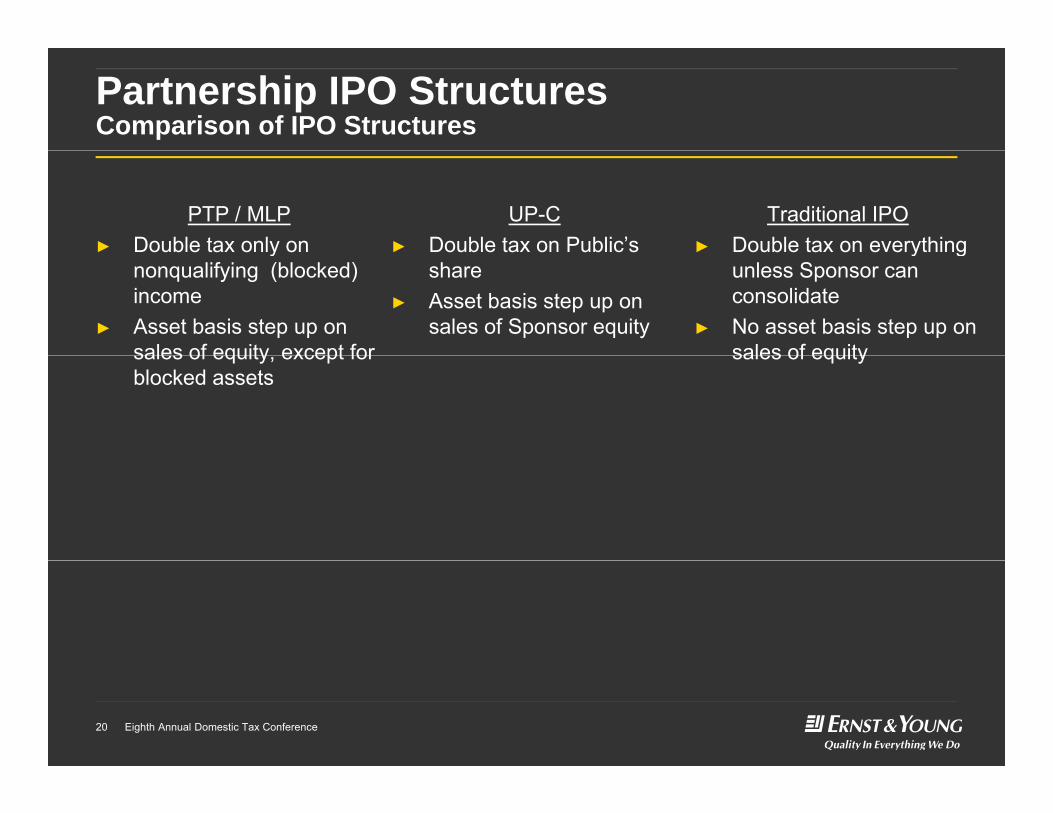

Partnership IPO StructuresComparison of IPO Structures

PTP / MLP► Double tax only on

UP-C► Double tax on Public’s

Traditional IPO► Double tax on everything y

nonqualifying (blocked) income

► Asset basis step up on sales of equity except for

share► Asset basis step up on

sales of Sponsor equity

y gunless Sponsor can consolidate

► No asset basis step up on sales of equitysales of equity, except for

blocked assetssales of equity

Eighth Annual Domestic Tax Conference20

Partnership IPO StructuresUp-C Structure Benefits and Considerations

► Benefits► Tax receivable agreements► Tax receivable agreements

► Cash benefit to Founders► PubCo agrees to pay the Founders a percentage (commonly 85%) of the

cash tax benefit it receives from a positive Section 743(b) adjustment (andcash tax benefit it receives from a positive Section 743(b) adjustment (and other attributes) in OpCo’s assets

► Founders are still subject to a single level of tax► Provides multiple currencies (OpCo interests and PubCo stock) for p ( p )

future acquisitions and/or executive compensation arrangements

► Considerations► Considerations► Anti-churning rules (if PubCo is related to Founders)► Introduces greater complexity from several perspectives (e.g.,

governance operating capital markets accounting tax)

Eighth Annual Domestic Tax Conference21

governance, operating, capital markets, accounting, tax)

Checkable Arrangements (a.k.a. Virtual Incorporations)p )

Eighth Annual Domestic Tax Conference22

Virtual incorporations

► USP operates division X (“Division X”). ► USP also owns 100% of the stock ofBeginning structure ► USP also owns 100% of the stock of

Oldco.► USP wants to incorporate Division X for tax

reasons, but, due to non-tax reasons (e.g.,

g g

USP

, , ( g ,non-transferrable assets, transfer taxes, regulatory, etc.), USP cannot transfer the assets of Division X to another legal entity.

§ ( )OldcoDivision

X ► Reg. §301.7701-3(a) provides that a “business entity” that is not classified as a corporation (i.e., an “eligible entity”) can elect to its classification for US federal tax

OldcoX

elect to its classification for US federal tax purposes. Division X is not an “entity” for purposes of the check-the-box regulations.

Eighth Annual Domestic Tax Conference23

Virtual incorporations (cont’d)

► In order to obtain the benefits of “incorporating” Division X, the

Contract execution

USPprofits interest in Branch

following steps are taken:1. USP and Oldco enter into a contractual

arrangement, under which Oldco will share in the economics of Division X.

Oldco

► See Reg. §301.7701-1(a)(2) (“A joint venture or other contractual arrangement may create a separate entity for federal tax purposes if the participants carry on a trade, business, financial operation, or

t d di id th fit th f ”)Check-the-box election

DivisionX

venture and divide the profits therefrom.”)2. Division X elects to be treated as a

corporation for US federal tax purposes.

► Same result if Division X is a

USP

Oldcobranch.

► See, e.g., PLR 201305006.► “Entity” status considerations – how

i ifi t?

DivisionX

profits interest

Eighth Annual Domestic Tax Conference24

significant?

Gone and back in 120 seconds – Taxable Distributions and Upstream Reorganizationsp g

Eighth Annual Domestic Tax Conference25

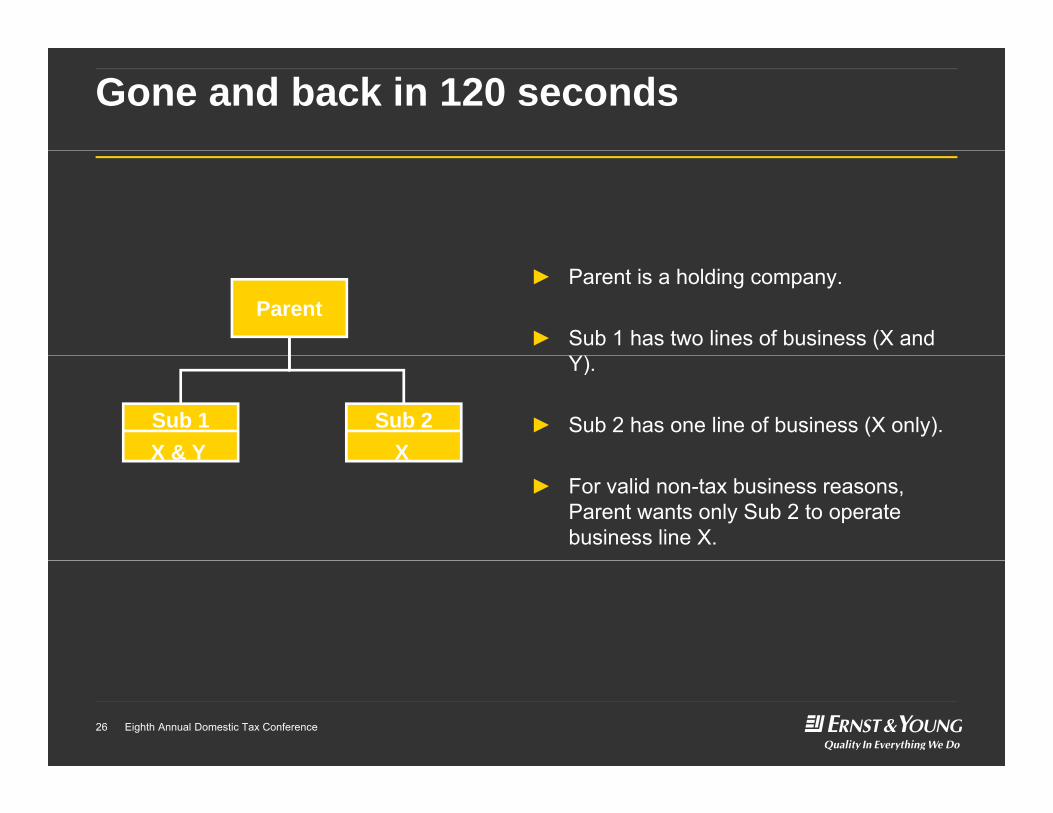

Gone and back in 120 seconds

► Parent is a holding company.

► Sub 1 has two lines of business (X and )

Parent

Y).

► Sub 2 has one line of business (X only).Sub 2Sub 1X & Y X

► For valid non-tax business reasons, Parent wants only Sub 2 to operate business line X.

X & Y X

Eighth Annual Domestic Tax Conference26

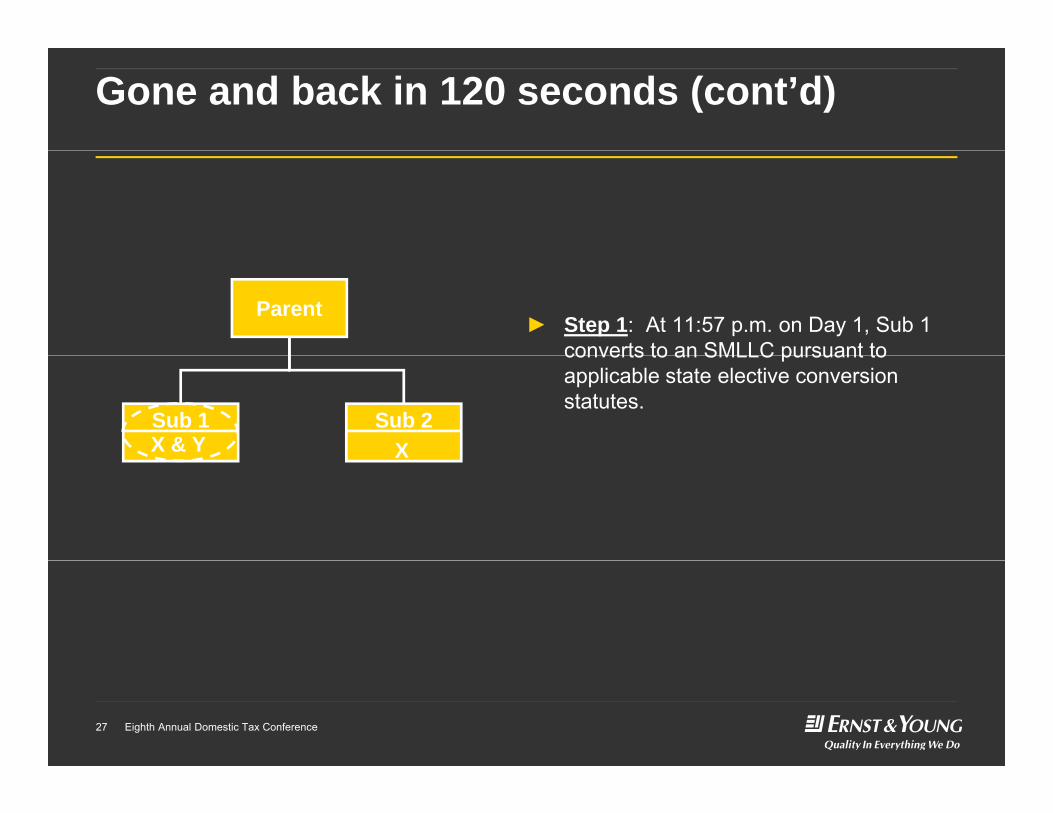

Gone and back in 120 seconds (cont’d)

► Step 1: At 11:57 p.m. on Day 1, Sub 1 converts to an SMLLC pursuant to

Parent

Sub 1

converts to an SMLLC pursuant to applicable state elective conversion statutes.

Sub 2X & Y X

Eighth Annual Domestic Tax Conference27

Gone and back in 120 seconds (cont’d)

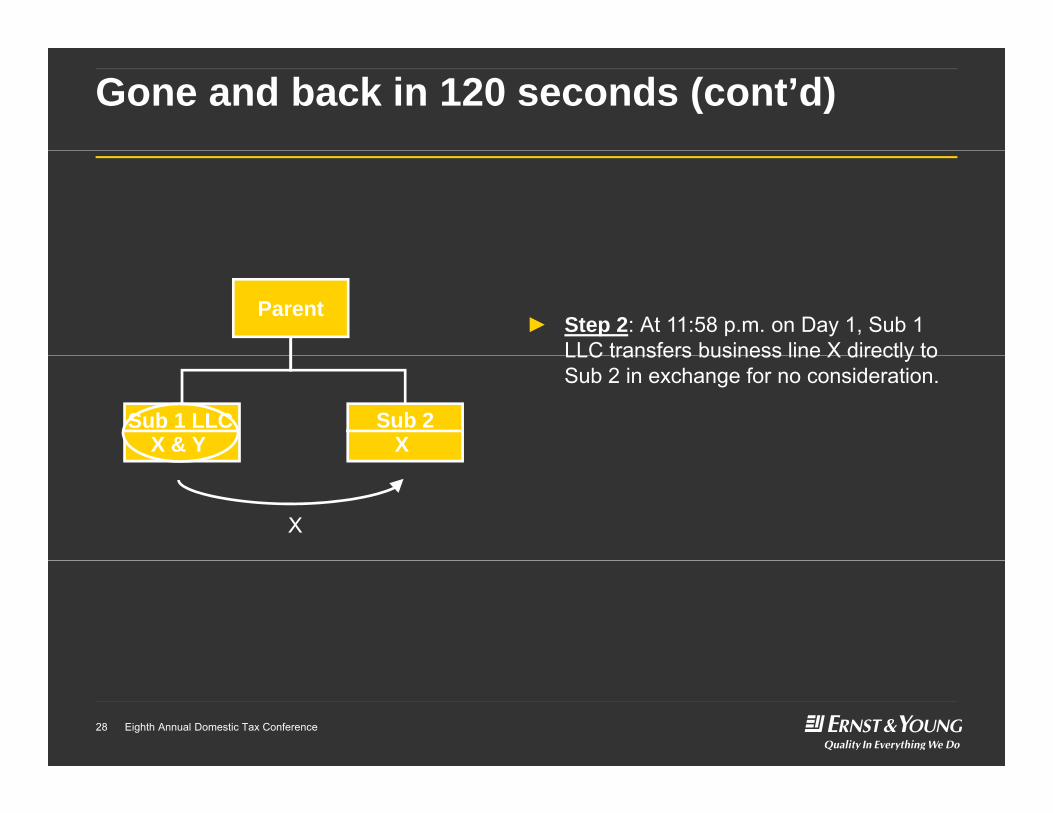

Parent► Step 2: At 11:58 p.m. on Day 1, Sub 1

LLC transfers business line X directly to

Sub 2S1Sub 1 LLC

LLC transfers business line X directly to Sub 2 in exchange for no consideration.

XX & Y

X

Eighth Annual Domestic Tax Conference28

Gone and back in 120 seconds (cont’d)

Parent► Step 3: At 11:59 p.m. on Day 1, Sub 1

LLC converts back to a corporation

Sub 2S1

LLC converts back to a corporation pursuant to applicable state elective conversion statutes.

Sub 1 LLCXY X

Eighth Annual Domestic Tax Conference29

Gone and back in 120 seconds (cont’d)

Parent

► Section 311(b) distribution?

► Section 332 liquidation followed by Section 11:56 p.m.

Sub 2Sub 1

q y351 transfer?

► Sideways reorganization with boot?

► Upstream reorganization?

► See, e.g., PLR 201201012; PLR 201127004.

XX & Y

► See, e.g., PLR 201201012; PLR 201127004.► New “technology?”

► PLR vs. opinion letter.

Parent11:59 p.m.

► State tax consequences.

► Impact of minority shareholder ownership of

Sub 2Sub 1XY

Eighth Annual Domestic Tax Conference30

► Impact of minority shareholder ownership of Sub 1?

Key Divestiture Tax Concepts and Complexitiesp

Eighth Annual Domestic Tax Conference31

Results of Global Corporate Divestment Study Show Significant Planned Divestiture Activity

► Survey of 567 corporate executives representing more than 14 industries across Americas, Asia Pacific, Europe, the Middle East and Africa)

► Significant findings► 46% of respondents are in the process of a divestiture or are planning to divest

within the next 2 yearsy► Sectors most likely to divest include power and utilities, and consumer products ► 50% of respondents indicated that the level of preparation required for a successful

divestiture has increased over the past 2-3 years► 27% of respondents found that "Determining and implementing tax planning" to be► 27% of respondents found that "Determining and implementing tax planning" to be

one of the 3 top challenges of their most recent divestiture► The other two are: (i) negotiating TSAs, and (ii) dealing with the complexity of closing

► One of 5 key leading practices of successful divestitures is separation planning, y g p p p g,including tax planning ► The other four are: (i) portfolio management, (ii) consider ing the full range of potential

buyers, (iii) articulating compelling value/growth story for each buyer, and (iv) preparing rigorously for the divestment process

Eighth Annual Domestic Tax Conference32

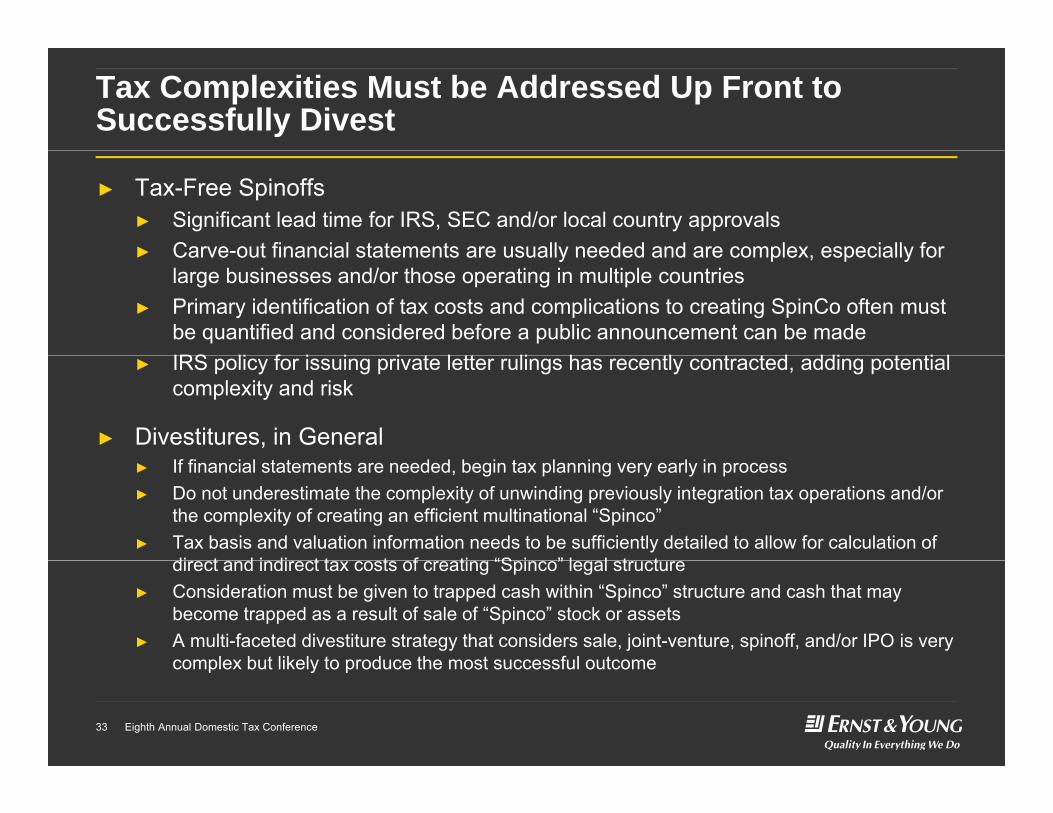

Tax Complexities Must be Addressed Up Front to Successfully Divest

► Tax-Free Spinoffs► Significant lead time for IRS, SEC and/or local country approvals► Carve-out financial statements are usually needed and are complex especially for► Carve out financial statements are usually needed and are complex, especially for

large businesses and/or those operating in multiple countries► Primary identification of tax costs and complications to creating SpinCo often must

be quantified and considered before a public announcement can be madeIRS li f i i i t l tt li h tl t t d ddi t ti l► IRS policy for issuing private letter rulings has recently contracted, adding potential complexity and risk

► Divestitures, in General► If financial statements are needed, begin tax planning very early in process► Do not underestimate the complexity of unwinding previously integration tax operations and/or

the complexity of creating an efficient multinational “Spinco”► Tax basis and valuation information needs to be sufficiently detailed to allow for calculation of

di t d i di t t t f ti “S i ” l l t tdirect and indirect tax costs of creating “Spinco” legal structure► Consideration must be given to trapped cash within “Spinco” structure and cash that may

become trapped as a result of sale of “Spinco” stock or assets► A multi-faceted divestiture strategy that considers sale, joint-venture, spinoff, and/or IPO is very

complex but likely to produce the most successful outcome

Eighth Annual Domestic Tax Conference33

complex but likely to produce the most successful outcome

Chairman Camp’s Small Business Tax Reform Draft Proposalp

Eighth Annual Domestic Tax Conference34

Camp Draft ProposalOverview

► On March 12, 2013, House Ways and Means Committee Chairman Dave Camp (R-MI) released a discussion draft for reforming the taxDave Camp (R MI) released a discussion draft for reforming the tax rules affecting small businesses.

► The draft is intended to solicit feedback from a broad range of stakeholders practitioners economists and members of the generalstakeholders, practitioners, economists, and members of the general public on how to improve on the proposal.

► The draft presents two options for the reform of pass-through entities► Option 1 – Retains Subchapter K and Subchapter S as separate.

► Option 2 – Unified rules for partnerships and S corporations.

Eighth Annual Domestic Tax Conference35

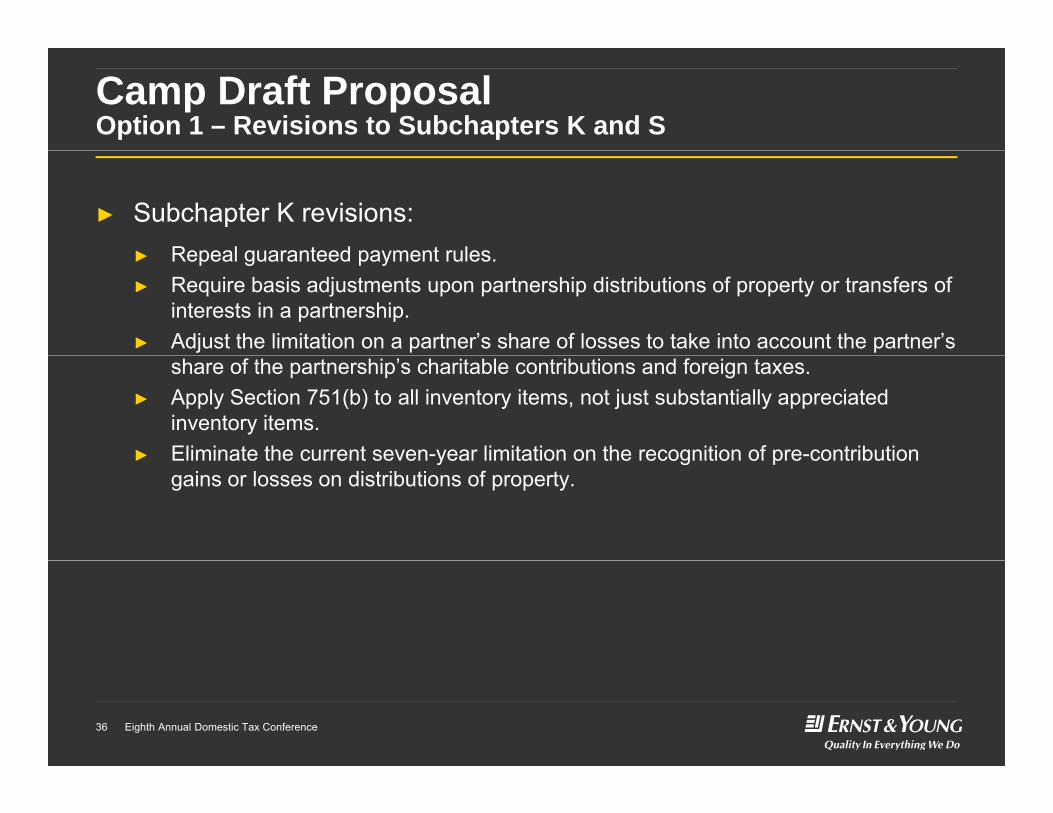

Camp Draft ProposalOption 1 – Revisions to Subchapters K and S

► Subchapter K revisions:► Repeal guaranteed payment rules► Repeal guaranteed payment rules.► Require basis adjustments upon partnership distributions of property or transfers of

interests in a partnership.► Adjust the limitation on a partner’s share of losses to take into account the partner’s

share of the partnership’s charitable contributions and foreign taxes.► Apply Section 751(b) to all inventory items, not just substantially appreciated

inventory items.► Eliminate the current seven-year limitation on the recognition of pre-contribution► Eliminate the current seven year limitation on the recognition of pre contribution

gains or losses on distributions of property.

Eighth Annual Domestic Tax Conference36

Camp Draft ProposalOption 1 – Revisions to Subchapters K and S

► Subchapter S revisions:► A permanent reduction in the recognition period for the built-in gains tax under► A permanent reduction in the recognition period for the built in gains tax under

Section 1374 from 10 years to 5 years. Correspondingly, the draft would make permanent the rule that installment sales are governed by the provision that was applicable when the sale occurred.

► Increase to 60 percent (from 25 percent) the amount of gross receipts that an S► Increase to 60 percent (from 25 percent) the amount of gross receipts that an S corporation with Subchapter C earnings and profits may have before being subject to the tax on excess passive investment income.

► Permit nonresident aliens to be potential current beneficiaries of electing small business trusts (ESBTs)business trusts (ESBTs).

Eighth Annual Domestic Tax Conference37

Camp Draft ProposalOption 2 – Unified Rules for Passthroughs

► This option repeals Subchapter K and Subchapter S and replaces them with a uniform set of rules that apply to non-publicly tradedthem with a uniform set of rules that apply to non publicly traded businesses for Federal tax purposes regardless of how the business is organized for state law purposes. ► Would the rules apply to any non-public entity?► Would publicly traded partnerships be eligible for flow-through treatment?► Transition rules?

► The new rules would:► Allow contributions of property and money on a tax-free basis.► Maintain the passthrough nature of an entity’s items (and preserve the character of

those items).► Permit special allocations of only net ordinary income or loss net capital gain or► Permit special allocations of only net ordinary income or loss, net capital gain or

loss, and tax credits (and prohibit special allocations of individual items within each of those three categories).

Eighth Annual Domestic Tax Conference38

Camp Draft ProposalOption 2 – Unified Rules for Passthroughs

► The new rules would (continued):► Require basis adjustments upon a distribution of property by the passthrough entity► Require basis adjustments upon a distribution of property by the passthrough entity

or a transfer of an interest in a passthrough entity.► Require entity-level withholding on the passthrough entity’s income and gain with a

corresponding credit for the owner’s tax reporting.► Limit deductions for losses to an owner’s basis in his passthrough interest but► Limit deductions for losses to an owner s basis in his passthrough interest, but

allow excess losses to be carried forward indefinitely.► Limit tax-free distributions (of money and property) to an owner’s basis in his

passthrough interest. ► Require passthrough entities to recognize gain on all distributions of appreciated

property and require owners to take a carryover basis in the distributed property (to preserve losses in distributed property).

► Allow owners to include entity-level debt (both recourse and non-recourse) in their y ( )basis in their passthrough interest.

► Allow owners to be treated as employees of the business.

Eighth Annual Domestic Tax Conference39

Questions and answers

Eighth Annual Domestic Tax Conference40

Thanks for participating

Eighth Annual Domestic Tax Conference41

![Ill & o No. 9 & fi & & z No. 15 El 0 c (D c CD < (D F < F & (D F & TJíi … · 2020-04-23 · No. 15 El -F (D s IÌíj t1J fi o o fili 3 B fi (D E (D þJJ 0) < < b ßJ D < Hi] 9](https://cdn.vdocument.in/doc/165x107/5ea7e57a93a609563d587341/ill-o-no-9-fi-z-no-15-el-0-c-d-c-cd-d-f-f.jpg)