Replacement Problem

Introduction

• The problem of replacement is felt when the job

performing units such as men, machines,

equipments, parts etc., become less effective or

useless due to either sudden or gradual deterioration

in their efficiency, failure or breakdown.

• By replacing them with new ones at frequent

intervals, maintenance and other overhead costs can

be reduced.

• However, such replacements would increase the

need of capital cost for new ones.

Introduction…

Example:

• A machine becomes more and more expensive to

maintain after a no. of years, a railway time table

gradually becomes more and more out of date, an

electric light bulb fails all of a sudden, pipeline is

blocked, or an employee loses his job etc.

• In all such situations, there is a need to formulate a

most economic replacement policy for replacing

faulty units or to take some remedial special action

to restore the efficiency of deteriorating units.

Introduction…

Following are the situations when the replacement of

certain items needs to be done:

• An old item has failed and does not work at all, or

the old item is expected to fail shortly.

• The old item has deteriorated and works badly or

requires expensive maintenance.

• A better design of equipment has been developed.

Introduction…

Replacement problems can be classified into the

following two categories:

• When the equipment deteriorate with time and the

value of he money

1. Does not change with time.

2. Changes with time.

• When the units fail completely all of a sudden.

Types of Failure

Gradual Failure

It is progressive in nature. That is, as the life of an

item increases, its operational efficiency also

deteriorates resulting in

1. increased running (maintenance & operating)

cost

2. decrease in its productivity

3. decrease in the resale or salvage value.

Mechanical items like pistons, rings, bearings etc. and

automobile tyres fall under this category.

Types of FailureSudden Failure

This type of failure occurs in items after some

period of giving desired service rather than

deterioration while in service. The period of desired

service is not constant but follows some frequency

distribution which may be progressive, retrogressive

or random in nature.

1.Progressive failure: If the probability of failure of

an item increases with the increase in its life, then

such failure is called progressive failure. (light bulb or

tubes fails progressively)

Types of Failure2.Retrogressive failure: If the probability of failure

in the beginning of the life of an item is more but as

time passes the chances of its failure become less,

then such failure is said to be retrogressive.

3.Random failure: In this type of failure, the constant

probability of failure is associated with items that

fail from random causes such as physical shocks,

not related to age. For example, vacuum tubes in air

born equipment have been found to fail at a rate

independent of the age of the tube.

Replacement of Equipment that deteriorates gradually Generally the cost of maintenance & repair of certain items

increases with time and a stage may come when these costs

become so high that it is more economical to replace the

item by a new one.

Replacement policy when value of money does not change

with time

The aim here is to determine the optimum replacement age

of an equipment/item whose running/maintenance cost

increases with time and the value of money remains static

during that period. Let

Replacement policy when value of money does not change with time…

C : capital cost of equipment

S : Scrap (waste) value of equipment

n : number of years that equipment would be in use

f(t) : maintenance cost function

A(n) : average total annual cost.

Case 1: When t is a continuous variable. If the

equipment is used for n years, then the total cost

incurred during this period is an under:

cost. totalannual average the

equalscost emaintenanc when replaced be shouldequipment at thesuggest th This

A(n) f(n)at 0A(n)dn

d

Clearly,

A(n) dt f(t) n

1

n

S - C f(n)

f(n) n

1dt f(t)

n

1

n

S - C- or

0A(n)dn

d

havemust wecost, minimumFor

dt f(t) n

1

n

S - C TC

n

1 A(n)

iscost totalannual Average

dt f(t) S - C

Cost eMaintenanc Cost Scrap -Cost Capital TC

2

2

n

0

n

022

n

0

n

0

Replacement policy when value of money does not change with time…

Case 2: When t is a discrete variable. Here period of

time is considered as fixed and n, take the values

1,2,3,…. Then

cost. totalavg. syear'

previous than theless iscost emaintenanc yearsnth theandyear nth in thecost totalavg. than the

more isyear the1)(n in thecost emaintenanc theif years,n of end at theequipment theReplace

:policyt replacemen optimal thesuggests This

1)A(n f(n) 0 1)-A(n- A(n)

shown that becan it Similarly,

A(n). 1)f(n 0 A(n) -1)A(n Thus,

A(n)-1)f(n1n

1 A(n)-1)A(n

1)f(nA(n)n 1n

1

1)f(n1n

1 f(t) S - C

1n

1

f(t) 1n

1

1n

S - C 1)A(n

can write weFor this,

01)-A(n A(n) and 0 A(n) 1)A(n or

A(n) 1)-A(n and A(n) 1)A(n

for which n, of aluefor that v minimum be willA(n) Now,

f(t) n

1

n

S - C A(n)

n

1t

1n

1t

1t

n

Example:

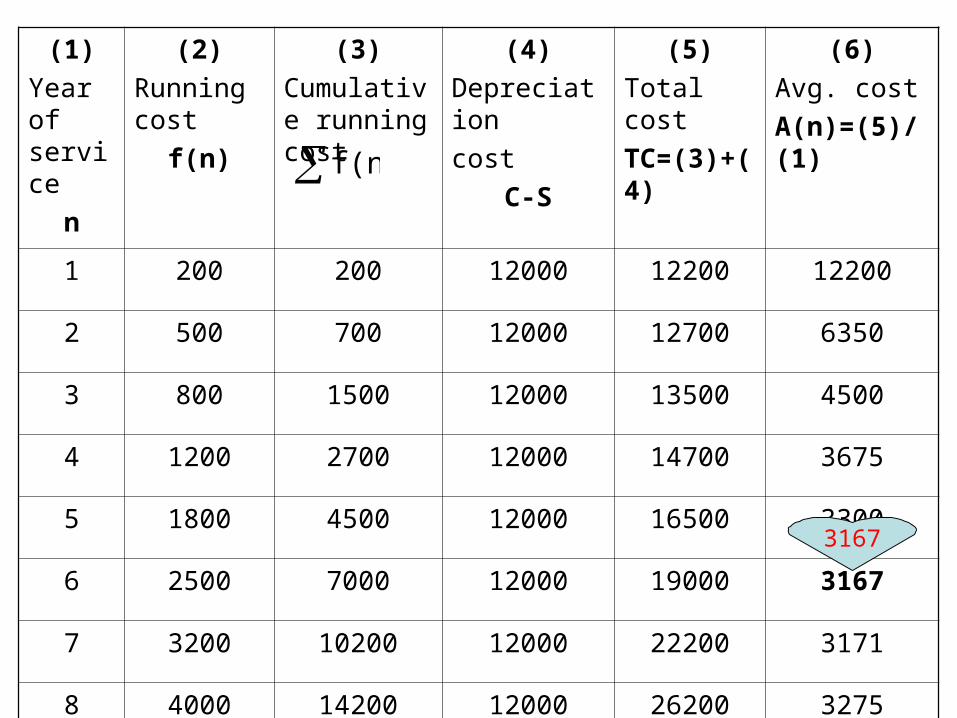

A firm is considering replacement of a machine, whose cost

per year is Rs. 12,200 and the scrap value, Rs. 200. The

running (maintenance & operating) costs in rupees are

found from experience to as follows:

Year 1 2 3 4 5 6 7 8

Running Cost 200 500 800 1200 1800 2500 3200 4000

When should the machine be replaced?

We have given:

The running cost, f(n)

The scrap value (s) = 200

Cost of the machine (C)= 12,200

To find out the optimal time n when the

machine should be replaced, we need to

calculate an avg. Total cost per year

during the life of the machine.

(1)

Year of service

n

(2)

Running cost

f(n)

(3)

Cumulative running cost

(4)

Depreciation

cost

C-S

(5)

Total cost

TC=(3)+(4)

(6)

Avg. cost

A(n)=(5)/(1)

1 200 200 12000 12200 12200

2 500 700 12000 12700 6350

3 800 1500 12000 13500 4500

4 1200 2700 12000 14700 3675

5 1800 4500 12000 16500 3300

6 2500 7000 12000 19000 3167

7 3200 10200 12000 22200 3171

8 4000 14200 12000 26200 3275

f(n)

3167

Replacement policy when value of money changes with time

When the time value of money is taken into

consideration, we shall assume that (1) the

equipment in question has no salvage value, and (2)

the maintenance costs are incurred in the beginning

of the different time periods.

• Since it is assumed that the maintenance cost

increases with time and each cost is to be paid just

in the start of the period, Let the money carry a rate

of interest r per year.

Replacement policy when value …

• Thus, a rupee invested now will be worth (1+r) after

a year, (1+r)2 after 2 years, and so on.

• In this way the Rs. invested today will be worth

(1+r)n after n years. Or, if we have to make a

payment of 1 Rs. In n years time, it is equivalent to

making a payment of (1+r)-n Rs. Today.

• The quantity (1+r)-n is called the present worth

factor (pwf) of 1 Rs. spent in n years time from

now onwards

• Thus, a rupee invested now will be worth (1+r) after

a year, (1+r)2 after 2 years, and so on.

• In this way the Rs. invested today will be worth

(1+r)n after n years. Or, if we have to make a

payment of 1 Rs. In n years time, it is equivalent to

making a payment of (1+r)-n Rs. Today.

• The quantity (1+r)-n is called the present worth

factor (pwf) of 1 Rs. spent in n years time from

now onwards

Replacement policy when value …

Replacement policy when value…

• (1+r)n is known as the payment compound amount

factor (Caf) of 1 Rs. spent in n years time.

• Let the initial cost of the equipment be C and let Rn

be the operating cost in year n. • Let v be the rate of interest in such a way that

v= (1+r)-1 is the discount rate (pwf).• Then the present value of all future discounts costs

Vn associated with a policy of replacing the

equipment at the end of each n years is given by

Replacement policy when value…

Then the present value of all future discounts costs Vn

associated with a policy of replacing the equipment

at the end of each n years is given by

)v(1

1Vv1RVVV similarly and

)v(1

1Vv1Rv

V)v(1 RvCVV

write weFor this,

0VV and 0VV

for which n, of aluefor that v minimum be willV Now,

)v(1

1 RvCv*RvC

....Rv.......RvRvvRCRv.......RvvRRCV

1nnn1n

1nn

1nnnn

n1n

1-n

0kk

kn1n

n1-nn1n

n

1n

1-n

0kk

k

0k

kn1-n

0kk

k

1n12n

22n

11n

n01n1n

22

10n

Replacement policy when value…

Since v is the value of money, it will always be less

than 1, and therefore 1-v will always be +ve. This

implies that Vn/(1-Vn+1) will always be +ve.

1n

0k

k1n

n1n21n

1n2

210

1n

n1n1-nnnnn1n

vv))(1v-(1

Rv.......vv1

Rv...........RvvRRCR

V v)-(1R0VV and V v)-(1R 0VV

Hence,

The expression which lies between Rn-1and Rn is called the weighted avg. cost of all the previous n years with weights 1,v,v2,…..,vn-1 respectively.

Replacement policy when value…

• Hence the optimal replacement policy of the

equipment after n periods is:

(a) Do not replace the equipments if the next

period’s operating cost is less than the weighted

avg. of previous cost.

(b) Replace the equipments if the next period’s

operating cost is greater that the weighted avg. of

previous costs.

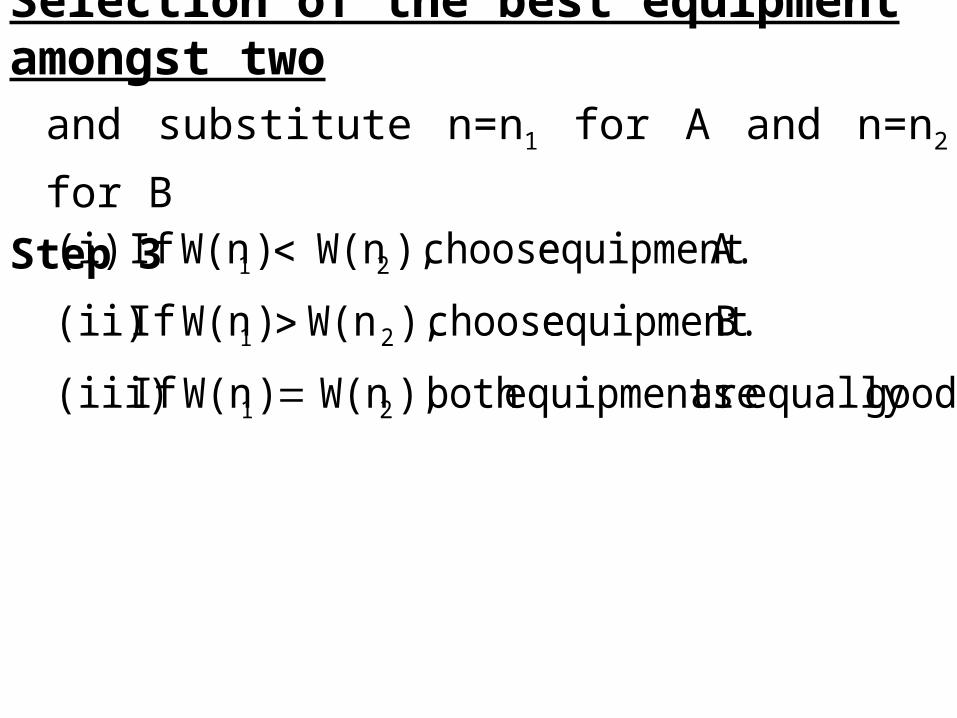

Selection of the best equipment amongst two

Step 1 Considering the case of 2 equipments (A & B),

we first find the best replacement age for both

equipments by making use of Rn-1<(1-v)Vn<Rn.

Let the optimal replacement age for A & B comes

out to be n1 and n2 respectively.

Step 2 Compute the fixed annual payment (or

weighted avg. cost) for A & B by using the formula

1n21n

1n2

210

n v.......vv1

Rv...........RvvRRCW

Selection of the best equipment amongst two

and substitute n=n1 for A and n=n2 for B

Step 3

good.equally are equipmentsboth ), W(n ) W(nIf (iii)

B.equipment choose ),W(n ) W(nIf (ii)

A.equipment choose ), W(n ) W(nIf (i)

21

21

21

Example

• Let the value of money be assumed to be 10% per

year and suppose that machine A is replaced after 3

years whereas machine B is replaced after every 6

years. The yearly costs of both the machines are

given below:Year 1 2 3 4 5 6

Machine A

1,000 200 400 1,000 200 400

Machine B

1,700 100 200 300 400 500

Determine which machine should be purchased (replaced).

Solution :

Rs. 461 2765/6 B Machine ofcost Yearly Avg.

Rs. 504 1512/3 A Machine ofcost Yearly Avg.

Rs. 2765 (0.9091) X 500

(0.9091) X 400 (0.9091) X 300 (0.9091) X 200 (0.9091) X 1001700

is yearssix for B ofcost discounted total theAgain,

approx. Rs. 1512(0.9091) X 400 (0.9091) X 2001000

is years 3for A of orth)(present wcost discount totalThe therefore,

9190.011

10

10100

100 v

isyear one of period aover

spent be money to theofrth present wo theinterest, of rate thecarriesmoney theSince

5

432

2

purchased.or repleced be shouldA machine Hence,

period. same over the B machinehan costlier t less 118 Rs. isamount This

Rs. 2647 (0.9091) X 400

(0.9091) X 200 (0.9091) X 1000 (0.9091) X 400 (0.9091) X 2001000

be A will ofcost total then thealso,A machinefor

periodyear 6consider weif So, different. are considered are costs thefor which periods the

sinceunfair isn comparisio theBut, B. machine with is advantageapparent that theshows This

5

432

Replacement of equipment that fails suddenly