© Ericsson AB 2009 Commercial in confidence 8 July 20092

Esta demostrado que las telecomunicaciones ayudan a reducir el impacto de la crisis

económica mundial siempre y cuando se aceleren las inversiones para las redes de

banda ancha móvil creando fuentes de trabajo, con regulaciones que promuevan el cuádruple

play y que faciliten la cobertura en zonas rurales ó de bajos ingresos

© Ericsson AB 2009 Commercial in confidence 8 July 20093

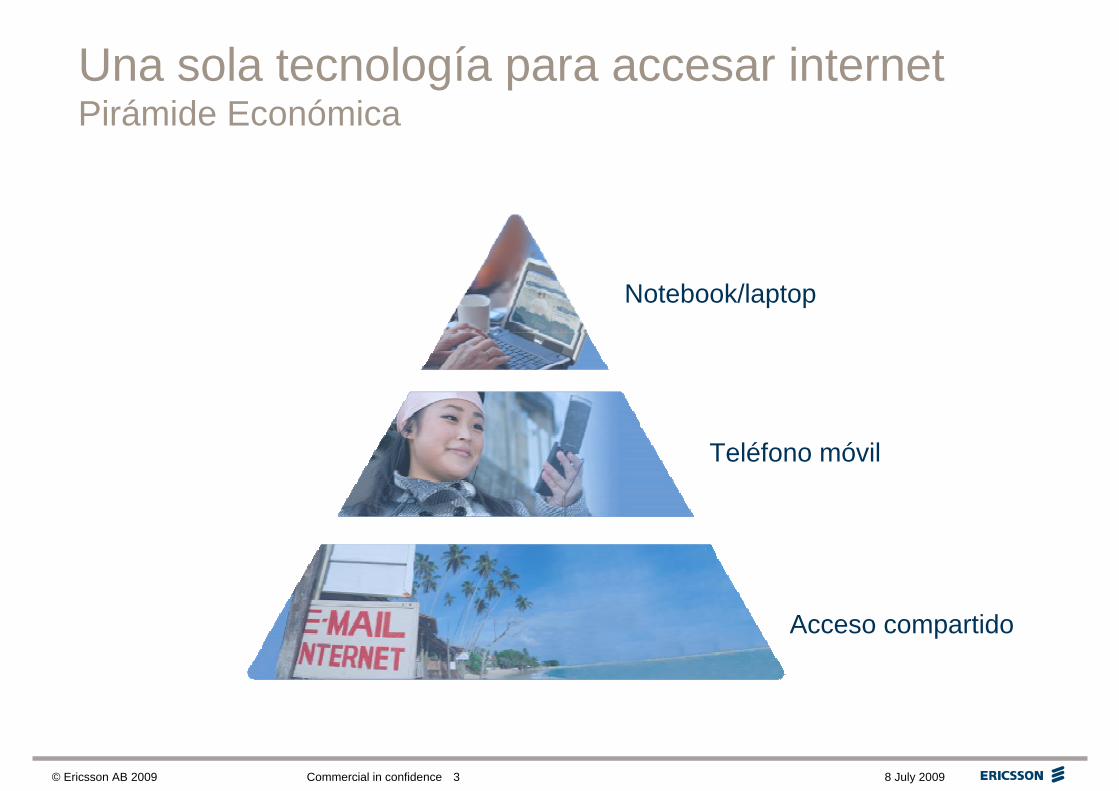

Una sola tecnología para accesar internetPirámide Económica

Notebook/laptop

Teléfono móvil

Acceso compartido

© Ericsson AB 2009 Commercial in confidence 8 July 20094

Internet como detonador económico

DesarrolloAdministración de

recursos

Negocios

Instituciones

La gente

Acceso a los mercados globales

Acceso instantáneo a la información

Encontrar o crearse un

trabajo

Rápida comunicación,

menos desplazamiento

Compras y transacciones desde el hogar

Acceso al conocimiento y

creación de nuevos negocios

Creación de comunidades en

línea, nuevosAmigos y contactos

El país

Base de datos común y

actualizada

Una nación moderna - Reducción de la pobreza- Estabilidad- Igualdad- Desarrollo ( crecimiento del PIB)

Personales

Source: Ericsson market research in Indonesia, South Africa and Rwanda

Mejora la coordinación interna y la

comunicación

© Ericsson AB 2009 Commercial in confidence 8 July 20095

El efecto Internet

Antes de banda ancha:– Imprimir reportes en un centro de

negocios– minibus 6h viaje redondo– Pérdida de dos días de trabajo + costos

de viaje

Con banda ancha móvil:– Retrazo de pago de prestamos

se redujo

– Incremento de ganancias de 30%

– Los clientes se beneficiaron al reducirse las tasas de interés

Sr. Robert, Director de región de un banco de Nyamata, Rwanda

Reporta a oficina principal en Kigali 2 veces a la semana

Source: Ericsson market research

© Ericsson AB 2009 Commercial in confidence 8 July 20096

Llegar a lo mas bajo de la pirámideCaso Bangladesh

Modelo de negociosUS$ 1,140 (PC)US$ 185 por modem EDGEUS$ 8.60/12 cargo mensual por servicio

Ingreso mensual US$ 160 – 260Servicios que se ofrecen

US$ 0.30 por hora por navegación

US$ 0.30 por una cuenta e-mail US$ 0.15 por resultados de la escuelaUS$ 0.07 por impresión de una hoja

US$ 0.70 por hora de Skype con video

© Ericsson AB 2009 Commercial in confidence 8 July 20097

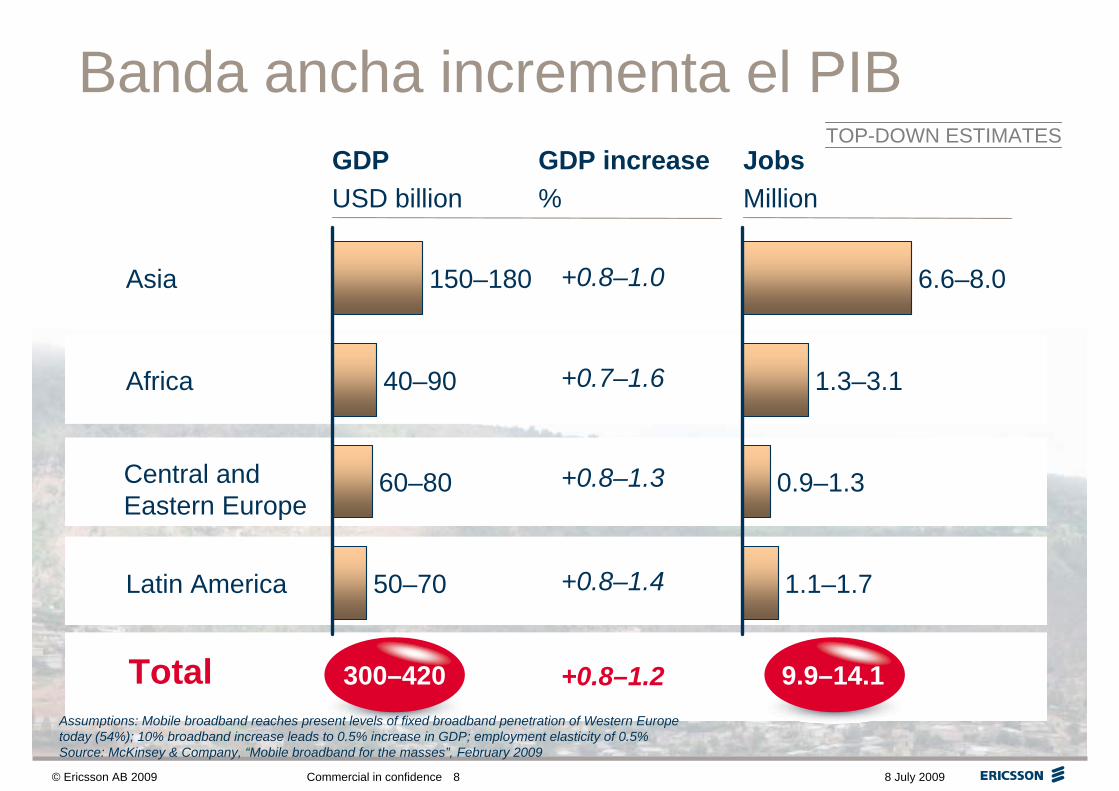

Banda ancha incrementa el PIB

Un aumento en los enlaces de banda ancha del 10 %, contribuirá con un alza del PIB nacional de 1.3%

(Fuente: Resultado de estudio del Banco Mundial, “Información y comunicación para el desarrollo de 2009”)

© Ericsson AB 2009 Commercial in confidence 8 July 20098

6.6–8.0

1.1–1.7

1.3–3.1

0.9–1.3

TOP-DOWN ESTIMATESGDPUSD billion

Latin America

Africa

Asia 150–180

40–90

60–80

50–70

JobsMillion

GDP increase%

+0.8–1.0

+0.7–1.6

+0.8–1.4

+0.8–1.3

Total 300–420 9.9–14.1+0.8–1.2

Central and Eastern Europe

Assumptions: Mobile broadband reaches present levels of fixed broadband penetration of Western Europe today (54%); 10% broadband increase leads to 0.5% increase in GDP; employment elasticity of 0.5%Source: McKinsey & Company, “Mobile broadband for the masses”, February 2009

Banda ancha incrementa el PIB

© Ericsson AB 2009 Commercial in confidence 8 July 20099

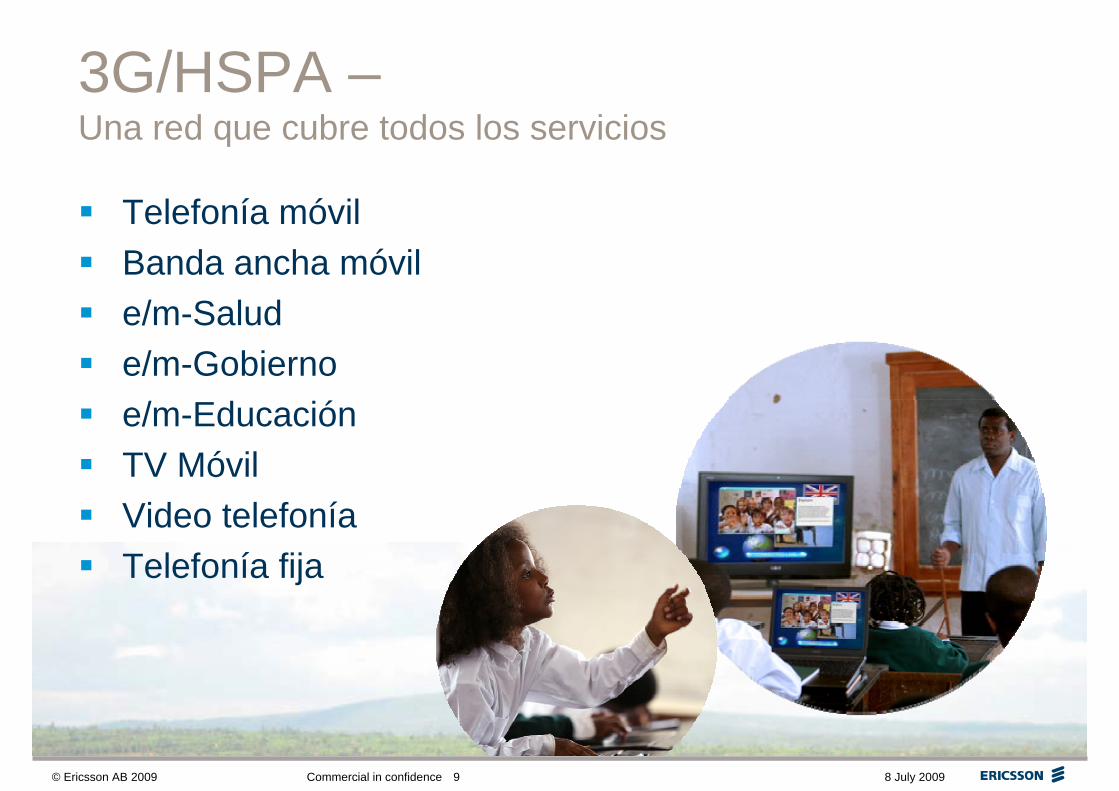

3G/HSPA –Una red que cubre todos los servicios

Telefonía móvilBanda ancha móvile/m-Salude/m-Gobiernoe/m-EducaciónTV MóvilVideo telefoníaTelefonía fija

© Ericsson AB 2009 Commercial in confidence 8 July 200910

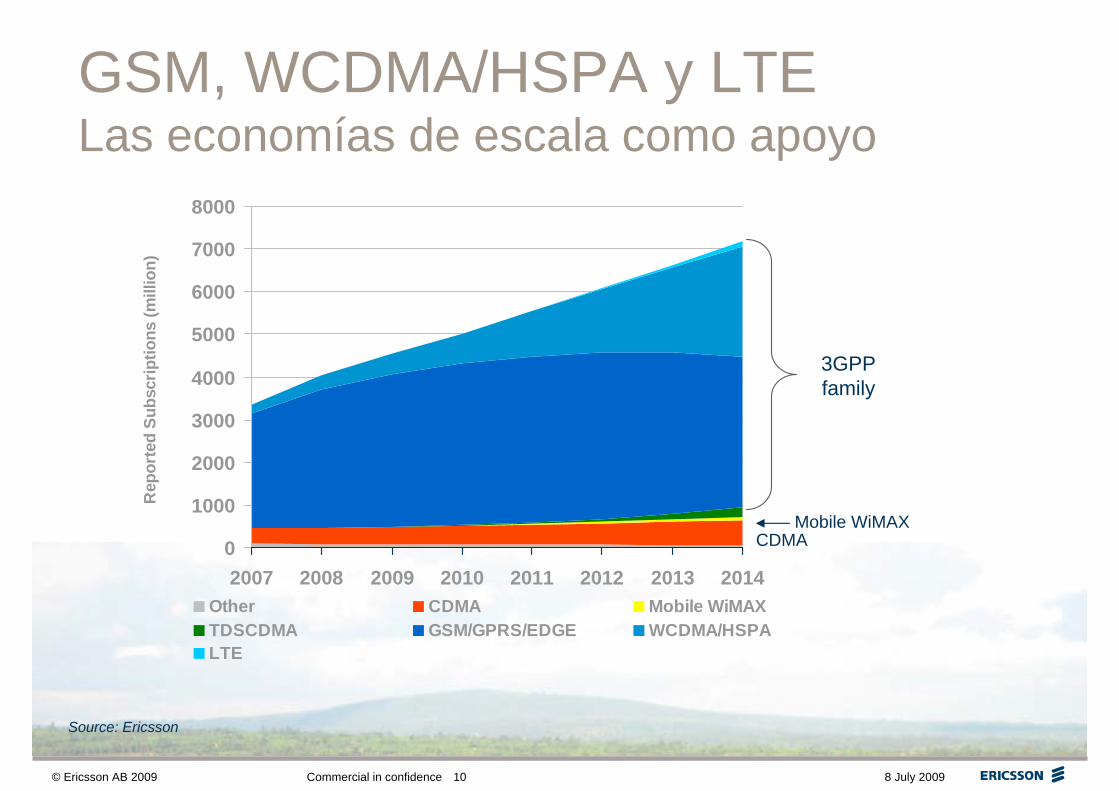

GSM, WCDMA/HSPA y LTE Las economías de escala como apoyo

Source: Ericsson

3GPP family

Mobile WiMAXCDMA0

1000

2000

3000

4000

5000

6000

7000

8000

2007 2008 2009 2010 2011 2012 2013 2014

Rep

orte

d Su

bscr

iptio

ns (m

illio

n)

Other CDMA Mobile WiMAXTDSCDMA GSM/GPRS/EDGE WCDMA/HSPALTE

© Ericsson AB 2009 Commercial in confidence 8 July 200911

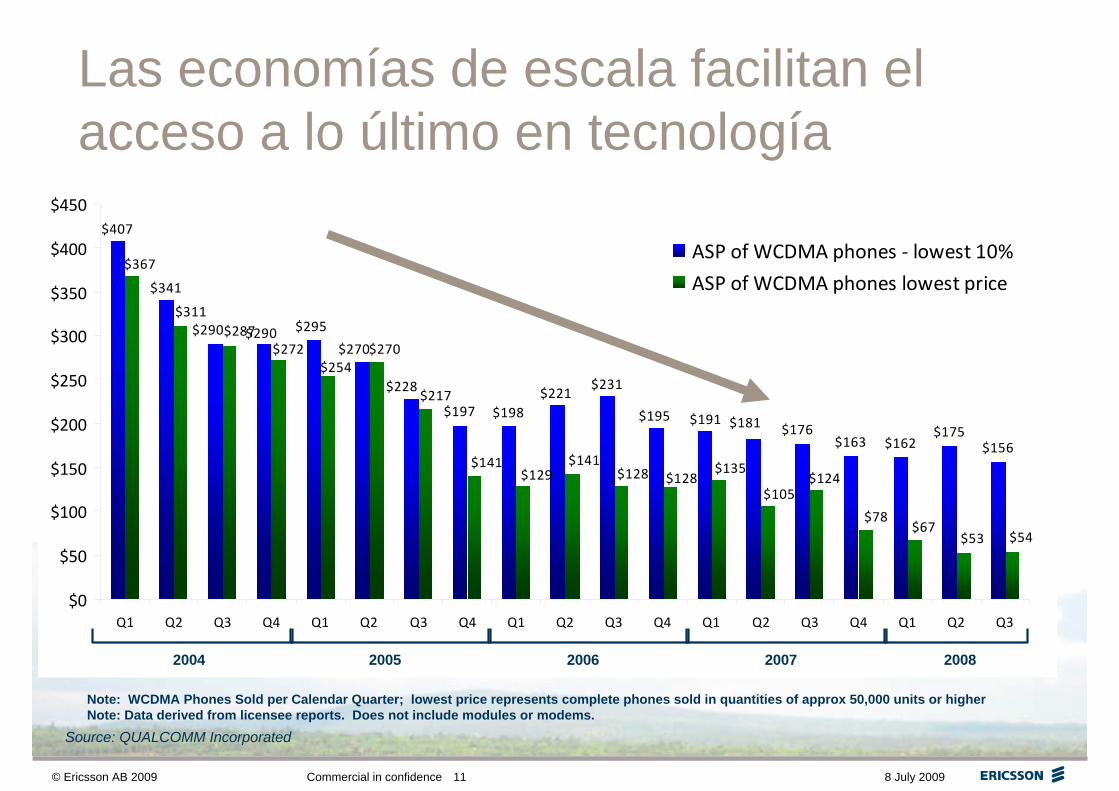

Las economías de escala facilitan el acceso a lo último en tecnología

Source: QUALCOMM Incorporated

Note: WCDMA Phones Sold per Calendar Quarter; lowest price represents complete phones sold in quantities of approx 50,000 units or higherNote: Data derived from licensee reports. Does not include modules or modems.

$163 $162$175

$156

$407

$341

$290 $290 $295

$270

$228

$197 $198$221

$231

$195 $191 $181 $176

$53 $54

$367

$311$287

$272$254

$270

$217

$141$129

$141$128 $128

$135

$105$124

$78$67

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

ASP of WCDMA phones ‐ lowest 10%

ASP of WCDMA phones lowest price

2004 2005 2006 2007 2008

© Ericsson AB 2009 Commercial in confidence 8 July 200912

Evolución continua de capacidades

3G

3G/HSPA

HSPA Evolution

LTE

2002 2005 2008/2009 2009

384 kbps

3.6Mbps

21/28/42 Mbps

~150Mbps

Peak rate

2007

7/14Mbps

LTE Advanced

20131 GbpsTarget

© Ericsson AB 2009 Commercial in confidence 8 July 200913

Banda ancha sustentable¿Como llegar a los segmentos de bajos ingresos en una forma rentable?

-Baja renta para banda ancha

-Terminales económicas

-Reducción de CAPEX

-Bajo OPEX

-Compartición de Infraestructura

© Ericsson AB 2009 Commercial in confidence 8 July 200914

>50% of PC households addressable at 10 USD/month- Bangladesh

Source: Ericsson ConsumerLab study in Bangladesh 2007Base: the 37% that were interested in getting broadband out of 2,500 interviews

0%

20%

40%

60%

80%

100%

0 5 10 15 20 25Broadband Subscription Cost per Household [USD/Month]

Add

ress

able

mar

ket*

Expensive Acceptable

Expensive

Cheap

Reasonable

© Ericsson AB 2009 Commercial in confidence 8 July 200915

Regional Broadband Tariffs – South East Asia

Sources: Service Provider websites, Dec 16 2008

MBB median

tariff: $21

Maxis (M) $22.65 TM(F)$22.36

Celcom & Maxis (M)$28.46

Celcom (M)$19.72

DiGi (M)$19.17

Globe (F)$21.05

Maxis (F) $25.56

Maxis (F)$14.52

Globe (F)$52.90

TM (F)$54.60

StarHub (C) $18.34 M1 (M) $18.90 Digitel (M) $21.14

TRUE (F) $25.81

SMART (F)$42.21

TRUE (F)$21.75

SMART (F)$63.48

Indosat (M)$51.75

SingTel (F)$22.95

GP (M) $14.90 Indosat (M) $10.35

M1 (M)$25.08

TM (F)$77.84

SingTel (F)$31.39

StarHub (C)$29.26

M1 (C)$33.84

SingTel (F)$43.50

SingTel & StarHub (M)$50.75

$-

$10

$20

$30

$40

$50

$60

$70

$80

- 1 000 2 000 3 000 4 000 5 000 6 000 7 000 8 000

Bandwidth [kbps]

Mon

thly

Tar

iff [U

S$]

© Ericsson AB 2009 Commercial in confidence 8 July 200916

Bringing down Cost per bit

Asset Sharing/NW Utilization

Transport

RNC & Core

RAN

Service differentiation

Terminals

x10 spectrum efficiency & extended coverage

Flexible Ethernet Migration & FTTx x5 capacity

Tunnelling, Flat-architecture/SAE>x10 RNC Capacity in 3 years, Terabit core

Economies of scale ⇒ $70 modems

Intelligent Traffic shaping and Priority Handling

Sharing sites and Transport Network

© Ericsson AB 2009 Commercial in confidence 8 July 200917

The base case Cost and cost drivers of Mobile Broadband

$/Sub/month

OPEX

Typical MBB network*Total cost ~7-10 $/Sub/month

CAPEX

Main cost drivers

International BW, 1.1

Sales & Marketing, License & Service Fees, 1.4

Customer Support, 0.6NW O&M, 0.8

RAN, 2.0

Core & Service Layer, 0.4Backhaul, 0.7

ITC, 0.4

0

1

2

3

4

5

6

7

8⇒ Number of Node Installations⇒ BH Traffic ⇒ BH Traffic

⇒ Number of Nodes & BH Traffic

⇒ Power, traffic, Maintenance, Site rental⇒ Number of subscribers &SLA

⇒ Campaigns, subs subsidies and licensefees

⇒ BH Traffic & Traffic mix

Source: Ericsson

*Usage: 3 GB (21 kbps in BH)Speed: 1.5 MbpsGSM Sites Available

© Ericsson AB 2009 Commercial in confidence 8 July 200918

Large cost differences for international bandwidth

Lowest lease price of STM-1 cables to/from the US. African prices are for cables connecting Africa and Europe or Asia.* Kenya: Expected price 2H 2009 when new cables are deployedSource: Ericsson

$400

$350$319

$300

$147

$94 $94

$21$39$51

Egypt

South

Africa

India

Kenya

*

Colombia Peru

Argenti

naKore

an R

ep

Singap

ore

Nordics

Mon

thly

cos

t for

Inte

rnat

ion

Gat

eway

C

apac

ity (U

SD

/Mbp

s/m

onth

)

© Ericsson AB 2009 Commercial in confidence 8 July 200919

HSPA results year oneClaro, Brazil (part 1)

Focus AreaClaro installs HSPA network to boost revenue and deliver innovative services such as television and video streaming and online gamingHSPA network used to deliver broadband access where fixed-line infrastructure is poor or doesn’t exist

Implementation of 3G/HSPA servicesNetwork launched November 2007Ideal spectrum (850MHz) to cost effectively serve the vast countryBy October 2008 HSPA technology rolled out in about 280 cities in 20 states of Brazil and available to >70 million people Broadband tariffs based on average throughput speed

* Q2 2008

Key Facts BrazilPopulation: 191,908,500GDP (per capita): US$ 9500Fixed line penetration: 20%Mobile penetration: 75%Internet penetration: 35.2%Broadband penetration: 3.5%

© Ericsson AB 2009 Commercial in confidence 8 July 200920

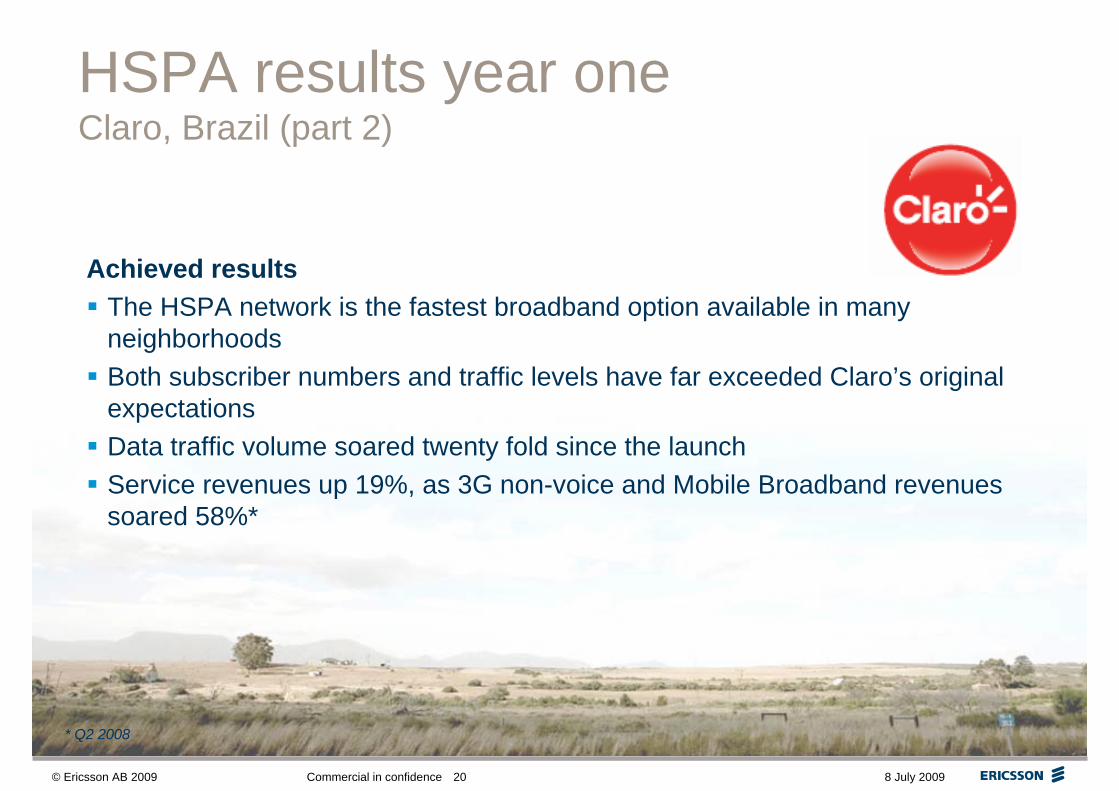

HSPA results year oneClaro, Brazil (part 2)

* Q2 2008

Achieved resultsThe HSPA network is the fastest broadband option available in many neighborhoodsBoth subscriber numbers and traffic levels have far exceeded Claro’s original expectationsData traffic volume soared twenty fold since the launch Service revenues up 19%, as 3G non-voice and Mobile Broadband revenues soared 58%*

© Ericsson AB 2009 Commercial in confidence 8 July 200921

Prepaid plans to address a mass market

Prepaid was essential to attract the next billion to mobile voice services

– 71% prepaid

Mobile broadband prepaid plans are under rollout all across Latin America and other regions

© Ericsson AB 2009 Commercial in confidence 8 July 200922

Rural HSPA targeting bottom of the pyramid Dialog Telekom, Sri Lanka (part1)

Key Facts Sri LankaPopulation: 21,324,000GDP (per capita): US$ 4,300 Fixed line penetration: 13%Mobile penetration: 40%Internet penetration: 1,4%Broadband penetration: 0.5%

Focus AreaTargets bottom of economic pyramid with rural mobile broadband leveraging HSPA technology

– rural economy generates $350 million/month compared to $110 million in the urban economy

Implementation of 3G/HSPA servicesHSPA services launched 2007, 3G 2006

– “a great opportunity from a financial perspective”

– “only requires a 20% incremental investment”

* By end 2008. HSPA launched 2007.

© Ericsson AB 2009 Commercial in confidence 8 July 200923

Rural HSPA targeting bottom of the pyramid Dialog Telekom, Sri Lanka (part 2)

Achieved results120k 3G subscribers, 30k HSPA users*Broadband commercially viable even among the poorestLeverage knowledge of the low-ARPU prepaid voice marketShared access & Sachet billing

0.56 USD/hour BB internet at 55 rural internet cafésIndividual access: Flat fee and bucket pricing

* By end 2008. HSPA launched 2007.

© Ericsson AB 2009 Commercial in confidence 8 July 200924

Soporte de la Regulaciónpara facilitar el mercado masivo

Acceso sin limites al espectro necesario Espectro armonizado a las recomendaciones internacionales Liberar serviciosCargo por licencias y contra prestaciones razonablesAplicación de impuestos después de crear cobertura y un sano negocioFacilitar compartición de partes de la red.Apoyar con la construcción rápida de la red de energía para el desarrollo rural

© Ericsson AB 2009 Commercial in confidence 8 July 200925

Resumen

La banda ancha ayuda a reducir la crisis económicaLa banda ancha móvil ayuda a los individuos, negocios, instituciones, la sociedad y la economía de las naciones

El regulador tiene un papel importante para que esto suceda

El operador requiere facilidades para invertir en zonas rurales en una manera rentable

El desarrollo tecnológico de EDGE/HSPA/LTE garantiza una gran economía de escala para banda ancha móvil / fija

© Ericsson AB 2009 Commercial in confidence 8 July 200926