Robert Davis

Hickman, Williams & Company

Steel Founders Society of America

March 23, 2011

Three area’s of interest

• World Production of Ferroalloys

• High Carbon Ferro Chromium

• Ferro Molybdenum

Globally, North America is a minor factor in the production of ferroalloys. The North American producers account for only 1.47% of all ferroalloy and specialty alloy production. Over 80% of the ferroalloys that are consumed in the United States are imported.

2000 5.30% of World Market

2004 2.14% of World Market – (1.20%

US)

2008 1.47% of World Market – (0.6%

US)

Asia

29.8%

Africa

20.5%

N. America

1.7%

S. America

5.6%

Europe

17.4%

Former CIS

19.2%

U.S.

3.6%

Others

2.1%

Africa17%

Asia39%

CIS20%

Europe11%

North America0.9%

U.S.1.2%

Other5%

South America6%

World Production of Ferroalloys26,300,000 MT produced in 2004

Source: USGS 2010

Africa12%

Asia56%

CIS14%

Europe6%

North America0.9%

U.S.0.6%

Other5%

South America5%

World Production of Ferroalloys36,100,000 MT produced in 2008

Source: USGS 2010

0

10

20

30

40

50

60

Asia Africa CIS Europe South America

U.S.

World Production of FerroalloysPercent of Total Production by Country

2000

2004

2008

Source: USGS 2010

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

5,000,000

2004 2005 2006 2007 2008

Africa, World ProductionMetric Tons

South Africa

Zimbabwe

Source: USGS 2010

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2,000,000

2004 2005 2006 2007 2008

Former CIS, World ProductionMetric Tons

Kazakhstan

Russia

Ukraine

Source: USGS 2010

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

2004 2005 2006 2007 2008

Europe, World ProductionMetric Tons

Norway

Finland

France

Source: USGS 2010

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

2004 2005 2006 2007 2008

“America's” World ProductionMetric Tons

Canada

Mexico

United States

Brazil

Source: USGS 2010

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

2004 2005 2006 2007 2008

"Other" countries, World ProductionMetric Tons

Australia

India

Source: USGS 2010

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

18,000,000

20,000,000

2004 2005 2006 2007 2008

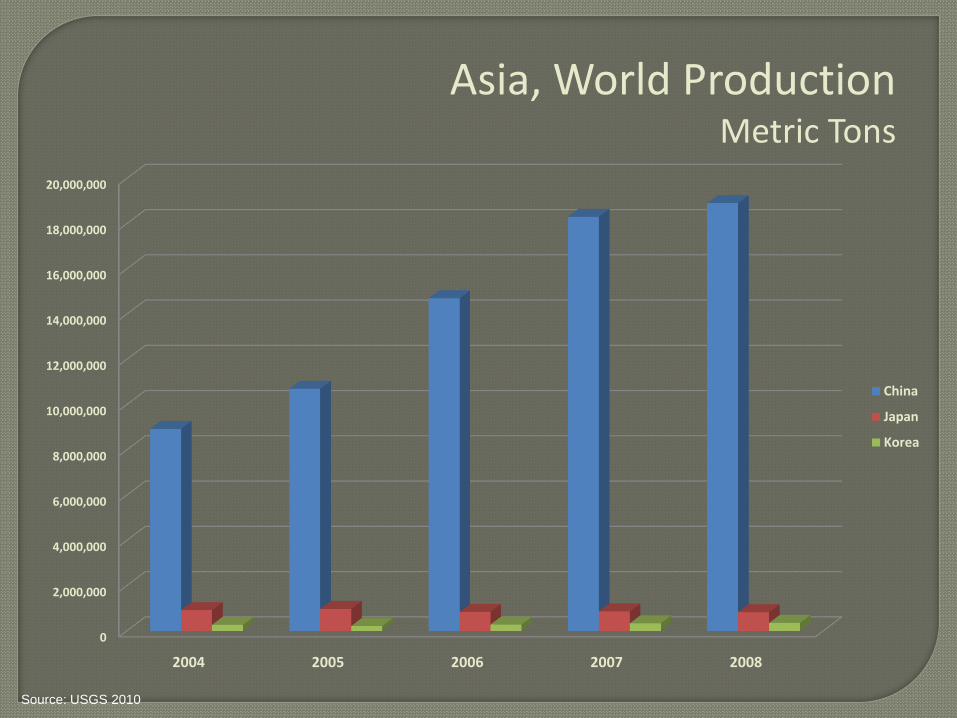

Asia, World ProductionMetric Tons

China

Japan

Korea

Source: USGS 2010

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

18,000,000

20,000,000

S. Africa Ukraine Norway Brazil India China

Largest Producers, by GeographicLocation, Metric Tons

2004

2005

2006

2007

2008

Source: USGS 2010

NORWAY INDIA

Ferro Manganese

• 215,000 Metric Tons

Ferro Silicon

• 210,000 Metric Tons

Silico Manganese

• 200,000 Metric Tons

Ferro Chromium

• 750,000 Metric Tons

Ferro Manganese

• 170,000 Metric Tons

Silico Manganese

• 90,000 Metric Tons

Source: USGS 2010

BRAZIL UKRAINE

Silico Manganese

• 350,000 Metric Tons

Ferro Manganese

• 340,000 Metric Tons

Ferro Chromium

• 196,000 Metric Tons

Silico Manganese

• 894,400 Metric Tons

Ferro Manganese

• 362,400 Metric Tons (BF)

Ferro Silicon

• 152,800 Metric Tons

Source: USGS 2010

SOUTH AFRICA CHINA

Ferro Chromium

• 3,100,000 Metric Tons

Ferro Manganese

• 610,000 Metric Tons

Silico Manganese

• 260,000 Metric Tons

Ferro Silicon

• 4,900,000 Metric Tons

Silico Manganese

• 4,500,000 Metric Tons

Ferro Manganese

• 2,100,000 Metric Tons

• 600,000 Metric Tons (BF)

Ferro Chromium

• 1,400,000 Metric Tons

Source: USGS 2010

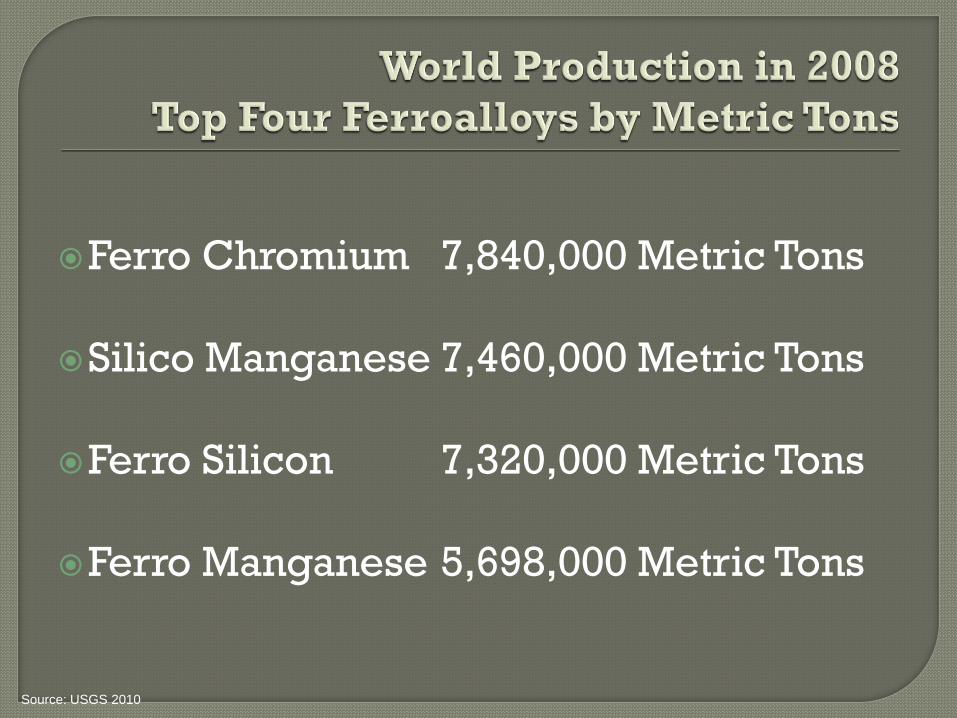

Ferro Chromium 7,840,000 Metric Tons

Silico Manganese 7,460,000 Metric Tons

Ferro Silicon 7,320,000 Metric Tons

Ferro Manganese 5,698,000 Metric Tons

Source: USGS 2010

Chromite Ore Mining

World Producers

Consumption / Importers to U.S.

World Resources of Chromite Ore are

greater than 12 Billion Tons of shipping

grade ore.

Sufficient supply to meet demand for

centuries.

About 95% of the worlds Chromite

resources are geographically

concentrated in Kazakhstan and South

Africa.

Source: USGS 2010

Country 2008 2009 2010

(Units are in million metric tons)

India 3.30 3.76 3.80

Kazakhstan 3.70 3.33 3.40

South Africa 9.60 6.87 8.50

Other 4.90 5.34 6.30

Total 21.50 19.30 22.00

One active chromite mine in the U.S. (North Western

U.S.)

In 2008, 94% of Chromite Ore was smelted in electric

arc furnaces to produce Ferro Chrome for the

metallurgical industry.

Source: USGS 2010

In 2008, the United States consumed about 10% of the worlds chromite ore production.

Forms were chromite ore, chromium chemicals, Ferro Chromium alloys, chromium metal and stainless steel.

In 2010, the United States consumed only about 2% of the worlds chromite ore production.

Source: USGS 2010

The major Ferro Chromium producing

countries are:

South Africa 3.1 million Metric Tons

China 1.4 million Metric Tons

Kazakhstan 1.2 million Metric Tons

India 750,000 Metric Tons

Russia 530,000 Metric Tons

Zimbabwe 150,000 Metric Tons

Source: USGS 2010

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

Ferro Chrome ProducersMetric Tons

2008

Source: USGS 2010

U.S. production of Ferro Chrome halted in

2008.

One plant in Marietta Ohio, that made

Nitrided Ferro Chrome.

South African Chrome is typically a

charge chrome (48 to 52% Cr).

Other producers vary in Cr – C – Si

ratios.

Source: USGS 2010

China’s role as a chromium consumer

grew along with its stainless steel

producing industry.

China’s stainless steel production

exceeded that of the U.S. in 2004.

By 2008, China’s stainless steel

production was 335% greater than that of

the United States.

Source: USGS 2010

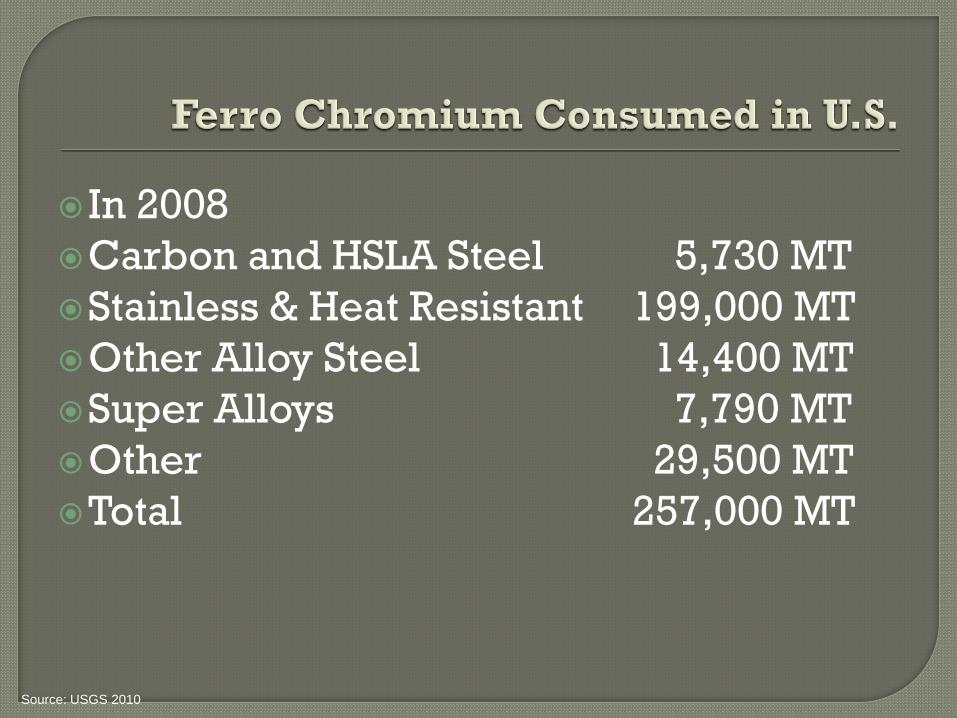

In 2008

Carbon and HSLA Steel 5,730 MT

Stainless & Heat Resistant 199,000 MT

Other Alloy Steel 14,400 MT

Super Alloys 7,790 MT

Other 29,500 MT

Total 257,000 MT

Source: USGS 2010

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

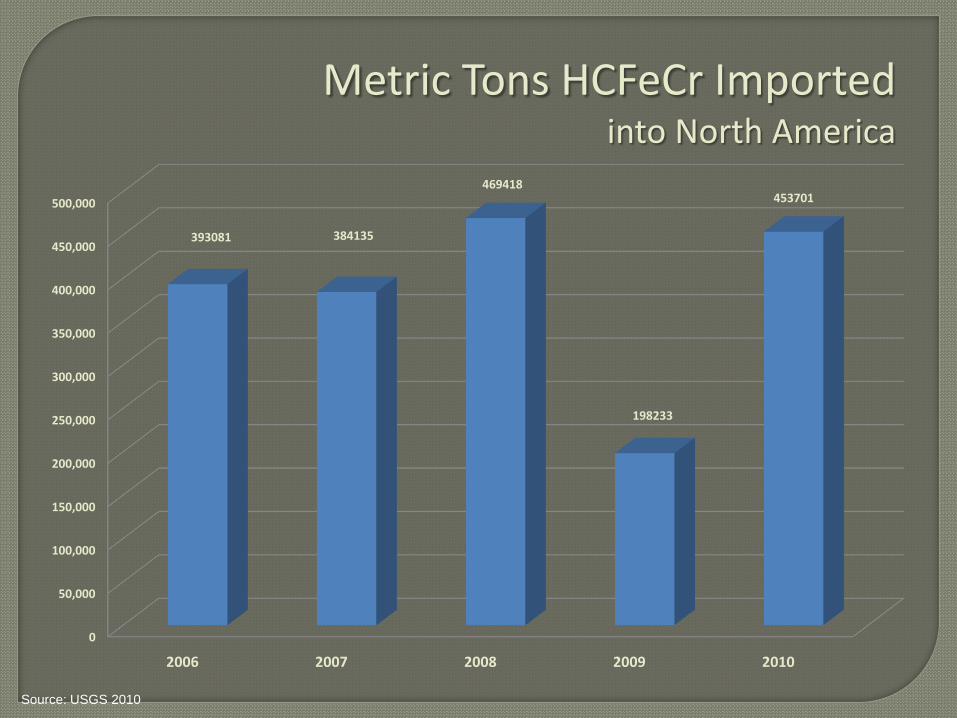

2006 2007 2008 2009 2010

393081 384135

469418

198233

453701

Metric Tons HCFeCr Importedinto North America

Source: USGS 2010

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

2006 2007 2008 2009 2010

61,500

152,000

29,357

17,76625,819

Metric Tons of HCFeCr sold by DLA

Source: USGS 2010

0

100,000

200,000

300,000

400,000

500,000

600,000

2006 2007 2008 2009 2010

454,581

536,135

498,775

215,999

479,520

Imports plus DLA Sales of HcFeCr

Imported

DLA

Total

Source: USGS 2010

Source: Ryan’s Notes

0

50,000

100,000

150,000

200,000

250,000

Metric Tons HCFeCr Imported into U.S., Plus DLA Sales

2006

2007

2008

2009

2010

Source: USGS 2010

42%

22%

10%

13%

13%

2006 Importers, HcFeCr454,581 Metric Tons

South Africa Kazakhstan Russia Zimbabwe DLA

Source: USGS 2010

44%

23%

8%

7%

6%

12%

2008 Importers of HCFeCr498,775 Metric Tons

South Africa Kazakhstan Russia Zimbabwe DLA India

Source: USGS 2010

51%

24%

7%

4%

5%3% 2% 2% 2%

2010 Importers of HCFeCr479,520 Metric Tons

South Africa Kazakhstan Russia Zimbabwe DLA India Albania Turkey Sweden

Source: USGS 2010

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

World Mine ProductionMetric Tons of Contained Mo

2004

2005

2006

2007

2008

Source: Indexmundi.com

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

China United States Chile Peru Canada

World Mine ProductionMetric Tons of contained Mo

2004

2005

2006

2007

2008

Source: indexmundi.com

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

China United States Chile Peru Canada

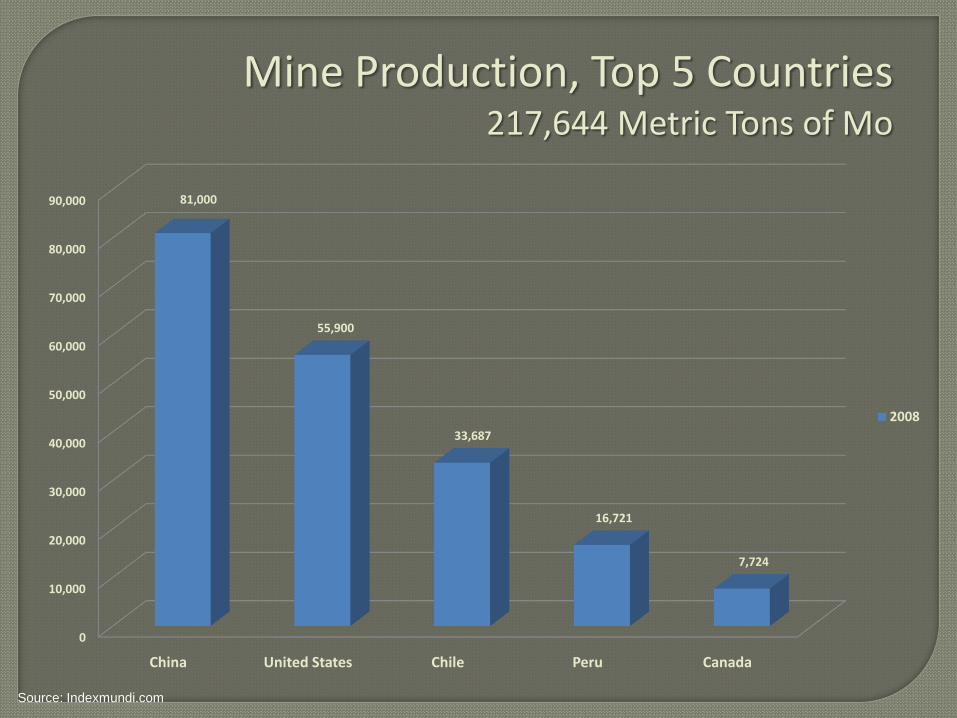

81,000

55,900

33,687

16,721

7,724

Mine Production, Top 5 Countries217,644 Metric Tons of Mo

2008

Source: Indexmundi.com

Source: Thompson Creek

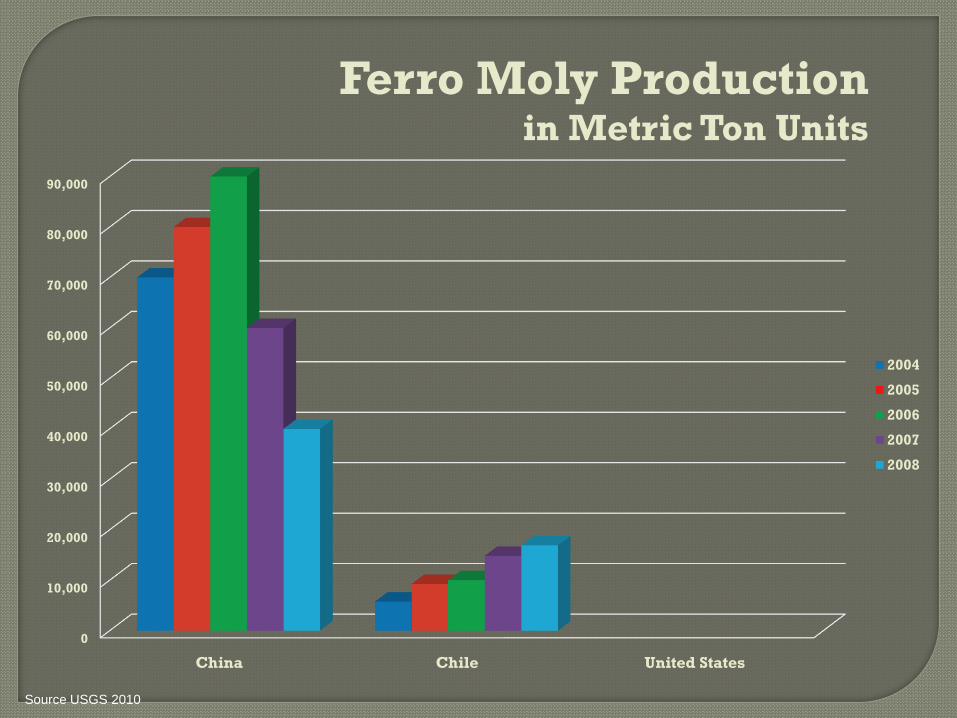

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

China Chile United States

Ferro Moly Productionin Metric Ton Units

2004

2005

2006

2007

2008

Source USGS 2010

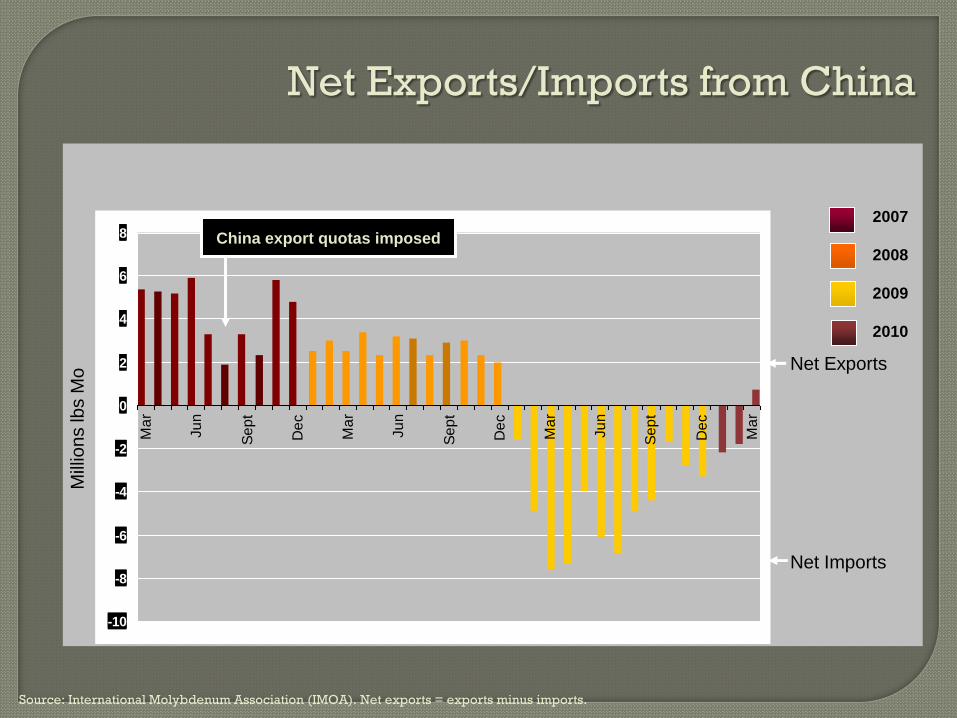

-10

-8

-6

-4

-2

0

2

4

6

8

Ma

r

Ju

n

Se

pt

De

c

Ma

r

Ju

n

Se

pt

De

c

Ma

r

Ju

n

Se

pt

De

c

Ma

r

Mill

ion

s lb

s M

o

2007

2008

2009

2010

Net Exports/Imports from China

Source: International Molybdenum Association (IMOA). Net exports = exports minus imports.

China export quotas imposed

Net Exports

Net Imports

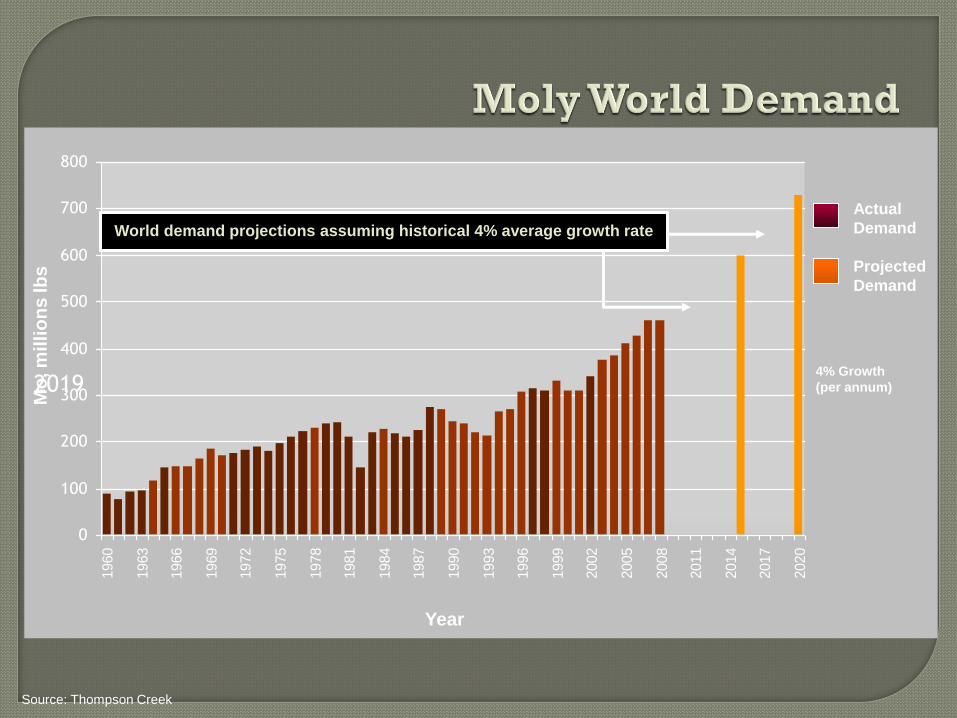

2019

0

100

200

300

400

500

600

700

800

1960

1963

1966

1969

1972

1975

1978

1981

1984

1987

1990

1993

1996

1999

2002

2005

2008

2011

2014

2017

2020

Actual

Demand

Projected

Demand

Year

Mo

, m

illi

on

s lb

s

4% Growth

(per annum)

World demand projections assuming historical 4% average growth rate

Source: Thompson Creek

Source: SMR GmbH

Main Driver: Oil Exploration and Development

• Increased demand for production: drilling

and pipelines

• Remote sources: deeper drilling, longer pipelines

• High-sulfur fuels including heavy oils and tar

sands: corrosive

• Nuclear power resurgence

• New and retrofit of coal fired power plants to super

critical operating levels

• Natural gas and oil fired plants

• Wind energy

Source: Thompson Creek

Main Driver: Capital Projects

A. Chemical Processing

• Petrochemical

• Desalinization

• Pulp & paper

• Food processing

• Pharmaceutical

B. Architectural

C. Power Generation: Nuclear, Coal, and Gas

Source : Thompson Creek

Approx. % Mo

Tool Steel 1-5%

High Speed Steel 5-9%

Foundry/Cast Iron up to 15%

Moly Metal 99.5%

Super alloys 4-16%

Chemicals

- Catalysts 8-20%

- Lubricants up to 15%

- Other 1-3%

Source: Thompson Creek

A. Moly is a metal for developed economies

• Rapid industrialization results in shift of consumption to

China, Korea, India, Brazil, and Russia

B. Industrial and Regulatory requirements demand

better steels

• CO2 reduction - Coal fired power plant, new & retrofits

• Tighter environmental standards – Tougher sulfur

emission standards results in new generation of de-

sulfurization catalysts with increased molybdenum

loading.

• Fuel economy – stronger and lighter steels improve

power efficiency in automobiles and trucks

Source: Thompson Creek

• Short-term: Recovery underway

• Demand supported by new uses and

continued energy/infrastructure investment

• Supply constrained: Development of major

new mines delayed by financial crisis

• Medium term: price strength anticipated as

world economy continues to grow

Source: Thompson Creek