Investis/GDPR/PIIData20181

Bowleven

Annual General Meeting

12th December 2018

Investis/GDPR/PIIData2018

Disclaimer

Important Notice

Nothing in this presentation or in any accompanying management discussion of this presentation (the "Presentation") constitutes, nor is it intended to constitute: (i)

an invitation or inducement to engage in any investment activity, whether in the United Kingdom or in any other jurisdiction; (ii) any recommendation or advice in

respect of the ordinary shares (the "Shares") in Bowleven plc (the "Company"); or (iii) any offer for the sale, purchase or subscription of any Shares.

The Shares are not registered under the US Securities Act of 1933 (as amended) (the "Securities Act") and may not be offered, sold or transferred except pursuant

to an exemption from, or in a transaction not subject to, the registration requirements of the Securities Act and in compliance with any other applicable state

securities laws.

The Presentation may include statements that are, or may be deemed to be "forward-looking statements". These forward-looking statements can be identified by

the use of forward-looking terminology, including the terms "believes", "estimates", "anticipates", "projects", "expects", "intends", "may", "will", "seeks" or "should"

or, in each case, their negative or other variations or comparable terminology, or by discussions of strategy, plans, objectives, goals, future events or intentions.

These forward-looking statements include all matters that are not historical facts. They include statements regarding the Company's intentions, beliefs or current

expectations concerning, amongst other things, the results of operations, financial conditions, liquidity, prospects, growth and strategies of the Company and its

direct and indirect subsidiaries (the “Group”) and the industry in which the Group operates. By their nature, forward-looking statements involve risks and

uncertainties because they relate to events and depend on circumstances that may or may not occur in the future. Forward-looking statements are not guarantees

of future performance. The Group’s actual results of operations, financial conditions and liquidity, and the development of the industry in which the Group

operates, may differ materially from those suggested by the forward-looking statements contained in the Presentation. In addition, even if the Group’s results of

operations, financial conditions and liquidity, and the development of the industry in which the Group operates, are consistent with the forward-looking statements

contained in the Presentation, those results or developments may not be indicative of results or developments in subsequent periods. In light of those risks,

uncertainties and assumptions, the events described in the forward-looking statements in the Presentation may not occur. Other than in accordance with the

Company's obligations under the AIM Rules for Companies, the Company undertakes no obligation to update or revise publicly any forward-looking statement,

whether as a result of new information, future events or otherwise. All written and oral forward-looking statements attributable to the Company or to persons acting

on the Company's behalf are expressly qualified in their entirety by the cautionary statements referred to above and contained elsewhere in the Presentation.

‘Bowleven’, ‘EurOil’ and the Bowleven logo are trade marks of Bowleven plc and copyright in the content of this document is owned by Bowleven plc. They should

not be used without permission.

Investis/GDPR/PIIData20183

Agenda

1. Strategic Review

2. What is the proposition for Bowleven shareholders?

3. Financial Results FY2018

4. Technical studies outline timetable

5. Overview of the Isongo Marine field reservoir

6. Overview of the IE field reservoir

7. Etinde roadmap towards commercialisation

8. Corporate Overview

9. Q & A

Investis/GDPR/PIIData20184

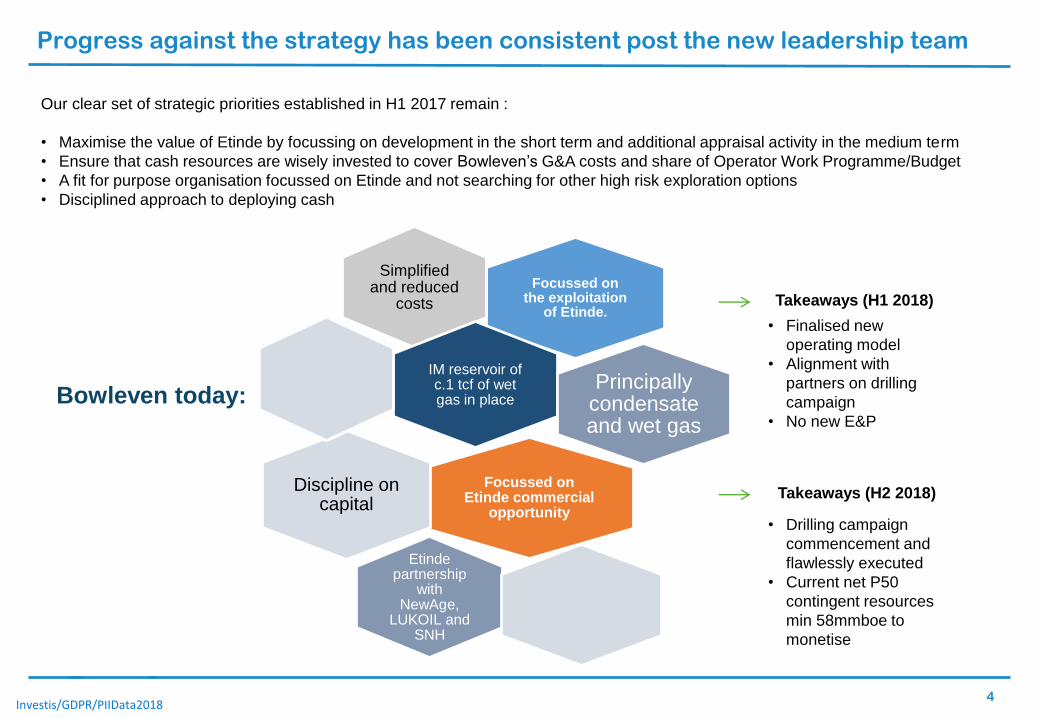

Progress against the strategy has been consistent post the new leadership team

Our clear set of strategic priorities established in H1 2017 remain :

• Maximise the value of Etinde by focussing on development in the short term and additional appraisal activity in the medium term

• Ensure that cash resources are wisely invested to cover Bowleven’s G&A costs and share of Operator Work Programme/Budget

• A fit for purpose organisation focussed on Etinde and not searching for other high risk exploration options

• Disciplined approach to deploying cash

Focussed on the exploitation

of Etinde.

Simplified and reduced

costs

IM reservoir of c.1 tcf of wet gas in place

Principally condensate and wet gas

Focussed on Etinde commercial

opportunity

Discipline on capital

Etinde partnership

with NewAge,

LUKOIL and SNH

Takeaways (H1 2018)

Takeaways (H2 2018)

• Drilling campaign

commencement and

flawlessly executed

• Current net P50

contingent resources

min 58mmboe to

monetise

• Finalised new

operating model

• Alignment with

partners on drilling

campaign

• No new E&P

Bowleven today:

Investis/GDPR/PIIData20185

What is the Bowleven proposition for investors?

* Enterprise Value = Market Capitalisation ($104.7 m)– Cash ($70.8 m) – Liquid Financial Instruments ($9.06m) = $24.8m.

• At current GBP:USD exchange rates.

Market Cap

£81.9

million

($104.7 million)*

JV partnership focussed

on developing a proven

well defined resource base

Development plan to be

designed and implemented

within 12 to 18 months

focussed on monetising the

value of the Condensate and

light Oil resources at EtindeChallenges around Associated

Gas manageable in the coming

year, utilising strong in-country

relationships

➢ Cash and financial investments of around $80*

million (circa £62.5 million)

➢ Market valuing Etinde stake at $25 million (c.

£19 million), equivalent to payment due upon

FID under farm out agreement

➢ Equivalent to the payment Bowleven will receive

in Cash at FID which is earmarked for late 2019.

➢ Set to realise the opportunity to generate

value for our shareholders through Etinde

FID catalyst

2018 appraisal drilling

programme successfully

delineated the gas/water

contact with significant

resource base of c.1 tcf of

wet gas in place

Investis/GDPR/PIIData20186

The market for African O&G asset has been encouraging during 2018

Norwegian oil firm Aker

Energy bought a 50-

percent stake in Ghana's

Deepwater Tano Cape

Three Points from Hess

for $100 million.

Royal Dutch Shell plc, July, signed PSCs for two

offshore blocks with the government of Mauritania -

exploration & potential future production of

hydrocarbons.

Assala Energy (backed by

Carlyle), acquired TOTAL

Gabon’s remaining stake in the

Rabi-Kounga Block located in

southern Gabon, July.

Swala oil & gas completes

$30 million deal to acquire

40% stake in Pan African

Energy Tanzania -

Tanzania.

Trident Energy (backed by

Warburg Pincus) acquired

stakes in three Equatorial

Guinea blocks EG-21, S and W

operated by Kosmos Energy.

ExxonMobil acquired 80% stake in

the Deepwater Cape Three Points

block. Ghana National Petroleum

Company Other key players in the 21

Ghanaian licenced blocks are Tullow,

Anadarko, Kosmos.

31 Oct: Vitol, Africa Oil Corp &

Delonex Energy acquire 50% of

Petrobras Oil & Gas for $1.4bn

in Nigeria.

Africa Oil & Gas acquires

Helios’ 25% stake in Impact

oil & gas for c. USD15

million, giving them access

to South, West & Central

Africa oil and gas assets.

Investment interest from PE funds, oil majors and trade players

Investis/GDPR/PIIData20187

Agenda

1. Strategic Review

2. What is the proposition for Bowleven shareholders?

3. Financial Results FY2018

4. Technical studies outline timetable

5. Overview of the Isongo Marine field reservoir

6. Overview of the IE field reservoir

7. Etinde roadmap towards commercialization

8. Corporate Overview

9. Q & A

Investis/GDPR/PIIData20188

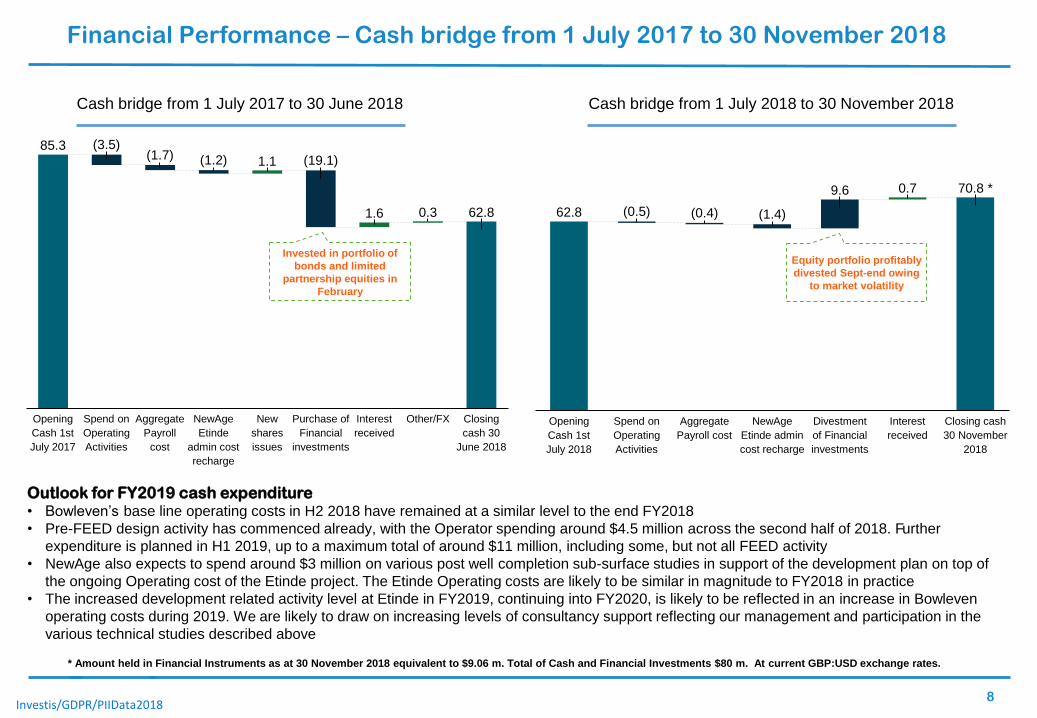

Financial Performance – Cash bridge from 1 July 2017 to 30 November 2018

62.8

70.8 *9.6 0.7

(0.4)

Opening

Cash 1st

July 2018

(0.5)

Spend on

Operating

Activities

Aggregate

Payroll cost

(1.4)

NewAge

Etinde admin

cost recharge

Divestment

of Financial

investments

Interest

received

Closing cash

30 November

2018

Equity portfolio profitably

divested Sept-end owing

to market volatility

85.3

62.8

1.1

1.6 0.3

Opening

Cash 1st

July 2017

(1.7)

Interest

received

Spend on

Operating

Activities

Purchase of

Financial

investments

(19.1)

Aggregate

Payroll

cost

(3.5)(1.2)

NewAge

Etinde

admin cost

recharge

New

shares

issues

Other/FX Closing

cash 30

June 2018

Cash bridge from 1 July 2017 to 30 June 2018 Cash bridge from 1 July 2018 to 30 November 2018

Outlook for FY2019 cash expenditure• Bowleven’s base line operating costs in H2 2018 have remained at a similar level to the end FY2018

• Pre-FEED design activity has commenced already, with the Operator spending around $4.5 million across the second half of 2018. Further

expenditure is planned in H1 2019, up to a maximum total of around $11 million, including some, but not all FEED activity

• NewAge also expects to spend around $3 million on various post well completion sub-surface studies in support of the development plan on top of

the ongoing Operating cost of the Etinde project. The Etinde Operating costs are likely to be similar in magnitude to FY2018 in practice

• The increased development related activity level at Etinde in FY2019, continuing into FY2020, is likely to be reflected in an increase in Bowleven

operating costs during 2019. We are likely to draw on increasing levels of consultancy support reflecting our management and participation in the

various technical studies described above

Invested in portfolio of

bonds and limited

partnership equities in

February

* Amount held in Financial Instruments as at 30 November 2018 equivalent to $9.06 m. Total of Cash and Financial Investments $80 m. At current GBP:USD exchange rates.

Investis/GDPR/PIIData20189

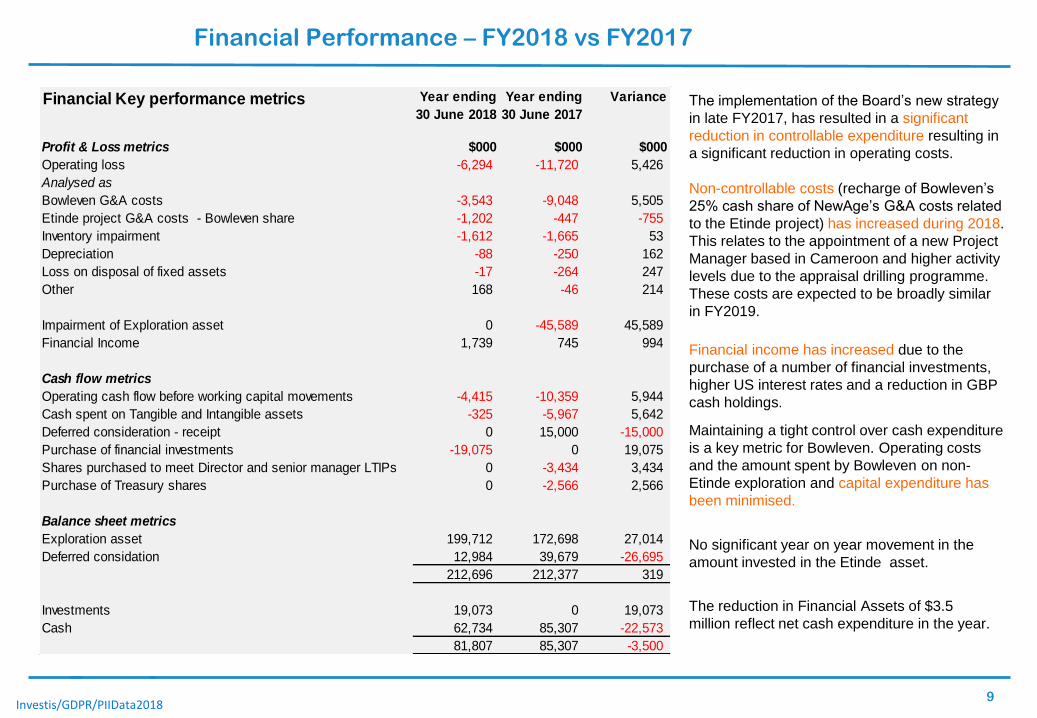

Financial Performance – FY2018 vs FY2017

Financial Key performance metrics Year ending

30 June 2018

Year ending

30 June 2017

Variance

Profit & Loss metrics $000 $000 $000

Operating loss -6,294 -11,720 5,426

Analysed as

Bowleven G&A costs -3,543 -9,048 5,505

Etinde project G&A costs - Bowleven share -1,202 -447 -755

Inventory impairment -1,612 -1,665 53

Depreciation -88 -250 162

Loss on disposal of fixed assets -17 -264 247

Other 168 -46 214

Impairment of Exploration asset 0 -45,589 45,589

Financial Income 1,739 745 994

Cash flow metrics

Operating cash flow before working capital movements -4,415 -10,359 5,944

Cash spent on Tangible and Intangible assets -325 -5,967 5,642

Deferred consideration - receipt 0 15,000 -15,000

Purchase of financial investments -19,075 0 19,075

Shares purchased to meet Director and senior manager LTIPs 0 -3,434 3,434

Purchase of Treasury shares 0 -2,566 2,566

Balance sheet metrics

Exploration asset 199,712 172,698 27,014

Deferred considation 12,984 39,679 -26,695

212,696 212,377 319

Investments 19,073 0 19,073

Cash 62,734 85,307 -22,573

81,807 85,307 -3,500

The implementation of the Board’s new strategy

in late FY2017, has resulted in a significant

reduction in controllable expenditure resulting in

a significant reduction in operating costs.

Non-controllable costs (recharge of Bowleven’s

25% cash share of NewAge’s G&A costs related

to the Etinde project) has increased during 2018.

This relates to the appointment of a new Project

Manager based in Cameroon and higher activity

levels due to the appraisal drilling programme.

These costs are expected to be broadly similar

in FY2019.

No significant year on year movement in the

amount invested in the Etinde asset.

Maintaining a tight control over cash expenditure

is a key metric for Bowleven. Operating costs

and the amount spent by Bowleven on non-

Etinde exploration and capital expenditure has

been minimised.

Financial income has increased due to the

purchase of a number of financial investments,

higher US interest rates and a reduction in GBP

cash holdings.

The reduction in Financial Assets of $3.5

million reflect net cash expenditure in the year.

Investis/GDPR/PIIData201810

Agenda

1. Strategic Review

2. What is the proposition for Bowleven shareholders?

3. Financial Results FY2018

4. Technical studies outline timetable

5. Overview of the Isongo Marine field reservoir

6. Overview of the IE field reservoir

7. Etinde roadmap towards commercialization

8. Corporate Overview

9. Q & A

Investis/GDPR/PIIData201811

Post-appraisal technical studies timetable to ascertain best development plan for FID

Subsurface project activity Q4 2018 Q1 2019 Q2 2019 Q3 2019 Q4 2019

Appraisal drilling – post completion technical studies

• Geochemical studies

• Core analysis

• Biostratigraphy

• Core sedimentology

Geophysics

• Update regional structural interpretation

Geology

• Geological model update – integration of new well data

• IM and IE static modelling and volumetric studies

Reservoir models

• PVT characterisation

• Dynamic modelling

Reserves/Resource update

Production/development related activities

Post appraisal drilling programme, technical studies are currently underway to determine development options and economics for FID

Studies are expected to

be completed in Q4 2019.

Technical analysis of the

data and physical samples

taken during drilling both

wells is ongoing.Existing geological, geophysical

and reservoir engineering

models will be re-examined in

light of the new data

Subsequently once completed, the Etinde project will have revised resources data, optimised development well locations, field

production projects by well combined with development well drilling programme and budget.

This data will be encapsulated in a revised Resource (Reserve) report prepared by an independent reserves auditor, which will support and

inform the FID decision for the Etinde project.

Investis/GDPR/PIIData201812

Agenda

1. Strategic Review

2. What is the proposition for Bowleven shareholders?

3. Financial Results FY2018

4. Technical studies outline timetable

5. Overview of the Isongo Marine field reservoir

6. Overview of the IE field reservoir

7. Etinde roadmap towards commercialisation

8. Corporate Overview

9. Q & A

Investis/GDPR/PIIData201813

What the Etinde Development currently offers

• Exploitation Authorisation (EA) awarded July 2014

• EA gives development and exploitation rights over

block MLHP-7 for an initial period of 20 years

• ‘Hub and Spoke’ development concept:

▪ Oil, condensate and wet gas to offshore

hub

▪ Liquids stripping at hub.

▪ Liquids marketable internationally.

▪ Gas offtake solutions under consideration

• IM field (Intra Isongo) to deliver first phase of

liquids & gas

• IM-5 well confirmed sufficient gas volumes in the

IM field of 1 tcf* in place at P50, to support offtake

various options

IM-5 Well Results

Upper Isongo

Intra Isongo

Middle Isongo

IM-5• Condensate-rich gas

flowed on test.

• Combined max. flow rates:

60mmscfd & 7,819 bcpd

(Total>17,800 boepd).

Upper Isongo

32 m (net) encountered; wet as

prognosed pre-drill.

Intra Isongo

Log evaluated net pay of

approximately 70 m.

Intra Isongo DST

Tested >10,800 boepd from 29

m net pay.

(37mmscfd & 4,664 bcpd)

Middle Isongo

Log evaluated net pay of

approximately 25m.

Middle Isongo DST

Tested >7,000 boepd from

14m net pay.

(23mmscfd & 3,155 bcpd)

Investis/GDPR/PIIData201814

IM field Reservoirs and current well location: Indicative P50 wet gas in place volumes

Upper

Isongo

c.200 bcf

CGR: 88

bbl/mMscfIntra Isongo

410 sand “Awl”

c.300 bcf

CGR: 124

bbl/mMscf

Middle Isongo

c.500 bcf

CGR: 104

bbl/mMscf

North

• Wet gas in place volumes (c.1 tcf)

are based on current estimates by

NewAge (field operator).

• These are subject to potential update

in 2019 as the IM-6 and IE-4 post

drilling data appraisal in assessed

and remapping is completed.

• Bowleven’s 2015 analysis differs

slightly in that it is based on 1.1 tcf of

wet gas in place with a slightly higher

amount assigned to the Intra-Isongo

and lower amount to the Middle

Isongo structure.

The Isongo deposits in the Etinde block were

deposited in a series of complex under water channels

during the Miocene (23 to 5 million years ago).

The channels flowed roughly NW to SE across the

licence transporting sands and muds from onshore

rivers from shallow water shelfs into deep water to the

west of Bioko Island.

Subsequent tectonic activity has broken the channel

deposits into a series of fault bounded blocks, each of

which potentially forms a separate trap.

Investis/GDPR/PIIData201815

Agenda

1. Strategic Review

2. What is the proposition for Bowleven shareholders?

3. Financial Results FY2018

4. Technical studies outline timetable

5. Overview of the Isongo Marine field reservoir

6. Overview of the IE field reservoir

7. Etinde roadmap towards commercialisation

8. Corporate Overview

9. Q & A

Investis/GDPR/PIIData201816

IE Reservoirs : Post appraisal well completion - Technical studies ongoing (1)

• Geological interpretation of the

channel deposits are complex

as the channels migrate

laterally and vertically over

time, both eroding and over

depositing earlier channel

sediments.

• At Etinde, these deposits have

then been broken into a

complex series of fault bounded

blocks making seismic analysis

and correlation difficult.

• The younger volcanic deposits

(typically Upper Miocene aged),

especially to the east, have the

effect of masking the underlying

seismic response, making the

correlation task more difficult

still.

IE-3

5 Km

IE block

on trend

4

1 2 3

7

6

85

Investis/GDPR/PIIData201817

IE Reservoirs : Post appraisal well completion - Technical studies ongoing (2)

The “410” channel sand deposits are the best developed across the IE reservoirs, although in reality there is

no direct correlation to the sands found in the IM-5 and IM-6 wells.

Lateral equivalents to the “510” and “310” channel deposits may also be present alongside less prominent

channel sand deposits between the major deposits.

• The “Drillbit” 410 channel deposits, comprising at least 2 separate channel sequences, were proved to be

water saturated at the IE-4 location. The result does not completely eliminate future prospectively at Drillbit

as there is a separate fault bounded four way closure to the east which has not been tested.

• The upper “410” channel sand body within the stratigraphically lower “Crowbar” was found to be Gas/Oil

bearing and may be hydrocarbon charged. The reservoir was very tight at the sampled location with

very poor hydrocarbon mobility. Further analysis is undergoing with a view to assessing any development

potential.

• The lower “410” Crowbar sand deposits were water saturated.

• Correlation between the IE-4 and earlier IE wells (especially IE-3) is ongoing based on seismic analysis

combined with chemical and biostratigraphy data is ongoing. Initial results suggest the channel deposit

stratigraphy is more complex than at the IM structures.

Investis/GDPR/PIIData201818

IE reservoirs : Post appraisal well completion: Technical studies ongoing (3)

The unexpected discovery at the IE-4 location was

a sequence of thin inter-bedded channel sands

above the main “410” Drillbit deposit and their

possible correlation with a thinner, but otherwise

similar deposit sequence at the IE-3 well location.

• The IE-4 sequence is about 30 metres thick with

around 20 metres net pay. The lower 12 metres

were subject to a DST test.

• Tested at a maximum average rate of 17.1

mmscf/d and 8,870 bbls/d on an open

choke basis. If producible, production

rates would be significantly lower.

• GOR of c.2,000 scf/stb indicative of a gas

rich light Oil.

* The IE-3 well tests (DST-3A and DST-3B) produced very similar results and suggest a similar high gas content light oil.

The key issue is the extent to which the gas rich light Oil in the IE-3* and IE-4 wells can be directly correlated with each other

and the potential volume of hydrocarbon trapped.

Very preliminary estimates from the Operator suggest a range from 10 to 40 million Barrels of Oil Equivalent (BOE) in place on

a P50 basis. However, a significant amount of work needs to be completed before an accurate estimate can be known.

An assessment of the potential for viable commercial development remains outstanding

Investis/GDPR/PIIData201819

Agenda

1. Strategic Review

2. What is the proposition for Bowleven shareholders?

3. Financial Results FY2018

4. Technical studies outline timetable

5. Overview of the Isongo Marine field reservoir

6. Overview of the IE field reservoir

7. Etinde roadmap towards commercialisation

8. Corporate Overview

9. Q & A

Investis/GDPR/PIIData201820

BT Consumer - EE (22% of FY2018 revenue)

• Post 2018 appraisal drilling the

expected incremental wet gas

discoveries are too small to make a

stand alone new build FLNG project

economically viable

• The majority of the economic value

lies in the Condensate and Light Oil

resources in the various IM and IE

reservoirs. However, the relatively

high volume of Gas and LPG fractions

which will be produced requires that

the development and commercial

solution must deal with the Gas.

• The JV partners aim to focus the

development design to maximise

Condensate and light Oil production.

Within the context of meeting any

supply requirements or obligations

related to the gas.

• A number of individual projects and tasks have

been developed by the Operator to examine

various field development parametres using

various internal and Consultant lead projects.

• We expect that these studies will be completed by

Q2 2019. Some individual elements are currently

ongoing.

• On completion of the pre-FEED (Front end

engineering design) in Q2 2019, the Upstream JV

partners aim to make a decision on the optimum

development scenario

• And commission more detailed FEED studies with

a view to making a FID decision by the end of

2019.

• On this basis, development contracts would be

place in 2020 or possibly late 2019 for long lead

items.

Economic and Commercial

considerations

The JV partners are taking a fresh look at all

available development options1. 2.

The Etinde roadmap towards commercialization has commenced (1)

Etinde

development

parametres

Partner

alignment of the

most technically

feasible and

commercial

robust plan

Investis/GDPR/PIIData201821

The Etinde roadmap towards commercialization has commenced (2)

IE Discoveries IM Options Under ConsiderationIM Discoveries

Phase One Phase Two

• Miocene aged

Upper, Intra- and

Middle Isongo

reservoirs

• Wet gas in place on

a P50 basis of c.1

tcf, based on

current Operator

assessment

• Likely to be based

on up to 6

production wells

tied back into a

central facility

• Production and Processing

platform (“CPF”) capable of

processing condensate

• Tied into production wells from

which subsequent well

maintenance activity is managed

with a Floating Storage vessel for

condensate moored in close

proximity

• Alternatively a Well head

platform with development well

gathering system with a Floating

Processing and Storage vessel

moored in close proximity

• Rich gas feed pipeline(s) from

the CPF/FPSO

Central facility options

under study

1 2

• Probably well head platform

with production gathering

system

• Pipeline tie back into CPF

or FPSO

3

Investis/GDPR/PIIData201822

1. Domestic option

• Etinde has an obligation to supply 70 mmscf/d of dry/lean Gas to the Cameroon

domestic market

• There are several pre-development gas to power schemes under consideration in the

Limbe/Douala area. Timeline for approval and development is uncertain. No one

project is likely to have sufficient gas demand to utilise the entire Etinde

obligation

• JV partners likely to commission onshore gas processing facility to remove Propane and

LPG fractions (and possibly CO2) from the rich gas pipeline feed from the offshore

facility. Propane/LPG would be sold separately for domestic/export purposes

2. Export options

The most likely options are a Rich gas feed pipeline to:

• Bioko Island (Equatorial Guinea) LNG facility (Marathon operated JV)

• Hilli Episeyo FLNG facility (Golar operated for Perenco/SNH)

• CMFLNG (NewAge FLNG concept)

• Other options are being considered including gas reinjection

• Commercial discussions are being undertaken with a variety of organisations. These

discussions range from early stage/initial discussion to relatively well developed and

detailed. Each gas sales option has its own particular hurdle to overcome

The likely configuration will depend on whether there is a single or multiple offtake solutions for Etinde gas

• Bioko Island LNG facility. This

would require an intra-governmental

agreement between the two

governments. Whilst we consider

this to be possible, it is likely to be a

relatively drawn out and complex

multi-party negotiation

• Hilli FLNG. The most significant

hurdle is the distance to Golar

owned vessel and its capacity to

process a direct relatively rich gas

feed from Etinde

• CMFLNG. This is currently a paper

project. Whilst it has Cameroon

government sanction we understand

CMFLNG would require additional

gas sources to be economically

viable

• Domestic supply is hampered by the

need to sanction and fund new Gas

to Electricity generation schemes

combined with concerns regarding

surety of funds from gas sales

Having examined and discussed these problems with a variety of individuals or organisations, we believe an export solution is feasible.

The JV partners collectively and individually are focussed on resolving and eliminating the gas export solution over the next 12 to 18 months.

Gas processing and Gas sales options (3)

Investis/GDPR/PIIData201823

Etinde upstream JV partners are LUKOIL/NewAge, along with the SNH (post back

in being exercised)

• The largest privately owned oil and gas company in the world by proved reserves. 3Q18 Revenue USD97B, 3Q18 Profit

USD7.5 B

• Accounts for in excess of 2% of global output of crude oil. Listed on both the Russian and London stock exchange.

• Over 25 years of operating experience.

• Extensive experience in operating multi-tcf gas fields, developing and producing hydrocarbons (including the processing

of natural gas liquids).

• Majority of exploration and production activity is located in Russia but has African interests in Ghana, Nigeria, and Egypt.

• Privately-owned oil and gas company. Has Etinde Operatorship with CAMOP (NewAge subsidiary).

• Operations in 7 countries, namely - Congo-Brazzaville, Cameroon, Nigeria, Ethiopia, Morocco, South Africa and

Kurdistan.

• In the event of the successful divestment of their Congo-Brazzaville asset, Etinde is the largest and their most

commercially attractive asset.

• NewAge has reached FID on five development projects with production having recently started on two of these projects.

• Along with Lukoil, NewAge has 37.5% (30% post government back-in) equity interest in the Etinde Permit.*

Participating interests: LUKOIL 30%, NewAge 30%, SNH 20% (post back in) and Bowleven 20%, .

Investis/GDPR/PIIData201824

Agenda

1. Strategic Review

2. What is the proposition for Bowleven shareholders?

3. Financial Results FY2018

4. Technical studies outline timetable

5. Overview of the Isongo Marine field reservoir

6. Overview of the IE field reservoir

7. Etinde roadmap towards commercialisation

8. Corporate Overview

9. Q & A

Investis/GDPR/PIIData201825

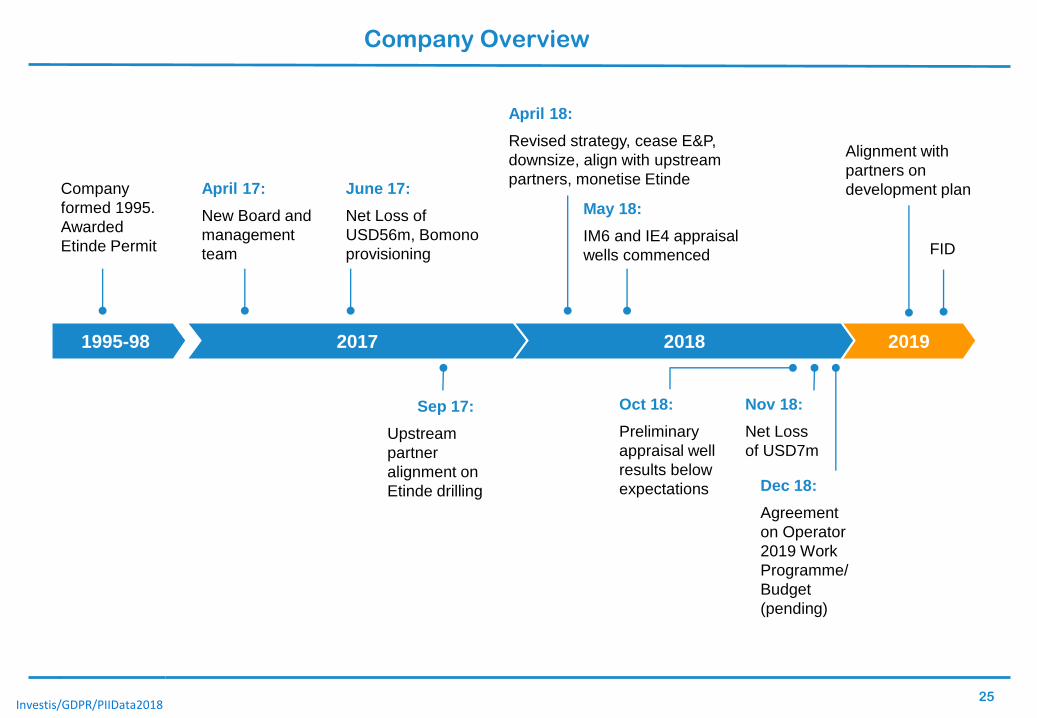

Company Overview

20171995-98 2018 2019

Company

formed 1995.

Awarded

Etinde Permit

April 17:

New Board and

management

team

June 17:

Net Loss of

USD56m, Bomono

provisioning

Sep 17:

Upstream

partner

alignment on

Etinde drilling

April 18:

Revised strategy, cease E&P,

downsize, align with upstream

partners, monetise Etinde

May 18:

IM6 and IE4 appraisal

wells commenced

Oct 18:

Preliminary

appraisal well

results below

expectations

Nov 18:

Net Loss

of USD7m

Dec 18:

Agreement

on Operator

2019 Work

Programme/

Budget

(pending)

FID

Alignment with

partners on

development plan

Investis/GDPR/PIIData201826

Capitalisation structure and share price movement

.

20.00

25.00

30.00

35.00

40.00

45.00

20

17

-12

-07

20

17

-12

-19

20

18

-01

-03

20

18

-01

-15

20

18

-01

-25

20

18

-02

-06

20

18

-02

-16

20

18

-02

-28

20

18

-03

-12

20

18

-03

-22

20

18

-04

-05

20

18

-04

-17

20

18

-04

-27

20

18

-05

-10

20

18

-05

-22

20

18

-06

-04

20

18

-06

-14

20

18

-06

-26

20

18

-07

-06

20

18

-07

-18

20

18

-07

-30

20

18

-08

-09

20

18

-08

-21

20

18

-09

-03

20

18

-09

-13

20

18

-09

-25

20

18

-10

-05

20

18

-10

-17

20

18

-10

-29

20

18

-11

-08

20

18

-11

-20

20

18

-11

-30

Share Price in Last 12 MonthsCapital Structure

Listing AIM

Share Price 24.7p

Market Capitalisation £80.88m

Issued Share Capital 335,272,933

Director and Staff

Holdings1,141,579

Average Daily Volume 459,194

12 month low (at

close)24.5p

12 month high (at

close)40.5p

• Data as at close on 11 December 2018

** Source - Vox Markets

Market volatility in O&G

sector

IM-6 spudding

IE-4 spudding

IM-6 prelim

results

IE-4 prelim

results

Key shareholders

as at 30th November 2018

% held of ISC

(rounded)

Crown Ocean Capital 28.94

HSBC James Capel as principal 9.03

OVMK Vermogensbeheer 5.20

M & G Investment 2.03

Investis/GDPR/PIIData201827

Small and focused Board and management team

• Small committed Board with

experience in corporate finance and

M&A

• London-based fit for purpose team

capable of analysing various

monetisation option

• Outsourced technical support

o Accessibility to reservoir and

commercialisation executives.

o Ability to access additional

resources where required

• Joint Venture partnerships with

NewAge and Lukoil

Matt McDonald

Chairman

Eli Chahin

Chief Executive Officer

Eric Taku

Cameroon Country Manager

Nick Brough

Group Financial Controller

Anne-Marie Tenace

IR Representative

Michael Clancy

Reservoir Engineer

Investis/GDPR/PIIData201828

Bowleven today

• Successfully proved and probable major gas asset with c.1 tcf of wet gas in place

• Fully carried for the latest two well appraisal programme

o IM-6 successfully delineated wet gas/water contact location

o IE-4 well – awaiting analysis of well results – potential resource uplift

o Interpretation of appraisal programme data further de-risks resource estimates

• Working with our partners to ensure an economically robust and value realising development

o Development options being actively assessed

o Targeting Etinde development FID by year end 2019

• Strong corporate position

o Robust balance sheet with strong cash position

o Strict capital discipline and focus on minimising G&A expenditure

• Positive Outlook

Focussed on development and exploration interests in Cameroon

Investis/GDPR/PIIData201829

Bowleven Plc

Ground Floor

Suite 1

Collegiate House

9 St. Thomas Street

London l SE1 9RY

00 44 (0) 20 3327 0150

www.bowleven.com