1

S.A. CAPITAL PARTNERS PRESENTS: Retro Lodge

2

Alexander Belden Investment Associate

Xenia Hotels

David Moore Summer Associate

Citigroup

Herbert McClary Assistant Vice President

Bank of America Merrill Lynch

Ben Harris Real Estate Manager

Verizon Wireless

MEET THE TEAM

Kyle Smith Acquisitions Officer

US Airforce

David Oppenheimer Vice President of Operations

Intercounty Judicial Sales Corp

3

AGENDA

Company Concept

Site Criteria

Terms

Hostel Market Dynamics

Pro Forma

4

COMPANY CONCEPT Concept: To build a ‘Poshtel’ that integrates modern design with local aesthetics, creating a vibrant atmosphere for social interaction and travel sharing experiences among youth travelers between the ages of 18 and 34. Poshtel: The term ‘poshtel’ is the blend of ‘posh’ and ‘hostel’ and is usually defined as an upscale or luxury hostel which combines the style and comfort of a boutique hotel with the price and sensibilities of a hostel. CHARACTERISTICS: - Prime Location - Large Social Areas - Frequent Events - Combination of private rooms and dorm rooms - En-suite private bathrooms and female-only dormitories - Modern design encompassing local area

5

HOSTEL MARKET DYNAMICS

6

TRADITIONAL HOSTEL

Limited cooking facility area

Large dormitory style rooms 8-20 Beds

Communal areas are old and outdated

Limited outdoor hangout area

7

POSHTEL VISION Shared 4 Bed Dorm Freeman Chicago, IL

Large Gathering Area The Bivvi Breckenridge, CO

Shared Kitchen Wayfarer Santa Barbara, CA

Lounge Area Freeman Miami, FL

8

MARKET PLACE

Low Price Point High

Lowe

st

High

est

Qual

ity Le

vel

The Budget Sector Space

Budget “Life-Style” Segment

The Market Potential for the Hostel Sector – Lifestyle and Blurred Lines Up-Market “Life-Style” Segment

Potential Market for Hostels

9

HOSTEL SUPPLY

Global Service Accommodation

Supply Est. 500,000 Properties

Global Budget Sector Related

Service Accommodation

Supply Est. 150,000 Properties

Global Hostel Sector Supply

Est. 7,000 Properties

US Hostel Sector

Supply Est. 350

Properties

Hostels account for less than 5% of global budget sector-related accommodation supply.

Hostels account for less than 1.5% of global serviced accommodation supply.

Chicago Hostel Supply 11 properties

*Statistics provided by api.hotelbase.org (2013 data)

10

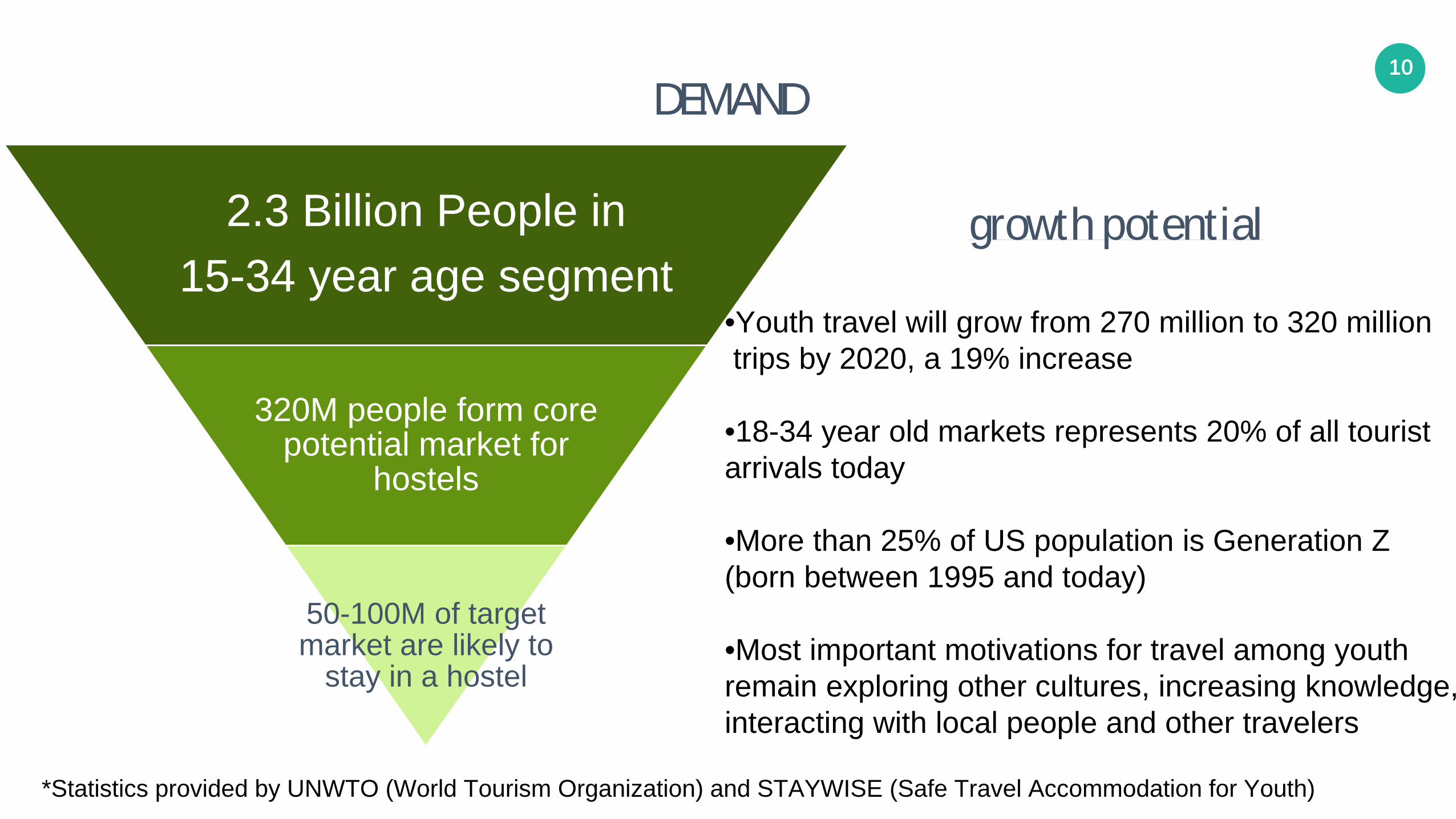

DEMAND

2.3 Billion People in 15-34 year age segment

320M people form core potential market for

hostels

50-100M of target market are likely to

stay in a hostel

*Statistics provided by UNWTO (World Tourism Organization) and STAYWISE (Safe Travel Accommodation for Youth)

growth potential

•Youth travel will grow from 270 million to 320 million trips by 2020, a 19% increase

•18-34 year old markets represents 20% of all tourist arrivals today •More than 25% of US population is Generation Z (born between 1995 and today) •Most important motivations for travel among youth remain exploring other cultures, increasing knowledge, interacting with local people and other travelers

11

CUSTOMER SEGMENT

MARKET SEGMENT DEFNITION Poshtel Markets

The Flashpacker Millennials and Generation Z Rough it in luxury Values boutique over mainstream Travels with technology

Primary

Couples Greater spending power Wants social interaction with privacy In Europe, couples account for 12% of all hostel guests

Primary

Business Cost conscious business professionals Greater availability of private rooms, central location and low rates Valuable customers who fill rooms during week days

Secondary

Students Poshtels are located near internationally recognized academic institutions Attract students on a short term basis through courses Provides hostels with strong occupancy during low demand periods

Secondary

Traditional Backpackers

Travel for long periods of time; 1-6 months Limited budget Travel in pairs or small groups

Tertiary

12

CONSUMER SEGMENTATION

Changing Consumer Landscape in the Hostel

Environment

Different Spending Power - Rise of the Flashpacker

International Profile – Demand for Non-Traditional Locations

- US experienced a boost for travel destinations by choice

Travel Habits Differ -The growth of budget airlines

Consumers More Emotional & Redefining Loyalty

Technology Savvy, with Different Booking Habits -Social media, online booking agents,

mobile apps are channels used by 18-34 year olds to book rooms

--New ways to market hostel

13

COMPETITOR ANALYSIS # of Hostels Locations Description

4 San Diego, Downtown San Diego, Oceanside San Francisco Hollywood

3

55

4

3

Focuses on organized activities. In 2013, USAHostels was awarded best hostel chain in the world by Hostelworld. Selling point is guest engaging activities.

Miami Chicago New York City Los Angeles

Part of Sydell Group. Focused on high-end luxury hostels.

In 20 States across The US

Focused on the conventional style hostel. Budget conscious and focused on providing guest activities.

New York City – 2 Miami

Modern hip hostels, but does not fall in the “luxury category.”

Chicago - 3 Has a mixture of high-end and luxury hostels in Chicago. Looking to open new locations in Wrigleyville, Nashville, and Atlanta

14

CHICAGO COMPETITOR ANALYSIS Neighborhood Beds Rooms

Dorm to Private Ratio

River North

River North

Buck Town

Wicker Park

52

65

35 96 12-15%

12-15%

Pricing

20

200

Private: $125 - $225 Dorm: $40 - $70

Private: $132 - $193 Dorm: $30 - $70

A Total of 11 hostels in the Greater Chicago Area

Description

Private: $125 - $225 Dorm: $20 - $70f

- Luxury hostel – ‘poshtel” - Amenities: cafe, bar, shared kitchen, lounge area - Dorm rooms max at 4 - Flashpackers, couples, business professionals

- Sporty high-end hostel - Amenities: cafe, bar, shared kitchen, lounge area -Dorm rooms max at 8 - Has 1 – 2 bedroom apartments - Flashpackers, couples, business professionals, and families

-Modern hostel style -Amenities: large open area, cafe, small bar, roof top -Flashpackers, couples, business professionals

-Modern hostel style -Amenities: large open area, coffee bar, roof top -Flashpackers, couples, business professionals

465 217 34%

50% Private: $125 - $305 Dorm: $20 - $70f

15

PRODUCT CONCEPT

Social Entertainment

• Bars provide entertainment facilities such as billiard tables, TV screens, and ping pong tables

• Organized social theme nights including comedy and musical events

Design

• Devoted to reflect local environment

• The bar areas mirror local destination and culture

• Open community spaces to promote social interaction

Hangout Areas

• Dedicated areas for guests to relax and “hang out”

• Spaces can offer changing stations for guests to recharge their mobile devices

• Can be roof decks, pool areas, or large open areas

16

PRODUCT CONCEPT

17

PRODUCT CONCEPT

Lower Requirement for FF&E in Rooms/Dorms

Per Bed Development Out Flexes Per Room Development

Larger Public Areas

Tailoring to Licensing and Accommodation Laws, and Planning

Requirements

Focus is on social engagement in the hostel, significantly reducing in-room entertainment costs such as expensive multimedia products

Hostel format is focused on “per bed” basis, allowing flexible format for development

Larger “public zones” to create social environment, providing flexibility in day time and night-time activities

Greater flexibility in hostel development and operational model can allow hostels to access sites more readily in locations that are not seen commercially viable for budget hotels

Tailoring Development to Maximize Opportunity

Flexible room design and layout fosters ability to build the correct mix of room and bed categories to maximize market and financial opportunity

Operational Efficiencies A greater amount of communal bathrooms shared by guests and limited in-room amenities reduce the amount of staff required to clean and operate the hostel

18

BUSINESS MODEL

Freehold Ownership

Qualified Management Team

Premium Locations

Product Quality

Social Media Leader

Local Market Sales Force

Retro Lodge

19

MARKETING STRATEGY Social Media Channels Hostel Intermediaries Hotel Intermediaries

20

OPERATIONAL PARTNER

Pivot Hotels & Resorts – The lifestyle division of Davidson Hotels & Resorts In homage to the truly unique differences that set lifestyle hotels apart from hard-branded assets, Pivot was purposefully incubated outside of Davidson. The Pivot team brings tremendous experience from Viceroy, Kimpton, sbe/SLS, Commune, The Irvine Company and Disney; all melding to allow them to operate with great diversity and dexterity. Though Pivot’s corporate team consists of highly capable professionals who have spent the bulk of their hospitality careers in the lifestyle space, they are aided and supported by all of Davidson’s shared services (accounting, IT, risk management, business development, investment management and legal). In addition to Davidson’s impressive and expansive portfolio, Pivot has already amassed an impressive list of partners, clients, and properties. Chicago, Illinois Properties: Hyatt Centric Chicago Magnificent Mile – Davidson Chicago Marriott Suites O’Hare - Davidson Marriott Chicago at the Medical Distric/UIC – Davidson Hotel Zachary (Under Construction) - Pivot Renaissance Chicago North Shore Hotel - Davidson

21

OPERATIONAL PARTNER (CONT.)

Client List: Pebblebrook KHP Capital Host Hotels & Resorts Rockbridge Capital Artemis GEM Realty Capital Regent Partners KSL Capital HSC Capital

Formerly launched in 2016, Pivot Hotels and resorts is Davidson’s lifestyle and operating division. Pivot’s clientele is true independent or “soft-branded” assets.

Hotel Zachary, Wrigleyville Hotel Zyphyr, San Francisco

Hotel Colonnade Gables, Miami

22

Risks & Mitigants

“Proof of Concept” in North America

Potentially Higher Development Costs

Seasonality

Low Brand Penetration

Demographic trends highlighted previously; future demand appears robust.

Renovation costs could be high; however ADR on a “quad” room with four beds is higher than a private room. Additionally, no “back of house” costs such as F&B.

Optionality to convert shared rooms to private rooms to combat periods of lower demand

The seven largest chains account for a total of 88 hostels comprising only 1.2% of total global supply. Opportunity to grab customer loyalty.

Complex Redevelopment Flexible room design and layout fosters ability to build the correct mix of room and bed categories to maximize market and financial opportunity

23

SITE CRITERIA

24

SITE CRITERIA

Location: Clos e proximity to public trans porta tion Within walking dis tance to res taurants , bars , and nightlife Key Markets – River North, Wes t Loop, Wicker Park, & Bucktown Costs: Within the price range of $22 - $24M for acquis ition Renovation cos ts between $1.5-2.5M Property: Size: 20,000 – 40,000s f Preferably exis ting hotel with large open areas

25

COMPETING SITES

1210 Lake Street 314 W. Institute 640 N. Wabash

PROS: - Located in Fulton Market District - 4 blocks from Green and Pink Lines - Walking distance to high end restaurants

CONS: - Asking Price: $4.5M - Very few windows - Right next to the ‘El’ line - Extensive improvements needed

PROS: - Positioned on borders of River North, Old Town, and Gold Coast - Market Auction: $4M - $5M - One block from Chicago El Stop - Walking distance to high end restaurants

CONS: - Office tenants on existing leases till 2018 - Extensive improvements to convert from office to hospitality

PROS: - Located in River North - One block from Red Line Stop - Walking distance to high end restaurants - Easily convertible hotel rooms

CONS: - Expensive property to purchase - Massive improvement costs needed

26

PRO FORMA

27

SOURCES AND USES

SOURCESSponsor 16% $1,332,439

Operator (Davidson/Pivot) 14% $1,232,439SA Capital Partners (Booth Team) 1% $100,000

LP Investors 84.4% $7,217,250Total Equity $8,549,689

Acquisition Financing $17,254,145Less: Loan Fees ($129,406)Total Debt Financing $17,124,739

TOTAL SOURCES $25,674,428

USES

Acquisition Price 24,648,779 Acquisition Fees (1% Purchase Price) 246,488 Owner Funded CapEx 2,100,000 Less: Net before tax cash flow ($1,320,839)

TOTAL USES 25,674,428

28

OTHER ACQUISITION/DISPOSITION DETAILS

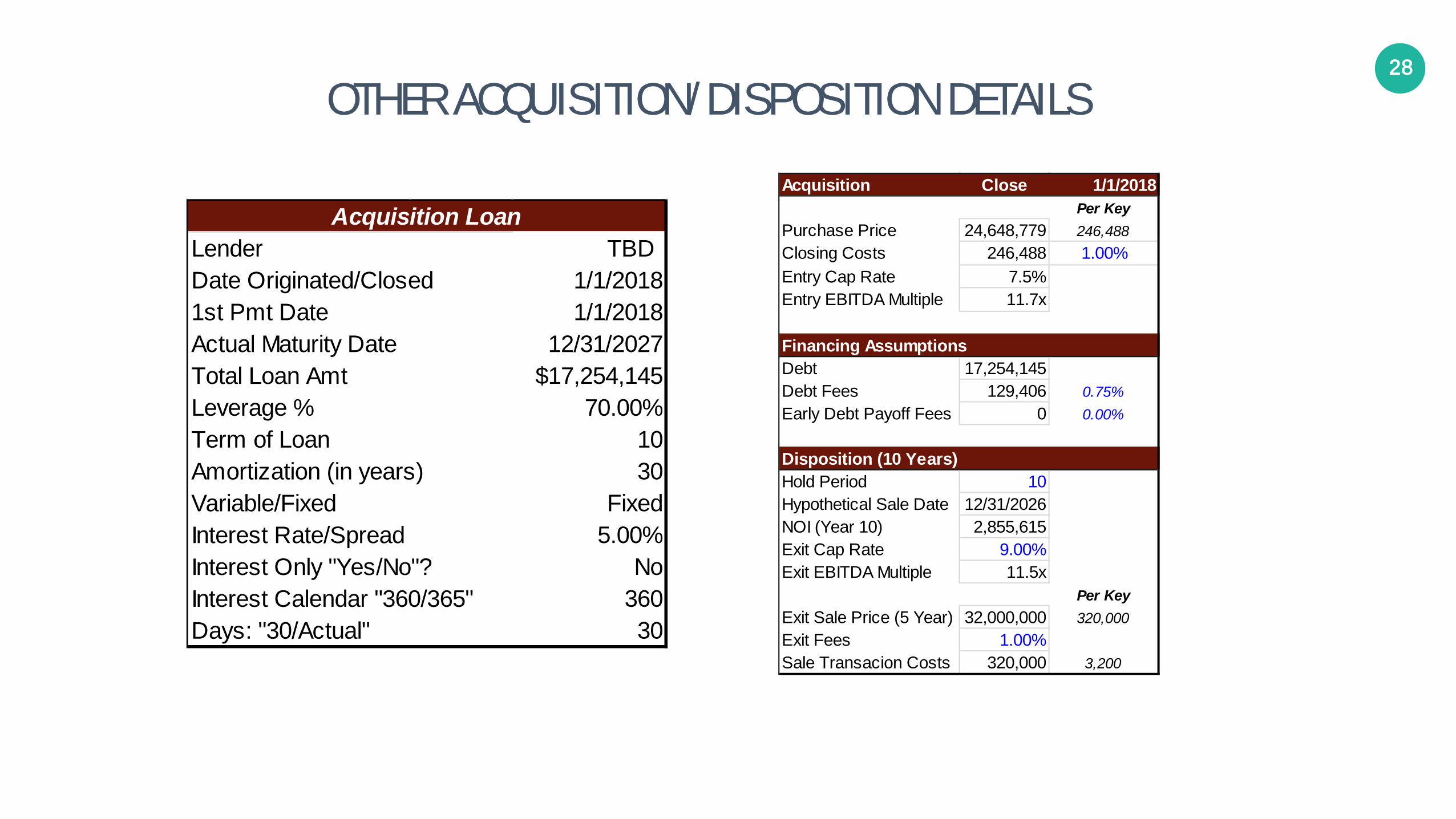

TBD1/1/20181/1/2018

Actual Maturity Date 12/31/2027$17,254,145

Leverage % 70.00%1030

Fixed5.00%

No36030

Interest Calendar "360/365"Days: "30/Actual"

Term of LoanAmortization (in years)Variable/FixedInterest Rate/SpreadInterest Only "Yes/No"?

Acquisition LoanLenderDate Originated/Closed1st Pmt Date

Total Loan Amt

Acquisition Close 1/1/2018Per Key

Purchase Price 24,648,779 246,488Closing Costs 246,488 1.00%Entry Cap Rate 7.5%Entry EBITDA Multiple 11.7x

Financing AssumptionsDebt 17,254,145Debt Fees 129,406 0.75%Early Debt Payoff Fees 0 0.00%

Disposition (10 Years)Hold Period 10Hypothetical Sale Date 12/31/2026NOI (Year 10) 2,855,615Exit Cap Rate 9.00%Exit EBITDA Multiple 11.5x

Per KeyExit Sale Price (5 Year) 32,000,000 320,000Exit Fees 1.00%Sale Transacion Costs 320,000 3,200

29

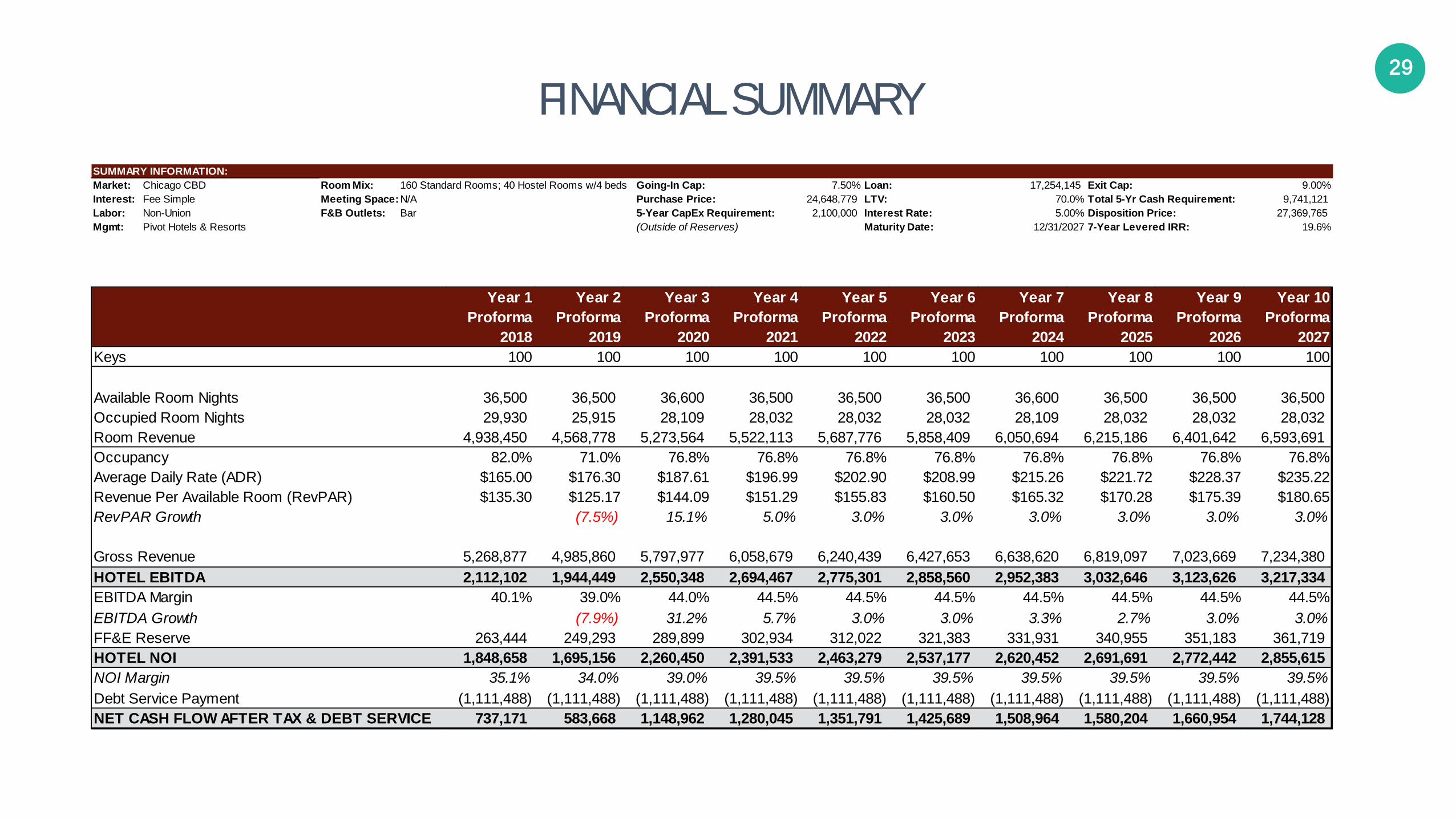

FINANCIAL SUMMARY Market: Chicago CBD Room Mix: 160 Standard Rooms; 40 Hostel Rooms w/4 beds Going-In Cap: 7.50% Loan: 17,254,145 Exit Cap: 9.00%Interest: Fee Simple Meeting Space:N/A Purchase Price: 24,648,779 LTV: 70.0% Total 5-Yr Cash Requirement: 9,741,121 Labor: Non-Union F&B Outlets: Bar 5-Year CapEx Requirement: 2,100,000 Interest Rate: 5.00% Disposition Price: 27,369,765 Mgmt: Pivot Hotels & Resorts (Outside of Reserves) Maturity Date: 12/31/2027 7-Year Levered IRR: 19.6%

SUMMARY INFORMATION:

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10Proforma Proforma Proforma Proforma Proforma Proforma Proforma Proforma Proforma Proforma

2018 2019 2020 2021 2022 2023 2024 2025 2026 2027Keys 100 100 100 100 100 100 100 100 100 100

Available Room Nights 36,500 36,500 36,600 36,500 36,500 36,500 36,600 36,500 36,500 36,500 Occupied Room Nights 29,930 25,915 28,109 28,032 28,032 28,032 28,109 28,032 28,032 28,032 Room Revenue 4,938,450 4,568,778 5,273,564 5,522,113 5,687,776 5,858,409 6,050,694 6,215,186 6,401,642 6,593,691 Occupancy 82.0% 71.0% 76.8% 76.8% 76.8% 76.8% 76.8% 76.8% 76.8% 76.8%Average Daily Rate (ADR) $165.00 $176.30 $187.61 $196.99 $202.90 $208.99 $215.26 $221.72 $228.37 $235.22Revenue Per Available Room (RevPAR) $135.30 $125.17 $144.09 $151.29 $155.83 $160.50 $165.32 $170.28 $175.39 $180.65RevPAR Growth (7.5%) 15.1% 5.0% 3.0% 3.0% 3.0% 3.0% 3.0% 3.0%

Gross Revenue 5,268,877 4,985,860 5,797,977 6,058,679 6,240,439 6,427,653 6,638,620 6,819,097 7,023,669 7,234,380 HOTEL EBITDA 2,112,102 1,944,449 2,550,348 2,694,467 2,775,301 2,858,560 2,952,383 3,032,646 3,123,626 3,217,334 EBITDA Margin 40.1% 39.0% 44.0% 44.5% 44.5% 44.5% 44.5% 44.5% 44.5% 44.5%EBITDA Growth (7.9%) 31.2% 5.7% 3.0% 3.0% 3.3% 2.7% 3.0% 3.0%FF&E Reserve 263,444 249,293 289,899 302,934 312,022 321,383 331,931 340,955 351,183 361,719 HOTEL NOI 1,848,658 1,695,156 2,260,450 2,391,533 2,463,279 2,537,177 2,620,452 2,691,691 2,772,442 2,855,615 NOI Margin 35.1% 34.0% 39.0% 39.5% 39.5% 39.5% 39.5% 39.5% 39.5% 39.5%Debt Service Payment (1,111,488) (1,111,488) (1,111,488) (1,111,488) (1,111,488) (1,111,488) (1,111,488) (1,111,488) (1,111,488) (1,111,488) NET CASH FLOW AFTER TAX & DEBT SERVICE 737,171 583,668 1,148,962 1,280,045 1,351,791 1,425,689 1,508,964 1,580,204 1,660,954 1,744,128

30

REVENUE MODEL

Subject Property Performance: 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027Daily Room Supply 100 100 100 100 100 100 100 100 100 100

Occupancy Percentage: Shared Rooms 0.0% 50.0% 60.0% 60.0% 60.0% 60.0% 60.0% 60.0% 60.0% 60.0%Occupancy Percentage: Individual Rooms 82.0% 80.0% 84.0% 84.0% 84.0% 84.0% 84.0% 84.0% 84.0% 84.0%Total Annual Occupancy Percentage 82.0% 73.5% 78.8% 78.8% 78.8% 78.8% 78.8% 78.8% 78.8% 78.8%Occupancy Growth (2.4%) 5.0% - - - - - - - Average Daily Rate (ADR): Shared Rooms $0.00 $50.00 $53.00 $55.65 $57.32 $59.04 $60.81 $62.63 $64.51 $66.45Average Daily Rate (ADR): Individual Rooms $165.00 $169.95 $180.15 $189.15 $194.83 $200.67 $206.69 $212.89 $219.28 $225.86Total Annual Average Daily Rate (ADR) $165.00 $170.41 $182.94 $192.08 $197.84 $203.78 $209.89 $216.19 $222.68 $229.36Rate Growth 3.0% 6.0% 5.0% 3.0% 3.0% 3.0% 3.0% 3.0% 3.0% Annual RevPAR: Shared Rooms $0.00 $25.00 $31.80 $33.39 $34.39 $35.42 $36.49 $37.58 $38.71 $39.87Annual RevPAR: Individual Rooms $135.30 $135.96 $151.32 $158.89 $163.66 $168.57 $173.62 $178.83 $184.20 $189.72Total Annual Revenue Per Occupied Room (RevPAR) $135.30 $125.17 $144.09 $151.29 $155.83 $160.50 $165.32 $170.28 $175.39 $180.65RevPAR Growth 0.5% 11.3% 5.0% 3.0% 3.0% 3.0% 3.0% 3.0% 3.0%

31

OCCUPANCY AND LEASEUP

32

NOI & CASH FLOW

33

TERMS

34

PROMOTE STRUCTURE & FORECASTED INVESTOR RETURNS Promote Structure Sponsor % LP %Hurdle 1 15.6% 84.4%

Preferred Return Sponsor LPHurdle 2 8.0% 15.0% 85.0% 28.2% 71.8%Hurdle 3 10.0% 20.0% 80.0% 32.5% 67.5%

Promote

Summary of Investor Level Returns Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10Limited Partner (LP) Returns

Total LP Distributions 23,012,289 - - 969,900 1,080,555 1,141,119 1,203,501 1,273,798 1,333,934 1,402,100 14,607,382 Total LP Contributions 7,217,250 5,937,233 1,280,017 - - - - - - - - Total LP Profit 15,795,039 LP IRR 18.0% (5,937,233) (1,280,017) 969,900 1,080,555 1,141,119 1,203,501 1,273,798 1,333,934 1,402,100 14,607,382 LP Equity Multiple 3.2x

Sponsor ReturnsTotal Sponsor Distributions 7,583,259 - - 179,062 199,491 210,672 222,189 235,167 246,269 258,854 6,031,557 Total Sponsor Contributions 1,332,439 1,096,124 236,315 - - - - - - - - Total Sponsor Profit 6,250,820 Sponsor IRR 25.8% (1,096,124) (236,315) 179,062 199,491 210,672 222,189 235,167 246,269 258,854 6,031,557 Sponsor Equity Multiple 5.7x

Net Cash Flow For Distribution Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 1031-Dec-18 31-Dec-19 31-Dec-20 31-Dec-21 31-Dec-22 31-Dec-23 31-Dec-24 31-Dec-25 31-Dec-26 31-Dec-27

Levered Before Tax Cash Flow (7,033,357) (1,516,332) 1,148,962 1,280,045 1,351,791 1,425,689 1,508,964 1,580,204 1,660,954 20,638,939 Levered IRR 19.6%Equity Multiple 3.6x

35

WHY INVEST?

Why Invest/Develop a Hostel Rather than

a Hotel?

Development Costs can be Potentially Lower Easier Conversion of Buildings

Greater Development Flexibility in high-demand

locations

First Mover Advantage in a “Hotspot” Market

Revenue, Profit and Return on investment per square foot potentially greater than the Conventional Budget Hotel

Model

“On-Trend” for Today’s and Tomorrow’s Markets

Flexibility to Tailor Product to Market Requirement –

Enhancing Revenue and Profit Streams

Similar Revenue/Profit Operating Model to the

Budget Hotel

36

WE ARE NOT SELLING YOU A BED, WE ARE SELLING YOU A SHARED EXPERIENCE