Ph

oto

by

Jam

es B

all -

ww

w.d

lsca

pe.

com

1

Safety

check

COFFEY INTERNATIONAL LIMITED

Half Year Results Presentation

15 February 2012

For

per

sona

l use

onl

y

November 2010 John Mulcahy becomes Chairman

December 2010 Board instigates management review and cost reduction program

$18 million annual cost base improvement by FY2012

March 2011 John Douglas commences as Managing Director

Business / strategy review initiated

June 2011 1st stage review completed

Financial update to market

August 2011 Reported FY2011 results

October 2011 Capital Raising

February 2012 Reported H1 FY2012 results

2

Improved Result Reflects Impact of Completed Strategic Initiatives

For

per

sona

l use

onl

y

• Financial Performance

• Business Performance

• Outlook

Agenda

3

For

per

sona

l use

onl

y

4

Improved Profitability

¹ Underlying EBITDA — EBITDA (Earnings Before Interest, Tax, Depreciation and Amortisation) before impairment and restructuring costs

² Underlying EBITDA from continuing operations excludes discontinued businesses of LA Environments and Rail

H1 H2 H1

6 months FY11 FY11 FY12

($m) ($m) ($m)

Fee revenue 222.6 201.1 212.5

Underlying EBITDA¹ 15.6 16.7 23.0

Underlying EBITDA² from continuing operations 15.9 15.0 20.4

Restructuring costs (5.3) (3.8) 0.0

Impairment 0.0 (62.9) 0.0

EBITDA 10.3 (50.0) 23.0

EBIT 5.1 (55.1) 18.6

NPAT (4.7) (65.0) 4.6

EPS (Basic – cents per share) (3.6) (49.2) 2.8

For

per

sona

l use

onl

y

$44.9m

$55.4m

$47.9m

$32.3m

$23.0m

$45.0m

FY08 FY09 FY10 FY11 FY12

Underlying EBITDA¹

Actual Guidance

5

Improved Margins

¹ Underlying EBITDA — EBITDA (Earnings Before Interest, Tax, Depreciation and Amortisation) before impairment and restructuring costs

² Underlying EBITDA Margin represents underlying EBITDA over Fee Revenue

11.9% 10.8%

10.1%

7.6%

10.8%

FY08 FY09 FY10 FY11 H1 FY12

Underlying EBITDA Margin²

For

per

sona

l use

onl

y

Positive Operating Cash Flow

6

$18.0m

$11.7m

$4.2m $4.6m

$10.8m

For

per

sona

l use

onl

y

7

Significant De-Risking

Net Debt/

EBITDA

= 1.72

Net Debt/

EBITDA

= 3.75

$45m

$77.5m

$32.3m

$121.2m

$23m

For

per

sona

l use

onl

y

Improved Net Asset Position

8

Dec June Dec

2010 2011 2011

($m) ($m) ($m)

Cash & equivalents 35.6 29.6 37.1

Current assets (excl. cash) 170.5 157.2 159.9

Non-current assets (excl. cash) 254.5 191.0 189.2

Total assets 460.6 377.8 386.2

Current borrowings 1.2 46.8 5.6

Other current liabilities 113.7 91.8 94.8

Non-current Borrowings 138.6 104.0 109.0

Other Non-current liabilities 19.9 12.8 12.5

Net assets 187.2 122.4 164.3

For

per

sona

l use

onl

y

Debt Paid Down

9

Components of Change in Net Debt

Net Operating Cash Inflow $10.8m

For

per

sona

l use

onl

y

Improved Gearing

10

6 months

Dec June Dec

2010

($m)

2011

($m)

2011

($m)

Total Cash

35.6 29.6 37.1 (including non-current cash deposits)

AUD$ denominated debt 99.8 116.5 79.2

Non AUD$ denominated debt 40.0 34.3 35.4

Total Debt 139.8 150.8 114.6

Net Debt 104.3 121.2 77.5

Total facilities (excl bank guarantees) 185.0 179.0 142.0

Cash and debt available 80.7 57.8 64.5

Equity 187.2 122.4 164.3

Net Debt to (Equity + Net Debt) 36% 50% 32%

For

per

sona

l use

onl

y

Improved Financing Facilities

11

Headroom

$64.5m

30 June 2011

31 December 2011

Post December 2011

Headroom

$79.5m

$77.5m

Net Debt

For

per

sona

l use

onl

y

Positive Net Profit After Tax

12

H1 H2 H1

6 months FY11 FY11 FY12

($m) ($m) ($m)

EBITDA 10.3 (50.0) 23.0

Depreciation and Amortisation (5.2) (5.1) (4.4)

Interest (7.3) (8.2) (9.4)

Taxation and Minority Interests (2.5) (1.8) (4.6)

NPAT (4.7) (65.1) 4.6

• No interim dividend declared

• The Board will review the potential for a dividend with the FY2012 full year results

For

per

sona

l use

onl

y

P & L by Segment

13

¹Underlying EBITDA before one-off impairment and restructuring costs

Footnote: Certain comparative data has been represented to align with the current period

FY09 FY10 FY11 FY12

H1 H2 YTD H1 H2 YTD H1 H2 YTD H1

($m) ($m) ($m) ($m) ($m) ($m) ($m) ($m) ($m) ($m)

Fee Revenue 261.2 249.3 510.5 241.0 234.7 475.7 222.6 201.1 423.6 212.5

Geosciences 138.1 118.1 256.2 126.7 111.9 238.5 117.9 117.0 234.9 132.4

International Development 71.6 80.3 151.9 71.2 82.0 153.2 67.5 54.8 122.3 54.2

Project Management 37.3 37.9 75.2 32.9 28.4 61.3 26.5 20.4 46.9 19.3

Other 14.2 13.0 27.2 10.3 12.4 22.7 10.7 8.9 19.6 6.6

Underlying EBITDA¹ 34.9 20.5 55.4 30.5 17.5 47.9 15.6 16.7 32.3 23.0

Geosciences 20.9 9.2 30.1 19.8 9.7 29.5 8.2 14.5 22.7 16.3

International Development 9.9 9.3 19.2 10.0 10.4 20.5 10.4 5.0 15.4 8.0

Project Management 5.5 4.7 10.1 4.1 0.4 4.5 0.7 (0.6) 0.1 0.0

Other 2.3 1.1 3.5 0.1 0.4 0.5 (0.2) 1.3 1.0 2.4

Corporate (3.8) (3.8) (7.6) (3.6) (3.5) (7.1) (3.5) (3.5) (7.0) (3.7)

EBITDA Margin % of Fee

Revenue 13% 8% 11% 13% 7% 10% 7% 8% 8% 11%

Geosciences 15% 8% 12% 16% 9% 12% 7% 12% 10% 12%

International Development 14% 12% 13% 14% 13% 13% 15% 9% 13% 15%

Project Management 15% 12% 13% 12% 2% 7% 3% (3%) 0% 0%

For

per

sona

l use

onl

y

Business Performance

14

For

per

sona

l use

onl

y

Safety is Our First Priority

15

For

per

sona

l use

onl

y

Safety Performance Remains On Track

*LTIFR = Lost Time Injury Frequency Rate.

16

1.56

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Jan-11 Feb-11 Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11

Coffey LTIFR* (12 Month Rolling Average) January 2011 to December 2011

2.36

For

per

sona

l use

onl

y

Ongoing Board Renewal

17

September 2009 John Mulcahy appointed Non-executive Director

October 2010 Susan Oliver appointed Non-executive Director

November 2010 John Mulcahy appointed Chairman

March 2011 John Douglas commenced as Managing Director

February 2012

Guy Cowan and Leeanne Bond appointed Non-executive Directors

Charles Jamieson AM and Stephen Williams retire as Non-executive Directors

Urs Meyerhans appointed Finance Director

For

per

sona

l use

onl

y

Leeanne Bond Guy Cowan

New Non-executive Directors

18

Age 60

Committees:

• Chair - Risk Committee

• Member - Audit Committee

Age 46

Committees:

• Member - Remuneration Committee

Mr Cowan spent 23 years working for energy

group Shell, most recently as Chief Financial

Officer of Shell Petroleum Inc, and CFO and

a Director of Shell Oil Company in the USA.

He was CFO of Fonterra Co-operative Group

Limited from Feb 2005 - Feb 2009.

Mr Cowan is a Non-executive Director of

Ludowici Ltd, UGL Limited, Queensland

Sugar Limited and Gold Oil PLC (UK), and

Chairman of the Advisory Board of Beak and Johnston Limited.

From 1996 to 2006 Ms Bond held a number of

roles with Worley Parsons in Queensland

including General Manager Hydrocarbons and

Development Manager (Queensland).

Ms Bond is a Non-executive Director of Liquefied

Natural Gas Ltd and Australian Water Recycling

Centre of Excellence Ltd, and a Board member of

the Queensland Bulk Water Supply Authority

(Seqwater).

For

per

sona

l use

onl

y

Overhead Salary Controlled

19

December 2010 to December 2011 For

per

sona

l use

onl

y

Falling Staff Turnover

20

Annualised Staff Turnover

February 2011 to January 2012

Sta

ff T

urn

ove

r %

For

per

sona

l use

onl

y

Bottom-Up Strategy Process Underway

• Markets remain positive particularly in Geosciences

• Further operational improvement is available

• Development for key technical and managerial staff is a priority

• Opportunities exist for organic growth within the existing geographic footprint

• Acquisition opportunities are being monitored but are not a short term focus

21

For

per

sona

l use

onl

y

Initial Portfolio Review Complete

• LA Environments divested – June 2011

• Commercial Advisory closed – July 2011

• Middle East Projects closed – September 2011

• Rail sold for $9.0 million – February 2012

The future of Specialist Training Australia (STA) is under review in light of current

exchange rates: provides less than 10% of International Development’s revenue and has

low margins

22

Ongoing Portfolio Review

For

per

sona

l use

onl

y

EBITDA Breakdown H1 FY12

(for continuing Businesses)

Fee Revenue H1 FY12

(for continuing Businesses)

Focused on 3 Key Businesses

23

• Geosciences ~ 1,800 employees

• International Development ~1,600 employees

• Project Management ~190 employees

Total: $206.0m Total: $24.3m

For

per

sona

l use

onl

y

Geosciences – A Well Integrated Offering

A very strong Australian brand in a discipline where Australia itself, is strong

24

For

per

sona

l use

onl

y

Geosciences – 4,000+ Active Projects, 2,000+ Active Clients

25

For

per

sona

l use

onl

y

Geosciences – Fee Revenue Continues to Improve

26

Geosciences Fee Revenue – Moving Annual Total

December 2009 to December 2011

De

c-0

9

Jan

-10

Fe

b-1

0

Ma

r-1

0

Ap

r-1

0

Ma

y-1

0

Jun

-10

Jul-

10

Au

g-1

0

Se

p-1

0

Oc

t-1

0

No

v-1

0

De

c-1

0

Jan

-11

Fe

b-1

1

Ma

r-1

1

Ap

r-1

1

Ma

y-1

1

Jun

-11

Jul-

11

Au

g-1

1

Se

p-1

1

Oc

t-1

1

No

v-1

1

De

c-1

1

$A

Mil

lio

ns

-F

ee

Re

ve

nu

e

Geosciences Fee Revenue - Moving Annual Total

Series1

$m

Fe

e R

eve

nu

e

For

per

sona

l use

onl

y

Geosciences – Improving Pricing & Efficiencies

27

Geosciences – 12 Month Moving Annual Total

Fee Revenue to Wage Ratio (Pre Bonuses)

December 2010 to December 2011

Fe

e to

Wa

ge

Ra

tio

For

per

sona

l use

onl

y

H1 FY12 Breakdown by Sector H1 FY12 Breakdown by Geography

Geosciences – Exposed to Good Geographies & Buoyant Sectors

28

Fee Revenue

Total: $132.4m For

per

sona

l use

onl

y

29

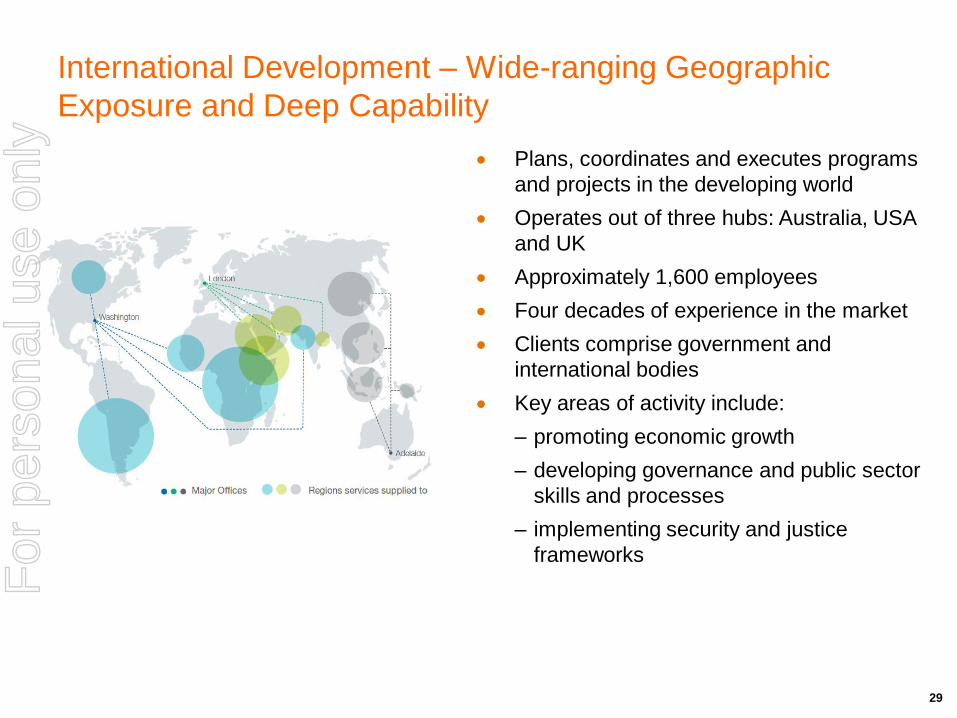

International Development – Wide-ranging Geographic

Exposure and Deep Capability

Plans, coordinates and executes programs

and projects in the developing world

Operates out of three hubs: Australia, USA

and UK

Approximately 1,600 employees

Four decades of experience in the market

Clients comprise government and

international bodies

Key areas of activity include:

– promoting economic growth

– developing governance and public sector

skills and processes

– implementing security and justice

frameworks

For

per

sona

l use

onl

y

Total: $67.5m Total: $54.2m

H1 FY11

International Development – Stable Revenues through

Geographic Diversification

30

Clients include:

H1 FY12 H2 FY11

Total: $54.8m

Fee Revenue

For

per

sona

l use

onl

y

31

Australia &New Zealand83%

Europe &Middle East10%

Africa 7%

H2 FY11 H1 FY11

Australia &New Zealand83%

Europe &Middle East10%

Africa 7%

Project Management – Refocused on ANZ and Africa with

Upside Exposure to the Property Cycle

Australia &New Zealand86%

Europe &Middle East3%

Africa 11%

Total: $19.3m Total: $20.4m Total: $26.5m

H1 FY12

Fee Revenue

For

per

sona

l use

onl

y

Coffey Outlook

• Coffey is well positioned with a solid cash flow and a strengthened balance sheet

• Geosciences’ core markets in infrastructure, oil & gas, and mining continue to have a

positive outlook

• In International Development increased spend in Australia and the UK is offsetting a

weaker US outlook

• Projects continue to contribute with future upside exposure to the property cycle

• We are reconfirming FY2012 EBITDA guidance of $45 million

• We expect reduced interest and tax costs in the H2 FY2012 with improved NPAT

• The Board will review the potential for a dividend with the FY2012 full year results

32

For

per

sona

l use

onl

y

33

Financial

Performance Improved profits – EBITDA of $23m

Improved margins – EBITDA margin of 10.8%

Positive operating cash flow – $10.8m

Significant de-risking – Net debt: EBITDA of 1.75

Improved net asset position – Net assets of $164.3m

Debt paid down – Net debt at $77.5m

Improved gearing – reduced to 32%

Positive NPAT – $4.6m

Business

Performance Safety is a key priority and performance remains on track

Ongoing Board renewal

Overhead salary expenses controlled

Falling staff turnover

Strategy process underway

Initial portfolio review completed

Geosciences

- Fee revenue continues to improve

- Improving pricing and efficiencies

- Exposed to good geographies and buoyant sectors

International Development

- Stable revenues through geographic diversification

Projects

- Subdued property cycle

Outlook Reconfirming FY2012 EBITDA guidance of $45m

Review potential for a dividend with FY2012 full year results

For

per

sona

l use

onl

y

Disclaimer

The material in this presentation is a summary of the results of Coffey International Limited (Coffey) for the 6 months ended 31 December 2011 and an update on Coffey’s activities and is current at the date of preparation, 15 February 2012. Further details are provided in the Company’s half year accounts and results announcement released on 15 February 2012.

No representation, express or implied, is made as to the fairness, accuracy, completeness or correctness of information contained in this presentation, including the accuracy, likelihood of achievement or reasonableness of any forecasts, prospects, returns or statements in relation to future matters contained in the presentation (“forward-looking statements”). Such forward-looking statements are by their nature subject to significant uncertainties and contingencies and are based on a number of estimates and assumptions that are subject to change (and in many cases are outside the control of Coffey and its Directors) which may cause the actual results or performance of Coffey to be materially different from any future results or performance expressed or implied by such forward-looking statements.

This presentation provides information in summary form only and is not intended to be complete. It is not intended to be relied upon as advice to investors or potential investors and does not take into account the investment objectives, financial situation or needs of any particular investor.

Due care and consideration should be undertaken when considering and analysing Coffey’s financial performance. All references to dollars are to Australian Dollars unless otherwise stated.

To the maximum extent permitted by law, neither Coffey nor its related corporations, Directors, employees or agents, nor any other person, accepts any liability, including, without limitation, any liability arising from fault or negligence, for any loss arising from the use of this presentation or its contents or otherwise arising in connection with it.

This presentation should be read in conjunction with other publicly available material. Further information including historical results and a description of the activities of Coffey is available on our website, coffey.com

Photos owned by Coffey or Coffey employees and permission is provided.

34

For

per

sona

l use

onl

y