Saudi Finance Company

(Closed Saudi Joint Stock Company)

INTERIM CONDENSED FINANCIAL STATEMENTS AND

INDEPENDENT AUDITOR’S LIMITED REVIEW REPORT

FOR THE THREE MONTHS PERIOD ENDED 31 MARCH 2017

Saudi Finance Company - (Closed Saudi Joint Stock Company)

INTERIM STATEMENT OF COMPREHENSIVE INCOME - UNAUDITED For the three months period ended 31 March 2017

The attached notes 1 to 19 form part of these interim condensed financial statements

2

Notes

31 March 2017 SR

31 March 2016 SR

Restated (Note 17)

Special commission income from Murabaha contracts 15,211,705 17,531,032

Financing facility cost and charges (special commission expenses) (2,208,094) (1,972,211)

──────── ────────

NET INCOME FROM MURABAHA 13,003,611 15,558,821

Other operating income

Management fees 14 - 532,000

Other income 603,590 10,508

──────── ────────

13,607,201 16,101,329

Operating expenses

General and administrative expenses 5 (7,271,621) (7,022,342)

Selling and marketing expenses 6 (1,442,382) (1,634,767)

Impairment loss on Murabaha receivable 8 (2,420,000) (2,480,000)

Unrealised loss on profit rate swap (13,730) (223,857)

──────── ────────

NET PROFIT FOR THE PERIOD 2,459,468 4,740,363

OTHER COMPREHENSIVE INCOME - -

──────── ────────

TOTAL COMPREHENSIVE INCOME 2,459,468 4,740,363

════════ ════════

Saudi Finance Company - (Closed Saudi Joint Stock Company)

INTERIM STATEMENT OF FINANCIAL POSITION As at 31 March 2017

The attached notes 1 to 19 form part of these interim condensed financial statements

3

Notes

31 March

2017 (Unaudited)

SR

31 December

2016 (Audited)

SR Restated (Note 17)

ASSETS

Cash and cash equivalents 18,526,165 20,258,398

Restricted cash deposits 7 5,244,409 5,484,409

Murabaha receivables, net 8 343,103,909 363,936,528

Prepayments, accrued income and other receivables 9 3,183,464 4,297,350

Assets acquired in satisfaction of claims 6,087,234 6,087,234

Property and equipment 5,409,986 5,869,566

Intangible assets 2,054,206 2,324,078

───────── ─────────

TOTAL ASSETS 383,609,373 408,257,563

═════════ ═════════

LIABILITIES AND SHAREHOLDERS’ EQUITY

Financing from financial institutions 10 221,845,383 251,399,696

Provision for zakat 11 18,066,346 16,839,346

Accounts payable, accruals and other payables 12 9,114,007 6,661,800

Employees' terminal benefits 2,273,631 2,279,183

───────── ─────────

TOTAL LIABILITIES 251,299,367 277,180,025

───────── ─────────

SHAREHOLDERS’ EQUITY

Share capital 13 100,000,000 100,000,000

Statutory reserve 3,301,038 3,301,038

Retained earnings 29,008,968 27,776,500

───────── ─────────

TOTAL SHAREHOLDERS’ EQUITY 132,310,006 131,077,538

───────── ─────────

TOTAL LIABILITIES AND SHAREHOLDERS’

EQUITY 383,609,373 408,257,563

═════════ ═════════

Saudi Finance Company - (Closed Saudi Joint Stock Company)

INTERIM STATEMENT OF CHANGES IN SHAREHOLDERS’ EQUITY For the three months period ended 31 March 2017

The attached notes 1 to 19 form part of these interim condensed financial statements

4

Share Capital

SR

Statutory reserve

SR

Retained earnings

SR Total SR

Balance at beginning of the period (Audited) 100,000,000 1,639,144 17,428,314 119,067,458

Net income for the period – before

adjustment - - 3,589,134 3,589,134 Prior period adjustment (Note 17) - - 1,151,229 1,151,229 ──────── ─────────

Net income for the period – after adjustment - - 4,740,363 4,740,363

──────── ──────── ──────── ─────────

Total comprehensive income – after

adjustment - - 4,740,363 4,740,363

Zakat for the period - - (1,151,229) (1,151,229)

───────── ──────── ──────── ─────────

Balance at 31 March 2016 (Unaudited) 100,000,000 1,639,144 21,017,448 122,656,592

═════════ ════════ ════════ ═════════

Balance at beginning of the period (Audited)

– before adjustment 100,000,000 2,840,152 28,237,386 131,077,538

Prior period adjustment (Note 17) - 460,886 (460,886) -

Balance at beginning of the period – after

adjustment (Note 17) 100,000,000 3,301,038 27,776,500 131,077,538

──────── ──────── ──────── ─────────

Net income for the period - - 2,459,468 2,459,468

──────── ──────── ──────── ─────────

Total comprehensive income - - 2,459,468 2,459,468

Zakat for the period - - (1,227,000) (1,227,000)

───────── ──────── ──────── ─────────

Balance at 31 March 2017 (Unaudited) 100,000,000 3,301,038 29,008,968 132,310,006 ═════════ ════════ ════════ ═════════

Saudi Finance Company - (Closed Saudi Joint Stock Company)

INTERIM STATEMENT OF CASH FLOWS - UNAUDITED For the three months period ended 31 March 2017

The attached notes 1 to 19 form part of these interim condensed financial statements

5

Notes

31 March 2017 SR

31 March 2016 SR

OPERATING ACTIVITIES Net profit for the period 2,459,468 4,740,363 Non-cash adjustment to reconcile profit to net cash used in operation activities:

Depreciation 5 503,292 500,906 Amortisation of intangible assets 5 295,846 277,359 Provision for employees’ terminal benefits 143,491 122,505 Impairment loss on Murabaha receivable 8 2,420,000 2,480,000 Unrealised loss on profit rate swap 8 13,730 242,227

───────── ─────────

Operating cash flows before working capital changes 5,835,827 8,363,360

Working capital adjustments:

Murabaha receivable 18,412,618 (16,535,034) Prepayments, accrued income and other receivables 1,113,886 1,205,450 Accounts payable, accruals and other payables 2,438,477 2,466,821

───────── ─────────

Net cash from (used in) operations 27,800,808 (4,499,403)

Employees’ terminal benefits paid (149,043) (7,061) ───────── ─────────

Net cash from (used in) operating activities 27,651,765 (4,506,464) ───────── ─────────

INVESTING ACTIVITY Purchase of property and equipment (43,712) (156,540) Purchase of intangible assets (25,974) (503,152) ───────── ─────────

Cash used in investing activity (69,686) (659,692) ───────── ─────────

FINANCING ACTIVITY Restricted cash deposits 240,000 - Financing from financial institutions - 200,000,000 Repayment of financing from financial institutions (29,554,312) (185,443,373) ───────── ─────────

Net cash (used in) from financing activity (29,314,312) 14,556,627 ───────── ─────────

NET CHANGES IN CASH AND CASH EQUIVALENTS (1,732,233) 9,390,471

Cash and cash equivalents at beginning of the period 20,258,398 12,726,130 ───────── ─────────

CASH AND CASH EQUIVALENTS AT END OF THE PERIOD 18,526,165 22,116,601 ═════════ ═════════

Supplementary information: Special commission income from Murabaha contracts received 16,560,114 14,399,288 ═════════ ═════════

Supplemental non-cash information: Murabaha receivable settled against collateralised asset 11 - 7,040,792 ═════════ ═════════

Saudi Finance Company - (Closed Saudi Joint Stock Company)

NOTES TO FINANCIAL STATEMENTS For the three months period ended 31 March 2017

6

1 LEGAL STATUS AND ACTIVITIES

Saudi Finance Company (the “Company”) is a Closed Saudi Joint Stock Company registered in the Kingdom of

Saudi Arabia under commercial registration numbered 1010078374 dated 23 Muharram 1411H (corresponding to

14 August 1990).

The main activities of the Company is to engage in finance lease, financing of small and medium-sized enterprises,

financing of productive assets and consumer finance in accordance with the Saudi Arabian Monetary Authority

(“SAMA”) license No. (201411/SA/26) issued on 27 Muharram 1436 H (corresponding to 20 November 2014).

The Company’s Head Office is located at the following address;

Saudi Finance Company

Korais Street

P.O. Box 18331

Riyadh 11415

Kingdom of Saudi Arabia

These interim condensed financial statements include the results, assets and liabilities of the following branches:

Branch Commercial Registration Number Date Location 1010137723 17 Rabi Thani 1416H Khurais, Riyadh

1010366245 23 Rabi Thani 1434H Olaya, Riyadh

1131013974 26 Dhul-Hijjah 1417H Buraidah

2251056896 16 Jumad Awal 1435H Al-Ahsa

4030242129 23 Rabi Thani 1434H Jeddah

4650073124 11 Sha’aban 1435H Madina

2051026306 24 Rabi Awal 1423H Damam

3350042118 11 Sha’aban 1435H Hail

The results for the three month period ended 31 March 2017 are not necessarily indicative of the results that may be

expected for the financial year ending 31 December 2017.

2 BASIS OF PREPARATION

2.1 STATEMENT OF COMPLIANCE

These interim condensed financial statements of the Company have been prepared in accordance with Accounting

Standards for Financial Institutions issued by SAMA and with International Accounting Standard (“IAS”) 34

“Interim Financial Reporting”.

These interim condensed financial statements do not include all the information and disclosures required in the

annual financial statements, and should be read in conjunction with the Company’s financial statements for the year

ended 31 December 2016.

Assets and liabilities in the interim statement of financial position are presented in the order of liquidity.

2.2 BASIS OF MEASUREMENT

The interim condensed financial statements are prepared under the historical cost convention modified to include

the measurement of Profit rate swaps at fair values.

2.3 FUNCTIONAL AND PRESENTATION CURRENCY

These interim condensed financial statements have been presented in Saudi Riyals, as it is the functional currency

of the Company.

Saudi Finance Company - (Closed Saudi Joint Stock Company)

NOTES TO FINANCIAL STATEMENTS (continued) For the three months period ended 31 March 2017

7

3 SIGNIFICANT ACCOUNTING POLICIES

The accounting policies adopted in the preparation of the interim condensed financial statements are consistent with

those followed in the preparation of the Company's annual financial statements as at 31 December 2016, except for

the following:

ZAKAT

On 14 Rajab 1438 (corresponding to 11 April 2017), SAMA has issued a new circular (number 381000074519)

regarding the accounting policy of Zakat and income tax in which it is mentioned that they should be charged

directly to the retained earnings of all finance companies irrespective of their ownership structure for the current

and comparative periods and this will be effective starting from 1 January 2017. Therefore, the Company has

adopted the above policy in the preparation of these interim condensed financial statements.

CREDIT LOSS PROVISIONING AND SUSPENSION OF INCOME FOR DELINQUENT ACCOUNTS

On 27 Rabie Alakher 1438 (corresponding to 25 January 2017), SAMA has issued a new circular (number

381000046342) regarding the accounting policy of credit loss provisioning in which it is mentioned that the

Company is required to set specific and general provisions, also, it is required to suspend the recognition of future

period income from delinquent accounts where delinquencies are more than 90 days until actually received.

Therefore, the Company has adopted the above policy in the preparation of these interim condensed financial

statements.

4 SIGNIFICANT ACCOUNTING JUDGEMENTS, ESTIMATES AND ASSUMPTIONS

The preparation of the Company’s interim condensed financial statements requires management to make

judgments, estimates and assumptions that affect the reported amounts of revenues, expenses, assets and liabilities,

and the accompanying disclosures, and the disclosure of contingent liabilities. Uncertainty about these assumptions

and estimates could result in outcomes that require a material adjustment to the carrying amount of assets or

liabilities affected in future periods.

The key assumptions concerning the future and other key sources of estimation uncertainty at the interim statement

of financial position date, that have a significant risk of causing a material adjustment to the carrying amounts of

assets and liabilities within the next financial period, are described below. The Company based its assumptions and

estimates on parameters available when the interim condensed financial statements were prepared. Existing

circumstances and assumptions about future developments, however, may change due to market changes or

circumstances arising beyond the control of the Company’s management. Such changes are reflected in the

assumptions when they occur.

Going concern The Company’s management has made an assessment of the Company’s ability to continue as a going concern and

is satisfied that the Company has the resources to continue in business for the foreseeable future. Furthermore, the

management is not aware of any material uncertainties that may cast significant doubt upon the Company’s ability

to continue as a going concern. The going concern assessment of the Company is based on a number of factors

including availability of financing lines from various financial institutions including related parties and the growth

of its Murabaha portfolio. Therefore, the financial statements of the Company have been prepared on going concern

basis.

Impairment losses on Murabaha receivables The Company reviews its non-performing Murabaha receivables at each reporting date to assess whether a specific

provision for credit losses should be recorded in the statement of comprehensive income. In particular, judgement

by management is required in the estimation of the amount and timing of future cash flows when determining the

level of provision required. Such estimates are based on assumptions about a number of factors and actual results

may differ, resulting in future changes to the specific provision.

The Company reviews its Murabaha financing portfolio to assess an additional collective impairment provision on

each reporting date. In determining whether an impairment loss should be recorded, the Company makes judgments

as to whether there is any observable data indicating that there is a measurable decrease in the estimated future cash

flows from a portfolio of Murabaha financing. Management uses estimates based on historical loss experience for

assets with credit risk characteristics and objective evidence of impairment similar to those in the portfolio when

estimating its cash flows. The methodology and assumptions used for estimating both the amount and the timing of

future cash flows are reviewed regularly to reduce any differences between loss estimates and actual loss

experience.

Saudi Finance Company - (Closed Saudi Joint Stock Company)

NOTES TO FINANCIAL STATEMENTS (continued) For the three months period ended 31 March 2017

8

4 SIGNIFICANT ACCOUNTING JUDGEMENTS, ESTIMATES AND ASSUMPTIONS (Continued)

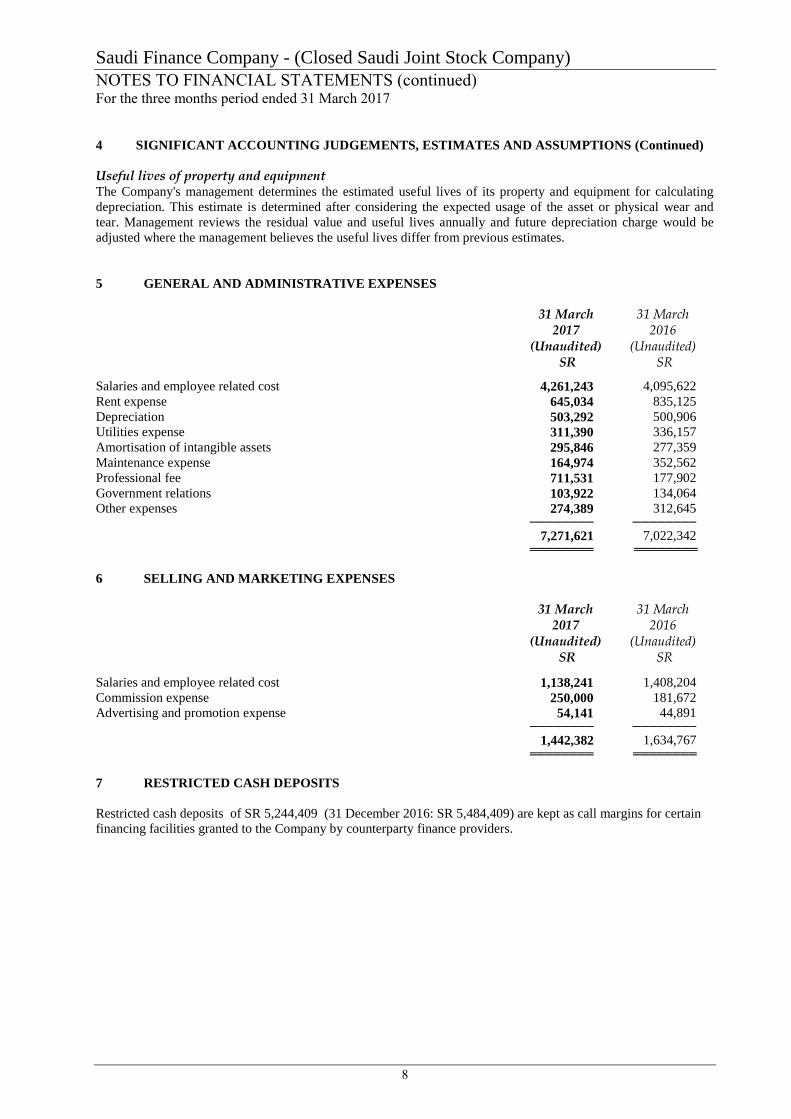

Useful lives of property and equipment The Company's management determines the estimated useful lives of its property and equipment for calculating

depreciation. This estimate is determined after considering the expected usage of the asset or physical wear and

tear. Management reviews the residual value and useful lives annually and future depreciation charge would be

adjusted where the management believes the useful lives differ from previous estimates.

5 GENERAL AND ADMINISTRATIVE EXPENSES

31 March 2017

(Unaudited) SR

31 March 2016

(Unaudited) SR

Salaries and employee related cost 4,261,243 4,095,622

Rent expense 645,034 835,125

Depreciation 503,292 500,906

Utilities expense 311,390 336,157

Amortisation of intangible assets 295,846 277,359

Maintenance expense 164,974 352,562

Professional fee 711,531 177,902

Government relations 103,922 134,064

Other expenses 274,389 312,645 ──────── ──────── 7,271,621 7,022,342 ════════ ════════

6 SELLING AND MARKETING EXPENSES

31 March 2017

(Unaudited) SR

31 March 2016

(Unaudited) SR

Salaries and employee related cost 1,138,241 1,408,204

Commission expense 250,000 181,672

Advertising and promotion expense 54,141 44,891 ──────── ────────

1,442,382 1,634,767 ════════ ════════

7 RESTRICTED CASH DEPOSITS

Restricted cash deposits of SR 5,244,409 (31 December 2016: SR 5,484,409) are kept as call margins for certain

financing facilities granted to the Company by counterparty finance providers.

Saudi Finance Company - (Closed Saudi Joint Stock Company)

NOTES TO FINANCIAL STATEMENTS (continued) For the three months period ended 31 March 2017

9

8 MURABAHA RECEIVABLES, NET

31 March 2017

(Unaudited) SR

31 December 2016

(Audited) SR

Gross Murabaha receivable 475,481,190 501,362,194 Less: Deferred profit (116,365,495) (123,833,880) ───────── ─────────

Murabaha receivable before impairment provision, net 359,115,695 377,528,314 Less: Impairment provision against Murabaha receivable (16,011,786) (13,591,786) ───────── ─────────

Murabaha receivable, net 343,103,909 363,936,528 ═════════ ═════════

The Murabaha finance includes related parties balance amounting to SR 48,868 (31 December 2016: SR

122,170) and related deferred profit amounting to SR 252 (31 December 2016: SR 2,520) (Note 14). Murabaha

receivable above also include Ijara receivable aggregating to SR 1,422,784 (31 December 2016: SR 1,533,821).

As at 31 March 2017, Murabaha finance at nominal value of SR 16,011,786 (31 December 2016: SR 13,591,786)

were impaired. The unimpaired Murabaha finance includes SR 205,990,437 (31 December 2016: SR 195,680,892)

which is past due more than normal collection cycle, but not impaired. Unimpaired receivables are expected, on the

basis of past experience, to be fully recoverable.

Movements in the provision for Murabaha receivable losses were as follows:

Three months ended 31 March

2017 (Unaudited)

SR

Year ended 31 December

2016 (Audited)

SR

Three months ended 31 March

2016 (Unaudited)

SR At beginning of the period / year 13,591,786 19,563,463 19,563,463

Charge for the period / year 2,420,000 9,080,000 2,480,000

Written of during the period / year - (15,051,677) - ──────── ──────── ────────

At end of the period / year 16,011,786 13,591,786 22,043,463 ════════ ════════ ════════

9 PREPAYMENTS, ACCRUED INCOME AND OTHER RECEIVABLES

31 March

2017 (Unaudited)

SR

31 December

2016 (Audited)

SR

Prepaid expenses 2,399,598 3,254,738

Due from a related party (note 14) 33,000 427,752

Special commission income receivable 60,058 51,074

Other receivables 690,808 563,786

──────── ────────

3,183,464 4,297,350

════════ ════════

Saudi Finance Company - (Closed Saudi Joint Stock Company)

NOTES TO FINANCIAL STATEMENTS (continued) For the three months period ended 31 March 2017

10

10 FINANCING FROM FINANCIAL INSTITUTIONS

This includes facilities obtained from local financial institutions in the form of medium term Islamic financing

(Tawarruq). These facilities are secured by assignment of receivables arising from financing contracts and a

comfort letter issued by the shareholders and carry commission at commercial rates. These facilities are repayable

on a monthly/quarterly basis. Financing from financial institutions also include various short term facilities of

eleven months obtained from Abu Dhabi Islamic Bank PJSC, a related party, UAE carrying commission at

commercial rates (note 14).

11 ZAKAT

The movement in the zakat provision for the period / year were as follows:

Three months ended 31 March

2017 (Unaudited)

SR

Year ended 31 December

2016 (Audited)

SR

Three months ended 31March

2016 (Unaudited)

SR

At beginning of the period / year 16,839,346 12,825,846 12,825,846

Provided during the period / year 1,227,000 4,608,861 1,151,229

Paid during the period / year - (595,361) -

───────── ───────── ─────────

At end of the period / year 18,066,346 16,839,346 13,977,075

═════════ ═════════ ═════════

Status of assessments

Subsequent to the year end, zakat assessments have been raised by the General Authority of Zakat and Income Tax

("GAZT") for the years 2005 to 2007 assessing an additional zakat of SR 2,621,509 and no provision has been

recorded in these financial statements as the Company is confident of a favorable outcome. The Company has filed

zakat returns and has obtained provisional zakat certificate for all the years up to 2015 and these are still under

review by the GAZT. During 2016, the Company received certain queries related to the year 2014 from GAZT and

has sent its responses to the GAZT.

12 ACCOUNTS PAYABLE, ACCRUALS AND OTHER PAYABLES

31 March 2017

(Unaudited) SR

31 December 2016

(Audited) SR

Accrued expenses 6,391,719 5,395,962

Trade payables 2,066,500 658,175

Unrealised loss on profit rate swap "PRS" (see note 12.1) 328,095 314,365

Amount due to a shareholder (note 14) 103,390 95,335

Other payables 224,303 197,963

──────── ────────

9,114,007 6,661,800

════════ ════════

12.1 This represents mark to market unrealised (loss)/gain on PRS with a notional principal amounting SR

37,344,482 as of 31 March 2017 (31 December 2016 SR 42,814,719).

PRS often involve at their inception only a mutual exchange of promises with little or no transfer of consideration.

However, these instruments frequently involve a high degree of leverage and are very volatile. A relatively small

movement in the value of the rate underlying a PRS contract may have a significant impact on the income of the

Company.

Saudi Finance Company - (Closed Saudi Joint Stock Company)

NOTES TO FINANCIAL STATEMENTS (continued) For the three months period ended 31 March 2017

11

13 SHARE CAPITAL

Paid in share capital as at 31 March 2017 and 31 December 2016 is as follows:

Capital

Shareholders Number of shares SR

ADIB Two Financial Invest LLC, U.A.E 5,100,000 51,000,000

Abdullah Ibrahim Al Khorayef Sons' Company, K.S.A 4,600,000 46,000,000

Mohamed Abdullah Al Khorayef 100,000 1,000,000

Saad Abdullah Al Khorayef 100,000 1,000,000

Hamad Abdullah Al Khorayef 100,000 1,000,000

──────── ───────── Total 10,000,000 100,000,000

════════ ═════════

14 RELATED PARTY TRANSACTIONS AND BALANCES

(a) Significant transactions with related parties during the period are as follows:

Related party Nature of transaction

Transactions 31 March

2017 (Unaudited)

SR

31 March 2016

(Unaudited) SR

Shareholders Rent expense 55,500 55,500

Financing 103,390 159,495

Collection fee income 16,010 15,340

Affiliates Special commission expenses 1,176,625 933,715

Management fees* - 532,000

Special commission income from Murabaha contracts 2,268 47,103

* The Company charges management fees to a related party at terms approved by the Company’s management.

(b) The compensation of key management personal for the period amounts to SAR 502,500 (three months ended 31

March 2016: SAR 929,500).

(c) The Company obtains financing from related party to meet its financing requirements.

(d) The following receivables and payables balances arose as a result of transactions with related parties:

Related party Name

31 March 2017

(Unaudited) SR

31 December 2016

(Audited) SR

Due from:

Affiliates Abu Dhabi Islamic Bank PJSC 33,000 427,752

Various (Murabaha receivable) 48,616 119,650

Due to:

Shareholders Abdullah Ibrahim Al Khorayef Sons Company K.S.A 103,390 95,335

Affiliates Abu Dhabi Islamic Bank PJSC (Financing from financial

institutions) 145,000,000 165,000,000

Saudi Finance Company - (Closed Saudi Joint Stock Company)

NOTES TO FINANCIAL STATEMENTS (continued) For the three months period ended 31 March 2017

12

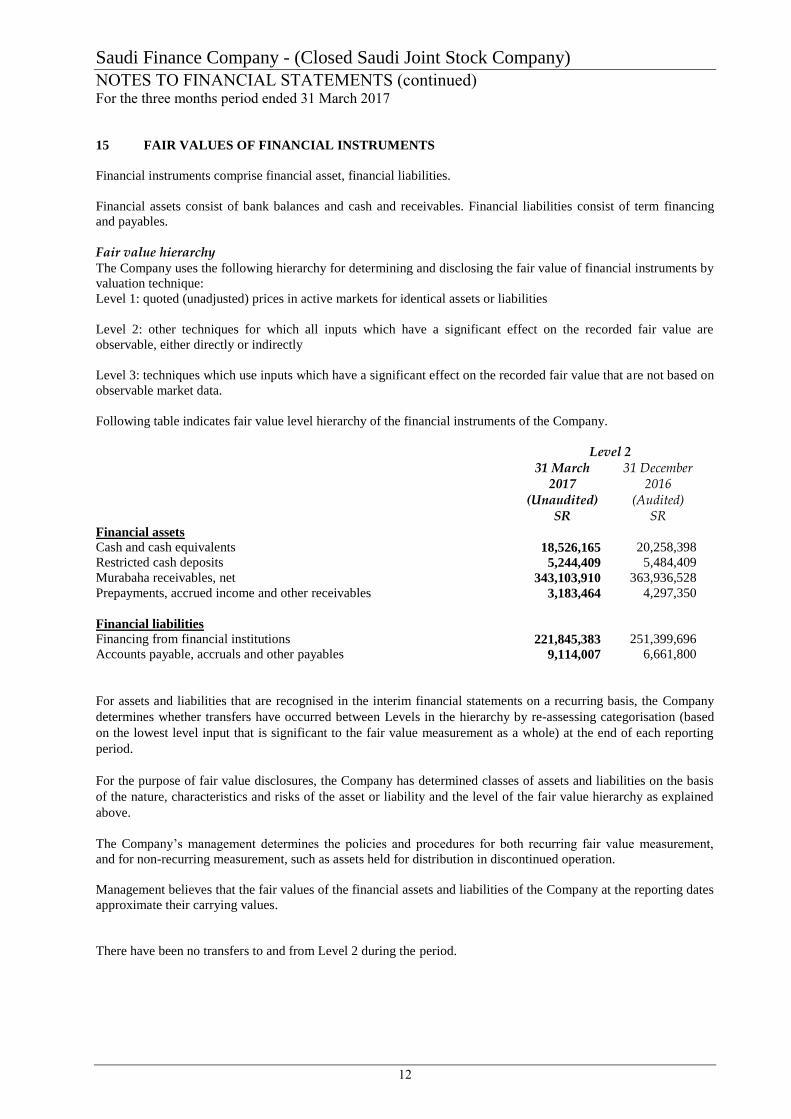

15 FAIR VALUES OF FINANCIAL INSTRUMENTS

Financial instruments comprise financial asset, financial liabilities.

Financial assets consist of bank balances and cash and receivables. Financial liabilities consist of term financing

and payables.

Fair value hierarchy The Company uses the following hierarchy for determining and disclosing the fair value of financial instruments by

valuation technique:

Level 1: quoted (unadjusted) prices in active markets for identical assets or liabilities

Level 2: other techniques for which all inputs which have a significant effect on the recorded fair value are

observable, either directly or indirectly

Level 3: techniques which use inputs which have a significant effect on the recorded fair value that are not based on

observable market data.

Following table indicates fair value level hierarchy of the financial instruments of the Company.

Level 2

31 March 2017

(Unaudited) SR

31 December 2016

(Audited) SR

Financial assets

Cash and cash equivalents 18,526,165 20,258,398

Restricted cash deposits 5,244,409 5,484,409

Murabaha receivables, net 343,103,910 363,936,528

Prepayments, accrued income and other receivables 3,183,464 4,297,350

Financial liabilities

Financing from financial institutions 221,845,383 251,399,696

Accounts payable, accruals and other payables

9,114,007 6,661,800

For assets and liabilities that are recognised in the interim financial statements on a recurring basis, the Company

determines whether transfers have occurred between Levels in the hierarchy by re-assessing categorisation (based

on the lowest level input that is significant to the fair value measurement as a whole) at the end of each reporting

period.

For the purpose of fair value disclosures, the Company has determined classes of assets and liabilities on the basis

of the nature, characteristics and risks of the asset or liability and the level of the fair value hierarchy as explained

above.

The Company’s management determines the policies and procedures for both recurring fair value measurement,

and for non-recurring measurement, such as assets held for distribution in discontinued operation.

Management believes that the fair values of the financial assets and liabilities of the Company at the reporting dates

approximate their carrying values.

There have been no transfers to and from Level 2 during the period.

Saudi Finance Company - (Closed Saudi Joint Stock Company)

NOTES TO FINANCIAL STATEMENTS (continued) For the three months period ended 31 March 2017

13

16 SIGNIFICANT STANDARDS ISSUED BUT NOT YET EFFECTIVE

A number of new standards and interpretations have been issued but are not yet effective. The Company intends to

adopt all the applicable standards and interpretations when these become effective. Management has assessed the

impact of these new standards and interpretations and believes that none of these would have any effect on the

future financial statements of the Company except for the following:

IFRS 15 Revenue from Contracts with Customers IFRS 15 was issued in May 2014 and establishes a new five-step model that will apply to revenue arising from

contracts with customers. Under IFRS 15, revenue is recognised at an amount that reflects the consideration to

which an entity expects to be entitled in exchange for transferring goods or services to a customer.

The principles in IFRS 15 provide a more structured approach to measuring and recognising revenue. The new

revenue standard is applicable to all entities and will supersede all current revenue recognition requirements under

IFRS. Either a full or modified retrospective application is required for annual periods beginning on or after 1

January 2019 with early adoption permitted. The Company is currently assessing the impact of IFRS 15 and plans

to adopt the new standard on the required effective date.

IFRS 9 Financial Instruments In July 2014, the IASB issued the final version of IFRS 9 Financial Instruments which reflects all phases of the

financial instruments project and replaces IAS 39 Financial Instruments: Recognition and Measurement and all

previous versions of IFRS 9. The standard introduces new requirements for classification and measurement,

impairment, and hedge accounting. IFRS 9 is effective for annual periods beginning on or after 1 January 2018,

with early application permitted. Retrospective application is required, but comparative information is not

compulsory. Early application of previous versions of IFRS 9 (2009, 2010 and 2013) is permitted if the date of

initial application is before 1 February 2015. The adoption of IFRS 9 will have an effect on the classification and

measurement of the Company’s financial assets, but no impact on the classification and measurement of the

Company’s financial liabilities. The Company is currently assessing the impact of IFRS 9 and plans to adopt the

new standard on the required effective date.

IFRS 16 Leases In January 2016, the IASB issued the final version of IFRS leases which sets out the principles of recognition,

measurement, presentation and disclosure of lease for parties to a contract, i.e. the costumer ("lessee") and the

supplier ("lessor"). IFRS 16 is effective for annual periods beginning on or after 1 January 2019 which early

application is permitted but only if it also applies IFRS 15 Revenue from Contracts with Costumers.

The adoption of IFRS 16 will have an effect on the classification and measurement on the Company's leased assets.

The Company is currently is assessing the impact of IFRS 16 and plan to adopt the new standard on the required

effective date.

Saudi Finance Company - (Closed Saudi Joint Stock Company)

NOTES TO FINANCIAL STATEMENTS (continued) For the three months period ended 31 March 2017

14

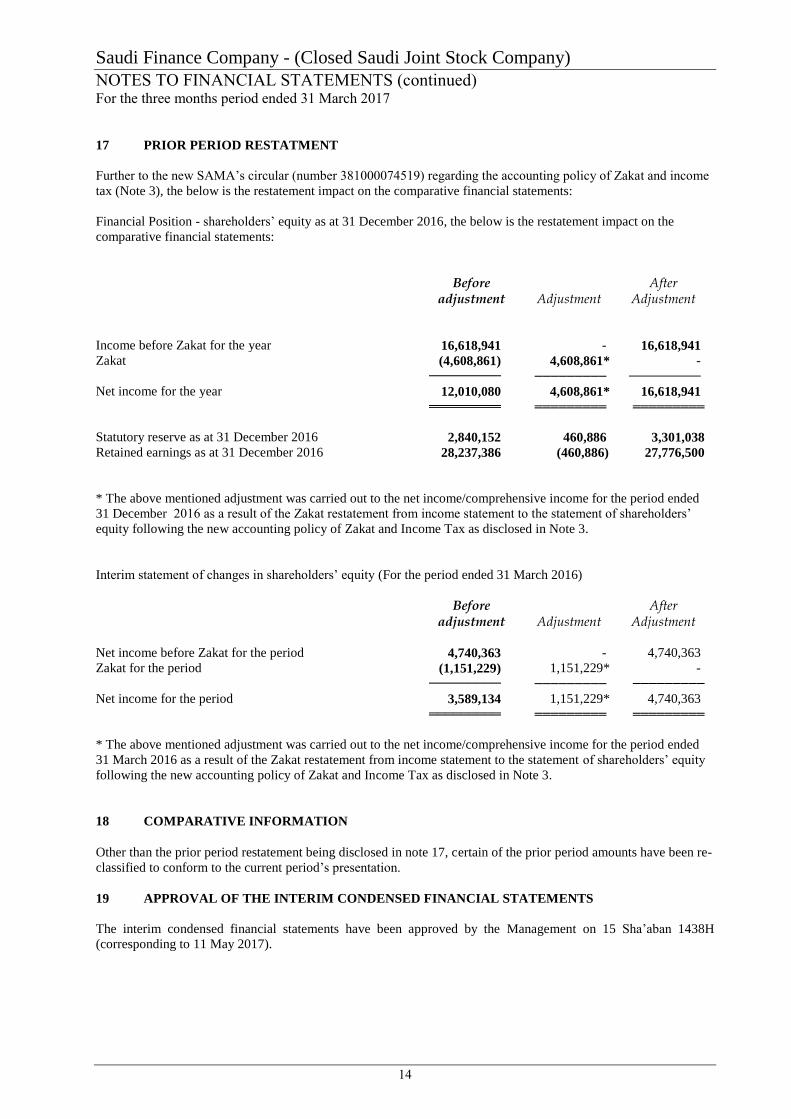

17 PRIOR PERIOD RESTATMENT

Further to the new SAMA’s circular (number 381000074519) regarding the accounting policy of Zakat and income

tax (Note 3), the below is the restatement impact on the comparative financial statements:

Financial Position - shareholders’ equity as at 31 December 2016, the below is the restatement impact on the

comparative financial statements:

Before adjustment Adjustment

After Adjustment

Income before Zakat for the year 16,618,941 - 16,618,941 Zakat (4,608,861) 4,608,861* -

───────── ───────── ─────────

Net income for the year 12,010,080 4,608,861* 16,618,941

═════════ ═════════ ═════════

Statutory reserve as at 31 December 2016 2,840,152 460,886 3,301,038 Retained earnings as at 31 December 2016 28,237,386 (460,886) 27,776,500

* The above mentioned adjustment was carried out to the net income/comprehensive income for the period ended

31 December 2016 as a result of the Zakat restatement from income statement to the statement of shareholders’

equity following the new accounting policy of Zakat and Income Tax as disclosed in Note 3.

Interim statement of changes in shareholders’ equity (For the period ended 31 March 2016)

Before adjustment Adjustment

After Adjustment

Net income before Zakat for the period 4,740,363 - 4,740,363

Zakat for the period (1,151,229) 1,151,229* -

───────── ───────── ─────────

Net income for the period 3,589,134 1,151,229* 4,740,363

═════════ ═════════ ═════════

* The above mentioned adjustment was carried out to the net income/comprehensive income for the period ended

31 March 2016 as a result of the Zakat restatement from income statement to the statement of shareholders’ equity

following the new accounting policy of Zakat and Income Tax as disclosed in Note 3.

18 COMPARATIVE INFORMATION

Other than the prior period restatement being disclosed in note 17, certain of the prior period amounts have been re-

classified to conform to the current period’s presentation.

19 APPROVAL OF THE INTERIM CONDENSED FINANCIAL STATEMENTS

The interim condensed financial statements have been approved by the Management on 15 Sha’aban 1438H

(corresponding to 11 May 2017).