Download - Scania Q2 2011 Presentation

Press conference E ik Lj b C t R l tiErik Ljungberg, Corporate Relations

1

Interim Report, January–June 2011 J Ytt b CFOJan Ytterberg, CFO

2

First six months of 2011 – highlights

Stable earningsI d l– Increased volume

– Currency head-winds– Altered market mix– Investments for future growth

ROCE 44.2% (23.4%)*

*Rolling 12 month

3

Volume trendT t l d li i t k d bTotal deliveries, trucks and buses

Units

Deliveries +42% in H1 2011

24,000

20,000

More vehicles to Russia and Middle

16,000

East – fewer to Brazil 8,000

12,000

Lower production rate in first part of

4,000

pQ2 2011 Q1

0Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1Q2 Q3Q4 Q1 Q2 Q3 Q4 Q2

2007 2008 2009 20112010

4

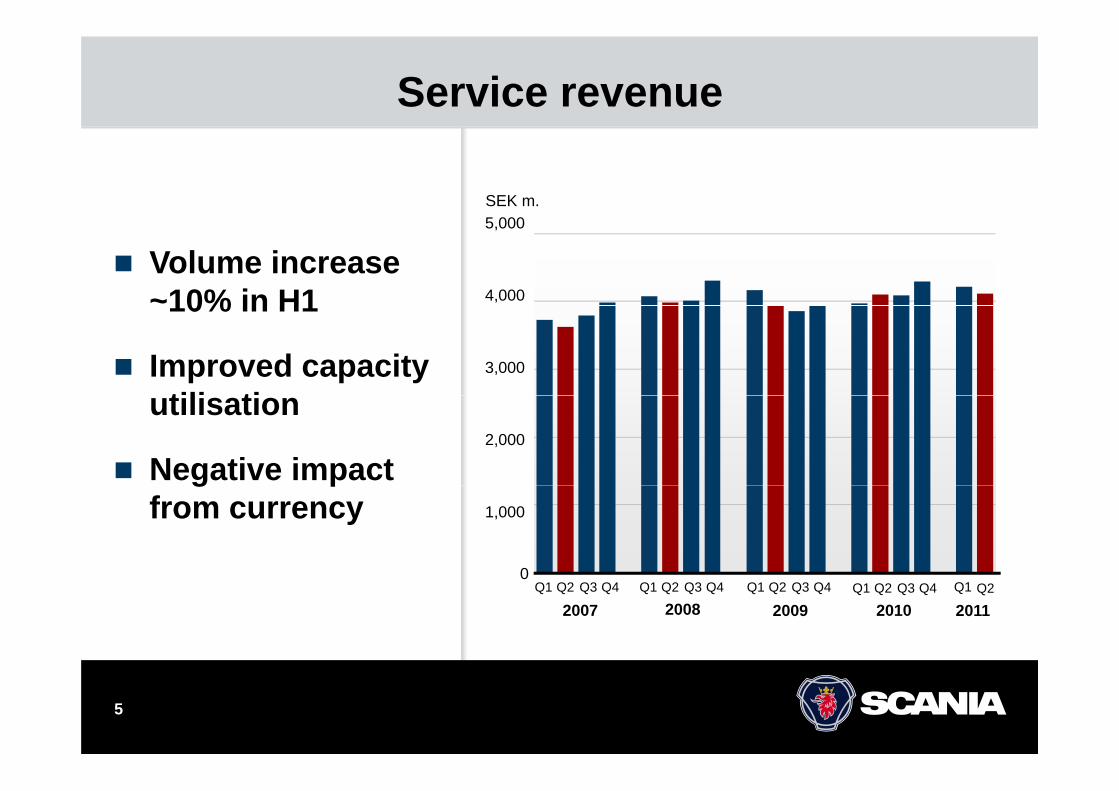

Service revenue

SEK m.

Volume increase ~10% in H1

5,000

4,00010% in H1

Improved capacity tili ti

3,000

utilisation

Negative impact 2,000

g pfrom currency 1,000

00Q1 Q2 Q3 Q4 Q1Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2007 2008 2009 2010 2011Q2

5

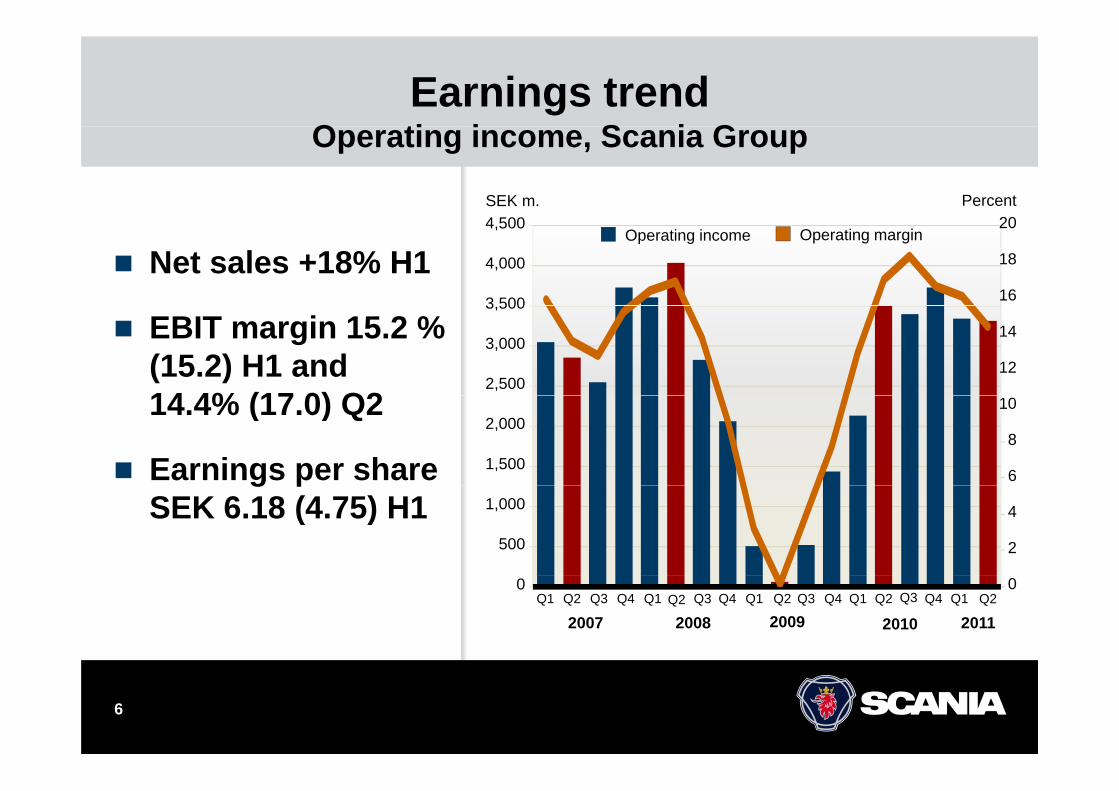

Earnings trendO ti i S i GOperating income, Scania Group

SEK m. Percent

Net sales +18% H1 4,000

4,500

3 500 16

20

18Operating marginOperating income

EBIT margin 15.2 % (15.2) H1 and 14 4% (17 0) Q2

3,000

3,500

2,50012

14

14.4% (17.0) Q2

Earnings per share 2,000

1,5008

6

10

g pSEK 6.18 (4.75) H1 1,000

500

4

2

Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q10

Q10

2007 2008 2009 2010 2011Q2

6

Operating incomeV hi l d S iVehicles and Services

EBIT increase due to:

EBIT increase:

+ Volume

+ Price

– Volume– Price

SEK 821 m. H1 2011

- Currency

- Mix

- Cost level

Negative effects:– Currency - Cost levely– Market mix– Higher cost level

7

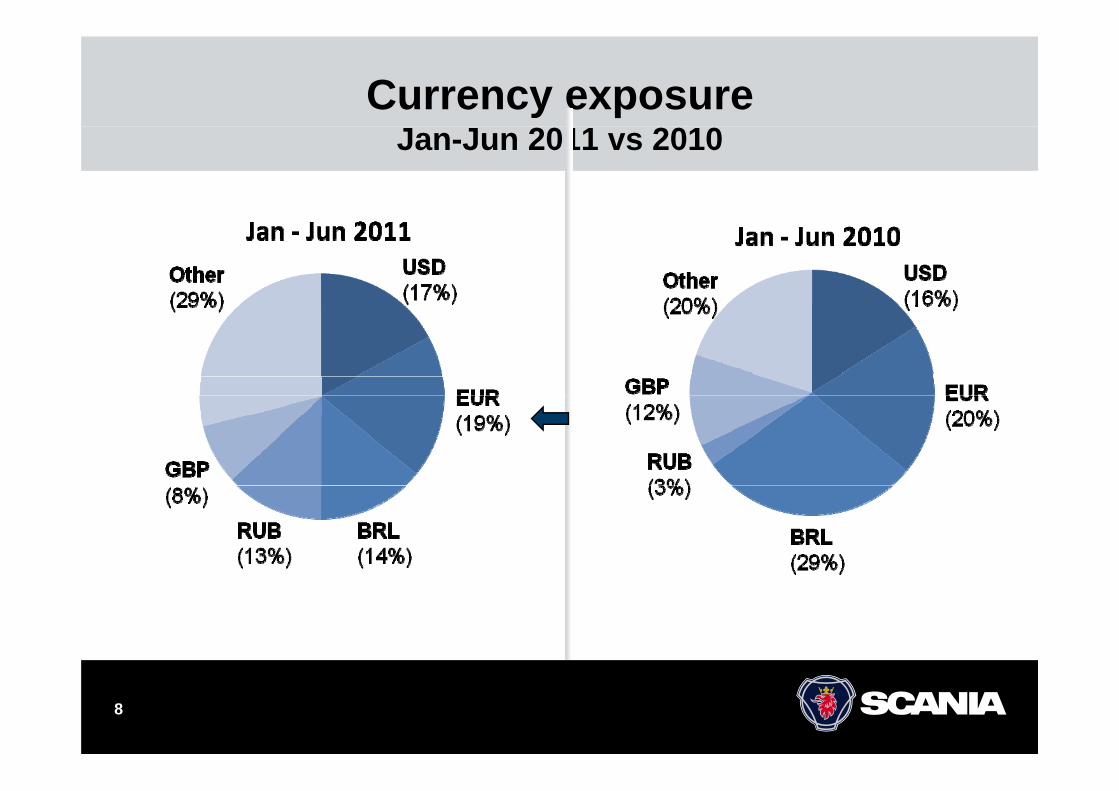

Currency exposureJan-Jun 2011 vs 2010

8

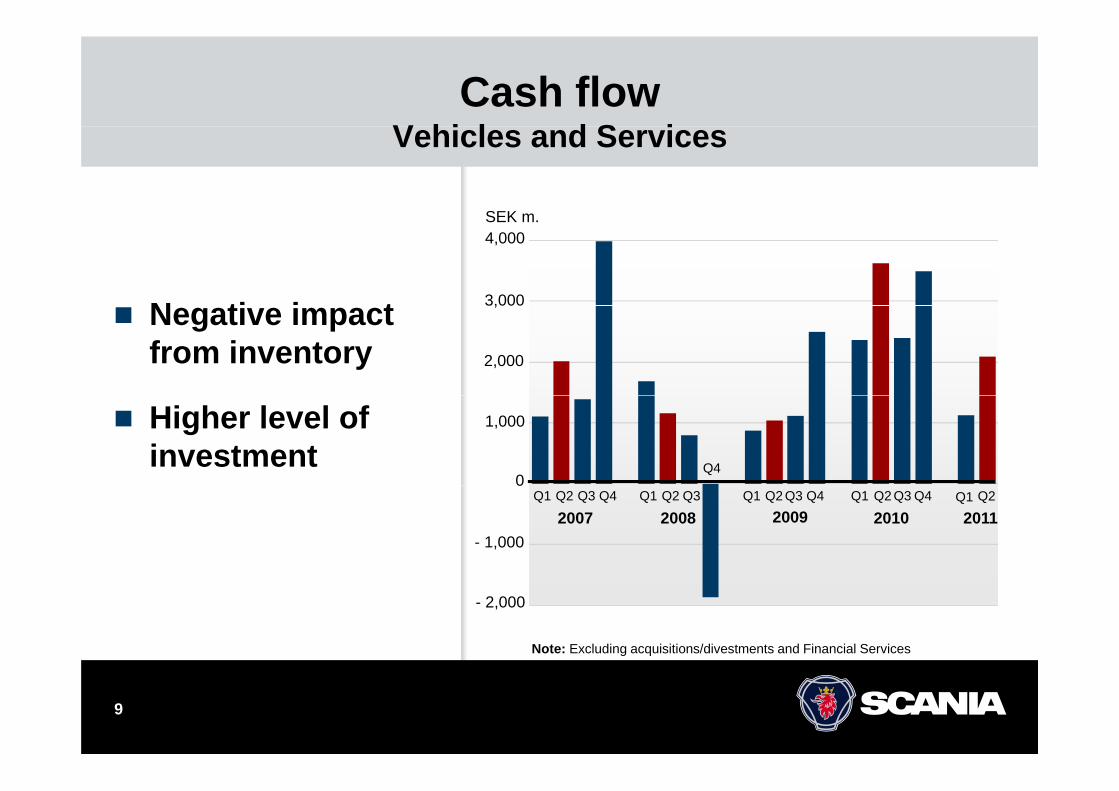

Cash flowV hi l d S iVehicles and Services

SEK m

N ti i t 3,000

4,000SEK m.

Negative impact from inventory 2,000

,

Higher level of investment

0

1,000

Q4

- 1,000

0

2007Q1 Q2 Q3 Q4

2008Q1 Q2 Q3

2009Q1 Q2 Q3 Q4

2010Q1 Q2 Q3 Q4

2011Q1 Q2

Note: Excluding acquisitions/divestments and Financial Services

- 2,000

9

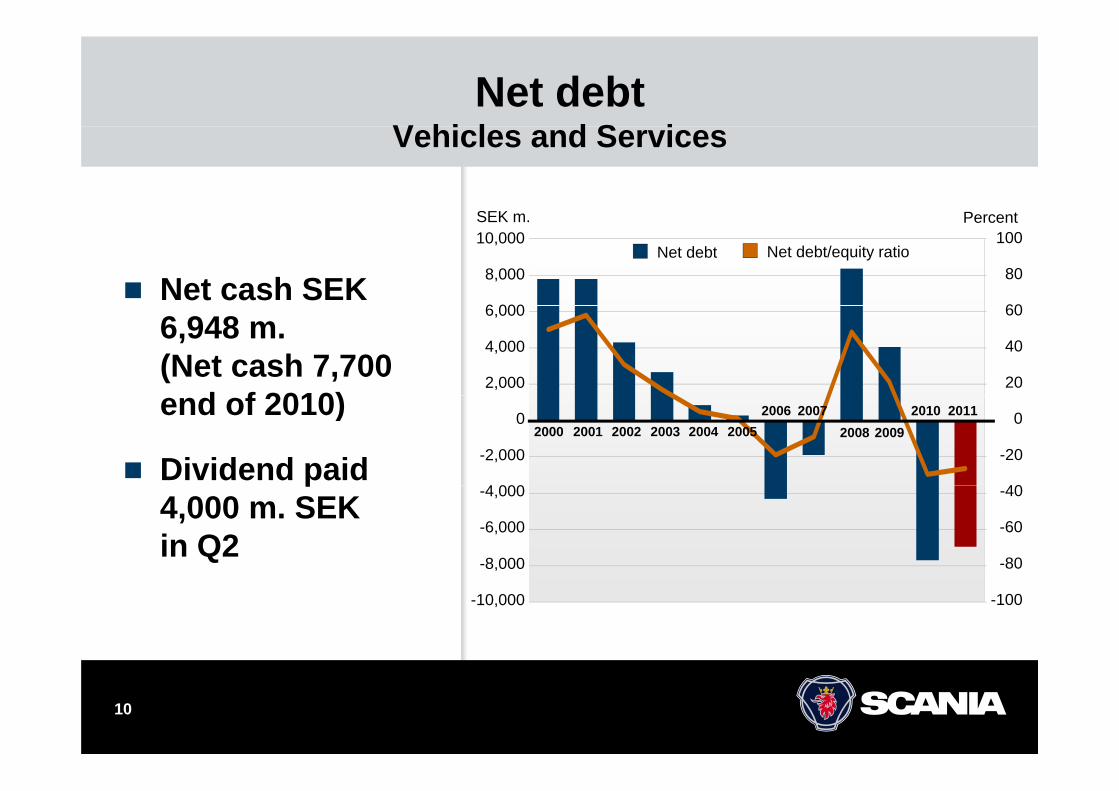

Net debtV hi l d S iVehicles and Services

SEK m Percent

Net cash SEK 8,000

6 000

SEK m.

60

100

80

Percent

Net debt/equity ratioNet debt10,000

6,948 m. (Net cash 7,700

d f 2010)2,000

6,000 60

404,000

20

end of 2010)

Dividend paid

0 20102008 20092001 2002 2003 2004 2005

2006 20072000

-2,000 -20

404 000

02011

p4,000 m. SEK in Q2

-40-4,000

-8,000

-6,000

-80

-60

-100-10,000

10

Volume trendC dit tf li Fi i l S iCredit portfolio, Financial Services

SEK m

Portfolio +8%*,i d f 2010

50,000

40 000

45,000

SEK m.

since end of 2010

Lower level of bad 30,000

35,000

40,000

debt expenses

Operating income 15 000

20,000

25,000

Operating income SEK 131 (49) m. in Q2

10,000

5,000

15,000

020071999 2001 2003 2005 20091997 2011

* In local currencies

11

Summary

Stable earningsVolume increase– Volume increase

– Currency head-windsAltered market mix– Altered market mix

– Investments for future growth

ROCE 44.2% (23.4%)*

*Rolling 12 month

12

13

OutlookL if Ö tli P id t d CEOLeif Östling, President and CEO

14

Business overview – First six months

Improved European demand

Still high demand in Latin America

Strong demand in Middle East and Russia

High demand for service

15

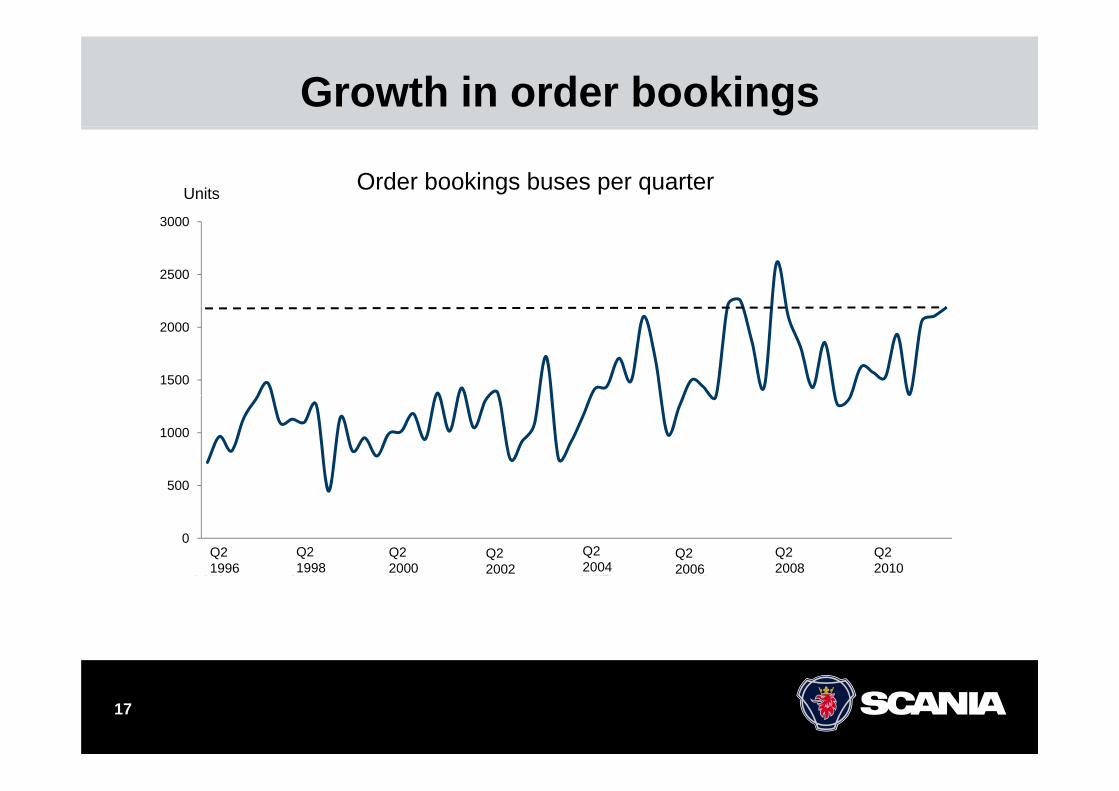

Growth in order bookings

Order bookings trucks per quarter30 000 Leadtimes 6-8

Units Lead times 8 10

20 000

25 000

weekstimes 8-10 months

15 000

20 000

5 000

10 000

0Q1

1996Q1

1998Q1

2000Q1

2002Q1

2004Q1

2006Q1

2008Q1

2010Q21996

Q21998

Q22000

Q22002

Q22004

Q22006

Q22008

Q220101996 1998 2000 2002 2004 2006 2008 20101996 1998 2000 2002 2004 2006 2008 2010

16

Growth in order bookings

Order bookings buses per quarterUnits

2500

3000

1500

2000

500

1000

0

500

Q11996

Q11998

Q12000

Q12002

Q12004

Q12006

Q12008

Q12010

Q21996

Q21998

Q22000

Q22002

Q22004

Q22006

Q22008

Q220101996 1998 2000 2002 2004 2006 2008 2010

17

Share of vehicle deliveries Q2 2011(2010)(2010)

EuropeEurasia

9% (2%)Europe 41% (38%)

9% (2%)

Latin America 26% (32%)

Asia19% (22%)26% (32%) Africa &

Oceania5% (6%)5% (6%)

1818

Investments to support growth

New companies in India and Japan

R&D investments to strengthen product

tf liportfolio

Investments in sales & service capacity

19

Investments to support growth

Boost production capacity to 120 000capacity to 120,000 vehicles

New agreement to increase flexibility in productionin production (Sweden)

20

21