Sears: Death by Debt

Minutemen Equity Fund

Hannah Kim, Joshua Owczarski, Sam Jezard

Isenberg School of Management

University of Massachusetts, Amherst

Submitted

February 20, 2015

2

Table of Contents

Company Overview .............................................................................................................................................. 3

Competition ............................................................................................................................................................. 3

Debt ............................................................................................................................................................................ 4

Financials ................................................................................................................................................................. 6

REIT Conversion ................................................................................................................................................. 10

Sears’ Turnaround potential? ........................................................................................................................ 11

Conclusion............................................................................................................................................................. 13

References ............................................................................................................................................................ 13

3

Company Overview

Sears Holding Corporation is a multi-billion dollar retailer with a 125 year history

operating across the United States. Presently with a market cap of approximately $4 billion, the

company operates 1,980 stores in the United States through Kmart and Sears, and 449 full-line

stores in Canada. The Company reports in three segments, Sears Domestic, Sears Canada, and

Kmart. In Canada, the Company operates as a majority stakeholder with 51% ownership.

Proprietary brands include Kenmore, Craftsman, and Diehard. Sears Domestic primarily focuses

on commercial sales, specialty stores, and home services while Canada focuses primarily on the

sale of apparel.

As of February 1, 2014, the Company operated 1,152 Kmart stores across the United

States, Guam, Puerto Rico, and the U.S. Virgin Islands. Kmart brands sells products in many

merchandise categories including apparel, consumables, and electronics. Notable apparel brands

include Joe Boxer and Jaclyn Smith. Presently, over 800 Kmart stores operate in-store

pharmacies.

Competition

Sears Holdings Corporation faces increasing pressure from other retailers that compete in

the same space. Since the company sells products in a variety of categories, there are many

competitors who are taking away market share. Competitors include Lowe’s, Home Depot,

Walmart, and Target have business models that are more efficient and profitable compared to

Sears.

4

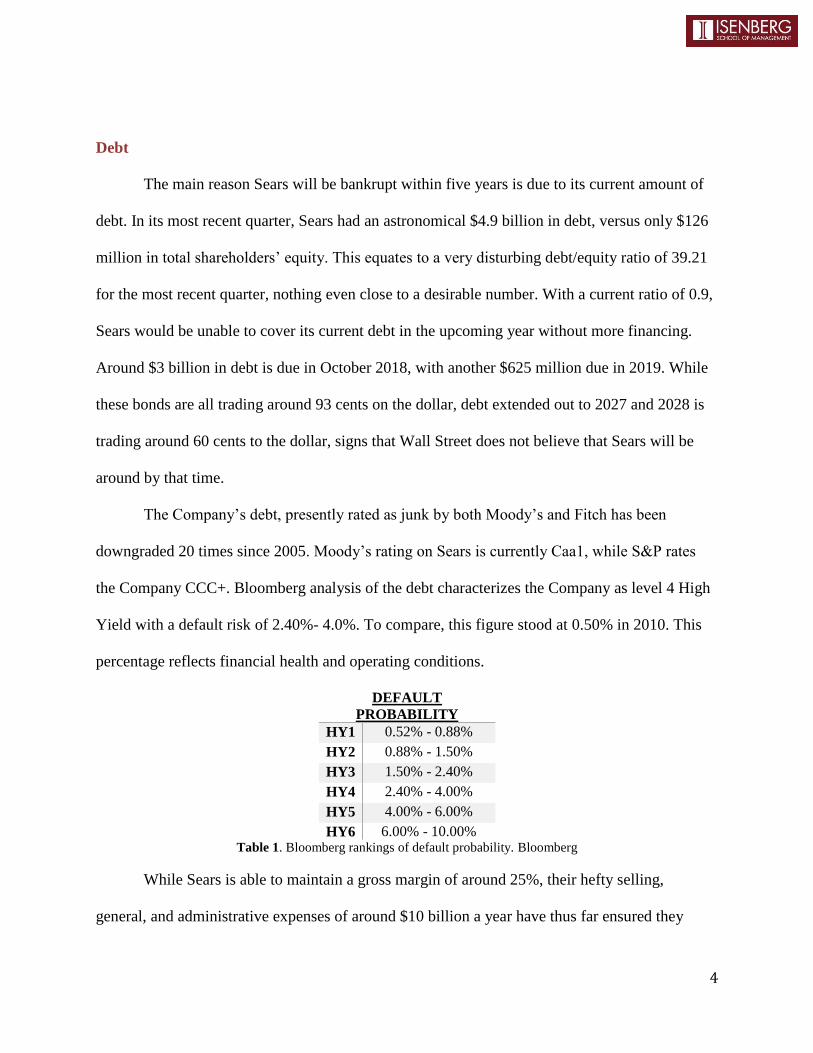

Debt

The main reason Sears will be bankrupt within five years is due to its current amount of

debt. In its most recent quarter, Sears had an astronomical $4.9 billion in debt, versus only $126

million in total shareholders’ equity. This equates to a very disturbing debt/equity ratio of 39.21

for the most recent quarter, nothing even close to a desirable number. With a current ratio of 0.9,

Sears would be unable to cover its current debt in the upcoming year without more financing.

Around $3 billion in debt is due in October 2018, with another $625 million due in 2019. While

these bonds are all trading around 93 cents on the dollar, debt extended out to 2027 and 2028 is

trading around 60 cents to the dollar, signs that Wall Street does not believe that Sears will be

around by that time.

The Company’s debt, presently rated as junk by both Moody’s and Fitch has been

downgraded 20 times since 2005. Moody’s rating on Sears is currently Caa1, while S&P rates

the Company CCC+. Bloomberg analysis of the debt characterizes the Company as level 4 High

Yield with a default risk of 2.40%- 4.0%. To compare, this figure stood at 0.50% in 2010. This

percentage reflects financial health and operating conditions.

DEFAULT

PROBABILITY

HY1 0.52% - 0.88%

HY2 0.88% - 1.50%

HY3 1.50% - 2.40%

HY4 2.40% - 4.00%

HY5 4.00% - 6.00%

HY6 6.00% - 10.00% Table 1. Bloomberg rankings of default probability. Bloomberg

While Sears is able to maintain a gross margin of around 25%, their hefty selling,

general, and administrative expenses of around $10 billion a year have thus far ensured they

5

sustain a heavy operating loss and a negative EBIT. These operating expenses primarily include

severances and expenses attributable to store closings. These expenses have been a weight on the

Company’s back as they try to compete in an increasingly crowded space. In the latest fiscal

year, Sears’ operating loss totaled $927 million and EBIT totaled $718 million.

Of the Sears outstanding debt, $400 million is a secured short-term loan agreement with

entities affiliated with ESL investments, Mr. Edward Lampert’s personal hedge fund. Mr.

Lampert and ESL investments also held an aggregate of $205 million in secured notes due 2018.

The debt issued by CEO Lambert’s hedge fund, while a lifeline to the company, are secured by

over two dozen properties that should the company declare bankruptcy, be forfeited to ESL

Investments.

A majority of the debt held by ESL is asset-backed, which relates to the one positive item

Sears has on its balance sheet: its stores. In 2014, Sears sold two full line stores for $64 million

in cash, resulting in a gain of $42 million. So, while Sears continues to post lower and lower

earnings, its one true defense against bankruptcy is and will be the sale of its property. However,

as Sears is forced to issue more debt to cover its losses, it will eventually run out of brands to

spin off and buildings to sell. According to Bloomberg, it now costs more to insure against a

default for a year than for five years, a sign that Wall Street traders are betting on bankruptcy.

If Sears does indeed sell and leaseback 300 stores as part of its turnaround efforts, it gives

it less leverage when it comes time to issue more debt in order to pay the bills, and it effectively

eliminates the cushion provided by owning those stores. Further sale of property would only

further hurt their already steeply declining revenues.

6

Financials

As has been plainly pointed out in the aforementioned sections, the financial situation of

Sears Holding Corporation is disastrous. To say that S is bleeding cash and racking up

exceptionally high levels of debt is naïve at best. The financial situation at Sears is more akin to

a sliced artery, haphazardly patched with duct tape and super glue. The core business segments

of Sears’ companies, namely retail sales of consumer goods and services, has not been profitable

for 4 years, and only marginally profitable prior to that. The only successful part of their newly

formulated business strategy has been the fire sale of real estate and long-standing exclusive

brand names such as Land’s End, which are only considered successful when compared to total

liquidation. As the company stands today, the only real value lies in its massive real estate

portfolio, nascent online “Shop Your Way” retail service, and the in-house brands Diehard

batteries, Craftsman tools, and Kenmore appliances, all shells of their former selves, much like

their parent company. Sears is a dying company when viewed in plain text, but the hard, publicly

available financial data spells the writing on the wall for the one-time king of American

consumer retail.

Sears’ financial distress can be seen as soon as one takes even a cursory glance at their

income statement. Using their Q3 2014 10-Q and 2013 10-K statements, numerous glaring trends

are laid out in black and white. Overall revenue has fallen 9.75% in the 39 weeks ended

November 1, 2014 when compared to revenue over the same period in 2013. Total costs and

expenses have fallen 7.24% over the same period, reflecting a failure to reduce costs adequately

in a smaller economy of scale. Sears’ failed to turn a profit during the 39 weeks ended November

2, 2013, posting a $1.007B net loss, and accelerated this hemorrhaging of cash to an eye-

watering $1.523B net loss over the same period in 2014.

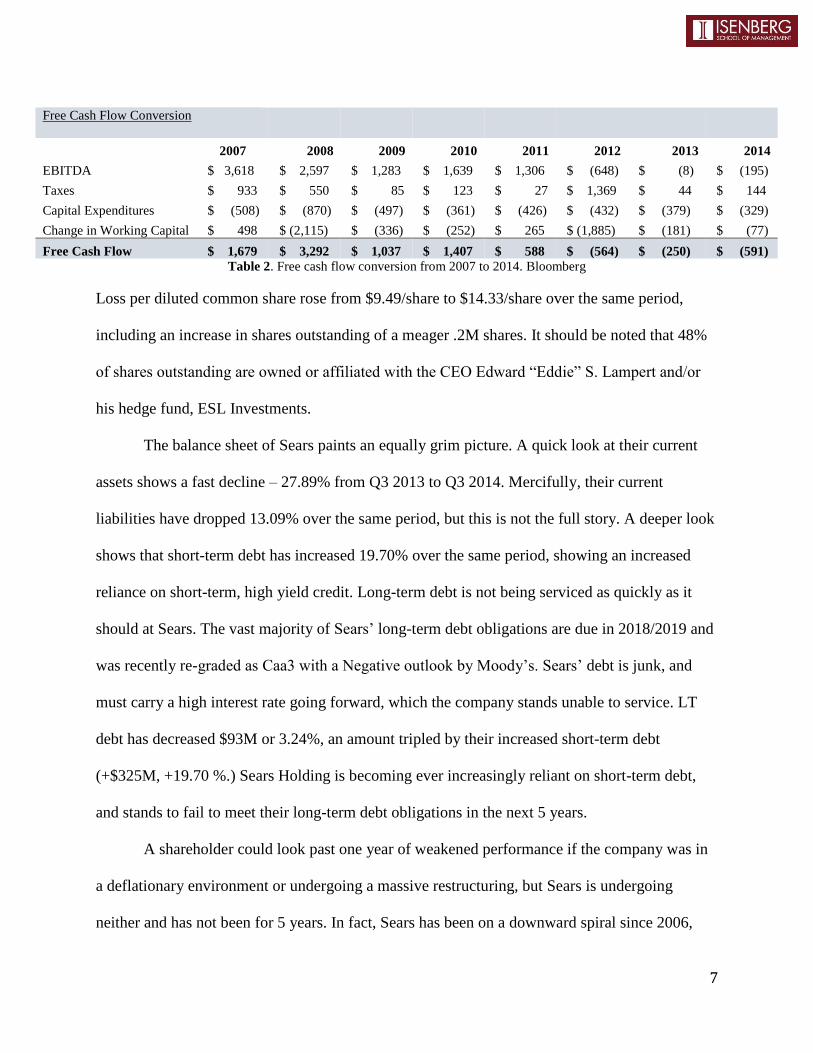

7

Table 2. Free cash flow conversion from 2007 to 2014. Bloomberg

Loss per diluted common share rose from $9.49/share to $14.33/share over the same period,

including an increase in shares outstanding of a meager .2M shares. It should be noted that 48%

of shares outstanding are owned or affiliated with the CEO Edward “Eddie” S. Lampert and/or

his hedge fund, ESL Investments.

The balance sheet of Sears paints an equally grim picture. A quick look at their current

assets shows a fast decline – 27.89% from Q3 2013 to Q3 2014. Mercifully, their current

liabilities have dropped 13.09% over the same period, but this is not the full story. A deeper look

shows that short-term debt has increased 19.70% over the same period, showing an increased

reliance on short-term, high yield credit. Long-term debt is not being serviced as quickly as it

should at Sears. The vast majority of Sears’ long-term debt obligations are due in 2018/2019 and

was recently re-graded as Caa3 with a Negative outlook by Moody’s. Sears’ debt is junk, and

must carry a high interest rate going forward, which the company stands unable to service. LT

debt has decreased $93M or 3.24%, an amount tripled by their increased short-term debt

(+$325M, +19.70 %.) Sears Holding is becoming ever increasingly reliant on short-term debt,

and stands to fail to meet their long-term debt obligations in the next 5 years.

A shareholder could look past one year of weakened performance if the company was in

a deflationary environment or undergoing a massive restructuring, but Sears is undergoing

neither and has not been for 5 years. In fact, Sears has been on a downward spiral since 2006,

Free Cash Flow Conversion

2007 2008 2009 2010 2011 2012 2013 2014

EBITDA $ 3,618 $ 2,597 $ 1,283 $ 1,639 $ 1,306 $ (648) $ (8) $ (195)

Taxes $ 933 $ 550 $ 85 $ 123 $ 27 $ 1,369 $ 44 $ 144

Capital Expenditures $ (508) $ (870) $ (497) $ (361) $ (426) $ (432) $ (379) $ (329)

Change in Working Capital $ 498 $ (2,115) $ (336) $ (252) $ 265 $ (1,885) $ (181) $ (77)

Free Cash Flow $ 1,679 $ 3,292 $ 1,037 $ 1,407 $ 588 $ (564) $ (250) $ (591)

8

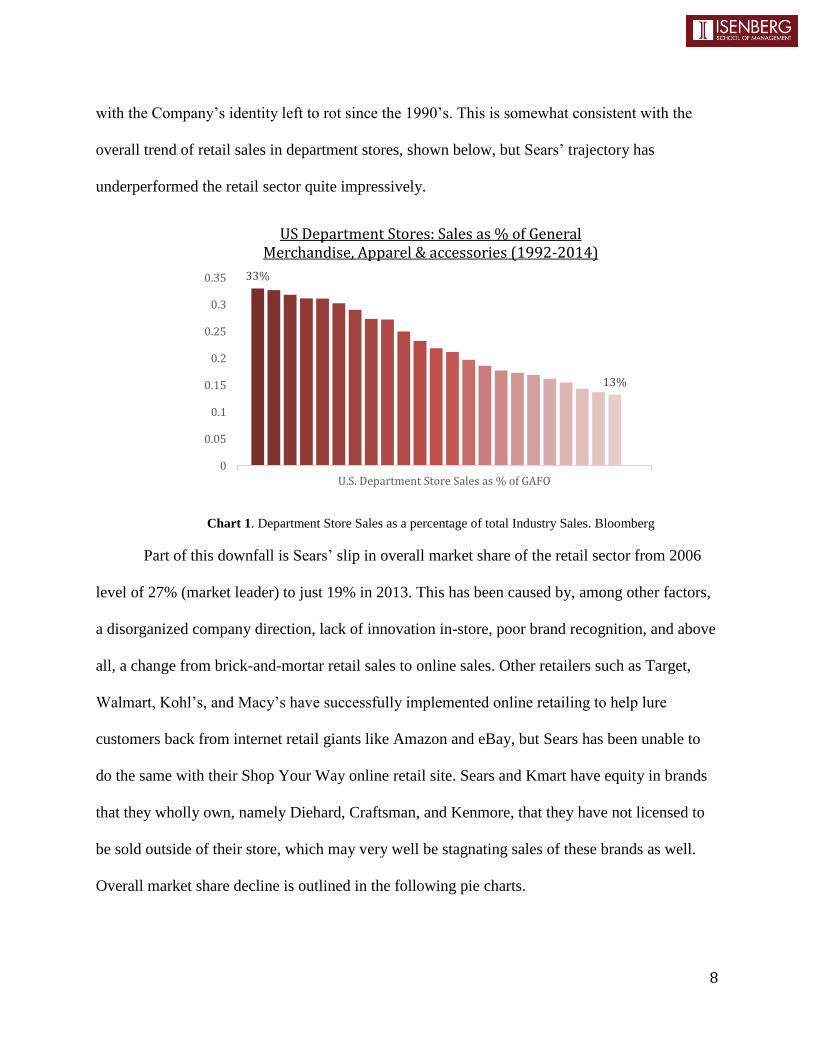

with the Company’s identity left to rot since the 1990’s. This is somewhat consistent with the

overall trend of retail sales in department stores, shown below, but Sears’ trajectory has

underperformed the retail sector quite impressively.

Chart 1. Department Store Sales as a percentage of total Industry Sales. Bloomberg

Part of this downfall is Sears’ slip in overall market share of the retail sector from 2006

level of 27% (market leader) to just 19% in 2013. This has been caused by, among other factors,

a disorganized company direction, lack of innovation in-store, poor brand recognition, and above

all, a change from brick-and-mortar retail sales to online sales. Other retailers such as Target,

Walmart, Kohl’s, and Macy’s have successfully implemented online retailing to help lure

customers back from internet retail giants like Amazon and eBay, but Sears has been unable to

do the same with their Shop Your Way online retail site. Sears and Kmart have equity in brands

that they wholly own, namely Diehard, Craftsman, and Kenmore, that they have not licensed to

be sold outside of their store, which may very well be stagnating sales of these brands as well.

Overall market share decline is outlined in the following pie charts.

33%

13%

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

U.S. Department Store Sales as % of GAFO

US Department Stores: Sales as % of General Merchandise, Apparel & accessories (1992-2014)

9

Charts 2 and 3. Change in Industry Market Share from 2006 to 2013. Bloomberg

Total revenue from 2006 has fallen every single year from $53.012B to $36.188B in 2013

– a 31.73% decline. Sears has not turned a profit since 2010. Same store sales have been

declining at a rate between 3-10% since 2006. Short term debt has ballooned from $95M in 2006

to $1.32B in 2013 – an incredible increase of 1289%. Net income and EPS have tanked since

2007 from healthy levels to negative levels, shown in the following graph:

Chart 4. Sears Holding Corporation Profitability from 2007 – Present. Bloomberg

Further insight into the current financial state of Sears is not necessary to determine that

the company is doomed. Unless the company can radically reduce costs through elimination of

(10.00)

(5.00)

-

5.00

10.00

EPS to Net Interest Margin

Adjusted EPS Net Income Margin %

Linear (Adjusted EPS)

Macy's Inc22%

Sears27%Kohl's

Corp12%

Nordstrom Inc7%

JC Penney Co Inc

16%

Other16%

Market Share FY 2006

Macy's Inc24%

Sears19%

Kohl's Corp16%

Nordstrom Inc10%

JC Penney Co Inc

10%

Other21%

Market Share FY 2013

10

non-key assets, recast their brand as a better alternative to internet and brick-and-mortar retailers,

and find a way to restructure and refinance 100% of their short and long term debt, the company

will be forced to liquidate their assets to satisfy their creditors in the next five years. The only

alternative is to constantly issue new debt, because their equity is for all intents and purposes,

worthless. The company has not turned a profit in 4 years, they pay no dividends although they

are structured as a REIT, their costs are increasing, and their revenues are set to further fall. No

business can stand to function without breaking even, and there seems to be no light at the end of

the tunnel for this once iconic American retailer. Chapter 7 bankruptcy will be the ultimate fate

of Sears by 2020.

REIT Conversion

Sears has been in financial trouble for quite some time with a net loss every year since

2011. Instead of focusing most of its energy on re-evaluating the business model, management’s

reaction to the poor state of its financials has been to engineer creative financial solutions to

manipulate the numbers and stave off the inevitable: bankruptcy.

Sears’ only valuable assets in this market are its real estate properties. In November 2014,

Sears introduced a plan to form a new real estate investment trust by selling anywhere from 200

to 300 stores to the REIT and leasing the stores back to Sears. This strategic move is meant to

protect the value of the real estate properties in case of bankruptcy. Putting some properties into

a REIT is also a move meant to appease shareholders who have been disappointed with Sears’

performance over the past few years.

11

Chart 5. Sears Holding Corporation Properties Structure. Bloomberg

Selling and leasing back real estate properties is usually a strategy that is employed when a

company wants to extract the value, namely capital, from real estate properties in order to direct

that cash flow to profitable areas of the business. Sears does not have profitable areas of

business. This last-ditch attempt at salvaging the business may buy the company time but it will

not reinvigorate the dying retailer.

Sears’ management is responsible for not just selling its stores to a REIT, but also

financial manipulation. The Sears’ CEO, Eddie Lampert, has been turning Sears’ major

subsidiaries into non-guarantor entities, which means that most creditors cannot touch the assets

that are in these specific subsidiaries. Sears had 4 main non-guarantor entities, with REMIC,

KCD IP, Sears Reinsurance, and SRe Holding.

Sears’ Turnaround potential?

Sears has a phenomenal management team with a proven track record. CEO Eddie

Lampert also serves as the CEO of ESL investments, a hedge fund that owns 49% of Sears’

195

517

16

957

311208 225

Kmart Sears Domestic Sears Canada

Properties

Owned Leased Independently Owned and operated

12

common stock. With ESL being so heavily invested in Sears, it is clear that Lampert has bought

in to bringing the retailer back to life. However, even with his attempts to capitalize on Sears’

real estate holdings and lease them back to Sears and other retailers, unless the Company is able

to generate more revenue, we are only delaying the inevitable. Sears last turned a profit in 2010,

and EBIT has been sloping downward ever since that time.

There is the possibility that Sears’ attempt to grow its online marketplace will indeed be

successful. As Sears looks to cut back on its number of brick and mortar stores and decrease

inventory, it may in fact be able to cut the costs that have been weighing it down and producing

negative financial results. It was number five amongst online retailers in 2013 in terms of sales.

A leaner, more efficient Sears may be in store for the future. Having said that, in-store sale still

account for more than 90% of revenue, and Sears’ high e-commerce sales are more of a

testament to the size of the company and its historical brand image rather than its future

potential. It is estimated that in 2012 Sears’ online sales of $1.2 billion accounted for just 3% of

its total sales. Even if e-commerce sales grew at 20% a year, it would be another 15 years before

the $18 billion mark was reached, and that wouldn’t even constitute half of total sales. By that

time, Sears will be fully drowned in debt and out of buildings to sell.

Despite the high amount of revenue earned in-store, Lampert continues to show that he

would rather focus on Sears’ online presence versus improve on its brick and mortar stores. This

is even when traditional online retailers like Amazon are looking to create physical locations for

customers to shop. In 2012, Sears spent only $1.51 per square foot on its Sears’ stores and $1.04

on its Kmart brand stores, paltry in comparison to companies such as Home Depot and Macy’s,

which spent $5.56 and $6.25 per square foot respectively (Bloomberg.com). It has also been

13

reported by Walter Loeb from Bloomberg.com that Sears’ traditional seven-year maintenance

cycle has been ignored in the vast majority of their stores (Loeb, Bloomberg.com).

Conclusion

It is coming to a point where Sears’ 129-year history is working against the Company.

During the prosperous days, the Company was the go to store for everything from power tools to

entertainment. In the modern day where consumers can compare dozens of prices from their

living room and stores are increasingly specialized, it is becoming increasingly difficult to

compete.

We believe that if not for CEO Eddie Lampert and ESL Investments, the Company would

have already run out of cash and began bankruptcy proceedings. A primary reason for ESL’s

continued support of Sears does not revolve around the Company’s operations but on the land.

While we see value in the land over the next 5 years, we do not see Sears making past 2020.

References

1. Natarajan, Sridhar. "Traders Are Betting Sears Will Be the Next Big Retailer to Fail."

Bloomberg.com. February 19, 2015. <http://www.bloomberg.com/news/articles/2015-02-

19/sears-turnaround-seen-failing-by-traders-in-credit-swaps-market>

2. Loeb, Walter. "Sears Will Drown In Debt As Savvy Consumers Shop Elsewhere."

Forbes. September 18, 2014. <http://www.forbes.com/sites/walterloeb/2014/09/18/sears-

will-drown-in-debt-as-savvy-consumers-shop-elsewhere/>

3. All data cited in this report was retrieved from the Bloomberg Terminal.

![Untitled-2 1 29/11/2017 16:30 [cdn.static-economist.com]](https://cdn.vdocument.in/doc/165x107/616a11f711a7b741a34e7a19/untitled-2-1-29112017-1630-cdnstatic-.jpg)