Download - Sell Sheet Package

� 1327 14th St NW #101, Washington, DC 20005

� 185 Admiral Cochrane Dr, Ste 205, Annapolis, MD 21401

� 437 Memorial Dr, SE Suite 2-A, Atlanta, GA 30312

p: 202.899.2600 w: downscapital.com

NMLS #15622

DOWNS CAPITAL IS PART OF CALIBER HOME LOANS

EXPERIENCEWINS REAL STORIES

IN REAL ESTATE LOANS

DOWNS CAPITAL | 202.899.2600 | DOWNSCAPITAL.COM

WHO IS DOWNS CAPITAL?

Downs Capital is a tight tribe of mortgage experts. We’re a unit of

Caliber Home Loans, the fi fth largest purchase lender in the United

States, and we’re licensed in all 50 states. Caliber makes $3.3 billion

in mortgages every month.

Our scale allows us to o� er great loans for all types of customers; our expertise enables us to

accelerate the lending process. The fact that we keep 98 percent of the loans we make speaks

to our commitment to our customers and their long term fi nancial health.

We are simply not a love ‘em and leave ‘em group; we’re interested in long term relationships,

which may be why 80 percent of our clients return to us when it comes time to refi nance or buy a

new home.

We get things done, even when there are hurdles to jump, timelines to meet, challenging or

unique properties, and clients that need education about the lending process.

Frankly, we’re persnickety fi nance geeks who sweat every detail of every transaction. We just

can’t help it. We love this business.

PARTNERS

Mortgages are about relationships. We are in love with our clients and will go to the ends of the

earth to help them build wealth by matching the right mortgage to their lives.

Yet our business isn’t only about clients; it’s about you. We must earn your trust fi rst and

always. You are our partner, in every sense of the word.

OUR COMMITMENTS TO YOU

Your clients will receive white glove service, and the transaction will not be derailed by hiccups in

the process. Our lending process is driven by understanding, not piles of paperwork.

We take great care to understand your client: What is your client trying to achieve? Not just

for now, but in life? Will they stay in the home for a couple of years, or 20 years? What is their fi nan-

cial situation, now and going forward? Do they have specifi c investment goals?

We understand the process: What documentation is really necessary? We assemble just

enough of the right evidence to shine a positive light on your client. Then we submit and tightly

manage the fi le through underwriting. We are by nature over-communicators, so you will always

know precisely what is happening, and when.

We get to know you and your business. What can we do to help your clients? How can we

enable you to do more business? How can we help YOU?

We appreciate that your client is our client, and vice versa. We’re both in this for the long

haul. Every time your client calls us, we’ll always keep you top of mind.

FRANKLY, WE'RE PERSNICKETY FINANCE GEEKS WHO SWEAT EVERY DETAIL OF EVERY TRANSACTION.

DOWNS CAPITAL | 202.899.2600 | DOWNSCAPITAL.COM

WHY DOWNS CAPITAL?

EDUCATION ANDPLANNING

Your clients will truly grasp

the market and fi nancial

benefi ts of ownership — the

nitty gritty and practical

information that is often

overlooked, but transforms

buyers into confi dent

homeowners.

KNOWLEDGE

We love this stu� . You’ll

always fi nd us waist deep in

research and exploring the

market. Plus, we have

decades of experience in

every situation a buyer may

face. Sharing knowledge is

our thing, so look to us to

bring success to you and

your clients.

MISTAKE-FREE

Emphasis on prequalifying

your clients allows us to

gather vital insights and do

the heavy lifting early. So,

when it’s time to get the loan

approved, we can do it in

record time and swiftly move

to close the transaction.

SPEED-TO-CLOSE

The art of a lightning fast

close is equal parts brains

and technology. We intelli-

gently prepare our clients

and underwriters so that

there are no obstacles to

closing quickly — and right

on time.

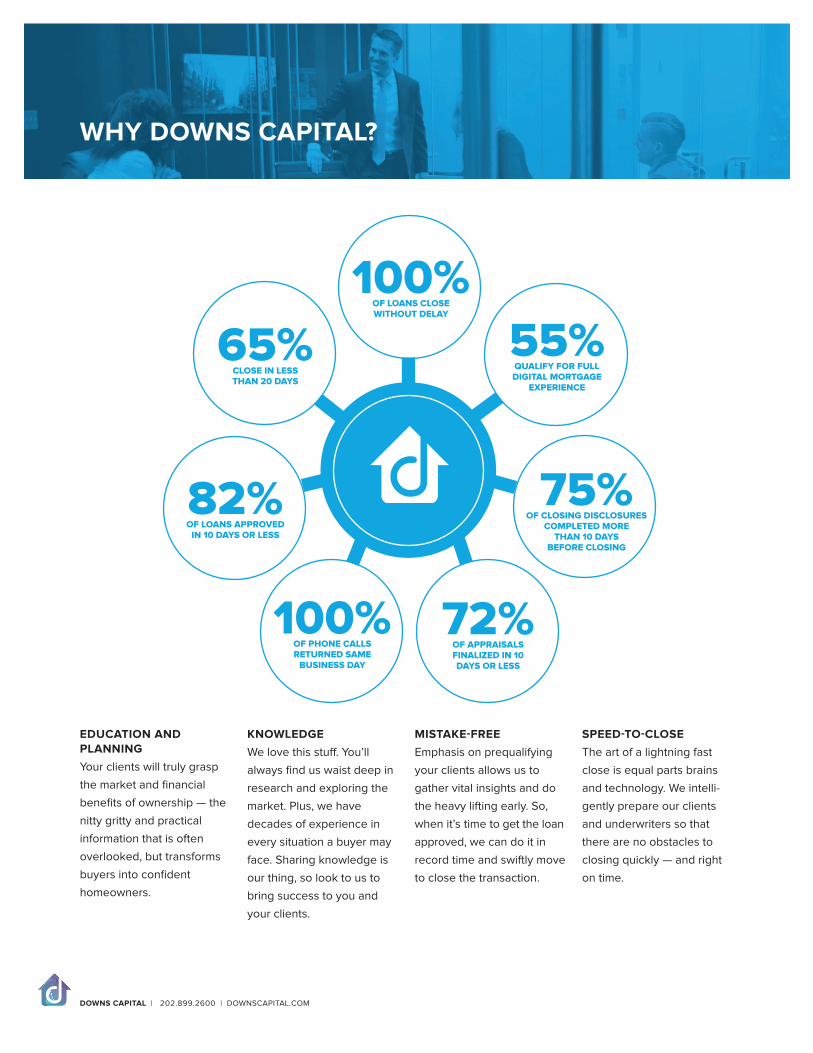

100%OF LOANS CLOSE WITHOUT DELAY

55%QUALIFY FOR FULL DIGITAL MORTGAGE

EXPERIENCE

65%CLOSE IN LESS THAN 20 DAYS

75%OF CLOSING DISCLOSURES

COMPLETED MORE THAN 10 DAYS

BEFORE CLOSING

72%OF APPRAISALS FINALIZED IN 10 DAYS OR LESS

82%OF LOANS APPROVED

IN 10 DAYS OR LESS

100%OF PHONE CALLS RETURNED SAME

BUSINESS DAY

DOWNS CAPITAL | 202.899.2600 | DOWNSCAPITAL.COM

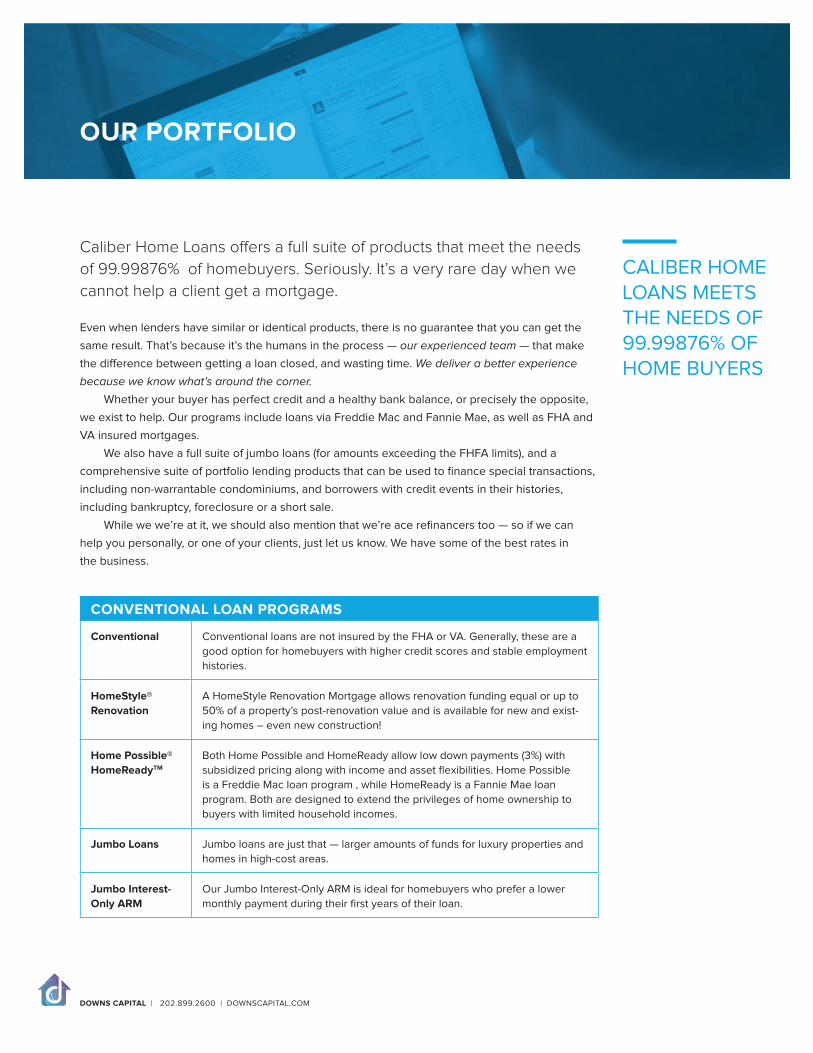

OUR PORTFOLIO

CONVENTIONAL LOAN PROGRAMS

Conventional Conventional loans are not insured by the FHA or VA. Generally, these are a

good option for homebuyers with higher credit scores and stable employment

histories.

HomeStyle®

Renovation

A HomeStyle Renovation Mortgage allows renovation funding equal or up to

50% of a property’s post-renovation value and is available for new and exist-

ing homes – even new construction!

Home Possible®

HomeReadyTM

Both Home Possible and HomeReady allow low down payments (3%) with

subsidized pricing along with income and asset fl exibilities. Home Possible

is a Freddie Mac loan program , while HomeReady is a Fannie Mae loan

program. Both are designed to extend the privileges of home ownership to

buyers with limited household incomes.

Jumbo Loans Jumbo loans are just that — larger amounts of funds for luxury properties and

homes in high-cost areas.

Jumbo Interest-

Only ARM

Our Jumbo Interest-Only ARM is ideal for homebuyers who prefer a lower

monthly payment during their fi rst years of their loan.

Caliber Home Loans o� ers a full suite of products that meet the needs

of 99.99876% of homebuyers. Seriously. It’s a very rare day when we

cannot help a client get a mortgage.

Even when lenders have similar or identical products, there is no guarantee that you can get the

same result. That’s because it’s the humans in the process — our experienced team — that make

the di� erence between getting a loan closed, and wasting time. We deliver a better experience

because we know what’s around the corner.

Whether your buyer has perfect credit and a healthy bank balance, or precisely the opposite,

we exist to help. Our programs include loans via Freddie Mac and Fannie Mae, as well as FHA and

VA insured mortgages.

We also have a full suite of jumbo loans (for amounts exceeding the FHFA limits), and a

comprehensive suite of portfolio lending products that can be used to fi nance special transactions,

including non-warrantable condominiums, and borrowers with credit events in their histories,

including bankruptcy, foreclosure or a short sale.

While we we’re at it, we should also mention that we’re ace refi nancers too — so if we can

help you personally, or one of your clients, just let us know. We have some of the best rates in

the business.

CALIBER HOME LOANS MEETS THE NEEDS OF 99.99876% OF HOME BUYERS

DOWNS CAPITAL | 202.899.2600 | DOWNSCAPITAL.COM

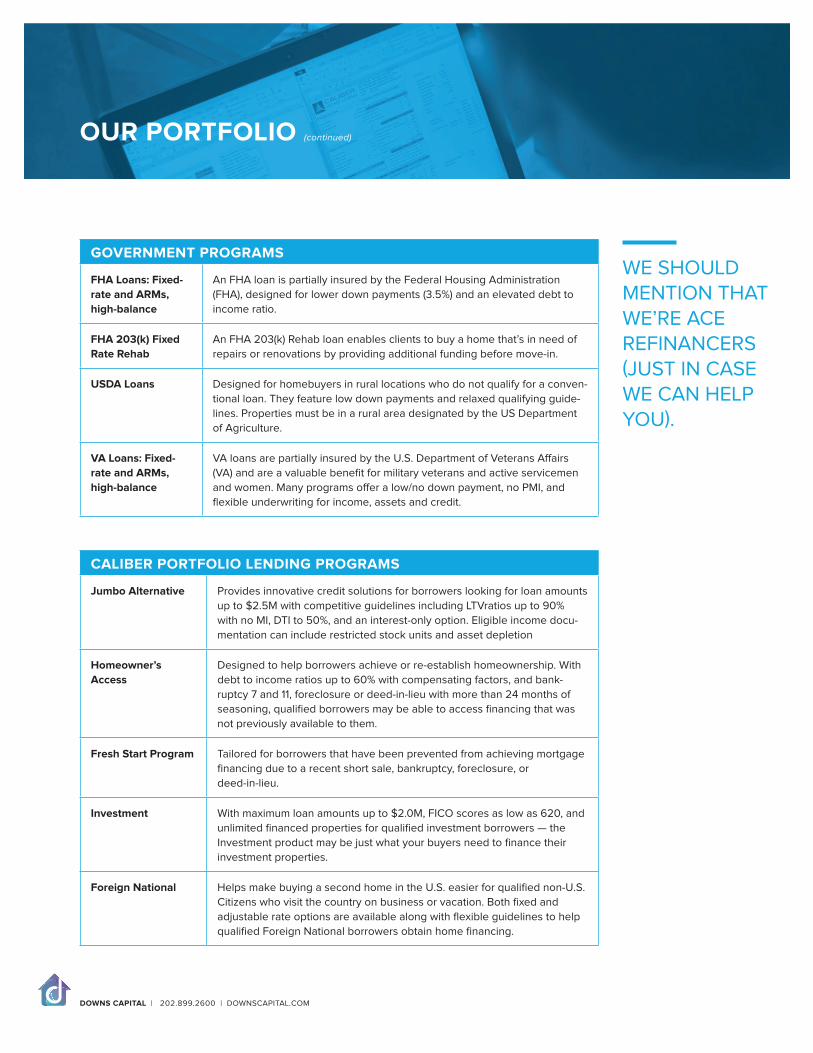

GOVERNMENT PROGRAMS

FHA Loans: Fixed-

rate and ARMs,

high-balance

An FHA loan is partially insured by the Federal Housing Administration

(FHA), designed for lower down payments (3.5%) and an elevated debt to

income ratio.

FHA 203(k) Fixed

Rate Rehab

An FHA 203(k) Rehab loan enables clients to buy a home that’s in need of

repairs or renovations by providing additional funding before move-in.

USDA Loans Designed for homebuyers in rural locations who do not qualify for a conven-

tional loan. They feature low down payments and relaxed qualifying guide-

lines. Properties must be in a rural area designated by the US Department

of Agriculture.

VA Loans: Fixed-

rate and ARMs,

high-balance

VA loans are partially insured by the U.S. Department of Veterans A� airs

(VA) and are a valuable benefi t for military veterans and active servicemen

and women. Many programs o� er a low/no down payment, no PMI, and

fl exible underwriting for income, assets and credit.

CALIBER PORTFOLIO LENDING PROGRAMS

Jumbo Alternative Provides innovative credit solutions for borrowers looking for loan amounts

up to $2.5M with competitive guidelines including LTVratios up to 90%

with no MI, DTI to 50%, and an interest-only option. Eligible income docu-

mentation can include restricted stock units and asset depletion

Homeowner’s

Access

Designed to help borrowers achieve or re-establish homeownership. With

debt to income ratios up to 60% with compensating factors, and bank-

ruptcy 7 and 11, foreclosure or deed-in-lieu with more than 24 months of

seasoning, qualifi ed borrowers may be able to access fi nancing that was

not previously available to them.

Fresh Start Program Tailored for borrowers that have been prevented from achieving mortgage

fi nancing due to a recent short sale, bankruptcy, foreclosure, or

deed-in-lieu.

Investment With maximum loan amounts up to $2.0M, FICO scores as low as 620, and

unlimited fi nanced properties for qualifi ed investment borrowers — the

Investment product may be just what your buyers need to fi nance their

investment properties.

Foreign National Helps make buying a second home in the U.S. easier for qualifi ed non-U.S.

Citizens who visit the country on business or vacation. Both fi xed and

adjustable rate options are available along with fl exible guidelines to help

qualifi ed Foreign National borrowers obtain home fi nancing.

OUR PORTFOLIO (continued)

WE SHOULD MENTION THAT WE’RE ACE REFINANCERS (JUST IN CASE WE CAN HELP YOU).

DOWNS CAPITAL | 202.899.2600 | DOWNSCAPITAL.COM

OUR PROCESS

People call on us for all sorts of reasons — great rates, our vast assort-

ment of loan programs, client service — but also because we fi x stressful

situations. For real estate agents who need a reliable partner in making

transactions happen, we o� er expertise, collaboration and lots and lots

of communication and insight.

CUSTOM CONSULTATION AND PROPOSALS

Our process begins with a thorough consultation, instead of an on-the-fl y rate check followed by a

breezy pre-approval letter that’s barely worth the paper it’s printed on.

Instead, we use the consultation and proposal process to identify the real factors that will infl uence

not just how your client will be fi nanced at an excellent rate, but how they’ll get through the trans-

action to a successful close. Our consultation isn’t just a recitation of rates and programs. We look

for issues and assets, and match our proposals to the client’s real needs and wants.

It’s the di� erence between buying a suit o� the rack or a custom-tailored suit. You might be able to

wear both suits, but the custom suit fi ts to perfection and makes you happy every time you look in

the mirror. When your client does accept our proposal, you can be confi dent it’s for a loan that will

actually close on schedule, because it’s based on reality.

LOVE EARLY

Ever wondered why it takes so long for lenders to do anything? There’s a reason for that: Other

lenders don’t give their loans any love until the last 10-14 days of the transaction. Even though the

application is in, at other lenders the application might gather dust for the fi rst 10 days after your

client goes under contract.

Here’s why: Lots of loan o� cers and processors play a waiting game. They stand by for

necessary documentation to roll in from your client and other entities involved in the transaction,

but aren’t proactive about the fi le itself. This lack of action can create pain and frustration down

the line.

It makes sense. If a loan application is untouched during the fi rst 6-10 business days of the

transaction, every problem will present itself late in the process, when it’s harder and more stress-

ful to resolve. If you’re on a tight close, the problems are exacerbated. That makes people cranky.

We hate that. So we just don’t do it that way.

IF YOU'RE ON A TIGHT CLOSE, YOU NEED LOVE EARLY SO YOU CAN CLOSE FAST.

DOWNS CAPITAL | 202.899.2600 | DOWNSCAPITAL.COM

START FAST, FINISH FAST

At Downs Capital, we’re fast because we start fast. The moment we accept an application and your

client is under contract, we begin the detective work to uncover any issues.

We look for anything in your client’s application that might impede the progress of a transac-

tion through underwriting to closing. Then we work with your client to creatively and quickly

resolve those issues right up front.

Our way enables us to resolve your clients’ issues early, when it’s really all about them and the

closing date isn’t in 24 hours. That makes it much faster to resolve any issues relating to the prop-

erty later, because your client’s fi le will be in a great position. For us, the fi rst 6-10 days of a loan is

our golden time — and it’s what makes our process unique.

FLEXIBLE WHERE IT COUNTS

Since we keep 98 percent of our loans, we can resolve issues that others simply can’t. Most lend-

ers will throw up all sorts of hurdles to getting things done (litigation, HOA delinquency, investor

concentration, industry overlays of self-promulgated lending rules, the sky is blue on Tuesday, etc.

etc. etc.).

At Caliber, we have the power to be fl exible because we’re lending our own money, on our

own terms. We don’t impose extra rules that make it harder to do business. For you, it means

smooth transactions and happy clients. For us, it’s standard operating procedure.

ETERNAL LOVE

There’s a reason 98 percent of our clients return: YOU.

That’s why we take our mission seriously when it comes to supporting your business.

Everything we do is designed to enhance your business as well as ours, from our e� orts to keep

you informed during the transaction, to the way we help clients keep tabs on their mortgage to

ensure they have the best rate possible.

Our job is create eternal love between Downs Capital, you and our joint client. That’s why

every step of our process is designed to deepen our relationship with our mutual client, and you.

The result? Plenty of new buyers for both of us, because happy clients share their experience

with others. That means an ever-growing sphere for both of us, and lots and lot of repeat business

for everyone. Not only can we not do this without you, we wouldn’t have it any other way.

OUR PROCESS (continued)

WE'RE LENDING OUR OWN MONEY, SO WE HAVE FLEXIBILITY WHEN OTHERS DO NOT.

DOWNS CAPITAL | 202.899.2600 | DOWNSCAPITAL.COM

Condominium Complications

CHALLENGE: When a client buys a condominium, underwriters can’t just approve the credit and

income of the borrower. They also have to approve the fi nancial profi le and stability of the building

itself and its homeowners’ association (HOA). Does it have enough reserves? Who owns the other

units? Homeowners or investors? Lenders have specifi c rules about condominium projects. You’ve

got to know them like the back of your hand, so a condominium purchase doesn’t fall out because

the underwriter doesn’t understand the composition of the building’s occupants, pending litigation,

governance or fi nancial position.

A CASE IN POINT: Downs Capital rescued a condominium buyer whose lender got tripped up in

their own rules. As is often the case, the other lender had a specifi c “overlay” rule that said that

only a certain percentage of the condominium project’s units could be owned by investors. What’s

more, there was pending litigation against the HOA along with excessive homeowner’s association

dues delinquency. On day 23 of a 30-day contract, the other lender dropped out, leaving the client

in the lurch, without fi nancing in place and earnest money on the line.

CALIBER DOESN’T BURDEN TRANSACTIONS WITH UNNECESSARY LENDER-SPECIFIC OVERLAYS.

OUR APPROACH: Immediately after taking our new client’s application, we set to work to under-

stand the ins and outs of this particular building and its homeowner association. Since Caliber

doesn’t burden transactions with unnecessary lender-specifi c overlays, we found that the investor

ownership percentage was a moot issue. And on further inspection of the HOA’s balance sheet,

we made the case that the building’s fi nances were sound, and the delinquency issues would be

solved via the sale of two units that were already in contract. We also assessed the litigation, and

found it to be a negligible risk given the fi nancial strength of the association.

THE TAKEAWAY: We signed o� on the condominium project within days of the application, and

closed the loan for our new customer within eight days. Our lesson: Dig deep and investigate when

the evidence is only circumstantial; the real situation is often di� erent.

SUCCESS STORIES

THE FACTS

Loan closed in eight

days after other lender

dropped out

Proved the building's

fi nances were sound,

when other lender

could not

Saved the client's

deposit and earnest

money, and earned a

client for life

DOWNS CAPITAL | 202.899.2600 | DOWNSCAPITAL.COM

SUCCESS STORIES

Mixed Use Mix Up?

CHALLENGE: For many buyers, living in a mixed-use building is an attractive option. These

projects are often in vibrant neighborhoods, and o� er great amenities to homeowners. But

they can be a headache for lenders that don’t understand the complexities that can arise

when a commercial entity exists within a residential complex.

A CASE IN POINT: Our borrower was relocating to the DC Metro area, and fell in love with a

condo in a mixed-use building just before Memorial Day. Her REALTOR suggested that she use

her company’s in-house lender. She went under contract, and just two days before the sched-

uled closing date, the in-house lender declined the loan.

The reason? The other lender determined that the condo was non-warrantable and swore

up and down that no lender would o� er fi nancing in the building. For our buyer, who was living

in a hotel, this was terrible news on top of horrifi c news, because her father had just been

placed in a hospice.

WHEN OTHER LENDERS WON’T OFFER FINANCING, WE DIG DEEP AND MOVE FAST.

OUR APPROACH: First and foremost, we put all hands on deck to help as soon as we got the

call and understood our new borrower’s stressful personal situation. We found that the original

lender had misinterpreted the impact of the commercial part of the building on our client’s

loan. All the residential condominiums in this project were warrantable.

All it took was a thorough review of the condominium’s legal documents, plat and plans,

and the building’s budget. We redefi ned the condo as being near a commercial space, not a

commercial space that had a condo within it. What’s more, we even the same conventional

Fannie Mae loan the other lender had told our client was impossible to get.

THE TAKEAWAY: We closed this loan in 14 days — including time o� for the Memorial Day

holiday. It worked because the only team we have is the “A” team. Between our underwriters,

appraiser network and deep understanding of mixed use projects, we pulled o� a fast close

thanks to a proven process and expertise that goes beyond standard loans.

THE FACTS

We can fi nance mixed-

use buildings

We got the very loan

for our client the other

lender said was impos-

sible to get

We closed in just 14

days, over Memorial

Day weekend

DOWNS CAPITAL | 202.899.2600 | DOWNSCAPITAL.COM

SUCCESS STORIES

Closing Costs Conundrum

CHALLENGE: Many buyers put together a down payment, but neglect to consider closing costs.

That’s a deal-killer. Not because the buyer might not have the money, but because most lenders

don’t let buyers know that even some conventional loans (in addition to government-backed loans)

can cover closing costs with a lender credit.

A CASE IN POINT: Our buyer had a great income and fi ve percent down, but little in the way of

401k or other reserves to cover closing costs. He was told by multiple lenders that he would need

to fi nd a seller willing to pay his closing costs. Even his REALTOR said he would have to use an

expensive FHA loan given his low down payment. That’s a tough row to hoe when the market is

tight. He was demoralized, because he didn’t know that with the right conventional loan and lender,

he could use a lender credit to cover closing costs.

NO IS NOT A WORD WE LIKE, AND WE ALMOST NEVER HAVE TO USE IT.

OUR APPROACH: Once we assessed the situation, we explained to our buyer that he was actu-

ally in great shape to buy with a fi ve percent down, conventional loan with a three percent lender

credit from Caliber. With this newfound confi dence, our buyer wrote a contract and closed within

30 days.

THE TAKEAWAY: No is not a word we like — and we almost never have to use it. If you run into a

buyer who has saved up a down payment but is stymied by closing costs, talk to us. With a vast

assortment of loan programs that can serve virtually any buyer, we can help anyone who is quali-

fi ed get creative to buy even in hot markets.

THE FACTS

Lender credits can

cover closing costs,

even on conventional

loans

Many buyers don’t

need as much cash as

they think they do

We built our client’s

confi dence, and closed

in 30 days

DOWNS CAPITAL | 202.899.2600 | DOWNSCAPITAL.COM

SUCCESS STORIES

VA Loans: If It’s a Yes, It’s a Yes

CHALLENGE: Veterans have earned the right to get a VA loan by serving their country. Yet many

agents are unaware of the VA loan process, and incorrectly steer veterans away from using their

hard-won benefi t. We’re out to change this, because VA loans are one of the safest and best loan

programs available.

A CASE IN POINT: Our borrower was an unmarried veteran who wanted to buy a condo in DC

with his signifi cant other. But because they weren’t married, his partner’s income could not be

counted in the loan application. That made his debt-to-income ratio 62 percent, which may be why

a dozen other lenders turned him down, and he was just about to give up and sign another year-

long lease. Other lenders wanted to push him into an expensive conventional loan with a minimum

of three percent down, with a hefty dose of PMI. All of that made the loan una� ordable, because it

added $320 a month to the payment.

IF THE VA ALLOWS IT, CALIBER WILL DO IT.

OUR APPROACH: Caliber’s philosophy is simple: If the VA allows it, we will do it. In practice, this

meant that we were able to make the loan because the VA would provide the insurance, and

Caliber would not overlay lender-specifi c rules specifi cally designed to protect us and thwart

borrowers and restrict credit. Besides, we realized our borrower had enough residual income to

warrant a higher debt-to-income ratio, so he qualifi ed on his own.

THE TAKEAWAY: When you hear the word “overlay,” it’s almost always a euphemism for a lend-

er-specifi c rule that is more restrictive than those of the Veteran’s Administration, FHA, Fannie Mae

or Freddie Mac.

Yet Caliber has a saying: If the agency allows it, we allow it. We don’t believe in making the

rules any harder than they must be by adding our own overlays.

Often, lender overlays are about selling the loan later to investors, and have little to do with

whether a borrower actually qualifi es according to the agency’s rules. Because we don’t add

unnecessary complexity and stick fi rmly to the agency’s rules, borrowers can often borrow more

with us than they can elsewhere, without compromising their fi nancial stability.

THE FACTS

Caliber doesn’t make it

harder by using lender

overlays

Every veteran has the

right to use this hard-

won benefi t

VA loans are one of the

safest and best loans

available

DOWNS CAPITAL | 202.899.2600 | DOWNSCAPITAL.COM

SUCCESS STORIES

Low on Cash

CHALLENGE: Too many fi rst-time buyers think they need a massive down payment to buy a home.

It’s a confi dence (and education) problem we can fi x.

A CASE IN POINT: Our buyers had been looking for eight months, and had $120,000 to put down.

But because another lender told them that they needed a full 20 percent (or $140,000) to buy a

$700,000 home, and were pitching their parents to chip in another $20,000. Their search for a

home was stuck in the rut of “we can’t do this.”

MANY BUYERS JUST DON’T KNOW WHAT THEY DON’T KNOW.

OUR APPROACH: Once we had the opportunity to talk to this couple, we realized that their cash

position and good incomes could actually qualify them for a $900,000 home without compromising

their fi nancial stability. It was a matter of educating them on their fi nancing options, to unlock the

possibilities in their home search. In the end, they bought a home for $725,000, put 10 percent

down, and had $55,000 left over to invest in other areas of their life.

THE TAKEAWAY: Since most people don’t buy a home every day, they’re not mortgage experts.

They simply don’t know what they don’t know about mortgages. Sometimes they even have

preconceived notions of how mortgages work that don’t square with reality, or what’s specifi cally

available to them. When you refer a client to us, we ensure that they understand the best options

available to them — even ones they didn’t know existed. Consider us matchmakers.

THE FACTS

First-time buyers don’t

necessarily need a

massive down payment

Our process educates

buyers and builds

confi dence

“We can’t do this” is

often a misconception

based on fear

DOWNS CAPITAL | 202.899.2600 | DOWNSCAPITAL.COM

SUCCESS STORIES

Banged up Credit

CHALLENGE: Not all borrowers have pristine credit, but many will still qualify for a mortgage.

We help borrowers understand their options, and enable them to get into a home.

CASE IN POINT: Our borrower had a credit score below 580, and felt that homeownership was

simply out of reach. But the biggest problem was not her credit score; it was her morale and a lack

of education about what actions she could take to improve her score.

NOT EVERYONE HAS PRISTINE CREDIT, BUT EVERYONE SHOULD KNOW WHAT THEY CAN DO WITH THEIR CREDIT.

OUR APPROACH: We immediately knew that a few months of credit-healing activities could help

our borrower push her score above 580 — which is the entry point for an FHA loan with no upfront

fees. All she needed to know was what to do, like paying down credit cards, clearing parking tick-

ets and phone bills. But our work wasn’t done; we stayed with this client to continue to improve her

score, with an eye towards refi nancing in the future, or trading up to a bigger home.

THE TAKEAWAY: Low or poor credit isn’t an insurmountable barrier to homeownership. When

we’re working with a borrower with banged-up credit, our fi rst objective is to help them understand

what they can do to improve their credit. Even if it takes several months, most borrowers can be

helped.

THE FACTS

Credit-healing activi-

ties can push scores up

in a matter of months

Many of Caliber’s

programs cater to

low-credit borrowers

Most borrowers, even

those with scores

down to 580, can be

helped

DOWNS CAPITAL | 202.899.2600 | DOWNSCAPITAL.COM

SUCCESS STORIES

Unsnarling Complicated Finances

CHALLENGE: Self-employed individuals often have complex incomes, from multiple entities.

Incomes can vary from year to year, and write-o� s can make their incomes look smaller than reality.

We specialize in helping self-employed borrowers untangle their fi nances so that underwriters can

clearly understand their income, assets and expenses.

A CASE IN POINT: Our borrower was a successful real estate investor, who owned, in whole or

in part, 198 buildings in the United States. Though his income appeared as a net loss on his tax

returns (and he hadn’t paid income taxes for two consecutive years thanks to depreciation and

carry-forward losses on his buildings), in reality he had more than enough income and assets to

qualify for a $2.7 million second home, with 20 percent down.

WE HELP UNDERWRITERS UNDERSTAND EVEN THE MOST COMPLEX SELF-EMPLOYED INCOMES.

OUR APPROACH: We combed through more than 3,000 pages of documentation and partnership

returns to reveal the truth of his situation to our underwriters. Then we structured his income so

that underwriters could understand it. We included his capital gains, interest income and hidden

depreciation, and removed carry-forward losses to paint a clear picture of his income, assets and

expenses.

THE TAKEAWAY: You don’t have to be Donald Trump to utilize complex strategies and business

structures to limit your tax exposure. Virtually all self-employed borrowers have a tax strategy to

reduce their taxable earnings. But these strategies often don’t illuminate their actual monthly

income, which may include other streams of revenue that are not clearly delineated on their tax

returns. We know how to ethically interpret these strategies so that underwriters can understand

how our self-employed borrowers really make money, so they can get a competitive mortgage

that is comparable to our W-2 borrowers.

THE FACTS

We combed through

3,000 pages of docu-

mentation to show how

this borrower really

made money

Every self-employed

individual uses tax

strategies that appear

to reduce income

Capital gains, interest

income and deprecia-

tion can often be used

to strengthen an

application

DOWNS CAPITAL | 202.899.2600 | DOWNSCAPITAL.COM

SUCCESS STORIES

Stronger Contracts on Tight Timelines

CHALLENGE: Contracts are like snowfl akes. They consist of a unique borrower, property, listing

agent and buyer’s agent. And they’re written in one moment of time — meaning that the market

can be hot, slow or somewhere in between. For buyer agents, this can make writing the strongest

contract challenging, because what works in one transaction might not work in another.

A CASE IN POINT: Our borrower wanted to write in a hot market on a condominium that would

clearly attract multiple o� ers, and the seller wanted a fast close. But our exceptionally qualifi ed

borrower was also rightly cautious — about paying too much, waiving contingencies, or taking

unnecessary risks. But she still wanted to win the deal. We knew we had to act fast, and limit our

borrower’s exposure to risk. But we also had to make the contract as attractive as possible to the

seller, who wanted our borrower waive her fi nancing contingency and the appraisal.

WE CAN HELP REMOVE CONTINGENCIES WITHOUT COMPROMISING BUYER SAFETY.

OUR APPROACH: When time is tight and the pressure is on, we use the calendar and the process

itself to help. Since this contract would be written on a Thursday, we knew that it would be ratifi ed

on a Friday. That meant the condominium packet would likely be handed over to our borrower on

Monday.

In turn, we would have three full business days the following week to complete her loan and

appraisal — just before the condo document package review expiration date. That allowed us to

remove her contingencies to write the strongest contract, without putting our borrower’s welfare

at risk. We knew that she could withdraw during the three-day review period if necessary. But she

didn’t have to. We threw everything in our arsenal (time, people, relationships and expertise) at this

transaction to get it done. And our borrower got her new home.

THE TAKEAWAY: Reputation counts. In this case, both the buyer and listing agent knew that we

could deliver on our promise to close the loan in eight days, without compromising the contract or

the safety of our borrower. Our business is built on relationships — between our agent partners,

our borrowers and our internal team at Caliber. We work hard because we know what’s at stake …

and we know how to get things done, even when time is tight.

THE FACTS

Timing is often a huge

factor in safely remov-

ing contingencies

The lender’s reputation

is an asset in a compet-

itive multiple-o� er

scenario

Our relationships made

this eight-day close

happen

DOWNS CAPITAL | 202.899.2600 | DOWNSCAPITAL.COM

OUR TEAM

John DownsMANAGING PARTNER

John is the architect and founder of Downs Capital. He’s not content to be a top

mortgage broker (which he is) — he wants to reinvent the process of getting a

mortgage.

John wants the lending process itself to illuminate a path to fi nancial inde-

pendence for his clients. That’s why he helps people become fi nancially literate

so that they can make intelligent fi nancial decisions.

John’s motto is wealth for the next generation. Whether you count yourself

as part of the next generation, or are ready to build the next level of wealth for

yourself, John thinks everyone deserves a great fi nancial foundation. John will

tell anyone who will listen that a mortgage is an instrument of leverage — and

that a mortgage allows you to use someone else’s cash to build your own

wealth.

Today, Downs Capital is a thriving unit of Caliber Home Loans. John’s team

is comprised of mortgage experts who also happen to be fi erce competitors,

client advocates and winners.

NMLS: 476406 CHL: 15622 States Licensed: DC/MD/VA

� 1327 14th St NW #101, Washington, DC 20005

� 185 Admiral Cochrane Dr, Ste 205, Annapolis, MD 21401

Phone: 202.899.2603

Email: [email protected]

DOWNS CAPITAL | 202.899.2600 | DOWNSCAPITAL.COM

Rob DownsMORTGAGE ADVISOR

Imagine this: your younger brother insists that the best business in the world is

the mortgage business. But you don’t believe him. Why would you? He’s just

your brother, after all.

Instead, you go o� and build an award-winning career in advertising,

managing projects for the likes of Coca Cola, GE, Mercedes-AMG and other

blue chip brands at top agencies after serving in the U.S. Navy.

Yet John keeps at it. “Help people,” he says over multiple family dinners.

“Make a di� erence,” he exclaims on New Year’s Day. “Have you ever thought

about the mortgage business?” he asks over hamburgers on July 4.

Then one day, you realize that he’s telling the truth — mortgages can really

help people build wealth. That fi ts with your world view. You actually do want to

help people, and the mortgage business really is the best business in the world.

So if you’re Rob Downs, you join Downs Capital as a loan advisor. You help

people understand the process of buying a home, so they can buy with confi -

dence and build wealth.

NMLS: 1480437 CHL: 15622 States Licensed: GA/DC/MD/VA/DE

� 437 Memorial Dr, SE Suite 2-A, Atlanta, GA 30312

� 1327 14th St NW #101, Washington, DC 20005

Phone: 202.899.2610

Mobile: 404.202.4735

Fax: 844.833.0540

Email: [email protected]

OUR TEAM

DOWNS CAPITAL | 202.899.2600 | DOWNSCAPITAL.COM

OUR TEAM

Louis BermanMORTGAGE LOAN ORIGINATOR

If you’re a linebacker who’s also on the honor roll at the University of Maryland,

doesn’t it seem like a natural path to go into the mortgage business after you

graduate? Of course it does … if you’re Louis Berman. That’s because teaching,

coaching and problem solving are inherent in the way Louis works with clients.

He is curious and capable, an unbeatable combination in matching clients to the

right loan programs that will help them build a sound fi nancial future.

Louis views every new client as a friend — and friends don’t let friends get

mortgages that aren’t right for them. That’s one reason Louis has little spare

time. But in his rare of hours, you can fi nd Louis working out and coaching acro-

batics and elite level stunting for cheerleaders (many of whom have been

accepted into Division One schools).

NMLS: 1403177 CHL: 15622 States Licensed: DC/MD/VA

� 1327 14th St NW #101, Washington, DC 20005

� 185 Admiral Cochrane Dr, Ste 205, Annapolis, MD 21401

Phone: 202.899.2606

Email: [email protected]

DOWNS CAPITAL | 202.899.2600 | DOWNSCAPITAL.COM

OUR TEAM

Regis WhittingtonMORTGAGE SPECIALIST

When you’re recruited by Villanova, Georgetown, Princeton, Temple and

Lafayette to play wide receiver, it’s pretty clear you have a competitive spirit and

the discipline to succeed. For Regis Whittington, it also meant a full athletic

scholarship to the University of Maryland College Park, and a major in family

and consumer sciences. He is a true team player, dedicated to the success of

his colleagues and clients.

Regis has always been passionate about helping people achieve their

goals, albeit life, fi nancial or athletic. His mission is to help as many people as

possible, which is why you’re as likely to fi nd him studying the latest market

trends and Fed actions as you are at the gym (where you might just get a lesson

in leverage, as well as a workout).

NMLS: 1185436 CHL: 15622 States Licensed: DC/MD/VA

� 1327 14th St NW #101, Washington, DC 20005

� 185 Admiral Cochrane Dr, Ste 205, Annapolis, MD 21401

Phone: 202.899.2605

Email: [email protected]

DOWNS CAPITAL | 202.899.2600 | DOWNSCAPITAL.COM

OUR TEAM

Victoria WilkersonPRODUCTION MANAGER

Like most people who are both expert and modest, Victoria Wilkerson prefers to

let her work speak for itself. She is preternaturally calm even when the pressure

is on, and that’s probably because she spent 14 years at a high-pressure law

fi rm before joining Downs Capital. Around the o� ce, she is the fi rst person

everyone turns to for a smile, an answer, and when called for, a particularly

funny joke. She is also the master of every detail, and keeps Downs Capital

running on schedule.

In her spare time, Victoria is devoted to her family and community service

(although she doesn’t particularly enjoy talking about her work with the home-

less through her church and other groups). She’s known John since childhood,

which may explain why she majored in psychology at Towson University (or so

she says). She is an excellent cook, experienced traveler, curious reader of all

things interesting, and enjoys spending time with her little dog, Emma.

NMLS: 1389742 CHL: 15622 States Licensed: DC/MD/VA

� 1327 14th St NW #101, Washington, DC 20005

� 185 Admiral Cochrane Dr, Ste 205, Annapolis, MD 21401

Phone: 410.216.3506

Fax: 844.672.6186

Email: [email protected]

DOWNS CAPITAL | 202.899.2600 | DOWNSCAPITAL.COM

OUR TEAM

Charlie HallMORTGAGE ADVISOR

Passionate and unequivocally committed to his clients, Charlie is a mortgage

veteran with more than 12 years of experience in virtually every role in our busi-

ness. No matter the situation, Charlie believes that everyone can and should

have just the right mortgage that will help them build wealth over the long term

(and it’s a serious bonus if he can save them a little money in the short term).

Every day, he uses his in-depth knowledge of the mortgage process to ensure

his clients get the best mortgage possible to fi t their fi nancial and life goals.

If there’s a central theme in Charlie’s life, it’s simply that he believes in

doing right, all the time, whether you’re buying your fi rst or your fi fth home.

When he’s not putting together the ideal loan for each of his clients, Charlie

serves as the CFO at his own digital comic book production studio. Charlie lives

in Annapolis with his wife and his super-smart dog, Ginger.

NMLS: 187257 CHL: 15622 States Licensed: DC/MD/VA

� 185 Admiral Cochrane Dr, Ste 205, Annapolis, MD 21401

Phone: 410.216.3508

Mobile: 410.703.5425

Fax: 844.929.9670

Email: [email protected]

DOWNS CAPITAL | 202.899.2600 | DOWNSCAPITAL.COM

OUR TEAM

Joshua J. DavidMORTGAGE ADVISOR

For most people, completing a Tough Mudder race (wherein you crawl under

barbed wire in a mud patch and over various thorny, blood-drawing obstacles)

would be a once in a lifetime event. But for Joshua David, with two mudders

under his belt, it’s obviously a habit to overcome giant hurdles. After working his

way through college so he could graduate without any debt, and entering the

mortgage industry, Joshua has proven over and over again that any goal can be

achieved as long as you have a plan.

Since no two clients or loans are alike, Josh never makes assumptions and

always takes care to educate his clients about every available option. It’s all part

of achieving the goal: happy and secure clients. In his o� hours, Josh plays

volleyball, golf and soccer, and throws the ball for his rescued Black Lab, Bubs.

Josh holds a bachelor of science in fi nance from the University of Maryland,

College Park.

NMLS: 885983 CHL: 15622 States Licensed: DC/MD/VA/DE

� 1327 14th St NW #101, Washington, DC 20005

� 185 Admiral Cochrane Dr, Ste 205, Annapolis, MD 21401

Phone: 410.216.3505

Mobile: 410.458.4291

Fax: 855.473.2917

Email: [email protected]

DOWNS CAPITAL | 202.899.2600 | DOWNSCAPITAL.COM

OUR TEAM

Sean HanleyLOAN COORDINATOR

The unsung hero in our business is the loan processor — the person who helps

clients prepare loan application packages. The truth is, it’s a bit of a marathon to

assemble the right details in the most expeditious fashion. Maybe it’s because

Sean Hanley really is a marathoner and youth sports coach that every loan

application he touches moves with grace and speed. Sean assembles loan

packages the way he runs his marathons, with just the right amount of prepara-

tion, a thorough understanding of the course, and an absolute commitment to

successfully crossing the fi nish line.

Sean holds and bachelor of science in economics from the University of

Maryland, and lives in Crofton, where he can usually be found rooting for the

Redskins or Nationals, or his beloved Terrapins.

� 1327 14th St NW #101, Washington, DC 20005

Phone: 410.216.3507

Fax: 844.964.7601

Email: [email protected]