Pag : 1

Sergio BaezaChairman of the Board of SCOMP S.A.May 2010

Reducing the transaction costs of retirement annuities in Chile

Pag : 2

Agenda

Conditions prior to the reform1

Goals of the reform 2

Organizational setup3Results4

Pag : 3

1. Conditions prior to the reform1. Conditions prior to the reform

Assimetrical information between affiliates and sales agents leading to overweight of agents in the pension decision and choice of annuity company

High sales commissions to the detriment of pensions giving agents the resources to financially influence the individual’s choice of annuity company

Pag : 4

1. Conditions prior to the reform1. Conditions prior to the reform

Agents only earned commissions paid by annuity companies having no incentive to present their clients with the option of installment withdrawals from the pension company

Therefore little competition between these two options of retirement

Pag : 5

2. Goals of the reform2. Goals of the reform

Provide CLEAR and COMPARABLE information of the two basic retirement options, annuities and installment withdrawals

REDUCTION OF COMMISSIONS puting a ceiling to them at 2.5%

Pag : 6

2. Goals of the reform2. Goals of the reform

INCREASE PRICE COMPETITION through a simultaneous biding process

EMPHASIZE SOLVENCY by demanding a claims payment rating no less than BBB

PREVENT PAYMENTS FOR RETIREE INFORMATION by the official disclosure of data on candidates for retirement

Pag : 7

3. Organizational setup 3. Organizational setup

By Law in 2004 pension and life insurance company were required to put in place a system to provide information to affiliates on the values of the different pension options

Similarly affiliates were mandated to make inquiries through this system as a requisite for retirement

Thus a corporation was set up, SCOMP S.A., to provide this information system; its owners are the pension companies 50% and the life annuity companies 50%

Pag : 8

3. Organizational setup3. Organizational setup

Access to SCOMP is given to the Pension Companies, the Life Annuity Companies and the Pension Advisors

The system is under the surveillance of both the pension and the annuity regulators

To develop and operate the information system SCOMP hires a systems provider through an open biding process

SCOMP finances itself by charging a fee for each information request and for each closing of a pension decision

Pag : 9

3. Organizatioal setup - retirement options3. Organizatioal setup - retirement options

At retirement affiliates have to choose between different pension options:

Installement withdrawals from the retirement account

Immediate Life Annuity with or without guaranteed term

Installment withdrawals plus deferred annuity

Immediate Annuity plus Installment Withdrawals

Pag : 10

3. Organizational setup - process3. Organizational setup - process

The most relevant processes in the system are:

Issue of Balance Certificate

Request for Pension Offers

Issue of Pension Offers Certificate

Selection of Pension Option

Pag : 11

3. Organizational setup - process3. Organizational setup - process

Pension Company

SCOMP

Affiliate/Beneficiaries

Pension Application

Issues Balance Certificate:- Personal data - Beneficiaries data- BalanceValid for 35 days

SCOMPBalance Certificate

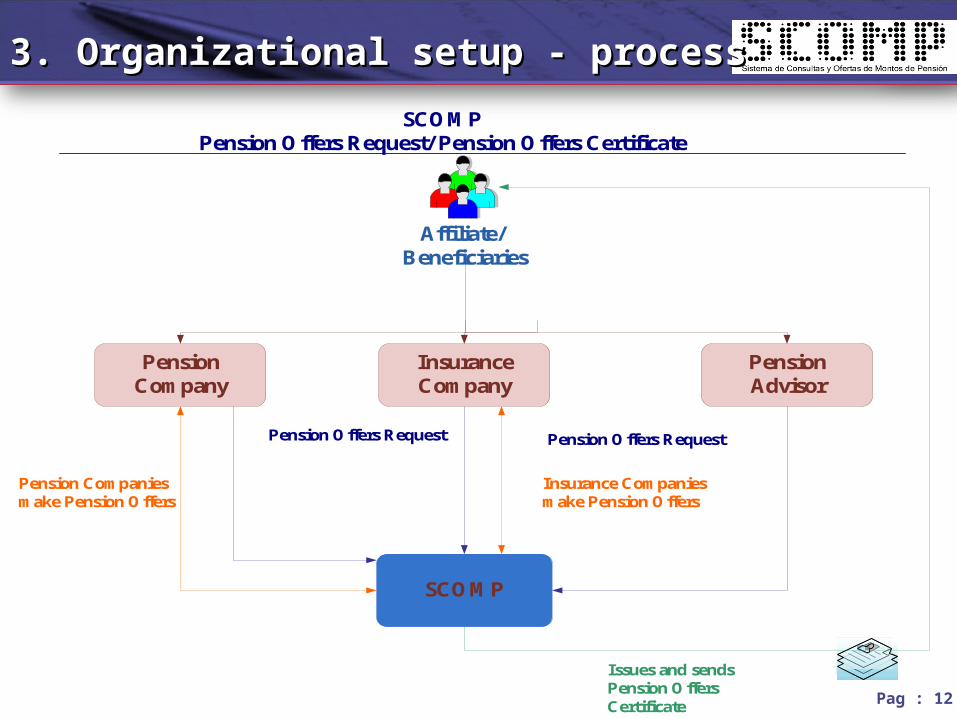

Pag : 12

3. Organizational setup - process3. Organizational setup - process

PensionCompany

SCOMP

Affiliate/Beneficiaries

Pension Offers Request

SCOMPPension Offers Request/ Pension Offers Certificate

PensionAdvisor

InsuranceCompany

Pension Offers Request

Pension Companiesmake Pension Offers

Insurance Companies make Pension Offers

Issues and sends Pension Offers Certificate

Pag : 13

3. Organizational setup - process3. Organizational setup - process

PensionCompany

Affiliate/Beneficiaries

SCOMPClosing

InsuranceCompany

Pension Company transfers balance of indivitual account

Decision making :· Accept offer· Request additonal life

insurance offers · Postpones pension

Selects Pension Option

Affiliate/Beneficiaries

SCOMP

Pension Company informs closing

Pag : 14

4. Results4. Results

Increase in price competition

Decrease in Agent’s Commisision with the corresponding increase in pensions

Affiliates easily have all relevant information to benefit from good pension advice to make a right choice of pension mode and carrier

The official disclosure of retiree candidates has added transparency to the marketing of pension offers

Pag : 15

4. Results – lower commissions 4. Results – lower commissions

Source: SVSSource: SVS

Agent́ s Commissions

3,40%3,62%

3,47%

4,67%4,66%

5,58%5,45%

5,84%5,91%

3,89%

2,67%2,68%2,47%

2,13%2,13%2,19%2,05%

1,47%

5,33%

0,00%

1,00%

2,00%

3,00%

4,00%

5,00%

6,00%

7,00%

1991 1992 1993 1994 19951996 1997 1998 1999 20002001 2002 2003 20042005 2006 2007 2008 2009

SCOMPstarts

Pag : 16

4. Results – Pension Offers Requests 4. Results – Pension Offers Requests

Number of Pension Offers Requests january/ 2005-december/ 2009

Pension Advisor 75.712Pension Company 80.425Insurance Company 60.176Total 216.313

Number of Pension Offers Requests(january/ 2005-december/ 2009)

Pension Company

37%

Insurance Company

28%

Pension Advisor35%

Pag : 17

4. Results - Closings 4. Results - Closings

Number of Closings(january/ 2005-december/ 2009)

86.461 64%

49.61336%

Pension CompanyInsurance Company

Pag : 18

4. Results - Capitals transacted 4. Results - Capitals transacted

Closings Capital 2009 (million US$)

915 36%

1.637 64% Pension Company

Insurance Company

Pag : 19

4. Results – Savings on commissions4. Results – Savings on commissions

Average commission before SCOMP: 4,40% Average commission before SCOMP: 4,40% ( 1991 - 2003)( 1991 - 2003)

Average commission since inception of Average commission since inception of SCOMP: 2,07% SCOMP: 2,07% ( 2004 - 2009)( 2004 - 2009)

Lower commissions of 2,33% on average Lower commissions of 2,33% on average On Capitals of US$ 1.760 million per year on On Capitals of US$ 1.760 million per year on average Represent savings of average Represent savings of US$ 41 million US$ 41 million per year per year

Pag : 20

4. Results – Service fees4. Results – Service fees

Fee concept Paid by Amount in US$

Fixed per request Advisor or provider 2

Fixed per closing Provider 7

Variable per closing Provider 26

Total 35

Pag : 21

4. Results - Balance Sheet4. Results - Balance Sheet

ASSETS: Dec-2008 Dec-2009 LIABILITIES: Dec-2008 Dec-2009

Cash and cash equivalents 9 47 Accounts payables 153 165 Securities 534 538 Allowances 69 81 Accounts receivables 207 299 Anticipated income 42 42 Tax receivable 73 12 Anticipated expenses 13 11 Total current liabilities 264 288 Deferred taxes 10 9

Total current assets 846 916 EQUITY:

Paid in capital 494 482 Computer equipment - 1 Retained earnings 35 86

Net income 113 61 Interim dividend (60) -

Total equity 582 629

TOTAL ASSETS 846 917 TOTAL LIABILITIES 846 917

SCOMP S.A.Balance Statements (thUS$)

Pag : 22

4. Results - Profit and Loss 4. Results - Profit and Loss

Operational revenue 834 893 Operational expense (479) (624)

Operational margin 355 269

General and administrative expenses (220) (227)

Operational profit 135 42

Other income net (1) 29

Profit before income tax 134 71

Income tax (21) (10)

Net income 113 61

SCOMP S.A.

Profit and Loss Statements (thUS$)

31/12/2008 31/12/2009

Pag : 23

CONCLUSIONSCONCLUSIONS

• SCOMP produces commission savings of US$ 41 million per year which divided into 17 thousand annuity closings per year represent savings of US$ 2.400 per closing

• This is achieved with a low initial investment in systems development of US$ 500 thousand

• The operational cost is very moderate, some US$ 35 per closing

• Efficiency per closing is great : spending US$ 35 to produce savings of US$ 2.400.