OCTOBER 26–29, 2020

Session 10B: AIT Research on Artificial Intelligence

October 29, 2020

SOCIETY OF ACTUARIESAntitrust Compliance Guidelines

Active participation in the Society of Actuaries is an important aspect of membership. While the positive contributions of professional societies and associations are well-recognized and encouraged, association activities are vulnerable to close antitrust scrutiny. By their very nature, associations bring together industry competitors and other market participants.

The United States antitrust laws aim to protect consumers by preserving the free economy and prohibiting anti-competitive business practices; they promote competition. There are both state and federal antitrust laws, although state antitrust laws closely follow federal law. The Sherman Act, is the primary U.S. antitrust law pertaining to association activities. The Sherman Act prohibits every contract, combination or conspiracy that places an unreasonable restraint on trade. There are, however, some activities that are illegal under all circumstances, such as price fixing, market allocation and collusive bidding.

There is no safe harbor under the antitrust law for professional association activities. Therefore, association meeting participants should refrain from discussing any activity that could potentially be construed as having an anti-competitive effect. Discussions relating to product or service pricing, market allocations, membership restrictions, product standardization or other conditions on trade could arguably be perceived as a restraint on trade and may expose the SOA and its members to antitrust enforcement procedures.

While participating in all SOA in person meetings, webinars, teleconferences or side discussions, you should avoid discussing competitively sensitive information with competitors and follow these guidelines:

• Do not discuss prices for services or products or anything else that might affect prices

• Do not discuss what you or other entities plan to do in a particular geographic or product markets or with particular customers.

• Do not speak on behalf of the SOA or any of its committees unless specifically authorized to do so.

• Do leave a meeting where any anticompetitive pricing or market allocation discussion occurs.

• Do alert SOA staff and/or legal counsel to any concerning discussions

• Do consult with legal counsel before raising any matter or making a statement that may involve competitively sensitive information.

Adherence to these guidelines involves not only avoidance of antitrust violations, but avoidance of behavior which might be so construed. These guidelines only provide an overview of prohibited activities. SOA legal counsel reviews meeting agenda and materials as deemed appropriate and any discussion that departs from the formal agenda should be scrutinized carefully. Antitrust compliance is everyone’s responsibility; however, please seek legal counsel if you have any questions or concerns.

Presentation Disclaimer

Presentations are intended for educational purposes only and do not replace independent professional judgment. Statements of fact and opinions expressed are those of the participants individually and, unless expressly stated to the contrary, are not the opinion or position of the Society of Actuaries, its cosponsors or its committees. The Society of Actuaries does not endorse or approve, and assumes no responsibility for, the content, accuracy or completeness of the information presented. Attendees should note that the sessions are audio-recorded and may be published in various media, including print, audio and video formats without further notice.

AIT Research on Artificial IntelligenceAgenda:• Introductions• Application in Time Series Predictions • Emerging techniques for Mortality modeling, claim modeling, and fraud detection • Applications in underwriting process, claim process and product comparison • Q&A

Blake Hill FSA FCIA, VP Insurance, dacadoo

Blake is leading insurers into the digital age with dacadoo! Blake has developed and launched insurance, savings, investment, and group health products, and through his leadership launching the Vitality program in Canada he implemented partner integrations and the use of advanced analytics in marketing and customer engagement. Blake is now supporting insurance companies globally as they transformation into customer centric and digitally enabled businesses using the dacadoo Health Risk Quantification and dacadoo Digital Health Engagement platform.

Victoria Zhang, FSA FCIA, Associate Director, Sun Life

Victoria Zhang, Associate Director at Sun Life, is a passionate research actuary for the SOA. Her research interest expands from Machine Learning applications in actuarial field, actuarial modeling, to stochastic modeling.

Marie-Claire Koissi-Kouassi , PhD

Marie-Claire Koissi is a Professor of Mathematics, faculty with the Actuarial Sciences Program at the University of Wisconsin – EC. Her research areas include stochastic mortality modelling and forecasting, risk management, and fuzzy logic application to insurance.

Dihui Lai, PhD, ASA, Lead Data Scientist, RGA

Dihui Lai is a Lead Data Scientist in RGA. In this role, Dihui uses machine learning and predictive modeling for various insurance applications, including artificial intelligence (AI)-augmented underwriting, predictive model-based pricing, and lapse experience studies. He has experience in quantitative modeling, nature language processing and document image processing.

Victoria Zhang, FSA FCIAAssociate Director, Sun Life

A Tour of AI Technologies

in Time Series Prediction

Victoria Zhang, FSA, FCIA

October 29th, 2020

Introduction of AI

What is AI - AI is the techniques that enable

computers to mimic human intelligence It has been used in many fields including speech recognition, self-

driving cars and language translation.

What is Machine Learning - ML is a subset of AI

where a computer system is trained with a large

amount of data to learn how to carry out a specific task.

What is Deep Learning - Deep learning is a

subset of machine learning. It applies neural network which tries to replicate the human brains’ approach to analyzing data.

Acerous or Non-Acerous?

?

What can we benefit from AI as an actuary Strong representability

Better Accuracy

Fast Adaptability

Today’s Agenda:

Victoria – Application in Time Series Predictions

Marie-Claire – Emerging techniques for Mortality modeling, claim modeling,

and fraud detection

Dihui – Applications in underwriting process, claim process and product

comparison

Time Series Prediction for Actuaries

What is time series prediction, why do actuaries need it?

What’s the current methodology for time series prediction?

What are the limitations/issues

What do we propose to do? (using AI for time series prediction)

In the following presentation: two Deep Learning examples(DNN and RNN)

DNN: Deep Neural Networks

What is DNN?

Why DNN is better?

How to use DNN?

Types of DNN: CNN (Convolutional Neural Networks)and MLP (Multi-layer

Perceptron)

DNN Example for Bitcoin Price

Data preprocessing(Bitcoin price from January 2012 – March 2019): 2,627 points

Create the model: CNN and MLP

Train the model

DNN Example for Bitcoin price - Result

Model CNN MLP

No. of Parameters ~9000 21,509

Mean Square Error 0.039 0.048

RNN: Recurrent Neural Networks

What is RNN? How is it different than DNN

How RNN is special? Why we consider RNN for time series prediction?

A type of RNN model: LSTM

RNN Example for Stock Market Data preprocessing

Create the model: LSTM

Train the model

Model result

RNN Example for Stock Market - Result

Summary and Future Work

Open sourced libraries. Many libraries are optimized with GPU, which has

very powerful computing power

Higher accuracy compare to classic statistic models

Emerging research in time series prediction

Marie-Claire Koissi, PhD, Professor, Actuarial Science Program, UWEC

Emerging Data Analytics Techniques with Actuarial Applications

Marie-Claire Koissi, PhD,Actuarial Science Program, [email protected]

October 29, 2020

Agenda

• Emerging techniques for mortality modeling

• Emerging techniques for claim modeling

• Emerging techniques to detect Insurance fraud

Part 1: Emerging techniques for mortality modeling

Emerging techniques for mortality modeling

• Trees models• Mortality regression with cause of mortality (Deprez, et al. 2017)• Mortality rates by cancer type (Shang, 2017)• Fit and predict maternity recovery rates and mortality rates (Kopinsky, 2017)

• Neural network• LC model with age specific cohort effects (Hainaut, 2018)• LC model with Multiple Populations (Richman and Wüthrich, 2018)• Mortality rates by cancer type (Shang, 2017)• Mortality Embedding- Entity-Embedding Neural Net (Vincelli, 2019)

• Predictive Modeling

8

Emerging techniques for mortality modeling and forecasting

9

Emerging techniques for mortality: Neural network on the Lee-Carter model for mortality

10

Emerging techniques for mortality: Neural network on the Lee-Carter model for mortality

Multi-population model 𝐥𝐨𝐠 𝒎𝒙,𝒕 = 𝒇 𝒙 + 𝒈 𝒙 𝒉(𝒕)

Deep Neural NetworkUsing back-propagation algorithm

NN learn directly from data

Age embedding with dimension reduction

MSE

LC(Standard) 5.50

LC-DNN 2.68

Question to audience:

In your work, what type of mortality model do you use?

A. Deterministic, with an improvement factor

B. Stochastic

C. Selected mortality table

D. Other

Part 2: Emerging techniques for claim modeling

• Standard method: GLM• Copula regression (idea is to use function that

link univariate marginals to their full multivariate distribution; Frees and Valdez, 1998)

• Popular in recent studies:Trees modelsNeural network

• Predictive Modeling

Emerging techniques:Modeling Claim in Motor Insurance using Regression Trees(Noll et al., 2018)

Variables of Interest:

Vehicle features:

Driver features:

Other variables: Area code (categorical)Number of claims on policy i: Ni

Vehicle power (categorical)Vehicle ageVehicle gas (categorical)Vehicle brand

Driver Age

Model:

𝑁𝑖 ~ Poisson (𝜆 𝑥𝑖 𝐸𝑖)

Where log(𝜆 𝑥𝑖 ) = 𝛽𝑜 + σ𝑖 𝛽𝑖𝑥𝑖

Part 3: Emerging techniques to detect Insurance fraud

• Data balancing method known as Adaptive Synthetic Sampling Approach for Imbalanced Learning.

• Clustering, K-mean• Tree models

Note: Circular symbol denotes a legitimate claim and a trianglea questionable claimR-function for Multi-Dimensional Scaling: cmdscale

Machine Learning is used to order claims along risk classes

Question to audience:

In your work, do you use this software?

A. R software, quite often

B. Python, quite often

C. R or Python, but rarely

D. Never use R or Python

Takeaways

• Machine learning aims at improving model efficiency and “easiness” to use.

• Machine learning help user in handling large data set and extracting relevant information (which will otherwise be disregarded).

• Lot of work still needs to be done, but possible applications in actuarial work are promising.

16

Thank you for your attention.

Extra

Mortality modelling packages in R• Lifemetrics (Cairns et al., 2006)

• The Lifecontingencies package (Spedicato, 2013)

• Demography (Hyndman 2014)

• ilc (iterative LC) (Butt, Haberman, and Shang 2014)

• StMoMo (Stochastic Mortality Modelling, by Villegas, Millossovich and Kaishev, 2018, most recent

19

Mortality modelling packages in Python

• Python has a full library of packages for actuarial science and survival analysis including: Lifelines

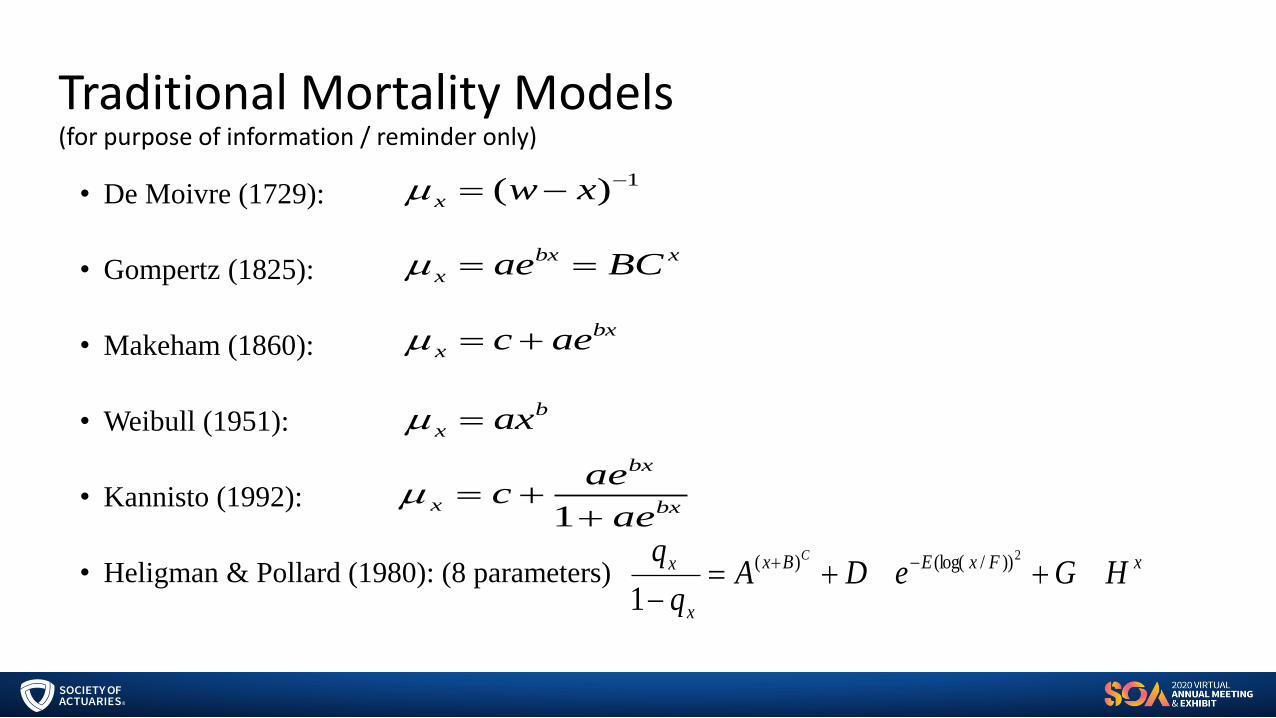

Traditional Mortality Models(for purpose of information / reminder only)

• De Moivre (1729):

• Gompertz (1825):

• Makeham (1860):

• Weibull (1951):

• Kannisto (1992):

• Heligman & Pollard (1980): (8 parameters)

1)( −−= xwx

xbx

x BCae ==

bx

x aec +=

b

x ax=

bx

bx

xae

aec

++=

1

xFxEBx

x

x HGeDAq

q C

++=−

−+ 2))/(log()(

1

Dihui Lai, PhD, ASALead Data Scientist, RGA

47

AIT Research on

Artificial Intelligence

Dihui Lai, PhD, ASA

Lead Data Scientist

Oct 2020

Contents

• Underwriting Process and AI

• Digital Health Data and NLP

• CI Coverage Comparison

• Claim Operations

AI Augmented Underwriting Process

Data Sources Stage 1 – Data Conversion,

Extraction, & Linkage

Quick

Decline

UW

decision

Stage 2 – Risk Assessment

Aggregate data from multiple

sources in multiple formats;

convert into structured,

linked, & interpretable data

Intelligent

Summary

Case triage

AI Function

• Intelligent Decision

• Recommendation

• Medical Interpret

• Warning/Red Flag

Additional requirement

STP/RuleETL

Fully UW

Feedback

NLP

Accelerated

UW

AI Function

• Info Extraction

• Data Linkage

• Unstructured → Structured

Underwriting Profile Summary

AI Augmented Underwriting Process: Summary

• Extract demographic information

from multiple sources (PDF, xml

etc.)

• Provide an overview of the

applicants’ underwriting profile

• Assess the risks for multiple

cohorts: lab, prescription drug, APS,

driving records etc.

• Provide severity score if possible

• Linkages to the source information

e.g. BMI

Digital Health Data (DHD) and NLP

Medical Entities

Unstructured DHD

Structured Process

51

DHD Description

rechk hasn’t passed kidney stone yet

• DHD contains both structured/unstructured data

• Unstructured data contains comprehensive information about individual health

• Read through all unstructured data is time consuming

• Unstructured data could contain information that is not covered in the structured data

• In one study, we use NLP and are able to identify ~15% of the cases that contain more severe

medical conditions from unstructured text.

Medical Severity

ICD Code [N20.0]

UW Impact

52

Product Definition Comparison

When it comes to CI product, companies share a lot of common features however, every company

could have varied definitions on detailed exclusions, time span, surgery procedures etc. The

review process of comparing CI definitions could be challenging and tedious. Could NLP offer

some help?

Surgery to Aorta - Definition 1

Surgery to Aorta - Definition 2 Similarity: 0.167

Claim Notes Classification

Sample Claim Notes: 2012.5.6投保822,2016.12.16投保1183、1185,本次于2017.10.27因脑白质病变申请理赔,本次疾病不符合条款约定的重疾,无对应重疾责任,已协谈,本次拒付处理。。脑白质病变 脑白质病变;。脑白质病变

Claim

Note

Benefit

Classifier

ESCI LSCI DEA

ESCI

Disease

identifier

LSCI

Disease

identifier

DEA

Disease

identifier

Use machine leaning based model to

categorize the claim notes into

appropriate type.

Questions

Question

• Where do you see the role of the Actuary fitting in with uses of AI?

Question

• Insurance and other traditional areas where Actuaries work are relatively data poor compared to new digital enterprises, such as Google, Tesla, Amazon. How will Actuaries need to evolve to work with (partner) or for these enterprises?

![10B-LR 10B-SUB - Bryston10B].pdf · The 10B crossover is available in three stock versions; 10B-SUB incorporating frequencies more ... MONO LOW PASS MODE (10B-SUB AND 10B-STD ONLY):](https://cdn.vdocument.in/doc/165x107/5afd7a367f8b9a434e8d9dda/10b-lr-10b-sub-10bpdfthe-10b-crossover-is-available-in-three-stock-versions.jpg)