Seven & i Holdings Co., Ltd.

Growth Strategy Presentation

March 9, 2016

Group Management

Strengthening Governance

Reform of Ito-Yokado

Reform of Sogo & Seibu

Content

Group Management

Copyright (C) Seven & i Holdings Co., Ltd. All Rights Reserved.

Holding companySeven & i Holdings

Operating CompaniesSeven-Eleven Japan (SEJ), Ito-Yokado (IY), and Sogo & Seibu (SS), etc.

Reflect shareholder concerns Reflect customer concerns

1) Control overall governance2) Maximize enterprise value as the

Group’s listed representative

1) Fulfill responsibilities in each operational domain

2) Realize autonomy, seek profit growth and enhance asset efficiency

The Goal is to maximize Group value

Basic policy “Shared strategies and independent brands”

Seven & i Group Management

1

Realizing Group synergies●

Copyright (C) Seven & i Holdings Co., Ltd. All Rights Reserved.

Pursuing Group Synergies

Drivers of Group synergy generation

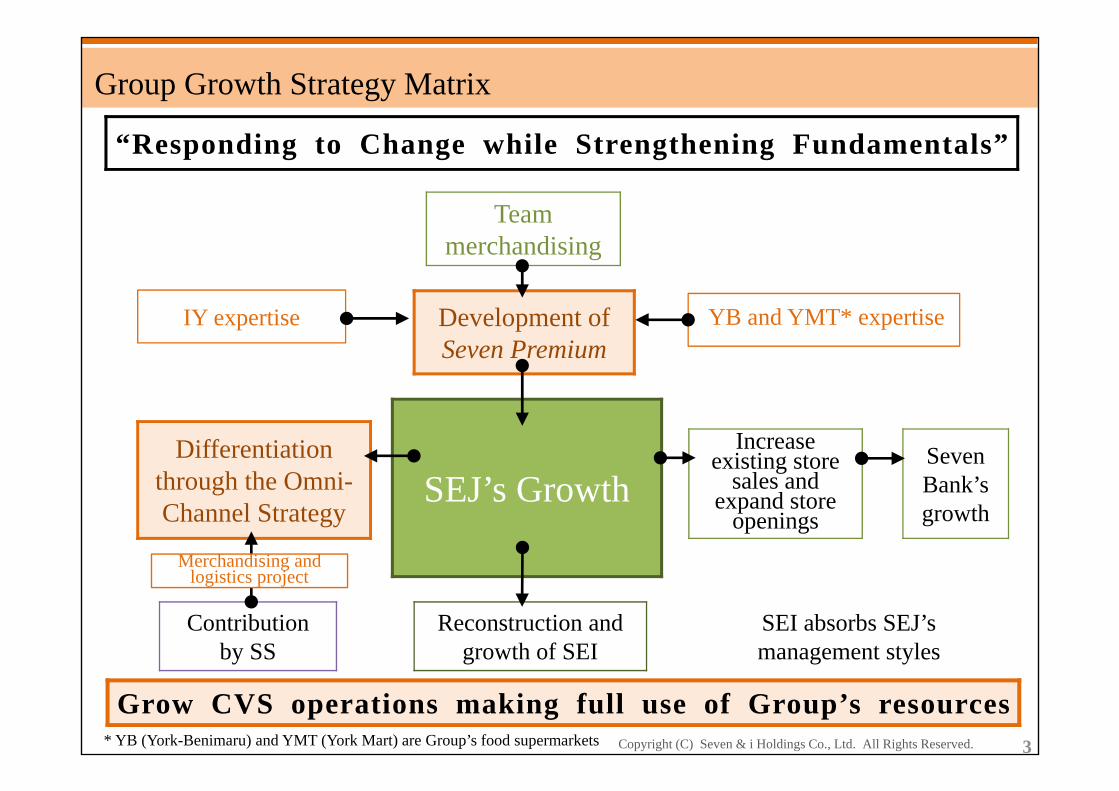

(1) Group principle : “Responding to Change while Strengthening Fundamentals”

(2) Marketing capabilities: Perceiving changes in consumer behavior through abundant customer-contacts

Group management is crucial to grasp broad trends in consumer behavior and raise gross profit through purchasing power

2

Foundation ofSeven-Eleven Japan

Modernization and revitalization of small and medium sized stores

Reconstruction of 7-Eleven, Inc.

Reconstruction through relisting and becoming a wholly owned subsidiary

Foundation of Seven Bank Pursuing further convenience of SEJ

Seven Premium Synergies focused on products through team merchandising

The Omni-ChannelStrategy

Synergies focused on customer behavior and Internet infrastructure

Copyright (C) Seven & i Holdings Co., Ltd. All Rights Reserved.

Team merchandising

Development of Seven Premium

SEJ’s GrowthDifferentiation

through the Omni-Channel Strategy

Increase existing store

sales and expand store

openings

SevenBank’sgrowth

Contributionby SS

Reconstruction and growth of SEI

SEI absorbs SEJ’s management styles

“Responding to Change while Strengthening Fundamentals”

IY expertise YB and YMT* expertise

Merchandising and logistics project

Group Growth Strategy Matrix

* YB (York-Benimaru) and YMT (York Mart) are Group’s food supermarkets 3

Grow CVS operations making full use of Group’s resources

Copyright (C) Seven & i Holdings Co., Ltd. All Rights Reserved.

120

140

160

180

200

220

240

1,500

2,000

2,500

3,000

3,500

4,000

4,500

01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

SevenPremiumlaunch

taspo effect

Lehman Brothers’ collapse

Special demand associated with earthquake

SEVEN CAFÉlaunch

■Total store sales (including Seven Premium sales) [left scale, bar graph] and operating income[right scale, line graph] by fiscal year

(Billions of yen)

SEJ Could Never Have Grown without Realization of Group Capabilities, Including from IY and YB

4

Total store sales (Left)

Operating income(Right )

Main growth drivers (as of January 2016)

Delicatessen foods

74 months

consecutive YOY increases

Daily products 69 months

consecutive YOY increases

Positive cycle: Social structure change⇒Product strategy change⇒Existing store sales increase⇒Increase store openings

Existing stores sales increase

▲0.2 ▲1.3 ▲0.2 ▲0.6 ▲0.7 ▲1.6 ▲1.9 ▲1.5 +5.2 ▲2.1 +2.2 +6.7 +1.3 +2.3 +2.4 +2.5

Net increase 449 458 630 613 523 484 425 299 264 455 479 773 1,067 1,247 1,142 1,100

Aging society and increase in dual-career couples, etc.

(Plan)(FY)

Seven Premium

Sales

Seven Premiumexpansion Realize synergies

(Billions of yen) Initiatives

for close-by, convenient

Copyright (C) Seven & i Holdings Co., Ltd. All Rights Reserved.

Since Seven Premium proposals (2009 onward)Previous lineupConvenience

stores

Supermarkets

Meal needsReady-

to-serve

Supermarkets

Ready-to-serve

Seven Premium Helps SEJ to be “Close-by, Convenient Stores” by Incorporating the Strengths of Supermarkets

Convenience stores product lineups meet meal needs through product development using supermarket knowledge and marketing capabilities

5

Convenience stores

Meal needs

Copyright (C) Seven & i Holdings Co., Ltd. All Rights Reserved.

229 192

380

564

637

150

250

350

450

550

650

750

5,000

7,000

9,000

11,000

13,000

15,000

17,000

FY00 FY01 FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15

Number of total stores 5,756 5,829 5,823 5,784 5,799 5,829 6,050 6,088 6,196 6,389 6,610 7,149 8,118 8,292 8,297 8,550

Number of franchisedstores

3,118 3,173 3,276 3,338 3,422 3,508 3,828 4,041 4,220 4,649 5,064 5,437 5,870 6,219 6,390 6,678

Franchise ratio (%) 54.2 54.4 56.3 57.7 59.0 60.2 63.3 66.4 68.1 72.8 76.6 76.1 72.3 75.0 77.0 78.1

SEI absorbs SEJ’s management styles

Development of merchandising Logistics strategy

6

(plan)

SEI Could Never Have Grown without Becoming a Wholly Owned Subsidiary■Trends of merchandising sales [left scale, bar graph] and operating income [right scale, line graph] on a dollar basis

Became a wholly owned subsidiary

Operating income [right scale]

AggressiveM&A

Merchandising sales [left scale]

(Millions of dollars)

(Millions of dollars)

(plan)

Strengthening Governance

Copyright (C) Seven & i Holdings Co., Ltd. All Rights Reserved.

Concept of Governance (1): Realize Sustainable Growth and Medium- to Long-Term Enterprise Value Increase

Goal Approach Key indicators

Medium- to long-term enterprise value increase

Realize synergiesIncrease capital efficiency

Operating income increaseROICROE (ROA)

Sustainable growth Maintain a sound financial structure

Credit ratingsOwners’ equity ratioInterest-bearing debt ratio

●Approaches and key indicators for achieving goals

R O E =Net income

×Net sales

×Total assets

Net sales Total assets Owners’ equity

= R O A × Financial leverage

Business management of operating companies based on ROA and consolidated financial leverage

7

Copyright (C) Seven & i Holdings Co., Ltd. All Rights Reserved.

Increase ROE

●Current ROE (FY2015) and target

8

Concept of Governance (2): Realize Sustainable Growth and Medium- to Long-Term Enterprise Value Increase

TargetROE

10%Current

ROE

7.9%

■Governance for operating companies

Set increasing operating income as the most important indicator, since this is the result of our core business

1. Operation Support each company’s sales strategies and create synergies across the organization

2. Investment decisions Make investment decisions based on a standard of ROIC 6%*

1. Strengthen operation 2. Streamline investmentIncrease operating

profit marginIncrease operating income

Increase capital efficiency

*(Operating income + interest income) × 0.6 + dividend income / (non-current assets + investment and financing)

Copyright (C) Seven & i Holdings Co., Ltd. All Rights Reserved.

Strengthening Governance

Matters currently under consideration

Setting of targets with set deadlines Specify when achieve the target of ROE 10%

PDCA cycle for achieving numerical targets

Deciding, executing, confirming on funds allocation and operating strategy

9

The holding company will strive to realize a structure capable of allocating the management resources (funds) of the entire GroupAs a result, we will create a framework that can generate cash flow that will enable continuous dividend increases

Plan

DoSee

PolicyInvolvement of

independent outside directors

Implementation process example

Copyright (C) Seven & i Holdings Co., Ltd. All Rights Reserved.

Capital policies

Credit ratings Maintain current rating

Owners’ equity ratio Manage the owners’ equity ratio of around 45%

Interest-bearing debt ratio Manage within 0.5 times

*Conduct fund procurement through large-scale investments, etc. using optimal methods considering management trends, financial status, market environment, etc.

Maintain a Sound Financial Structure (Sustainable Growth)

Reference: Trends on owners’ equity ratio

45.6 45.4 44.4 43.6 43.9

54.6 55.7 55.0 53.5 54.0

0.43 0.40

0.45 0.45 0.41

0.3

0.4

0.5

0.6

30

40

50

60

2011 2012 2013 2014 2015

Owners’ equity ratio (left scale)

Estimated owners' equity ratio excluding financialservices (left scale)Interest-bearing debt ratio (right scale)

(%) *Financial servicesATM, credit card, electronic money (pursue settlement functions)insurance, and lease services

With financial stability as the core focus, aim to also increase capital efficiency

10

(times)

(FY)

*Maintain around 55 % in retail business

Copyright (C) Seven & i Holdings Co., Ltd. All Rights Reserved.

●GoalEnsure objectivity and transparency for important matters relating to personnel and compensation

Committee chair

Kunio Ito, Director (Independent Outside Director): Nominated by the Board of Directors

Committee members

Chairman and Chief Executive Officer (CEO) , President and Chief Operating Officer (COO), Independent Outside Directors (Two members)

Establishment of a Voluntary Nomination and Compensation Committee Establish the Nomination and Compensation Committee as a voluntary advisory committee to the Company’s Board of Directors

●DeliberationsDeliberate on the following and report to the Board of Directors

NominationsFormulation of basic policy and standardClarify reason for nomination

7&i HD : Representative Directors, Directors, Executive Officers, Audit & Supervisory Board Members

Subsidiaries : Representative Directors*

Compensation Formulate basic policy and standards relating to executive compensation, discuss and confirm compensation proposals

*Integrated committee

*Observer: One Internal Audit & Supervisory Board Member and one Outside Audit& Supervisory Board Member, without voting rights

11*SEJ, IY, SS, YB, YMT, Seven & i Food Systems

Reform of Ito-Yokado

Copyright (C) Seven & i Holdings Co., Ltd. All Rights Reserved.

Earnings and Direction of Ito-Yokado (IY)

IY earnings

Apparel and household goods

Decrease in floor-space efficiency and gross profit margins resulted in a sharp increase in loss

Food Breadwinner, mainly in the Tokyo metropolitan area

TenantsProfit growth through increase in Ario stores and shift from corporate to emphasizing tenanting existing stores

Regional characteristics

Continuing to make profit in Tokyo, Chiba, Saitama, and Kanagawa prefectures, loss in regional areas

Environmental changes

Consumption environment・Further shortening of product life

cycles・Emergence of Internet drivesdemand for increased specialization

Internal issues

Break Away from Conventional Chain Store Concept・Uniform companywide

merchandizing・Reliance on wholesaler

merchandizing・Increase in disposal loss and sales

promotion expenses12

Base on individual store management, move away from mainly corporate general merchandise stores and change the earnings structure

Thoroughly reinforce food

Downsize apparel and household goods in line with individual store characteristics

Strengthen Ario(shopping center) format

Leverage potential in the Tokyo metropolitan area

Utilize the Omni-Chanel Strategy

Copyright (C) Seven & i Holdings Co., Ltd. All Rights Reserved.

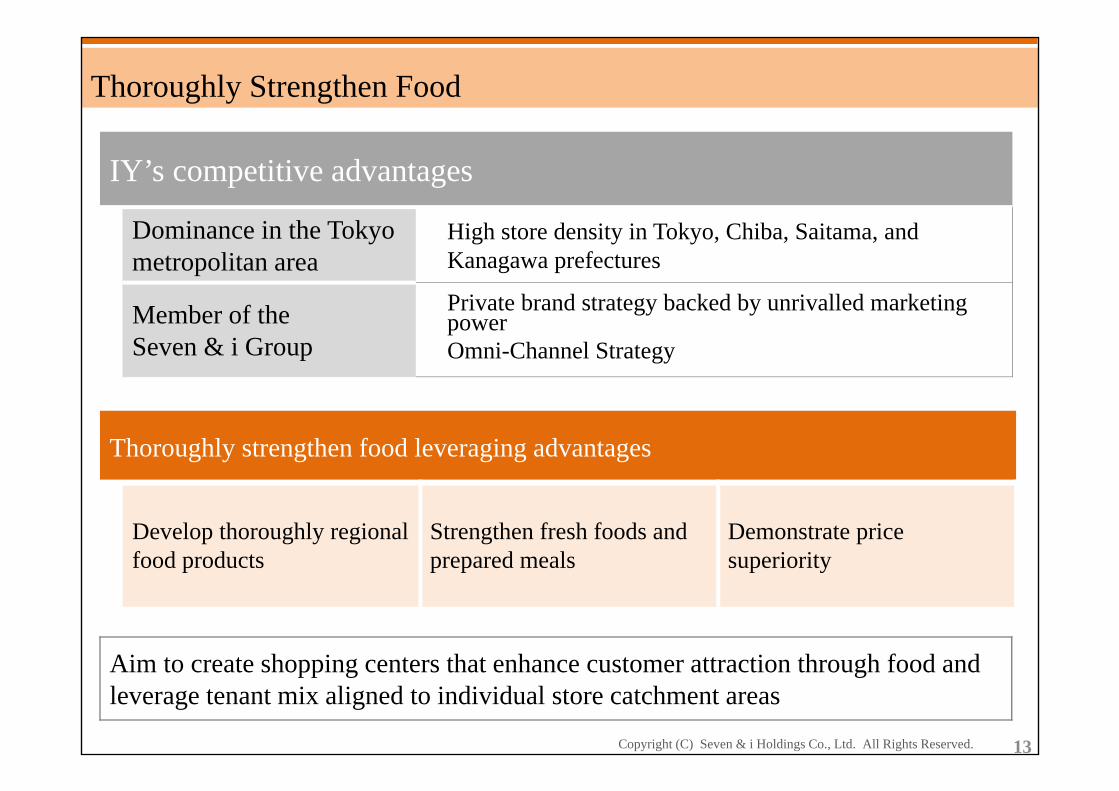

Thoroughly Strengthen Food

IY’s competitive advantages

Dominance in the Tokyo metropolitan area

High store density in Tokyo, Chiba, Saitama, and Kanagawa prefectures

Member of theSeven & i Group

Private brand strategy backed by unrivalled marketing powerOmni-Channel Strategy

Thoroughly strengthen food leveraging advantages

Develop thoroughly regional food products

Strengthen fresh foods and prepared meals

Demonstrate price superiority

Aim to create shopping centers that enhance customer attraction through food and leverage tenant mix aligned to individual store catchment areas

13

Copyright (C) Seven & i Holdings Co., Ltd. All Rights Reserved.

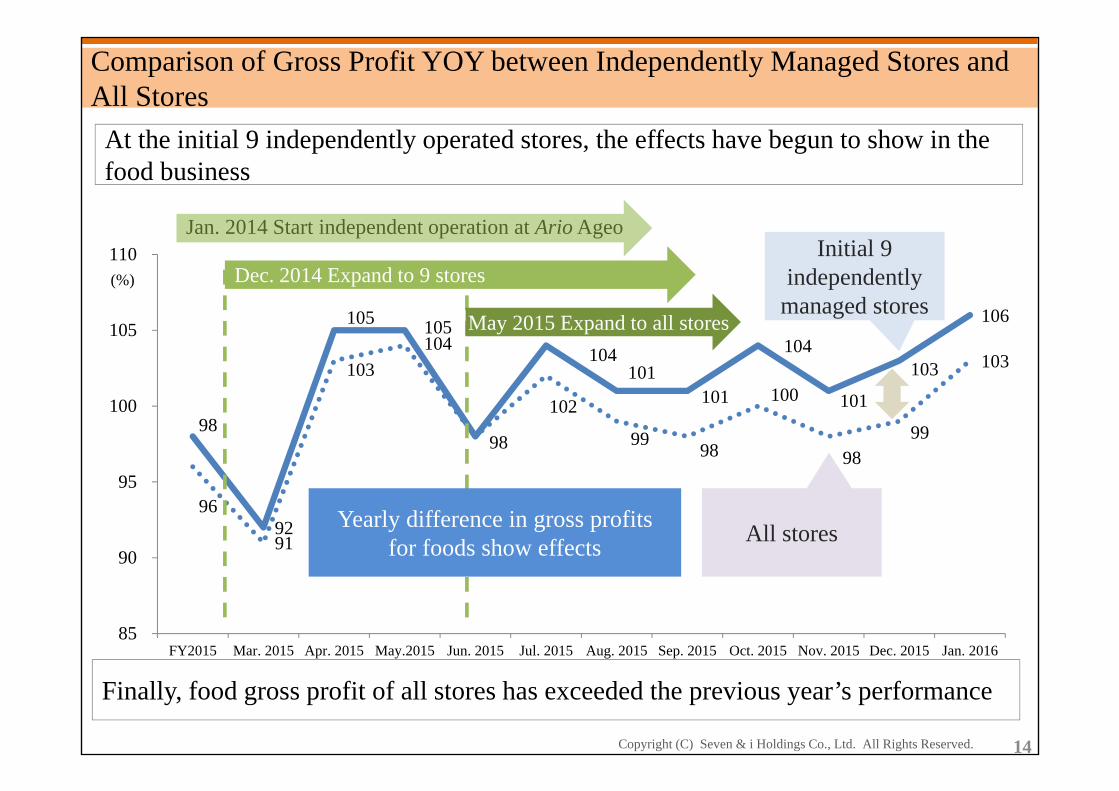

At the initial 9 independently operated stores, the effects have begun to show in the food business

Comparison of Gross Profit YOY between Independently Managed Stores and All Stores

98

92

105 105

98

104 101

101

104

101

103

106

96

91

103 104

102

99 98

100

98 99

103

85

90

95

100

105

110

FY2015 Mar. 2015 Apr. 2015 May.2015 Jun. 2015 Jul. 2015 Aug. 2015 Sep. 2015 Oct. 2015 Nov. 2015 Dec. 2015 Jan. 2016

Initial 9 independently

managed stores

All stores

Dec. 2014 Expand to 9 stores

May 2015 Expand to all stores

Jan. 2014 Start independent operation at Ario Ageo

Yearly difference in gross profitsfor foods show effects

(%)

14

Finally, food gross profit of all stores has exceeded the previous year’s performance

Copyright (C) Seven & i Holdings Co., Ltd. All Rights Reserved.

●Steadily close stores that are unable to earn profit through foodClose 20 stores for FY2017

FY February 2016 FY2017 – FY2021

No. of stores

182stores 20 store closures

40 cumulative store closures142 stores

IY’s Target Status

Start by conducting steady restructuring aimed at business structural reforms●

15

Impact on profit / loss after20 store closures for FY2017

Impact on profit / loss after 40 store closures

Special lossApprox. 11.0 billion yenWill record approx. 4.0 billion yen for FY2016

Special loss Approx. 20.0 billion yen

Revenue from operations

Approx. (77.0) billion yen

Revenue from operations

Approx. (160.0) billion yen

Operating income Approx. 1.9 billion yen

Operating income Approx. 4.0 billion yen

Copyright (C) Seven & i Holdings Co., Ltd. All Rights Reserved.

Status of 142 stores in 2020

1 Structural reform to Arioshopping center format

Approx. 45stores

Over 16,500 ㎡ , including existing17 stores

2 General merchandise stores + introduction of tenant mix

Approx. 60stores

Under 16,500 ㎡, attract tenants to suit catchment area

3 Food + tenants Approx. 15stores Food specialty store format

4 Shokuhinkan and THE PRICE 18stores

18 existing storesBusiness alliance with Group supermarkets

Of which, 15 stores Hokkaido, Tohoku

IY’s Target Status

Status after Business Structural Reforms●

Create profitable formats while carrying out new store openings

16

Reform of Sogo & Seibu

Copyright (C) Seven & i Holdings Co., Ltd. All Rights Reserved.

SS Reforms Pillar: Business Reform

Thorough business reform

Close unprofitable stores

September 30, 2016 (Plan)Sogo Kashiwa , SEIBU Asahikawa

*Will record a special loss of approx. 1.5 billion yen for FY2016

Promote reorganization

Reduce Head Office personnel (100 employees)Introduce merchandiser system to Merchandising Dept.Reduce the layers of management at Sales Dept. (from 3 layers to 2 layers)

Invigorate regional stores

・Promote reform toward shopping centers utilizing tenants・Strengthen regionally-retailer-managed merchandising:

Limited Edition areamode・Utilize Omni-Channel:

Establish centers where customers can “view, touch, and try” products not available in stores

Use the reform as an opportunity to promote awareness reforms among employees and change the approach to work

17

Copyright (C) Seven & i Holdings Co., Ltd. All Rights Reserved.

Promoting new growth strategies = Expanding market share

Initiatives to cultivate areas using the Omni-Channel and utilize SS’s location advantages

⇒Form a strategic area for nationwide deployment

SS Reforms Pillar: Growth Strategy

The meaning for Seven & i Holdings of positioning SS as the entire department store business ・Holds the highest location as a vital element in the market concentration strategy for the Tokyo metropolitan area

・Complements the holding company’s branding capabilities

・Utilizes customer management systems

Draw out the SS’s competitive advantage and latent capabilities through the Omni-Channel Strategy

18

Copyright (C) Seven & i Holdings Co., Ltd. All Rights Reserved.

Choice of Format by Customer Objective ●Customers choose formats within their area depending on distance and frequency of use

7&i HD Customer needs(Way of use/characteristics)

Catchment areaaverage distance

Average frequency of use

SSSpecial (fancy) shopping Relaxed and refined(Customer service, consultation shopping)

30 km radius 0.6 times / month

IYHigh quality daily shopping Daily needs and extras (Semi-self-service)

5 km radius 3.0 times / month

SEJClose-by, convenient/daily shopping Immediate needs (Quick self-service)

0.5 km radius 18.6 times / month[4.2 times / week]

Strengthen the Omni-Channel Strategy to nurture the entire Group’s market concentration strategy

19

*Profit for the Company ultimately derives from keeping individual customers for longer

Uniform management of customer information⇒Implement meticulous personalized sales

promotions

⇒Point promotion utilizing lifetime value*

Utilize SS expertise of customer management

Copyright (C) Seven & i Holdings Co., Ltd. All Rights Reserved.

Semi-self service – IY

Bi no Garden

Self-service – SEJ

Seven Premium

Seven Lifestyle

Close-by, convenient (quick-self-service)

High quality day-to-day (semi-self-service)

Consultant – SS

Kirei Station

Special needs(consultant sales)

20

Seven & i Group meets all manner of customers living needs other than beauty

Capture high-quality customersDatabasing customer information Customer data linkage

●Capture high-quality customers at SS. Use customer data to encourage them to use IY and SEJ

Collecting customer needs as a group – an example of Beauty

Copyright (C) Seven & i Holdings Co., Ltd. All Rights Reserved.

Trends on Operating Income and Dividend per Share Since the Foundation of 7&i HD

21

25 26 27 28 28 29 31 33 36.5 38.5

27 28 29 28 29 33 33 3536.5

38.5

150

200

250

300

350

400

0

20

40

60

80

100

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Operating income(right scale)

Net Income(billion yen) 133.4 130.6 92.3 44.8 111.9 129.8 138.0 175.6 172.9 183.0

Dividendper share 52 54 56 56 57 62 64 68 73 85

Payout Ratio(%) 36.4 39.4 55.7 112.7 45.2 42.2 41.0 34.2 37.3 41.1

Aim to the continuous increase of dividend and free cash flow

■ Interim ■ Year-End ■ Commemorative

8.0

(yen) (Billions of yen)

(forecast)

38.5

(FY)

This document contains certain statements based on the Company’s current plans, estimates,strategies, and beliefs; all statements that are not historical fact are forward-lookingstatements. These statements represent the judgments and hypotheses of the Company’smanagement based on currently available information. It is possible that the Company’sfuture performance will differ from the contents of these forward-looking statements.Accordingly, there is no assurance that the forward-looking statements in this document willprove to be accurate.